global outlook and development trends for copper - … outlook - pmc...global outlook and...

TRANSCRIPT

© 2012 CRU International Limited confidential1

Global Outlook andDevelopment Trends for Copper

Richard Schodde

Philippines Mining Conference, Manila20 September 2012

31 Mount Pleasant, London

WC1X 0AD UK

Tel +44 20 7903 2000

www.crugroup.com

© 2012 CRU International Limited confidential2

• Will the average copper price in 2012 be higher thanthat in 2011?

• In terms of price, is copper one of the favourednon-ferrous commodities for 2012 and beyond?

• Is the market still considered attractive for new copperprojects?

Key messages in a nutshell …

NoNo

YesYes

YesYes

© 2012 CRU International Limited confidential3

• Copper prices have slid from 2011 highs but remain well above thecost of production

• Supply remains tight, and recent decisions by mining companiesto sell or delay mining projects will keep supply tight further out

• However, the global economic picture is not rosy. Questions arebeing asked about China, in particular.

• Global consumption has seen lower than expected growth thisyear.

Copper has its strong points but it is affectedby the uncertain macro-economic situation

© 2012 CRU International Limited confidential4

Global economic news has been pretty gloomy

© 2012 CRU International Limited confidential5

Previous recessions typically lasted 36-48 months ...

Index of OECD Industrial Production

Data: OECD

80

84

88

92

96

100

104

-6 -4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50

Current

Mid-1970s

Early 1980s

Early 2000s

Early 1990s

months after cyclical peak

© 2012 CRU International Limited confidential6

This time around, recovery from the 2008 GFC has stalled

Index of OECD Industrial Production

Data: OECD

80

84

88

92

96

100

104

-6 -4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50

Current

Mid-1970s

Early 1980s

Early 2000s

Early 1990s

months after cyclical peak

Have another coupleof years to go ??

Have another coupleof years to go ??

© 2012 CRU International Limited confidential7

Of concern that China’s growth is decelerating..

1716

13

6

10 9

12

18

1516

141315

14 1413

12

10

0

5

10

15

20

25

Q108

Q3 Q109

Q3 Q110

Q3 Q111

Q3 Q112

Industrial Productiony-o-y % change

%

111010

7

16

1819

21

15131313

111010 98 8

0

5

10

15

20

25

Q108

Q3 Q109

Q3 Q110

Q3 Q111

Q3 Q112

Constructiony-o-y % change

%

© 2012 CRU International Limited confidential8

...and this slowdown is impacting copper consumption –leading CRU to revise down its estimates for the latestquarter

Current view = <2.0MtCu in Q2 2012

Jan 2012estimate was~130Kt higher

Refined Copper Consumption in China (Mt Cu)

© 2012 CRU International Limited confidential9

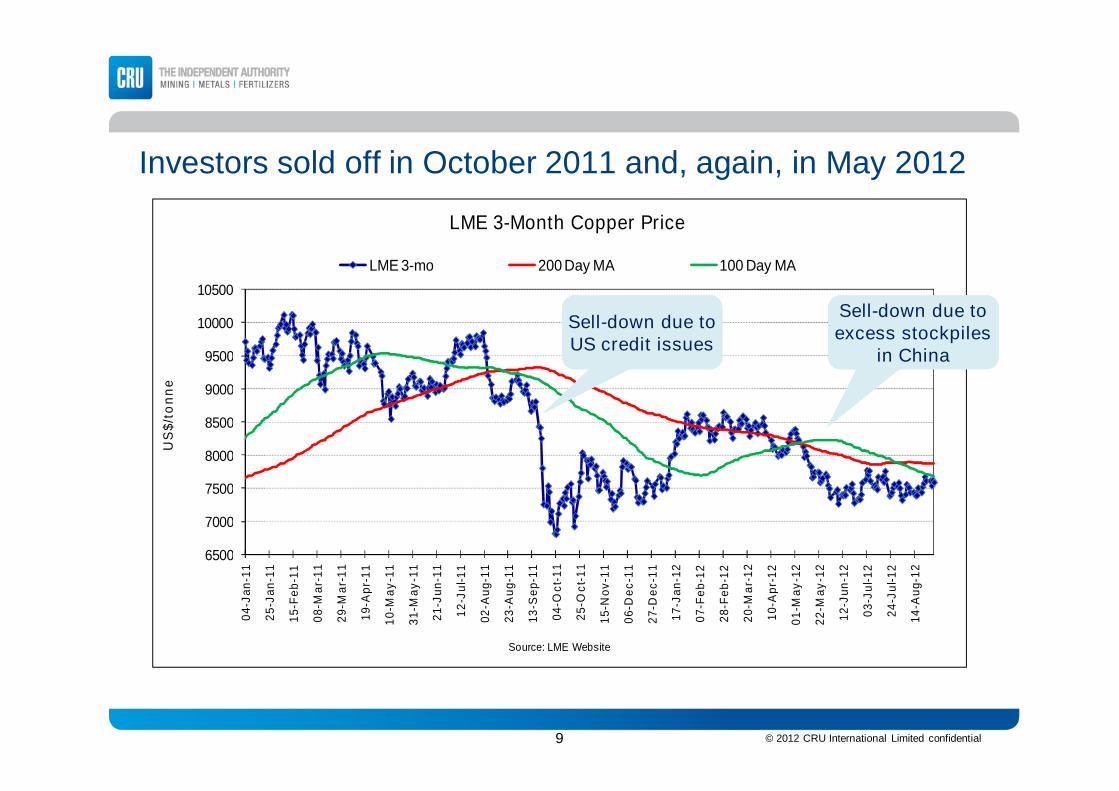

6500

7000

7500

8000

8500

9000

9500

10000

10500

04

-Ja

n-1

1

25

-Ja

n-1

1

15

-Fe

b-1

1

08

-Ma

r-1

1

29

-Ma

r-1

1

19

-Ap

r-1

1

10

-Ma

y-1

1

31

-Ma

y-1

1

21

-Ju

n-1

1

12

-Ju

l-1

1

02

-Au

g-1

1

23

-Au

g-1

1

13

-Se

p-1

1

04

-Oc

t-1

1

25

-Oc

t-1

1

15

-No

v-1

1

06

-De

c-1

1

27

-De

c-1

1

17

-Ja

n-1

2

07

-Fe

b-1

2

28

-Fe

b-1

2

20

-Ma

r-1

2

10

-Ap

r-1

2

01

-Ma

y-1

2

22

-Ma

y-1

2

12

-Ju

n-1

2

03

-Ju

l-1

2

24

-Ju

l-1

2

14

-Au

g-1

2

US

$/t

on

ne

Source: LME Website

LME 3-Month Copper Price

LME 3-mo 200 Day MA 100 Day MA

Investors sold off in October 2011 and, again, in May 2012

Sell-down due toUS credit issuesSell-down due toUS credit issues

Sell-down due toexcess stockpiles

in China

Sell-down due toexcess stockpiles

in China

© 2012 CRU International Limited confidential10

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000PriceUS$/t

Investment Factors $4,305Copper Fundamentals $5,325/t

Source: CRU Copper Price Perspective, March 2011.

SupplyDemandInventory

Shortterm

Investors

HedgeFunds

IndexFunds

TotalPrice

ChinaBalance

EnergyCurrency

Copper prices are set by cost inputs and investment demand

MARCH 2011

$9630

PhysicalETFs

$4.36 / lb

© 2012 CRU International Limited confidential11

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000 Investment Factors $1,525/tCopper Fundamentals $5,970/t

Source: CRU

PhysicalETFs

Low-growth China and the strong US dollar have causedinvestors to exit copper, and commodities in general

PriceUS$/t

$7495

AUGUST 2012

SupplyDemandInventory

Shortterm

Investors

HedgeFunds

IndexFunds

TotalPrice

ChinaBalance

EnergyCurrency

RisingCostsRisingCosts

Subdued interestby investors

Subdued interestby investors

$3.40 / lb

© 2012 CRU International Limited confidential12

As of last month, total investor influence in copper was atits lowest point since October 2009

-2000

-1000

0

1000

2000

3000

4000

5000

Jan-0

6

Apr-

06

Jul-06

Oct-

06

Jan-0

7

Apr-

07

Jul-07

Oct-

07

Jan-0

8

Apr-

08

Jul-08

Oct-

08

Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

$/t

on

ne

Investor Influence on the LME Copper Price

Long-term Investors Index Fund Investors

Short-term Speculators Physical ETFs

Investor Influence

© 2012 CRU International Limited confidential13

• Will the average copper price in 2012 be higher thanthat in 2011?

• In terms of price, is copper one of the favourednon-ferrous commodities for 2012 and beyond?

• Is the market still considered attractive for new copperprojects?

Key messages in a nutshell …

NoNo

YesYes

YesYes

© 2012 CRU International Limited confidential14

0%

0%

-1%

-6%

-10%

-10%

-12% -10% -8% -6% -4% -2% 0% 2%

Copper

Aluminium

Nickel

Lead

Tin

Zinc

Copper avoids slump seen in most other LME metals in H1

LME 3-month contracts, % change between 30th Dec 2011 and 29th Jun 2012

Data: LME

Copper traded sideways while mostother metals slid in first half of this yearCopper

© 2012 CRU International Limited confidential15

Regular CRU product coverage

Bespoke CRU product coverage

CRU covers other metals too!

Some of these are important for copper (as competitors and as co-products)

© 2012 CRU International Limited confidential16

Vanadium, Palladium, Tin,Aluminium,

Met Coke, Silver, Alumina, Uranium,

Copper, Platinum, Iron Ore, Gold,

Zinc, Lead, Manganese,

Phosphate DAP, Coking Coal,

Potash, Nickel, Cobalt

Urea, Ammonia, Sulphuric Acid,Sulphur,

CRU sees copper as “mild” in H2 2012 and “warm” in 2013

Hot> 15%

Warm5% to 15%

Cold-5% to 15%

Freezing< -15%

Mild0% to 5%

Cool0% to -5%

*2012 & 2013 annual average price forecast (nominal $or benchmark) versus 2012 Q2 average actual prices

CRU Commodity Heat for the next 18 months

Palladium, Manganese , Platinum,Silver

Uranium, Gold, Zinc, Aluminium, Met

Coke, Tin, Lead, Iron Ore, Copper,Sulphuric Acid,

Alumina, Phosphate DAP, Cobalt,Vanadium, Sulphur, Potash,

Coking Coal, Ammonia, Nickel, Urea

H2 2012 2013

Metals importantto the PhilippinesMetals importantto the Philippines

© 2012 CRU International Limited confidential17

• Will the average copper price in 2012 be higher thanthat in 2011?

• In terms of price, is copper one of the favourednon-ferrous commodities for 2012 and beyond?

• Is the market still considered attractive for new copperprojects?

Key messages in a nutshell …

NoNo

YesYes

YesYes

© 2012 CRU International Limited confidential18

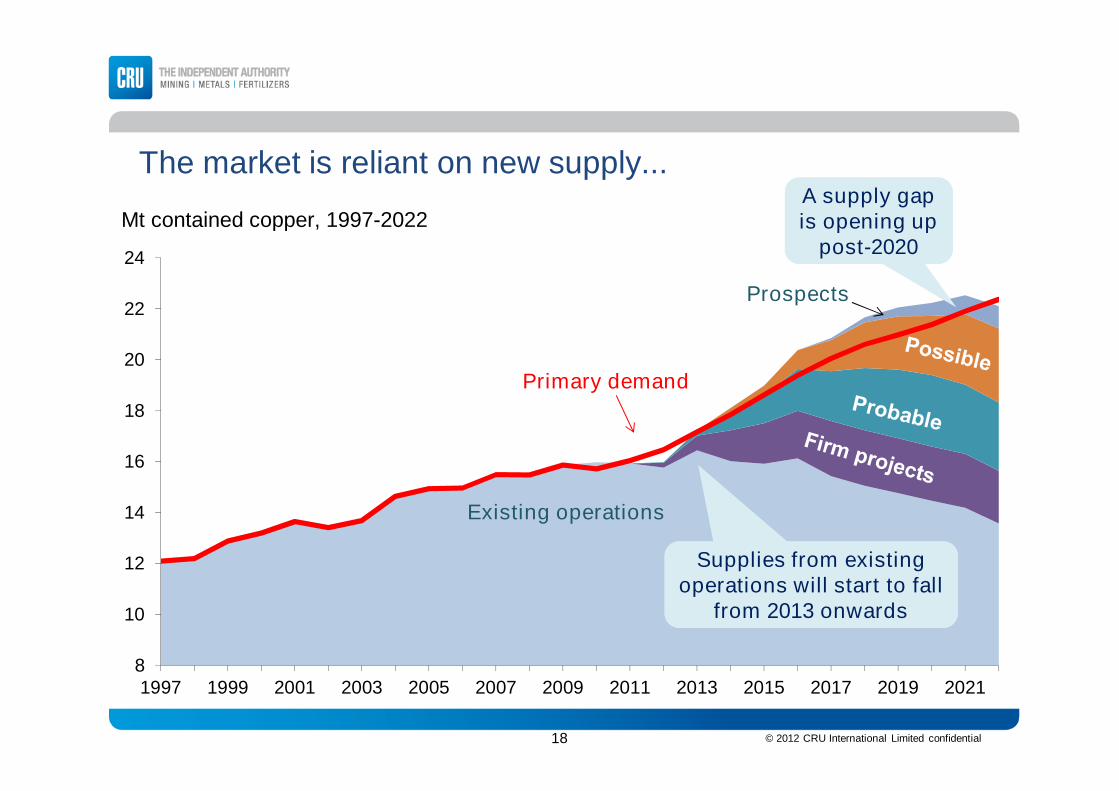

8

10

12

14

16

18

20

22

24

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

The market is reliant on new supply...

Mt contained copper, 1997-2022

Primary demand

A supply gapis opening up

post-2020

A supply gapis opening up

post-2020

Supplies from existingoperations will start to fall

from 2013 onwards

Supplies from existingoperations will start to fall

from 2013 onwards

Existing operations

Prospects

© 2012 CRU International Limited confidential19

%Cu

0.60

0.65

0.70

0.75

0.80

0.85

1997 2001 2005 2009

..but the copper industry, particularly the mining sector, hasstruggled to meet demand increases for the last decade

© 2012 CRU International Limited confidential20

Governments worldwide look to increase revenue from copperRecent changes and developments in government policy in copper mining countries

Poland: Largeroyalties increase in

March 2012

Poland: Largeroyalties increase in

March 2012

Chile: Royalties increasedin 2010; legal framework

drafted around ILO-169 inJune 2012

Chile: Royalties increasedin 2010; legal framework

drafted around ILO-169 inJune 2012

Australia: Higher Cu taxesmooted but left out of final

draft of new mining tax

Australia: Higher Cu taxesmooted but left out of final

draft of new mining tax

Zambia: Royalties doubled to 6% for 2012budget, April announcement that raw

material exports to be banned; intensepublic debate over raising mineral taxes

Zambia: Royalties doubled to 6% for 2012budget, April announcement that raw

material exports to be banned; intensepublic debate over raising mineral taxes

Peru: Royaltiesincreased in 2011Peru: Royalties

increased in 2011

Indonesia: New 20% mineral exporttax, May 2012. FCX, Newmontexempt for now, but required to

submit plans for domesticprocessing in future.

Indonesia: New 20% mineral exporttax, May 2012. FCX, Newmontexempt for now, but required to

submit plans for domesticprocessing in future.

Philippines: Mining law reviewcomplete June 2012, government

intends to increase royaltiesbefore moratorium is lifted. OPmining ban in South Cotabato.

Philippines: Mining law reviewcomplete June 2012, government

intends to increase royaltiesbefore moratorium is lifted. OPmining ban in South Cotabato.

DRC: Mining code underreview, increased taxes

planned

DRC: Mining code underreview, increased taxes

planned

© 2012 CRU International Limited confidential21

0.60

0.70

0.80

0.90

1997 1999 2001 2003 2005 2007 2009 2011

Ore grades have declined quite rapidly,constraining production

(% Cu), 1997-2011, world annual average

0.81%

0.65%

© 2012 CRU International Limited confidential22

0.0%

0.5%

1.0%

1.5%

0 100 200 300 400 500Current Resource (Mt of Cu metal)

Data: MinEx Consulting

Refers to projects at the Exploration and Feasibility Study Stages containing >500kt Cu

The average grade for the next generation of mineswill be even lower

Size and Cu grade of undeveloped open pit copper projects in the World

Weighted averagegrade is 0.45% CuWeighted averagegrade is 0.45% Cu

© 2012 CRU International Limited confidential23

750

1,250

1,750

2,250

2,750

3,250

3,750

4,250

Aitik Batu Hijau Buenavista(Concs)

Collahuasi(Concs)

Cerro Verde(Concs)

Mount Isa

-20% -10% Current +10% +20%

Lower ore grades also lead to higher operating costsEstimated change in net of by-product cash costs in 2011 when ore grades are adjustedup and down, for randomly selected mines, US$/t contained copper

US$/t

The overall impactvaries by project

due to by-product creditsand processing costs

The overall impactvaries by project

due to by-product creditsand processing costs

© 2012 CRU International Limited confidential24

Location of major copper deposits

Data: MinEx Consulting

There is a wide distribution ofcopper deposits around the world

There is a wide distribution ofcopper deposits around the world

On a per km2

basis thePhilippines iswell-endowed

On a per km2

basis thePhilippines iswell-endowed

By-ProductCopper

PrimaryCopper

50100

200

101

Mt Cu

© 2012 CRU International Limited confidential25

By-ProductCopper

PrimaryCopper

50100

200

101

Mt Cu

Data: MinEx Consulting

Location of major undeveloped copper deposits

There are 560 deposits containing 880 Mt Cupotentially available for development

There are 560 deposits containing 880 Mt Cupotentially available for development

Tampakan

Pebble

Reko Diq

Udokan

Resolution

Cobre Panama

Los SulfatosLa Granja

El Pachon

Frieda River

Top 10 undeveloped depositscontain 200 Mt Cu

Top 10 undeveloped depositscontain 200 Mt Cu

© 2012 CRU International Limited confidential26

Not all copper projects get developed as mines

0%

20%

40%

60%

80%

100%

19

50

-54

19

55

-59

19

60

-64

19

65

-69

19

70

-74

19

75

-79

19

80

-84

19

85

-89

19

90

-94

19

95

-99

20

00

-04

20

05

-09

20

10

+

Stalled

Advanced Exploration

Feasibility - New Project

Development Construction

Operating Mine

Care & Maintenance

Closed Mine

Analysis based on 384 copper deposits >0.5 Mt Cu found in the World 1950-2011

Discovery Year

~60% of copper discoverieseventually get developed.Caution: Rate varies withsize, grade and location

~60% of copper discoverieseventually get developed.Caution: Rate varies withsize, grade and location

Data: MinEx Consulting

Current status of copper deposits by discovery year

© 2012 CRU International Limited confidential27

For those projects that do get developed there is, on average,a 15 year delay between discovery and production

Discovery Year

Start-up Year 0 Years delay10 Years20 Years

11 Years

Discoveries in LowRisk Countries arequicker to develop

Discoveries in LowRisk Countries arequicker to develop

Time delay between Discovery & Mine Start-up for copper projects in the Western World

19 Years

18 Years

19 Years

Data: MinEx Consulting

In 1960s mostnew mines

were in LowRisk countries.

Today, most arein High Riskcountries.

In 1960s mostnew mines

were in LowRisk countries.

Today, most arein High Riskcountries.

1950

1960

1970

1980

1990

2000

2010

1950 1960 1970 1980 1990 2000 2010

Low

Moderate

High

Very High

© 2012 CRU International Limited confidential28

2012-18

Chile Peru North America Other S&C America Africa Asia Other

2026-322019-25

Most of the future growth will be in the AmericasLocation of new production* from 170 Tier 1 & 2 projects during each period

Mix of USbrown- andgreenfields

Mix of USbrown- andgreenfields

Total 6 years production = 23.4Mt Total production = 68.4Mt Total production = 99.2Mt

Major Chileanbrownfieldexpansion/extensions

Major Chileanbrownfieldexpansion/extensions

Asiangreenfieldsstart up

Asiangreenfieldsstart up

PeruviangreenfieldsPeruviangreenfieldsBrownfield

expansions inthe Copperbelt

Brownfieldexpansions inthe Copperbelt

*Production after estimated disruption allowance and probable contribution (dictated by project status), projects with 50Kt/y capacity or more contained Cu

© 2012 CRU International Limited confidential29

Miner Project Announcement Reason

BHP BillitonOlympic Dam

expansionDelayed Capex

Xstrata Frieda River Plans to sell stake ?

Newmont Minas Conga Suspended Local opposition

Barrick Cerro Casale Suspended Capex

Nautilus Minerals Solwara-1 Delay risk Government dispute

However, the same factors constraining supply, and thereforesupporting prices, make project development a risky businessCu miners that have announced project delays, delay risks or withdrawal plans in the last year

© 2012 CRU International Limited confidential30

Conclusions …1/3

The average copper price in 2012 will be lower than 2011

• Uncertainty around the banking and sovereign debt crises in Europeare a significant constraint to economic growth everwhere.

• The recent bounce in China’s economy is in jeopardy due to weakexternal demand.

• Prices have been range-bound since May and investor impact hasbeen relatively limited.

– Investor buying in “commodities” requires a weaker US dollar and aglobal economic recovery.

– Copper-specific buying requires that deficit conditions are a nearcertainty for at least one year.

© 2012 CRU International Limited confidential31

Conclusions … 2/3

In the medium-term copper prices will be favourable

• Copper projects continue to be an attractive investment sector becausethe industry struggles to keep up with demand. Despite a near-termwave of new supply coming in from 2013, new deficits are likely to occurin the medium to long term.

• This is caused by lengthy development times and numerous disruptivefactors to mining.

© 2012 CRU International Limited confidential32

Conclusions … 3/3

In the longer term, there is strong demand for new copper projects.As always, the challenge will be how to manage the business risks

• Ore grades are declining, constraining production and raising costs.

• Only 60% of all copper discoveries get developed as mines.

• The time delay between discovery and development is likely to increase(beyond the current 15 years).

• Increasing percentage of projects located in riskier parts of the world.

• “Resource nationalism” is becoming a major risk.

• However, we have to note that the problems that harm a given projectactually help support copper prices for the others !

So … will the Philippines be part of the problem or part of the solution?

© 2012 CRU International Limited confidential33

THANK YOU

Richard SchoddeMelbourne

Tel: +61 418 909 769Email: [email protected]

Philip SewellSydney

Tel: +61 418 290 342Email: [email protected]

LONDON | SEATTLE | PHILADELPHIA | BEIJING | SYDNEY | SANTIAGO | RIO DE JANEIRO| MUMBAI