oww initiation 1-19-2011 final

TRANSCRIPT

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 1/16

PLEASE SEE PAGES 13-16 FOR IMPORTANT DISCLOSURES, REG AC ANALYST CERTIFICATION AND DISCLAIMERS

Analyst: Brian Bolan 773.413.0285 [email protected] January 19, 2011

WILLIAMS CAPITAL RESEARCH

OWW Mkt Perform Curr. Q. 1 yr ago Q

Price $5.30

Price Target $5 (Rev in $M)

52 Week High $7.65 Rev prev.

52 Week Low $3.56 Rev new 737.65 777.42 846.6 202.29 174.69 202.11 208.11 214.25

NTM P/E 23.74 EPS prev.

Market Cap $539.15M EPS new 0.06 0.21 0.18 0.01 0.21 0.04 0.06 0.1Ent Value $896.16M P/E NM 25.24 29.44

Shares Outstanding 102.30M

Avg Daily Volume 268,956

Cash/Share 1.36

BV/Share 2.59

12/

Next 4 Quarters

Key Data

Fiscal Year

FY09 FY10E FY11E 12/31/2010 12/31/2009 3/31/2011 6/30/2011 9/30/2011

Overview

What started out as a potential anti-trust case when first proposed by the five major carriers has moved on to focus

on the hotel aspect of the travel industry. With a broad array of brands, Orbitz Worldwide Inc. offers customerstravel services from several major suppliers.

With a complex capital structure and significant debt load the company is often overlooked by investors in thetravel space. We believe that with solid execution in the remainder of 2010, the company will be profitable. Thiscould cause a number of investors to take a second look at one of the smaller players in the space.

We initiate coverage of Orbitz with a neutral rating and $5 price target.

Company Background

Founded in 1999 by five major airlines that invested $145M in an effort to derail the success of Travelocity,

Orbitz Worldwide Inc. (Orbitz) officially launched in June of 2001. The company went public in 2003 and was

subsequently purchased by Cendant in November of 2004. After the sale of Cendant’s travel properties

(Travelport) to BlackStone Group L.P. (BX, $15.31 – Not rated) in 2006 the company was again sent into the

market in a July 2007 IPO. Travelport still holds approximately 60% of Orbitz shares.

quity Research Orbitz Worldwide, Inc.(OWW)

ompany Update Current Rating: Market Perform

anuary 19, 2011 Initiating Coverage on Orbitz with a

Market Perform rating

nternet Analyst: Brian Bolan 773-413-0285; [email protected]

rading Desk: NY 800-924-1511 CT 800-688-6349

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 2/16

WILLIAMS CAPITAL RESEARCH PAGE 2 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Orbitz has several brands for distinct segments of the travel market.

Orbitz – Orbitz.com allows consumers to search and book travel services provided by Airlines, Hotels and rental

car companies. Users can purchase packages of services in order to obtain a better rate.

CheapTickets - U.S. travel website that focuses on value-conscious customers.

The Away Network is a series of travel content websites that includes Away.com, Trip.com, GORP.com,GORPTravel.com and Lodging.com. The Away Network also hosts, maintains and develops outsideonline.com

Orbitz for Business is a full-service global travel management company that provides online booking and call

center support to a broad array of organizations, ranging from small businesses to Fortune 500 companies.

ebookers offers customers the ability to book an array of travel products and services through websites in Austria,

Belgium, Denmark, Finland, France, Germany, Ireland, the Netherlands, Norway, Sweden, Switzerland and the

U.K.

HotelClub, Accomline and Asia-hotels are hotel-only websites that offer customers the opportunity to book hotel

stays in over 130 countries.

RatesToGo website offers customers the opportunity to book hotel stays at last-minute discounts.

Business Models Merchant vs. Retail

Merchant Model

The merchant model provides customers the ability to book air, hotel, car, destination services reservations and

dynamic vacation packages. Hotel transactions comprise the majority of merchant bookings. The company

generates revenue for services based on the difference between the total amount the customer pays for the travelproduct and the negotiated net.

Retail Model

The retail model provides customers the ability to book air, hotel, cruise and car rental reservations. Air

transactions comprise the majority of retail bookings. The company earns commissions from suppliers for airline

tickets, hotel stays, car rentals and other travel products and services booked on our websites.

Traffic to Orbitz

The clickstream for Orbitz is provided below.

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 3/16

WILLIAMS CAPITAL RESEARCH PAGE 3 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Exhibit 1

Upstream Sites

Which sites did users visit immediately preceding orbitz.com?

15.89% google.com

6.13% expedia.com

5.36% travelocity.com

4.67% priceline.com

4.65% kayak.com

4.41% yahoo.com

3.37% facebook.com

3.07% tripadvisor.com

2.51% hotwire.com

2.08% hotels.comSource: Alexa.com

This table shows a sizeable dependence on the major search engines and a surprisingly high number of referrals

from properties that compete directly with Orbitz. We believe that this suggests that consumers are looking at

multiple sources for pricing information. It also shows the total reach of Expedia as its sites dominate this list.

Management

Barney Harford, President and Chief Executive Officer and also serves as a director and as a member of theexecutive committee of the board of directors. Prior to joining the Company in January 2009, Mr. Harford served

in a variety of roles at Expedia, Inc. from 1999 to 2006. He holds an M.B.A. from INSEAD and a Master of Arts

degree in Natural Sciences from Clare College, Cambridge University.

Marsha C. Williams, Senior Vice President, Chief Financial Officer, having served in that capacity since July

2007. From August 2002 to February 2007, Ms. Williams served as Executive Vice President and Chief Financial

Officer of Equity Office Properties Trust, the nation’s largest owner and operator of office buildings. Ms.

Williams earned an M.B.A. from the University of Chicago Graduate School of Business and a Bachelor of Arts

degree from Wellesley College.

Financial Statement Analysis

Revenue was down slightly in 1Q10 vs. the same period a year ago, a trend that persisted throughout the entire

calendar year of 2009. We expect that the company will post its first year over year increase in revenue in 2Q10.

Challenges still present themselves to Orbitz as consolidation in airlines (United and Continental) (UAL, $25.02 –

Not rated) and in the rental car business mean less potential clients for the company. Problems in the airline

sector include the removal of Delta (DAL, $11.70 – Not rated) and American Airlines (AMR, $8.29 – Not rated)

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 4/16

WILLIAMS CAPITAL RESEARCH PAGE 4 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

from its listings. We believe that other airlines may follow the lead of Delta and American as Orbitz has

highlighted the possibility that consumer can save money with two one way trips from different carriers as

opposed to standard round trip purchases.

Balance Sheet

At the end of 3Q10, Orbitz had more than $139 million in cash and equivalents and short term

investments on the balance sheet. This is an increase of 14% from the year ago period when the

company had approximately $122 million. At the end of the first quarter of 2010 the company has

more than $162 million in cash, similarly a decrease of 14% from the high point of the year.

At the end of 3Q10, Priceline.com had approximately $485 million in long term debt. We should note that long

term debt has decreased approximately 31% from the year ago period as excess cash flow was used to repay debt.

Financial Outlook

As airlines increase prices for due to higher oil prices, we believe that consumers will continue to look to OTA’s

for discounts and optimal rates. This bodes well for Orbitz despite the expected weakness in European travel

market. We believe that there could be upside to our below consensus 2011 EPS estimate of $0.18.

Investment Thesis

The online travel agent (OTA) industry has four major players that compete for the business of a highly

fragmented hotel industry as and to a lesser extent the airline industry and rental car industry. Airlines sales

provide large gross dollar bookings, but contribute little to the bottom line. The rental car industry, while possibly

constrained by supply, has the exact opposite problem the airlines have in that their gross bookings are very small.

The savior of the sector is the hotel industry which is highly fragmented and the biggest contributor to net income

of the three major suppliers.

We believe that hotel bookings will continue to drive the OTA industry due to the consolidation in the airline

industry (United and Continental) and in the rental car business (Hertz HTZ, $14.21 – Not rated) plans to acquire

Dollar Thrifty (DTG, $48.08 – Not rated) , although Avis (CAR, $14.52 – Not rated) may show up as a late

bidder). The hotel industry is coming off of a consolidation boom which saw both strategic (hotel buying hotel)

and financial (private equity buying hotel) buyers bidding up a market that had severe capacity concerns in 2005-

2007. Another chronic problem for the hotel industry has been its ill timed expansions that seem to coincide with

economic downturns. With occupancy rates around 60%, hotels are lowering average daily rates (ADR) to

stimulate demand, and continue to look to OTA’s to find customers.

There are several concerns that the OTA’s face in both the short and near terms. One of the biggest is the

economic concerns of Europe. Priceline.com in particular generates a majority of its revenues from the hotelbusiness in Europe, which, given the economic uncertainty, may not be a destination of choice for foreign

travelers. The situation could be compounded should a second volcano from Iceland erupt and possibly disrupt

travel on an even larger scale that than the Eyjafjallajokull eruption in April 2010.

Longer term the implications of contract re-negotiations with several airlines loom on the horizon for 2012.

Crude oil prices which continue to dramatically affect the airline industry, which also affects the hotel and rental

car industries, could move higher and again strangle the leisure travel market as they did in the summer of 2008.

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 5/16

WILLIAMS CAPITAL RESEARCH PAGE 5 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Our view of the industry is that there will be several players for some time to come. Competition, whether via

metasearch players like Kayak.com, or other OTA’s tends to benefit the consumer and stimulate travel. We view

Expedia.com as having the deepest breadth throughout the categories of services provided, and Orbitz the weakest

in that category. Priceline.com is our top pick in the space due to its clean balance sheet, brand recognition and

retention and market perception of being a leader in the space. Expedia is also attractive but its brand is diluted

across several properties and its financial structure may worry some. Orbitz, founded by five airlines, has shifted

its focus to hotels and continues to try to build its brand, but its debt structure may impede future third partyinvestment.

Industry Discussion

As we look at the online travel industry we want to highlight a few key areas to better understand the industry as a

whole. First we will discuss the primary components of the online travel agent, the suppliers of travel services.

Then we will look into the fees and metasearch and, finally, we will touch on traffic.

Airline Segment

The airline industry has been plagued by overcapacity, financial losses and volatility in oil prices. Consolidation

continues in the space, with the most recent tie up of United Airlines and Continental showing that even the

biggest airlines need to find ways to save on costs. From the consumer perspective, bigger isn’t necessarily

better, as less competition ultimately drives prices higher. The same is true for OTA’s in that fewer suppliers

could lead to lower revenues sources and thus potential decreases in future sales. Although an airline ticket does

a lot to boost gross bookings, it is generally a very small contribution to net income.

The recent moves by bother American Airlines and Delta point to further consolidation and cost cutting in the

airline industry. We expect other airlines to look the potential of squeezing the OTA’s for better pricing or face a

100% elimination of supply. Positioning in front of negotiations is one move that Expedia has employed and it

resulted in the airline suggesting consumers use Priceline.com. The eventual consumer decision has traditionally

been one that has included competitor information unless a purchase comes solely from brand loyalty or brand“dislike”. Our research shows that air related revenue for all OTA’s has been dropping over the last few years.

Rental Car Segment

The proposed consolidation of two major players in the rental car industry supports some recent anecdotal stories

of very low supply of rental cars in select markets. The inventory issues of rental cars companies is a problem

that can be solves quite quickly and with minimal impact to the OTA’s. The health of the business appears to be

relatively stable with a small majority of rental cars coming from corporate travelers as opposed to leisure. Avis

notes its mix is a 60/40 split of corporate and leisure customers respectively. Currently, the rental car sector is a

small focus of the OTA’s.

Hotel Segment

With a highly fragmented ecosystem, the hotel industry appears as though it will always need the OTA’s to

inform potential consumers and provide an easy transaction for those wishing to be customers. Large national

chains serve as good proxies for the entire industry, but there are many smaller entities that will require OTA’s to

maintain acceptable occupancy rates.

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 6/16

WILLIAMS CAPITAL RESEARCH PAGE 6 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

The hotel sector has historically been out of touch with the supply and demand of the broader market over the last

few decades. When times were good, supply was constrained and new construction was initiated. As the broader

economy cooled, many new properties came on line just as demand was close to or had bottomed. More recently

the pattern has repeated itself as supply grew in the face of economic recession. Hotel News Resources has

estimated that there are 1.1 million new hotel rooms under construction as of April 2010, suggesting that the trend

will continue.

While lower occupancies have historically increased the availability of discounted hotel rooms, and a lower rate

of ADR growth can positively impact underlying room night growth, lower ADRs also decrease Expedia revenue

per room night as their payment varies proportionally with the room price. Revenue per room night in 2009

declined 17% primarily due to the downward movement in ADRs as well as adverse movements in foreign

exchange rates and lower fees. Key leisure markets like Las Vegas and Hawaii have seen dramatic declines in

ADR’s.

Fees and Metasearch

The OTA’s are coming off the anniversary of a reduction in fees that occurred in 1Q09. This reduction in fees

was spurred on by the success of the metasearch companies such as Kayak.com. Metasearch is simply anaggregator of all of the data from several sites presented to the consumer in a usable format to help locate the

lowest price or best outcome from multiple service provider locations. Other metasearch companies in the past

would “scrape” data off sites, sometimes with permission, mostly without. Kayak.com employs a different

model, one where the OTA’s pay them for placement.

This aggregation of prices ended up prompting a price war that saw the end of most fees by the OTA’s. This led

to lower revenue and earnings for OTA’s and lower prices for consumers. The advertising expense that the

OTA’s pay Kayak.com and the other metasearch sites is likely to be the focus of other technology companies,

particularly Google which has been rumored to be interested in purchasing ITA Software. Yahoo! (YHOO,

$16.50 – Not rated) has a travel site that has transactions powered by Travelocity, whereas Google (GOOG,

$639.63 – Not rated) is not likely to partner for a transaction but instead deliver consumers to advertisers. Thismeans that Google is a threat to the metasearch companies more than the OTA’s, and Yahoo! has partnered with

Travelocity potentially limiting the amount of advertising the other OTA’s are willing to spend on Yahoo!.

The graph below from Compete.com shows that Expedia holds an edge over the other OTA’s in terms of uniqueusers per month over the last year. Expedia’s depth of portfolio is the likely reason for the sizeable advantage itenjoys over its rival OTA’s.

Exhibit 2

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 7/16

WILLIAMS CAPITAL RESEARCH PAGE 7 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Macro Concerns for OTA’s

The OTA’s are facing a challenging 2011. The weakening of the Euro may become a material problem for the

entire industry as US-based travelers, who would normally take leisure trips to Europe when the exchange rate is

so favorable, may not travel abroad due to the economic concerns in multiple countries. Those same concerns

cast doubt on the amount of intra-European leisure travel as well, in effect causing a double hit to demand.

Asian travel is also coming under pressure as civil unrest in Thailand will undoubtedly curtail a percentage of

travel to the region. Australia and Canada have lowered the threat level to its citizens that have planned travel but

still advise that people use caution and reconsider their travel plans.

The volcano in Iceland that disrupted air travel in Europe in April 2010 due to the massive ash cloud may see its

larger neighbor erupt in the near term as well. Mid-May earthquakes around the site of the larger Katla volcano

were thought to signal an eruption in near future. Although the near term in geological time could be several

decades, it could also mean in the next several months or quarters. Should this volcano erupt, we would believe

that shares of OTA companies will face severe pressure as European travel would like halt entirely.

Finally, domestic concerns over the oil spill in the Gulf of Mexico have derailed travel in several Gulf states,

particularly in the tourist-heavy Florida Gulf coast. The struggles of the Gulf Coast have been well documented

and there is limited proof of any full scale tourism increase. This may benefit other domestic travel destinations,

but concerns of a double dip recession may keep the leisure traveler spending less than average again this year.

Comparable Companies

OTA’s compete directly with one another (Priceline.com, Expedia, Orbitz and Travelocity) as well as many other

firms. The OTA’s offer transaction services that separate them from the metasearch players such as Kayal.com

and the Fly.com division of TravelZoo.

Priceline.com Expedia and Orbitz compete for advertising revenue with large internet portal sites, such as

America Online (AOL, $24.73 – Not rated) and MSN (MSFT, $28.66 – Not rated) who offer listing or other

advertising opportunities for travel-related companies. The companies also compete with search engines like

Google, Bing and Yahoo! Search that offer pay-per-click advertising services.

Priceline.com (NASDAQ: PCLN - $440.91, rated Outperform) - Priceline.com Incorporated enables

consumers to use the Internet to save money on a variety of products and services. The Company's product allows

customers to name their own price on products or services and communicates that demand directly to

participating sellers or to their private databases. Participants include domestic and international airlines, and hotel chains.

Expedia (NASDAQ: EXPE - $26.69, rated Market Perform) - Expedia, Inc. provides branded online travel

services for leisure and small business travelers. The Company offers a wide range of travel shopping and

reservation services, providing real-time access to schedule, pricing and availability information for airlines,

hotels, and car rental companies..

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 8/16

WILLIAMS CAPITAL RESEARCH PAGE 8 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Orbitz. (NYSE: OWW) - Orbitz Worldwide, Inc. offers travel services over the Internet. The Company's website

offers air, hotel, vacation package, car rental, cruise, travel insurance, ground transportation, event ticket, and

tour bookings.

Travelzoo (NASDAQ: TZOO - $51.72, Not rated) - Travelzoo Inc. provides online marketing solutions to the

travel industry. Through the Company's Web site, its newsletter, and by using its listing management software,

travel companies can inform Internet users about their specials. Travelzoo serves companies such as Alamo Rent- A-Car, Delta Airlines, Expedia, and Hilton Hotels.

Universal Travel Group (NYSE: UTA - $7.20, Not rated) - Universal Travel Group provides travel services.

The Company's core services include booking services for air tickets, hotels, restaurants as well as tour routing

for customers.

Ctrip.com (NYSE: CTRP - $43.03, Not rated) - Ctrip.com International, Ltd. is a consolidator of hotel

accommodations and airline tickets in China.

Sabre Holdings (Privately Held) - Sabre Holdings, owner of Travelocity, is a world leader in the travel

marketplace, Sabre Holdings merchandises and retails travel products and provides distribution and technology

solutions for the travel industry. Sabre Holdings supports travelers, travel agents, corporations and travel

suppliers around the worl

Exhibit 3

Symbol$

PriceMarketCap $

2010eps $

eps est.2011 $

Forward P/E(1yr) PE P/B P/S ev/EBITDA

EXPE 26.36 7.18B 1.71 1.98 13.31 15.42 2.69 2.33 8.85

PCLN 431.21 21.27B 13.02 17.65 24.43 32.67 12.93 6.97 27.24

TZOO 47.11 787.45M 0.77 0.99 47.59 61.18 18.47 7.17 31.76

AMZN 184.34 82.54B 2.50 3.49 52.82 73.74 12.94 2.67 41.94

EBAY 28.36 36.88B 1.69 1.86 15.25 16.78 2.46 4.09 11.33

YHOO 16.58 21.63B 0.86 0.79 20.99 19.28 1.79 3.50 13.82

GOOG 616.01 196.97B 28.90 33.65 18.31 21.32 4.54 7.11 14.67

OWW 5.23 539.15M 0.13 0.23 22.74 40.23 2.02 0.67 6.37

Average: 35.08 7.23 4.31 19.50

SOURCE: YAHOO! FINANCE, ALL STOCKS PRICED ON THE CLOSE OF 1/11/11

Amazon.com Inc (AMZN, $191.25 – Not rated), eBay Inc. (EBAY, $29.45 – Not rated)

Conclusion and Valuation

We are initiating coverage of Orbitz Worldwide with a Market Perform rating and a one-year price target of $5.

We estimate topline growth of 9% in calendar 2011, well below that of its peers although the growth is better than

the decrease of 15% witnessed in 2009. We are also forecasting profitability for Orbitz in calendar 2010, but we

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 9/16

WILLIAMS CAPITAL RESEARCH PAGE 9 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

caution investors from focusing too much on PE in this instance. A multiple of 28x 2011 EPS brings us to a

target price of $5, right around where shares trade currently.

We are wary of potential multiple contraction which would be based on uncertainty in Europe, civil unrest in Asia

and a potential for a double dip domestic recession. There are several other scenarios that could cause our

projections not to come true, which could derail the path to profitability. We recognize the hard to swallow

premium of 29x could also go down a little easier if the company were to beat expectation by only 8%, as shownin the table below. An 8% improvement in earnings for the year could translate to a higher target price if the

multiple remains the same, but we would be more inclined to lower the multiple and maintain our $5 target.

Exhibit 4

Source: Williams Capital Research

Exhibit 5 Income Statement

Source: Company reports and Williams Capital estimates

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 10/16

WILLIAMS CAPITAL RESEARCH PAGE 10 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Exhibit 6 3Q10 Earnings Review

Source: Company reports and Williams Capital estimates

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 11/16

WILLIAMS CAPITAL RESEARCH PAGE 11 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Investment Risks

If the company experiences any or all of the following risk factors, as well as others, the company’s stock price

may be affected.

The travel market is susceptible to significant swings. Terrorism, SARS, H1N1 and volcanic ash are just afew random events that can significantly affect travel behaviors of consumers and business travelers alike.Should such an unforeseen event occur, travel patterns are likely to swing and could cause a material impacton revenue and earnings.

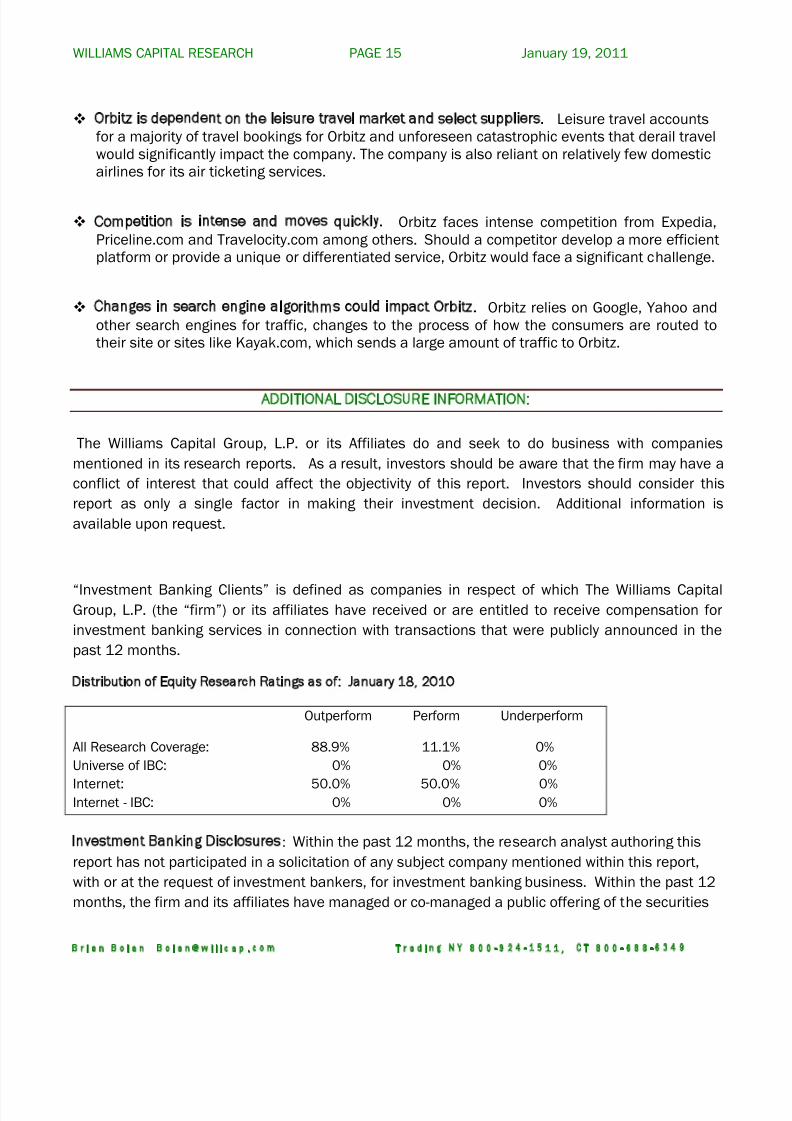

Orbitz is dependent on the leisure travel market and select suppliers. Leisure travel accounts for amajority of travel bookings for Orbitz and unforeseen catastrophic events that derail travel would significantly

impact the company. The company is also reliant on relatively few domestic airlines for its air ticketingservices.

Competition is intense and moves quickly. Orbitz faces intense competition from Expedia, Priceline.comand Travelocity.com among others. Should a competitor develop a more efficient platform or provide aunique or differentiated service, Orbitz would face a significant challenge.

Changes in search engine algorithms could impact Orbitz. Orbitz relies on Google, Yahoo and othersearch engines for traffic, changes to the process of how the consumers are routed to their site or sites likeKayak.com, which sends a large amount of traffic to Orbitz.

Loss of key management. Turnover at Orbitz could become a challenge to top management. Should largescale turnover occur the talent drain will result in an inability to properly serve clients which would putfuture revenues at risk.

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 12/16

WILLIAMS CAPITAL RESEARCH PAGE 12 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Exhibit 7 Balance Sheet

2010 Q3

9/30/10

2010 Q2

6/30/10

2010 Q1

3/31/10

2009 Q4

12/31/09

2009 Q3

9/30/09

ASSETS

Cash & Short Term Investments 139 145 162 89 122

Receivables - Net 79 68 82 58 73

Inventories - Total 0 0 0 0 0

Prepaid Expenses 19 17 18 17 15

Other Current Assets 5 21 4 5 18

CURRENT ASSETS - TOTAL 243 250 265 169 228

Property, Plant and Equipment - Gross 343 330 323 317 305

Accumulated Depreciation (180) (163) (150) (136) (123)

Property, Plant and Equipment - Net 163 167 173 181 182

Total Intangible Other Assets - Net 883 873 884 887 890

Other Assets - Total 941 935 949 944 952

TOTAL ASSETS 1,339 1,343 1,378 1,284 1,349

LIABILITIES

Accounts Payable 22 25 31 30 32

Short Term Debt & Current Portion of Long Term Debt 8 10 20 21 6

Other Current Liabilities 435 450 470 368 400

CURRENT LIABILITIES - TOTAL 465 485 521 419 438

Long Term Debt 484 482 486 598 635

Deferred Taxes - Debit 7 9 9 10 13

DEFERRED TAXES (7) (9) (9) (10) (13)

Other Liabilities 133 136 146 147 148

TOTAL LIABILITIES 1,075 1,094 1,143 1,154 1,208

EQUITY

Non-Equity Reserves 0 0 0 0 0

Minority Interest 0 0 0 0 0

Preferred Stock 0 0 0 0 0

Common Stock 1 1 1 1 1

Capital Surplus 1,027 1,027 1,023 922 919

Retained Earnings (766) (781) (791) (787) (769)

Treasury Stock (52)K (52)K 0 0 0

COMMON EQUITY 265 249 235 130 141TOTAL LIABILITIES & SHAREHOLDERS’ EQUITY 1,339 1,343 1,378 1,284 1,349

SHARE INFORMATION

Common Shares Outstanding 102 84 84 84 84

() = Negative Values

In U.S. Dollars

Values are displayed in Millions except for earnings per share and where noted

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 13/16

WILLIAMS CAPITAL RESEARCH PAGE 13 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

APPENDIXExhibit 8

Source: BigCharts.com

All prices as of 1/18/11

ANALYST CERTIFICATION

I, Brian Bolan, hereby certify that the views expressed in the foregoing research report accurately

reflect my personal views about the subject companies and their securities mentioned in this

report. I further certify that no part of my compensation was, is, or will be directly, or indirectly,

related to the specific recommendations or views contained in this research report.

Financial Interests: Neither I, Brian Bolan, nor a member of my household owns securities in any of

the subject companies mentioned in this research report. Neither I, nor a member of my household

is an officer, director, or advisory board member of the subject company or has another significant

affiliation with the subject company. I do not know or have reason to know at the time of this

publication of any other material conflict of interest.

By: Brian Bolan

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 14/16

WILLIAMS CAPITAL RESEARCH PAGE 14 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

__________________________________________________________________________

IMPORTANT DISCLOSURE INFORMATION

Analyst Compensation: The author's compensation is based upon the value directly or indirectly

attributed to the research services by Williams Capital institutional brokerage clients. The author of

this report is compensated based on the performance of the firm, and has not received anycompensation in the past 12 months from any of the subject companies mentioned in this report.

The performance of the firm is driven by its secondary trading revenues, investment banking

revenues, and asset management revenues.

WILLIAMS CAPITAL RESEARCH STOCK RATING KEY:

Outperform: (BUY) In the analyst's opinion, the stock will outperform the sector by 5% over the next

12 months.

Perform: (HOLD) In the analyst's opinion, the stock will perform in line with the sector over the next

12 months.

Underperform: (SELL) In the analyst's opinion, the stock will underperform the sector by 5% over

the next 12 months.

Company Ratings History as of January 19, 2011

Company Name Ticker Date Action

Prior

Rating

Current

Rating Price

Target

Price

Orbitz World Wide. OWW 1-19-11 Initiate coverage none Perform $5.30 $ 5.00

Valuation Methodology:

As of the market close on January 18, 2011, Orbitz traded at 25.24x our 2010 earnings estimate

of $.21 and 29.44x our 2011 earnings estimate of $.18 Our price target of $5 is based on a

multiple of 28x 2011 EPS brings us to a target price of $5, right around where shares trade

currently.

Risks:

The travel market is susceptible to significant swings. Terrorism, SARS, H1N1 and volcanic ashare just a few random events that can significantly affect travel behaviors of consumers andbusiness travelers alike. Should such an unforeseen event occur, travel patterns are likely toswing and could cause a material impact on revenue and earnings.

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 15/16

WILLIAMS CAPITAL RESEARCH PAGE 15 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

Orbitz is dependent on the leisure travel market and select suppliers. Leisure travel accountsfor a majority of travel bookings for Orbitz and unforeseen catastrophic events that derail travelwould significantly impact the company. The company is also reliant on relatively few domesticairlines for its air ticketing services.

Competition is intense and moves quickly. Orbitz faces intense competition from Expedia,Priceline.com and Travelocity.com among others. Should a competitor develop a more efficientplatform or provide a unique or differentiated service, Orbitz would face a significant challenge.

Changes in search engine algorithms could impact Orbitz. Orbitz relies on Google, Yahoo andother search engines for traffic, changes to the process of how the consumers are routed to their site or sites like Kayak.com, which sends a large amount of traffic to Orbitz.

ADDITIONAL DISCLOSURE INFORMATION:

The Williams Capital Group, L.P. or its Affiliates do and seek to do business with companies

mentioned in its research reports. As a result, investors should be aware that the firm may have a

conflict of interest that could affect the objectivity of this report. Investors should consider this

report as only a single factor in making their investment decision. Additional information is

available upon request.

“Investment Banking Clients” is defined as companies in respect of which The Williams CapitalGroup, L.P. (the “firm”) or its affiliates have received or are entitled to receive compensation for

investment banking services in connection with transactions that were publicly announced in the

past 12 months.

Distribution of Equity Research Ratings as of: January 18, 2010

Outperform Perform Underperform

All Research Coverage: 88.9% 11.1% 0%

Universe of IBC: 0% 0% 0%

Internet: 50.0% 50.0% 0%Internet - IBC: 0% 0% 0%

Investment Banking Disclosures: Within the past 12 months, the research analyst authoring this

report has not participated in a solicitation of any subject company mentioned within this report,

with or at the request of investment bankers, for investment banking business. Within the past 12

months, the firm and its affiliates have managed or co-managed a public offering of the securities

8/7/2019 OWW Initiation 1-19-2011 FINAL

http://slidepdf.com/reader/full/oww-initiation-1-19-2011-final 16/16

WILLIAMS CAPITAL RESEARCH PAGE 16 January 19, 2011

B r i a n B o l a n B o l a n @ w i l l c a p . c o m T r a d i n g N Y 8 0 0 - 9 2 4 - 1 5 1 1 , C T 8 0 0 - 6 8 8 - 6 3 4 9

of a subject company mentioned within this report, and the firm received compensation for

investment banking products or services from the company. The firm does not expect to receive or

intend to seek compensation for investment banking services from this subject company during the

next three months.

Firm Compensation: Within the past 12 months, the firm and its affiliates have not received

compensation for any non-investment banking products or services from subject companies

mentioned in this report, and the subject company has been a client of the firm during the past 12

months.

Stock Ownership: The firm and its affiliates do not own 1% or more of any class of equity security

discussed in this report, and do not make a market in any such securities.

DISCLAIMER

The information and opinions contained in this report were prepared by the firm and have been

derived from sources believed to be reliable, but no representation or warranty, expressed or

implied, can be made as to their accuracy. All opinions expressed herein are subject to change

without notice. This report is for information purposes only and should not be construed as an offer

to buy or sell any securities. The firm makes every effort to use valuation methodologies that it

believes to be reasonable in the derivation of price targets, but we do not guarantee that such

methodologies are accurate.

To receive any additional information upon which this report is based, please contact the following individuals or write to:

Williams Capital Research, Research Department650 Fifth Ave. 11 th FloorNew York, NY [email protected]

Suling Lew, Head of Institutional Sales or Jack Murphy, Director of Research212-373-4243 203-659-6007