part 2 of 2 - nasdaq omx corporate...

TRANSCRIPT

2014 Investor Day May 6, 2014

New York, New York

1

Part 2 of 2

Bill Weber VP, General Manager,

Marketing and Product

Development - Extremities

New Markets

2

Nerve Repair and Protection

29%

25%

24%

22%

2013 US Nerve Market (~$50M)

Autograft • Patient-derived nerve

Current Technology

Integra Nextgen Nerve • Environment to encourage Schwann cell

Integra Stryker

Axogen Other Launch in 2016

Manufacturer Products Product

Composition

Clinical Evidence

Integra NeuraGen Nerve Guide

NeuraWrap Nerve

Protector

Bovine Collagen

Bovine Collagen

Human prospective randomized trial;

Equivalent to suture/Autograft

AxoGen Avance Nerve Graft

AxoGuard Nerve

Connector

AxoGuard Nerve Protector

Allograft Nerve

Porcine SIS

Porcine SIS

Registry; Equivalent to Autograft

Stryker NeuroMatrix & NeuroFlex

NeuroMend

Bovine Collagen

Bovine Collagen

Limited data referenced

3

Chronic Wounds

34%

33% 8%

4%

21%

2013 US Wound Technology Market ($0.8B)

0.0

0.6

1.2

1.8

2.4

2013 2014 2015 2016 2017 2018

Wo

un

ds

in

mil

lio

ns

Hard-to-Heal Volume Projections

Chronic Wounds Acute Wounds

Current Products Composition Feature/Benefit Clinical Evidence

Integra BMWD Bilayer matrix; silicone + type 1

collagen

Potentially fewer applications

& single step

Apligraf Dermal layer (fibroblasts in type 1

collagen) + epidermal layer

Multiple applications, single

step supported by MC-RCT

Dermagraft Cryopreserved fibroblasts in a

bioabsorbable ECM

Multiple applications, single

step supported by MC-RCT

Epifix Human amniotic membrane Multiple applications, 5-yr shelf

life, activates healing, SSPS

Oasis Porcine SIS ECM Low cost, multiple applications,

off the shelf, MC-RCT

Chronic wounds increasing at twice the rate of

acute wounds

Smith & Nephew Integra All Other

Organogenesis MiMedx Group

*

* Based on positive outcome of DFU trial 4

Our Path Toward Success – DFU and Beyond

Near-Term Milestones

2H 2014:

• Complete trial

• Submit regulatory filings to FDA

• Submit randomized clinical trial results for publication

2015

• Potential regulatory approval

• Apply for reimbursement (MACS & private payers)

2016

• Launch DFU product into the wound clinic

2017 & beyond

• Expand indications and reimbursement

Commercial Highlights

Revenue generation depends on:

• Approval and reimbursement

• High-cost vs. low-cost

• Health economics

• New indications and broader reimbursement

• Enterprise selling

Distribution options

• Begin by leveraging existing channel

• Ultimately build focus in the clinic

Other opportunities

• Expand product offering (PD and business

development)

Expanding indications and increasing clinical evidence

5

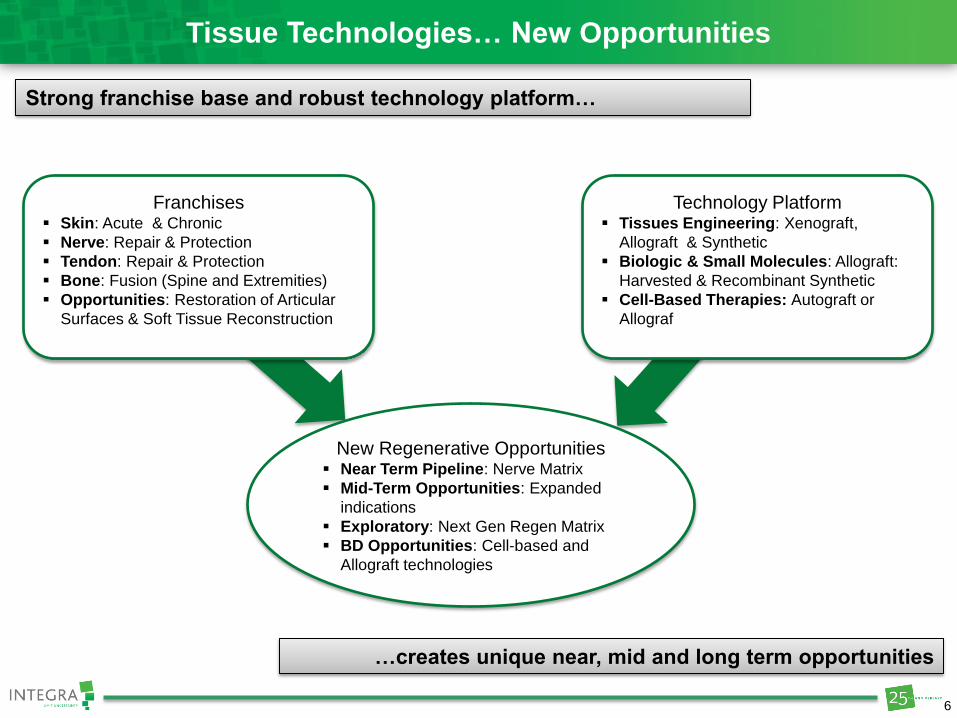

Tissue Technologies… New Opportunities

Franchises Skin: Acute & Chronic

Nerve: Repair & Protection

Tendon: Repair & Protection

Bone: Fusion (Spine and Extremities)

Opportunities: Restoration of Articular

Surfaces & Soft Tissue Reconstruction

Technology Platform Tissues Engineering: Xenograft,

Allograft & Synthetic

Biologic & Small Molecules: Allograft:

Harvested & Recombinant Synthetic

Cell-Based Therapies: Autograft or

Allograf

New Regenerative Opportunities Near Term Pipeline: Nerve Matrix

Mid-Term Opportunities: Expanded

indications

Exploratory: Next Gen Regen Matrix

BD Opportunities: Cell-based and

Allograft technologies

Strong franchise base and robust technology platform…

…creates unique near, mid and long term opportunities

6

2-Piece Total Ankle Replacement

Design Principles

• Simplified instrumentation to Limit Uncertainty

• Repeatable/Reproducible technique

• Anatomic/customizable to patient and bone sparing

Key Opinion Leaders

• Global design team

• Orthopedic and Podiatric representation

Regulatory Path: 510(k) and CE

26%

30%

24%

18%

2%

Total US Ankle Replacement Market (~$60M)

$0

$20

$40

$60

$80

$100

$120

2013 2014 2015 2016 2017 2018

Mil

lio

ns

Projected Market Growth

Wright SBI Other

Tornier Depuy

7

2-Piece Total Ankle: New Product Introduction

Design Plan

Design Qualification Phase

• Completed 4 of 5 design labs to date

• 5th design lab will freeze design

Design Verification and Validation

• Perform physical characterization and testing of

device and predicate

• Validate design with surgeons from US and key

International markets

Global Launch

• Scale up from prototype to full-scale production to

build inventory required for global launch

• Build global KOL team to assist with product roll-out

and surgeon education

• Global awareness and adoption key to success

Timeline

2H 2014 • Design Freeze

2015

• Complete Design Verification and Validation

2016

• Regulatory Approval and Global Launch

8

Shoulder

19%

16%

22%

21%

6%

16%

US Shoulder Market ($0.7B)

Anatomic Shoulder

• Reproduces existing anatomy

• Patients with bone-on-bone osteoarthritis and intact rotator cuff tendons

Reverse Shoulder

• Reverses the anatomy

• Patients with severe arthritis and/or torn rotator cuff

• Revision of a failed anatomic shoulder

Product Feature/Benefit Launch Status

Reverse Shoulder Provides choice Launched Q3 13

Proximal Humeral Plate Addresses fracture Launched Q4 13

Advanced Glenoid Solves glenoid loosening 2015

Conventional Pegged Glenoid Ease of use 2015/2016

Advanced shoulder options Bone sparing Pipeline

Pyrocarbon HRA Restoration of function Pipeline

Pyrocarbon Hemi Option for younger patient Pipeline

7%

10%

Market

Growth

Zimmer Depuy Exactech

Tornier Biomet Other

9

Integra’s Titan Shoulder System

Benefits of Modularity:

• Simplifies conversion from primary to a reverse shoulder –

saves OR time

• Multiple body heights allows for better anatomical fit and

optimal stability

• Utilization of instruments across primary, fracture, and

reverse shoulders reduces number of required instrument

trays

Benefits of PyroCarbon – Building off Modularity:

• Builds off the same stem/body platform

• Improved long-term functional outcome

• Reduction of pain

• Mitigation of glenoid loosening

• Preserves options for future revision procedures

Only modular system that potentially benefits from pyrocarbon

Solid foundation designed for the future

10

Shoulder Pipeline

Three-pronged approach to building shoulder:

• (1) Complete conventional portfolio of products

• (2) Address glenoid loosening with advanced glenoid solutions

• (3) Develop disruptive technologies that drive better clinical outcomes

(i.e. improved long-term functional outcome and reduction of pain)

2011 2012 2013 2014 2015 2016+

US

Int’l

Fracture

Plate

Advanced

Glenoid

Platform

PyroHemi™

PyroTITAN®

PyroHemi™

Reverse

Shoulder

Fracture

Plate

WW Launch

Total Shoulder

PyroTITAN®

Reverse

Shoulder

11

Paul Gonsalves SVP, Enterprise Selling and

Corporate Marketing

Enterprise Selling

12

Significant Changes in Clinical and Financial Models

Acute

Inpatient

Care

Specialty

Care

Primary

Care

Acute

Inpatient

Care

Specialty

Care

Primary

Care

Depending on the market, over the next 3 years payment models will change through new legislation,

regulations, market dynamics and activist payors/employers requesting:

Fee-for-Service model Episodic model

13

Hospital

Admin

Surgeon

Sales Team

Media

ACO’s

Payor

Growing

Declining

GPO/

IDN’s

Patient

Strong relationships between physician and sales team changing to include broader fabric of influencers

Evolving Healthcare Marketplace - Stakeholders

Changing Influence

14

“Episodic” Payment

• Support engagement of patients in

treatment decision-making process

• Pay for team-based care for the total

episodic care

• Pay based on evidence-based care

• Creates opportunities to engage with

providers at highest levels - Enterprise

• Rewards innovative approaches to care

delivery – both provider and vendor

• Rewards team based approach now

including technology provider/vendor

Fee-for-Service

• Reward volume over value of services

• Discourage coordination of care over

time and across the continuum of care

• Undermine strong physician/patient

relationships and team-based care

• Drives specialization by segment or

disease state, fails to look at broader

healthcare econ of provider

• Relies heavily on vendor/physician

relationship – large teams

• Narrow focus on technology versus

solutions & partnership

Changing Marketplace – Providers Shifting To Adapt

Provider Community

FROM TO

Pro

vid

er

Ma

nu

factu

rer

Accelerating alignment to shared goals

H

15

Repositioning our Coverage Model – Key Acct Strategy

Instr Neuro Spine Ortho-Bio Extremity/Recon

Today

Instr Neuro Spine Ortho-Bio Extremity/Recon

Tomorrow

Enterprise Mgr & Customer

Alignment and Repositioning

Simplifying how customers do business with Integra

16

Competitive Advantages

Company Clinical

Support

Multi Product

Solutions

Cost

Savings Agility

Typical Single-modality Co

INTEGRA

Typical Large Diversified Co

2

5

%

2

5

% 2

5

%

2

5

%

Integra Core Customer Value: • Regenerative Platform - Company anchored in cutting edge science, clinically disruptive and aligns with the

medical goals of self-healing

• Organizational Structure - Aligned and flat allows us to take calculated risks-pilot, sales strategies to grow our business

• Speed and Agility - Allows us to take advantage of new opportunities

Integra positioned to WIN with agile organization, differentiated product

offering and culture of collaboration

2

5

%

2

5

%2

5

%

17

Integra Integrated Contracting

Where? • Academic accounts

• Integrated delivery networks

• Government accounts

• Large regional networks/affiliates

• Group purchasing organizations

How? • Technical/clinical support

• Single point of contact

• Knowledge of customer business structure

• Multi-product/multi-vendor solutions

• Enterprise-wide pricing, purchasing and service

Customer Segments

Academic Regenerative & Organizational structure

Financially Driven - Cost Constrained Enterprise contracting & rapid decision making

Stand Alone - Stable, High Control Portfolio contracting

Outcomes Driven Building deeper clinical & scientific teams to work with

our clients

18

VA / DoD… Building Out Sales Volume in Largely Untapped Customer Base

Contracting partner in place

1 contract for Surgical

instruments

Delivering $4M per year

Introduce Enterprise leader in

January

Develop portfolio approach

Begin broad discussion to build

out portfolio approach

Successful partnership

accelerating

Move from single product to

multi-product contract

Consideration for Neuro, Recon

and Orthobiological product

underway = $9M

Integrated Delivery Systems… Building Deeper Relationships with Current Customers

Partner with general hospital in

place, one division

Contracting for neurosurgical

equipment only

Delivering $1M per year

Introduce Enterprise leader in

January

Develop portfolio approach

Begin broad discussion to

build out portfolio approach

including Skin, Recon, Spine

and Surgical instruments

Successful partnership

accelerating

Moving from single product to

ACO and clinical program

development

Customers – Delivering Impact

Innovative approach to evolving market

19

John Mooradian CVP, Global Operations and

Supply Chain

Operational

Improvements

20

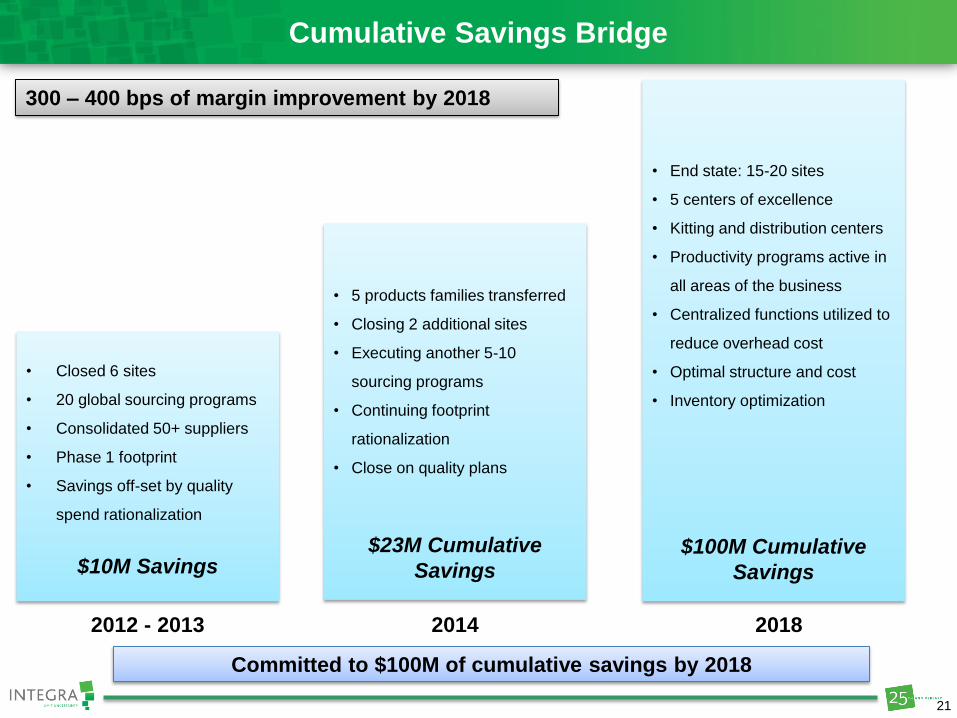

Cumulative Savings Bridge

• Closed 6 sites

• 20 global sourcing programs

• Consolidated 50+ suppliers

• Phase 1 footprint

• Savings off-set by quality

spend rationalization

$10M Savings

2012 - 2013

• 5 products families transferred

• Closing 2 additional sites

• Executing another 5-10

sourcing programs

• Continuing footprint

rationalization

• Close on quality plans

$23M Cumulative

Savings

2014

• End state: 15-20 sites

• 5 centers of excellence

• Kitting and distribution centers

• Productivity programs active in

all areas of the business

• Centralized functions utilized to

reduce overhead cost

• Optimal structure and cost

• Inventory optimization

$100M Cumulative

Savings

2018

300 – 400 bps of margin improvement by 2018

Committed to $100M of cumulative savings by 2018

21

Supply Chain Program-to-Date Savings

$2.7

$0.1

$1.0

$1.5

Total Program Savings 2013

Production Materials

Non-Production Spend

Services

Inventory Scrap

Total

Savings

$5.3M

• Established centrally-led strategic sourcing group to

optimize all areas of spend (company-wide)

• Spend mapping and analysis directed group to

opportunity areas

• Leveraged spend with preferred suppliers identified

through strategic sourcing process

• Service providers targeted to go from 50+ to 2

preferred

Sourcing Projects

Production Materials:

• Orthopedic Metals, Plastic Tubing, Plastic Parts

Non-Production Materials:

• Insurance, Consumables (Supplies)

Services:

• Temporary Staffing, Travel Management, Janitorial

Cumulative Savings

$-

$3

$6

$9

$12

$15

$18

2012 2013 2014

Milli

on

s

Cumulative Savings Run Rate

Early savings on track

22

Supply Chain Strategy

Suppliers

Sourcing

Team

25+

Sites

25+ Sites

Sourcing Team

Suppliers

Opportunistic

Low hanging fruit

Supplier awareness

Operationalize sourcing

Common approach

Contract terms

Supplier dashboards

Consolidate resources

Accelerate savings

Sustainable savings

Global Strategic Sourcing & Procurement

Production

Materials

MRO* Systems &

Performance

*MRO – Maintenance,

Repair,

Operational Supplies

Packaging

Electronics

Metals

Plastics

Biologics

2012/2013

2014+

Strategic Sourcing Structure

Service &

Support

Non

Production

23

Footprint Rationalization Plan

Complete

Strategic optimization plan 2014

2015 – 2018 Q1 Q2 Q3 Q4

• 6 site

closures

• 5 year

strategic

optimization

plan

• Purchasing

management

team and

structure

• 2014

transfer

plans

• Detailed due

diligence

• Plans

finalized

• Hired core

transfer teams

• Begin

transition

inventory

builds

• Install

equipment at

receiving sites

• Hire labor and

begin training

• Begin

validations at

receiving

sites

• Finish

transition

inventory

builds

• Develop 2015

transfer plans

• Conclude

validations at

receiving sites

• Transfer

remaining

equipment

and inventory

• Close 2

facilities

• Closure of

additional sites

• Complete

transition to

centers of

excellence

• Optimize

capacity

utilization

• Logistics and

distribution

• Lean 6 sigma

program

$4M

(thru ’13)

$15M

(thru ’15)

$50-70M

(thru ‘18)

• 2 site closures

• 5 product family transfers

Going from planning mode to execution

24

Site construction work complete

Over 25 new facility systems tested and qualified

Over 13 manufacturing process systems installed;

first run of skin product successful

Q4 2014 – target for all validation completion

First manufacturing lots release will be 510K

products; PMA products to follow upon FDA

approval

New Plainsboro, NJ, regenerative

medicine manufacturing facility

109 strategy and opportunity

• Skin (510k/pma)

• Private Label expansion

• Growth capacity

• International growth

• Long-term viability of the facility

• Capacity utilization/cost

• Quality and compliance capability

World class regenerative products manufacturing

Quality product delivered on time … every time

• Plainsboro 105 - collagen production

• Anasco, Puerto Rico - collagen, biopatch (private

label), neurogen, medical products

Plainsboro 109 - capacity to grow 3-4x

Regenerative medicine center of

excellence

World Class Manufacturing Facility - 109

Begin production by the end of 2014

25

Supply chain

optimization

Footprint

consolidation

Common systems

$30-50M Cumulative Savings

$50-70M Cumulative Savings

Enabler

+300-400bps

Margin

2012 – 2018 Timeline

2012 2013 2014 2015 2016 2017 2018

Plan generates 300 – 400 bps of margin improvement versus 2012…

…Restructuring plan on track to drive savings by 2018

26

Padma

Thiruvengadam CVP, Chief Human Resources

Officer

Organization and

Priorities

27

2014 – 2016 Priorities

Select Key Priorities Tightly Aligned to Our Strategy

Building the capabilities and focusing capacity to achieve our objectives

I. Deliver on restructuring plan: Advance on our plans to achieve 23-24%

Adjusted EBITDA by 2018

II. Deliver consistent growth: 5-7% Organic, 7%+ with M&A

III. Focus and align the portfolio

IV. Make commercial changes to adapt to healthcare reform

V. Leverage scale for commercial advantage and cost competitiveness

28

Areas of Advancement Across the Company

• Enhanced global

commercial capabilities

• Field inventory

management

• Engrain culture of

replicating best practices

– e.g. Plainsboro

• New CSO organization to

increase velocity of

product development

processes

Margin Improvement,

FCF Conversion

Improving Execution

• Strategic sourcing and

footprint plans

• Centers of Excellence –

e.g. manufacturing,

regenerative platform

• Globalized priorities

reduce time to

registration and increase

speed to market

Simplification, Focus,

Consistent Performance

Optimizing the

Company

• Rationalize product

portfolio to focus in

profitable, scalable areas

• Increase capacity in key

areas of focus

• Enable stable supply

• Align portfolio to market

needs

• Introduce wound care

channel

• Achieve peak market

share sooner

5-7% Organic Growth,

M&A upside

Margin and Cash

Improvement

Quality Excellence and

Stable Operations

Accelerating Growth

New Product

Introductions

Building the foundation for profitable growth

29

Governance

Getting the Most Out of Marketing to Support Our Goals

• Implement a global marketing platform… supporting

international growth

• Global commercial owners for key product

franchises

• Leveraging existing channels; assess new channels

• Enhancing and evolving current go-to-market

strategies

• Achieving peak market share sooner

Global Commercial Effectiveness

• Program management fundamentals increase capacity

by enabling:

• Common language

• Common approach

• Simpler processes

• Lean Six Sigma program and operational excellence;

over 600 colleagues

• Yield – more efficient at:

• New product introductions

• International registrations

Framework Measurement

Building Competencies to Enable

Profitable Growth

30

Organizational Effectiveness - ERP

Pilot go-live: March 2013

US order to cash go-live: April 30, 2014

>75% of revenues running on common

system

• Enables back-office consolidation and phase I

savings

• New expense burden: $10M annualized

ERP Implementation – Go-Live

• Enables us to grow sales faster than fixed costs

• More efficient and effective processes simplify overall

org structure

• Better access to information will enable us to make

fact-based decisions faster

Common System to Enable

Efficiency and Effectiveness

• US Order to Cash

• US Distribution

• HQ Finance,

Procurement, HR

• US Manufacturing

• US Service and Repair

• Order to Cash – Int’l

Wave 1 Go-Live Wave 2

31

Operational Model for Growth

Grow the

business Lead to

perform

Drive

execution

Sustain the

platform

Processes in place to execute on growth strategy

Outside-In

Insight, intelligence and

ideas

Inside-Out

Values and culture

Bottom-Up

Execution

Top Down

Strategy

32

Jack Henneman CVP, Chief Administrative

Officer

Financials

33

Financial Summary

Total Revenue Adj. Gross Margin

Operating Cash Flow Adj. EBITDA

$836M$780M$732M

$1,400

$1,200

$1,000

$800

$600

$400

$200

$0

2018E

$1.1 - $1.3B

2014E

$920 - $940M

2013 2012

$831M

2011 2010

$53M

$104M$106M

$59M

60.0%

40.0%

20.0%

0

$200

$150

$100

$50

$0

100.0%

80.0%

2018E

$185M+

2014E

$60 - $80M

2013 2012

$120M

$60M

2011 2010

OCF Adjustments* FCF Conversion

*In 2012, we generated $59.1 million in cash flows from operations, which was reduced by a $29.8 million tax withholding payment in connection with

the release of certain deferred stock units and $30.6 million of accreted interest paid at the maturity of our 2012 Senior Convertible Note.

** FCF Conversion = TTM (Operating Cash Flow – Capital Expenditures) / TTM Adjusted Net Income

*** GAAP Reconciliations can be found in the Appendix.

20.0%19.8%20.6%

15%

18%

21%

24%

27%

2018E

23-24%

2014E

20-22%

2013

15.8%

2012 2011 2010

63.9%

64.9%64.4%64.7%

62%

64%

66%

68%

70%

2014E

65-66%

2013 2012 2011 2010 2018E

68-70%

34

Bridge from 2012 Investor Day Guidance

2017 Targets:

Oct 2012

2013 Actuals 2018 Targets:

Current

Core Revenue Growth 5-7% 0.6% 5-7%

Adj. Gross Margin 68-70% 63.9% 68-70%

Adj. SG&A (% of Rev)* 41-43% 45.1% 41-43%

R&D (% of Rev) 6-7% 6.1% 6-7%

Adj. EBITDA Margin 23-24% 15.8% 23-24%

Adj. EPS Growth 9-13% -24.7% 10%+

Adj. Tax Rate High 20s /

Low 30s 26.8% Low 30s

Adj. FCF Conversion N/A 7.1% >90%

Diluted Shares Outstanding Flat 28.8M ~33-35M

*Adjusting 2012 Adj. SG&A target to move the location of the medical device excise tax (“MDET”) (rounds to 1% of revenue).

In 2012, the MDET was forecast in Adj. EBITDA but was not allocated yet to either gross margin or SG&A.

Changes

from 2012

investor

meeting

Plans enable us to maintain our 2012 long-term targets

35

Revenue Growth

Division 2010 – 2013

Growth Growth Driver

2013 – 2018

Growth

Visible drivers to lead recovery in top line performance

*US Spine & Other segment includes revenue from Spine Hardware, Orthobiologics and Private Label.

• Selling and marketing investments

• New product introductions

• Expansion to near adjacencies

1.3% 2-6%

US Neurosurgery

• Specialty products, clinical focus

• Advantages in enterprise selling

• Value-added services

0.4% 1-4%

US Instruments

• Strong shoulder product pipeline

• DFU, wound care launch

• Specialization of sales channels

14.6% 10-14%

US Extremities

• New products

• Stronger distribution

• Private Label, collagen capacity

5.7% 1-5%

US Spine & Other*

• Focus products, focus markets

• New product launches

• Infrastructure investment

4.4% 9-13%

International

36

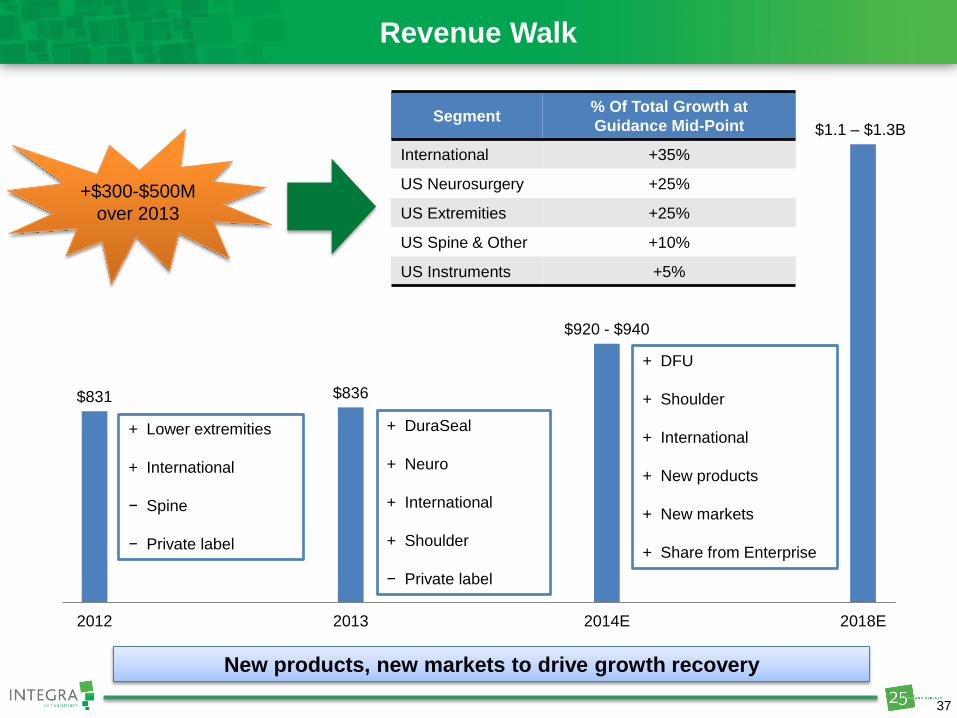

Revenue Walk

$831 $836

$920 - $940

$1.1 – $1.3B

2012 2013 2014E 2018E

+ Lower extremities

+ International

− Spine

− Private label

+ DuraSeal

+ Neuro

+ International

+ Shoulder

− Private label

+ DFU

+ Shoulder

+ International

+ New products

+ New markets

+ Share from Enterprise

+$300-$500M

over 2013

Segment % Of Total Growth at

Guidance Mid-Point

International +35%

US Neurosurgery +25%

US Extremities +25%

US Spine & Other +10%

US Instruments +5%

New products, new markets to drive growth recovery

37

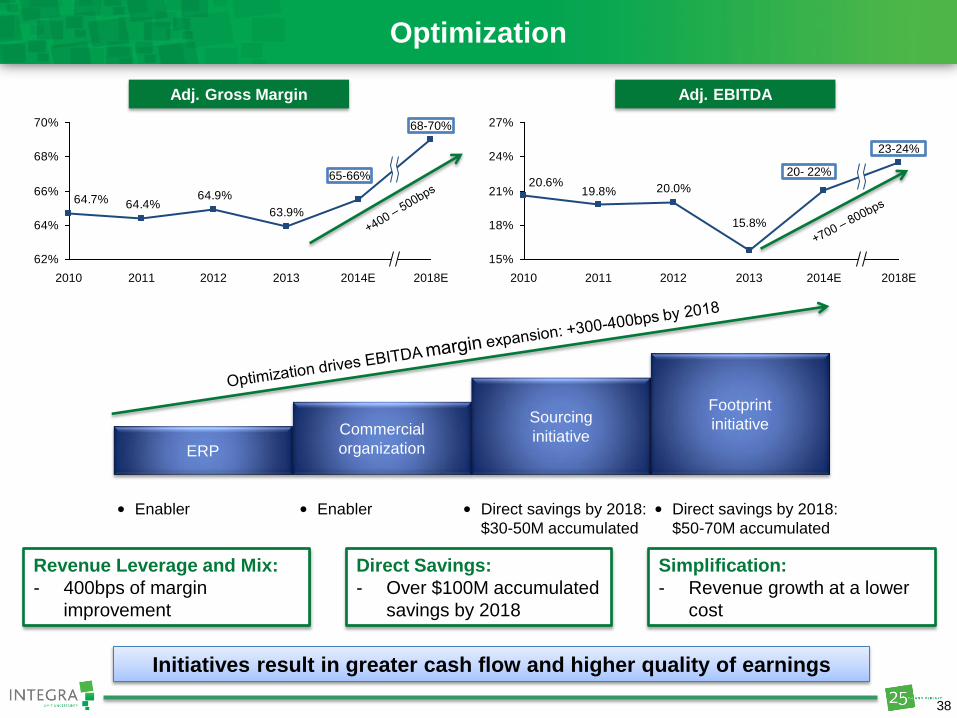

Optimization

ERP

Commercial

organization

Sourcing

initiative

Footprint

initiative

• Enabler • Enabler • Direct savings by 2018:

$30-50M accumulated

• Direct savings by 2018:

$50-70M accumulated

Direct Savings:

- Over $100M accumulated

savings by 2018

Simplification:

- Revenue growth at a lower

cost

Adj. Gross Margin Adj. EBITDA

Revenue Leverage and Mix:

- 400bps of margin

improvement

63.9%

64.9%64.4%64.7%

62%

64%

66%

68%

70%

2014E

65-66%

2013 2012 2011 2010 2018E

68-70%

20.0%19.8%20.6%

15%

18%

21%

24%

27%

2018E

23-24%

2014E

20- 22%

2013

15.8%

2012 2011 2010

Initiatives result in greater cash flow and higher quality of earnings

38

Adjusted Gross Margin Walk

64.9%

63.9%

65-66%

68-70%

2012 2013 2014E 2018E

+ Footprint plans

+ Sourcing savings

− Recall / higher

quality expense

− MDET

+ Product mix

+ Sourcing savings

+ Footprint plans

+ Sourcing savings

+ Product mix

+400-500bps

over 2013

Contributor Impact

Product Mix +200 bps

Footprint +100-150 bps

Sourcing +100-150 bps

Optimization initiatives, improved sales performance to drive GM higher

39

Adjusted EBITDA Margin Walk

20.0%

15.8%

20-22%

23-24%

2012 2013 2014E 2018E

+ Footprint plans

+ Sourcing savings

− Recall / higher

quality expense

− MDET

+ Gross margin

+ Sourcing

+ Leverage on

revenue

+ Gross margin

+ Footprint

+ Leverage on

revenue

− Selling

+700-800bps

over 2013

Contributor Impact

Gross Margin +400-500 bps

G&A:

Footprint

Leverage on revenue

+300bps

+100bps

+200bps

Direct savings, leverage drive improvement against headwinds

40

Cash Flow: Increasing Quality of Earnings

Operating Cash Flow

• FCF Conversion = TTM (Operating cash flow –

capital expenditures) / TTM Adjusted Net Income

• Greater than 10% by end of 2014

• Greater than 50% by end of 2015

• Greater than 80% by end of 2016

FCF Conversion

Improving quality of earnings to drive FCF

conversion higher

2013 2018E

-10%

10%

30%

50%

70%

90%

2012 2013 2014 2015 2016

>10%

>50%

>80%

$53M

$185M +

Direct savings, completion of key projects and leveraged growth drive

greater cash generation

41

Cash Generation and Capital Allocation

Priority capital allocation:

Strategic M&A

Paying down debt

Share repurchases (longer-term)

ROIC hurdle for investments: accretive to cost of capital in 3-5 years

Generating more cash Direct savings and leverage will drive a doubling of

cash flow in the next 2-3 years

42

Peter Arduini President and

Chief Executive Officer

Wrap-Up

43

Key Takeaways – INTEGRA Increasing Value

• Margin improvement: 23-24%

Adjusted EBITDA by 2018

• Deliver better cash flow and

higher quality of earnings: FCF

Conversion* above 80% by

end of 2016

• Consistency of results

• Integrated ERP and systems

implementations

• Restructuring plan focused on

operations with 300-400 bps

of improvement

• Portfolio optimization and

SKU simplification

Driving Above-Market

Growth

• Organic growth: 5-7%

• with M&A: 7% +

• Enhanced R&D pipeline

• New market expansion

opportunities

• International expansion

• Active BD pipeline

Improving Execution Optimizing the Company

You will hear today how we will deliver these key value-driving metrics

Building the foundation for profitable growth and accelerated earnings

*FCF Conversion = TTM (Operating cash flow – capital expenditures) / TTM Adjusted Net Income

44

Financial Summary

Total Revenue Adj. Gross Margin

Operating Cash Flow Adj. EBITDA

$836M$780M$732M

$1,400

$1,200

$1,000

$800

$600

$400

$200

$0

2014E

$920 - $940M

2013 2012

$831M

2011 2010 2018E

$1.1 - $1.3B

$53M

$104M$106M

$59M

100.0%

80.0%

60.0%

40.0%

20.0%

0

$200

$150

$100

$50

$0

2018E

$185M+

2014E

$60 - $80M

2013 2012

$120M

$60M

2011 2010

OCF Adjustments* FCF Conversion

*In 2012, we generated $59.1 million in cash flows from operations, which was reduced by a $29.8 million tax withholding payment in connection with the release of certain deferred stock

units and $30.6 million of accreted interest paid at the maturity of our 2012 Senior Convertible Note.

** FCF Conversion = TTM (Operating Cash Flow – Capital Expenditures) / TTM Adjusted Net Income

*** GAAP Reconciliations can be found in the Appendix.

19.9%19.8%20.6%

15%

18%

21%

24%

27%

2018E

23 – 24%

2014E

20 – 22%

2013

15.8%

2012 2011 2010

63.9%

64.9%64.4%64.7%

62%

64%

66%

68%

70%

2018E

68 – 70%

2014E

65 -66%

2013 2012 2011 2010

45

Leading Franchises and Markets

Lower Extremities

9-12% Growth

Shoulder

7-10% Growth

Orthobiologics

5-8% Growth

Skin – Burn/Wounds

6-9% Growth

International 6-12% Growth

Leading Markets Leading Franchises

46

2014 – 2016 Priorities

Select Key Priorities Tightly Aligned to Our Strategy

Building the capabilities and focusing capacity to achieve our objectives

I. Deliver on restructuring plan: Advance on our plans to achieve 23-24%

Adjusted EBITDA by 2018

II. Deliver consistent growth: 5-7% Organic, 7%+ with M&A

III. Focus and align the portfolio

IV. Make commercial changes to adapt to healthcare reform

V. Leverage scale for commercial advantage and cost competitiveness

47

Why Invest in Integra?

Profit Footprint

Sourcing

ERP

Organizational

Changes

Growth New Products

New Markets

Strategic M&A

Above-

Market

Performance

Integra is unique as a diversified mid-cap executing both margin expansion and

growth acceleration

Plans in place to execute and deliver above-market performance in 2015-

2016

48

49

2014 Investor Day May 6, 2014

New York, New York

2014 Investor Day May 6, 2014

New York, New York

Bios

50

Peter Arduini President and Chief Executive Officer

He joined Integra in November 2010 as President and Chief Operating Officer and was

appointed Chief Executive Officer and a director in January 2012. Before joining

Integra, Mr. Arduini was Corporate Vice President and President of Medication Delivery,

Baxter Healthcare, which he joined in 2005. Mr. Arduini was responsible for a $4.8

billion global division of Baxter. Prior to joining Baxter, Mr. Arduini worked for General

Electric Healthcare, where he spent much of his 15 years in a variety of management

roles for domestic and global businesses. Prior to joining General Electric Healthcare,

he spent four years with Procter and Gamble in sales and marketing. Mr. Arduini serves

on the Board of Directors of ADVAMED, the Advanced Medical Technology Association, and the Board of Directors of the National Italian American Foundation. Mr. Arduini received his bachelor's degree in

marketing from Susquehanna University and a master's in management from Northwestern University's Kellogg School

of Management.

51

John B. Henneman III CVP, Chief Administrative Officer

He is responsible for the Company’s finance department, including accounting and

financial reporting, budgeting, internal audit, tax, and treasury. In addition, he is

responsible for information systems, business development, the law department and

investor relations. Mr. Henneman was appointed Integra’s Corporate Vice President in

December 2012, and has been Integra’s Executive Vice President since February 2003,

was our Chief Administrative Officer from February 2003 until May 2008 and was Acting

Chief Financial Officer from September 2007 until May 2008, when he was appointed

Chief Financial Officer. Mr. Henneman was our General Counsel from September 1998

until September 2000 and our Senior Vice President, Chief Administrative Officer and

Secretary from September 2000 until February 2003. Mr. Henneman received an A.B. degree from Princeton University

and a J.D. from the University of Michigan Law School.

52

Wyeth integration globally for oncology and also served as Vice President, Oncology Asia-Pacific/Canada operations.

Prior to joining Pfizer, Ms. Thiruvengadam served as a Senior Vice President, Human Resources Executive at Bank of

America, from 2005 to 2007, and as Executive Vice President, Human Resource, at Loral Skynet – Loral Space and

Communications, from 2001 to 2004. Ms. Thiruvengadam completed her Master's program from Madras University and

her Bachelor’s from Osmania University.

Padma Thiruvengadam CVP, Chief Human Resources Officer

Padma Thiruvengadam is Integra’s Corporate Vice President, Chief Human Resources

Officer. She is responsible for providing leadership in developing and executing human

resources strategy in support of the overall business plan and strategic direction of the

organization. She is also responsible for Integra’s strategic initiatives and program

management. Ms. Thiruvengadam was appointed Integra’s Corporate Vice President in

December 2012. Previously, from September 2011 to December 2012, Ms.

Thiruvengadam served as Integra’s Chief Human Resources Officer. Prior to joining

Integra, Ms. Thiruvengadam held several leadership positions at Pfizer, Inc., from 2008

to 2011, including Vice President, Global Human Resources for Oncology. She led the

53

Robert T. Davis Jr. CVP, President Neurosurgery

His responsibilities include leadership of sales, marketing, product development, quality

assurance and manufacturing. Mr. Davis joined Integra in July 2012 as President of the

Global Neurosurgery business and was appointed Integra’s Corporate Vice President in

December 2012. He brings more than 25 years of executive management experience in

the global healthcare industry. Prior to joining Integra, Mr. Davis was the General

Manager for the Global Anesthesia & Critical Care business at Baxter Healthcare, from

2009 to 2012, and held various general management positions at GE Healthcare in the

areas of interventional therapeutics, cardiovascular imaging and diagnostic ultrasound,

from 1997 to 2009. Mr. Davis earned his B.S. in Sports Medicine from the University of Delaware, a Master’s degree in Exercise & Cardiovascular Physiology from Temple University, and an M.B.A. from

Drexel University.

54

Dan Reuvers CVP, President International

His responsibilities include executive oversight and leadership of all of Integra's

international businesses, including Europe, Middle East, Africa, Latin America, Asia

Pacific and Canada. He joined Integra in 2008 as Vice President of Marketing and

Product Development for Integra's surgical business and was promoted to President of

the acute surgical business in June 2010. He was appointed President, Instruments in

2011, Corporate Vice President in December 2012, and President - International in

November 2013. Mr. Reuvers was President of Omni-Tract Surgical from September

2005 until December 2008, when the company was acquired by Integra. Mr. Reuvers

has over 25 years of experience in the medical technology field, including holding various executive level positions in sales, marketing and general management. He serves on the board of directors of

Respirtech, Inc.

55

Debbie Leonetti CVP, President Instruments

Her responsibilities include sales, marketing and product development for Integra's

acute and alternate site instrument businesses. She joined Integra in 1997 as Director

of Marketing, was promoted to Vice President of Marketing in April 1999, Senior Vice

President of Global Marketing in May 2004, Chief Marketing Officer in September 2007,

President of Latin America, Asia Pacific and Canada (LAPAC) in 2008, and President of

Integra Surgical in 2009. In 2010, Ms. Leonetti was appointed President of Integra's

Instrument business and LAPAC. Ms. Leonetti was appointed President, International,

in 2011, Corporate Vice President in December 2012, and President - Instruments in

November 2013. From 1989 through 1997, Ms. Leonetti worked for Olympus Corporation and held positions in sales, sales training, and marketing. Prior to her experience at Olympus, Ms. Leonetti

completed fifteen years of clinical practice as a registered nurse at St. Christopher's Hospital for Children in

Philadelphia. Ms. Leonetti received her Nursing degree from St. Joseph's Hospital School of Nursing and La Salle

University.

56

Mark Augusti CVP, President Orthopedics and Tissue Technologies

Mr. Augusti is responsible for the management of the Spine and Extremities divisions

which includes spine and extremity implants, orthobiologics and our tissue products. His

responsibilities include US commercial leadership, global portfolio management,

evaluation of corporate development opportunities and overall strategic direction. He

joined Integra in April 2014 as Corporate Vice President and President of Orthopedics

and Tissue Technologies, and brings over 25 years of executive management

experience in medical technology. Prior to joining Integra, Mr. Augusti served as Chief

Executive Officer at Bioventus LLC May 2012 to August 2013 and was a member of the

company's Board of Directors during the same period. Prior to that Mr. Augusti spent

nine years with Smith & Nephew April 2003 to April 2012 in a series of leadership roles, including President of Smith &

Nephew's Biologic Division, where he was appointed to lead Smith & Nephew's new biologics initiative. He also served

as Smith & Nephew's President of the Orthopedic Trauma & Clinical Therapies Global Business and Senior Vice

President and General Manager of the Trauma business. Prior to that, from 1987 to 2000, he spent 13 years at GE

Medical Systems, where he held various sales, marketing and strategic management roles, both in the US and

internationally. Mr. Augusti received his M.B.A. from the UCLA Anderson School of Management, and his B.S. in

Computer Science and Economics from Duke University.

57

John Mooradian CVP Global Operations and Supply Chain

John Mooradian is Integra’s Corporate Vice President, Global Operations and Supply

Chain. His responsibilities include global manufacturing and supply chain. Mr.

Mooradian was appointed Integra’s Corporate Vice President in December 2012. He

joined Integra in September 2012 as Senior Vice President, Global Operations and

Supply Chain. Before coming to Integra, Mr. Mooradian spent 24 years at Abbott

Laboratories in a series of leadership roles, including managing the Hematology and

Point of Care businesses and, more recently, worldwide operations at Abbott

Diagnostics Division, a $4 billion business with over 11,000 employees. Prior to Abbott,

Mr. Mooradian held several positions at General Motors. Mr. Mooradian received a B.B.A. degree in Management from the University of Texas, Arlington.

58

Paul W. Gonsalves SVP Enterprise Selling and Corporate Marketing

As Integra’s Enterprise Sales leader, Mr. Gonsalves is responsible for developing,

managing and executing Integra’s Enterprise Selling strategy. This includes strategic

key account planning, account development, executive-level relationship management

at specified key accounts and partnering with the cross-divisional and cross-functional

leadership teams to ensure the best possible service and communications to Integra’s

customers. Mr. Gonsalves also leads Corporate Marketing. Before joining Integra, Mr.

Gonsalves was the SVP/Chief Transformation Officer at AccentCare, Inc. He played an

integral role as part of a private equity group’s acquisition of this home health & hospice

company. He improved the business processes, created deeper collaborative bonds between both field and headquarters sales, marketing, and operational teams, and solidified their mission to develop

strong operating principles and processes. Prior to AccentCare, Paul was the VP & General Manager for Novartis

Pharmaceuticals Corporation’s Primary Care business unit with sales, marketing, and operational responsibility for the

US Additionally, Paul has held leadership positions in sales, marketing, and operations at WellCare Health Plans, GE

Healthcare and Siemen’s Medical Systems. Paul is a graduate of Rutgers University and holds a B.S. degree in

Business Management.

59

William Weber VP, General Manager Marketing & Product Development - Extremities

Dr. Weber joined Integra in July 2004 as a marketing manager for its Neurosurgery

Business. Before Integra, Dr. Weber spent a short period of time at Mutual of New York

as a financial advisor. Prior to being a financial advisor, Mr. Weber worked for ZS

Associates as a consultant. During this time he worked on sales and marketing strategy

for both device and pharmaceutical companies. Preceding ZS, Dr. Weber was a senior

staff engineer at Mobil’s Strategic Research Center in Paulsboro, NJ. While at Mobil

(and subsequently Exxon Mobil), Dr. Weber focused on the discovery and

commercialization of new petrochemical process technologies. Dr. Weber has a

bachelor’s of science degree in chemical engineering from Cornell University and Ph.D in chemical engineering from the

University of California at Davis. Dr. Weber also has a master’s degree of business administration from Columbia

Business School.

60

2014 Investor Day May 6, 2014

New York, New York

Appendix

61

$ In Thousands 2010 2011 2012 2013

COGS 268,188$ 299,150$ 314,427$ 327,045$

Non-GAAP Adjustments 9,498 21,611 22,881 24,846

Adjusted COGS 258,690$ 277,539$ 291,546$ 302,199$

Revenue 732,068$ 780,078$ 830,871$ 836,214$

Adjusted Gross Margin 64.7% 64.4% 64.9% 63.9%

Adjusted Gross Margin

$ In Thousands 2010 2011 2012 2013

SG&A 305,055$ 358,132$ 373,114$ 407,802$

Adj 9,424 37,420 23,669 30,255

Adjusted SG&A 295,631$ 320,712$ 349,445$ 377,547$

Revenue 732,068$ 780,078$ 830,871$ 836,214$

As a % of Revenue 40.4% 41.1% 42.1% 45.1%

Adjusted SG&A

Adjusted Gross Margin and SG&A Reconciliation

62

$ In Thousands 2010 2011 2012 2013

GAAP Net Income 65,669$ 27,989$ 41,204$ (21,067)$

Non-GAAP Adjustments (Total) 85,366 126,714 125,142 153,503

Adjusted EBITDA 151,035$ 154,703$ 166,346$ 132,436$

Revenue 732,068$ 780,078$ 830,871$ 836,214$

Adj EBITDA Margin 20.6% 19.8% 20.0% 15.8%

Adjusted EBITDA

Adjusted EBITDA Reconciliation

63

$ In Thousands 2010 2011 2012 2013

GAAP Net Income (loss) 65,669$ 27,989$ 41,204$ (21,067)$

Non-GAAP Adjustments (Total) 24,211 54,201 46,015 87,539

Adjusted Net Income 89,880$ 82,190$ 87,219$ 66,472$

Weighted average common shares outstanding for diluted net

income (loss) per share- - 28,416

Non-GAAP adjustment for dilutive effects of equity awards - - 386

Weighted average common shares outstanding for adjusted

diluted net income per share30,149 29,495 28,516 28,802

GAAP net income (loss) per diluted share 2.18$ 0.95$ 1.44$ (0.74)$

Non-GAAP adjustments detailed above (per share) 0.80 1.84 1.62 3.05

Adjusted net income per diluted share 2.98$ 2.79$ 3.06$ 2.31$

Adjusted EPS

Adjusted EPS Reconciliation

64

Free Cash Flow

$ In Thousands 2010 2011 2012 2013

Cash Flow from Operations 105,571 104,328 119,120 53,268

Capex (37,138) (38,425) (69,031) (47,851)

FCF 68,433 65,903 50,089 5,417

Shares Outstanding 30,149 29,495 28,516 28,802

Adj. Net Income 89,880 82,190 87,219 66,472

FCF/Share TTM 2.27$ 2.23$ 1.76$ 0.19$

FCF Yield TTM 76% 80% 57% 8%

FCF

65