overview of financial statements - wordpress.com · 23.08.2017 · financial accounting is...

TRANSCRIPT

Why Learn

Accounting?

Accounting

is the

language of

business

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Why Learn

Accounting?

Accounting | Balkrishna Parab | [email protected]

Accounting

helps us

know the

score

Why Learn

Accounting?

Accounting | Balkrishna Parab | [email protected]

Accounting

is the

language of

business

Why Learn

Accounting?

Accounting | Balkrishna Parab | [email protected]

Accounting

is the

language of

business

Accounting

is the

language of

business

Accounting

is the

language of

business

Accounting | Balkrishna Parab | [email protected]

Financial Accounting

Cost Accounting

Government Accounting

Management Accounting

Accounting | Balkrishna Parab | [email protected]

Accounting

Financial

Accounting

Cost

Accounting

Management

Accounting

Government

Accounting

Financial accounting is concerned with the aggregation

of financial information into external reports.

Cost accounting measures and reports financial and

non-financial information related to the organisation’s

acquisition or consumption of resources.

Management accounting measures and reports

financial and non-financial information with the goal of

assisting managers in achieving corporate goals.

Government accounting uses a unique accounting

framework to create and manage funds related to the

provision of services by a government entity.

Accounting | Balkrishna Parab | [email protected]

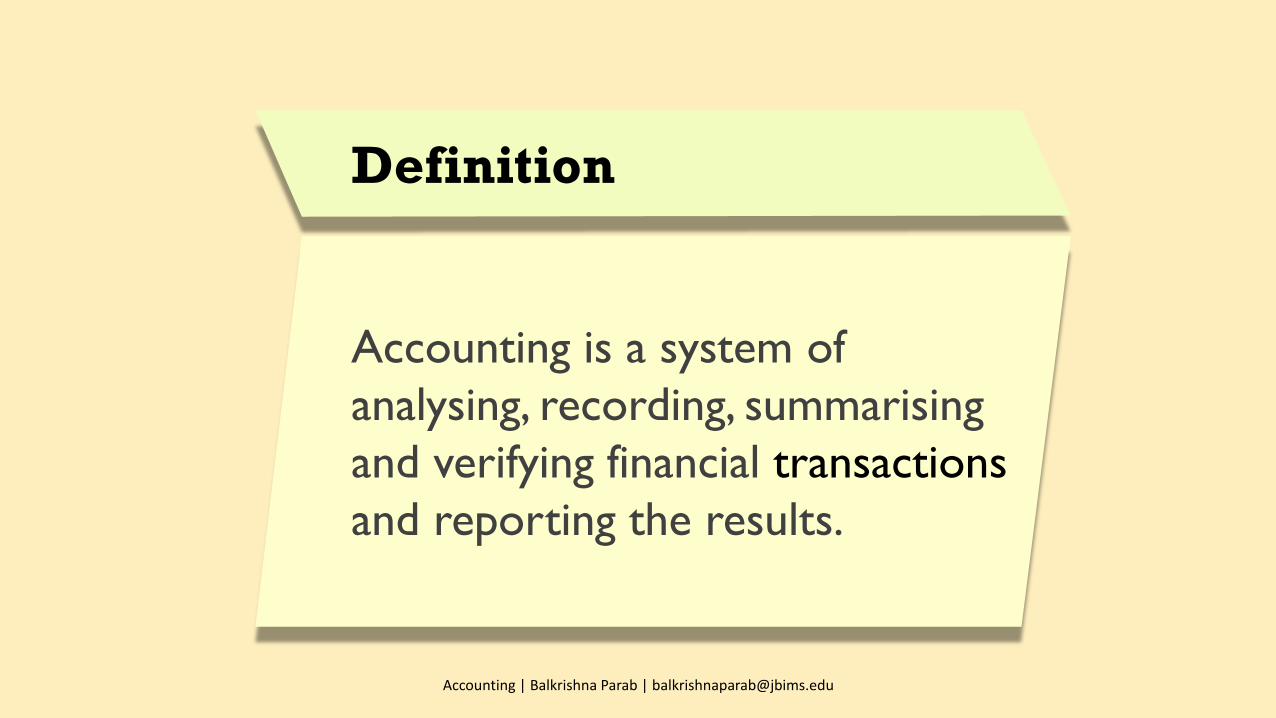

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

Defining

Accounting

Accounting | Balkrishna Parab | [email protected]

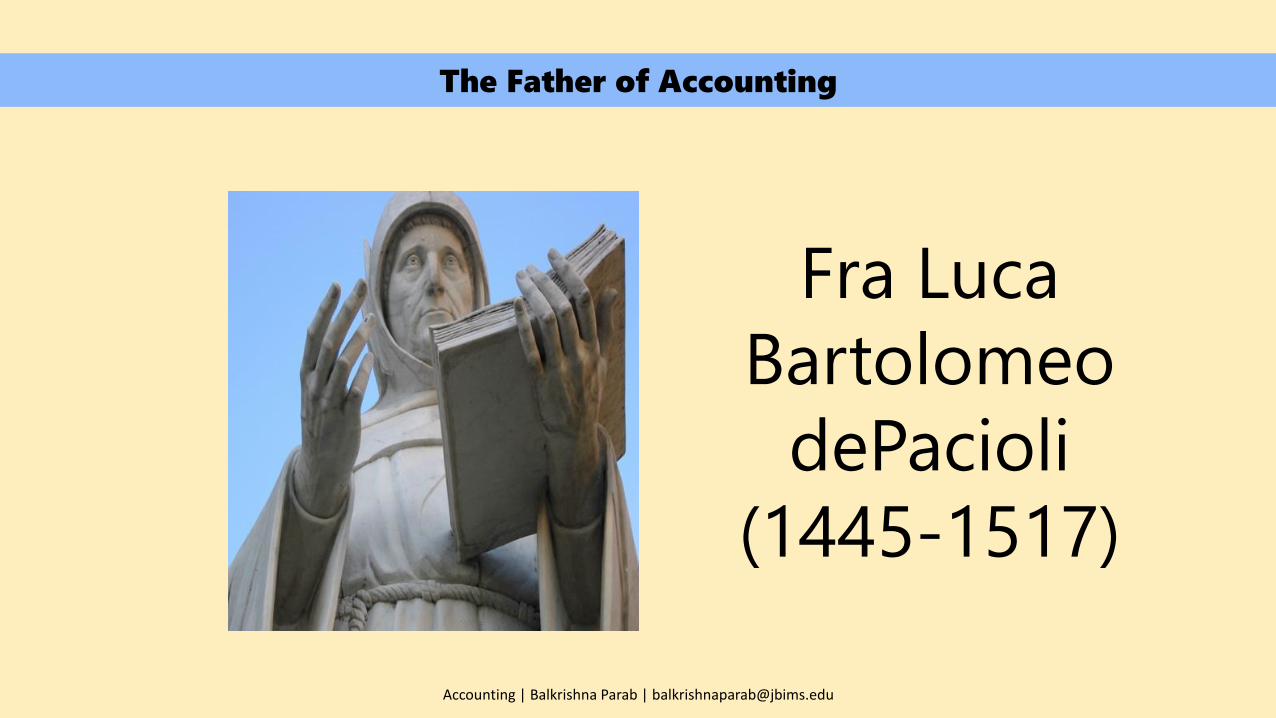

Fra Luca

Bartolomeo

dePacioli

(1445-1517)

The Father of Accounting

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

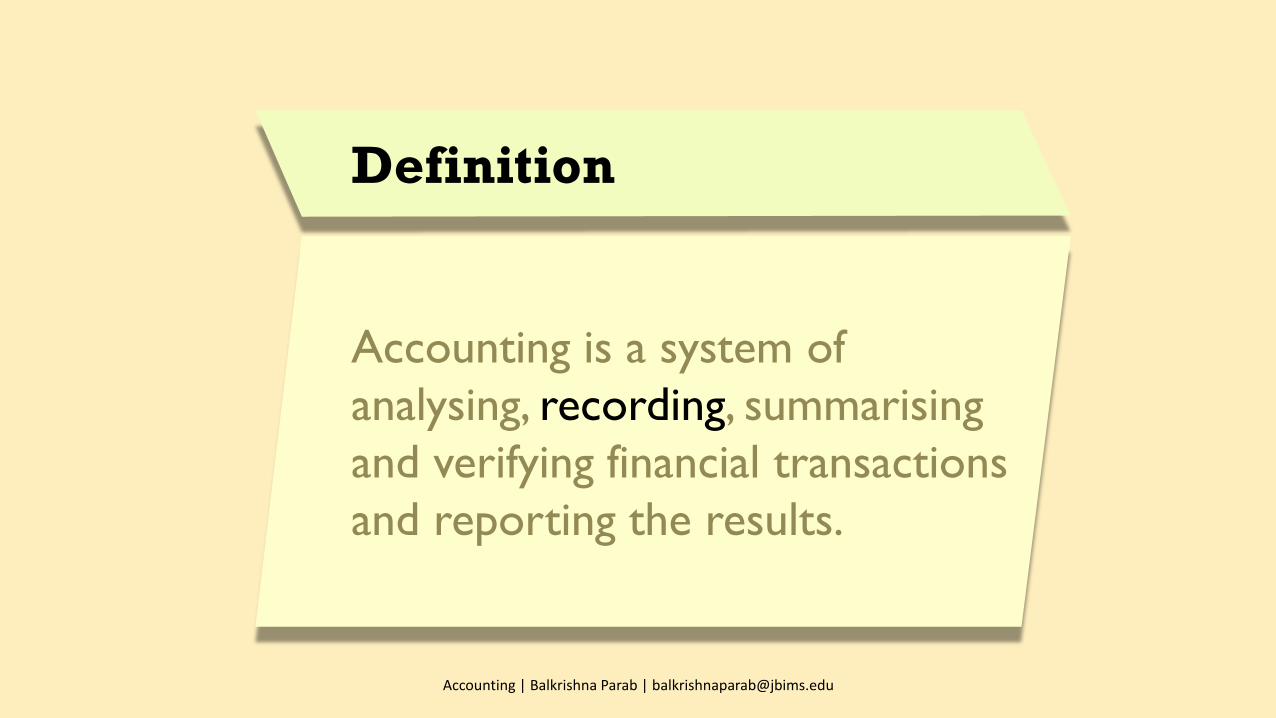

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

Definition

Accounting is a system of

analysing, recording, summarising

and verifying financial transactions

and reporting the results.

Accounting | Balkrishna Parab | [email protected]

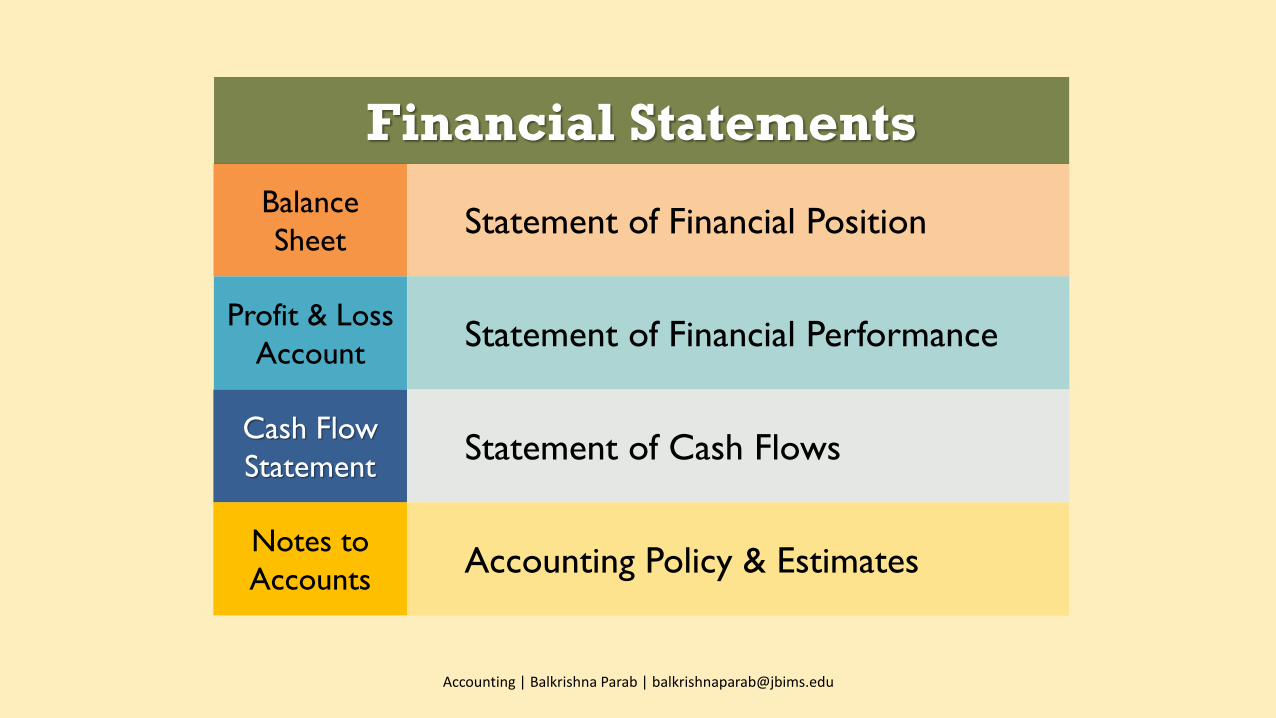

Balance

Sheet

Profit & Loss

Account

Cash Flow

Statement

Statement of Financial Position

Statement of Financial Performance

Statement of Cash Flows

Accounting | Balkrishna Parab | [email protected]

Notes to

AccountsAccounting Policy & Estimates

Financial Statements

Balance

Sheet

Profit & Loss

Account

Cash Flow

Statement

Operating Activities

Investment Activities

Financing Activities

Revenue

Expenditure

Profit (Loss)

Assets

Liabilities

Owners’ Equity

Financial Position

Financial Performance

Cash Flows

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

A company purchased a plot of land on April 1, 1967 for

Rs. 500,000; its current worth is Rs. 500 crores.

In the company’s balance sheet prepared on March 31,

2017 what amount should be mentioned with respect to

this plot of land?

Standard Setting Process

Accounting | Balkrishna Parab | [email protected]

Identify Need for a Standard

Draft Proposed Standard

Constitute a Study Group

Prepare Preliminary Standard

Circulate to Business

Associations

PrepareExposure

Draft

Circulate to Public

Elicit Public Comments

Release the Standard

Accounting | Balkrishna Parab | [email protected]

International Financial

Reporting Standards (IFRS)

Accounting | Balkrishna Parab | [email protected]

Elements of

Financial

Statements

Accounting | Balkrishna Parab | [email protected]

Asset Liabilities Income Expenditure

Equity Profit

Balance Sheet Profit & Loss Account

Financial

Statements

Cash Flow

Statement

Profit and

Loss Account

Balance

Sheet

Accounting | Balkrishna Parab | [email protected]

Balance Sheet

A balance sheet is a financial statement that

summarizes a company's assets, liabilities and

shareholders' equity at a specific point in time.

These three balance sheet segments give investors an

idea as to what the company owns and owes, as well

as the amount invested by shareholders.

Accounting | Balkrishna Parab | [email protected]

Profit and Loss Account

The profit and loss account is a financial statement that

reports a company's financial performance over a specific

accounting period.

Financial performance is assessed by giving a summary of

how the business incurs its revenues and expenses. It also

shows the net profit or loss incurred over a specific

accounting period.

Accounting | Balkrishna Parab | [email protected]

Cash Flow Statement

The cash flow statement (CFS) shows the amounts of cash

and cash equivalents entering and leaving a company. The

CFS allows investors to understand how a company's

operations are running, where its money is coming from, and

how it is being spent.

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Balance

Sheet

Balance

Sheet

Assets

Equity and

Liabilities

Current

Liabilities

Non Current

Liabilities

Equity

Non Current

Assets

Current

AssetsAccounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Equity

Share Application

Money

Share Warrants

Reserves of

Surplus

Share Capital

Accounting | Balkrishna Parab | [email protected]

Equity

Equity, also called shareholders' equity, is equal to a

company's total assets minus its total liabilities.

Equity represents the net value of a company, or the

amount that would be returned to shareholders if all

the company's assets were liquidated and all its debts

repaid.

Accounting | Balkrishna Parab | [email protected]

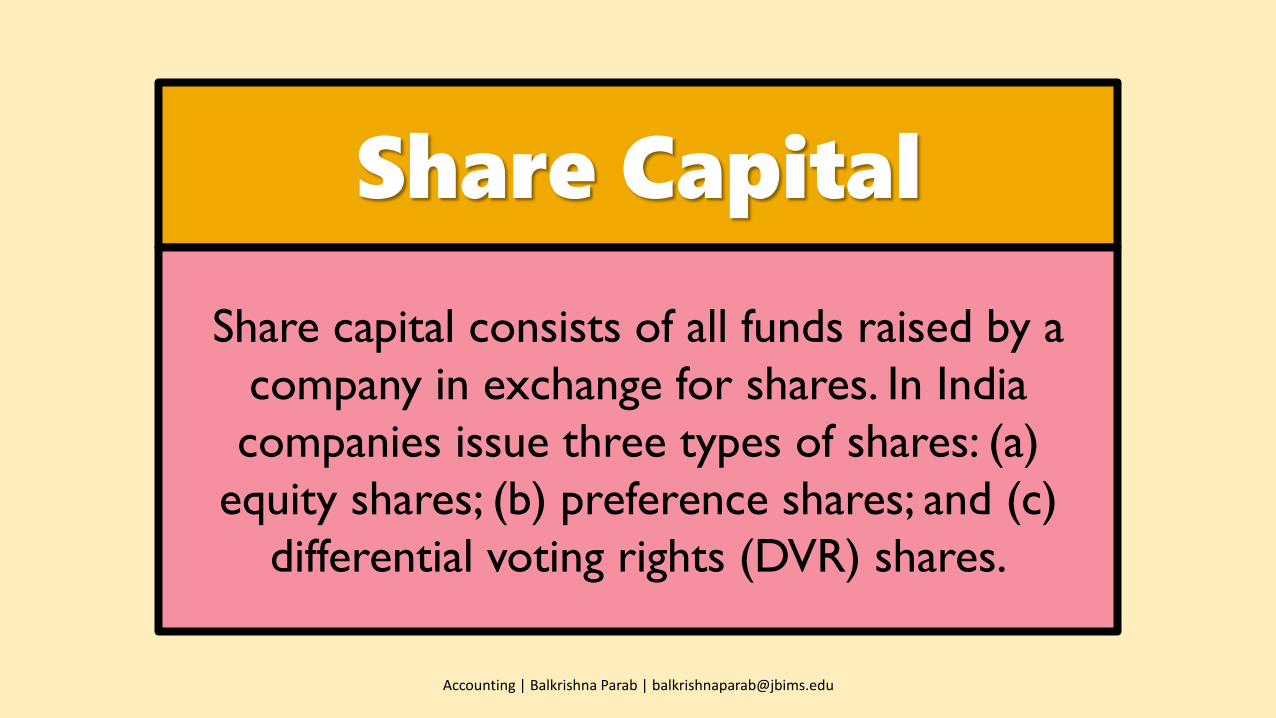

Share Capital

Share capital consists of all funds raised by a

company in exchange for shares. In India

companies issue three types of shares: (a)

equity shares; (b) preference shares; and (c)

differential voting rights (DVR) shares.

Accounting | Balkrishna Parab | [email protected]

Reserves and Surplus

Reserves and surplus refer to the profits of the

company not paid out as dividends, but retained by

the company to be reinvested in its core business, or

to pay debt. It is recorded under ‘equity’ on the

balance sheet.

Accounting | Balkrishna Parab | [email protected]

Share Warrant

A share warrant is a security that entitles the

holder to buy the underlying stock of the

issuing company at a fixed price called exercise

price until the expiry date.

Accounting | Balkrishna Parab | [email protected]

Share Application Money

Share application money is the amount

received by a company from applicants who

wish to purchase its shares. It is the money

received in respect to an initial public offering

of shares.

Accounting | Balkrishna Parab | [email protected]

Equity

Share

Applications

Share

Warrants

Reserves of

Surplus

Share Capital

Preference

Share

DVR Share

Equity Share

Accounting | Balkrishna Parab | [email protected]

Equity Shares

Equity shares were earlier known as ordinary shares.

The holders of these shares have voting right in the

shareholder meetings. Exercising these voting rights

equity shareholders elect a board of director to run

the company on their behalf.

Accounting | Balkrishna Parab | [email protected]

Preference Share

A preference share, also called as preferred stock, enjoy two

preferences over equity shares: (a) they are entitled to get a

fixed dividend before dividends are paid to holders of equity

shares; and (b) at the time of winding up of the company,

capital is repaid to preference shareholders prior to the

return of equity capital. Generally, preference shares do not

carry voting rights.

Accounting | Balkrishna Parab | [email protected]

DVR Share

A DVR share is like an equity share, but it provides

fewer voting rights to the shareholder. In India, listed

companies are no longer allowed to issue DVR

shares, however, unlisted companies are free to issue

such shares.

Accounting | Balkrishna Parab | [email protected]

Liabilities

Current

Liabilities

Non Current

Liabilities

Accounting | Balkrishna Parab | [email protected]

Liability

A liability is a present obligation of the

entity arising from past events, the

settlement of which is expected to result

in an outflow of resources embodying

economic benefits.

Accounting | Balkrishna Parab | [email protected]

Noncurrent Liabilities

Noncurrent liabilities are those liabilities

that not due for settlement within one

year. These liabilities are separately

classified in an entity's balance sheet, away

from current liabilities.

Accounting | Balkrishna Parab | [email protected]

Current Liability

A current liability is a liability that is payable

within one year. The cluster of liabilities

comprising current liabilities is closely watched,

for a business must have sufficient liquidity to

ensure that they can be paid off when due.

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Non Current

Liabilities

Other Non Current

Liabilities

Deferred Tax

Liabilities

Long Term

Provisions

Long Term

Borrowings

Accounting | Balkrishna Parab | [email protected]

Long Term Borrowings

Borrowing refers to obtaining or receiving

money on loan with the promise or

understanding of returning it or its equivalent.

Long term borrowings obligations that are to

come due in a greater than twelve-month

period.

Accounting | Balkrishna Parab | [email protected]

Long Term Provision

A provision is an amount set aside from profits in the

accounts of an entity for a known liability, or for the

diminution in the value of an asset.

A long term provision is an amount set aside for a

liability that is expected to come due in a greater

than twelve-month period.

Accounting | Balkrishna Parab | [email protected]

Deferred Tax Liabilities

A deferred tax liability is one that a company

owes and does not pay at that current point,

although it will be responsible for paying it at

some point in the future.

A deferred tax liability arises due to differences in

accounting practices and tax regulations.

Accounting | Balkrishna Parab | [email protected]

Other Non Current Liabilities

Other noncurrent liabilities are ones

that cannot be categorised under (a)

long term borrowings; (b) long term

provisions; (c) deferred tax liabilities.

Accounting | Balkrishna Parab | [email protected]

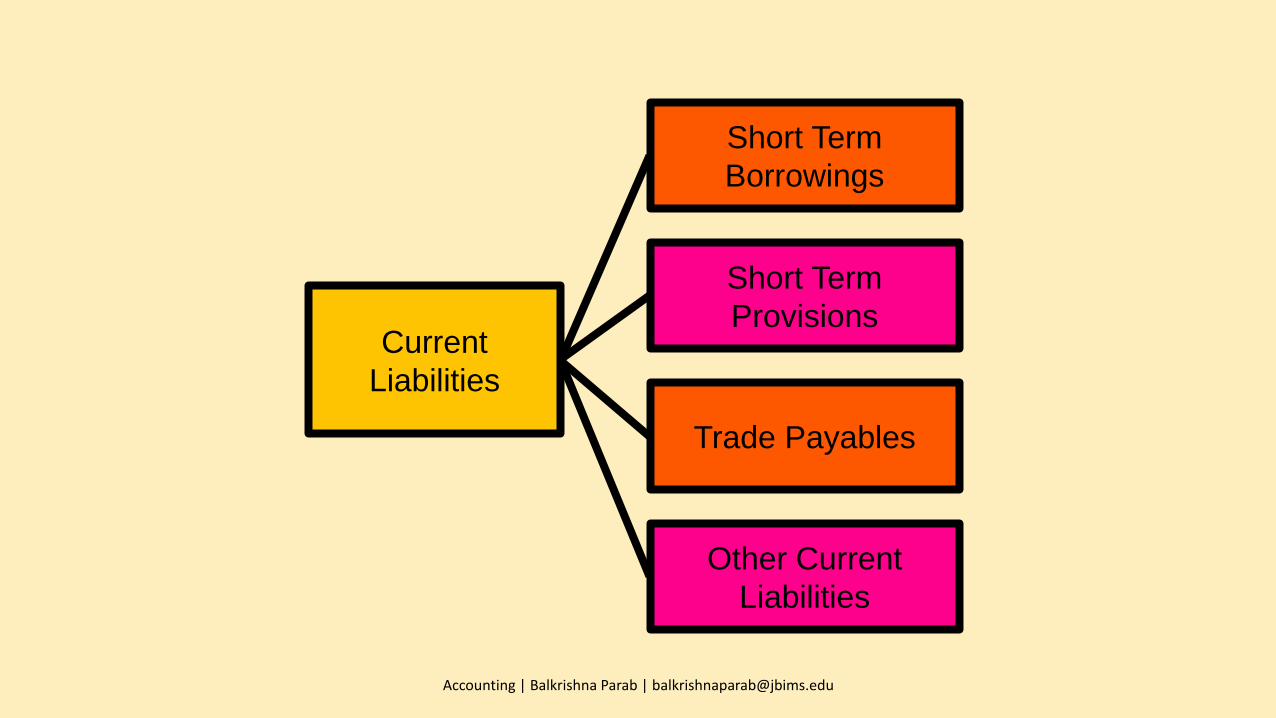

Current

Liabilities

Other Current

Liabilities

Trade Payables

Short Term

Provisions

Short Term

Borrowings

Accounting | Balkrishna Parab | [email protected]

Short Term Borrowings

Short term borrowings obligations

that are to come due in a within a

twelve-month period.

Accounting | Balkrishna Parab | [email protected]

Short Term Provisions

A short term provision is an

amount set aside for a liability that

is expected to come due within a

twelve-month period.

Accounting | Balkrishna Parab | [email protected]

Trade Payables

A trade payable is an amount billed to a

company by its suppliers for goods

supplied to or services consumed by

the company in the ordinary course of

business.

Accounting | Balkrishna Parab | [email protected]

Other Current Liabilities

Other current liabilities are ones that

cannot be categorised under (a) short

term borrowings; (b) short term

provisions; (c) trade payables.

Accounting | Balkrishna Parab | [email protected]

Asset

An asset is a right or access to

future economic benefits,

controlled by the entity as a

result of past transaction

Accounting | Balkrishna Parab | [email protected]

Non Current Assets

A noncurrent asset is one where the

right is expected to subsist, or the

access to future economic benefits is

expected to accrue to the entity, for a

period beyond twelve months.

Accounting | Balkrishna Parab | [email protected]

Current assets

Current assets are assets used by the

entity and intended to be sold/

consumed in the ordinary course of

business within a period of twelve

months

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Non Current

Assets

Fixed Assets

Non Current

Investments

Deferred Tax

Assets

Long Term Loans

and Advances

Other Non Current

Assets

Accounting | Balkrishna Parab | [email protected]

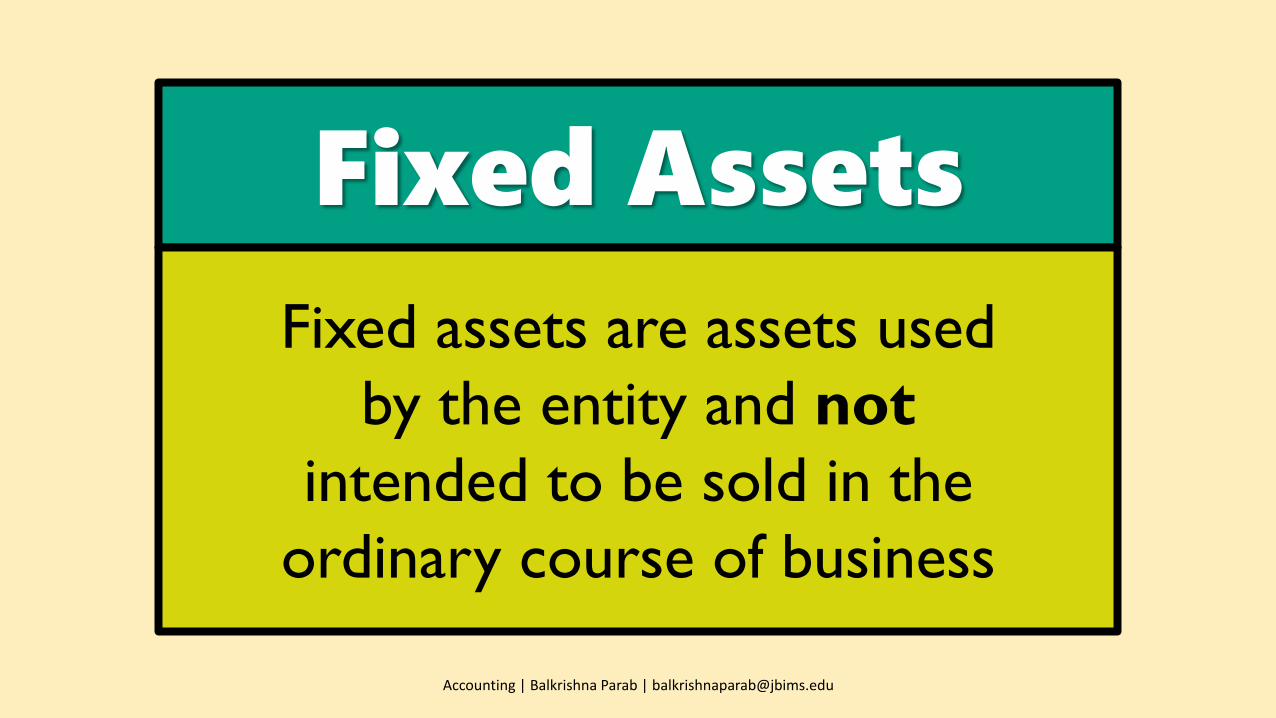

Fixed Assets

Fixed assets are assets used

by the entity and not

intended to be sold in the

ordinary course of business

Accounting | Balkrishna Parab | [email protected]

Non Current Investments

Investments are assets not used by the

entity in the ordinary course of business.

A non current investment is one that is

intended to be held for a period beyond

twelve months.

Accounting | Balkrishna Parab | [email protected]

Deferred Tax Assets

A deferred tax asset is one that a company

has paid but it expects to recover it at some

point in the future.

A deferred tax asset arises due to

differences in accounting practices and tax

regulations.

Accounting | Balkrishna Parab | [email protected]

Long Term Loans and

Advances

Long term loans and advances are monies lent

or given as an advance by the entity to others,

usually suppliers and employees, and which it

expects to recover in a period beyond twelve

months.

Accounting | Balkrishna Parab | [email protected]

Other Noncurrent Assets

Other noncurrent assets are ones that

cannot be categorised as: (a) fixed assets;

(b) non current investments; (c) deferred

tax assets; and (d) long term loans and

advances.

Accounting | Balkrishna Parab | [email protected]

Fixed Assets

IAUD

Capital Work

in Progress

Intangible

Assets

Tangible

Assets

Accounting | Balkrishna Parab | [email protected]

Tangible Assets

Tangible assets are fixed assets

that have physical substance.

Accounting | Balkrishna Parab | [email protected]

Intangible Assets

An intangible asset is a separable

non-monetary asset not having

physical substance.

Accounting | Balkrishna Parab | [email protected]

Capital Work in Progress

Capital work-in-progress is a

tangible asset that is under

construction as on the balance

sheet date.

Accounting | Balkrishna Parab | [email protected]

IAUD

Intangible assets under development

(IAUD) are intangible assets under

development as on the balance

sheet date.

Accounting | Balkrishna Parab | [email protected]

Current

Assets

Inventories

Trade

Receivables

Cash and Bank

Short Term Loans

and Advances

Short Term

Investments

Accounting | Balkrishna Parab | [email protected]

Inventories

Inventory is the raw materials, work-in-

process products and finished goods that are

considered to be the portion of a business's

assets that are ready or will be ready for sale.

Accounting | Balkrishna Parab | [email protected]

Trade Receivables

Trade receivables are amounts billed by a

business to its customers when it

supplies goods or services to them in the

ordinary course of business.

Accounting | Balkrishna Parab | [email protected]

Cash and Bank

These current assets are the

balance of cash, or cash

equivalents and balance of bank

accounts of the company.

Accounting | Balkrishna Parab | [email protected]

Short Term Loans & Advances

Short term loans and advances are monies

lent or given as an advance by the entity to

others, usually suppliers and employees, and

which it expects to recover within a period of

twelve months.

Accounting | Balkrishna Parab | [email protected]

Short Term Investments

A short term investments is an asset not

used by the entity in the ordinary course

of business and which is intended to be

held for a period of twelve months or

less.

Accounting | Balkrishna Parab | [email protected]

Profit and

Loss Account

Profit and Loss Account

The profit and loss account is a financial statement that

reports a company's financial performance over a specific

accounting period.

Financial performance is assessed by giving a summary of how

the business incurs its revenues and expenses. It also shows

the net profit or loss incurred over a specific accounting

period.

Accounting | Balkrishna Parab | [email protected]

Profit and

Loss Account

Profit/ Loss

Expenses

Income

Accounting | Balkrishna Parab | [email protected]

Income

Income is increases in economic benefits in the form

of inflows or enhancements of assets or decreases of

liabilities that result in increases in equity, other than

those relating to contributions from equity

participants.

Accounting | Balkrishna Parab | [email protected]

IncomeIncrease in

Assets

Inflows

Decrease in

Liabilities

Enhance

ment of

Equity

Oth

er

than

Contr

ibution b

y

equity

par

tici

pan

ts

Accounting | Balkrishna Parab | [email protected]

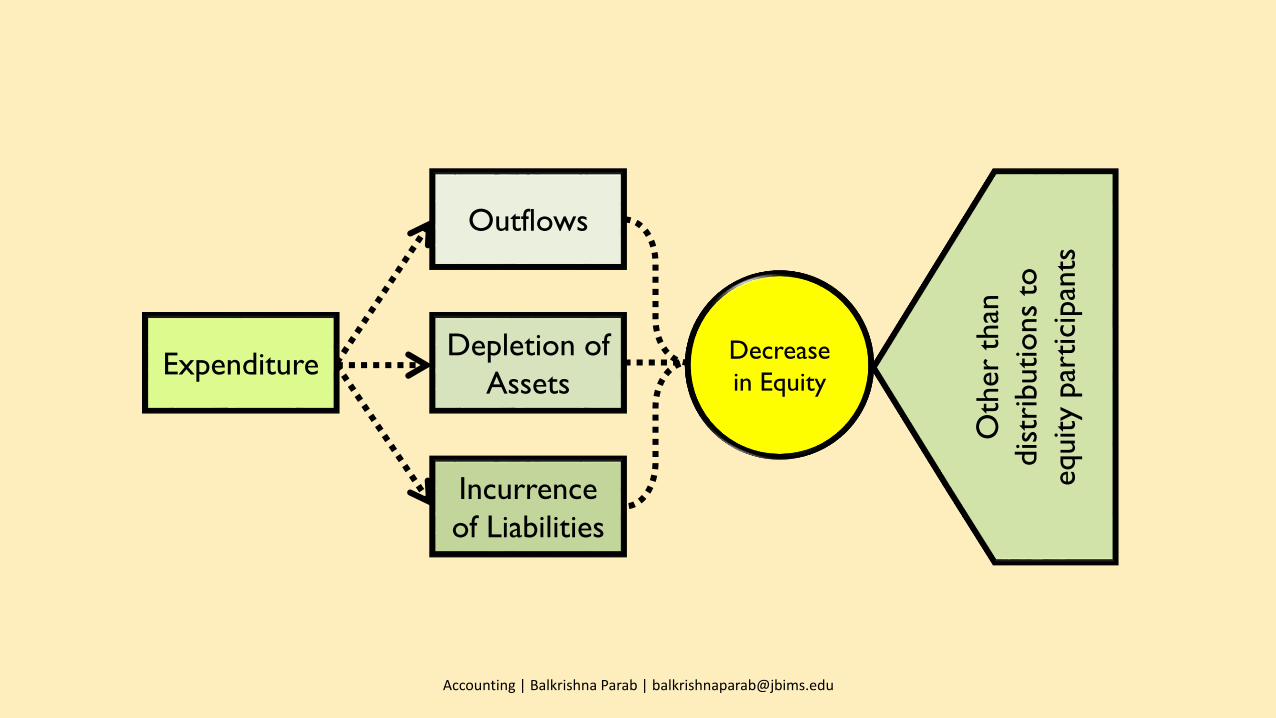

Expenses

Expenses are decreases in economic benefits in the

form of outflows or depletions of assets or

incurrences of liabilities that result in decreases in

equity, other than those relating to distributions to

equity participants.

Accounting | Balkrishna Parab | [email protected]

ExpenditureDepletion of

Assets

Outflows

Incurrence

of Liabilities

Decrease

in Equity

Oth

er

than

dis

trib

utions

to

equity

par

tici

pan

ts

Accounting | Balkrishna Parab | [email protected]

Operating Income

Operating income or operating revenue is

revenue generated from a company's day-to-day

business activities, which means revenue posted

from selling the company's products and

services.

Accounting | Balkrishna Parab | [email protected]

Non-operating Income

Non-operating income is income

earned by a company from activities

other than day-to-day business

activities.

Accounting | Balkrishna Parab | [email protected]

Expenses

Non

Operating

Expenses

Operating

Expenses

Accounting | Balkrishna Parab | [email protected]

Operating Expenses

Operating expenses are expenses

incurred by a company on its day-

to-day business activities.

Accounting | Balkrishna Parab | [email protected]

Non-operating Expenses

Non-operating expense is expense

incurred by a company on activities

other than day-to-day business

activities.

Accounting | Balkrishna Parab | [email protected]

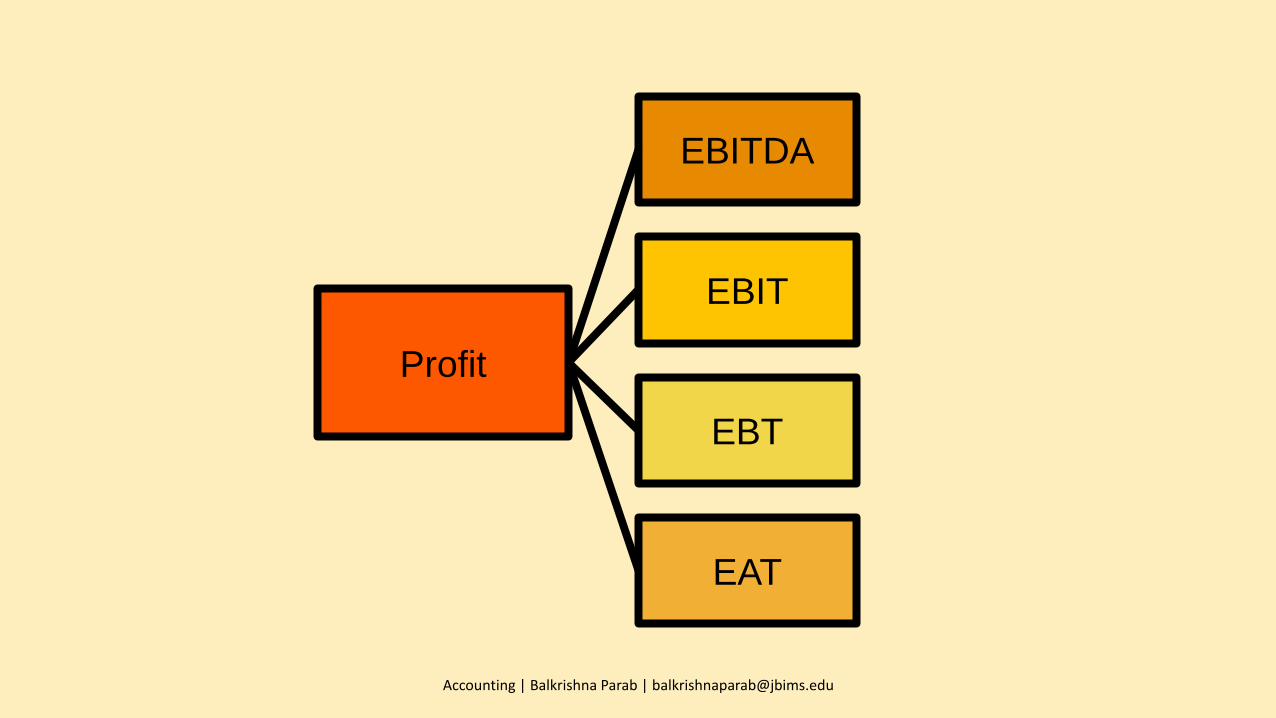

ProfitProfit is a financial benefit that is realized when the amount of revenue gained from a business activity exceeds the expenses, costs and taxes needed to

sustain the activity. Any profit that is gained goes to the shareholders, who may or may not decide to

spend it on the business.

Accounting | Balkrishna Parab | [email protected]

EBITDA

EBITDA stands for earnings before interest, taxes, depreciation and amortization. EBITDA is one

indicator of a company's financial performance and is used as a proxy for the earning potential of a business, although doing so has its drawbacks.

Accounting | Balkrishna Parab | [email protected]

EBITEBIT (Earnings Before Interest and Tax) is an indicator

of a company's profitability, calculated as revenue minus expenses, excluding tax and interest.

EBIT is also referred to as "operating earnings", "operating profit" and "profit before interest and

taxes (PBIT).

Accounting | Balkrishna Parab | [email protected]

EBT

Earnings before tax (EBT) is an indicator of a company's financial performance. EBT is a line item on a company's

profit and loss account that shows how much the company has earned after the cost of goods sold (COGS), interest,

depreciation, general and administrative expenses and other operating expenses have been subtracted from gross sales.

Accounting | Balkrishna Parab | [email protected]

EAT

Earnings after taxes, abbreviated as EAT, refers to financial performance for an accounting period. It is already after taxation and it is available for distribution between the

shareholders and the company. EAT is also referred to as net income (NI), profit after taxes

(PAT) and net profit (NP)

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

Cash Flow

Statements

Cash Flow Statement

The cash flow statement (CFS) shows the amounts

of cash and cash equivalents entering and leaving a

company. The CFS allows investors to understand

how a company's operations are running, where its

money is coming from, and how it is being spent.

Accounting | Balkrishna Parab | [email protected]

Cash Flow

Statement

Financing

Activities

Investing

Activities

Operating

Activities

Accounting | Balkrishna Parab | [email protected]

Cash Flow From

Operating Activities

Cash flow from operating activities (CFO)

indicates the money a company brings in from

ongoing, regular business activities, such as

manufacturing and selling goods or providing a

service.

Accounting | Balkrishna Parab | [email protected]

Cash Flow From

Investing Activities

Cash flow from investing activities is an item on the cash

flow statement that reports the aggregate change in a

company's cash position resulting from any gains (or losses)

from investments in the financial markets and operating

subsidiaries and changes resulting from amounts spent on

investments in capital assets such as plant and equipment.

Accounting | Balkrishna Parab | [email protected]

Cash Flow From

Financing Activities

Cash flow from financing activities is a category in a

company’s cash flow statement that accounts for

external activities that allow a firm to raise capital

and repay investors, such as issuing cash dividends,

adding or changing loans or issuing more stock..

Accounting | Balkrishna Parab | [email protected]

Accounting | Balkrishna Parab | [email protected]

BALKRISHNA PARAB teaches law, accounting and finance

at the Jamnalal Bajaj Institute of Management Studies, 164,

DN House, HT Parekh Marg, Backbay Reclamation. Mumbai

400 020, India. Cell: 9833528351

eMail: balkrishnaparab@jbims,edu