panorama of the vod services in the european union andré lange, head of department for information...

Post on 20-Dec-2015

224 views

TRANSCRIPT

PANORAMA OF THE VOD SERVICES IN THE EUROPEAN UNION

André LANGE, Head of Department for Information on Markets and Financing

with the collaboration of Boris Chaleur, Florence Hartmann and Deirdre Kevin

2

CHALLENGES IN MONITORING THE DEVELOPPMENT OF ON-DEMAND AUDIOVISUAL SERVICES IN EUROPE

• Complexity of the technological possibilities

• Complexity of the business models

• Diversity of professional definitions

• Extreme fragmentation of the markets

• Extreme fluidity of the offers

• Absence sofar of national monitoring

3

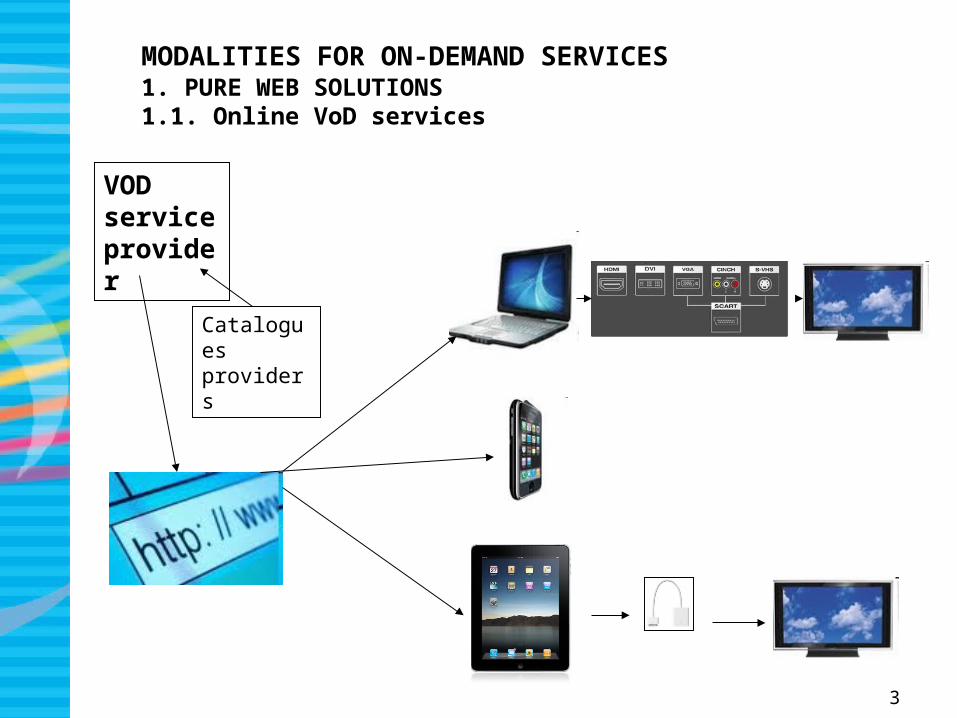

MODALITIES FOR ON-DEMAND SERVICES 1. PURE WEB SOLUTIONS1.1. Online VoD services

VOD service provider

Cataloguesproviders

4

PURE ONLINE VoD SERVICES IN THE EU 159 in December 2009 – 165 in June 2010 (not included : adults, catch-up TV, channels on video sharing platforms) Source : OBS

0

5

10

15

20

25

30

35

40

45

50

FR NL DE GB ES BE DK IT SE FI HU AT PL IE LU

Dec. 2008

June 2010

5

MARKET SHARE OF WEB VoD IN FRANCE IN

2009 (% of the total transactions) – Source : Gfk/CNC

Web VoD

IPTV

8,7 %

6

30 PURE WEB VOD SERVICES CLOSED SINCE DECEMBER 2008

7

SOME OF THE NEWCOMERS ON THE ONLINE VOD MARKET

8

MODALITIES FOR ON-DEMAND SERVICES : 1. PURE WEB SOLUTIONS 1.2. Channels in Video Sharing platforms

CATALOGUES PROVIDERS

UGC

9

INDUSTRY ON-DEMAND SERVICES IN THE FRAMEWORK OF VIDEO SHARING PLATFOMSNUMBER OF SERVICES : Not available

10

MODALITIES FOR ON-DEMAND SERVICES : 2. HYBRID SOLUTIONS : CAB-SAT TV + ONLINE CATCH UP TV

TV

CATCH UP TV

11

NUMBERS OF ONLINE SERVICESIN THE HYBRID CATCH UP TV OFFERS

June 2009 - Source : OBS

7

23

8

2 1

47

5 5 5

1

0

5

10

15

20

25

30

35

40

45

50

Canal+ à lademande

Canalsat à lademande

Viasat onDemand SE

Viasat onDemand DK

Viasat onDemand FI

Sky Player

Catch up

VoD catalogue

12

MODALITIES FOR ON-DEMAND SERVICES :2. OVER THE TOP SOLUTIONS (OTT) 2.1. iTunes Stores

iTunes Stores catalogues

Studios and networks catalogues

13

NUMBER OF FILM AND TV TITLES IN iTUNES

STORES CATALOGUES (June 2010) – Source : OBS

0

200

400

600

800

1000

1200

1400

1600

US DE FR GB IE

Films

TV programmes

14

NUMBER OF « NETWORKS AND STUDIOS »

CHANNELS ON iTUNES STORES – June 2010 Source : OBS

41

28

32 34

0

5

10

15

20

25

30

35

40

45

US

DE

FR

GB

15

MODALITIES FOR ON-DEMAND SERVICES :2. OVER THE TOP SOLUTIONS (OTT) 2.2. VideoGame consoles

STUDIOS

XBOX360

PSP3

WII

ZUNE MARKETPLACE

PSP VIDEOSTORE

16

ONLINE MOVIE STORES IN OPERATION IN EUROPE - June 2010

• Apple iTunes Store : GB, DE, FR, IE

• Microsoft Zune Marketplace : AT, BE, CH, DE, DK, ES, FR, FI, GB, IE, IT, NL, NO, SE

• Sony PlayStation Store : DE, ES, FR, GB

17

MODALITIES FOR ON-DEMAND SERVICES :2. OVER THE TOP SOLUTIONS (OTT) - 2.3. Stand-alone Set-Top-Box

23 CATCH UP TV SERVICES

18

MODALITIES FOR ON-DEMAND SERVICES :2. OVER THE TOP SOLUTIONS (OTT) - 2.4. Web-enabled devices (Blu Ray player, Home cinema, connected TV set)

19

FIRST ALLIANCES BETWEEN VOD SERVICES PROVIDERS AND MANUFACTURERS

20

CONNECTED DEVICES IN FRANCE, GERMANY

AND UK (2009-2014) Source : Screen Digest

0

2

4

6

8

10

12

14

16

18

XBoX PS3 StandaloneSTB

Blu Rayplayers

TV

2009

2014

21

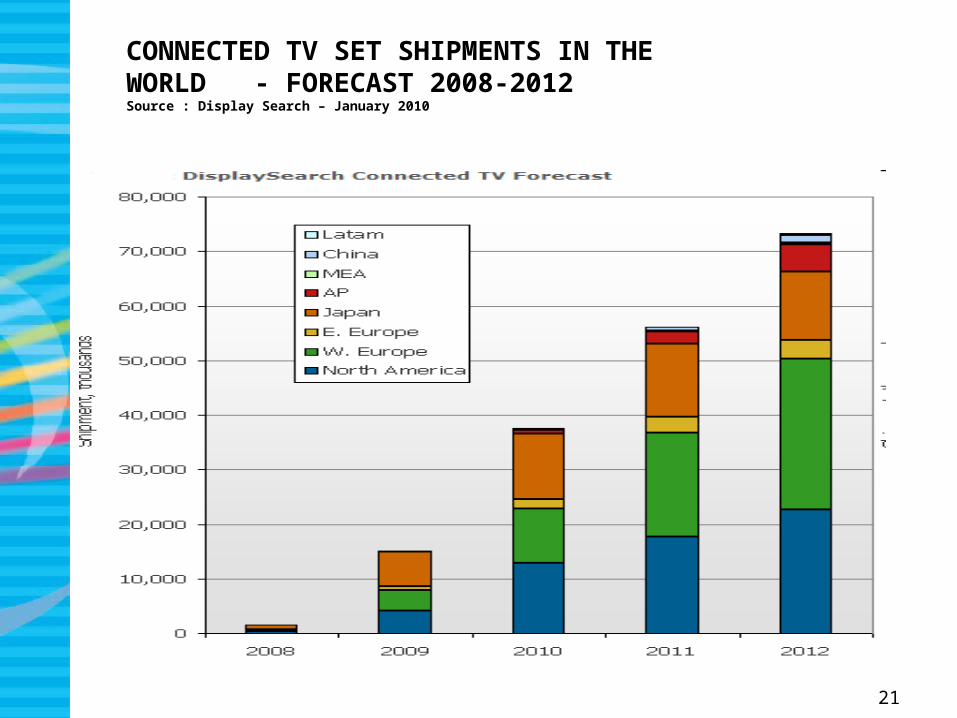

CONNECTED TV SET SHIPMENTS IN THE WORLD - FORECAST 2008-2012Source : Display Search – January 2010

22

FILM ON-LINE MARKET IN EUROPE (EUR MILLION) - GROWTH IN 2009 : + 89 % Source : Screen Digest

34,4

64,9

0

10

20

30

40

50

60

70

2008 2009

EUROPE

23

NEXT GENERATION OF OVER THE TOP SOLUTIONS : DIRECT ACCESS ON THE WEB TV SERVICES ON THE TV SCREEN

24

3. ON-DEMAND SERVICES ON TV DISTRIBUTION PLATFORMS3.1. IPTV 55 OF THE 88 IPTV OPERATORS IN THE EU PROVIDE AT LEAST ONE ON-DEMAND SERVICE

(December 2009) – Source : OBS

IPTV OPERATOR

OWN VOD SERVICE

THIRD PARTIES VOD SERVICES

CATCH-UP TV SERVICES

UGC

RADIO & TV CHANNELS

25

NUMBER OF IPTV OPERATORS IN THE EU PROVIDING n ON DEMAND SERVICES (Dec. 2009) – Source : OBS

33

28

11

3 2 1 13

01

5

0

5

10

15

20

25

30

35

0 1 2 3 4 5 6 7 8 9 >10

26

EXEMPLES OF MULTI-SERVICES OFFERS ON IPTV PLATFORMS

17 VOD AND 2 CATCH UP TV SERVICES

2 OWN VOD SERVICES AND 24 CATCH UP TV SERVICES

27

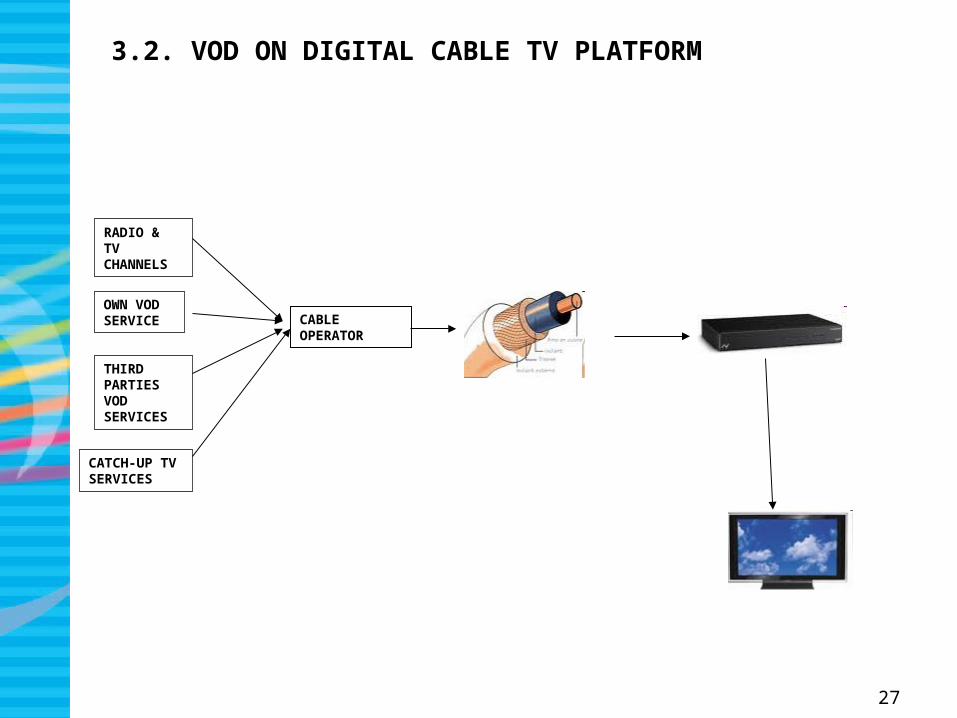

3.2. VOD ON DIGITAL CABLE TV PLATFORM

CABLE OPERATOR

OWN VOD SERVICE

THIRD PARTIES VOD SERVICES

CATCH-UP TV SERVICES

RADIO & TV CHANNELS

28

NUMBER OF ON-DEMAND SERVICES PROVIDED BY MAIN CABLE OPERATORS IN EU – June 2010 Source : OBS

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

15 1512

1

25

53

16

2

3 4 42 1

0

5

10

15

20

25

30

Catch up

VoD third

VoD own

29

3.3. PUSH ON DEMAND SERVICES BY SATELLITE OPERATORS : 6 PROPOSALS IN THE EUROPEAN UNION

30

3.4. PUSH ON DEMAND SERVICES THROUGH DIGITAL TERRESTRIAL TELEVISION

TOP UP TV

2008 : 23 catch up TV and 2 SVOD services

2009 : 1 catch up TV services and 2 SVoD service

MEDIASET PREMIUM

2010 : Premium on Demand

31

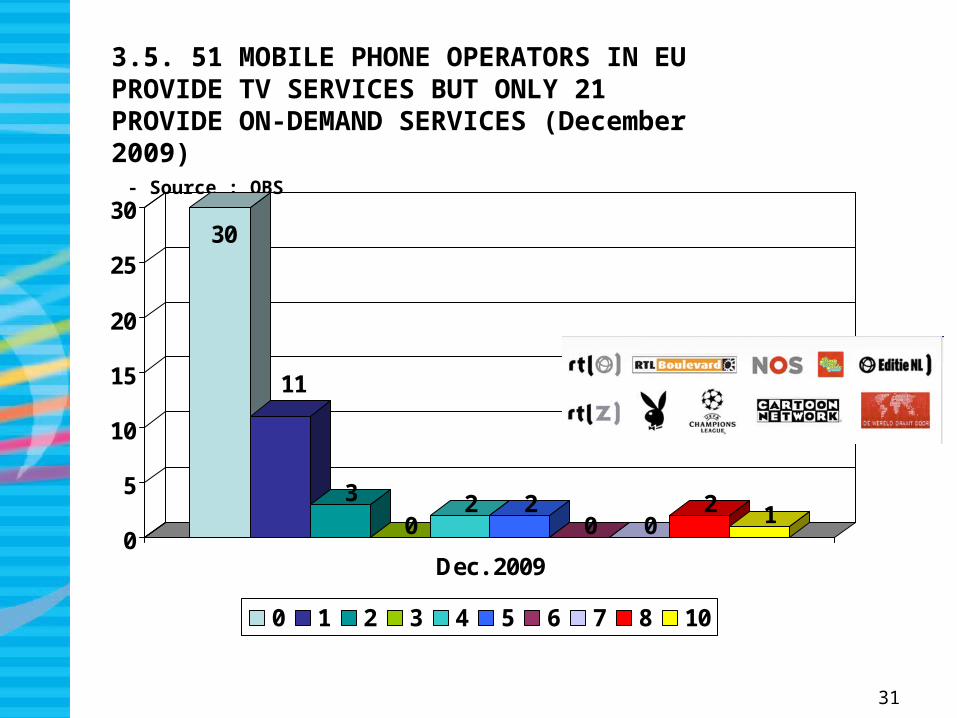

3.5. 51 MOBILE PHONE OPERATORS IN EU PROVIDE TV SERVICES BUT ONLY 21 PROVIDE ON-DEMAND SERVICES (December 2009) - Source : OBS

30

11

30

2 20 0

2 10

5

10

15

20

25

30

Dec. 2009

0 1 2 3 4 5 6 7 8 10

32

ON-DEMAND SERVICES ON MOBILE INTERNETFREE VOD : TRAILERS, NEWS, FREE CATCH-UP TV, PROMO OF PAY-VOD SERVICES,…

33

ON-DEMAND SERVICES ON MOBILE INTERNET : FREE VOD SUBSCRIPTION VOD OR CATCH-UP TV SERVICES THROUGH iPHONE APPS

34

ON-DEMAND SERVICES ON MOBILE INTERNET : PAY VOD SERVICES OUTSIDE OF THE APP STORE

35

ON DEMAND AND NVOD REVENUES (INCLUDING SPORTS) OF PROVIDERS IN EUROPE (2004-2008) - EUR million - Source : Screen Digest / OBS

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008

Online providers

DTT operators

IPTV operators

Cable operators

Satellite packagers

36

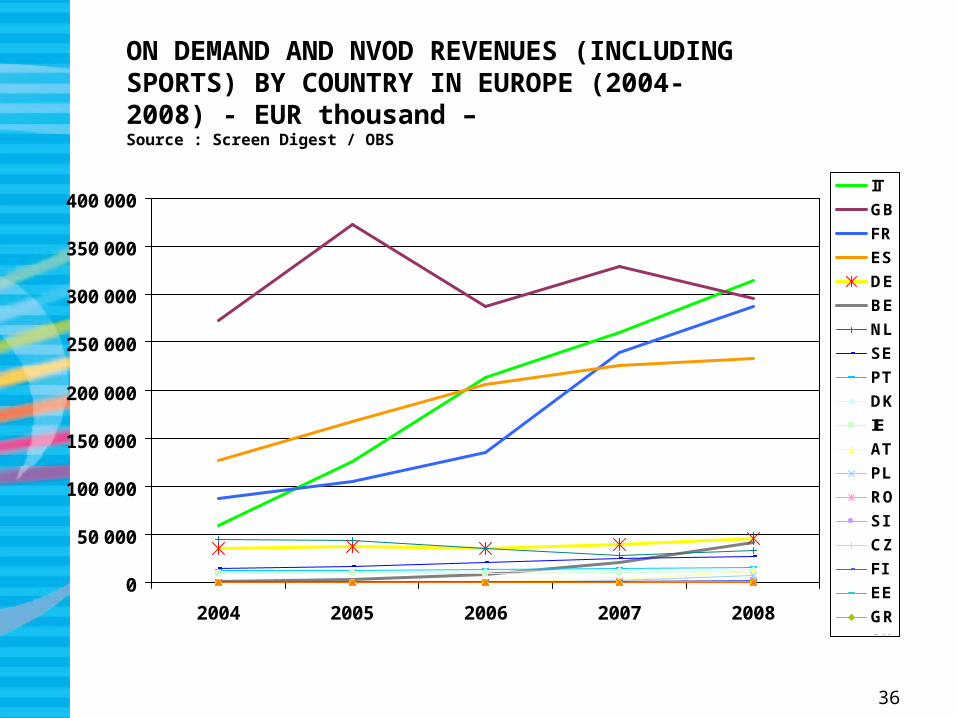

ON DEMAND AND NVOD REVENUES (INCLUDING SPORTS) BY COUNTRY IN EUROPE (2004-2008) - EUR thousand – Source : Screen Digest / OBS

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

2004 2005 2006 2007 2008

IT

GB

FR

ES

DE

BE

NL

SE

PT

DK

IE

AT

PL

RO

SI

CZ

FI

EE

GR

SK

LT

37

8 services provide monthly data - Orange (avril 2006)- Canal Play (mai 2006)- TF1 Vision (juillet 2006)- France Télévisions VOD (septembre 2006)- Virgin Mega (septembre 2006)- Arte VOD (octobre 2006)- Univers Ciné (janvier 2008)- Club Vidéo - SFR (janvier 2009)

Supply : monthly lists of film catalogues

Consumption : Breakdown according 2 criteria - origin of films- age of films

A MODEL OF MONITORING : THE CNC OBSERVATORY OF FILM VoD SERVICES IN FRANCE

3838

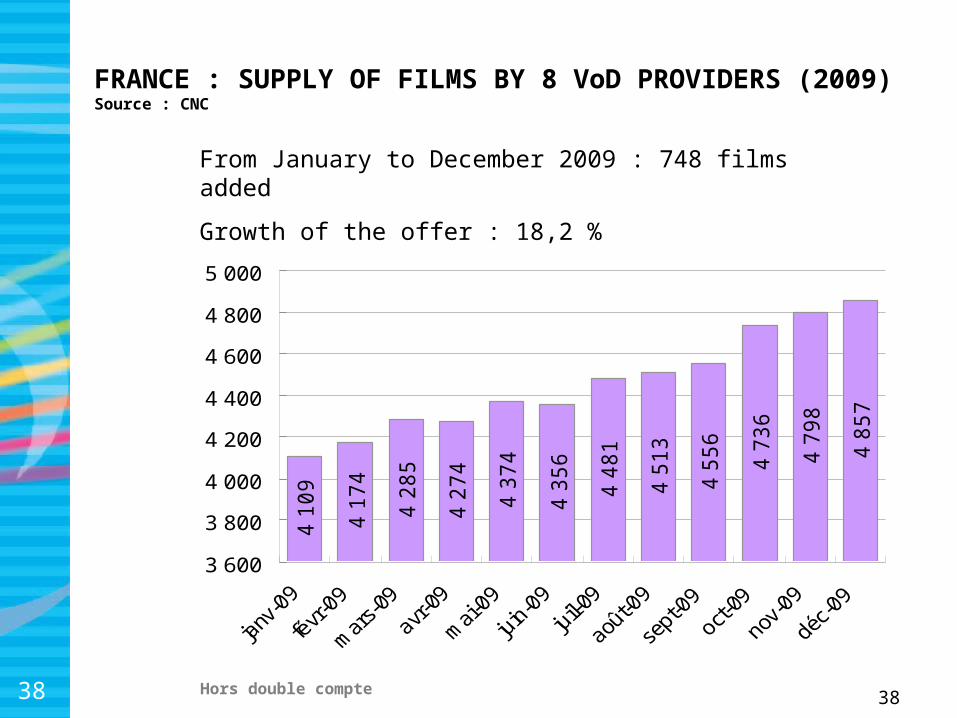

FRANCE : SUPPLY OF FILMS BY 8 VoD PROVIDERS (2009) Source : CNC

From January to December 2009 : 748 films added

Growth of the offer : 18,2 %

4 1

09

4 1

74

4 2

85

4 2

74

4 3

74

4 3

56

4 4

81

4 5

13

4 5

56

4 7

36

4 7

98

4 8

57

3 600

3 800

4 000

4 200

4 400

4 600

4 800

5 000

Hors double compte

3939

FRANCE – ORIGIN OF FILMS IN THE CATALOGUE OF 8 VoD SUPPLIERS (2009) – Source : CNC

December 2009 :

- 2 190 French (+ 23,7 %)- 1 665 US films (+7,9 % en un an)

France45,1%

US34,3%

Europe14,1%

Others6,5%

France43,1%

US37,6%

Europe13,7%

Others5,7%

January 2009 December 2009

40

• Feature films: 64,9 %• Adult films : 30,4 %• TV programmes : 4,7 %

FRANCE : BREAKDOWN OF THE TURNOVER OF 8 VoD PROVIDERS (2009) - Source : GfK / NPA /CNC

40

Source :

GfK/NPA

Films64,9%

Adult30,4%

Others0,3%Youth

0,7%

Music0,4%

Entertainment0,8%

Documentaries0,7%

Série TV 1,2%

41

•2009 :• French films : 30,9 %• US films : 58,6 %• Others: 10,5 %

FRANCE : MARKET SHARE OF FILMS IN THE TURNOVER OF 8 VoD PROVIDERS (2007-2009) – Source : GfK / NPA /CNC

41

Source :

GfK/NPA

0,0%

20,0%

40,0%

60,0%

80,0%

100,0%ja

nv-0

7fé

vr-0

7m

ars-

07av

r-07

mai

-07

juin

-07

juil-

07ao

ût-0

7se

pt-0

7oc

t-07

nov-

07dé

c-07

janv

-08

févr

-08

mar

s-08

avr-

08m

ai-0

8ju

in-0

8ju

il-08

août

-08

sept

-08

oct-0

8no

v-08

déc-

08ja

nv-0

9fé

vr-0

9m

ars-

09av

r-09

mai

-09

juin

-09

juil-

09ao

ût-0

9se

pt-0

9oc

t-09

nov-

09dé

c-09

FR US Others

42

CONSUMPTION ON THE TV SET IS THE KEY OF THE PAY-VoD MARKET

• Online market is relatively marginal

• In France 93 % of the film VoD turnover is realised on IPTV services

• In other countries, growing interest for the VoD set-top box (US exemples, Maxdome, Video Futur, Canvas project,…)

• Growing importance of the « Over the top » services

• Web-enabled TV sets : alliances between TV manufactures and VoD providers

• Hypothesis of an European equivalent of Google TV ?

• Regulatory question : monitoring the catalogues of services or monitoring the access to the distribution platforms for services promoting European works ?

43

NO AUTOMATIC LONG TAIL EFFECT IN FAVOUR OF THE EUROPEAN FILMS

• The « Long Tail » theory is reviewed by academic researchers

• Some pofessionnals argue that it was valid only in the first years of the Internet

• The French case does not demonstrate a proportion between offer and consumption of European/others films

• Almost no promotion policy by the operators sofar

44

TRANSPARENCY ISSUES FOR THE MARKET ANALYSIS

• Identification of the services and of the providers

• Catalogue analysis

• Potential audience of services : number of subscribers to distribution platform

• Households expenditures

• Companies revenues for on-demand services

• Analysis of revenues flows between distributors, providers of services and content providers

• Success of individual titles

• > Report Attentional on the implementation of article 3 and 4 of the TWSF Directive includes analysis on the difficulties of monitoring the VoD market

• > Need for an European regulation ?

45

THANK YOU !

• http://www.obs.coe.int