page 5beyondmarket.nirmalbang.com/issue73/download/magazine.pdf · the coalgate scam has dented the...

TRANSCRIPT

It’s simplified...Beyond Market 19th Oct ’12 3

DB Corner – Page 5

A Promising AlternativeNCDs offer high returns with moderate risks while offering investors the flexibility to choose between short and long tenures – Page 6

Easier Said Than DoneA lot needs to be done on the ground level for investors and companies to actually reap the benefits of the recently announced reforms in the airline, retail and insurance sectors – Page 9

Far-reaching ImplicationsThe Coalgate scam has dented the government exchequer and depleted a natural resource, the implication of which will be felt even after it is forgotten – Page 12

The Learning CurveE-learning is gaining popularity in India since it offers mobility and is equally interactive, making it a preferred choice of countless individuals – Page 15

Hanging PrecariouslyOnce regarded as a safe bet, companies from the consumer space too have taken a beating and are looking bleak at the moment – Page 18

Small Size, Big ImpactSmall and mid-sized hotels are benefiting from the shift in demand for premium hotels – Page 21

Seeking Common GroundThere is a need for guidelines on revenue recognition by real estate companies in the absence of a uniform method to compute the same – Page 24

A Proactive InterventionThe SC directive to the government on pharma pricing policy is an initiative in the right direction and is hoped to make drugs affordable to a majority of the Indian population – Page 27

Has Crude Oil Peaked Out For 2012?The recent drop in oil prices is more politically driven than fundamentally - Page 30

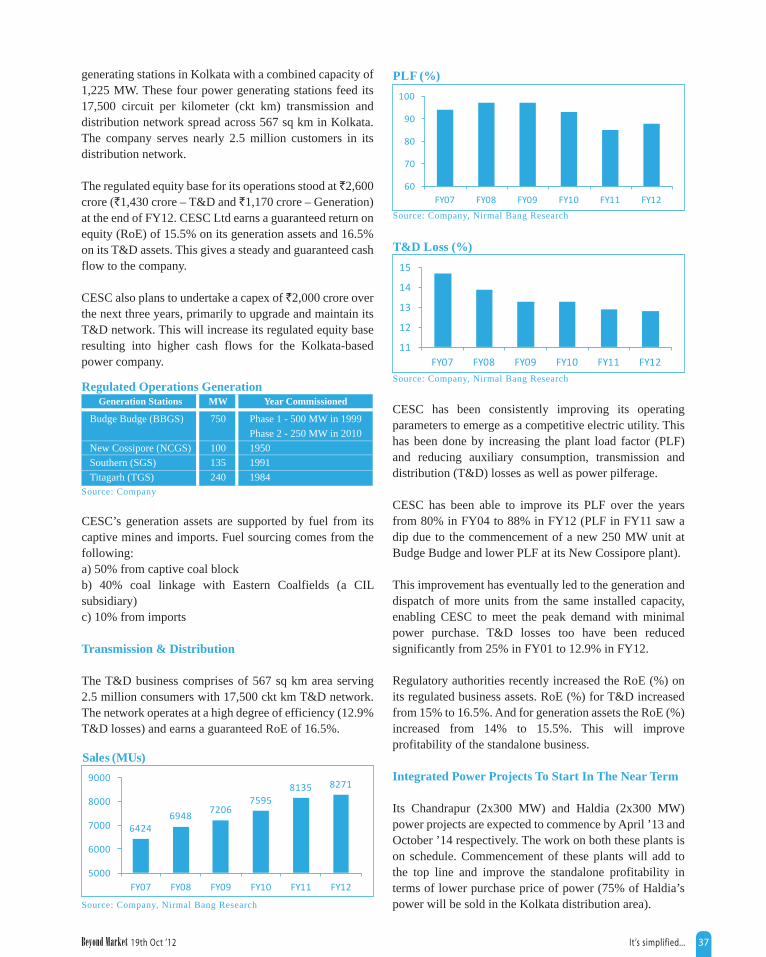

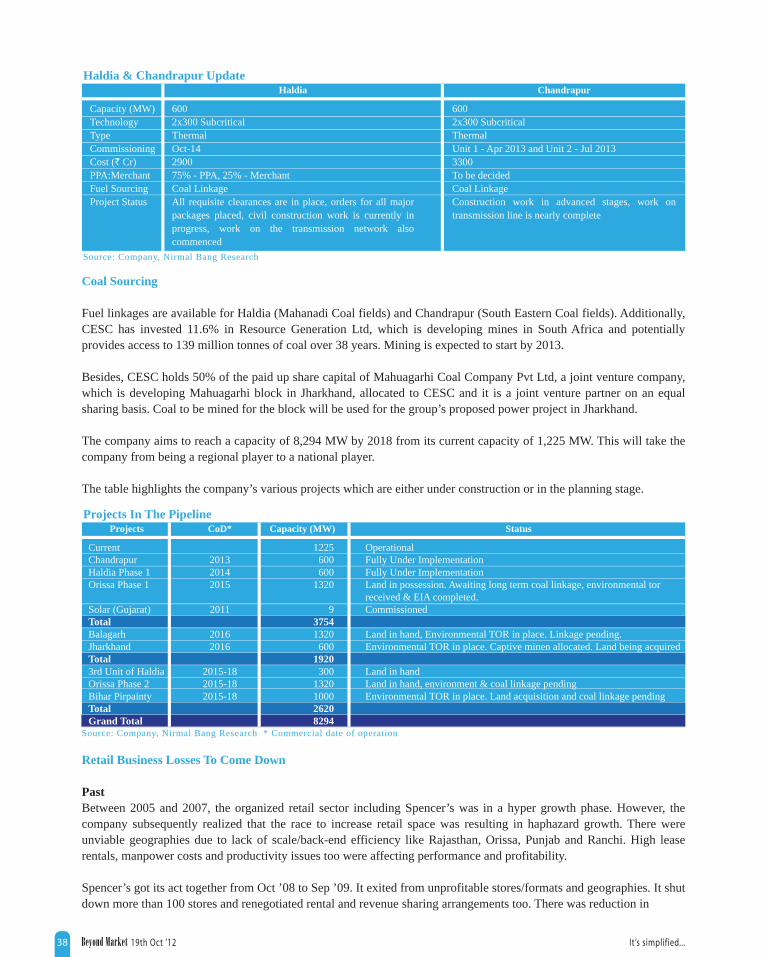

CESC Limited: Rise To PowerRegular tariff hikes, improvement in retail operations and commissioning or signing of power purchase agreement of the Chandrapur power project are likely to help CESC Ltd to grow in the coming times - Page 36

Theme Party On The BoursesThematic funds are doing well on the bourses and have given good returns to investors in recent times – Page 40

Muthoot Capital Services Ltd – Page 43

Technical Outlook For The Fortnight – Page 44

Indicators Of ChangeTechnical analysts use indicators to understand, interpret, predict, alert and/or confirm moves in the markets or individual stocks – Page 46

Volume 1 Issue: 73, 19th Oct ’12

Editor-in-Chief & Publisher: Rakesh BhandariEditor: Tushita NigamSenior Sub-Editor: Kiran V Uchil

Art Director: Sachin KambleJunior Designer: Sagar Padwal

Marketing & Operations:Divya Bhurat, Afsana Tamboli

We, at Beyond Market welcome your views, comments and feedback. Do help us to grow better as per your liking. This is our attempt to reach you better while crossing horizons...

Web: www.nirmalbang.com [email protected] No: 022 - 3926 8047

HEAD OFFICE Nirmal Bang Financial Services Pvt LtdSonawala Building, 25 Bank Street, Fort, Mumbai - 400001 Tel. 022-3926 7500/7501

CORPORATE OFFICE B-2, 301/302, Marathon Innova,Off Ganpatrao Kadam Marg,Lower Parel (W), Mumbai - 400 013Tel: 022 - 3926 8000/8001

Research Team: Sunil Jain, Vishal Jajoo, Kunal Shah, Somya Dixit, Dipesh Mehta, Anand Shendge, Manav Chopra, Vikas Salunkhe, Amish Pansuria

It’s simplified...Beyond Market 19th Oct ’124

Oil is considered to be the one of the most important commodities in each and every economy across the globe. Oil has assumed such great importance that no country in the world can survive without it and its byproducts. And a nation that does not have sufficient oil reserves to meet its domestic demand resorts to imports.

A large share of earnings of several economies comes from oil exports alone. Diverse usage, environment-friendliness, lower capital costs and higher efficiency are some of the advantages that oil has over other sources of primary energy.

It is therefore imperative to understand the importance and necessity of oil and our cover story does just that. Oil is one of the many commodities that have fallen in price the fastest despite growing tensions in the Middle East and the tightening sanctions on Iran. Oil prices have also fallen because of increased production of crude oil in the US. Through the cover story, we are trying to ascertain the reasons for the recent fall in oil prices and whether or not oil prices have peaked out. Traders and investors can take heart as our experts have also offered their outlook on this commodity for the near future.

We also have interesting articles like the advantages of investing in non convertible debentures (NCDs), the impact of the recently announced reforms in certain sectors allowing foreign direct investment (FDI) in them, the booming e-learning industry in the country and its future prospects, the surge in demand for small and mid-sized hotels as opposed to premium hotels that are losing their business, the Supreme Court directive on pharmaceutical pricing policy and the different technical tools used by technical analysts to understand as well as predict stock prices and their market movements, that will keep you riveted till the very last page of this edition of the magazinE.

Tushita NigamEditor

SAPPED ENERGY

It’s simplified...Beyond Market 19th Oct ’12 5

Disclaimer It is safe to assume that my clients and I may have an investment interest in the stocks/sectors discussed. Investors are required to take an independent decision before investing. Investment in equity is subject to market risk. Our research should not be considered as an advertisement or advice, professional or otherwise. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professional advice before investing.

he government has been on a reform overdrive since the past few weeks. It opened up key sectors

like retail, aviation and insurance by allowing foreign direct investment (FDI), deferred the General Anti Avoidance Regulation (GAAR), announced highway and road contracts under the engineering, procurement and construction (EPC) model as against the earlier model of build, operate and transfer (BOT) among a host of important announcements. All these measures lent support to the markets in the previous fortnight.

The markets were not only propelled by government intervention, they also

T got a boost from the appreciation in the rupee, which reduced the landed prices of a lot of imported materials, especially oil. However, inflation continues to be a major cause of concern since it is high due to the recent hike in petrol and diesel prices announced by the government.

Markets look good on declines. The upside on the index is likely to remain range bound. However, traders and investors can buy stocks at current levels or on declines around the 5,500 – 5,600 levels. Stocks like Cairn India Ltd (LTP: `334.65), Power Finance Corporation Ltd (LTP: `197.30), Rural Electrification Corporation Ltd (LTP: `217.30), Tech Mahindra Ltd (LTP: `944.75), Balrampur Chini

Mills Ltd (LTP: `71.55), Indiabulls Financial Services Ltd (LTP: `221.40) and CCL Products (India) Ltd (LTP: `299) look good from investment and trading perspectives.

In the coming fortnight, market performance is likely to be driven mainly by the quarterly results of India Inc. Also, the street will be eagerly awaiting the upcoming monetary policy review by the Reserve Bank of India (RBI) and see if this time around the apex bank will cut interest rates or noT.

Markets look goodon declines.

Nifty: 5,648Sensex: 18,577.70

(as on 15th Oct ’12)

A PROMISINGALTERNATIVENCDNCDs offer high returns with moderate risks while offering

investors the flexibility to choose between short and long tenures

It’s simplified...Beyond Market 19th Oct ’126

It’s simplified...Beyond Market 19th Oct ’12 7

SIMPLIFYING NCDs

The DNA of an NCD is that of a corporate bond. This means the company raises money from you and you in return earn regular interest as income against your investment.

These NCDs are listed on the stock exchange, which means you are free to trade in it like any other secondary market instrument. As an investor it is your choice to either accumulate more debentures or sell them before their maturity. The price of an NCD will depend mainly on interest rates.

Though it is a debenture, unlike other debentures you cannot convert it into equity at the end of its tenure. There are two types of NCDs that can be on offer. You can have a secured NCD or an unsecured NCD. Secured NCDs, as is evident from the name itself, is an instrument that has underlying assets that can be liquidated to repay holders of this security in case there is a problem.

An unsecured NCD on the other hand is a financial instrument that does not offer any such guarantee. Therefore, if something goes wrong, then the investor will not get back the investment. Understandably, this is a kind of instrument that carries a higher rate of interest.

NCDs may also come with a Put or a Call option. If a callable bond is issued it means that the issuer can exercise the option of redeeming the NCD before the end of its maturity term. This option is usually exercised if the company has issued an NCD when the interest rate was high, but the rate cycle changes eventually.

A put option works in the exact opposite manner. Here, the investor can choose to sell the bond back to the issuer at a stipulated price before the maturity term comes to an end. An

investor can choose to exercise this option if the interest rate rises after the issuance of the NCD.

An NCD may also be of different maturities and come with different options for payout. Some NCDs come with a maturity of three years while others have a maturity of six years or more. The interest payment also varies from three months to six months to an annual payment option. The rate of interest may also vary depending on such issuances.

WHAT TO LOOK OUT FOR

Interest rates may be the biggest incentive that draws an investor towards NCDs. However, as an investor there are certain things he/she needs to watch out for while opting for NCDs.

First and foremost the investor must look at the financial strength of the company. But looking at the profitability of the company is not enough. The investor should also check other factors such as sources of revenue of the company and whether the company has a diverse portfolio or it is majorly dependent on just one source. Since it is mostly NBFCs that are issuing NCDs now, also look out for the asset quality of the NBFC.

The asset quality of the company may be judged from its level of non-performing assets or NPAs. This is particularly relevant in case of gold loan NBFCs or companies that have a high exposure to sectors such as real estate, which is subject to volatility.

The credit quality of the company issuing an NCD may also be judged from the ratings it receives from credit rating agencies such as ICRA, CRISIL or CARE. All NCDs are assigned a rating before they make a debut and you can be assured of the safety or credibility of the company

ith the equity markets in a flux, investors are increasingly flocking towards the

fixed income segment. This is because debt instruments seem to be a safer option in such times.

Making the most of this trend, a number of companies are offering non convertible debentures (NCDs) to mop up funds from the market. NCD is a security that has loans as its underlying assets. It cannot be converted into a stock at the end of its tenure and usually carries a rate of interest that is considerably higher than a convertible debenture.

In the past couple of months, a host of companies (most of which were non-banking financial companies or NBFCs) such as Shriram Transport Finance, Shriram City Union Finance, India Infoline Finance and Religare Finvest have mopped up more than `2,000 crore from investors.

Two more NCDs – one from Muthoot Finance, an NBFC company that doles out gold loans and Kolkata-based Srei Infrastructure Finance are currently open for subscription and plan to raise another `650 crore.

The trend of launching NCDs may continue for quite some time as the equity markets and other asset classes seem to be inconsistent with their returns as of now.

Investors seem to be buying the bait of these companies that are offering high rates of interest in the range of 12% that beats not only equity returns but also that of bank deposits.

But does that mean you too should invest in NCDs? Let us delve into the details to find out whether or not NCDs can be a good investment option for you.

W

It’s simplified...Beyond Market 19th Oct ’128

and even a guarantee of the rate of interest if the NCD has received a high rating from such rating agencies.

But then again, don’t rely on the credit rating alone. It is a good idea to look at the financial statements of the issuer before you make a final decision on your investment.

TAX IMPLICATIONS OF NCDs

The most important thing that influences your investment decision is the tax implication on any instrument. You, therefore, need to keep in mind that the interest you receive as payments from an NCD is not tax-free in your hands.

The total interest that you earn in a year from an NCD is taxed according to the income tax slab you fall into. Therefore, if you are in the higher bracket of income, you will have to bear a cut of 30% on your returns. So, if you are investing in an NCD with a particular goal in mind, make sure that you know about the tax implications of the same.

ARE NCDs THE RIGHT THING FOR YOU?

For those who are in the lower tax bracket and want to earn or are looking for an opportunity to diversify their debt portfolio, NCDs are a good choice. However, financial advisors advise their clients to tread carefully where NCDs are concerned. This is because there are a large number of NBFCs that are making a beeline to raise money from NCDs and their underlying assets have always been a cause of concern in the financial world.

Adequate amount of research needs to be done before choosing an NCD, say experts. And the NCD should not exceed more than 10% to 15% of their overall exposure to debT.

It’s simplified...Beyond Market 19th Oct ’12 9

he ushering of new reforms in different sectors by the government, after a deep

slumber, is a welcome change. Capital-intensive sectors like airlines, retail and insurance had been grappling with low investment for years. But with the government allowing foreign companies to have

T

A lot needs to be done on the ground level for investors and

companies to actually reap the benefits of the recently announced

reforms in the airline, retail and insurance sectors

Implement

EASIER SAIDTHAN DONE

an equity stake in Indian companies from these sectors, there is some hope for them. But would this hope sustain for long? Sectororal experts believe that a lot needs to be done on the ground level for investors and companies to reap appropriate benefits of these reforms. This time we explore the impact of

these reforms in terms of its efficacy given the various challenges faced by these sectors. RETAIL At present the prospects of a foreign company investing in the retail sector is fraught with a lot of challenges. Currently, only nine states have

It’s simplified...Beyond Market 19th Oct ’1210

fund elections of local politicians within their states. Most experts believe that if foreign retail companies come into India, it may impact earnings of small kirana shops, which serve as an election-funding machine for local politicians. Hence, most states, it is perceived, would offer stiff opposition to this reform.

AIRLINES On the other hand, allowing foreign airline companies to buy a minority stake in Indian airline companies may not serve as a game changer for the airline industry as it would not address the systemic and operational challenges of the industry.

One of the biggest operational challenges in India’s strongly cyclical airline industry is the inconsistency in taxes, especially aviation turbine fuel tax, in various states. To begin with Jet Airways and Indigo Airlines would not have any foreign investments as they already have a strong presence of foreign promoters. Owned by Naresh Goyal, Jet has an 80% stake. Kingfisher Airlines, on the other hand, appears to be quite unattractive for a foreign player given its small market share, heavily leveraged balance sheet and resistance from lenders.

It makes sense for an international airline company to start a new airline with a local company instead of investing in a company neck-deep in debts. It has been observed in the past eight years that it is easy for a new carrier to gain 20% market share in five to seven years.

Not only its highly leveraged balance sheet, but also its loss of goodwill makes Kingfisher Airlines unattractive for a foreign partner. Spicejet and GoAir are the likely

contenders to benefit from the 49% FDI approval. Given these realities to start with, foreign carriers can opt for a 20% stake in airline companies.

SpiceJet, whose promoters recently invested `100 crore through the preferential allotment route, can strategically divest its stake to a foreign airline company. For investors, however, the steep rise in the stocks of airline companies offers an attractive exit. The stocks of SpiceJet and Kingfisher Airlines have appreciated more than 25% in the last one week.

Given high aviation turbine fuel prices and low passenger growth in recent months, there is hardly any trigger for these companies to demonstrate good financial performance in the coming quarter. INSURANCE Reforms in the insurance sector were long awaited. It is estimated that the limit for foreign direct investment in insurance is very high not only in BRIC nations but also in most Asian countries such as Japan, Korea, Indonesia and Malaysia.

In India though, FDI was restricted to a mere 26%, which the government recently increased to 49%. For investors and companies, this is a big leap and would provide a strong source of capital for the already loss-making insurance companies.

The implications of reforms can be best understood if one takes into consideration the nature of the industry. Insurance is a capital-intensive business. It is estimated that an insurance company would take 8 to 10 years to become profitable in India.

A company needs to invest heavily in

expressed their support to foreign direct investment in retail. And developing a consensus on the issue would be difficult in the near future. The clauses involved in channelizing investments will make it even less attractive for foreign investors.

For instance, the clause that foreign investors must invest at least 50% of their investment in back-end infrastructure in India seems to be quite a dampener.

Besides, Indian retailers will have to undergo a lot of restructuring and create special purpose vehicles (SPVs) for their businesses in the nine states in which FDI is allowed, which can take a while. Also, assuming that Indian retailers manage to get foreign partners would not ensure that businesses would turnaround. For instance, Walmart, the world’s biggest retail company, has been unsuccessful in other Asian countries such as South Korea, Japan and China.

It has already pulled out of South Korea and Japan. Although it has been in China for more than 12 years, it continues to make losses. Walmart and its peers - Carrefour and Tesco - have been cautious about expanding in China. This is reflected in its sheer market share, which at present stands at 12% in China’s retail sector.

Among Indian retailers, Pantaloon Retail will continue to show good financial performance than its peers - Shoppers Stop and Trent - given its slow growth, high inventory and leveraged balance sheet. A concern that weighs heavy on experts and investors is the perceived tacit involvement of local politicians in opposing the reform. It is perceived that most small retailers - kirana shops, to a very meaningful extent

It’s simplified...Beyond Market 19th Oct ’12 11

distribution, marketing and expansion of an insurance business. Hence, there is a long gestation period to turn profitable. It is estimated that India’s insurance sector needs a capital infusion of $10 billion to $12 billion in the next five years. The reforms are, however, expected to benefit private insurance companies, which had been bleeding since a while due to lack of funds, strict regulations and competition.

By allowing foreign companies to own an equity stake of 49% would provide the right amount of capital for growth. Providing a minority stake to insurers would check their commitment to the Indian markets. Presently, only 5% of the Indian population is believed to invest in insurance, with a large part of the investment coming in from urban areas and to a certain extent from Tier-II cities.

Hence, strong investments would lead to the emergence of best practices and innovative product offerings in the industry. These products can capture a vast section of the untapped population and meet the needs of various classes.

At present, 22 of 24 life insurance companies and 18 of 27 non-life insurance companies have foreign investment. With this reform, a new door would be opened for a plethora of foreign insurers, which have long-recognized the size and potential of India’s insurance industry. These reforms when implemented will offer new investment options to investors. However, a lot needs to be done by the government for the smooth execution of these reforms given the ulterior motives of middle men in the form of corporations and other agentS.

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENCY | MUTUAL FUNDS | IPOs | INSURANCE | DP# # #

QUALAT NIRMAL BANG, YOU’RE MORE THAN

JUST A BUSINESS ASSOCIATE,YOU’RE AN EQUAL PARTNER.

Contact Person: Gaurav Mohta - 07738380299 &Nilesh Sonawane - 07738380027

Address: B-2, 301/302, 3rd Floor, Marathon Innova,

O�. G. K. Marg, Lower Parel (W), Mumbai - 400013.

BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme-related document carefully before investing. Security is subject to market risk. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not offering for commodity segment. *Through Nirmal Bang Commodities Pvt. Ltd. #Distributors

Registered Office: 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400 001. Tel: 39268600 / 8601; Fax: 39268610, Corporate Office: B-2, 301/302, 3rd Floor, Marathon Innova, Off Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel.: 39268000 / 8001 Fax: 39268010

www.nirmalbang.com

We understand and value the equation of our relationships.

Which is why, we offer our sub-broker/authorized

person/remisier equal independence and status that our

partner merits.

That apart, we provide unparalleled knowledge and

exceptional market analysis to keep you ahead of the curve,

to the advantage of your customers.

After all, at NIRMAL BANG, it’s a relationship beyond broking.

FAR-REACHINGIMPLICATIONS

The Coalgate scam has dented the government exchequer and depleted a

natural resource, the implication of which will be felt even after it is forgotten

It’s simplified...Beyond Market 19th Oct ’1212

It’s simplified...Beyond Market 19th Oct ’12 13

many sectors till date and how its scarcity has impacted the growth of the concerned sectors. The coal sector in India is largely dominated by public sector undertakings. The CRISIL Coal Outlook research suggests that more than 90% of the coal produced in India in fiscal 2009 was produced by government-owned companies. According to a CRISIL Coal Outlook, coal met 52.4% of the total primary energy requirement of India in FY09. The research also suggests that non-coking coal off-take to the power sector was around 77% for power generation. Besides, the planning commission on the other hand highlights the importance of coal as an energy fuel.

In the Integrated Energy Policy 2006, the Planning Commission estimates that coal is projected to meet over 50% of the primary commercial energy requirement by FY32. Experts believe that known coal reserves are expected to last for over 80 years at the 2006 levels of production. However, there is a dire situation as regards availability of coal. More so, the situation also points to the very role coal as a fuel plays in the growth of the economy of a country. One of the reasons is that coal is used as an important input in the production and generation of power, cement and steel, among other things. THE AFFECTED ONES Energy remains a key input for metals and mining companies. For example, power costs account for almost 30% of the total costs incurred by companies while extracting aluminium from bauxite.

Manufacturers of steel, aluminium and allied products have been facing

two challenges pertaining to power supply. First is the availability of power and the second challenge is securing cheap power.

Power costs shoot up further if the miner does not have access to cheap options such as coal. Captive coal mines ensure guaranteed supply of power, which is a scarce input in most parts of India. And more importantly it is a cheap source of power, ensuring higher profitability for miners.

In many cases miners can put up a power generation facility and enter into power purchase agreements with state electricity boards (SEBs). Miners can sell extra power, if any, to state electricity boards. Such revenues enhance profits of the company and in tough times, can support their earnings. The logic naturally is bought by many established players in metals and mining sector along with some new companies in this sector. Bhushan Steel, Hindalco, Jindal Steel and Power, JSW Steel, Tata Steel, Hindustan Zinc, Sterlite Energy, Usha Martin, Monnet Ispat, Jai Balaji Sponge, Electrosteel Castings, Adhunik Metalics and Tata Sponge are some of the companies from the metals and mining sector, which may be impacted adversely. Cement is another sector where the requirement of coal block is very crucial. As energy bill is a major expenditure head for cement manufacturers, they prefer a captive power plant which is run on coal. In case of suspension or cancellation of the coal blocks, Ultratech Cement Ltd, Grasim Industries Ltd, Birla Corporation Ltd, Ambuja Cements Ltd would be affected. As regards the power sector, it must be noted that coal-fired thermal power stations constitute a major

I ndian equity investors were waiting for an influx of measures, policies and directives that would help

revive the country’s coal industry. But what ensued is a lesson in ‘equity investments and policy shocks’.

The Comptroller and Auditor General of India in its report commented that the policy adopted for coal block allocation by the government of India has resulted in windfall gains of ̀ 1.86 trillion for companies that were rewarded 57 coal blocks.

Opposition parties have been demanding the resignation of Prime Minister Manmohan Singh on account of the ‘coalgate’ scam. Meanwhile, beneficiaries of the coal blocks may not enjoy peaceful possession of the coal blocks. The government’s stance on the coal blocks is yet not clear and there is a possibility of a policy U-turn. There are certain possibilities that investors have to take into consideration in this situation if the government gives in to the pressure from the opposition. First, the government may ask for extra royalty or some other way to have an extra share of profit from the beneficiaries. Second, the government may cancel all allocations and go for competitive bidding altogether.

And third, the government may go back to nationalization - handing over all the coal blocks to Coal India. Whichever way it goes, it will have a serious impact on metals and mining as well as the cement and power generation sectors, among other industries in the country. This time we explore how the coal industry in India has evolved in the last 40 years and how coal continues to be scarce and an important fuel for

It’s simplified...Beyond Market 19th Oct ’1214

chunk of power source in India. A number of corporate entities have quoted aggressively for ultra mega power projects.

Low per unit cost of power bid by winners in ultra mega power projects was based on the simple assumption that there will be a captive coal block in some cases. Tata Power, Lanco, CESC and Navabharat are some companies that are likely to be affected by the alleged coal scam.

These companies are seen as the direct victims of the possible cancellation of the coal blocks by the government. However, there are certain businesses that may be impacted, although indirectly, by this scam. Material handling companies may see cancellation of orders placed by these companies.

An important point to note is that no material handling company is dependent on these companies for its very existence. The impact is likely to result in moderate growth estimates.

Some equipment finance deals too may be cancelled, resulting into a minor impact on equipment financing business of banks. Though this is negligible, one cannot ignore it.

THE WAY AHEAD At a time when imported steel from China is giving Indian steel manufacturers sleepless nights, increased energy costs is adding to the woes of these companies. Some of the allocated coal blocks are yet to operate at full capacity due to factors like inability to raise funds to support operations, delayed environmental clearances and geographical locations in naxalite areas.

In the due course, the government may allow companies to continue with their operations where the project has achieved certain minimum operational levels and cancel the rest of the blocks. In such a scenario, it is better to look at each of the blocks individually. This of course will take some time.

Whatever be the case, the cost of energy is expected to go up. This will be inflationary in nature. For most industries, be it manufacturing or services, power is a critical input. In the medium term, this should be detrimental to corporate earnings. The only entity that may benefit from the alleged coal scam is Coal India, that is, if the government chooses to

cancel the coal block allocation and hand over all the blocks to Coal India.

There is a possibility that another public sector undertaking like the National Thermal Power Corporation could also benefit from the reallocation of the coal blocks.

The coal scam will adversely impact the ‘investment-capex’ cycle of Corporate India. The entire issue is a classic example of how a U-turn in policy framework can materially impact the corporate strategy and investors’ returns.

A policy action initiated a decade ago has started playing against all investments undertaken by the stakeholders, including corporations. Hence, it is very important that policies are implemented instead of being framed. Policy changes, affirmative action by the government are welcome.

But policy stability is the need of the hour, feel industry insiders. It is time to think about the next century and not about the next five-year plan. Otherwise more and more such policy irregularities could hit unsuspecting victims in the long ruN.

Contact - Daisee Boga: +91-22-39268244, 7738068289

E-learning

t is astonishing but true. India has the world’s largest population in the age group of 0-24 years. Therefore, it should come as little surprise to anyone that India is also home to one of the top 10 education markets in

the world, valued at around $100 billion.

What’s more, the revenue growth in the sector is one of the fastest in the world with the education spend growing at a median rate of 15% every year since 2000. The education sector is attracting entrepreneurs and investors from all over the world, leading to a massive expansion of private institutes

I

TheLearningCurve

E-learning is gaining

popularity in India since it

offers mobility and is

equally interactive,making it

a preferred choice of

countless individuals

It’s simplified...Beyond Market 19th Oct ’12 15

It’s simplified...Beyond Market 19th Oct ’1216

EDUCOMP SOLUTIONS LTD

Educomp is one of India’s oldest and leading companies in the e-learning segment. The company was started in 1994 and in the beginning it dealt with setting up and maintaining computer labs in schools.

However, in 1998, it took another route and launched eCampus, which was an online student information system. In 1999, it started its first education portal and called it planetvidya.com.

The year 2000 was important for the company as in June that year, US-based investment company Carlyle invested $2.10 million for a 15% equity stake and later on 18th September Educomp became a public limited company.

With the aim of turning an entire classroom into a technology-enabled classroom, it came up with SmartClass, a highly successful multimedia educational product.

After the year 2006, the company expanded its horizon by acquiring a 51% stake in US-based portal learning.com, signing an MoU with Raffles Institute Singapore, acquiring a 51% stake in Takshita Management and entering into a joint venture with Pearson to support vocational learning in India.

CORE EDUCATION & TECHNOLOGIES LTD

Formerly known as Core Projects and Technologies Ltd, Core Education was founded in 2003 as a low-end IT-service provider, which after 12 acquisitions in six years, turned into a high-end education–service provider.

The year 2005 was an important year for Core as it entered the US market with the acquisition of the first US

product company, ECS. Between 2005 and 2008, it acquired 9 companies and businesses with over 100 clients. Currently, the company has business operations in 3 continents and it provides integrated ICT solutions, end-to-end management of government schools and vocational training of government staff. The key alliances of Core Education are the University of Oxford, IGNOU, nationteacher.org and NASA.

EDSERV SOFTSYSTEMS LTD

EdServ was formed in 2001 as a private company known as Lambent Softsystems Pvt Ltd, which in 2008, was re-christened as EdServ Softsystems Ltd. On 5th Feb ’09, Edserve went for an IPO.

During the first two days of the IPO, EdServ received lukewarm response from investors as CARE assigned an IPO Grade 1 to EdServ IPO. However, it got oversubscribed by 1.3 times by the end of the IPO.

Before entering the online education sector, EdServ was focused on IT training and placement solutions. But after the IPO, it acquired many online education companies such as 2tion.com, SchoolMate, SmartLearn WebTV and Sparkling Mind, among others. EdServ now offers coaching for competitive exams, IT courses for graduates and post-graduates, vocational skills training and online ERP training for schools.

EVERONN EDUCATION LTD

Everonn Systems India Ltd, incorporated on 19th Apr ’00 as a public limited company is a pioneer in satellite-based education delivery through the VSAT platform.

In the same year, that is, in 2000 the

in the last 5-6 years. According to estimates, India’s private education industry is expected to grow from $30 billion currently to $45 billion by the end of 2015.

The education sector can be broadly divided into segments like formal education, parallel education and ancillary education.

The formal education sector comprises schools, colleges, universities and professional education. Parallel education is a complementary segment to formal education, comprising private tuition, exam preparation, skill-oriented vocational institutes as well as corporate training.

The formal education system is heavily regularized in India, whereas the parallel education sector is virtually outside the scope of any regulation or supervisory system.

The regulations act as a deterrent to investors in the formal education system, which has led to a rapid growth in the parallel education system primarily through e-learning.

Students prefer this model because it saves time and they can learn at their own pace in the comfort of their homes. E-learning has become so popular that even corporate India is using it to train their employees thanks to the potential and effectiveness of this platform.

The e-learning segment is growing at a fast pace of about 27.9% since the last three years. About 100 new e-learning companies have started in the last three years, taking the total number of e-learning companies in India to over 140.

Following are few of the leading companies in India that provide e-learning products.

It’s simplified...Beyond Market 19th Oct ’12 17

company was awarded a contract for computer education of 332 government schools in Tamil Nadu by the state government of Tamil Nadu. Later, in 2002 it partnered with HughesNet Global Communications Ltd to bring management courses from premier business schools.

Everonn is also the first company to provide education through mobile phones in the country. In 2011, it sold a 12% stake to Dubai-based Varkey group (GEMS education) through preferential allotment.

Currently, Everonn offers education from pre-school to professionals in over 1,400 schools, 1,900 colleges and 50 retail centers. It has also entered into a JV with the union government’s Nation Skill Development Corporation (NSDC) with a target to train 15 million people in various technical streams over the next 10 years.

TATA INTERACTIVE SYSTEMS

A part of the $83 billion Tata Group, Tata Interactive Systems (TIS) was founded in the year 1990 and became the first company in the country to develop a Computer-based Training (CBT) product.

Since its formation, it has won several awards and certificates worldwide, notably, gold at British Interactive Multimedia Awards (1997), SEI CMM Level 5 certification (2001), SEI P-CMM Level 5 certification (2003) and also Brandon Hall Excellence in Learning, APEX, BETT, BIMA, and Business World -NID Design Excellence awards. It is the only e-learning organization in the world to receive level 5 from both SEI CMM and SEI P-CMM.

As of now TIS offers multimedia educational products, consulting services, electronic performance

support systems and training outsourcing services for corporates, schools, universities and government institutions worldwide by creating about 3,000 hours of e-learning content annually.

CAREER POINT LTD

A well known name in the area of competitive exams in north India, Career Point is also using internet technology for expansion. In the year 2008, the company test launched its e-learning system known as TechEdge class. Using the VSAT technology, these e-learning classes are conducted in schools as well as centers where it is not economically feasible for the company to set up full-fledged classrooms.

There are several reasons for the boom in the e-learning market. Cost effectiveness is the primary reason. The investment required for this model is very low and comes at very high margins (as high as 80%). The companies face fewer barriers while entering into the online market.

Earlier, low penetration of broadband was one of the major drawbacks for the e-learning model. However, after the initiatives undertaken by the government of India, the penetration has increased and a large number of students can now access the Internet.

According to the status report on broadband by the Department of Telecom (DoT), 62 gram panchayats will be connected with fibre optics by 15th Oct ’12.

After the completion, various activities including e-learning, tele-medicine and skill development will be tested and based on the outcome, the process of laying of optical cables across the country will start. The government is investing `20,000 crore in the project which

will connect 160 million Indian households with high speed internet as compared to the current figure of 10.3 million homes.

The government has also launched two schemes – National Mission on Education through Information and Communication Technology (NMEICT) And National Program on Technology Enhanced Learning – to promote learning through videos and web-based courses.

Many organisations such as Centrum Learning as well as Tata Interactive Services are being set up using the public-private partnership model.

Moreover, with the changing face of technology, companies are moving towards delivering educational products through platforms in the 3G environment using devices such as tablets and mobiles.

For mobiles, Ericsson is developing a learning platform where the course material for IGNOU can be downloaded. Educomp has formed a joint venture with US-based Zeebo to develop an education platform for school children where they can access course material via 3G network.

The government of India in an effort under NMEICT has formed an alliance with HCL Technologies to launch a tablet called Sakshat. The tablet is said to be the world’s most inexpensive tablet and is aimed to help connect 25,000 colleges and 400 universities across the country as part of the scheme.

It has been a long journey for e-learning companies. But considering the demand for education and the initiatives taken by the government to expand the coverage of e-learning, the future of the e-learning industry in India only looks bright from herE.

HangingPrecariouslyOnce regarded as a safe bet, companies from the consumer space too have taken a beating and are looking bleak at the moment

It’s simplified...Beyond Market 19th Oct ’1218

It’s simplified...Beyond Market 19th Oct ’12 19

CHANGE IN GUARD

Earlier investors and fund managers used to accumulate defensive names and stocks from the consumer space instead of high beta stocks or stocks which were considered risky, as many believed the former would continue to do well owing to structurally sustainable demand and relatively better balance sheets despite economic concerns.

Also, the valuations of stocks from the consumer space touched historical highs as many of them began trading at 35 to 50 times their earnings.

At such a time (almost two months back), most high beta and cyclical stocks were trading at single digit price to earnings multiples owing to economic concerns.

However, this trend is changing for consumer stocks now as not only demand side issues but also valuations in a number of cases have started reversing the positive view of this sector.

As against consumer stocks, cyclical stocks are more depressed at present. A number of cyclical stocks are trading much below their historical low valuations.

And if there are cuts in interest rates and a revival is witnessed in capex, then cyclical stocks will be the first to get rerated and start moving compared to consumer stocks.

In fact, we have already seen rerating of cyclical stocks on the back of reforms announced by the UPA government recently.

In this context, consumer stocks face the risk of diversion or shifting of trades in favour of high beta and cyclical stocks, leading to price erosion of the stock.

Cyclical stocks or companies from sectors like metals and construction, among others, are largely influenced by the ups and downs in a country’s economy. On the contrary, the consumer space is considered relatively stable.

Moderation in the industrial sector also leads to a slowdown in the consumer space. Moreover, the impact of the slowdown could be huge if the slowdown in the industrial space occurs along with a decline in the agricultural sector.

In fact, economists are now expecting a negative GDP growth in the agricultural sector. In the current context, both industrial as well as agricultural growth have come down in India.

Add to this, the exports market is quite weak at present, which in totality is hurting consumer sentiments and their incomes, especially since costs have increased but incomes have remained the same, in an inflationary environment.

Jobs are few and employers are leaving no stone unturned to cut corners by slashing jobs as well as salaries. This situation could have been salvaged if there was no delay in monsoons and the resultant deficiencies were met on time. Not to be left behind, the rural population is also feeling the pinch, increasing the slowdown in the consumer space.

SHORT-TERM PAIN

According to the official data released recently, the April-June GDP or gross domestic product grew 5.5%. But this figure is not desirable given the fact that India has witnessed growth in excess to 7% to 8% in the past.

Unlike manufacturing data, the slowdown in the services sector was

he domestic economic slowdown which was largely restricted to capex and investment-led sectors

like power, infrastructure as well as other heavy engineering sectors, is now seen impacting the consumer space too.

Certain indicators from both the discretionary and non-discretionary spending sides signal a moderation in consumer demand.

Volume growth for companies from the consumer space, particularly those involving discretionary spending on products from the lifestyle, jewellery and fast food segment has also come down drastically.

The fall can be gauged from the decline in footfalls at listed companies from the retail sector. According to the first quarter results of FY12, same-store sales for Jubilant FoodWorks Ltd grew at 22.3% as against 36.7% last year.

Similar was the case with Pantaloon Retails as it recorded a 4.7% growth in same-store sales in the lifestyle segment as compared to 11.4% growth a year ago.

Even watch and jewellery maker Titan reported a 21% decline. Shoppers Stop reported a 1% growth as compared to a 7% growth in the corresponding period last year.

Apart from the retail sector, even the services sector as well as the automobile sector, particularly the two-wheeler segment saw a drastic fall in sales.

All these things clearly indicate a slowdown in the consumer space, which used to be regarded as a safe spot by investors and money managers while dealing with volatility in the markets.

T

It’s simplified...Beyond Market 19th Oct ’1220

surprisingly higher at 6.9%, the slowest pace since Q4 FY09, reflecting the slowdown in growth in the private sector, exports as well as the IT sector. Leading rating agency CRISIL in a media release said, “Given the weak global economic environment and deficient monsoons, GDP growth is expected to remain subdued over the remaining quarters of this fiscal as well. We, therefore, expect GDP to grow at 5.5% during FY13.”

It also added that swift policy action to solve issues related to mining, land acquisition and speedy clearance of projects can create an upside to the growth projection.

Policy action by the government, conducive global economic environment and benign interest rates are the three important initiatives that everybody is seeking as these could propel economic recovery. However, there is not much clarity or action on these fronts.

Due to policy inaction and inordinate delays, demand slowdown, particularly in the consumer space, which had begun moderating, could intensify in the coming months. This will certainly have a bearing on the discretionary and non-discretionary spending in the consumer space.

For instance, in fiscal year 2011, two-wheeler and four-wheeler sales grew 25.8% and 29%, respectively. However, the same is expected to witness a single digit growth in the current financial year.

Importantly, the magnitude of the slowdown is only visible in the month of June and August ’12, which means that the financial impact on the companies from this sector will only be visible with a lag effect in the coming quarters.

LONG-TERM GAIN

If a nation’s economy is going through a difficult phase, then it is bound to impact demand, which will subsequently put pressure on companies in the near term.

While this may require investor attention in the near term, they should not vitiate their views about the long-term opportunities in the consumer space. The slowdown in the economy notwithstanding, India’s long-term economic fundamentals look strong.

India has the ability and the potential to grow higher in the long run given the structure of the economy as well as its demography.

This is also the reason why investor and money managers are keen on being optimistic about the consumer space, even as consumption takes a back seat in the near term due to high valuations and demand issues.

The reasons for the same are aplenty. First is the demography of the country. India accounts for about 16% of the world’s population but hardly contributes to the GDP.

Its vast consumer base, untapped markets and structural changes like level of education, infrastructure, urbanization, working population, communication as well as rising income levels, among others, could have a glaring impact on demand in the long run.

The impact of these drivers has already been felt in the last few years. The per capita income in India has risen from around $450 in the year 2000 to about $1,200 per person currently. This is almost a three-fold increase in the per capita incomes of people in the country.

Not only this, even huge investments undertaken by the Indian government as well as the private sector had quite a major impact on demand across most sectors.

Companies involved in the business of jewellery, FMCG, footwear, food, clothing and several others, from this space have benefitted immensely. However, if estimates and future potential in the consumer space is to be believed this could just be the beginning for them.

THE SLEEPING GIANT

According to consulting firm McKinsey & Co, India’s middle class population, which was around 50 million in 2005, is likely to move up by almost 12 times or nearly 583 million by the end of 2025.

Also, the number of people in the annual income category of `10 lakh will jump four-fold to about `18 million by 2020 from the present count of 4.4 million.

Further, the company projects that with the rise in income, about 290 million people will move from poverty to the higher income group.

The per capita income in the country is expected to move up from the current $1,200 per person to $3,200 -$3,500 per person by the end of the year 2020.

The rise in income levels, coupled with shift of mass consumers into high income categories will mean more opportunities for companies in the consumer space.

There will be more demand for discretionary and non-discretionary products fuelled by increase in education levels, urbanization, working class as well as a humungous young populatioN.

SMALL SIZE,BIG IMPACT

he global economic slowdown had a cascading impact on a number of sectors. And the hospitality industry was no

exception. However, the premium hotel segment has had to bear the maximum brunt of the financial meltdown.

Decline in occupancy rates and room rates shrank their operating margins and pushed costs, adding pressure on the already burdened segment.

Premium hotels derive a substantial part of their revenue from foreign tourist arrivals. But their numbers have dwindled due to the slowdown in the US and Europe.

In the last five calendar years beginning 2007, foreign tourists’ arrivals grew at a Compound

TSmall and

mid-sized

hotels are

benefiting

from the shift

in demand for

premium hotels

It’s simplified...Beyond Market 19th Oct ’12 21

It’s simplified...Beyond Market 19th Oct ’1222

levels by providing luxury services at affordable rates. This was not the case in FY09 as the occupancy rate at mid-sized hotels was 50%. However, businesses gained momentum and occupancy rates grew to 65% to 70% later on.

Increased occupancy rates also boosted cash flows from operations of small and mid-sized hotels. Bhagwati Banquets & Hotels is one such example. Its cash flow from operations grew at a CAGR of 79% to `26.78 crore as of FY11, in the past four fiscals.

While the cash flow from operations of a large and premium hotel like Hotel Leela Ventures was 22% in the last four fiscals. Also, EIH and Indian Hotels could not match up to the growth of mid-sized hotels.

HARD LUCK

In addition to this, small and mid-sized hotels saw better growth since most international operations of large-sized hotels are either making losses or are in the break-even stage. Indian Hotels has five hotels spread across the US, UK and Australia.

The company’s subsidiaries, which include its international hotels business, showed a net loss of `245 crore in FY11 as against a loss of `265 crore in FY10. This has pulled down their performance in the last few years and they continue to make losses even now.

Also, EIH, which has hotels in the Middle East, Egypt and Indonesia, made losses due to the crisis in the Middle East.

Mid-sized hotels, on the other hand, continue to depend on domestic travellers who are increasingly spending and vacationing. Take for instance Oriental Hotels. Its revenues

grew at a CAGR of around 30% in the past four fiscals when most large-sized and premium hotels are witnessing a single-digit growth in their revenues.

BUSINESS OPPORTUNITY

Sensing business opportunity, most international hotel companies have entered into joint ventures with small and mid-sized hotels in recent years. The Intercontinental Hotel Group, for instance, has signed a joint venture with Duet Hotels, a mid-sized hotel to launch the Holiday Inn brand.

Also, international hospitality chain Starwood Hotels & Resorts plans to open 15 hotels and has spelt out its keen focus on tapping the mid-market segment to expand.

Back home, on the domestic front, even the segment leader Indian Hotels has allotted 48% of its hotels inventory in the mid-market and the budget hotels segment for the next 2 to 3 years.

GOING FORWARD

It is estimated that the operating profit margins of premium hotels would be under pressure in the next two fiscals given the strong pipeline of rooms and reduced foreign tourist arrivals.

In the last five years, the operating profit margins of premium hotel companies like Indian Hotels, EIH and Hotel Leela Ventures have almost halved. The operating profit margin of Indian Hotels declined from 34% in FY08 to close to 17.9% in FY12. Going forward, however, there would be an excess supply of rooms in 14 key cities in India, which would put pressure on the operating profit margins of premium hotel companies.

According to research firm CRISIL,

Annual Growth Rate (CAGR) of 4.12% as against a CAGR of 13.2% in the preceding five years, ending 2007. This led to a huge decline in occupancy rates at premium hotels. The occupancy rate at The Indian Hotels Company dropped to 66% at the end of the December ’11 quarter from 73% in FY08.

Owing to the global economic slowdown, coupled with inflation and high interest rates, stocks of premium hotel companies like Indian Hotels, EIH and Hotel Leela Ventures as well as travel companies like Cox & Kings India and Thomas Cook India are trading at a huge discount to their five year prices. Further, it is estimated that the operating profit margins of premium hotels are likely to touch a 10-year-low in the next two years.

LOSE SOME, WIN SOME

Someone’s loss can become someone else’s gain. Thus, small and mid-sized hotels have gained tremendously when premium hotels are struggling to make profits.

The small and mid-sized hotels have been able to post encouraging financials owing to their keen focus on domestic tourism, low operational costs as well as expansion in unexplored territories.

Small and mid-sized hotels like Bhagwati Banquets & Hotels, Royal Orchid Hotels, Oriental Hotels and Asian Hotels (West) have performed considerably better than their bigger counterparts on the back of growth parameters such as cash flow from operations, increased net profits, net sales and better occupancy rates in times of economic slowdown.

The fall in foreign tourists’ arrivals has been favourable for small and mid-sized hotels who earned better revenues from increased occupancy

It’s simplified...Beyond Market 19th Oct ’12 23

the operating profit margins of premium hotel companies (4-and-5-star, listed and unlisted) in 12 cities would be just over 16% in the next two fiscals – the lowest in the last 10 years.

There would be an oversupply in the industry. Property consultancy firm Cushman and Wakefield feels that around 66,371 rooms are likely to be added to the present inventory of 1,12,818 rooms.

The estimate suggests that 14,800 rooms would be added in top six cities in 2012 alone. Of these, 2,000 rooms

have already entered the markets. This oversupply is a big concern when juxtaposed with the falling occupancy rates and average room rates of premium hotels companies.

At present, average occupancy rates of these companies are in the range of 55% to 60% from 63% in FY10, while average room rates have come down by 9% in the same period. This fall in average room and occupancy rates would further decline revenue per available room (RevPAR) of these hotel companies.

CRISIL foresees a decline in the

average RevPAR for premium hotels to `3,900 per day in FY14 from `5,000 per day in FY12. The RevPAR of hotels in Ahmedabad and Chennai, which have oversupply of rooms, is expected to decline by 20%.

While in Bengaluru, Hyderabad, NCR, Jaipur and Kochi, the RevPAR is expected to fall by 15%.

For listed entities though, one favourable factor that assuages concerns related to high interest outgo is their low debt to equity ratio. The debt to equity is less than 1 for both EIH and Indian HotelS.

It’s simplified...Beyond Market 19th Oct ’12 25

investing in the real estate company.

Suppose a project gets completed by the June quarter of a fiscal year, investors can expect the September quarter as one of the strongest ones in that fiscal.

A project is considered complete when apart from the main cost of construction, its other expenses and external risks are relatively less. This method works for projects, which are small and of short duration. It gives an idea to investors to time their investments accordingly.

Apart from this, investors should take into account the location of the project that has been completed. A project that has completed construction does not ensure immediate booking and buying. In this method, though, the pattern and timing of recognizing revenues are quite irregular. As and when a project is completed, the company recognizes revenues and, hence, this can be a tad unpredictable for investors to time their investments.

PERCENTAGE COMPLETION METHOD

In a percentage completion method, real estate companies recognize revenues at the stage a project is completed. This indicates that companies recognize revenues in parts and not as a whole.

So, as and when a particular stage of development of a project is completed, a real estate company would recognize revenues in its profit and loss statement.

Experts believe that this method works well when it is reasonably possible to estimate the stages of the project or estimate the costs and revenues of the project.

Here investors must bear in mind that in this method the costs involved in a project can blow up disproportionately and hamper the continuation of the project.

More so, a project may land in legal issues from different considerations, equipment unavailability and many other glitches that obstruct the progress of a project. Hence, investors should be wary of such possible glitches in a project.

Moreover, the method also involves certain anomalies, which real estate experts claim could possibly mislead investors when it comes to investing. It has been observed that a large number of listed real estate companies project the percentage completion method, while a large section of unlisted companies follow the project completion method. This strategy is employed by many a listed real estate company as well due to certain tax considerations.

THE ANOMALIES

Although by definition, the two methods seem simple, there are lots of anomalies in the way these methods are used in recognizing revenues. For instance, it has been observed that most real estate companies set a minimum benchmark for recognizing of revenues and costs as regards percentage completion method.

Hence, these companies don’t recognize their revenues in the profit and loss statement till they achieve the benchmark. This benchmark sometimes varies in the range of 20% to 35%.

So, there may be a situation where a real estate company following percentage completion method would recognize revenues when 20% of the project is completed, while some

T he real estate sector unlike other sectors has a seemingly strong connection with its buyers.

Being in the business of tangible assets, many consumers can gauge the performance of a real estate company by merely visiting its site or by finding out more about the quality of construction.

Many consumers hold this opinion and are convinced about the fact that such assumptions are fair and unerring. And these consumers then begin buying into the stock of real estate companies.

However, analyzing a real estate company is not that simple in reality. There are various ways by which real estate companies recognize and report their revenues.

Hence, it is important to understand the basic facts associated with various revenue recognition methods followed by real estate companies before investing in the companies.

This time we explain the nitty-gritties of the two main revenue recognition methods of real estate companies: Project Completion and Percentage Completion. We will also delve into the aspects that work best for investors when it comes to investing in real estate companies.

PROJECT COMPLETION METHOD

Project Completion Method means that a real estate company would recognize its revenues from a project only after completing the project.

If a project remains incomplete, the real estate company would not account for its revenues in its profit and loss account statement. This keeps out any kind of doubt in the mind of an investor when it comes to

It’s simplified...Beyond Market 19th Oct ’1226

would recognize revenues when 35% of the project is completed. So, there is no standard as to how much one must recognize as revenues when it comes to the percentage completion method of computation.

A concern that many experts raise is the mere definition of the percentage completion method. Some real estate firms consider the cost of land, development rights and borrowing costs as costs that they have to bear while following the percentage completion method.

On the other hand, there are certain companies which consider the actual cost of construction as total costs.

In addition to this, there are companies which account for costs related to projects in the profit and loss account, while there are companies which recognize them as the project’s costs. There are also companies which consider borrowing costs as part of the project’s costs and charge them in the profit and loss account of the company.

Experts have also found that some companies consider the sale of undivided interest in land as part of the complete contract and apply percentage completion method in recognizing revenues, while others

consider the undivided interest as a separate part and recognize the sale upfront even though the construction of an apartment may take a long time.

Also, in certain cases companies fail to meet their commitments to customers. These companies use terms to signify income that is not generated through the customers.

Typically termed as “unbilled receivables”, various companies employ the percentage completion method and increase their sales in their profit and loss account. And in doing so they also do not care about the completion of their projects.

According to PropEquity, a property research firm, it is estimated that nearly half of the 9,30,000 residential units under construction in India, which are due for delivery between 2011 and 2013, are likely to be delayed by up to 18 months.

IN A NUTSHELL

In order to keep such practices under check, sector experts stress the role of a regulator. There have been talks that the regulator Institute of Chartered Accountants of India (ICAI) plans to deal with such discrepancies in the sector swiftly. Consensus suggests three means to

regulate accounting practices.

The first means is to observe the accounting standards that companies are expected to follow. Second, is the guidance note. Normally, companies are required to implement their guidance note though companies can deviate, provided they furnish acceptable reasons. The third relates to securing an explanation of frequently asked questions, where different situations are projected.

It is strongly believed that these differences can be weeded out of the sector if the Indian real estate sector adopts the International Financial Reporting Standards (IFRS), the global accounting norms that all nations adhere to avoid any anomaly. The IFRS strictly accepts revenue recognition in real estate only when the project is completed. Hence, it is very important that ICAI meaningfully intervenes in these matters. Unless ICAI brings a cogent argument to these practices, any analysis by investors and analysts would be irrelevant and hollow.

Investors seeking exposure to such real estate companies are advised to invest in companies that follow the project completion method for recognising revenueS.

Micro analysis. Mega gains.Trading at Nirmal Bang is based on extensive research and in-depth analysis, where we focus on the smallest of details and turn them into an advantage for you.

Over the years, the analytical approach coupled with decades of experience has helped us maximize returns for our investors and thereby inspire con�dence in them.

EQUITIES* | DERIVATIVES* | COMMODITIES | CURRENCY* | MUTUAL FUNDS^ | IPOs^ | INSURANCE^ | DP* www.nirmalbang.com

REGD. OFFICE: Sonawala Building, 25 Bank Street, Fort, Mumbai - 400 001. Tel: 022 - 39267500 / 7501; Fax: 022 - 39267510 CORPORATE OFFICE: B-2, 301/302, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400 013. Tel: 022 - 39268000 / 8001; Fax: 022 - 39268010BSE SEBI REGN No. INB011072759, INF011072759 & INE011072759, NSE SEBI REGN No. INB230939139, INF230939139 & INE230939139 DP SEBI REGN. No NSDL: IN-DP-NSDL-136-2000, CDS(I)l: IN-DP-CDSL-37-99, AMFI REGN. No. arn-49454 NCDEX REGN. NO. 00362, FMC Code-0075, MCX REGN. No. 16590, FMC Code-MCX/TCM/CORP/0490, MCX SX-INE260939139, PMS-INP000002981

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. The PMS Service is not o�ering for commodity segment. *Through Nirmal Bang Securities Pvt. Ltd. ^Distributors #Prepared by Research Analyst of Nirmal Bang Commodities Pvt. Ltd.

SMS ‘BANG’ to 54646 | Contact at: 022-3926 9404 | e-mail: [email protected]

It’s simplified...Beyond Market 19th Oct ’12 27

APROACTIVE

INTERVENTIONThe SC directive to the government on

pharma pricing policy is an initiative in

the right direction and is hoped to make

drugs affordable to a majority of the

Indian population

It’s simplified...Beyond Market 19th Oct ’1228

market and benefit the patient fraternity and the industry at large.

Since the prices of medicines in the bulk market and the cost of manufacturing formulations are widely known, there is no difficulty in fixing prices based on a cost-based formula. Currently, as per the 1995 Drug Price Control Order, the post manufacturing expense (MAPE) allowed is 100% and includes profit for the company.

The Jan Swasthya Abhiyan, the Indian circle of the People’s Health Movement, a worldwide movement to establish health and equitable development as top priorities through comprehensive primary health care and action on the social determinants of health, demands that the government pay heed to the Supreme Court directive and control the prices of all 348 essential drugs by continuing to use the cost plus formula of price fixation.

Essential drugs have a total sale of around `29,000 crore, accounting for almost 60% of the domestic market. Before recommendation, only 74 bulk drugs and their formulations were under the control of the government.

However, the panel has finalized the market-based Weighted Average Prices (WAP) for those companies enjoying more than 1% market share. It includes 348 drugs but has excluded combination drugs.

According to industry sources, the initial assessment was a sales impact in excess of `20 billion when the market share in excess of 5% was being used.

The total value of the compound would be 100% and the weighted average price of products in excess of 1% market share would be taken as the maximum retail price. Hence,

companies which are in the premium pricing band would be impacted the most from this.

MNCs in particular, with a pure domestic play like GSK Pharma and Sanofi India, would be impacted the most, with contraction in EBITDA margins for the business as a whole.

Indian companies not having very huge exposure to the domestic play would be insulated to some extent, but what we would be seeing is contraction in EBITDA margins for the domestic segment as a whole, thus impacting their profitability.

Companies such as Dr Reddy’s (DRL), Sun Pharma, Lupin, Ranbaxy Labs and Cipla would be lesser impacted due to their presence in the exports space. The impact of the new policy may be nearly the same as was the impact under the NPPP.

MNCs like GSK Pharma will be adversely impacted along with Indian pharma players like Ranbaxy, Cipla as well as Cadila.

While the actual impact on these companies will be known only when further details on the policy are available, industry watchers believe that these three companies will be relatively more impacted as compared to others given their significant exposure to the anti-infective segment. None of the companies have confirmed the impact depicted and, hence, more clarity from the management of these companies is keenly awaited.

AIOCD President JS Shinde believes that market-based pricing would balance patient as well as industry interests, while preventing formulations going off the market on account of unviable manufacturing environment – as it happened during the cost-based pricing regime.

T he Group of Ministers (GoM), headed by Union Agriculture Minister Sharad Pawar along with

Minister of State for Chemicals and Fertilizers Srikant Jena and other members of the group including Health Minister Ghulam Nabi Azad, Minister for HRD, Communications and IT Kapil Sibal, Law Minister Salman Khurshid and Planning Commission Deputy Chairman Montek Singh Ahluwalia, recently gave its approval to the final pharmaceutical pricing policy, bringing 348 essential drugs under the government’s price control regime.

The GoM will be sending its recommendations to the cabinet in the next 10-15 days, said senior government officials.

However, given the fact that medicines are often outside the reach of the common man, India’s Apex Court responded by saying that the government will not disturb the retail price mechanism of essential drugs under the price control order, while increasing the list of important medicines under the National List of Essential Drugs (NLED).

The new pharma pricing policy had been pending since the year 2009. Hence, the Supreme Court gave an ultimatum to the government and asked it to take a decision on the policy, failing which it will pass an interim order.

Further, the All India Organization of Chemists and Druggists (AIOCD) wrote a letter to Sharad Pawar, Chairman, Group of Ministers – National Pharmaceutical Pricing Policy, to urgently finalize the new drug pricing policy, which seeks to determine the prices at which pharma companies sell essential medicines in the retail market. This is hoped to dispel the prevalent uncertainty in the

It’s simplified...Beyond Market 19th Oct ’12 29

It is been observed that consumers are benefited because the NLEM list has been increased from the current 74 to 348 drugs (includes approximately 750 formulations), which will reduce prices of these drugs by up to 20%.

The grey area here is that specific drugs for specific strengths are only included in the current NLEM list. Hence, it would be interesting to see how the industry looks at bypassing this regulation. On the whole, this can be seen as a win-win situation for all.

The mechanism for market-based pricing should be seen against this background. Reports indicate that the government is set to introduce the concept of WAP as the method for fixing the ceiling price of drugs.

In such a system, the present prices of existing brands and their respective share in the entire market of a particular drug will be taken into account to compute the ceiling price. Such a method is entirely skewed as

the ceiling price fixed would largely reflect the price of the brand leaders.

Generally 2 to 3 top selling brands - usually the most expensive or some of the more expensive brands - control a bulk of the market.

Therefore, price control will do nothing to bring down drug prices, and will in fact encourage cheaper brands to start charging more and approach the high ceiling price.

This situation has risen because medicine prices in India have no relation to the actual cost of production, packaging and marketing.

A study commissioned by the National Commission on Macroeconomics and Health showed that there is a very wide variation in the prices of drugs sold in the retail market and those sold in bulk through tenders to institutions. The price differences range from around 100% to 5600%.

There is also a wide variance in prices of the same medicine sold under different brands by different pharmaceutical companies

Moreover, the more expensive brands sell much more than the less expensive ones because big pharmaceutical companies are able to promote their expensive brands by offering incentives to prescribers as well as chemists.

The proposed method of price fixation for medicines is likely to push up the prices of brands that are cheaper. And hence, the cost of procuring drugs for the free medicine scheme by the government will increase significantly.

As we know the Supreme Court has asked the government to see the affordability factor as well. Now the GoM is getting ready to present the report to the Cabinet and, hence, we need to wait till the final decision is taken by the CabineT.

The most intelligent strategy in Chess is to be ready with the next move.

Similarly, currency trading involves moves that are a combination of

knowledge and skill, backed by years of experience.

Currency Derivatives Trading with us keeps you a few steps ahead, always.

Registered O�ce: Nirmal Bang Securities Private Limited. 38-B, Khatau Building, 2nd Floor, Alkesh Dinesh Mody Marg, Fort, Mumbai - 400001. Tel: 3926 8600 / 01; Fax: 3926 8610Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risk. Please read the scheme related document carefully before investing. Please read the Do’s and Don’ts prescribed by Commodity Exchange before trading. Through Nirmal Bang Securities Pvt. Ltd. *Through Nirmal Bang Commodities Pvt. Ltd. #Distributors investment in securities is subject to market risk. investment in securities is subject to market risk

EQUITIES | DERIVATIVES | COMMODITIES* | CURRENC Y | MUTUAL FUNDS# | IPOs# | INSURANCE# | DP

Contact: 022-39268088 | e -mail: [email protected] | www.nirmalbang.com

2011 2010 2009Aug Jul Jun Q2 Q1 Q4 Q3 Q2 Q1 Year Year Year

DemandOECD 48 47 46 45 46 47 47 45 47 46.4 46.9 46.3Rest of the World 44 44 45 43 43 43 43 42 42 42.3 41.2 39.1Total 92 90 91 89 89 90 89 88 89 88.7 88.1 85.4SupplyOPEC 31 31 31 31 31 31 30 29 30 29.7 28.9 28.7Non-OPEC 52 51 51 51 51 51 51 51 51 49.9 50.4 49Others 8.7 8.7 8.6 8.6 8.6 8.4 8.3 8.1 8.2 8.3 8.1 7.6Total 92 91 91 91 91 90 89 88 88 87.9 87.4 85.3

2012 2011

Source: EIA Unit: mbpd

Global Supply And Demand

It’s simplified...Beyond Market 19th Oct ’12 31

On 21st Dec ’11 the European Union came out with LTRO (Long Term Refinancing Operation) to overcome the ongoing debt crisis in the nation. LTRO1 infused 489 billion Euros and the LTRO2 pumped around 529 billion Euros into the system. Ignoring geopolitical tensions, the infusion of around 1 trillion Euros through LTROs had a very limited upside in oil prices.

WILL RISE IN GASOLINE PRICES HELP OBAMA?

On 14th September, the national average price for regular gasoline rose to $3.878 a gallon as per the US Energy Information Administration. Prices are up 7.7% from $3.601 in the year 2011 and at a record-high for this time of the year.

Gasoline prices gained after the Federal Reserve came up with its plan to buy mortgage backed securities worth $40 billion every month till there is a meaningful recovery in the job market. Retail gasoline prices climbed above year-earlier levels for the sixth consecutive week ended on 14th September. A jump in the cost of gasoline pushed US consumer prices up in August and during mid September was at the fastest pace in more than three years.

Source: Bloomberg

00.5

11.5

22.5

33.5

44.5

5

01-Jan-08 01-Jan-09 01-Jan-10 01-Jan-11 01-Jan-12

$/ba

rrel

US GasolineAny further risethen Obama may