passive activity loss rules: strategies for pass...

TRANSCRIPT

Passive Activity Loss Rules:

Strategies for Pass-Throughs Leveraging Latest Federal Guidance and Rulings to Establish Material Participation

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, FEBRUARY 28, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Robert S. Barnett, Partner, Capell Barnett Matalon & Schoenfeld, Jericho, N.Y.

Carolyn Turnbull, Tax Director, McGladrey, Orlando, Fla.

Bryan Rimmke, Tax Manager, Ernst & Young, Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Tips for Optimal Quality

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Continuing Education Credits

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Passive Activity Loss Rules: Strategies for Pass-Throughs Seminar

Robert Barnett, Capell Barnett Matalon &

Feb. 28, 2013

Bryan Rimmke, Ernst & Young

Carolyn Turnbull, McGladrey

Schoenfeld

Today’s Program

Overview Of Key Passive Activity Loss Concepts

[Bryan Rimmke]

General Problems Related To Grouping

[Bryan Rimmke]

Issues With The Real Estate Professional Designation

[Robert Barnett]

Issues Arising With The New 3.8% Tax

[Carolyn Turnbull]

Slide 64 – Slide 89

Slide 8 - Slide 22

Slide 23 – Slide 35

Slide 36 – Slide 63

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

7

OVERVIEW OF KEY PASSIVE ACTIVITY LOSS CONCEPTS

Bryan Rimmke, Ernst & Young

Passive Activity Limitations Slide 9

Circular 230

► Any U.S. tax advice contained herein was not intended or written to

be used, and cannot be used, for the purpose of avoiding penalties

that may be imposed under the Internal Revenue Code or applicable

state or local tax law provisions.

► These slides are for educational purposes only and are not intended,

and should not be relied upon, as accounting advice.

Passive Activity Limitations Slide 10

Objectives For This Section

► Define passive activity

► Apply the material participation rules

► Identify activity groupings

Basic Rules And Concepts

Passive Activity Limitations Slide 12

Taxpayers Subject To Passive Activity Limitations

► The passive activity limitations apply to:

► Individuals (including partners and S corporation shareholders)

► Estates and trusts

► Closely held C corporations

► Personal service corporations

► The passive activity limitations do not apply to:

► Partnerships and S corporations

► C corporations that are not closely held or personal service

corporations

Passive Activity Limitations Slide 13

Passive Activity

► A passive activity includes:

► A trade or business activity in which the taxpayer does not

materially participate, and

► Any rental activity except

► Certain rental real estate activities of a qualifying real estate

professional

Passive Activity Limitations Slide 14

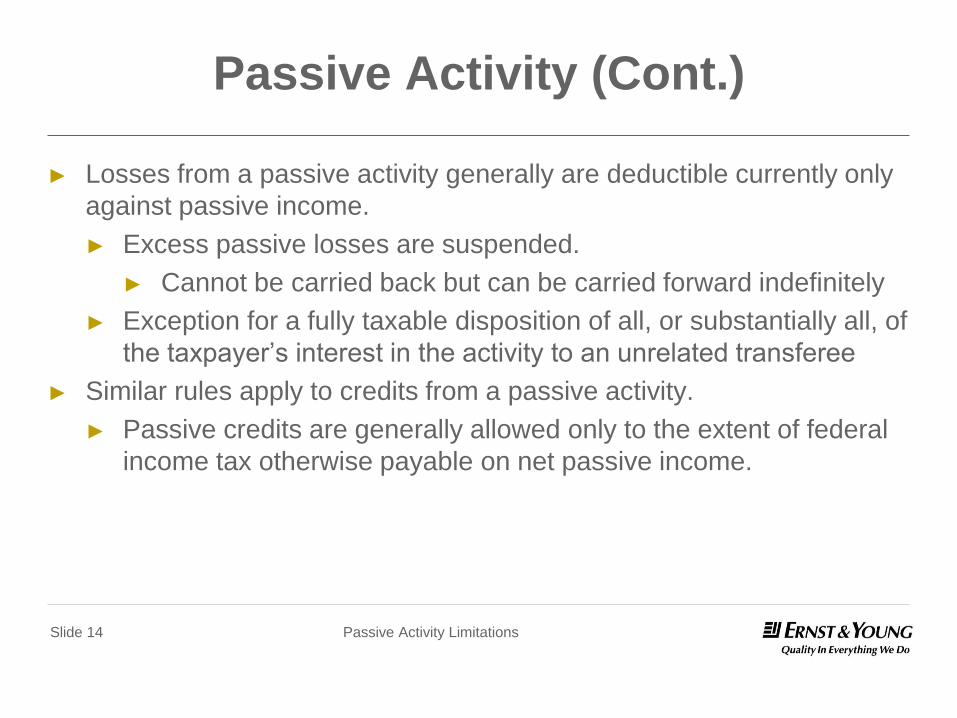

Passive Activity (Cont.)

► Losses from a passive activity generally are deductible currently only

against passive income.

► Excess passive losses are suspended.

► Cannot be carried back but can be carried forward indefinitely

► Exception for a fully taxable disposition of all, or substantially all, of

the taxpayer’s interest in the activity to an unrelated transferee

► Similar rules apply to credits from a passive activity.

► Passive credits are generally allowed only to the extent of federal

income tax otherwise payable on net passive income.

Passive Activity Limitations Slide 15

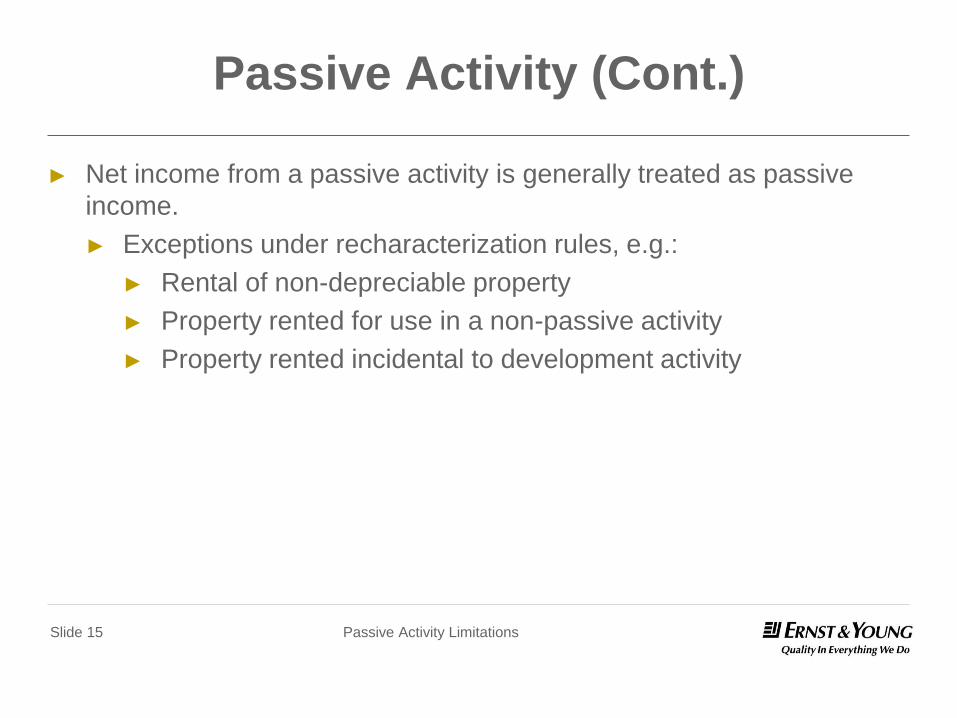

Passive Activity (Cont.)

► Net income from a passive activity is generally treated as passive

income.

► Exceptions under recharacterization rules, e.g.:

► Rental of non-depreciable property

► Property rented for use in a non-passive activity

► Property rented incidental to development activity

Passive Activity Limitations Slide 16

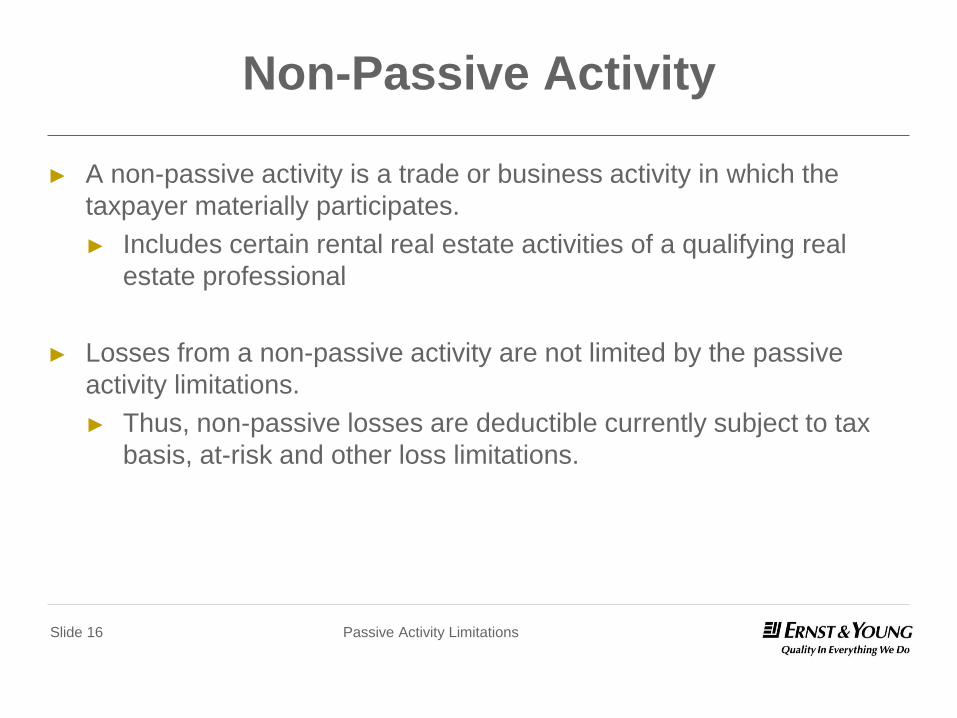

Non-Passive Activity

► A non-passive activity is a trade or business activity in which the

taxpayer materially participates.

► Includes certain rental real estate activities of a qualifying real

estate professional

► Losses from a non-passive activity are not limited by the passive

activity limitations.

► Thus, non-passive losses are deductible currently subject to tax

basis, at-risk and other loss limitations.

Passive Activity Limitations Slide 17

Non-Passive Activity (Cont.)

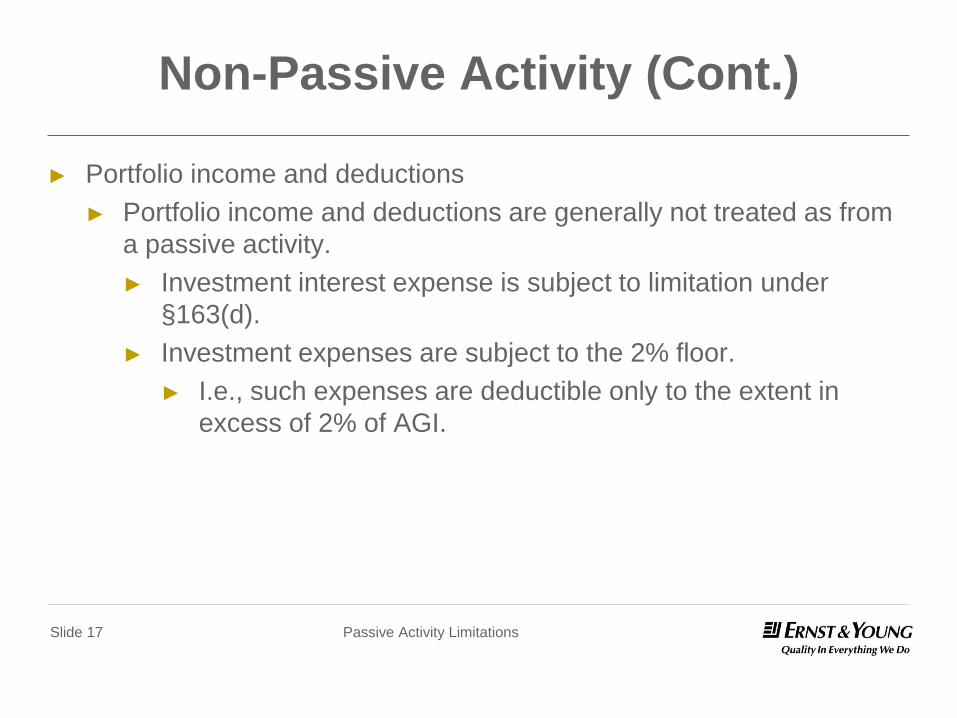

► Portfolio income and deductions

► Portfolio income and deductions are generally not treated as from

a passive activity.

► Investment interest expense is subject to limitation under

§163(d).

► Investment expenses are subject to the 2% floor.

► I.e., such expenses are deductible only to the extent in

excess of 2% of AGI.

Material Participation

Passive Activity Limitations Slide 19

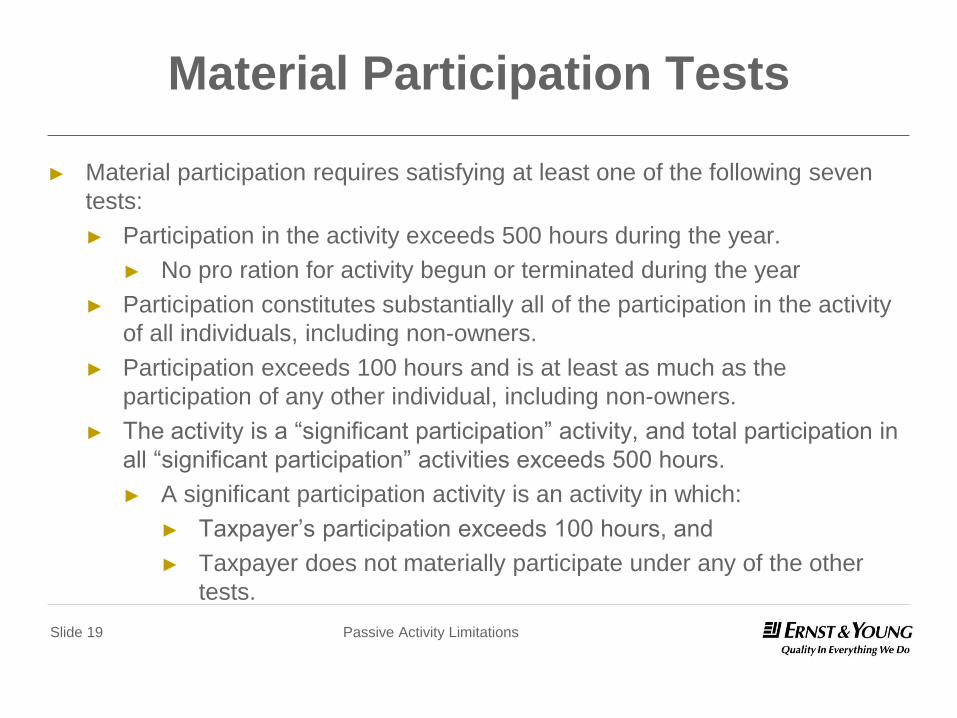

Material Participation Tests

► Material participation requires satisfying at least one of the following seven

tests:

► Participation in the activity exceeds 500 hours during the year.

► No pro ration for activity begun or terminated during the year

► Participation constitutes substantially all of the participation in the activity

of all individuals, including non-owners.

► Participation exceeds 100 hours and is at least as much as the

participation of any other individual, including non-owners.

► The activity is a “significant participation” activity, and total participation in

all “significant participation” activities exceeds 500 hours.

► A significant participation activity is an activity in which:

► Taxpayer’s participation exceeds 100 hours, and

► Taxpayer does not materially participate under any of the other

tests.

Passive Activity Limitations Slide 20

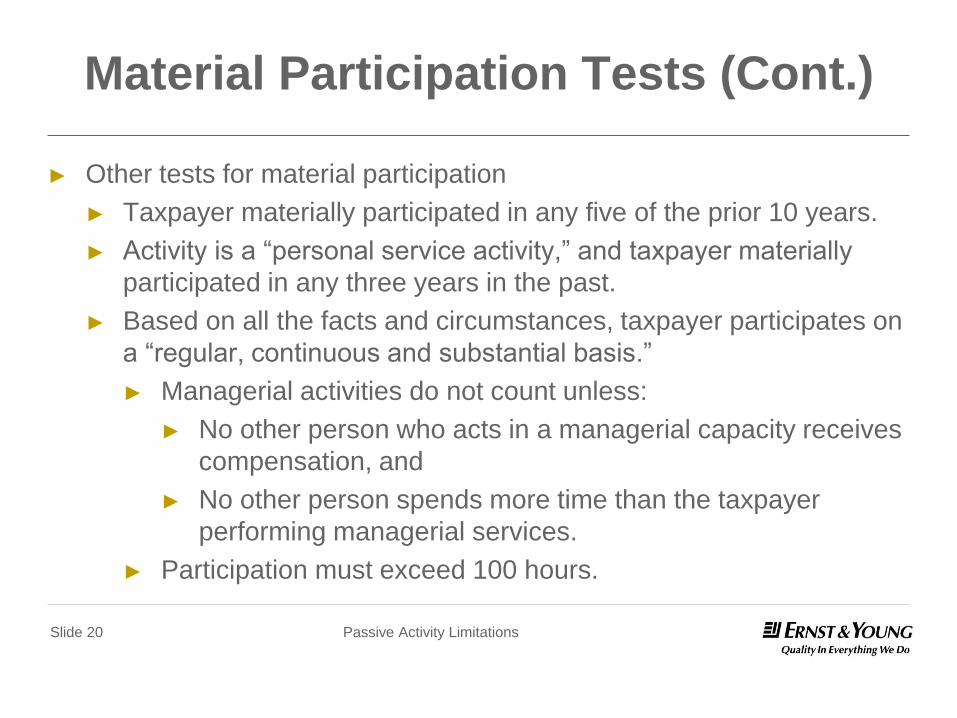

Material Participation Tests (Cont.)

► Other tests for material participation

► Taxpayer materially participated in any five of the prior 10 years.

► Activity is a “personal service activity,” and taxpayer materially

participated in any three years in the past.

► Based on all the facts and circumstances, taxpayer participates on

a “regular, continuous and substantial basis.”

► Managerial activities do not count unless:

► No other person who acts in a managerial capacity receives

compensation, and

► No other person spends more time than the taxpayer

performing managerial services.

► Participation must exceed 100 hours.

Passive Activity Limitations Slide 21

Material Participation Of Limited Partners

► Limited partners may achieve material participation only under the

following three of the seven tests:

► Participation of more than 500 hours

► Material participation in any five of prior 10 years

► Material participation in a personal service activity in any three

prior years

► LLC members – not addressed in regulations

► Case law favorable in not treating LLC members as limited

partners

► Court decisions in Gregg, Garnett, Thompson, Newell

► Proposed regulations look to rights to participate in management.

Passive Activity Limitations Slide 22

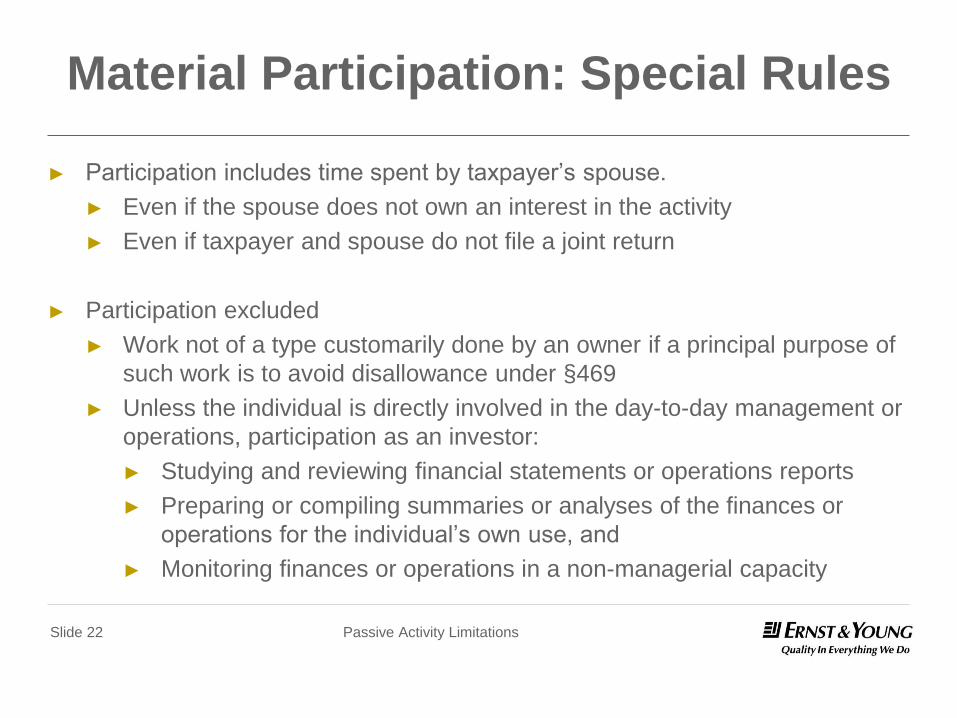

Material Participation: Special Rules

► Participation includes time spent by taxpayer’s spouse.

► Even if the spouse does not own an interest in the activity

► Even if taxpayer and spouse do not file a joint return

► Participation excluded

► Work not of a type customarily done by an owner if a principal purpose of

such work is to avoid disallowance under §469

► Unless the individual is directly involved in the day-to-day management or

operations, participation as an investor:

► Studying and reviewing financial statements or operations reports

► Preparing or compiling summaries or analyses of the finances or

operations for the individual’s own use, and

► Monitoring finances or operations in a non-managerial capacity

GENERAL PROBLEMS RELATED TO GROUPING

Bryan Rimmke, Ernst & Young

Activity Grouping

Passive Activity Limitations Slide 25

Grouping Activities

► Material participation is tested at the activity level.

► Can include activities conducted through partnerships and S

corporations, closely held and personal service C corporations

► Activity can be a trade or business activity or rental activity.

► A “trade or business activity” is an activity:

► Other than a rental activity

► Not incidental to an activity of holding property for investment, and

► Either:

► Involves the conduct of a trade or business under §162,

► Is conducted in anticipation of commencing a trade or business, or

► Involves research or experimental expenditures that are or would

be deductible under §174

Slide Intentionally Left Blank

Passive Activity Limitations Slide 27

Grouping Activities (Cont.)

► Taxpayers may aggregate multiple activities into a single activity or

fragment a single activity into multiple activities.

► Activity grouping must be an “appropriate economic unit.”

► Based on the facts and circumstances

► Regulations list five factors:

► Similarities and differences in types of trades or businesses

► Extent of common control

► Extent of common ownership

► Geographical location

► Inter-dependencies between or among the activities

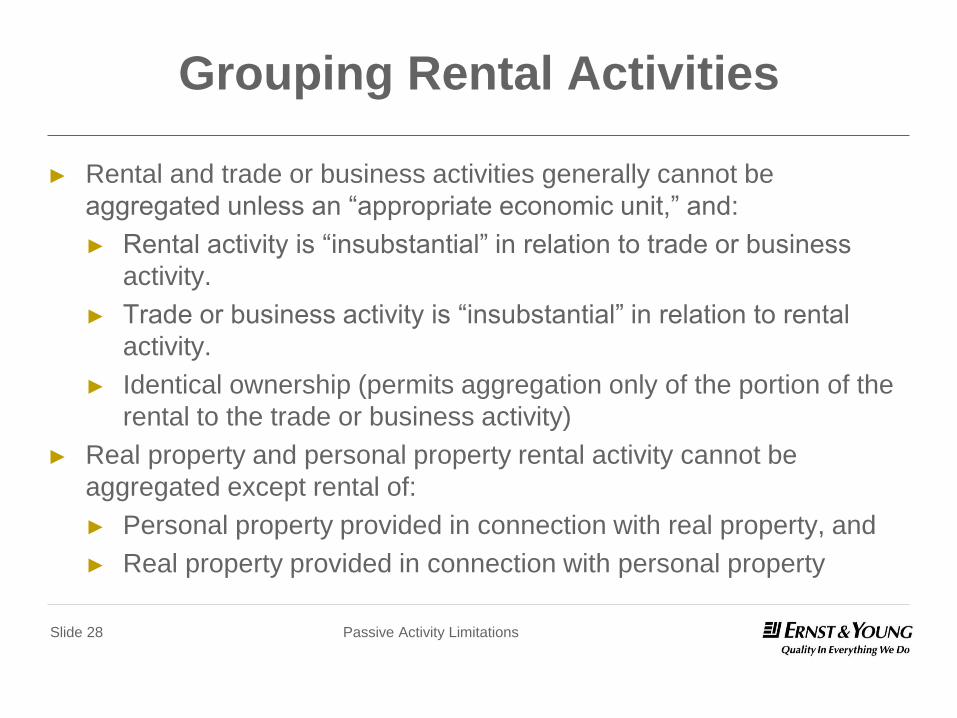

Passive Activity Limitations Slide 28

Grouping Rental Activities

► Rental and trade or business activities generally cannot be

aggregated unless an “appropriate economic unit,” and:

► Rental activity is “insubstantial” in relation to trade or business

activity.

► Trade or business activity is “insubstantial” in relation to rental

activity.

► Identical ownership (permits aggregation only of the portion of the

rental to the trade or business activity)

► Real property and personal property rental activity cannot be

aggregated except rental of:

► Personal property provided in connection with real property, and

► Real property provided in connection with personal property

Passive Activity Limitations Slide 29

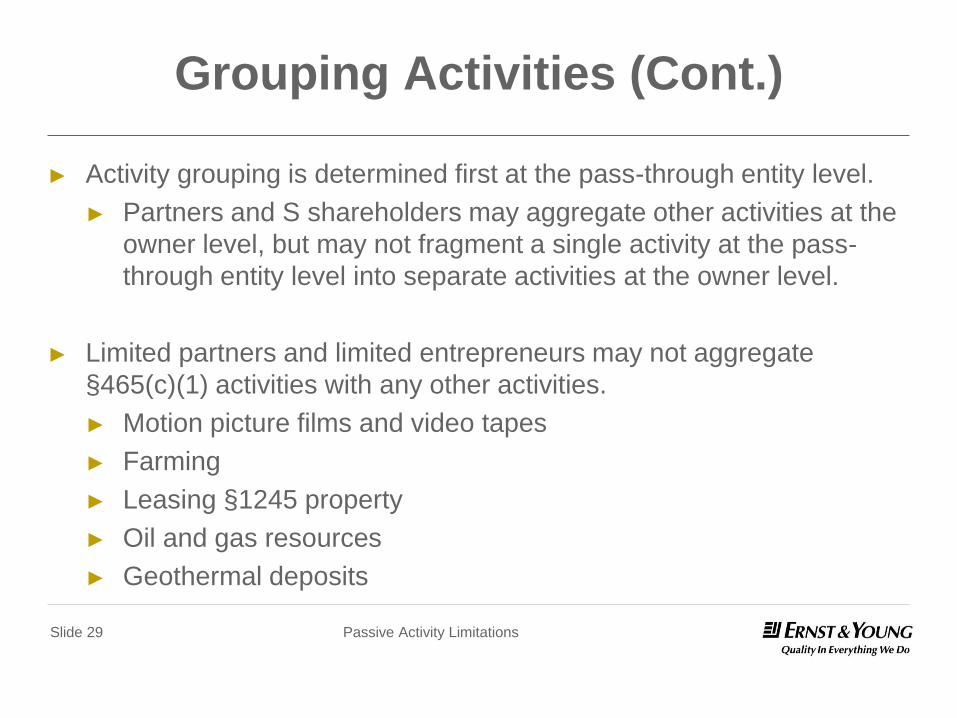

Grouping Activities (Cont.)

► Activity grouping is determined first at the pass-through entity level.

► Partners and S shareholders may aggregate other activities at the

owner level, but may not fragment a single activity at the pass-

through entity level into separate activities at the owner level.

► Limited partners and limited entrepreneurs may not aggregate

§465(c)(1) activities with any other activities.

► Motion picture films and video tapes

► Farming

► Leasing §1245 property

► Oil and gas resources

► Geothermal deposits

Passive Activity Limitations Slide 30

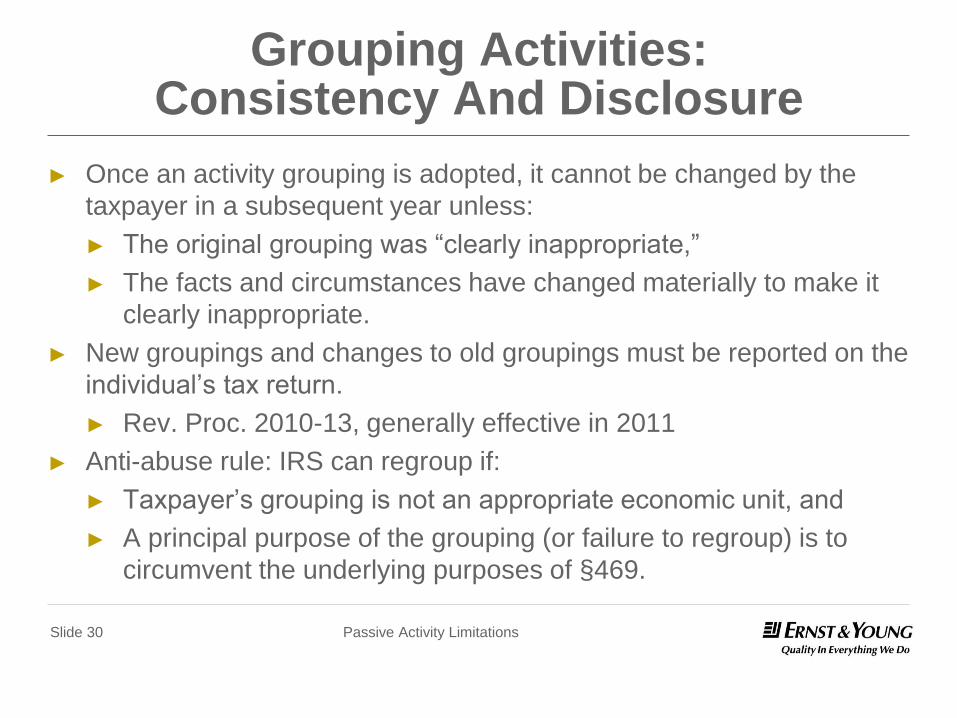

Grouping Activities: Consistency And Disclosure

► Once an activity grouping is adopted, it cannot be changed by the

taxpayer in a subsequent year unless:

► The original grouping was “clearly inappropriate,”

► The facts and circumstances have changed materially to make it

clearly inappropriate.

► New groupings and changes to old groupings must be reported on the

individual’s tax return.

► Rev. Proc. 2010-13, generally effective in 2011

► Anti-abuse rule: IRS can regroup if:

► Taxpayer’s grouping is not an appropriate economic unit, and

► A principal purpose of the grouping (or failure to regroup) is to

circumvent the underlying purposes of §469.

Passive Activity Limitations Slide 31

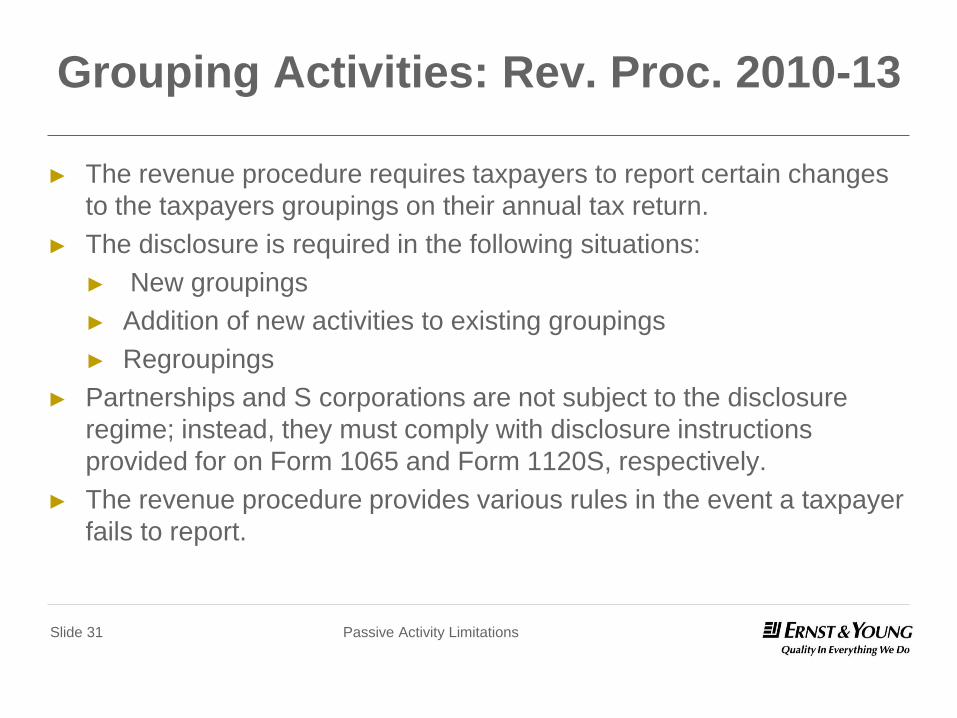

Grouping Activities: Rev. Proc. 2010-13

► The revenue procedure requires taxpayers to report certain changes

to the taxpayers groupings on their annual tax return.

► The disclosure is required in the following situations:

► New groupings

► Addition of new activities to existing groupings

► Regroupings

► Partnerships and S corporations are not subject to the disclosure

regime; instead, they must comply with disclosure instructions

provided for on Form 1065 and Form 1120S, respectively.

► The revenue procedure provides various rules in the event a taxpayer

fails to report.

Planning

Passive Activity Limitations Slide 33

Planning

► Material participation and non-passive treatment are not always

beneficial.

► Passive treatment is generally beneficial for activity with net

income.

► Beware recharacterization rules

► Non-passive treatment is generally beneficial for activity with net

losses.

Passive Activity Limitations Slide 34

Planning (Cont.)

► To achieve or avoid material participation, consider activity groupings that

may be permissible.

► E.g., perhaps a loss activity with no material participation can be

aggregated with another activity with material participation.

► Thus, loss activity is non-passive.

► Alternatively, perhaps a net income activity with material participation can

be fragmented into multiple activities with no material participation.

► Thus, net income activity is passive.

► Beware consistency rule

► Is new activity grouping precluded by prior year activity groupings?

► Will new activity grouping continue to be beneficial in future years?

Passive Activity Limitations Slide 35

► Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. For more information about our organization, please visit www.ey.com

► Ernst & Young LLP is a client-serving member firm of Ernst & Young Global operating in the U.S.

► This presentation is © 2013 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of U.S. and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are not necessarily those of Ernst & Young LLP.

Disclaimer

ISSUES WITH THE REAL ESTATE PROFESSIONAL DESIGNATION

Robert Barnett, Capell Barnett Matalon & Schoenfeld

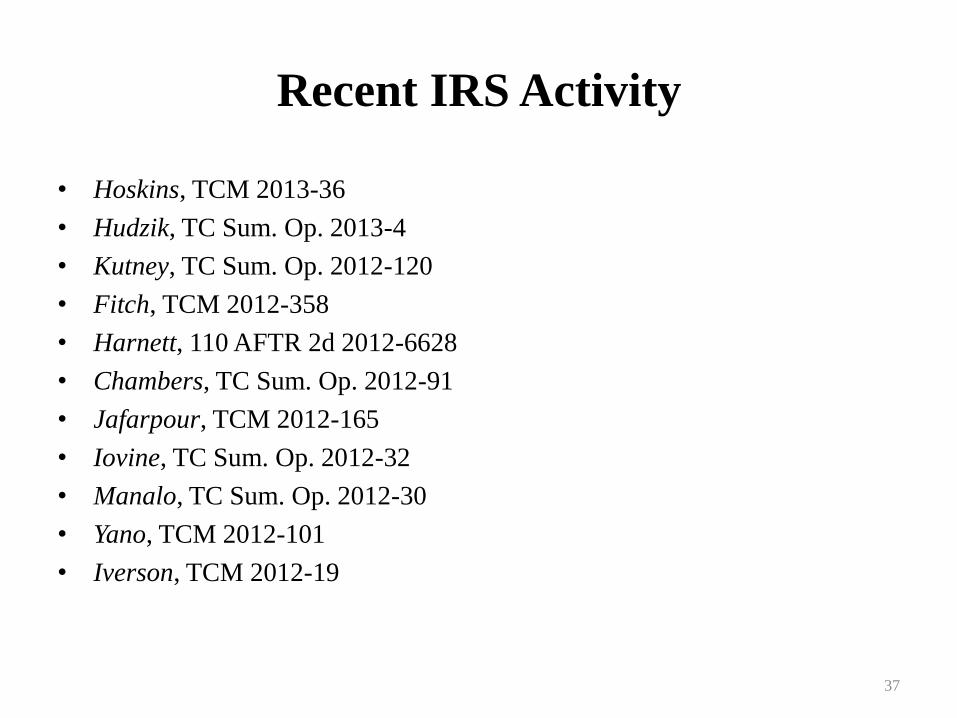

Recent IRS Activity

• Hoskins, TCM 2013-36

• Hudzik, TC Sum. Op. 2013-4

• Kutney, TC Sum. Op. 2012-120

• Fitch, TCM 2012-358

• Harnett, 110 AFTR 2d 2012-6628

• Chambers, TC Sum. Op. 2012-91

• Jafarpour, TCM 2012-165

• Iovine, TC Sum. Op. 2012-32

• Manalo, TC Sum. Op. 2012-30

• Yano, TCM 2012-101

• Iverson, TCM 2012-19

37

Slide Intentionally Left Blank

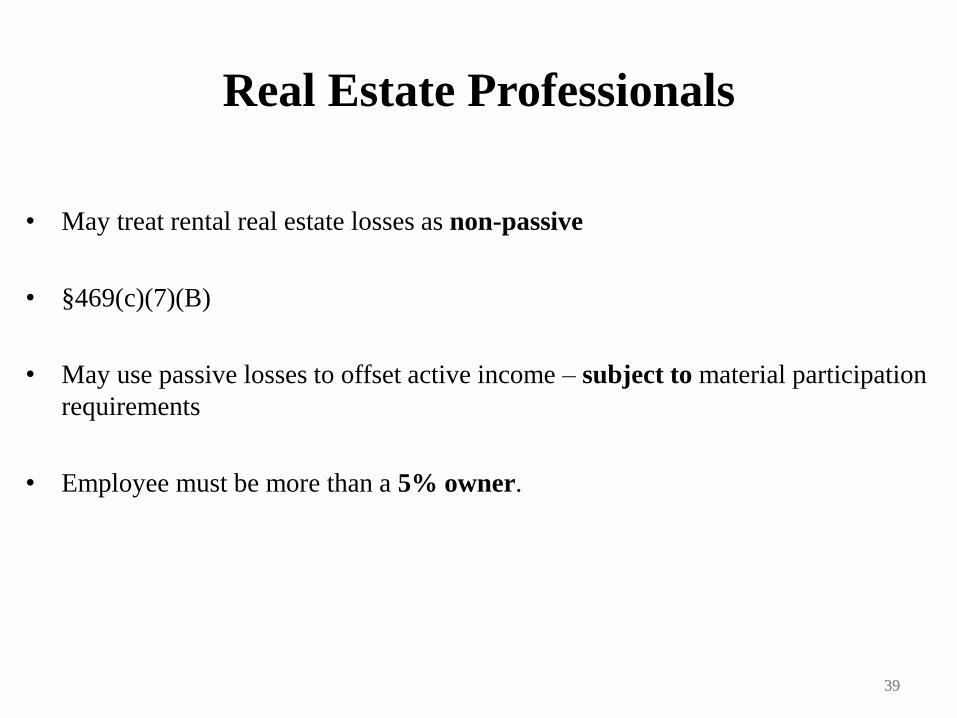

Real Estate Professionals

• May treat rental real estate losses as non-passive

• §469(c)(7)(B)

• May use passive losses to offset active income – subject to material participation

requirements

• Employee must be more than a 5% owner.

39 39

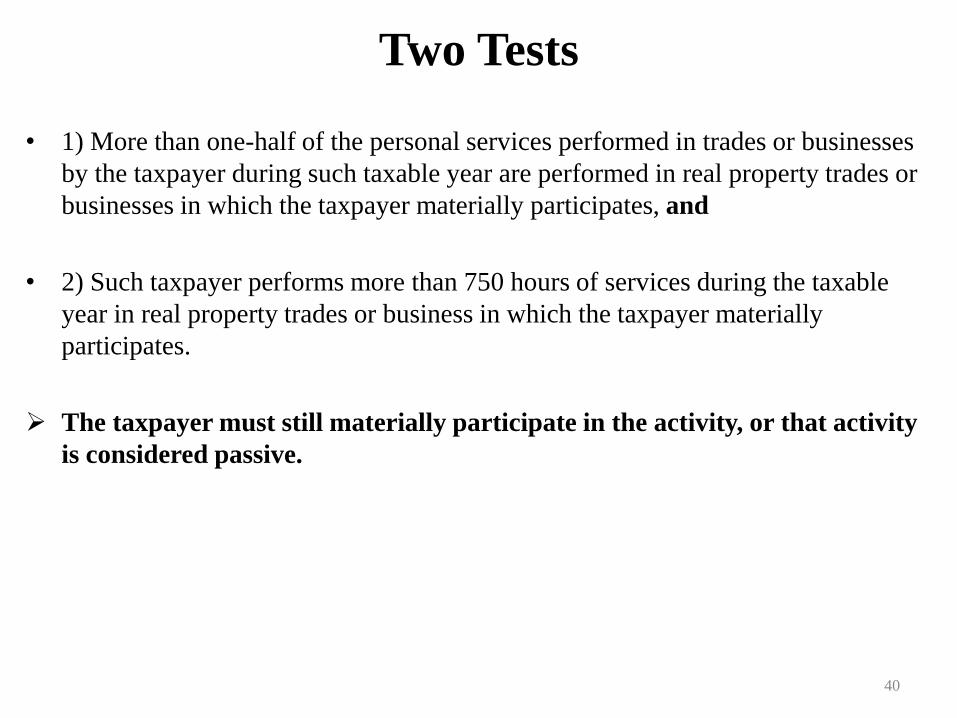

Two Tests

• 1) More than one-half of the personal services performed in trades or businesses

by the taxpayer during such taxable year are performed in real property trades or

businesses in which the taxpayer materially participates, and

• 2) Such taxpayer performs more than 750 hours of services during the taxable

year in real property trades or business in which the taxpayer materially

participates.

The taxpayer must still materially participate in the activity, or that activity

is considered passive.

40

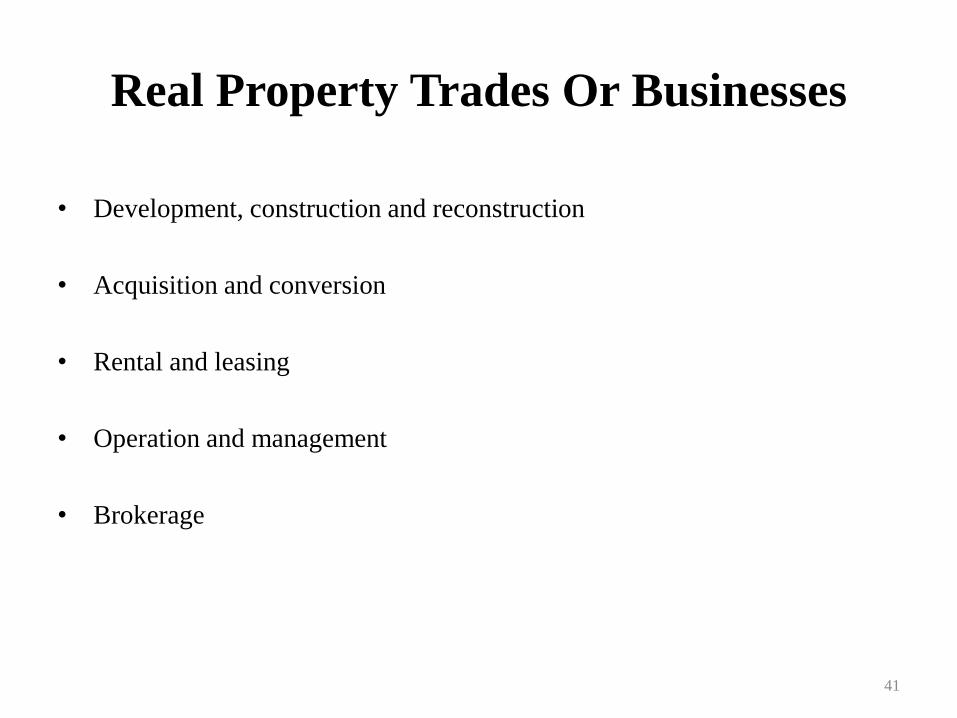

Real Property Trades Or Businesses

• Development, construction and reconstruction

• Acquisition and conversion

• Rental and leasing

• Operation and management

• Brokerage

41

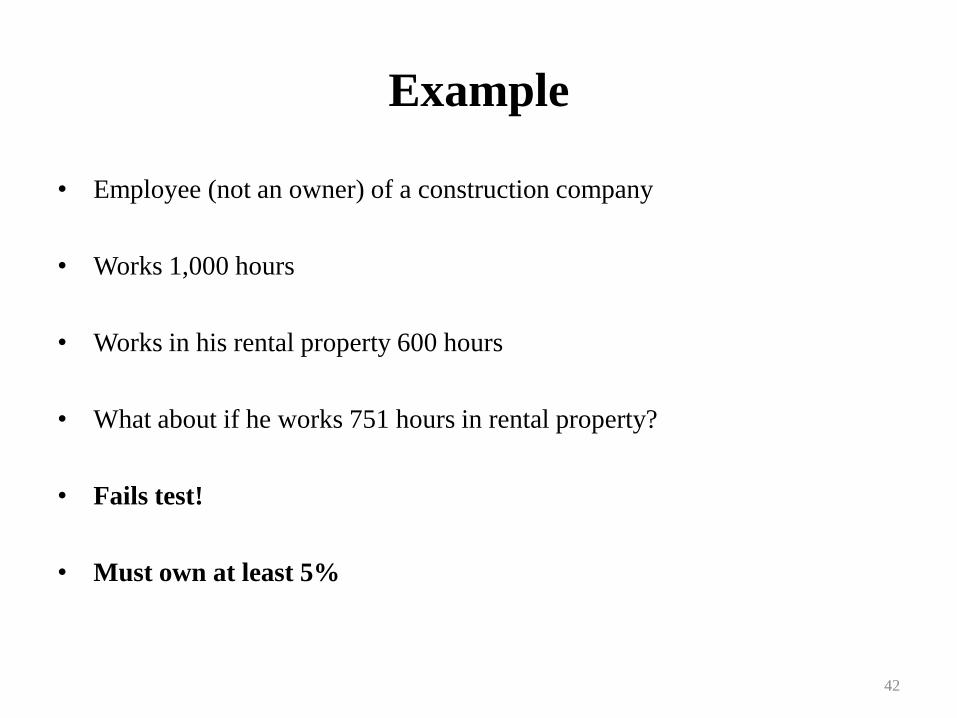

Example

• Employee (not an owner) of a construction company

• Works 1,000 hours

• Works in his rental property 600 hours

• What about if he works 751 hours in rental property?

• Fails test!

• Must own at least 5%

42

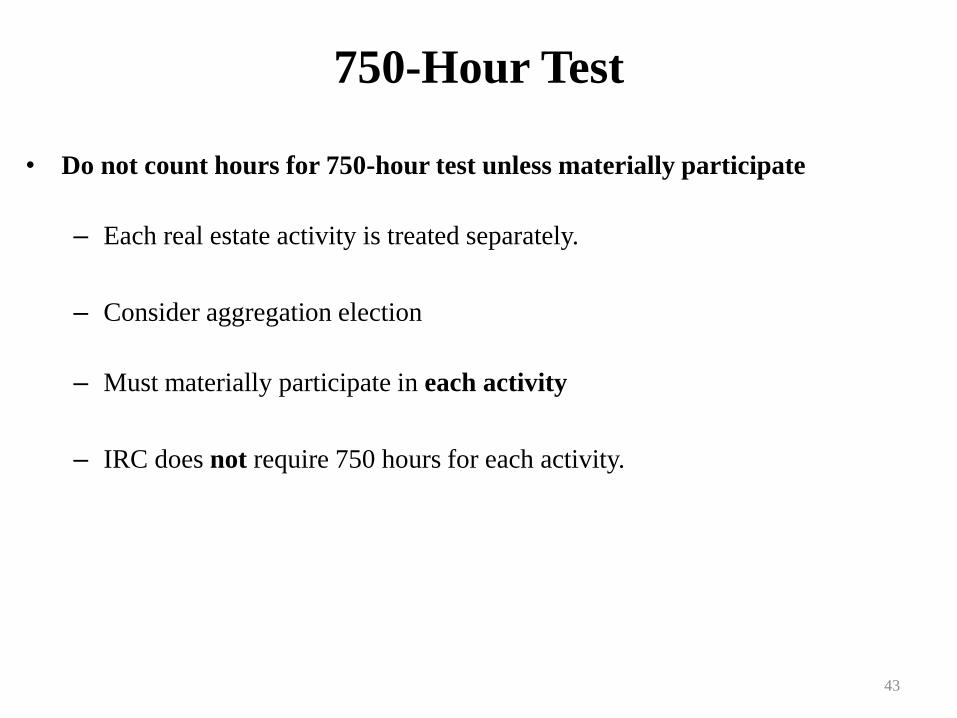

750-Hour Test

• Do not count hours for 750-hour test unless materially participate

– Each real estate activity is treated separately.

– Consider aggregation election

– Must materially participate in each activity

– IRC does not require 750 hours for each activity.

43

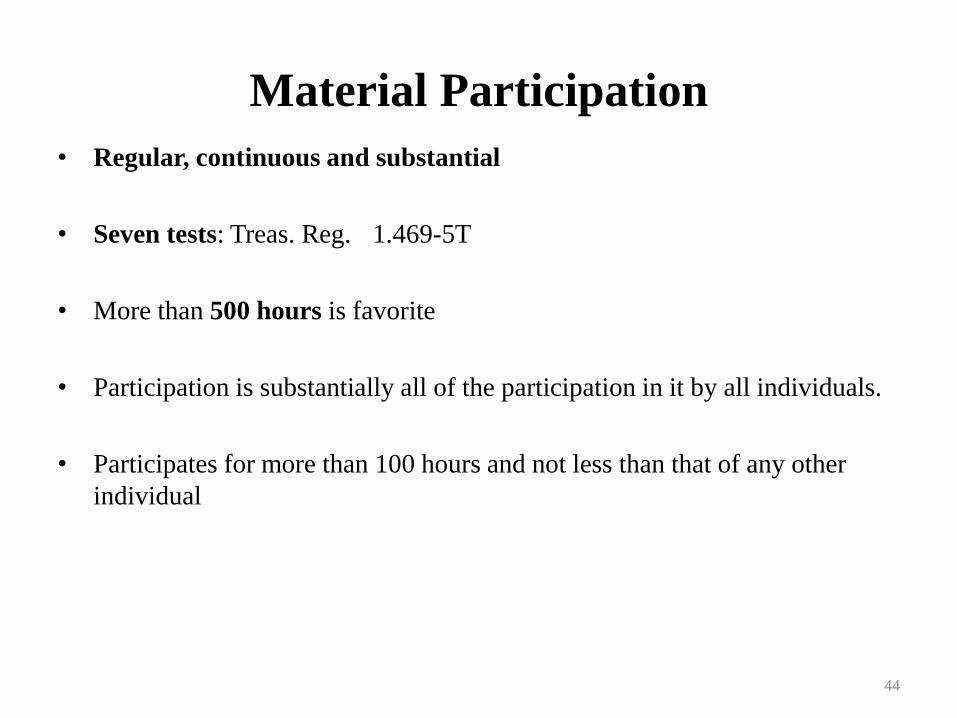

Material Participation

• Regular, continuous and substantial

• Seven tests: Treas. Reg.

1.469-5T

• More than 500 hours is favorite

• Participation is substantially all of the participation in it by all individuals.

• Participates for more than 100 hours and not less than that of any other

individual

44

How Do You Prove Participation?

• Regs – any reasonable means

• Calendars, appointment books, logs

• Contemporaneous daily logs are not required if other reasonable means exist to

establish material participation.

• Participation as an investor requires day-to-day management or operation of the

activity.

45

Married

• Can count participation by spouse to meet material participation only

• Even if do not file joint return!

46

Miller v. Commissioner TC Memo 2011-219

• Two property losses not passive in 2005 and 2006

• Four property losses were passive.

• No penalty imposed

• H worked as a tugboat pilot

47

Miller v. Commissioner (Cont.)

• H had a contractor’s license.

• Kitchen remodeling, siding, decks, fences, etc.

• Wife – leases, advertising, research, bidding

• H – contemporaneous time sheets for contracting work but not

administrative work such as planning, ordering

• H rental maintenance and repair

48

Miller v. Commissioner (Cont.)

• Burden of proof – for a deduction

• Deficiency notice presumed correct

• Burden may shift to Commissioner, if certain conditions satisfied - §7491

• Petitioner did not claim that the burden was shifted.

49

Miller v. Commissioner (Cont.)

• Prove participation – by any reasonable means

• Not “ballpark estimate”

• Look at performance of both spouses, for material participation

• H performed more than 750 hours as a contractor and on rental properties.

• H performed more time on real estate than as a tugboat pilot.

50

Miller v. Commissioner (Cont.)

• Contemporaneous work logs, but

• Failed to aggregate

• Seven tests reviewed by the court

• Reasonable cause and good faith – no penalties

51

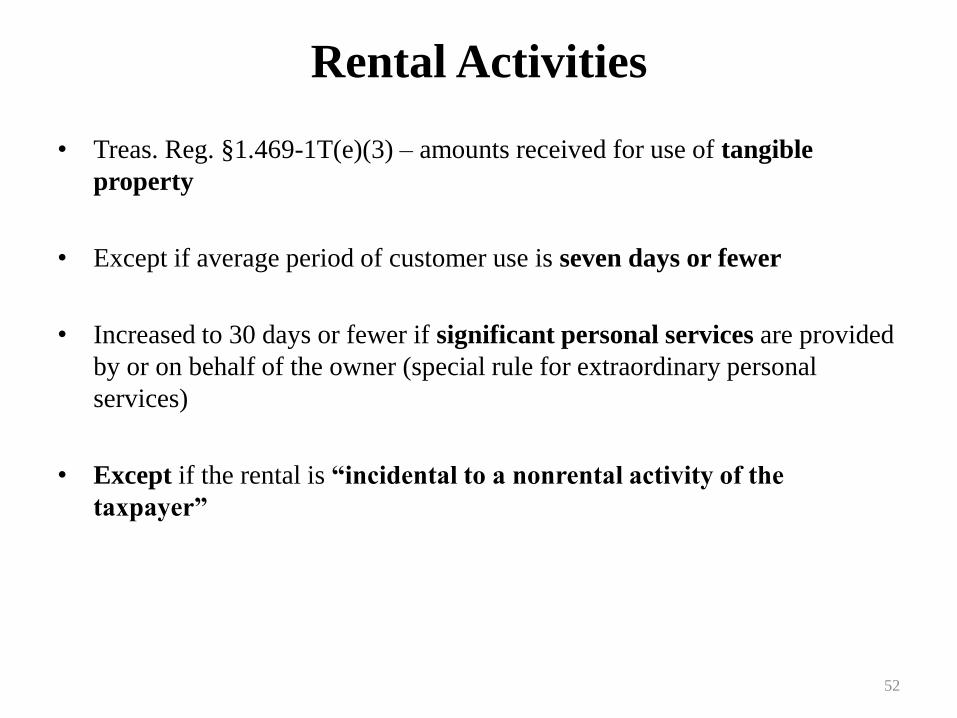

Rental Activities

• Treas. Reg. §1.469-1T(e)(3) – amounts received for use of tangible

property

• Except if average period of customer use is seven days or fewer

• Increased to 30 days or fewer if significant personal services are provided

by or on behalf of the owner (special rule for extraordinary personal

services)

• Except if the rental is “incidental to a nonrental activity of the

taxpayer”

52

Bailey v. Comm’r TC Summary Opinion 2011-22

• B&B inn having several buildings

• One property was rented for short term – average period of customer use

under 8 days

• Not counted for 750-hour test of real estate professional

53

Rev. Proc. 2011-34:

Aggregation Election

54

Separate Activity

• Each interest in rental real estate is treated as a separate activity – subject to

the material participation requirements.

• Unless aggregation election

• Treat ALL rental realty as single activity

• Election makes it easier to meet the material participation requirement.

55

Anjum Shiekh TCM 2010-126

• Taxpayer had several rental properties.

• Claimed he was a real estate professional

• Required material participation for each activity

• IRS said he failed the material participation test for one property.

• Failed to present evidence of hours worked - use contemporaneous log

56

Schedule E

• Is not sufficient to constitute aggregation

• Need formal election and notice

• Net leases more troublesome

57

To Elect Or Not To Elect

• Do not make if have passive income from real estate and passive losses

from other activities, because you want to keep the income passive

• Do not include property to be sold

58

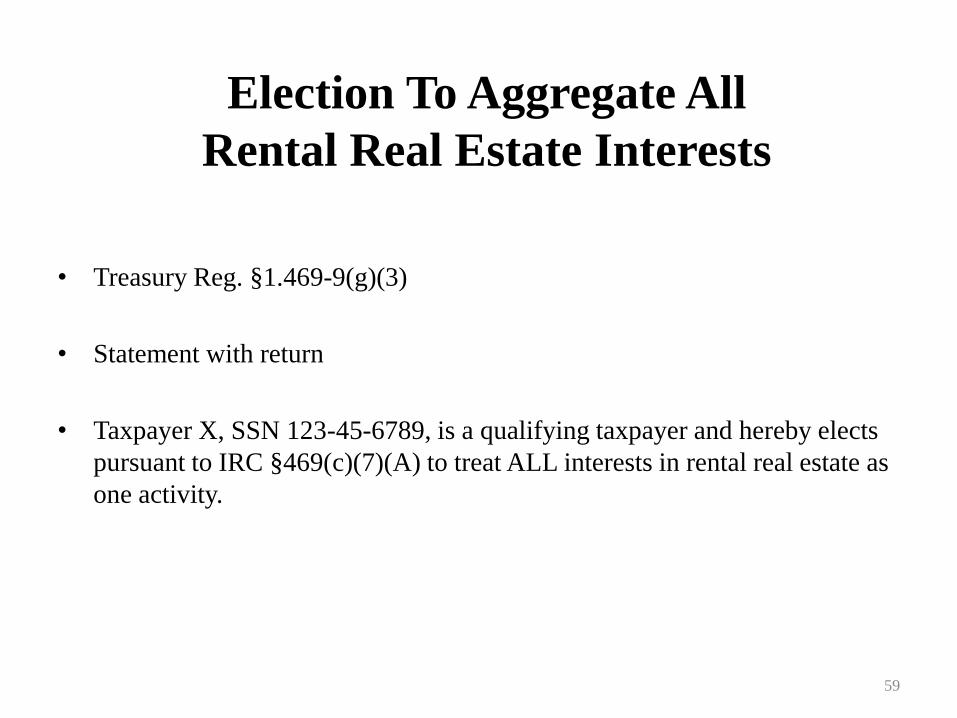

Election To Aggregate All

Rental Real Estate Interests

• Treasury Reg. §1.469-9(g)(3)

• Statement with return

• Taxpayer X, SSN 123-45-6789, is a qualifying taxpayer and hereby elects

pursuant to IRC §469(c)(7)(A) to treat ALL interests in rental real estate as

one activity.

59

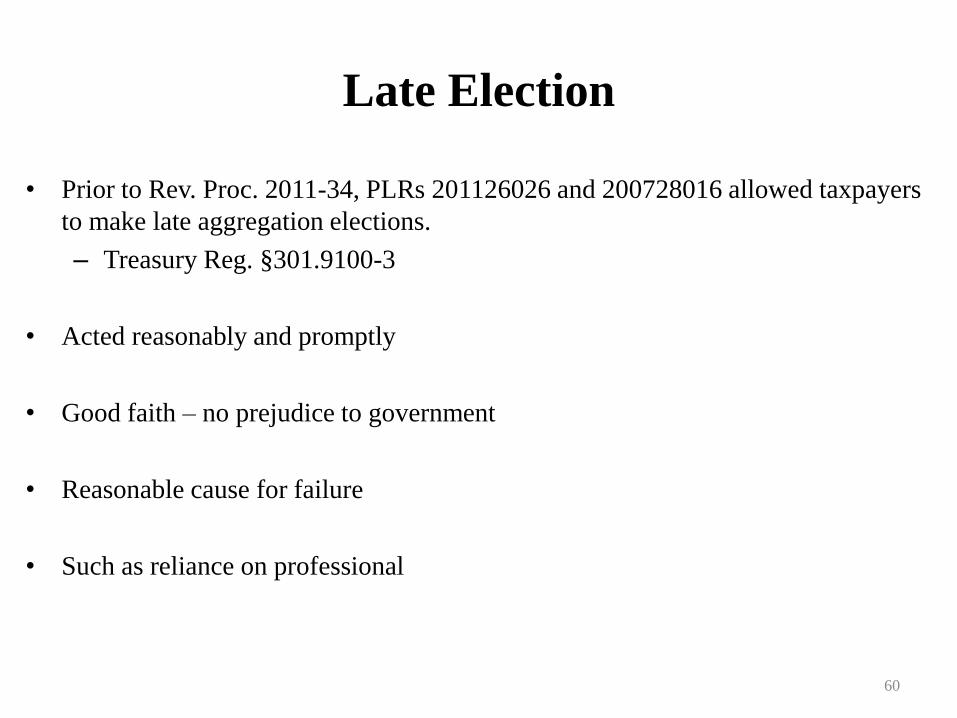

Late Election

• Prior to Rev. Proc. 2011-34, PLRs 201126026 and 200728016 allowed taxpayers

to make late aggregation elections.

– Treasury Reg. §301.9100-3

• Acted reasonably and promptly

• Good faith – no prejudice to government

• Reasonable cause for failure

• Such as reliance on professional

60

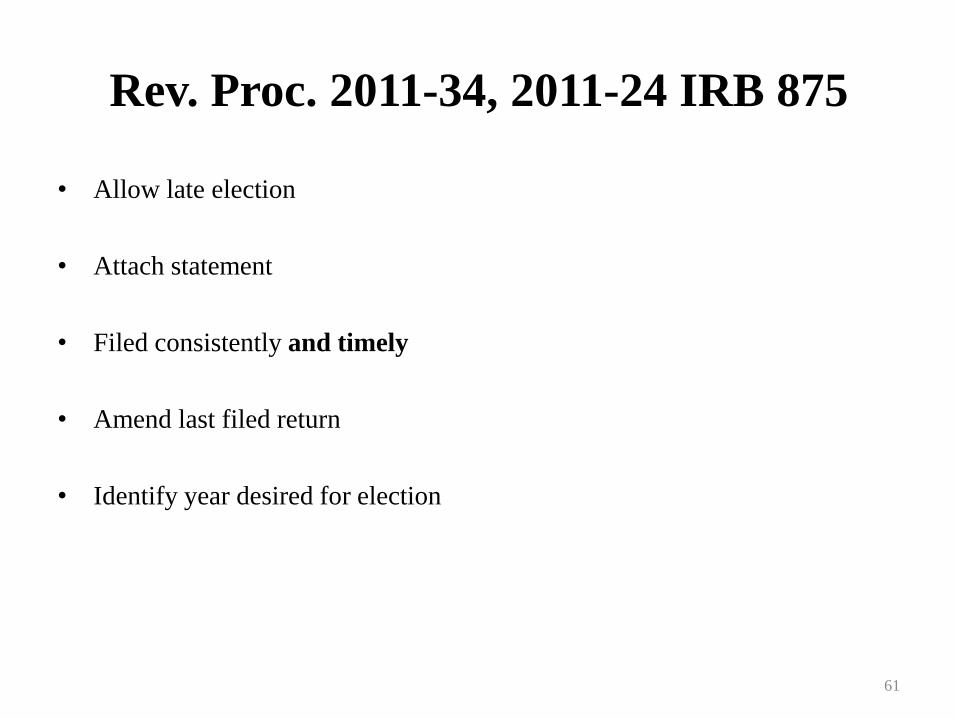

Rev. Proc. 2011-34, 2011-24 IRB 875

• Allow late election

• Attach statement

• Filed consistently and timely

• Amend last filed return

• Identify year desired for election

61

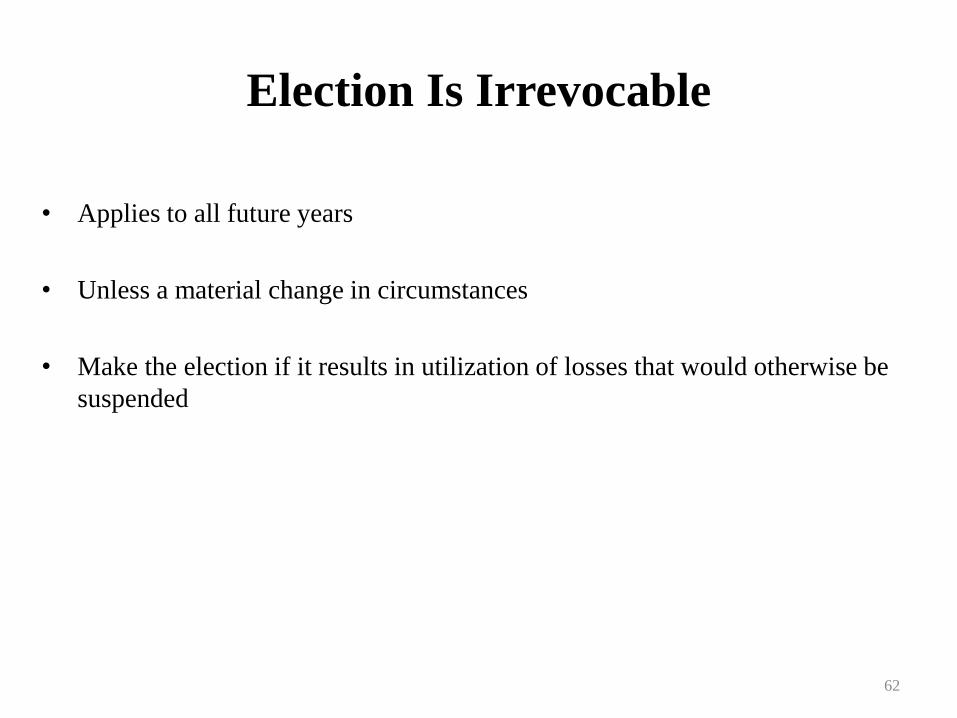

Election Is Irrevocable

• Applies to all future years

• Unless a material change in circumstances

• Make the election if it results in utilization of losses that would otherwise be

suspended

62

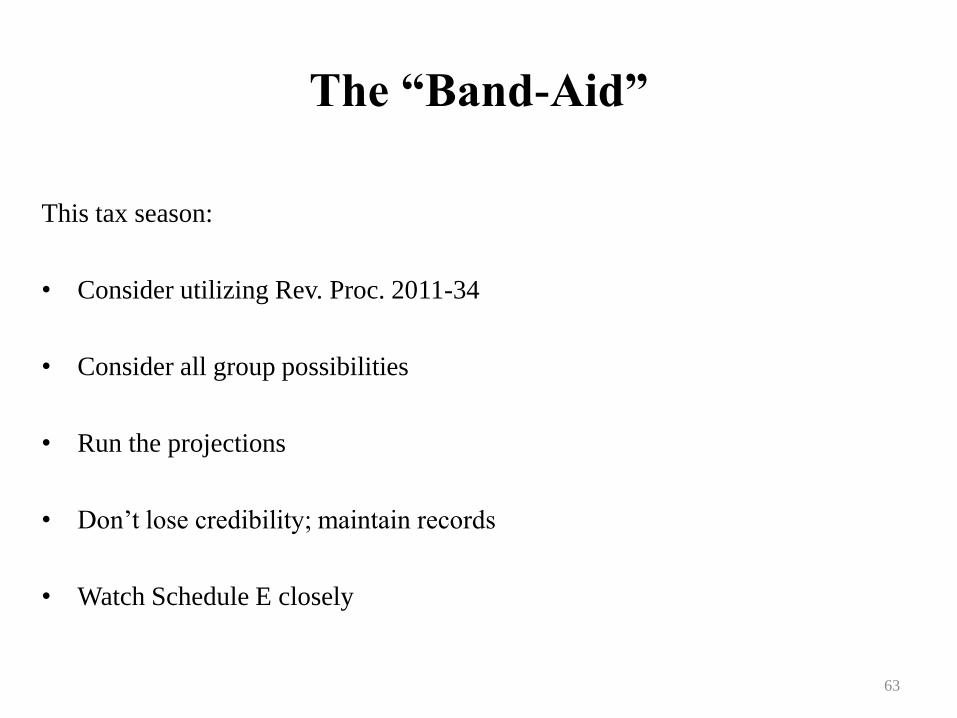

The “Band-Aid”

This tax season:

• Consider utilizing Rev. Proc. 2011-34

• Consider all group possibilities

• Run the projections

• Don’t lose credibility; maintain records

• Watch Schedule E closely

63

ISSUES ARISING WITH THE NEW 3.8% TAX

Carolyn Turnbull, McGladrey

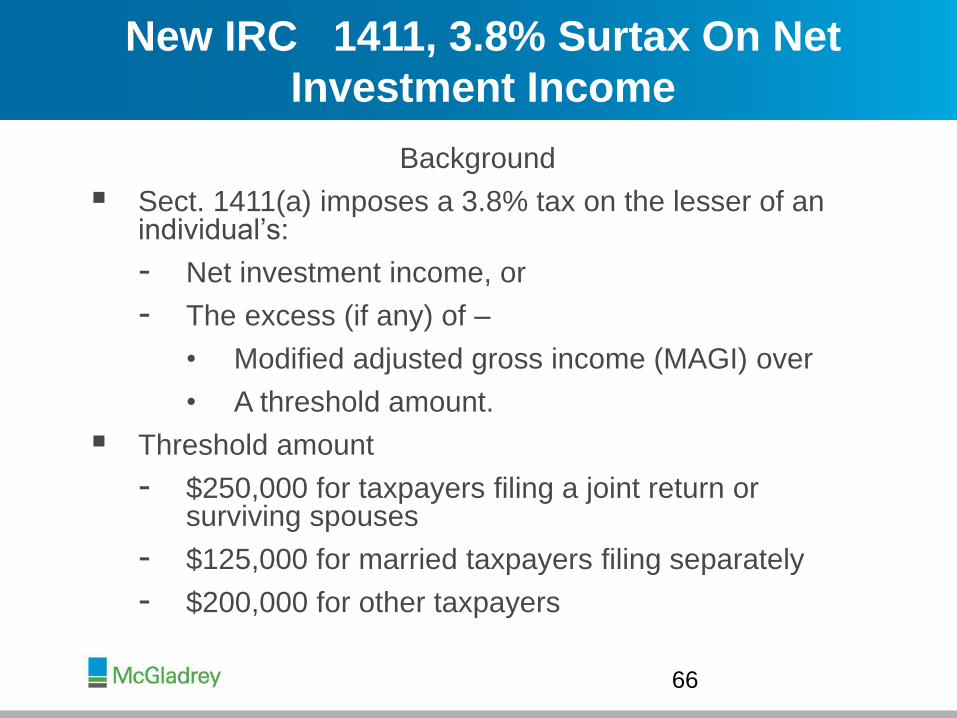

Background

New IRC

1411, 3.8% Surtax On Net

Investment Income

Background

Sect. 1411(a) imposes a 3.8% tax on the lesser of an individual’s:

- Net investment income, or

- The excess (if any) of –

• Modified adjusted gross income (MAGI) over

• A threshold amount.

Threshold amount

- $250,000 for taxpayers filing a joint return or surviving spouses

- $125,000 for married taxpayers filing separately

- $200,000 for other taxpayers

66

Slide Intentionally Left Blank

New IRC

1411, 3.8% Surtax On Net

Investment Income (Cont.)

Background (Cont.)

For estates and trusts,

1411(a)(2) imposes a 3.8% tax on

the lesser of:

- Undistributed net investment income, or

- The excess (if any) of –

• Adjusted gross income, over

• The dollar amount at which the highest tax bracket in

which

1(e) begins for the year.

68

New IRC

1411, 3.8% Surtax On Net

Investment Income (Cont.)

Background (Cont.)

Sec. 1411(c) defines “net investment income” as the excess (if any) of:

- The sum of:

• Gross income from interest, dividends, annuities, royalties and rents, other than such income which is derived in the ordinary course of a trade or business (emphasis added) described in

1411(c)(2);

• Other gross income derived from a trade or business described in 1411(c)(2); and

• Net gain (to the extent taken into account in computing taxable income) attributable to the disposition of property other than property held in a trade or business not described in

1411(c)(2);

over

- The deductions allowed by Subtitle A of the Internal Revenue Code that are properly allocable to such gross income or net gain.

A trade or business is described in

1411(c)(2) if the trade or business is:

- A passive activity with respect to the taxpayer, or

- A trade or business of trading in financial instruments or commodities.

69

New IRC

1411, 3.8% Surtax On Net

Investment Income (Cont.)

Background (Cont.)

Disposition of an interest in an S corporation or partnership

(pass-though entity)

- Sect. 1411 (c)(4) provides that gain (or loss) from the

disposition of an interest in a pass-through entity is taken

into account under

1411(c)(1)(A)(iii) only to the extent of

the net gain (or net loss) that would be so taken into

account by the transferor, if all property of the pass-

through entity were sold for FMV immediately before the

disposition of such interest.

Sect. 1411(c)(6) provides that

1411 does not include any

item taken into account in determining self-employment

income.

70

Proposed

1411 Regulations, REG-

130507-11, Issued Dec. 5, 2012

Proposed

1411 Regulations, REG-

130507-11, Issued Dec. 5, 2012

Net Investment Income

Public hearing is scheduled for April 2, 2013.

Proposed regulations are generally scheduled to take effect

for tax years beginning after Dec. 3, 2013.

72

Proposed Reg.

1.1411-4, Net

Investment Income (NII)

Net Investment Income

NII includes gross income from rents, dividends, annuities,

royalties, rents, substitute interest payments and substitute

dividend payments, except to the extent derived in the ordinary

course of a trade or business.

- Level for determining whether gross income is derived in the

ordinary course of a trade or business

• Made at the individual level when the individual, estate,

or trust owns or engages in a trade or business directly

or indirectly through a disregarded entity (DE)

• Made at the entity level when the individual, estate or

trust owns or engages in a trade or business through

one or more pass-through entities

73

Proposed Reg.

1.1411-4, Net

Investment Income (NII), Cont.

Net Investment Income (Cont.)

Items of NII in

1411(c)(1)(A)(i) and Prop. Reg.

1.1411-4(a)(1)(i) that are portfolio income will, by definition, be included in

1411 because these portfolio items are not

derived in the ordinary course of a trade or business.

Self-charged interest, which is treated as passive income under Reg.

1.469-7, is subject to the surtax under

1411(c)(1)(A)(i).

Self-charged rent will be subject to the surtax under 1411(c)(1)(A)(i), if the gross rents are from an activity

described in Reg.

1.469-2(f)(6) that is not derived in the ordinary course of a trade or business.

Interest on working capital will generally be subject to the surtax under

1411(c)(1)(A)(i).

74

Proposed Reg.

1.1411-4, Net

Investment Income (NII), Cont.

Computation Of Net Gain

Net gain under

1411(c)(1)(A)(iii) does not include gain or loss

attributable to property (other than property from the investment of

working capital) held in a trade or business from other than a

passive activity.

- General rule

• A partnership interest or S corporation stock is not property

held in a trade or business.

- Level for determining whether net gain is attributable to property

held in a trade or business

• Made at the individual level if individual, estate or trust

owns or engages in trade or business, directly or indirectly,

through a DE

• Made at the entity level if individual, estate or trust owns an

interest through one or more pass-through entities 75

Proposed Reg.

1.1411-4, Net

Investment Income (NII), Cont.

Properly Allocable Deductions

Proposed Reg.

1.1411-4(f) provides that, unless specifically stated otherwise, only properly allocable deductions described in paragraph (f) may be taken into account in determining net investment income. These deductions include:

- Deductions allocable to gross income from rents and royalties under

62(a)(4)

- Deductions allocable to passive activities described in proposed Reg.

1.1411-5

- Investment interest expense (as defined in

163(d)(3))

- Investment expenses (as defined in

163(d)(4)(C))

- Taxes imposed under

164(a)(3)

76

Proposed Reg.

1.1411-4, Net

Investment Income (NII), Cont.

Properly Allocable Deductions (Cont.)

Except to the extent allowed under Chap. 1 (e.g., carryover of

excess investment interest expense), current-year deductions

in excess of NII may not offset NII in another year.

NOL carryovers and carrybacks are not deductible in

computing NII.

Itemized deductions may be allocated to NII only to the extent

they exceed the 2% floor on miscellaneous itemized

deductions and the overall limitation on itemized deductions.

Deductions allowed under proposed Reg.

1.1411-4(f) do not

include losses described in

165.

- Such losses are deductible only in determining net gain

under

1411(c)(1)(A)(iii).

77

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies

Provides that the

1411 tax applies to a trade or business

that is a passive activity

- Whether an activity is a trade or business is determined

under

162.

- Whether a trade or business is a passive activity is

determined under

469.

Sect. 469(c)(1) provides that a passive activity involves the

conduct of a trade or business activity in which the taxpayer

does not materially participate.

78

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Note that under Reg.

1.469-4(b)(1), trade or business

activities are activities, other than rental activities (emphasis

added) or activities that are treated under Reg.

1.469-

1T(e)(3)(vi)(B) as incidental to an activity of holding property

for investment, that:

- (i) Involve the conduct of a trade or business (within the

meaning of Sect. 162),

- (ii) Are conducted in anticipation of the commencement of

a trade or business, or

- (iii) Involve research or experimental expenditures that

are deductible under

174 (or would be deductible if the

taxpayer adopted the method described in

174(a)).

• The proposed

1411 regulations do not appear to

follow subparagraphs (ii) and (iii), above.

79

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

To be engaged in a trade or business, the taxpayer must be

involved in the activity with continuity and regularity, and the

taxpayer’s primary purpose for engaging in the activity must be

for income or profit. (Groetzinger, Sup. Ct. 1987)

The rental of even a single property may constitute a trade or

business, under various provisions of the Code.

- Hazard (TC 1946) (1939 IRC

117)

- Post (TC 1956) (1939 IRC

117)

- Gilford (2d Cir. 1953) (1939 IRC

117)

- Schwarcz (TC 1955) (1939 IRC

122)

- Elek (TC 1958) (1939 IRC

122)

- Fegan (TC 1979) (

482)

- Pinchot (2d Cir. 1940) (1926 IRC

302)

- Flint (Sup. Ct. 1911)

80

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Sect. 469(c)(2) provides that rental activities are automatically

deemed to be passive, for purposes of the passive activity

rules.

Sect. 468(j)(8) defines the term “rental activity” to mean any

activity in which payments are principally for the use of

tangible property.

- See Reg.

1.469-1T(d)(3)(ii) for certain exceptions

Sect. 469(c)(7) provides an exception for real estate rental

activities conducted by certain real estate professionals.

- This exception provides that the qualified rental real

estate activity is not per se passive.

- Note that a qualified real estate professional must still

materially participate in his real estate rental activities to

have this exception to the passive loss rules apply.

81

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

The proposed regulations generally follow the taxpayer’s grouping

rules to determine whether a taxpayer materially participates in a

trade or business activity, for purposes of

1411.

- Proposed Reg.

1.469-11(b)(3)(iv)(A) would allow an individual,

estate or trust to regroup its activities, without regard to the

manner in which the activities were grouped in the preceding

taxable year, in the first taxable year beginning after Dec. 31,

2013 in which

1411 would apply to such taxpayer.

A proper grouping under Reg.

1.469-4(d)(1) (grouping rental

activities with other trade or business activities) will not convert

gross income from rents into other gross income derived from a

trade or business described in Prop. Reg.

1.1411-5(a)(1).

- Gross income from the rental activity must derived in the

ordinary course of a trade or business under

162 in order to

escape taxation under

1411.

82

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Example 1: Rental Activity

A, an unmarried individual, rents a commercial building to B for

$50,000 in Year 1. A’s rental activity does not involve the conduct

of a

162 trade or business, but under

469(c)(2), A’s rental

activity is a passive activity. Because the rental activity does not

satisfy the trade or business requirement of proposed Reg. 1.1411-5(b)(1)(i), A’s rental income of $50,000 will not constitute

NII under

1411(c)(1)(A)(i). A’s rental income of $50,000 will still

constitute gross income from rents within the meaning of 1411(c)(1)(A)(i), however, because this provision does not

require a trade or business.

83

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Example 2: Application Of Grouping Rules Under

469

In Year 1, A, an unmarried individual, owns an interest in PRS, which is a

partnership for federal income tax purposes. PRS is engaged in two

activities, X and Y, which constitute trades or businesses (within the

meaning of

162), neither of which constitute trading in financial

instruments or commodities. Pursuant to Reg.

1.469-4, A has properly

grouped X and Y (the grouped activity). A participates in X for more than

500 hours during Year 1 and would be treated as materially participating

in the activity, within the meaning of Reg.

1.469-5T(a)(1). A only

participates in Y for 50 hours during Year 1 and, but for the grouping of

the two activities together, would not be treated as materially

participating in Y within the meaning of Reg.

1.469-5T(a). Pursuant to 1.469-4 and 1.469-5T(a)(1), however, A materially participates in the

grouped activity, and therefore for purposes of proposed Reg.

1.1411-

5(b)(1)(ii), neither X nor Y is a passive activity with respect to A.

Accordingly, with respect to A, neither X nor Y is a trade or business

described in proposed Reg.

1.1411-5(b)(1).

84

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Example 3: Application Of The Rental Activity Exceptions

B, an unmarried individual, is a partner in PRS, which is engaged in an

equipment leasing activity. The average period of customer use of the

equipment is seven days or fewer (and therefore meets the exception in

Reg.

1.469-1T(e)(3)(ii)(A)). B materially participates in the equipment

leasing activity (within the meaning of Reg.

1.469-5T(a)). The

equipment leasing activity constitutes a trade or business within the

meaning of

162.

In Year 1, B has modified adjusted gross income (as defined in proposed

Reg.

1.1411-2(c)) of $300,000, all of which is derived from PRS. All of

the income from PRS is derived in the ordinary course of the equipment

leasing activity, and all of PRS’ property is held in the equipment leasing

activity. Of B’s allocable share of income from PRS, $275,000 constitutes

gross income from rents (within the meaning of proposed Reg.

1.1411-

4(a)(1)(i)).

85

Slide Intentionally Left Blank

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Example 3: Application Of The Rental Activity Exceptions (Cont.)

While $275,000 of the gross income from the equipment leasing activity meets

the definition of rents in proposed Reg.

1.1411-4(a)(i), the activity meets one

of the exceptions to rental activity in Reg.

1.469-1T(e)(3)(ii), and B materially

participates in the activity. Therefore, the trade or business is not a passive

activity with respect to B for purposes of proposed Reg.

1.1411-5(b)(1)(ii),

and because the rents are derived in the ordinary courses of a trade or

business, the ordinary course of a trade or business exception in proposed

Reg.

1.1411-4(b) applies, which means that the rents are not subject to

proposed Reg.

1.1411-4(a)(1)(i). Furthermore, because the equipment

leasing trade or business is not a trade or business described in proposed

Reg.

1.1411-5(a)(1) or (a)(2), the $25,000 of other gross income is not

subject to proposed Reg.

1.1411-4(a)(1)(ii). Finally, gain or loss from the sale

of the property held in the equipment leasing activity will not be subject to

proposed Reg.

1.1411-4(a)(1)(iii), because although it is attributable to a

trade or business, it is not a trade or business to which the

1411 tax applies.

87

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Example 4: Application Of

469 And Other Gross Income

Under Proposed Reg.

1.1411-4(a)(1)(ii)

Use the same facts as Example 3, except that B does not materially

participate in the equipment leasing trade or business, and therefore the trade

or business is a passive activity with respect to B for purposes of proposed

Reg.

1.1411-5(b)(1)(ii). Accordingly, the $275,0000 of gross income from

rents is subject to proposed Reg.

1.1411-4(a)(i), because the rents are

derived from a trade or business described in proposed Reg.

1.1411-5(a)(1)

(that is, the ordinary course of a trade or business exception in proposed Reg. 1.1411-4(b) is inapplicable). Furthermore, the $25,000 of other gross income

from the equipment leasing trade or business is subject to proposed Reg. 1.1411-4(a)(1)(ii), because that income is derived from a trade or business

described in proposed Reg.

1.1411-5(a)(1). Finally, gain or loss from the sale

of the property used in the equipment leasing trade or business is subject to

proposed Reg.

1.1411-4(a)(1)(iii), because the trade or business is a passive

activity with respect to B.

88

Proposed Reg.

1.1411-5, Trades Or Businesses

To Which The

1411 Tax Applies, (Cont.)

Example 5: Application Of The Portfolio Income Rule And

469

C, an unmarried individual, is a partner in PRS, a partnership engaged in a trade or

business (within the meaning of

162) that does not involve a rental activity. C does not

materially participate in PRS within the meaning of Reg.

1.469-5T(a), and therefore

the trade or business of PRS is a passive activity with respect to C for purposes of

Prop. Reg.

1.1411-5(a)(1). C’s $500,000 allocable share of PRS’ income consists of

$450,000 of gross income from a trade or business and $50,000 of gross income from

dividends and interest (within the meaning of proposed Reg.

1.1411-4(a)(1)(i)) that is

not derived in the ordinary course of the trade or business of PRS. Thus, under 469(e)(1)(A)(i)(1) and the regulations thereunder, C’s allocable share of gross income

from dividends and interest consists of portfolio income. Therefore, C’s $500,000

allocable share of PRS’ income is subject to

1411. C’s $50,000 allocable share of

PRS’ income from dividends and interest is subject to proposed Reg.

1.1411-4(a)(1)(i),

because the share is gross income from interest and dividends that is not derived in the

ordinary course of a trade or business (that is, the ordinary course of a trade or

business exception of proposed Reg.

1.1411-4(b) is inapplicable). C’s $450,000

allocable share of PRS’ income is subject to proposed Reg.

1.1411-4(a)(1)(ii),

because it is gross income from a trade or business that is a passive activity.

89