overview of the european lubricant demand - kline & · pdf file © 2014 kline &...

TRANSCRIPT

www.KlineGroup.com

© 2014 Kline & Company

Overview of the European Lubricant Demand

17 September, 2014

A presentation at:

Alicante, Spain

© 2010 Kline & Company 1 © 2014 Kline & Company

Overview of Kline

About Kline & Company:

Corporate Overview:

Our Philosophy:

Kline is a respected provider of world-class consulting services and high-quality market intelligence that consistently lead to client successes in growing or improving their business.

Our focus is on providing solutions throughout the entire value chains of the industries we serve. We are large enough to have the blend of functional capabilities, industry experience, and geographical spread that successful projects require, yet small enough for clients to get our individualized full attention.

Our purpose is to help our clients succeed and our philosophy is built around this. Our clients value our people and the working relationships they form while working together.

© 2010 Kline & Company 2 © 2014 Kline & Company

Study Background

This presentation is based on Kline’s global series of including: Global Lubricant: Market Analysis and

Opportunities” “Global Lubricant Basetocks: Market

Analysis and Opportunities” This presentation will provide an overview

of synthetic lubricant demand and growth in key regions including Europe, North America, and providing a focus on selected emerging countries (Brazil, Russia, and China) All base year data refers to 2013 and

projections to 2023. All market numbers are in kilotonnes.

© 2010 Kline & Company 3 © 2014 Kline & Company

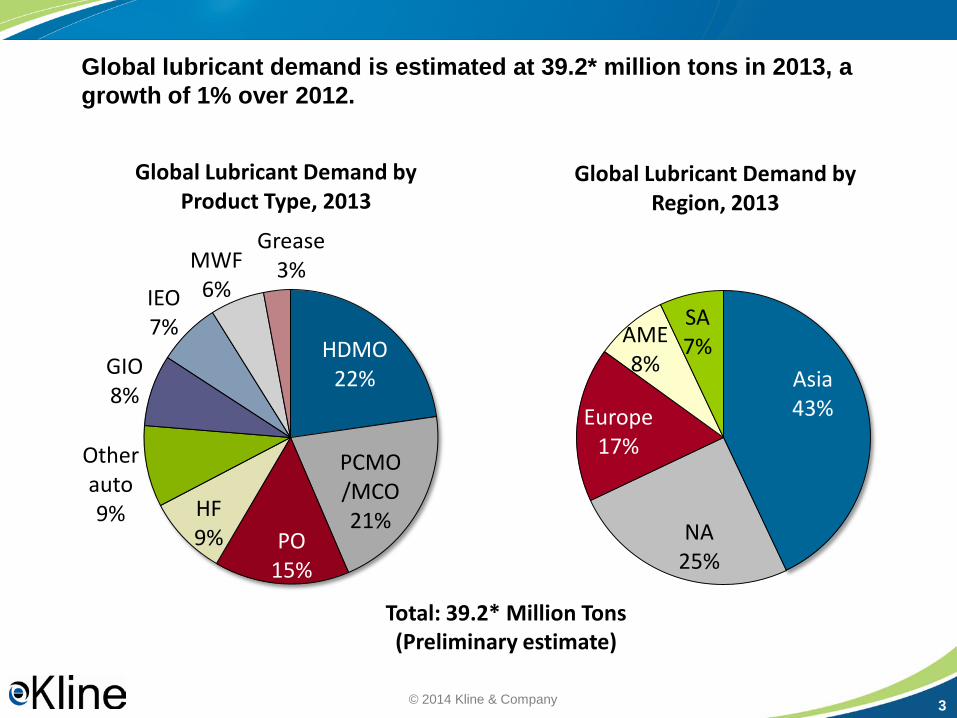

Global lubricant demand is estimated at 39.2* million tons in 2013, a growth of 1% over 2012.

HDMO 22%

PCMO /MCO 21%

PO 15%

HF 9%

Other auto 9%

GIO 8%

IEO 7%

MWF 6%

Grease 3%

Global Lubricant Demand by Product Type, 2013

Asia 43%

NA 25%

Europe 17%

AME 8%

SA 7%

Global Lubricant Demand by Region, 2013

Total: 39.2* Million Tons (Preliminary estimate)

© 2010 Kline & Company 4 © 2014 Kline & Company

How has the global lubricants market performed through the recession?

-10

-5

0

5

10

2007 2008 2009 2010 2011 2012 2013

Global GDP and Lube Demand Growth (%/Yr)

GDP growth* Lube demand growth

20

30

40

50

2007 2008 2009 2010 2011 2012 2013

Global Lubricant Consumption, 2007-2013 (Million Tons)

Global lubricants demand growth has generally tracked global GDP growth, but with

greater volatility

Global lubricants demand in 2013 has nearly recovered to the high water mark set

in 2007

* - Real GDP at market exchange rates.

© 2010 Kline & Company 5 © 2014 Kline & Company

From a variety of indicators, the message is clear – 2013H1 was bad for most of Europe’s major economies with a few exceptions

Country CV* PC* Steel prod

Germany -10.2% -8.1% 1.6%

UK 7.2% 10.0% -17.2%

Italy -19.5% -10.3% 17.3%

Spain -6.0% -4.9% -1.1%

France -9.4% -11.2% 4.5%

Retail sales in Eurozone grew for the first time in August 2013. Strong growth in Germany, modest in France. In Germany manufacturing PMI rose to

two year high and services PMI is the highest in six month French and Italian manufacturing PMI

turned to growth in July 2013. Tough Spain continued to decline, the

trajectory suggest it will return to growth shortly. Among other countries Poland has also

returned to growth, Turkey continues to stagnate, and contraction in Greece has slowed down.

Growth in 2013 H1 vs. 2012 H1

SOURCE: www.acea.be, Markit Economics, PMI Survey *CV = commercial vehicle registrations *PC = passenger car registrations

© 2010 Kline & Company 6 © 2014 Kline & Company

While things appear unchanged on the surface, a significant realignment of regional shares has occurred.

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012

Global Lubricant Consumption Share by Region, 2007-2012

Asia N America Europe AME S America

European share in global lubricant demand has declined from about 24% to 17%. In contrast, Asian share in global lubricant demand has grown from 33% to 43% in the last five years.

© 2010 Kline & Company 7 © 2014 Kline & Company

Most European countries have experienced a significant contraction in demand during the recession.

-6

-4

-2

0

2

Turkey Russia Poland Germany Benelux France UK Iberia Italy

Europe Lubricant Demand Growth By Major Countries (2008-2013) , CAGR %

Major markets Other

The contraction in demand in major countries accelerated Europe’s reducing share in global lubricant demand. The situation has not changed in 2013.

© 2010 Kline & Company 8 © 2014 Kline & Company

Despite the contraction in the last five years, the top five lubricant markets in Europe account for nearly two-thirds of the region demand.

Russia

Germany

UK France Italy

Turkey

Iberia

Ukraine

Benelux Poland

Minor

Other

Europe Lubricant Consumption by Country, 2013

Total: 6.6 million tons

© 2010 Kline & Company 9 © 2014 Kline & Company

In contrast to its position in the overall market, Europe accounts for the highest share of the global synthetic and semi-synthetic lubricant demand.

0% 20% 40% 60% 80% 100%

Total

Mineral

Synthetic

Semi-synthetic

Regional Share in Global Lubricant Demand by Product Type, 2013 (%)

Europe Asia North America South America AME

Note: Excludes Process Oils.

© 2010 Kline & Company 10 © 2014 Kline & Company

Germany leads in penetration of synthetic and semi-synthetic lubricants.

0

25

50

75

100

Germany France UK Italy Poland Benelux Russia Turkey Other

Synthetic and Semi-synthetic Lubricant Penetration by Country, 2013 (%)

Synthetic Semi-synthetic Conventional

High penetration of synthetics coupled with demographic factors makes Europe a declining market even without other economic factors.

Note: Excludes Process Oils.

© 2010 Kline & Company 11 © 2014 Kline & Company

What drives lubricant market in Europe?

Increased lubricant consumption due to: −Economic recovery −Manufacturing recovery −Changing regional base oil supply

Other factors include:

−Socio-economic trends − Lubricant quality improvements −Focus on fuel economy and CO2 reduction

© 2010 Kline & Company 12 © 2014 Kline & Company

What is the global economic outlook?

-6

-4

-2

0

2

4

6

8

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Real GDP* Growth Rate, 2009-2018 (%)

World North America Western Europe Asia & Australasia (incl Japan)

* GDP at market prices Source: www.eiu.com

Europe is projected to show improvement in economic growth rate.

© 2010 Kline & Company 13 © 2014 Kline & Company

Going by the purchasing manager index, most European countries are experiencing growth in manufacturing.

Country February January December Austria 53.0 54.1 54.1 Czech Republic 56.5 55.9 54.7 Euro Zone 53.2 54.0 52.7 France 49.7 49.3 47.0 Germany 54.8 56.5 54.3 Greece 51.3 51.2 49.6 Ireland 52.9 52.8 53.5 Italy 52.3 53.1 53.3 Netherlands 55.2 54.8 57.0 Poland 55.9 55.4 53.2 Russia 48.5 48.0 48.8 Spain 52.5 52.2 50.8 Turkey 53.4 52.7 53.5 U.K. 56.9 56.7 57.2 Source: www.markiteconomics.com

Manufacturing continues to contract in France and Russia

© 2010 Kline & Company 14 © 2014 Kline & Company

Example – Impact of growing synthetic and semi-synthetic products on overall PCMO demand.

0.9

1.0

1.1

1.2

1.3

2011 2013 2015 2017 2019 2021 2023

Vehicle Population and PCMO Consumption Growth in Select Countries*, 2011-2023

Vehicle population PCMO demand Synthetic and Semi-synthetic PCMO demand

* - Russia, Germany, UK, France, and Italy All data expressed as ratio of 2011 value

© 2010 Kline & Company 15 © 2014 Kline & Company

Emphasis on fuel economy, and a modernizing vehicle park, will drive an increase in the use of lighter viscosity PCMOs

0%

20%

40%

60%

80%

100%

2012 2017 2022 0Ws 5Ws 10Ws 15Ws Other multigrades Monogrades

PCMO Grade Shifts in Europe, 2012 to 2022

0%

20%

40%

60%

80%

100%

2012 2017 2022 0Ws / 5Ws 10Ws 15Ws Other multigrades Monogrades

HDMO Grade Shifts in Europe, 2012 to 2022

HDMO market will see moderate movement to lighter viscosity oils.

© 2010 Kline & Company 16 © 2014 Kline & Company

European Baseoil Supply, 2012-2021 (Million Tons)

0.0

2.0

4.0

6.0

8.0

10.0

European Lubricant Demand Growth (CAGR %, 2012 -16)

0

0.5

1

1.5

2

2.5

Synthetic Semi- Mineral

0

20

40

60

80

100

120

140

160

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Group I Group II/II+ Group III/III+ Naphthenics

KBD

While overall baseoil supply in Europe will be flat, share of Group II and Group III will grow rapidly. This will impact blending approach in the region and drive a further expansion of synthetics.

© 2010 Kline & Company 17 © 2014 Kline & Company

Lubricant consumption in Russia and Germany will drive demand in Europe

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5 R

ussi

a

Ger

man

y

UK

Iber

ia

Fran

ce

Italy

Ben

elux

Lubricant demand growth by major countries in Europe, CAGR %

(2013-2021)

Largest European Lubricant Market

Germany

Russia

United Kingdom

France

Italy

© 2010 Kline & Company 18 © 2014 Kline & Company

The net impact of these market drivers will be a flat lubricant market in Europe.

3

4

5

6

7

8

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Europe Lubricant Demand Outlook, 2009-2022 (Million Tons)

No growth (0.2%/yr growth) Contraction (-0.6%/yr growth) Historical

In the optimistic scenario, the overall demand will be flat with growth in some countries compensating the contraction in others.

© 2010 Kline & Company 19 © 2014 Kline & Company

European lubricant is a mature market but opportunities can still be pursued in various segments

Opportunities in Europe are not volume growth based, rather the growth that is expected to come from lubricants in the high performance categories

Market opportunities exist at both ends of the product spectrum – synthetic engine

oils and industrial lubricants– but present different challenges − Europe continues to be the largest market for high quality / high performance

lubricants as measured by penetration of synthetics and low viscosity engine oils.- Synthetic will grow 3x to 2x times faster than overall market

− Growing availability of Group II and Group III in this region will aid this trend − Group III supply in the region will expand significantly creating growth for Group

III based synthetic products. − In the industrial segment food-grade products showing biodegradability

credentials, but also fire resistant oils will continue to grow

© 2010 Kline & Company 20 © 2014 Kline & Company

European lubricant is a mature market but opportunities can still be pursued in various segments

To spot opportunities, lubricant marketers need to look beyond the Europe region as a whole. Opportunities exist at the country market level. Marketers need to think in terms of which market segment is addressable and which is not. − Lubricant marketers in Europe will need to look towards Eastern Europe and

East of the Suez for organic growth opportunities

Global reach, flexibility, quality consistency, strong reputation and reliability are key factors to succeed.

© 2010 Kline & Company 21 © 2014 Kline & Company 21

Questions or comments?

Americas ____________ Asia ___________ Europe ___________

If you require additional information about the contents of this document or the services that Kline provides, please contact:

Kline is a worldwide consulting and research firm dedicated to providing the kind of insight and knowledge that helps companies find a clear path to success. The firm has served the management consulting and market research needs of organizations in the chemicals, materials, energy, life sciences, and consumer products industries for over 50 years. For more information, visit www.KlineGroup.com.

Sharbel Luzuriaga Senior Consultant Phone: +420-222-33-00-19 Email: [email protected]

Kline & Company, Inc. 35 Waterview Blvd. Suite 305 Parsippany, NJ 07054 Phone: +1-973-435-6262 Fax: +1-973-435-6291 www.KlineGroup.com