shariah guidelines for sukuk - assaif shariah guidelines for sukuk mufti ismail ebrahim shariah...

TRANSCRIPT

0

Shariah Guidelines for Sukuk

Mufti Ismail Ebrahim

Shariah AdvisorMalta,

October 2014

1

Outline of Presentation

Page

■ Credentials – Mufti Ismail Ebrahim [2]

■ Islamic Financial Services Products – Mufti Ismail Ebrahim [3]

■ Shari’ah Advisory Services – Mufti Ismail Ebrahim [5]

Introduction to Sukuk

■ Introduction to Sukuk [7]

■ General and Specific Shariah Guidelines [8]

■ Sukuk Vs. Conventional Bond Instruments (10)

Sukuk Structures and Examples

■ Musharakah [13]

■ Ijarah [16]

Wakalah [20]

Shariah Compliance: Contemporary Issues (23)

2

Credentials – Mufti Ismail Ebrahim

• Shariah Advisor:

• Ethica Institute of Islamic Finance, Dubai (Shariah Education and Advisory)

• Infinity Consultants, India (Shariah Consultancy Pr actice)

• Al-Mabroor Investments, RSA (Shariah Compliant Inve stment Vehicle)

• Jenuard AG, Austria (Shariah Investment Vehicle)

• IFSCAR, Trinidad and Tobago (Shariah Advisory)

• PSG Investment Bank, RSA (Shariah Wealth Management )

• Centre for Advanced Islamic Economics, Pakistan (Sh ariah Education and Advisory)

• Shariah Review Bureaux, Bahrain (Shariah Advisory)

• Lishui Prefecture Municipality, Peoples Republic of China (Shariah Advisory)

• Advisor to Governments and Central Banks on Islamic Finance

• Executive Director and Shariah Advisor, Russian Isl amic Finance Council (Shariah Advisory and Fatawa)

3

Islamic Financial Services Products – Mufti Ismail E brahim

1.Advised and developed several Shariah Compliant R eal Estate and Asset Management Funds Worldwide

2.Developed first Domestic Shariah Compliant Sukuk for South African Market

3.Issued hundreds of Fatawa (Islamic Legal Edicts) on Islamic Finance and Economics

4.Developed Shariah Wealth Management Products for leading investment bank in South Africa

5.Conducted Shariah training for hundreds of banker s and financial professionals in the GCC and beyond

6.Advising the Chinese Government on Shariah Compli ant Energy Project worth $150 Million

7.Advising South American Government on Sukuk

8.Conducted annual Shariah Compliance review and au dit for leading Shariah Compliant Investment Firm i n South Africa

4

Islamic Financial Services Products – Mufti Ismail E brahim

9.Advised Government and central Banks on Shariah R egulations and Guidelines for Islamic Finance

10.Advised and executed Shariah Compliant Trade Fin ance transactions worth more than $300 Million

11.Advising leading Turkish Bank on setting up Shar iah Compliant Window

12.Developed first ever Shariah Compliant asset man agement company in Austria

13.Advising major European religious agency on Isla mic Finance

5

Shari’ah Auditing and Advisory Services – Mufti Isma il Ebrahim

● Shariah Product Development

● Fatāwā and Certification.

● Shar īàh Review

● Shar īàh Audit and Assurance

● Shariah Mediation and Arbitration

● Islamic Private Wealth Management

● Shariah Board Development

● Islamic Finance Training and Human Capital Development

● Central Bank Regulatory Assistance

● Sukuk and Islamic Fund Structuring

● Islamic Finance Knowledge and Research

6

“ Embracing Islamic Finance through Shariah Compliance,

achieving new heights in expansion and growth”

7

Introduction to Sukuk

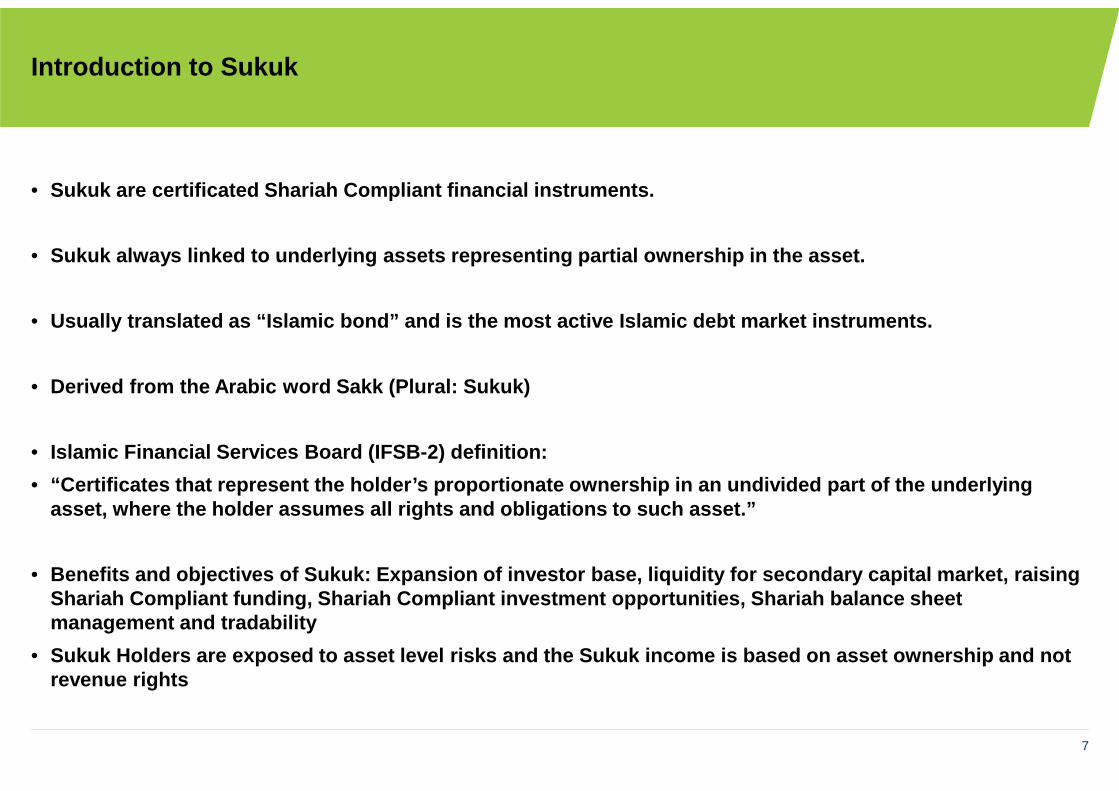

• Sukuk are certificated Shariah Compliant financial instruments.

• Sukuk always linked to underlying assets representi ng partial ownership in the asset.

• Usually translated as “Islamic bond” and is the most active Islamic debt market instruments.

• Derived from the Arabic word Sakk (Plural: Sukuk)

• Islamic Financial Services Board (IFSB-2) definitio n:

• “Certificates that represent the holder’s proportion ate ownership in an undivided part of the underlyin g asset, where the holder assumes all rights and obli gations to such asset.”

• Benefits and objectives of Sukuk: Expansion of inve stor base, liquidity for secondary capital market, raising Shariah Compliant funding, Shariah Compliant invest ment opportunities, Shariah balance sheet management and tradability

• Sukuk Holders are exposed to asset level risks and the Sukuk income is based on asset ownership and no t revenue rights

8

General Shariah Guidelines

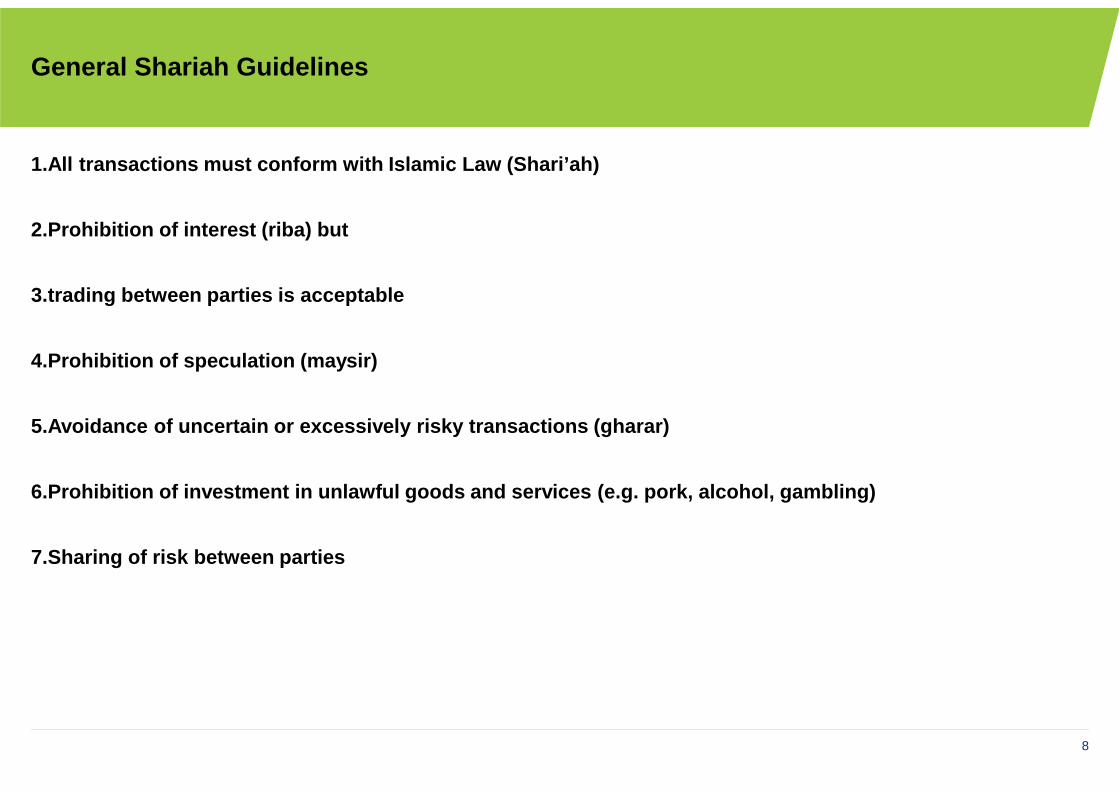

1.All transactions must conform with Islamic Law (S hari’ah)

2.Prohibition of interest (riba) but

3.trading between parties is acceptable

4.Prohibition of speculation (maysir)

5.Avoidance of uncertain or excessively risky trans actions (gharar)

6.Prohibition of investment in unlawful goods and s ervices (e.g. pork, alcohol, gambling)

7.Sharing of risk between parties

9

Specific Sukuk Shariah Guidelines

1. Funds raised must be used for Shariah compliant a ctivities.

2. All funds raised may be used to finance tangible assets. Specificity of assets is important, since Sukukunlike conventional bonds cannot be used for genera l financial needs of the issuer. Non-tangible asset s may be used based on Urf and Aaadah subject to Shariah Boa rd approval.

3. Income received by sukuk holders (investors) must be derived from the direct cash flows generated by the underlying assets.

4. Sukuk holders have a right to the ownership of th e underlying asset and its cash-flows.

5. Clear and transparent specification of rights an d obligations of all parties to the transaction, in particular

the originator (customer) and sukuk holders.

6. No fixity in returns and no financial guarantees .

7. Generic Shariah Compliant screening.

10

Specific Sukuk Shariah Guidelines

8. All the rules of original contract on the basis of which Sukuk are created should be applied.

9. The issuer cannot guarantee the face value of th e certificate for the holder except in case of negligence/misconduct.

10. In Sukuk based on sale and lease back, the issu er can unilaterally undertake that he will purchase the asset after one year for a pre-agreed price.

11. Different types of reserves (e.g. profit equali zation reserve) or takaful pool can be created.

12. Only those Sukuk can be traded that represent p roportionate ownership of tangible assets, usufruct s or services.

13. In Sukuk of Musharakah/Mudarabah, the issuer ca n redeem the certificates on the market price. Purc hase undertaking is allowed however the purchase price s hould be market value of the underlying assets.

11

Sukuk Vs. Conventional Bond Instruments

Sukuk:

• Each Sukuk unit represents an ownership of the underlying asset;

• Maturity of the Sukuk corresponds to the term of the underlying project or activity;

• The Sukuk prospectus contains all the Shariahrules related to the issue;

• The underlying asset / project / business has to be Shariah complaint (i.e. not dealing with pork related items, gambling, tobacco, institutions that deal with Riba (interest) etc.); and

• The Sukuk manager is required to abide by Shariahrules

• The Sukuk holders have the rights to profits but also bear losses

Conventional Debt Instruments:

• Bonds represent pure debt obligations due from the issuer;

• The core relationship is a loan of money, which implies a contract whose subject is purely earning money on money;

• The issue prospectus does not include Shariahconstraints; and

• The underlying asset / project / business can belong to any sector / industry

• Can be issued to finance almost any purpose which is legal in its jurisdiction.

• Bond holders are not exposed to losses on the asset although they might bear losses in the event of insolvency by the issuer.

12

Sukuk Structures

• Musharakah Sukuk:

− Issued with the aim of using the mobilized funds for establishing a new project, developing an existing project or financing a business activity on the basis of any of partnership contracts.

• Participation Certificates – represent projects or a ctivities managed on the basis of Musharaka.

• Mudaraba Sukuk – represent projects or activities ma naged on the basis of Mudaraba.

• Investment Agency Sukuk – represent projects or acti vities managed on the basis of an investment agency by appointing an agent to manage the operation.

• Murabaha Sukuk:

− Issued for the purpose of financing the purchase of goods through Murabaha so that Sukuk holders become the owners of Murabaha Commodity

13

Sukuk Structures

• Salam Sukuk

− Issued for the purpose of mobilizing funds so that the goods to be delivered on the basis of salam come to be owned by the Sukuk holders

• Istisna’ Sukuk

− Issued for the purpose of mobilizing funds to be employed for the production of goods so that the goods produced come to be owned by the Sukuk holders

• Muzara’ah (sharecropping) / Musaqa (irrigation) Suku k

− Issued for the purpose of using the mobilized funds for financing a project so that Sukuk holders become entitled to a share in the crop as per the agreement.

• Mugharasa (agricultural) Sukuk

− Issued for the purpose of mobilizing funds so that Sukuk holders become entitled to a share in the land and plantation.

14

Sukuk Examples and Shariah Guidelines: Musharakah

Musharakah is a mode of financing which can be secu ritized easily especially in the case of large proje cts where huge amounts are required.

An SPV is formed to collect funds from the Islamic investors, acquire assets and serve as partner in t he Musharakah agreement on behalf of the Islamic inves tors.

The obligor serves as Musharik and is typically app ointed the management agent of the Musharakah proje ct.

Every subscriber is given a Musharakah certificate, which represents his proportionate ownership in th e assets of the Musharakah.

After the project is started, these Musharakah cert ificates can be treated as negotiable instruments. Certificates can be bought and sold in the secondar y capital market.

Securitization of Musharakah can be used for: Constr uction of projects and factories, expansion Project s, working capital finance

15

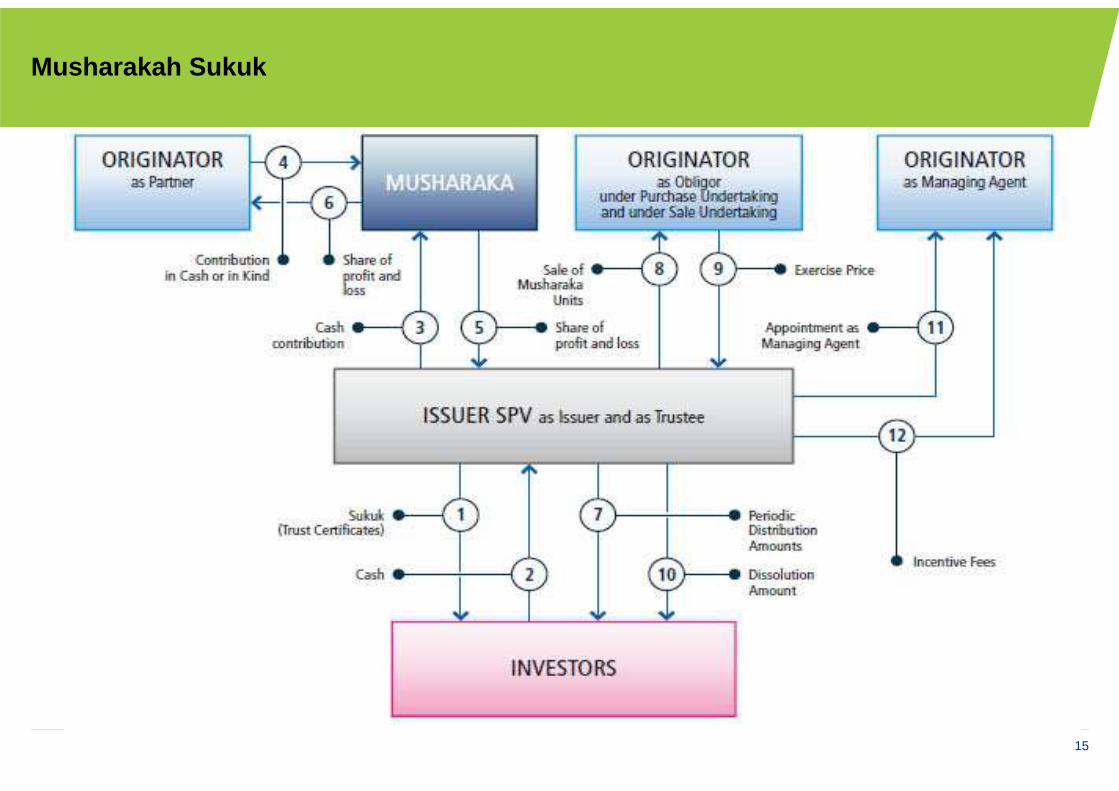

Musharakah Sukuk

16

Musharakah Sukuk – Shariah Guidelines

• Profit earned by the Musharakah is shared according to an agreed ratio.

• Loss is shared on pro rata basis.

• All the assets of the Musharakah should not be in li quid form. Portfolio of Musharakah should consist of non-liquid assets valuing more than 33% of its tota l worth.

• However, if the Hanafi view is adopted, trading wil l be allowed even if the non-liquid assets are less than 33% but the size of the non-liquid assets should not be negligible.

• Whenever there is a combination of liquid and non-l iquid assets, it can be sold and purchased for an a mount greater than the amount of liquid assets in combina tion.

• Bilateral undertaking (Wa’d Mulzim) is not permissibl e in Shariah. However unilateral undertaking (Wa’dGhair Mulzim) is permitted.

• Guaranteed fixed returns are not permitted as this constitutes Riba (interest).

17

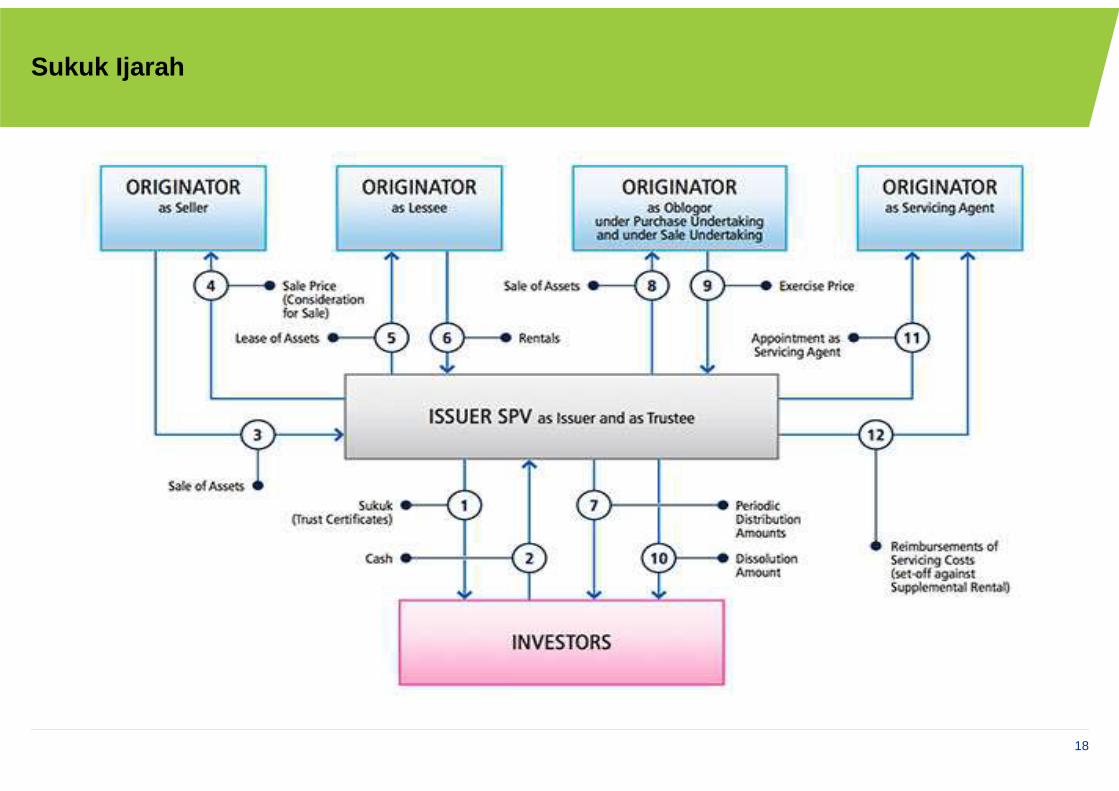

Sukuk Ijarah

• Sukuk Ijarah are title deeds of equal shares in a lea sing project giving their holders the right to hold shares, receive rental payments and dispose of their assets /properties. Ijarah certificates are tradable on the secondary markets.

• The lessor (owner) can sell the leased asset wholly or partly either to one party or to a number of individuals to recover his cost of purchase of the asset with a profit thereon.

• This purchase of a proportion of the asset by each individual may be evidenced by a certificate, which may be called 'Ijarah certificate’.

• The Ijarah certificate represents the holder's propo rtionate ownership in the leased asset.

• The holder will assume the rights and obligations o f the owner/lessor to the extent of his ownership.

• The holder will have the right to enjoy a part of t he rent according to his proportion of ownership in the asset.

• In the case of total destruction of the asset, he w ill suffer the loss to the extent of his ownership.

• These certificates can be negotiated and traded fre ely in the market and can serve as an instrument ea sily convertible into cash.

18

Sukuk Ijarah

19

Shariah Guidelines: Sukuk Ijarah

• The rental payments maybe structured such that it c omprises of (i) profits on the rental and (ii) rede mption amount on the principal. Rental payments cannot be guaranteed.

• Sukuk Ijarah does not represent debts; but undivide d proportionate ownership of the leased asset (participatory certificates).

• Because the Sukuk Ijarah are not debts nor monetary , the issue of sale of monetary-debts with a discou nt do not arise. Hence Sukuk Ijarah may be traded in the secondary market freely.

• It is essential that the Ijarah certificates are de signed to represent real ownership of the leased as sets, and not only a right to receive rental payments.

• The Sukuk holders are responsible for major asset m aintenance whereas the obligor (lessee) is respons ible for ordinary maintenance.

• All contractual agreements should be separated and individualized. For example, sale and lease agreemen ts should be separated. Conversion should be well defi ned.

20

Sukuk Wakalah

• Wakalah is an agreement whereby one party entrusts another to act on its behalf. Wakalah is akin to an agency agreement.

• A principal (the investor) appoints an agent (wakee l) to invest funds provided by the principal into a pool of investments or assets and the wakeel lends it exper tise and manages those investments on behalf of the principal for a particular duration, in order to ge nerate an agreed upon profit return.

• The Wakalah agreement will govern the scope of the services provided, remuneration and appointment term. There should be no ambiguity.

• The Wakalah portfolio assets should be Shariah Comp liant and approved by the Shariah Supervisory Board.

21

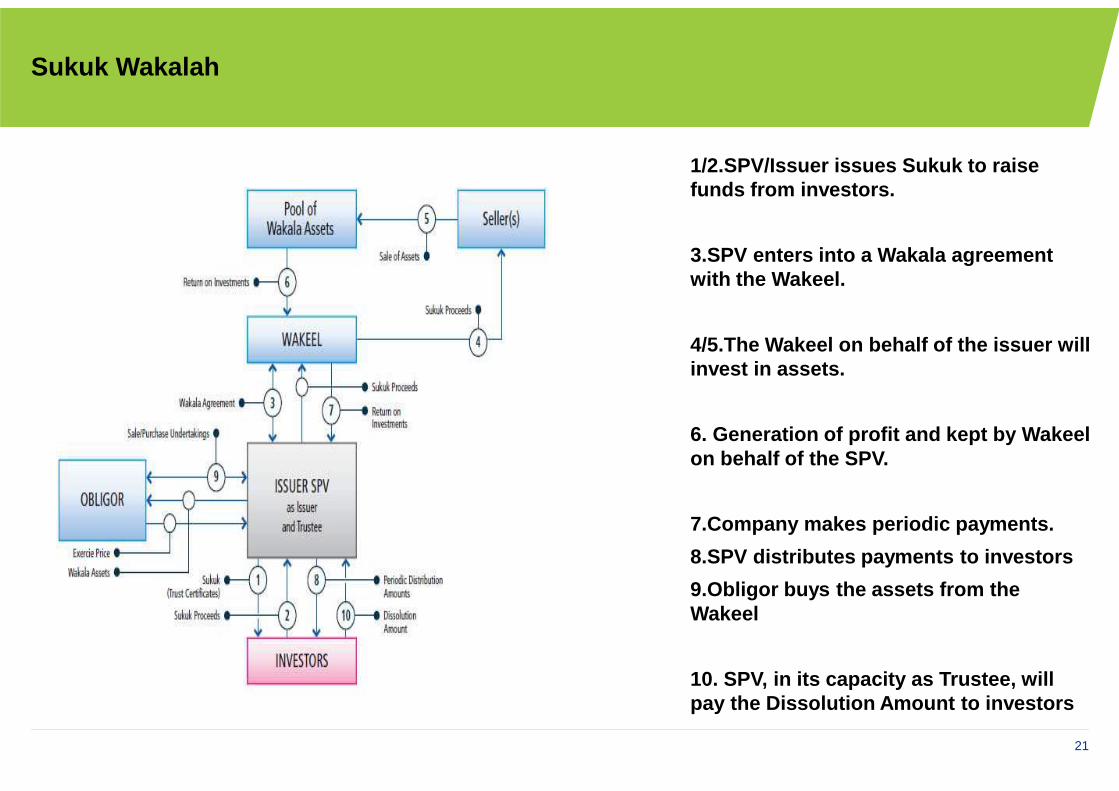

Sukuk Wakalah

1/2.SPV/Issuer issues Sukuk to raise funds from investors.

3.SPV enters into a Wakala agreement with the Wakeel.

4/5.The Wakeel on behalf of the issuer will invest in assets.

6. Generation of profit and kept by Wakeel on behalf of the SPV.

7.Company makes periodic payments.

8.SPV distributes payments to investors

9.Obligor buys the assets from the Wakeel

10. SPV, in its capacity as Trustee, will pay the Dissolution Amount to investors

22

Sukuk Wakalah: Shariah Guidelines

• The scope of the wakala arrangement must be within t he boundaries of Shari’a i.e. the principal cannot require the wakeel to perform tasks that would not o therwise be Shari’a compliant.

• The Wakalah Agreement must be clear and well defined . The scope of services provided, appointment term, duties, terms and conditions and fees payable shoul d be well defined. Any ambiguity will render the agreement voidable.

• All portfolio assets should be screened and endorse d by the Shariah Supervisory Board.

23

Shariah Compliance: Contemporary Issues

1. Shariah Supervisory Boards should ensure the unde rlying structure, all financial documentation including prospectus and implementati on of the transaction is Shariah Compliant.

2. The prospectus must mention the obligation to com ply with all the guidelines and principles of Shariah as advised by the Shariah Supervisory Bo ard.

3. All transactions should be separated and individu alized. No bilateral agreements permitted in Shariah.

4. External Shariah Oversight Committee should be es tablished to ensure optimal Shariah Governance.

5. Regular Shariah Audits should be conducted by ext ernal oversight committee.

24

Shariah Non- Compliance

Shariah non-compliance risk very high due to severa l reasons including:

• Ambiguity in conversion process

• Conventional options

• Organized Tawarruq structures

• Commercial guarantees of cash flows and capital fun ds

• Conventional insurance

• Bilateral sale-lease back agreements

• Tradability of debt-receivable instruments

• Improper Shariah oversight and implementation

• Conventional funding placement

• No genuine risk sharing

25

What we do today will determine the success of the Islamic Finance Industry in

the future. The sustainability of this industry is our

responsibility.

26

Shukran And May God Bless!

27

Contact Details: Mufti Ismail Ebrahim

Presenter’s contact details:

Mufti Ismail Ebahim Desai

Executive Director : Russian Islamic Finance Counci l and Global Islamic Financial Services Firm

+27 (31) 207 5772

+27 (72) 282 6012

[email protected]/[email protected]/CEO@rif c.su

www.rifc.su

The information contained herein is of a general na ture and is not intended to address the circumstanc es of any particular individual or entity. Although we endeavour to provide accurate and timely informatio n, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one shoul d act on such information without appropriate profe ssional advice after a thorough examination of the particular situation. We will be pleased to provide definitive advice on request and following written acceptance of our standard terms and conditions.