retail research diysip picks 05 july 2017 picks...source: capitaline database, *= standalone number...

TRANSCRIPT

RETAIL RESEARCH DIYSIP Picks 05 July 2017

RETAIL RESEARCH P a g e | 1

We present herewith two set of stocks (Better known – Medium risk and Lesser known stocks – High Risk), which investors, based on their risk profile, can look at for investing from a medium term perspective in a systematic investment way (SIP). While the frontline indices are near their all time highs, mid and small caps havealso done well (though they have come under pressure lately). While a further rise is possible, there are higher chances of markets correcting later in terms of values and time. In such a circumstance, using a SIP or averaging policy may be advisable (for aggressive investors, this may be in addition to an initial lumpsum investment, if they so choose). This will enable lowering the average entry level due to expected fall in prices (in line with the expected fall in these stocks). SIP investments will give good returns only if the average entry price is lower (due to the initial fall expected). In case the stock price first rises and then falls, SIP investment may not generate attractive returns. One of the criteria for choosing these stocks is that there is a good chance that they could first fall for some weeks/months and then rise so that the full benefit of averaging is available.

Systematic Investment Plans, or SIPs, are expected to curb volatility, both on the upside as well as downside. This is done by cost averaging since the investments are made on a periodic basis, and not in a lump sum. Though the investment amount is fixed, more units are purchased when the market/stock trends down, and fewer units are purchased when the market/stock moves up. If compared with lump-sum investing, cost averaging does not work to the investor’s benefit in a rising market. While cost averaging cushions your investment during a downside, it also irons out gains made in a bull run to some extent. But to be effective, it needs to be sustained over a long time frame or at least an entire market cycle. In case, at any time during the period of SIP, the stock price moves up sharply (compared to the average entry price) – to attain the probable upside level or a good return above the average entry price – depending on the period of investment, capitalization and volatility of the individual stocks, then it would be a good idea to stop the SIP and sell the stocks booking the profits accrued.

Better Known Stocks

Sr No Company Industry Equity Latest FV CMP

Book Value latest

Net Sales FY17

Change in sales

y-o-y PAT FY17

Change in PAT y-o-y

EPS TTM

P/E TTM P/BV

Last Div %.

Dividend Yield

1 Chambal Fert. Fertilizers 416.2 10 128.2 51.0 7553.5 -16.1% 361.7 90.1% 10.2 12.5 2.5 19 1.5%

2 Dr Reddy's Labs Pharmaceuticals 82.9 5 2623.7 739.6 14080.9 -9.0% 1292.1 -39.4% 77.9 33.7 3.5 400 0.8%

3 JK Tyre &Indust Tyres - Large 45.4 2 166.9 86.6 7689.4 11.5% 326.4 -31.5% 16.4 10.2 1.9 125 1.5%

4 JSW Steel Steel - Large 241.7 1 208.4 93.5 54628.2 33.7% 3467.2 110.8% 14.7 14.1 2.2 225 1.1%

5 KotakMah. Bank Banks - Private Sector 951.8 5 958.8 232.7 22324.2 9.4% 4315.4 40.7% 19.8 48.4 4.1 12 0.1%

6 Larsen & Toubro Engineering - Turnkey Services 186.7 2 1683.4 537.8 110011.0 7.9% 6402.8 42.8% 66.8 25.2 3.1 1050 1.2%

7 PidiliteInds. Chemicals - Organic - Large 51.3 1 820.3 67.7 5616.8 4.8% 863.2 6.9% 16.8 48.7 12.1 475 0.6%

8 Titan Company Diamond Cutting / Jewellery 88.8 1 535.6 39.5 12978.9 15.1% 768.2 13.9% 9.4 57.0 13.6 260 0.5% Source: Capitaline Database, *= Standalone Number All figures are Consolidated and in Rs. except for Equity, Sales FY17 and PAT FY17 which are in Rs.Cr., CMP is as of July 04, 2017, EPS is adjusted for extraordinary items.Past dividend yield may not necessarily sustain in future

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 2

A brief write up on the eight stocks is as under: Chambal Fertilizers and Chemicals Ltd. (Mcap Rs 5333.70 cr)

Chambal, incorporated in 1985, in Kota (Rajasthan), has the largest installed urea capacity in the private sector in India. The company also has significant investments in the shipping, and software businesses.

Chambal enjoys has largest market position in urea and DAP with 8% of total domestic production share of urea and 11% of total domestic DAP sold. It has a strong hold in the North Indian market with a strong recall for the brand Uttam Veer and a robust distribution channel. The favourable location of its plants near its end users and near Gas producing units foster company’s operational efficiency.

Chambal maintains high operating efficiencies at both the plants. The new policy (fixed incentive beyond reassessed capacity subject to maximum of import parity price of urea plus incidental charges), along with gas pooling, has aided production above reassessed capacity and, subsequently, lent relatively more stability to Chambal's overall profitability over the medium term.

Because of the pass-through nature of feedstock costs and Chambal's superior operating efficiencies, it enjoys good cash accruals which allows it on the financial flexibility parameter. It has the ability to replace its debt at competitive prices and also has unutilized bank facilities. This helps it maintain a strong credit profile.

Timely completion of the brownfield expansion project will further enhance the strong market position in the urea business.

Company’s board has approved plan to sell its shipping business. The proposed transaction will be consummated as and when the company receives commercially viable and acceptable offers.

With the government introducing DBT (Direct Benefits Transfer), we believe that companies across the sector are likely to benefit in terms of working capital cycle.

Large scale project implementation risks at Gadepan, high debts due to working capital requirements and capex funding requirements, high regulations in the fertilizer industry are some of the major risks attached to Chambal’s business.

Dr.Reddy’s Laboratories (Mcap Rs 43501.46 cr)

DRL’s net profit grew 175% Y-o-Y in Q4FY17 as margins improved. This happened as other income fell by 76% Y-o-Y to Rs205mn from Rs850mn. Its tax rate declined to 2.9%from 57.3% of PBT due to the resolution of certain tax matters amounting to Rs.568mn. There are new launches in line in the US generics anddomestic businesses segments that could bring good turnarounds in the business in the coming quarters.

The company has acquired a portfolio of 8 ANDAs in the US for $350mn (Rs23.3bn) from Teva. Outof eight ANDAs six are Para IV.

DRL’s operating working capital decreased by $72 million during the fourth quarter. Capital expenditure for the quarter was at $36 million and for the full year it was $179 million. DRL also had a lower tax rate for the quarter primarily due to resolution of certain tax matter pertaining to prior year.

Consolidated gross profit margin for the quarter is 51.2%, gross margin for Global Generic and PSAI were at 58.4% and 10% respectively. Relative to the previous quarter, this is a sharp decline primarily on account of continuing pricing pressure, no new significant product launch in the quarter together with supply constraint.

Given the weakness in the US business, the company is now focusing on expanding presence in Europe and other emerging markets—especially through launch of limited-competition, higher-margin biosimilars—and is additionally increasing local presence by setting up local offices and exploring alliances for further growth.

The upside moves in the stock can come from increased traction in the non-US markets driven by geographical expansion and increasing penetration in these markets, further supported by stabilization of exchange rates.

The institutional business is gaining traction and may additionally benefit from supply disruptions in the API facilities of some peer group companies in its key products.

Risks faced by the company include continuing to grapple with remediation of key facilities, potentially delaying approvals/launches during the year, while the base business continues to witness increasing competition (especially the injectables franchise) and pricing pressure.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 3

JK Tyres Ltd (Mcap Rs 3784.38 cr)

Construction of roads on such a large scale would pep up demand for commercial vehicles. Once the new roads are constructed it would provide easier last mile connectivity and give a push to commercial vehicle as well as passenger car demand.

The acquisition of Cavendish has given JKTL a strategic entry into the very fast moving 2/3W segment which was lacking in its portfolio. With the Cavendish acquisition JK Tyres’ domestic capacity has gone up by as much as above between 50-60% totally. The 2/3 wheeler capacity can be increased by adding some balancing equipment.

With most capex completed, focus will now be on sweating these assets including the Cavendish assets for the next 1-1.5 years post which plans for next capex would be finalized. In the meanwhile the cashflows will be utilized to pare down the debt on books.

The manufacturers have been introducing next generation better equipped trucks and buses which require premium products. The Indian CV industry has been moving away from looking at the initial cost towards cost of ownership over the life of the vehicle. The increasing awareness of cost-benefits of radial tyres over bias tyres is also resulting in strong growth of radial tyres in the replacement markets as well. As per industry estimates OEM radialization is expected to reach 88% by FY21 while overall radialization is likely to be 77%.

The prices of raw material consumed by the company like natural rubber, carbon black, synthetic rubber, etc. are extremely volatile and could impact the margins if the company is not able to pass on the increase. The last couple of years have witnessed strong growth in the automobile industry leading to strong replacement demand for tyres. Any slowdown in the industry could result in lower growth for JKTL. Continous capacity addition by the players could result in oversupply and undercutting going forward.

JSW Steel (Mcap Rs 50362.79 cr)

JSWSL is part of the JSW group, which in turn is part of the O.P. Jindal group. JSWSL is one of the leading steel producers in India with a steelmaking capacity of 18 mtpa. Its integrated steel manufacturing units located across three states (i.e., Karnataka, Maharashtra and Tamil Nadu) have facilities to produce a wide range of flat and long steel products. Furthermore, through its wholly-owned subsidiary (JSW Steel Coated Products Ltd), the company is one of the leading producers of value-added downstream steel products in India specializing in galvanized sheets, galvalume products and high-end colour coated sheets.

It announced projects of Rs ~190bn to augment the steelmaking capacity by 5 mTPA (BF capacity at Dolvi, Rs 150bn) and downstream capacities by 1 mTPA (CRM -1 at Vijayanagar, Rs 20bn) and 0.96 mTPA (Cold rolling at JSW coated products, Rs 12bn). These projects will likely be completed by March 2020. The capex also includes enhancement of BF-3 at Vijayanagar by 1.5 mTPA and shutdown of higher cost BF-2, thus keeping Vijaynagar capacity constant at 12 mTPA.

Domestic steel demand is expected to recover post demonetization with the higher infrastructure outlay in the budget and recovery in rural demand on the back ofnormal monsoon expectations which shall directly benefit company’s core business. MIP and import duties on steel and steel products will also help.

US subsidiary's plate and pipe mill operations reported a positive EBITDA in the recent quarter ended as compared to a loss for the same period in previous fiscal and utilizations levels improved YoY. Coated products reported a sharp increase of 66% YoY increase in EBITDA with improved realizations and profitability.

Consolidated net debt, excluding acceptances and payables for capital projects, stood at Rs.415.5bn, decreasing from Rs.442.6bn at the end of Dec-16 aided by strongoperational cash flows.

Domestic spot steel prices have corrected since March following a fall in China FOB prices. Despite protection, current HRC CIF import prices imply a further downside. Given weaker demand and low global prices, spreads may remain under pressure. Slower growth in demand (within & outside India) remains another risk.

Kotak Bank (Mcap Rs 182507.67 cr)

Consolidated loan grew 5% QoQ in Q4FY17 led by almost all non-corporate segments. In retail loan growth, CV and agriculture segments saw sharp improvements of 12% and 14% QoQ respectively. Management has guided for > 20% loan growth in FY18.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 4

Led by a superior NIM performance (4.6%, +10bps QoQ), healthy fee growth of 24% (driven by third party distribution income), and higher recoveries and controlled opex (+2% QoQ), PPOP grew 43/11% YoY/QoQ. Operating leverage was visible with Cost to Income improvement of 220bps to 46%. A stable NIM (4.6%), steady traction in fees (17% CAGR) and controlled opex (15%) will drive efficiencies.

KMB’s stressed exposures remain minuscule, with a restructured book of 7bps, SMA II of 10bps and no utilisation of RBI dispensation.

Management intends to maintain higher per branch employee compared to industry, as it continues to push acquisitions and servicing of business by a bigger ground presence. Management indicated there is still scope for business optimisation from erstwhile ING branches and it could lead to continued traction in CASA growth hereon.

With a well-distributed loanbook acrosssegments, KMB is among the best placed banks to capture growth momentumacross business verticals. KMB has strong presence across all financial product verticals and should gain with its improved reach and strong cross-marketing skills, leading to improvement in RoE.

While merger synergies continue to kick-in, controlling deterioration in asset quality would be key.

Larsen & Toubro (Mcap Rs 157126.66 cr)

L&T is exposed to several levers across business/geographic segments and has emerged as the E&C partner of choice in India, which provides a robust foundation to capitalize on the next leg of investment cycle.

L&T has a dominant position and market share in most operating verticals, be it oil & gas, process projects, roads, bridges, or industrial structures. This imparts flexibility to cherry-pick projects across a wide range of projects and thus helps optimize overall business profitability.

Revenue growth of L&T was led by 52% growth in other segments, led by strong execution in material handling orders. Performance in the core Infra segment was a bit subdued, with 8.2/6.7% YoY growth in 4QFY17/ FY17 respectively.

Manufacturing businesses like Power BTG, Shipbuilding and Special Forgings are expected to witness sharp improvement in order intake, led by pick-up in project awards in Power BTG, Defence and Nuclear segments.

Apart from traditional public sector capex (Roads, Railways, Metros, Power T&D and Water), order inflow visibility has improved from sectors like Defence and Hydrocarbons. With a strong order pipeline, coupled with book-to-bill of over 2x (TTM sales), L&T is well set to meet its guidance.

Government is mandating a focused approach for the private sector on defence capex. Tactical communication system/Battlefield Management System is currently not in focus due to fund allocation. L&T is positioned to do submarines only in strategic partnership category. It will take 10 years for any private player to do aerospace and hence does not look practical. In Future Infantry Combat Vehicle, L&T is the highest scorer, but will take some time.

Perceived risk of a slowdown in Middle East capex due to sharp drop in global oil prices can severely impact L&T’s order intake and revenue accruals.

From a balance sheet perspective, net working capital saw a significant improvement during Q4FY17 as the same was at 19% of sales vs. 23% of sales in FY16. Even from a cash flow perspective, the company generated CFO to the tune of Rs.12200 crore in FY17 vs. Rs.7700 crore in FY16. This is also reiterated by interest costs that were down, on a standalone, consolidated basis, by 10.2%, 6% YoY, respectively.

L&T reported a strong order intake of Rs.47,289crore, up 9.6% YoY. Also, going forward, the company has guided 12% growth in its revenue and 12-15% growth in its order intake. In terms of opportunities, L&T expects to bag orders to the tune of Rs.15000 crore and Rs.10000 crore from the hydrocarbon and the defence segment.

During Q4FY17, the company reported a backlog of Rs.216000 crore. However, the company removed Rs.18000 crore worth of non/slow moving orders from the backlog. These orders were from the building & factories and Power T&D space

The work on Hyderabad metro is completed to the tune of 70%. The project is slated to be fully commissioned by December 2018. The company is expecting a favourable settlement with the respective state government within next year.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 5

Pidilite Inds (Mcap Rs 42052.8 cr)

With an iconic brand like Fevicol, Pidilite is the largest branded adhesives player in India. Company has expanded into emerging segments like mechanized joinery, modular furniture, flooring, automotive care and water proofing through Dr Fixit and Roff.

The company will be a clear beneficiary of GST.Adhesives are under 18% GST (25-26% earlier), irrespective of unit pack size. Sealants are at 28% GST (earlier ~26%); rate on art products is 28% (earlier ~26%) and on industrial segment is 18% (earlier 18-19%). Reduction in GST rates will be passed on to customers.

Pidilite has set up construction chemicals manufacturing unit in Middle East and has acquired its local distributor, which should enable turnaround in this region. Bangladesh remains a highly profitable market and acquisition of market leader in Sri Lanka holds potential for higher growth in this region. However Brazil business could be restructured or sold off in future.

Adhesives, sealants and construction chemicals are tipped as key growth drivers over the long term. These segments contribute ~71% to the standalone sales and PidiliteInds has leading positions in these products with brands like Fevicol, Dr Fixit and Roff. Overall increase in furniture and interior demand and sustained trend of homemade furniture in the Tier 2‐3 cities will continue to provide growth to Pidilite.

Pidilitehas grown its revenues at a ~17% CAGR over the last 15 years.While growth has slowed down over the last two years (FY16 and FY17) due to a macro slowdown as well price deflation, mid-doubledigit growth rates is expected from FY18 on the back of recovery in volume growth and resumption of pricing.

Titan Inds (Mcap Rs 47545.39 cr)

Company is aggressively eyeing for growth over next five years, supported by the shift in consumer preference toward organized brands. The company could also see a focus on new opportunities/businesses (smart watches, fragrances, silk sarees, ecommerce) going forward.

Titan aims to open 27 new stores in 19 towns in FY18 as part of this initiative. There could be a greater focus on locally popular products in these stores. Company considers this as an opportunity to grab share from unorganized as well as other organized peers, especially as unorganized segment is likely to struggle for a couple of years to comply with GST requirements.

In Eyewear, the company expanded rapidly with 95 new stores (20 low-cost stores for small towns) and discontinued/closed down Spexx format of stores. It converted a number of company stores to franchisee stores for better profitability.

There has been a strong revival and market share gains in Jewellery, company has set an ambitious target of 2.5x growth in Jewellery by 2022, implying a CAGR of 20%. Since next two years could potentially offer strong opportunities for market share gains (as unorganized players take time to cope with GST requirements), the company intends to go all out even at the cost of near-term profitability and RoEs.

Lesser Known Stocks

Sr No Company Industry Equity Latest FV CMP

Book Value latest

Net Sales FY17

Change in sales y-o-y

PAT FY17

Change in PAT y-o-y

EPS TTM

P/E TTM P/BV

Last Div %.

Dividend Yield

1 Brigade Enterpr. Construction 135.7 10 260.7 161.2 2024.1 -0.7% 167.2 20.2% 12.0 21.7 1.6 25 1.0%

2 Control Print Packaging - Others 15.7 10 339.7 86.1 145.2 9.2% 25.74 6.1% 16.7 20.4 3.9 60 1.8%

3 G M D C Mining / Minerals 63.6 2 150.0 126.0 1536.7 30.4% 324.09 48.0% 10.2 14.7 1.2 150 2.0%

4 GreenlamIndustr Laminates 12.1 5 860.5 120.4 1075.9 4.5% 49.8 32.1% 17.8 48.4 7.1 30 0.2%

5 ION Exchange Pollution Control Equi 14.7 10 495.0 135.2 1016.1 17.3% 28.34 85.1% 31.3 15.8 3.7 35 0.7%

6 Kaveri Seed Co. Miscellaneous 13.8 2 645.1 146.8 705.0 -5.4% 131.27 -21.6% 19.8 32.6 4.4 0 0.0%

7 Manappuram Fin. Finance - Small 168.4 2 97.5 39.9 3387.7 43.5% 755.85 112.9% 9.0 10.9 2.4 100 2.1%

8 Volt.Transform.* Electric Equipment 10.1 10 1253.3 513.1 609.4 8.2% 67.97 54.5% 67.2 18.7 2.4 150 1.2%

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 6

Source: Capitaline Database, *= Standalone Number All figures are Consolidated and in Rs. except for Equity, Sales FY17 and PAT FY17 which are in Rs.Cr., CMP is as of July 04, 2017, EPS is adjusted for extraordinary items. Past dividend yield may not necessarily sustain in future

A brief write up on the eight stocks is as under: Brigade Enterprises Ltd (Mcap Rs 3536.77 cr)

Brigade Enterprise Limited (BEL) is the flagship company of the Brigade group, which was established in 1986 by Mr. M R Jaishankar, and is one of the largest players in the real estate market of South India. Till date, it has developed around 26 million sqft, 90% of which has been in the residential segment. It has developed a market for itself in Bengaluru,Mysuru, Cochin, and Chennai.

BEL is a prominent real estate developer with 30 years of healthy track record in Bengaluru and a strong market position helping it maintain a good 3-4% market share in a highly fragmented market.

BEL's revenue profile is moderately diverse comprising of three main businesses: real estate development, leased assets and hospitality.In addition to the ongoing real estate development portfolio of 14.6 million sqft, the group has a healthy lease asset portfolio of around 2.2 million sqft and three operational hotels in Bengaluru and Mysuru. Customer advances received and the realizations on sales already booked shall allow BEL to enjoy healthy cash flow generation.

BEL has Rs 9.9bn of asset / land capex over next 4 years pending and has a further new capex pipeline of Rs 7bn. QIP funds raised (2.2 cr shares @Rs.227.50 in May 2017) shall although dilute the equity but bring down the financial leverage levels for the company.

BEL's cash flows will be further supported by stabilization of operations in commercial and hospitality business, which are currently undergoing capex cycle. The group is expected to add 1.5 million sqft of leasable commercial/retail area and expand its hospitality business to about 1,000 keys over the next 24 months. The resulting increased diversification will help offset the higher volatility in the residential segment.

Higher debt levels due to increased capex, lesser land acquisition programs, highly cyclical nature of real estate business, headwinds of demonetization, etc. are all some of the major concerns associated with this stock.

Control Print Ltd (Mcap Rs 532.39 cr)

Control Print is a leading coding & marking player domestically with manufacturing capability in printing machines, spare parts & associated consumables (ink). These are required to print essential real time product details like manufacturing date, expiry date, batch number, maximum retail price, etc, on any manufacturing product. As of FY17, CPL has a market share of ~18% in the oligopolistic market (valued at ~Rs 900 crore).Control print has technology tie up with KBA Germany for CJI printers and consumables (inks & solvents).

Increasing share of high margin consumables has resulted in ~1260 bps EBITDA margin expansion over FY12-FY17 from 13.8% to 26.4%. Share of consumables in FY12 gross sales was at 49% while the same in FY17 was at ~80%.

CPL is present in a lucrative opportunity landscape, which is bound to grow given the stringent legal requirements on display of essential product details, better inventory control & counterfeit prevention.

Sound balance sheet with nil debt and return ratios in excess of 20% coupled with strong demand in newer segments of dairy and sugar should result in improved results going forward.

Control Print is targeting 20% CAGR in revenues over the next 2-3 years.

Temporary disruption on implementation of GST and elongated working capital cycle of over 200 days are key risks for the company.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 7

GMDC Ltd. (Mcap Rs. 4768.41 cr)

Gujarat Mineral Development Corporation Ltd (GMDC) is a mining and mineral processing company formed in the year 1963 by the Govt of Gujarat. It is also the largest merchant seller of Lignite in India. The company produces lignite, bauxite, fluorspar, and manganese ore and is also engaged in power generation.

Company has ramped up its operations and production capacities at other mining sites. With the persistent and growing demand from various fast growing sectors of the economy like textiles, chemicals, ceramics, bricks, power, etc. company is expected to increase its mining activities at its will and reap the benefits of higher operating leverage it is exposed to owing to the nature of its business. The same is evident from the fact that company could increase the production at its Mata No Madh site to 1.07 mt of lignite as against 1.37 mt of lignite in whole of FY16.

GMDC supplies ~80% of its volumes to small customers operating in sectors like bricks/ceramics, textiles, paper, chemicals and other SMEs. These operations typically use hand-fired boilers which work better with lignite and may be unable to use high energy intensity fuels. Further, the ticket sizes of these customers prevent them from accessing the imported coal market. Continued strengthening of pet-coke prices shall aid the company achieve higher demand from the cement and other industries running on pet-coke. It also helps the company improve its pricing power among other customers and in turn help it improve its realizations.

GMDC, operational in state of Gujarat, has to bear the incidence of 22.50% VAT and 6% Excise duty on the production of lignite. On considering the overall share of indirect levies on lignite’s cost structure, it would sum up to around 37% of its cost due to the cascading effect of taxes. The roll out of GST would be a major positive bringing down its costs and leaving better pricing power at its hands.

In the Power generation segment, Company is expected to continue at this level of PLF for the coming two years maintaining a stable outlook over the thermal power generating segment of the company. Company has recently increased its wind energy generation capacity from 155 MW to 200 MW and had witnessed a rough period in H2FY17.

Changes in environmental laws, changes in land acquisition / mining laws, changes in the prices of substitutes for lignite like coke and petcoke, disappointment in extraction levels, change in PLF / power generation lawsetc are some of the major concerns and risks attached with the company.

Greenlam Industries Ltd(Mcap Rs 2076.81 cr)

GIL has raised its capacity at Nalagarh, in Himachal Pradesh, to manufacture additional 2.00 million laminate sheets per annum, the installed capacity for laminate has become 12.02 million laminate sheets per annum. This increased capacity of laminates in FY18 could provide an upside and visibility to revenue growth and generate revenue of Rs.120 Cr per annum on full capacity utilization. On the part of capacity utilization GIL has delivered 110% of capacity utilization till Q4FY17.

GIL has extensive export market. During the year 2015-16, the Company recorded agrowth of 5.23% in export turnover from Rs.31,002.12 lac to Rs.32,624.18 lac. Recognizing the fact the company continued to expand itsexport markets for Laminates, Veneers and Engineered Wood flooring. It is India’s largest Exporters of laminates.

The Recent GST implication has a positive impact in increasing the market share of GIL, and, the threat of from unorganized share would get curbed.

On a consolidated basis, although Revenue growth for FY17 is only 4% as compared to previous year’s 11%, PAT margin grew 5% as compared to 4% last year, with EBIDTA margin being maintained at the same 13% rate. Furthermore, Debt-equity ratio is falling over the years as can be seen. The long-term debt has declined from Rs.237.4 Cr in FY13 to Rs.97 Cr in FY17.A declining capital spending coupled with increased cash flow has helped minimize its debt.Even theNalagarh capacity was raised through internal accruals.

GIL’s major raw material component is paper and chemicals. 83% of cost of material consumed is formed up by paper & Chemicals. Raw material cost (including traded goods) formed about 53.3% for FY16. Around 60% of the raw materials consumed in FY16 were met throughimports. Methanol and Phenol being the primary chemical requirements are dependent on crude oil prices, which is highly fluctuating.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 8

Ion Exchange Ltd (Mcap Rs 726.07 cr)

Ion Exchange Ltd is into waste water management and the same is projected to grow at a CAGR of 8-10% through 2015-2022. The water chemicals market in India is expected to grow at a CAGR of 15% over FY15-19 from $0.4 bn in FY14 to $0.8bn in FY19 The company posted a Y-o-Y revenue growth of 17% for FY17 on consolidated terms.

Ion Exchange has a health order book of ~Rs.2040 Cr (including the desalination order of $200 mn from Sri Lanka) out of which orders worth ~Rs.680 Cr are executable over a period of 18-36 months. The order from Sri Lanka (~Rs.1,350 Cr) is expected to be executed over a period of 3 years and the billing for the same will be milestone driven.

US FDA approval for the manufacturing facilities of Ion Exchange opens up huge market potential in the US and Europe for Drug Active resins. Ion exchange plans to utilise the US and Europe markets for drug active resins, which has strong growth potential with very good margins.

Revenue from the chemical segment has grown at a CAGR of 14.1% to Rs.297.7 Cr in FY16 from Rs.175.8 Cr in FY12. Going forth, revenue from the Chemical business is expected to grow at a CAGR of 15% from Rs.342.4 Cr in FY16 to Rs.452.8 Cr in FY19, driven by robust growth prospects of the global and domestic chemical market and USFDA approvals for resins used in the Pharma industry.

The company has plans to contemplate a CAPEX amounting to Rs.130 Cr for the purpose of increasing its capacity In the Chemicals division and help in executing the Sri Lanka order. A major portion of this CAPEX amount is to be funded internally. However, the debt is expected to rise to ~Rs.128 Cr by FY19 from Rs.90 Cr in FY16.

Although the company is having a good order book still, it is highly dependent on growth and infra spend across geographies. Slowdown in the infra spends can lead to delay in order execution resulting into poor cash flows and revenue.

Kaveri Seed (Mcap Rs 4454.4 cr)

Kaveri is one of the leading seeds players in India with a large network of over 15,000 distributors and dealers spread across the country, company has 700+ employees and a strong product line of hybrids. Company has dominant positioning in most of the key crops: cotton (20% market share), Corn (~13% market share), Bajra (13% market share) and Rice (~9% market share).

Out of the total cash reserves, company has announced to allot Rs 200 Crores for a buyback (announced share buyback of 2,962,963 equity shares of face value of Rs. 2 each at a price of Rs. 675 per share). The rest is used for royalty settlement with Monsanto and company could allocate some money for Kharif season. As management indicates, post first quarter they could get the clarity on how much they would spend on dividends.

Hybrid vegetable seed is one of the fastest-growing segments in India estimated to be around Rs. 2,000 crore. For vegetables, Kaveri Seed has built an exclusive sales team of more than 20 dedicated employees, launched new products, built a focused distribution network and evaluating in-licensing opportunities. Looking ahead, cotton seed production is expected to be better than last year both in terms of quantity and quality with recovery rates expected to be higher.

Kaveri Seeds has launched 8 new products in FY17 - 3 in Maize, 3 in Bajra and 2 Rice; increased number of demonstration of pre commercial products and expect to report better earnings from the same over the coming years.

Kaveri Seed’s multi-crop portfolio, superior R&D, strong product launch capabilities, supply chain efficiencies, farmer relationships and comprehensive distribution network are key rationale for long term and sustainable success, company could see profitable revenues, a strong ROCE profile and strengthen cash flows.

Vagaries of monsoon, regulatory issues and increasing competition are the main risks faced by the company. Manappuram Finance Ltd. (Mcap Rs 8204.8 cr)

MFL has its re-aligned its gold loan portfolio and added shorter tenure loans of 3-6-9 months as compared to a single product offering of 12 months loan. It has also linked the product LTVs to the tenure of the loan thereby reducing its risk. The introduction of shorter duration of loans and linking the LTV to the tenure has resulted in margin of safety for a 12 month loan increasing to 23% from 4% earlier.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 9

As per ICRA estimates, the Gold Loan market is expected to regain some of its lost momentum and grow at an annual rate of 13-15% over FY15-FY18, to reach a market size of about Rs 1,900-2,100 billion in FY18.

Specialized gold loan companies enjoy competitive advantage particularly in terms of their last mile connectivity, availability vis-à-vis the other organized lenders in the market. The benefits that these niche financiers enjoy primarily due to focused nature of their business, outnumber the other financiers in the organized lending market.

The non-gold loan businesses of MFL continue to witness strong growth aiding in product diversification and reducing dependence on gold loans for business growth. The company is targeting non-gold business of 25% in FY18.

The recent stipulation of the RBI that loans above Rs. 20,000 have to be disbursed only by cheque is one such adverse regulation (for the near term). Higher NPAs in the non-gold business could impact growth and profitability.

Voltamp Transformers Ltd (Mcap Rs 1268.29 cr)

Voltamp’s sales comprises 58% of revenue from renewable (Solar power, Wind) and T&D (State Transcoms) and both these sectors are showing strong growth in investment.

Delayed power projects due to economic slowdown or other issues are being revived which should result in higher order flows in the coming years. Capacity utilization of the company has increased from ~50% in FY14 to over 70% in FY16. We expect the utilization to improve further to ~80-89% over FY17-FY18E on back of robust order inflows and higher execution.

With sufficient generation capacity, there would be a need for a robust transmission network integrating the various conventional and renewable power sources as a key policy objective. India has achieved almost 100% of the transmission infrastructure target set in the 12th Five-Year Plan (FY13-17). The transmission capex for the 13th Plan (FY18-22) is at Rs2.6tn.

VTL has remained a debt free company since 2008. Due to its debt free nature the company has been able to report decent profits even during slowdown in which its competitors were making losses. The company also has investment of Rs 295 cr which it can liquidate whenever there is need for funds.

The Company enjoys better margins as there is high level of customization involved in the designs of the products as per the clients requirement and also as the execution cycle is shorter for the industrial client, due to a very tight delivery schedule.

The company has orderbacklog of Rs.300 crore (4,739 MVA) that imparts revenue visibility of next 2 quarters. The company has declared Rs.670 crore (11,056 MVA) of order inflow in FY17E from different verticals like Solar Power Generation, State Transcoms, Refining, Chemicals, Sugar and other SMEs.

Structural demand recovery especially from Solar Power Generation and investment by State Transcoms over next 3-4 years that will drive demand for transformers.

Due to the entry of large number of players during favourable time, there is overcapacity in the industry currently. As a result there is huge competition and aggressive pricing is undertaken by some of the players which could impact margins.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 10

Technical report on 16DIYSIP (Do it yourself Systematic Investment Plan) Stocks

Better Known Stocks S.No Scrip CMP Max. Downside Probable Upside Period

1. Chambal Fertilizers & Chemical Rs.127.7 Rs .110 Rs .200 1-2 Years

2. Dr. Reddy’s Lab Rs.2623.0 Rs.2370 Rs.3700 1-2 Years

3. JK Tyre & Industries Rs.166.7 Rs .135 Rs .238 1-2 Years

4. JSW Steel Rs.208.0 Rs.180 Rs.265 1-2 Years

5. Kotak Bank Rs.959.0 Rs .850 Rs .1250 1-2 Years

6. Larsen & Toubro Ltd Rs.1683.0 Rs.1560 Rs.2100 1-2 Years

7. Pidilite Rs. 821.2 Rs. 700 Rs. 995 1-2 Years

8. Titan Rs.534.2 Rs .460 Rs .750 1-2 Years

Lesser Known Stocks

S.No Scrip CMP Max. Downside Probable Upside Period

1. Brigade Rs.261 Rs. 237 Rs .408 1-2 Years

2. Control Print Rs .341.80 Rs .300 Rs .450 1-2 Years

3. GMDC Rs.149.95 Rs.125 Rs.222 1-2 Years

4. Greenlam Industries Rs.866 Rs .710 Rs.1100 1-2 Years

5. ION Exchange Rs.496 Rs 410 Rs .700 1-2 Years

6. KSCL Rs. 642.60 Rs.530 Rs. 860 1-2 Years

7. Manapuram Rs.97.45 Rs .79 Rs .170 1-2 Years

8. Voltamp Transformers Ltd Rs.1253 Rs.1100 Rs.1900 1-2 Years

Note: 1. These stocks have been picked on the assumption that they have some downside possible/left, post which a healthy uptrend could begin. 2. SIP investments will give good returns only if the average entry price is lower (due to the initial fall expected). In case the stock price first rises and then falls, SIP

investment may not generate attractive returns. 3. In case at any time during the period of SIP, the stock price moves up sharply (compared to the average entry price) – to attain the probable upside level or say 13-

25% above the average entry price – depending on the capitalization and volatility of the individual stocks, then it would be a good idea to stop the SIP and sell the stocks booking the profits accrued.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 11

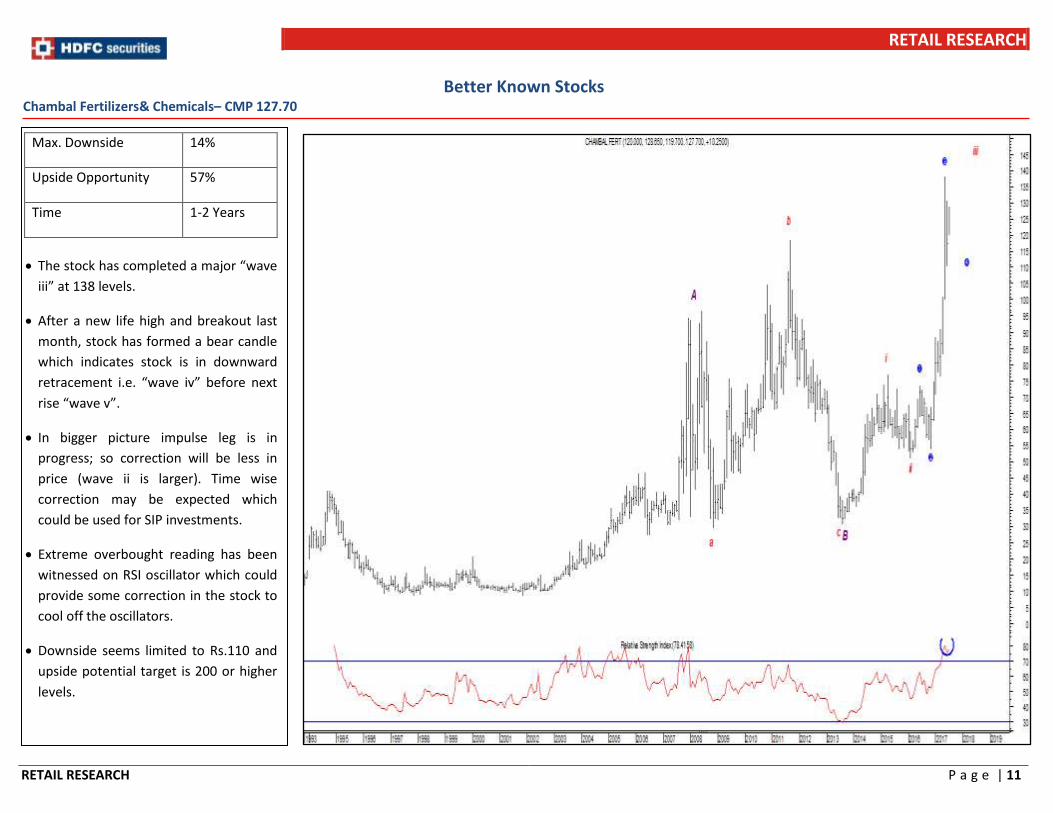

Better Known Stocks Chambal Fertilizers& Chemicals– CMP 127.70

Max. Downside 14%

Upside Opportunity 57%

Time 1-2 Years

The stock has completed a major “wave

iii” at 138 levels.

After a new life high and breakout last

month, stock has formed a bear candle

which indicates stock is in downward

retracement i.e. “wave iv” before next

rise “wave v”.

In bigger picture impulse leg is in

progress; so correction will be less in

price (wave ii is larger). Time wise

correction may be expected which

could be used for SIP investments.

Extreme overbought reading has been

witnessed on RSI oscillator which could

provide some correction in the stock to

cool off the oscillators.

Downside seems limited to Rs.110 and

upside potential target is 200 or higher

levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 12

Dr. Reddy’s Lab Ltd - CMP Rs.2623.0

Max. Downside 10%

Upside Opportunity 41%

Time 12-18 Months

The stock price has been in a

downtrend over the last many months,

as per monthly timeframe.

Presently,it is showing near term

bottom reversal pattern around the

support of 50% Fib retracement at

Rs.2370 levels.

Monthly 8 period trend strength

indicator ADX is placed at the key lower

levels of 20 and is turning up.

Previously, we observe emergence of

sharp buying interest from the ADX

turning up near 20-25 levels.

Look to invest in SIP mode.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 13

JK TYRE & Industries – CMP 166.75

Max. Downside 19%

Upside Opportunity 43%

Time 1-2 Years

The stock has completed a five wave

advance at 186 levels.

Last two months stock has formed two

consecutive bearish reversal candle

which indicates stock is in downward

retracement before next rise.

In bigger picture impulse leg is on the

cards; so correction will be less in price

(throwback fall). Time wise correction

may be expected which could be used

for SIP investments.

Negative divergence has been

witnessed on RSI which could provide

some correction in the stock.

Downside seems limited to Rs.135 and

upside potential target is Rs.238 or

higher levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 14

JSW Steel - CMP Rs.208.0

Max. Downside 13%

Upside Opportunity 27%

Time 1-2 Years

JSW Steel has been consistently

making higher tops and higher

bottoms for the last several years.

With long term momentum readings

still not extremely overbought, we

believe the stock still has more upside

potential.

While the uptrend is still intact, we

believe any correction could see the

stock coming down towards its 200-

day EMA at 180.

We expect the stock to head towards

new life highs of 265 after a short term

correction as the stock resumes its

long term uptrend.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 15

Kotak Bank - CMP Rs.959.0

Max. Downside 11%

Upside Opportunity 30%

Time 1-2 Years

Kotak Bank has been consistently

making higher tops and higher bottoms

for the last several years. We believe

this pattern is set to continue for the

foreseeable future.

The stock is however now in a short

term downtrend as it has broken its

near term supports and trades below

the 13 day SMA. It could therefore

correct further towards the 850 levels

in the near future.

The 850 levels correspond to the 200-

day EMA thereby making it a crucial

support and a good level to buy more

of this stock.

We expect the stock to head towards

new life highs of 1250 after a short

term correction as the stock resumes

its long term uptrend.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 16

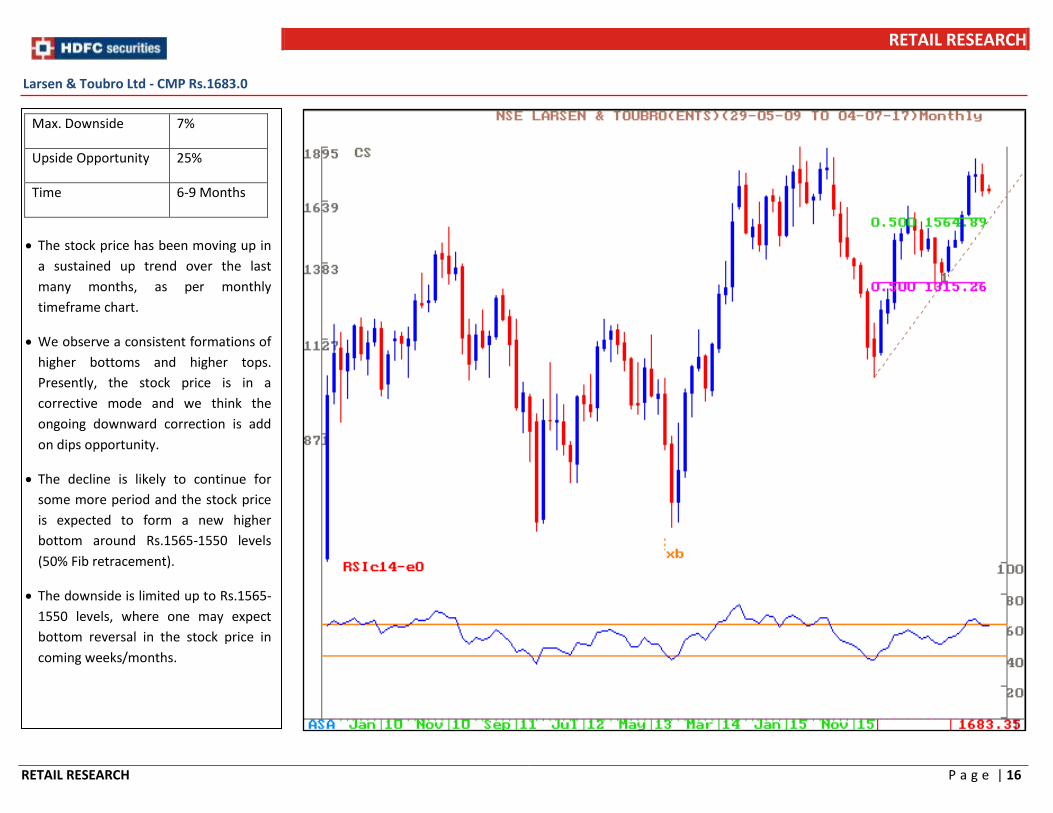

Larsen & Toubro Ltd - CMP Rs.1683.0

Max. Downside 7%

Upside Opportunity 25%

Time 6-9 Months

The stock price has been moving up in

a sustained up trend over the last

many months, as per monthly

timeframe chart.

We observe a consistent formations of

higher bottoms and higher tops.

Presently, the stock price is in a

corrective mode and we think the

ongoing downward correction is add

on dips opportunity.

The decline is likely to continue for

some more period and the stock price

is expected to form a new higher

bottom around Rs.1565-1550 levels

(50% Fib retracement).

The downside is limited up to Rs.1565-

1550 levels, where one may expect

bottom reversal in the stock price in

coming weeks/months.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 17

Pidilite - CMP Rs. 821.2

Max. Downside 15%

Upside Opportunity 21%

Time 1-2 Years

The stock is making higher top higher

bottom formation and currently it is

facing resistance at 100% extension

level. However the stock has the

potential to move higher.

This upmove in the stock could

continue in the coming months.

Time wise correction in the stock

seems possible where stock could

come down to Rs. 700 level which

coincides with 33.3% extension level

with change of polarity level. Hence

Traders can do the SIP investment as

stock is in time wise correction.

Oscillators and indicators are placed

with a positive bias.

Downside for the stock is limited to Rs.

700 and upside potential target is Rs.

995 or above levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 18

Titan - CMP Rs.534.2

Max. Downside 14%

Upside Opportunity 40%

Time 1-2 Years

The stock is currently trading above the

upward gap which stock has created on

05th June 2017. The stock has also

crossed above the downward sloping

trend line which is a bullish indication

for the stock. The upper line of the gap

value is also coinciding with change of

polarity level suggesting good support

at that level.

Oscillators and indicators are placed

with a positive bias. ADX is suggesting

current trend in the stock could

continue.

Time wise correction may be expected

where traders may try to fill the gap but

this down move could be a good

opportunity to accumulate the stock,

which could be used for SIP

investments.

Downside seems limited to Rs.460 and

upside potential targets are Rs. 750 or

higher levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 19

Lesser Known Stocks Brigade - CMP Rs.261.0

Max. Downside 9%

Upside Opportunity 56%

Time 1-2 Years

Brigade has broken out of a

consolidation pattern on the

Monthly/Quarterly charts and made

new 52-week highs in the process.

The breakout was accompanied with

above average volumes, which

indicates that there has been significant

accumulation in this counter.

Technical indicators are also supporting

the stock as it trades above the 13-

month Simple Moving Average and also

the 200-day EMA.

Long term momentum readings like the

14-month and 14-Quarter RSI are in

rising mode and not yet extremely

overbought. The MACD indicator too is

in rising mode.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 20

Control Print – CMP 341.8

Max. Downside 12%

Upside Opportunity 32%

Time 1-2 Years

The stock has provided a breakout of

inverted head & shoulder pattern.

After a breakout it may provide

throwback fall which could take longer

time but lesser price correction which

is good SIP opportunity.

In bigger picture impulse leg is in

progress and stock is in “wave v” which

could be slow in nature as “wave iii”

has outperformed in lesser time.

RSI is approaching overbought territory

(70 levels) currently placed at 67.22 so

there could be some minor corrective

leg unfolding.

Downside seems limited to Rs.300 and

upside potential target is 450 or higher

levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 21

Gujarat Mineral Development Corporation Ltd - CMP Rs.150.0

Max. Downside 17%

Upside Opportunity 48%

Time 1-2 Years

The stock price as per larger timeframe

has been moving up consistently over

the last 15-16 months.

We observe a formation of larger

higher tops and bottoms and minor

intermittent corrections have been

absorbed into further upmoves.

The stock price is now placed at the key

overhead resistance of primary down

trend line (brown dashed horizontal

line) and there is a possibility of minor

downward correction in the stock price

for the near term.

Oscillators and indicators are placed

with positive sign.

This stock could be considered for

systematic investment for substantial

gains for medium to long term.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 22

Greenlam Industries - CMP Rs.866.0

Max. Downside 18%

Upside Opportunity 27%

Time 1-2 Years

GreenlamInd been consistently making

higher tops and higher bottoms for the

last few years. We believe this pattern

is set to continue for the foreseeable

future.

While the uptrend is still intact, we

believe any correction could see the

stock coming down towards its trend

line supports of 710, which also roughly

coincides with the 200-day EMA,

thereby making it a strong support.

We expect the stock to head towards

new life highs of 1100 after a short

term correction as the stock resumes its

long term uptrend.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 23

ION Exchange – CMP 496.0

Max. Downside 17%

Upside Opportunity 41%

Time 1-2 Years

The stock has completed a five wave

advance at 548 which is “wave i of iii”.

After a breakout of channel the stock

price has rallied sharply and last month

stock has formed long upper shadow

candle which indicates the stock price

may in downward retracement i.e.

“wave ii of iii” before next rise “wave iii

of iii”.

In bigger picture impulse leg is in

progress; so correction will be less in

price (wave ii is larger). Time wise

correction may be expected which

could be used for SIP investments.

Negative divergence has been

witnessed in RSI oscillator which may

provide a minor correction.

Downside seems limited to Rs.410 and

upside potential target is 700 or higher

levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 24

Kaveri Seeds - CMP Rs.642.6

Max. Downside 18%

Upside Opportunity 34%

Time 1-2 Years

The stock is making higher top higher

bottom formation by crossing above

161.80% extension level

This upmove in the stock could

continue in the coming months.

Time wise correction in the stock

seems possible where stock could

come down to Rs. 530level which

coincides with earlier bottom level.

Hence Traders can do the SIP

investment as stock is in time wise

correction.

Oscillators and indicators are placed

with a positive bias.

Downside for the stock is limited to Rs.

530 and upside potential target is Rs.

860 or above levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 25

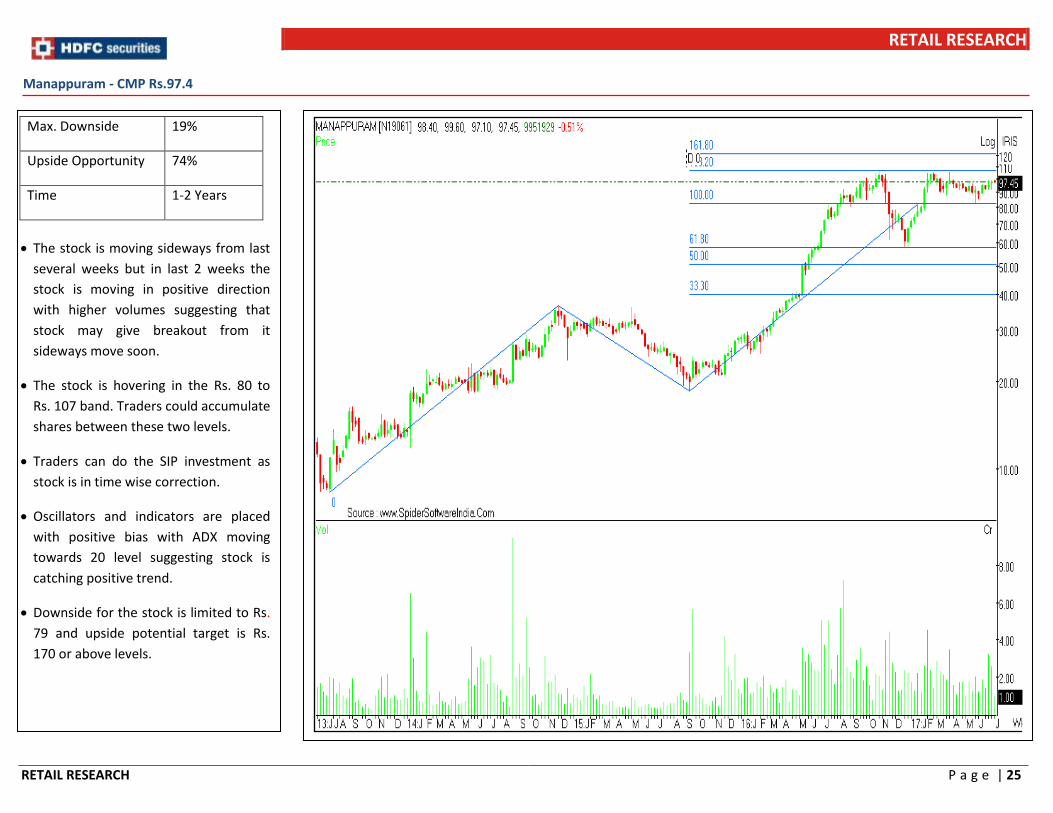

Manappuram - CMP Rs.97.4

Max. Downside 19%

Upside Opportunity 74%

Time 1-2 Years

The stock is moving sideways from last

several weeks but in last 2 weeks the

stock is moving in positive direction

with higher volumes suggesting that

stock may give breakout from it

sideways move soon.

The stock is hovering in the Rs. 80 to

Rs. 107 band. Traders could accumulate

shares between these two levels.

Traders can do the SIP investment as

stock is in time wise correction.

Oscillators and indicators are placed

with positive bias with ADX moving

towards 20 level suggesting stock is

catching positive trend.

Downside for the stock is limited to Rs.

79 and upside potential target is Rs.

170 or above levels.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 26

Voltamp Transformer - CMP Rs.1253.0

Max. Downside 12%

Upside Opportunity 52%

Time 1-2 Years

We observe an intermediate upmove

in the stock price as per the larger

positive sequence of higher tops and

bottoms.

After witnessing upside breakout of the

key hurdle of Rs.1150 levels, the stock

price has now shifted into

consolidation in the last few months.

Recent chart set up is indicating a

possibility of downward correction to

Rs.1100 levels, which could be add on

dips opportunity.

The strength of upside momentum of

the last few years is suggesting

expected correction is unlikely to

damage the trend and the stock price

could shift again into further upmove.

Buying can be initiated with SIP and

one may add systematically on dips for

long term gains.

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 27

Analyst Educational Qualification Stock Holding

SubashGangadharan MBA, Research Analyst Brigade No

GajendraPrabhu MBA, Research Analyst Chambal Fertilizers & Chemical No

GajendraPrabhu MBA, Research Analyst Control Print No

NagarajShetti Graduate-BA, Research Analyst Dr. Reddy’s Lab No

NagarajShetti Graduate-BA, Research Analyst GMDC No

SubashGangadharan MBA, Research Analyst Greenlam Industries No

GajendraPrabhu MBA, Research Analyst ION Exchange No

GajendraPrabhu MBA, Research Analyst JK Tyre & Industries No

SubashGangadharan MBA, Research Analyst JSW Steel No

SubashGangadharan MBA, Research Analyst Kotak Bank No

Siddharth Deshpande MBA, Research Analyst KSCL No

NagarajShetti Graduate-BA, Research Analyst Larsen & Toubro Ltd No

Siddharth Deshpande MBA, Research Analyst Manapuram No

Siddharth Deshpande MBA, Research Analyst Pidilite No

Siddharth Deshpande MBA, Research Analyst Titan No

NagarajShetti Graduate-BA, Research Analyst Voltamp Transformers Ltd No

RETAIL RESEARCH

RETAIL RESEARCH P a g e | 28

This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HDFC Securities Ltd or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HDFC Securities Ltd .

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk.

It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HDFC Securities Ltd may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments.

HDFC Securities and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.

HDFC Securities Ltd, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc.

HDFC Securities Ltd and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report.

HDFC Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

HDFC Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction in the normal course of business.

HDFC Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HDFC Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HDFC Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report. HDFC Securities Ltd. is a SEBI Registered Research Analyst having registration no. INH000002475."