overview : industry analysis wai chamornmarn thammasat university 2006

TRANSCRIPT

Overview : Industry Analysis

Wai ChamornmarnThammasat university 2006

2 Industry Analysis

International Trade Theory

• Why do nations trade with each-other?

• How do different theories explain trade flows?

• How does free trade raise the economic welfare of all participating nations? Any disagreements?

• Can government actively influence a country’s competitive advantage?

• Why is an understanding of trade theory important for managers?

3 Industry Analysis

An Overview of Trade Theory

• Free Trade occurs when a government does not attempt to influence, through quotas or duties, what its citizens can buy from another country or what they can produce and sell to another country.

• The Benefits of Trade allow a country to specialize in the manufacture and export of products that can be produced most efficiently in that country.

• The Pattern of International Trade displays patterns that are easy to understand (Saudi Arabia/oil or China/crawfish). Others are not so easy to understand (Japan and cars).

• The history of Trade Theory and Government Involvement presents a mixed case for the role of government in promoting exports and limiting imports. Later theories appear to make a case for limited involvement.

4-7

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

4 Industry Analysis

Capitalism Requires

• Consumers.

• Monopolies and imperfect forms of competition to facilitate the accumulation of capital. Pure competition feeds the market economy, not necessarily capitalism.

• Capital and credit have always been the surest way of capturing and controlling a foreign market. True in all forms of capitalism since the 15th century Florentines.

- 13th century - Florence.

- 16th century - Augsburg, Antwerp, Genoa,

- 18th century - Amsterdam and London

- 19th and 20th centuries - New York

- 21st century - Beijing??

Industry Analysis www. wai .bangkaew.comDate

Amartya Sen – The Modern Face of Capitalism?

• 1998 Nobel Prize winner in Economic Science.

• Developed and developing nations face the persistence of poverty, hunger, violations of basic freedoms, environmental issues and concerns about sustainability of economic and social lives.

• Overcoming these problems is central to development.

• “Expansion of freedom is viewed…both as the primary end and as the principal means of development.”

• “Development consists of the removal of various types of unfreedoms that leave people with little choice and little opportunity of exercising their reasoned agency.”

6 Industry Analysis

Sen’s Prescription

• What people can achieve is influenced by:

- Economic opportunities (process vs. opportunity freedom).

- Political liberties.

- Social power.

- Conditions of good health.

- Basic education.

- Encouragement and cultivation of initiatives.

- Freedom to enter labor markets and exchange freely.

7 Industry Analysis

Rod’s 21st Century Synthesis

• Capitalism is becoming more accessible with the advent of globalization and technology.

• Knowledge and human capital are becoming the most important sources of capital (knowledge capitalism).

• Increase transience and fragmentation in “centers of gravity” of capitalism.

• Decreased periods of competitive advantage.

• More freedom in the world.

8 Industry Analysis

Free Trade

• Free trade refers to a situation where a government does not attempt to influence through quotas or duties what its citizens can buy from another country or what they can produce and sell to another country.

- USA imports most of the sneakers and jeans consumed although these can be produced at home. Why???

9 Industry Analysis

International Trade Theory

• What is international trade?

- Exchange of raw materials and manufactured goods (and services) across national borders

• Classical trade theories:

- explain national economy conditions--country advantages--that enable such exchange to happen

• New trade theories:

- explain links among natural country advantages, government action, and industry characteristics that enable such exchange to happen

10 Industry Analysis

Classical Country-Based Theories

• Mercantilism

- Emerged in England in the mid-16th century

- It is in a country’s best interest to maintain a trade surplus, to export more than it imports.

- Takes an us-versus-them view of trade; other country’s gain is our country’s loss

- Government intervention to achieve a surplus in the balance of trade.

- Neo-mercantilism views persist today

11 Industry Analysis

Free Trade supporting theories

• Show that specialization of production and free flow of goods grow all trading partners’ economies.

- Absolute Advantage (Adam Smith, The Wealth of Nations, 1776)

• countries differ in their ability to produce goods efficiently, and that a country has an absolute advantage in the production of a product when it is more efficient than any other country in producing it.

• countries should specialize in the production of goods for which they have an absolute advantage and then trade these goods for the goods produced by other countries.

12 Industry Analysis

Absolute Advantage

• Adam Smith: The Wealth of Nations, 1776

• Mercantilism weakens a country in the long run and enriches only a few segments

• A country should specialize in and export products for which it has absolute advantage; import others

• A country has absolute advantage when it is more productive than another country in producing a particular product

Rice

Ghana

40

G'

15

50

S. Korea

30

Cocoa

13 Industry Analysis

• When each country has an absolute advantage in one of the products, it is clear that trade is beneficial. But what if one country has an absolute advantage in both products?

- Comparative Advantage (David Ricardo, Principles of Political Economy.1817)

• it makes sense for a country to specialize in the production of those goods that it produces most efficiently and to buy the goods that it produces less efficiently from other countries, even if this means buying goods from other countries that it could produce more efficiently itself.

• Many assumptions

Free Trade supporting theories, cont’d.

14 Industry Analysis

Comparative Advantage

• David Ricardo: Principals of Political Economy, 1817

• Country should specialize in the production of those goods in which it is relatively more productive... even if it has absolute advantage in all goods it produces

• Absolute advantage is really a special case of comparative advantage

Rice

Cocoa 30

12

15

50

Ghana

S. Korea

15 Industry Analysis

Classic Theory Limitations

• Fundamentally: Free Trade expands the world “pie” for goods/services

Theory Limitations

• Simple world (two countries, two products)

• no transportation costs

• no price differences in resources

• resources immobile across countries

• constant returns to scale

• each country has a fixed stock of resources and no efficiency gains in resource use from trade

• full employment

16 Industry Analysis

Simple Extensions of the Ricardian Model

• Immobile resources:

- Resources do not always move easily from one economic activity to another.

• Diminishing returns:

- More a country produces, at some point, will require more resources (diminishing returns to specialization).

- Different goods use resources in different proportions.

• However:

- Free trade might increase a country’s stock of resources (as labor and capital arrives from abroad), and

- Increase the efficiency of resource utilization.

4-16

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

17 Industry Analysis

Ghana’s PPF under Diminishing Returns

Coco

a

Rice

G’

G

0

Figure 4.3

18 Industry Analysis

The Influence of Free Trade on the PPF

Figure 4.4

Coco

a

Rice

G’

PPF2

0

PPF1

19 Industry Analysis

Heckscher (1919)-Ohlin (1933) Theory

• The pattern of international trade depends on differences in factor endowments not on differences in productivity

• Absolute amounts of factor endowments matter• Products differ according to the types of factors that they need as inputs• A country has a comparative advantage in producing products that

intensively use factors of production (resources) it has in abundance• Factors of production: labor, capital, land, human resources, technology• Leontief paradox:

- US has relatively more abundant capital yet imports goods more capital intensive than those it exports

- Explanation(?): • US has special advantage on producing new products made with innovative

technologies• These may be less capital intensive till they reach mass-production state

20 Industry Analysis

International Product Life-Cycle (Vernon)

• As products mature both the location of sales and the optimal production location will change affecting the flow and direction of trade. - Most new products initially conceived and produced in the US in 20th

century- US firms kept production close to the market

• Aid decisions; minimize risk of new product introductions• Demand not based on price yet; low production cost not an issue

- Limited initial demand in other advanced countries • Exports more attractive than production there initially

- With demand increase in advanced countries• Production follows there.

- With demand expansion elsewhere• Product becomes standardized• production moves to low production cost areas• Product now imported to US and to advanced countries

21 Industry Analysis

The Product Life-Cycle Theory

Figure 4.5

4-24

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

production

consumptionExports

160

140

120

100

80 60 40 200

United States

Other Advanced Countries

Developing Countries

Stages of Production Development

New Product Standardized ProductMaturing Product

Imports

Imports

Exports

Exports

Imports

160

140

120

100

80 60 40 200

160

140

120

100

80 60 40 200

22 Industry Analysis

The New Trade Theory

• Began to be recognized in the 1970s.

• Deals with the returns on specialization where substantial economies of scale are present.

- Specialization increases output, ability to enhance economies of scale increase.

• In addition to economies of scale, learning effects also exist.

- Learning effects are cost savings that come from “learning by doing”.

4-25

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

23 Industry Analysis

Application of the New Trade Theory

• Typically, requires industries with high, fixed costs.

• World demand will support few competitors.

• Competitors may emerge because “they got there first”.• First-mover advantage.

• Some argue that it generates government intervention and strategic trade policy.

4-26

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

24 Industry Analysis

First-Mover Advantage

• Economies of scale may preclude new entrants.

• Role of the government.

4-27

McGraw-Hill/Irwin © 2003 The McGraw-Hill Companies, Inc., All Rights Reserved.

25 Industry Analysis

Competitive Advantage• Porter’s “National Diamond”

- “Advantages throughout the ‘diamond’ are necessary for achieving and sustaining competitive success … [but]

• Advantage in every determinant is not a prerequisite…” (73)

26 Industry Analysis

Competitive Advantage

• Factors matter but may enhance CA through their absence:

- “an abundance of factors may undermine instead of enhance competitive advantage. Selective disadvantages in factors, through influencing strategy and innovation, often contribute to sustained competitive success.” (74)

• Opposite of economic theory belief

- Gives example of Holland’s advantage in flowers “despite its cold, grey climate”…

• Second factor also important for Dutch flowers:

- Home demand

• Quality more important than quantity

• Discerning consumers drive product innovation

27 Industry Analysis

Competitive Advantage

• “Nations gain competitive advantage … where the home demand gives local firms a clearer or earlier picture of buyer needs…

• if home buyers pressure local firms to innovate faster…” (86)

• “A product’s fundamental or core design nearly always reflects home market needs.” (87)

- “small nations can be competitive in segments which represent an important share of local demand but a smaller share of demand elsewhere, even if the absolute size of the segment is greater in other nations.” (88)

28 Industry Analysis

Competitive Advantage• Related & supporting

industries

- Suppliers assist “process of innovation and upgrading…

- Suppliers help firms perceive new methods and opportunities to apply new technology.” (103)

• The full pattern of interlinking industries is very complex…

29 Industry Analysis

Competitive Advantage

• A more disaggregated view…

30 Industry Analysis

Competitive Advantage

- Competitive advantage in suppliers means spinoffs from one industry can be means to develop new ones

- “Italian world leadership in gold and silver jewelry has been sustained … because other Italian firms produce two-thirds of the world’s jewelry-making machinery.” (101)

- Related industries give strength to each other…

31 Industry Analysis

Competitive Advantage

• Competitive advantage in related industries

TABLE 3-1 Internationally Competitive Related Industries

Nation Industry Related IndustryDenmark Dairy products, brewing Industrial enzymesGermany Chemicals Printing inkItaly Lighting FurnitureJapan Cameras CopiersKorea VCRs VideotapeSingapore Port services Ship repairSweden Automobiles TrucksSwitzerland Pharmaceuticals FlavoringsUnited Kingdom Engines Lubricants, antiknock preparationsUnited States Electronic test and measuring equipment Patient monitoring equipment

32 Industry Analysis

Competitive Advantage

• “Japan's strength in long-filament synthetic textile fibers reflects a long tradition of success in silk, as does a leading export position in silk-like continuous synthetic weaves, woven from long-filament synthetic fibers. Carbon fibers employ technology closely related to synthetic filament fibers and many of the same competitors participate in both.

• Also, while not overall leaders in textile machines, Japanese firms are leaders in water jet weaving machines, used to weave long-filament synthetic fibers into synthetic weaves. Such groups of linked competitive industries in a nation are common.” (105)

33 Industry Analysis

Competitive Advantage

• Firm strategy structure & rivalry

- “No one management system is universally appropriate”

- But character of national management structure needs to suit needs of industry.

• “Nations will tend to succeed … where the management practices and modes of organization favored by the national environment are well suited to the industries’ sources of competitive advantage.

• Italian firms … are world leaders in a range of fragmented industries … operating in small niches…

• In Germany … the engineering and technical background of many senior executives produces a strong inclination towards methodical product and process improvement…” (108)

34 Industry Analysis

Competitive Advantage

• National goals

- Short term focus of US firms—advantage in accounting

- Long term focus of German/Japanese—advantage in engineering…

• Domestic rivalry

- Desire to beat own national competitors often drives innovation

• Italian supercars; Japanese electronics; US software, computers…

- “With little domestic rivalry, firms are more content to rely on the home market.” (119)

Competitive Advantage

• Japan in particular has large number of internationally competitive firms in different industries:TABLE 3-2 Estimated Number of Japanese Rivals in Selected Industries, 1987

Air conditioners 13 Motorcycles 4Audio equipment 25 Musical instruments 4Automobiles 9 Personal computers 16Cameras 15 Semiconductors 34Car audio 12 Sewing machines 20Carbon fibers 7 Shipbuilding 33Construction equipment 15 Steel 5Copiers 14 Synthetic fibers 8Facsimile machines 10 Television sets 15Lift trucks 8 Truck and bus tires 5Machine tools 112 Trucks 11Mainframe computers 6 Typewriters 14Microwave equipment 5 Videocassette recorders 10

36 Industry Analysis

Competitive Advantage

• National competitive advantage therefore tends to occur in clusters

- Geographic clusters: “Many of the Italian jewelry firms, for example, are located around two towns, Arezzo and Valenca Po…” (120)

- Industry clusters

• Related industries and supplier-buyer chains

37 Industry Analysis

Competitive Advantage

• “The individual determinants that define the national environment are mutually dependent because the effect of one often depends on the state of the others…” (129)

• Example of clustering: Denmark

38 Industry Analysis

Competitive Advantage

39 Industry Analysis

Competitive Advantage

• Geographic clustering also strikingly obvious:

• Clustering of internationally competitive industries in Italy:

40 Industry Analysis

Competitive Advantage

• Interactions in the “Diamond” for Italian Ski Boot industry:

41 Industry Analysis

Implications for Business

• Location implications:makes sense to disperse production activities to countries where they can be performed most efficiently.

• First-mover implications:It pays to invest substantial financial resources in building a first-mover, or early-mover, advantage.

• Policy implications:promoting free trade is generally in the best interests of the home-country, although not always in the best interests of the firm. Even though, many firms promote open markets.

42 Industry Analysis

Export orientation

• Specialization on comparative advantage

• Requires successive stages of comparative advantage (flying geese model)

• Supported by export subsidies which are only given temporarily

43 Industry Analysis

Characteristics of developmental state (Gerschenkron, 1962)

• Vertically integrated enterprises

• Development of investment banking

• Major role for government in investment decision making

• Resolve problems on asymmetric information by finance for industrialization, mobilize savings and develop infant industries

Hence: a large role for government and a strong orientation towards industrialization

44 Industry Analysis

Rethinking the East Asian Miracle (Stiglitz and Yusuf, 2001)

• Optimal macroeconomic management depends on range of country-specific factors

• Slower accumulation of human & physical capital gives greater role for TFP & technology assimilation

• Exports as engine of productivity growth is questionable, whereas imports and investment are more often seen as driving forces

• Interventionist policies are increasingly difficult with global capital markets and free trade

• With increased complexity of economic relationships, market-based rules for contracting, property and other rights emerge

45 Industry Analysis

“So What” for business?

• There are at least three main implications of the material discussed in this chapter for international businesses: - First mover implications

• invest to be first, particularly in global industries or in markets which can support a few firms- Location Implication

• if countries have comparative advantages MNEs want to locate appropriate activities in those countries…

- Government Policy implications• companies generate imports and exports. Thus can influence government decisions on trade

policy... - Foreign Investment Decisions

46 Industry Analysis

Foreign subsidiary characteristics

•subsidiary strategy

•level of technology

•training (formal, informal)

•international interdependence

Nation-level resources

•skilled workforce

•innovative capability

National competitiveness

•unemployment rate

•standard of living

•competitiveness of local firms

Firm level resources

•technical and managerial skills

•product and process technology

Published in: S. O’Donnel, T.Blumentritt/Journal of International Management 5 (1999)

Which factors influence a host country’s national competitiveness?

47 Industry Analysis

Cluster Analysis: What Is It?Cluster Analysis: What Is It?

““Clusters are geographically close groups of interconnected companies Clusters are geographically close groups of interconnected companies and associated institutions in a particular field, linked by common and associated institutions in a particular field, linked by common technologies and skills.” technologies and skills.”

Michael Porter, Michael Porter, Clusters of Innovation, 2002Clusters of Innovation, 2002

““Binding the cluster together are ‘buyer-supplier relationships, or common Binding the cluster together are ‘buyer-supplier relationships, or common technologies, common buyers or distribution channels, or common labor technologies, common buyers or distribution channels, or common labor pools.’ Competitive firms make a competitive cluster … and economic self-pools.’ Competitive firms make a competitive cluster … and economic self-interest is ultimately the glue that binds the cluster together.”interest is ultimately the glue that binds the cluster together.”

Edward M. Bergman and Edward J. Feser,Edward M. Bergman and Edward J. Feser,

Industrial and Regional Clusters: Concepts and Comparative Applications, 1999Industrial and Regional Clusters: Concepts and Comparative Applications, 1999

48 Industry Analysis

Case Study

Diamond-Framework contents additional factors

49 Industry Analysis

Cluster Characteristics

• Critical Factors for Cluster Emergence- Strong, diverse and tech-savvy talent pool

• Florida’s three ‘T’s- Presence of established pillar companies with global reach- Strong knowledge infrastructure

• research university, government labs etc.

- Risk tolerant venture capital and angel investors- Sustained development strategies by civic entrepreneurs

and local governments (civic capital)

50 Industry Analysis

Flying Geese model of trade structures in East Asia

51 Industry Analysis

Behind the shifting structure

15

20

25

30

35

40

45

50

55

60

50 55 60 65 70 75 80 85 90 95 OO

% o

f to

tal p

rod

uct

ion

Agriculture Industry Services

Stress on industrializationthrough protectionism;financed by foreign loans

Period of liberalization;Importance of OFWs

52 Industry Analysis

Successive stages of comparative advantage in East-Asian trade structure

1) Primary import-substitution: replace labour intensive manufacturing imports with domestically produced goods

2) Primary export-“substitution”: replace agricultural exports by labour-intensive manufacturing exports

3) Secondary import-substitution: production of intermediate and capital goods for domestic market

4) Secondary export-“substitution”: shift from labour-intensive to capital- and knowledge intensive production

53 Industry Analysis

Conclusions on industrialization

• Industrial development requires productivity growth beyond exploitation of capital

• Export orientation is more supportive growth, but requires strong developmental state

• Careful balance between transferring resources from agriculture and supporting development within agriculture

• Support of “informal” sector can be potential source of growth

54 Industry Analysis

Macro Environment

Interest Rates

Inflation RatesEmployment Levels

Regulatory Climate

Tax Policy

Consumer Spending

Duties & TariffsCurrency Exchange Rates

International Cultural Differences

Government Spending

Rate of Innovation

Consumer Characteristics

Societal Norms

Social Values

Research FundingLevels

55 Industry Analysis

Competitive Analysis

Digitalization

A Changing Competitive Landscape

Globalization

Deregulation

Communication is faster, information availability is vastly extended, coordinationcost are reduced, integration of work tasks is eased, customer reach is extended.

Travel, transportation and exchange of media content (news and cultural events) extendsthe globe. Some tastes and consumer behaviors emerge toward a global standard.

National markets are being deregulated (privatized), e.g. financial services, transportation, telecommunication, energy, etc., and cross-border business transactions are liberalized.

56 Industry Analysis

57 Industry Analysis

58 Industry Analysis

59 Industry Analysis

60 Industry Analysis

Web BrowsersMedia Companies

Content Providers

Internet Industry

InternetPortals

ASPsISPs

What is an Industry?

Industry Analysis www. wai .bangkaew.comDate

Industry & Competitive AnalysisIndustry & Competitive Analysis5 Forces Model of Competition

Key Success FactorsDriving Forces

Strategic Group Maps IdentifyStrategic Optionsfor the

Company

Select the Best

Strategyfor the

Company

Macro-Environment

Micro-Environment

Company AnalysisCompany AnalysisSWOT Analysis

Value Chain Analysis

Competitive Strength Assessment

62 Industry Analysis

FUNDAMENTAL ANALYSIS QUESTIONS

1. What are the characteristics of my industry?

2. Who are/will be my competitors?

3. What are the current/likely positions of my competitors?

4. What moves are/will my competitors make?

5. What moves can/should I take to achieve a competitive advantage?

63 Industry Analysis

Natural and Strategic Competition

• Natural Competition

• Strategic Competition

64 Industry Analysis

Sources of Competition

• Customer need

• Industry competition

• Product-line competition

• Organizational competition

65 Industry Analysis

Competitive Advantage

• Outperform competitors

• Grow despite competitors

• Develop own distinctive competencies that hold potential for competitive advantages

66 Industry Analysis

Competitive Advantage: Two Analytical Tools

• Industry analysis:

- market attractiveness based on economic structure

• Comparative analysis:

- likely future performance of an individual firm in a particular market given the structure of the industry

67 Industry Analysis

Factors Contributing to Competitive Rivalry

• Opportunity potential

• Ease of entry

• Nature of product

• Exit barriers

• Homogeneity of market

• Industry structure

68 Industry Analysis

Factors Contributing to Competitive Rivalry II

• Industry structure

• Commitment to industry

• Technological innovations

• Scale economies

• Economic climate

• Diversity of firms

69 Industry Analysis

Existing Rivalry

• Involves jockeying for position.

• Intensity of rivalry a function of - - Number of competitors

- Industry growth rate

- Level of fixed costs

- Diversity of competitors

- Lack of product differentiation

- Height of “Exit Barriers”

70 Industry Analysis

Entry/Exit Barrier Interaction

Exit BarriersExit Barriers

LowLow HighHigh

Low

Low

Hig

hH

igh

En

try

Bar

rier

sE

ntr

y B

arri

ers

Low, StableLow, StableReturnsReturns

High, StableHigh, StableReturnsReturns

Low, RiskyLow, RiskyReturnsReturns

High, RiskyHigh, RiskyReturnsReturns

Porter, Competitive Strategy, 1980

71 Industry Analysis

Competitive Intelligence

• Strategies, objectives, goals

• Importance of specific markets

• Level of commitment

• Strengths

• Limitations

• Weaknesses

• Future changes in strategy

• Effects on industry, market, our strategies

72 Industry Analysis

Forces Influencing Industry

IndustryRivalry amongCurrent Firms

Substitute Products

BuyersSuppliers

NewEntrants

Technological Change

Government Policy

Global Economic Factors

73 Industry Analysis

การวิ�เคราะห์โครงสร�างอุ�ตสาห์กรรม Michael Porter

Bargaining power

of buyers

Bargaining power

of suppliers

Threat of substitute products or services

Threat of new entrants

Rivalry among existing competitors

Entry barriers- economies of scale- product differentiation- capital requirements- brand identity- access to distribution channels

- improve price performance trade-off- produced by industries earning high profits

- bargaining leverage- price sensitivity

- high concentration- threat of forward integration- switching costs

- slow industry growth- lack of differentiation- numerous competitors- high exit barriers

Industry Analysis www. wai .bangkaew.comDate

Porter’s “5 Forces”: Thinking about the balance of power

EntrantsEntrants

SubstitutesSubstitutes

SuppliersSuppliers BuyersBuyersRivalsRivals

Political, regulatory and institutional context

“Complementors”

Industry Analysis www. wai .bangkaew.comDate

Assets/Uniqueness speak to Rivalry and the Threat of Entry.

EntrantsEntrants

SubstitutesSubstitutes

SuppliersSuppliers BuyersBuyersRivalsRivals

Industry Analysis www. wai .bangkaew.comDate

Porter reminds us to think about the structure of the value chain:

EntrantsEntrants

SubstitutesSubstitutes

SuppliersSuppliers BuyersBuyersRivalsRivals

Industry Analysis www. wai .bangkaew.comDate

Powerful suppliers and buyers may constrain profitability

SuppliersSuppliers BuyersBuyers

78 Industry Analysis

79 Industry Analysis

Role of Competitive Strategy

• Create a defendable position against the 5 forces.- Positioning

- Shifting the balance of forces.

- Exploit change resulting from shifts in the factors underlying the forces.

80 Industry Analysis

Business Level Strategies

• What do we need to understand?

- Key Success Factors

- Generic Business Level Strategies

- Where to find business level advantages

- “Core” and “Distinctive” Competencies

81 Industry Analysis

Key Success Factors

• Each industry has certain areas that firms competing in that industry must do well in in order to survive

• Can be thought of as the bare minimum that must be done in order to compete in that industry

82 Industry Analysis

GenericBusiness Level Strategies

• Generic Strategies are general ways to classify strategies

• Examples:

- Miles & Snow (prospectors, defenders, analyzers, reactors)

- Ansoff & Stewart (1st mover, 2nd mover, low cost producers, niche)

83 Industry Analysis

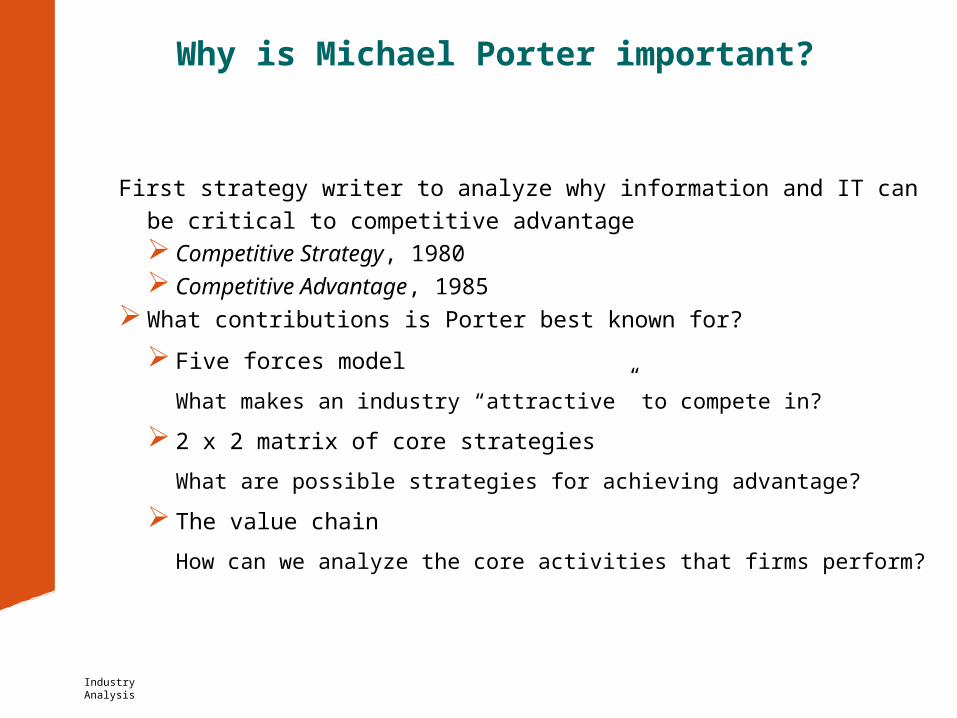

Why is Michael Porter important?

First strategy writer to analyze why information and IT can be critical to

competitive advantage Competitive Strategy, 1980 Competitive Advantage, 1985

What contributions is Porter best known for?

Five forces model

What makes an industry “attractive” to compete in?

2 x 2 matrix of core strategies

What are possible strategies for achieving advantage?

The value chain

How can we analyze the core activities that firms perform?

84 Industry Analysis

Porter’s GenericBusiness Level Strategies

• Three (3) ways that a firm can compete and get above average returns

Overall Cost Leadership

Differentiation

Focus

85 Industry Analysis

Porter’s GenericBusiness Level Strategies

• You can still be profitable without following one of these but these profits usually will be below the industry average

- squeezed by the Five (5) Forces

86 Industry Analysis

Overall Cost Leadership

• Basic idea is that if you can produce it more cheaply than anybody else, you will have the most profit at any price

• Cost Leadership Price Leadership

87 Industry Analysis

Overall Cost Leadership

• Companies need to be extremely aggressive at finding cheaper, more efficient ways of doing things

• efficient scale facilities

• pursuit of cost reductions

• tight cost and overhead control

• avoidance of marginal customers

88 Industry Analysis

Overall Cost Leadership and the Five (5) Forces

• Competitors

- lower costs mean that it can still earn returns after its competitors have competed away their profits through rivalry

89 Industry Analysis

Overall Cost Leadership and the Five (5) Forces

• Entry

- potential entrants have to overcome greater entry barriers in terms of scale economies or cost advantages

• Substitutes

- a better cost/benefit ratio than its competitors

90 Industry Analysis

Overall Cost Leadership and the Five (5) Forces

• Buyers

- can exert power only to drive down prices to the level of the next most efficient competitor

• Suppliers

- more flexibility to cope with input cost increases

91 Industry Analysis

The Risks Associated with Overall Cost Leadership

• Technological change nullifies basis for cost advantage

• Low cost learning by new entrants

92 Industry Analysis

Differentiation

• Rests on the creation of some product or service that is perceived industry-wide as being unique

• Perception is more important than substantive differences

• The firm still has to be cost conscious but this is not its primary focus

93 Industry Analysis

Differentiation andThe Discipline of Market Leaders

• Three (3) types of differentiation

- Price

- Product

- Service

94 Industry Analysis

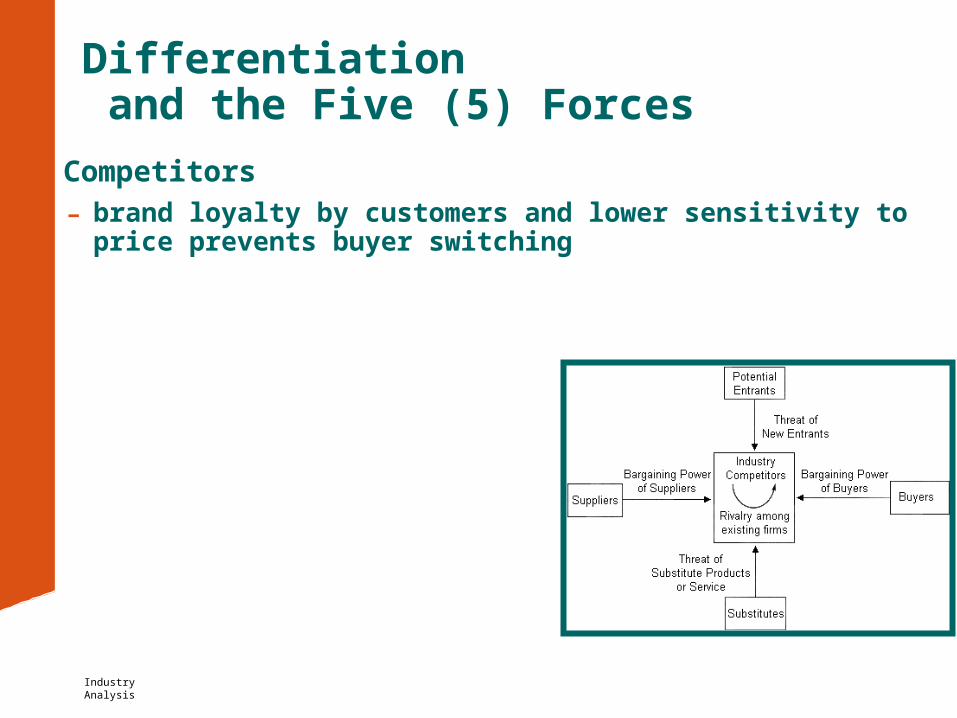

Differentiation and the Five (5) Forces

• Competitors

- brand loyalty by customers and lower sensitivity to price prevents buyer switching

95 Industry Analysis

Differentiation and the Five (5) Forces

• Entry

- potential entrants must overcome the perceived uniqueness of the firm

• Substitutes

- brand loyalty prevents buyers from switching to substitutes

96 Industry Analysis

Differentiation and the Five (5) Forces

• Buyers

- buyers lack comparable alternatives

• Suppliers

- differentiation yields higher margins to give firms more leeway in dealing with suppliers

97 Industry Analysis

The Risks Associated with Overall Cost Leadership

• Customers may decide that the extra expense is not worth the benefit

• Imitation narrows perceived differentiation

98 Industry Analysis

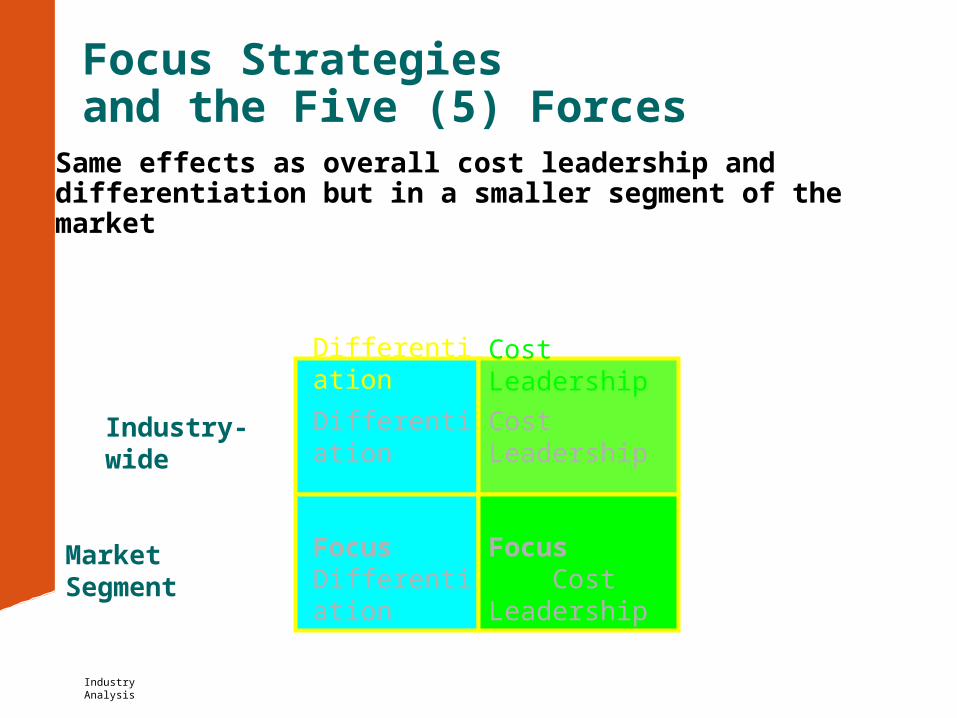

Focus Strategiesand the Five (5) Forces

• Same effects as overall cost leadership and differentiation but in a smaller segment of the market

Differentiation Cost Leadership

Industry-wide

Market Segment

Differentiation

Focus Differentiation

Cost Leadership

Focus Cost Leadership

99 Industry Analysis

Stuck in the Middle

• Describes firms that have failed to establish themselves as following one of the above generic strategies

• Loses high volume sales to cost leader and high margin sales to differentiators

100

Industry Analysis

Where Do We Find These Competitive Advantages?

The Value Chain

Support

Activities

Industry Analysis www. wai .bangkaew.comDate

Porter’s Value Chain(well suited for analyzing product/manufacturing firms)

102

Industry Analysis

Property and Casualty Industry Value Chain

INBOUNDLOGISTICS

OPERATIONS OUTBOUNDLOGISTICS

MARKETING AND SALES

SERVICE

PROCUREMENT

TECHNOLOGY DEVELOPMENT

HUMAN RESOURCE

MANAGEMENT

FIRM INFRASTRUCTURE

-Financial Policy -Regulatory Compliance - Legal - Accounting

Actuary Training

Agent Training

Claims Training

Claims Procedures

•Claims Settlement•Loss Control

•Policy Sales•Policy Renewal•Agent Manage- ment•Advertising

•Independent Agent Network•Billing and Collections

• Underwriting• Investment

•Policy Rating

Actuarial MethodsInvestment Practices

I/TCommunications

Product DevelopmentMarket Research

Figure 3-7

Included with permission of Michael E. Porter based on ideas in Competitive Advantage: Creating and Sustaining Superior Performance, copyright 1985 by Michael E. Porter.

103

Industry Analysis

Technologies in the Value Chain

INBOUNDLOGISTICS

OPERATIONS OUTBOUNDLOGISTICS

MARKETING AND SALES

SERVICE

PROCUREMENT

TECHNOLOGY DEVELOPMENT

HUMAN RESOURCE

MANAGEMENT

FIRM INFRASTRUCTURE

Information System Technology

Planning and Budgeting TechnologyOffice Technology

Training TechnologyMotivation Research

Information Technology

Product TechnologyComputer-Aided DesignPilot Plant Technology

•Diagnostic and Testing Technology•Communications Technology•Information Technology

•Transportation Technology•Material Handling Technology•Storage and Preservation Technology•Communication System Technology•Testing Technology•Information Technology

Information Systems TechnologyCommunication System TechnologyTransportation System Technology

Software Development ToolsInformation Systems Technology

•Basic Process Technology•Materials Technology•Machine Tools Technology•Materials Handling Technology•Packaging Technology•Testing Technology•I/nformation Tech.

•Transportation Technology•Material Handling Technology•Packaging Technology•Communications Technology•Information Technology

•Multi-Media Technology•Communication Technology•Information Technology

Figure 3-8Adapted with the permission of the Free Press, an imprint of Simon & Schuster Inc.. from COMPETITIVE ADVANTAGE: Creating and Sustaining Superior Performance by Michael Porter. Copyright © 1985 by Michael E. Porter., p. 167.

104

Industry Analysis

The Primary Activities

The “Line” Activities of the Firm

Inbound logistics

Operations Outbound Logistics

Marketing and Sales

Service

105

Industry Analysis

The Support Activities:Firm Infrastructure

The Structure of the Organization

106

Industry Analysis

The Support Activities:Human Resource Management

The People Considerationsof the Organization

107

Industry Analysis

The Support Activities:Technology Development

What the Firm Createsand How It Creates It

108

Industry Analysis

The Support Activities:Procurement

Getting the Necessary Materials

for the Primary Components

From the Environment

109

Industry Analysis

The Underlying Idea Behind Porter’s Value Chain

• Break things down into components;

• Maximize the value of each component;

• Maximize the value of how they interact;

• Be considered brilliant.

110

Industry Analysis

Comprehensive MNC Strategy Model

IndustryGlobalization

Drivers:Market

CostGovernmentCompetitive

Strategy:Multidomestic

GlobalInternationalTransnational

OrganizationalStructure:Centralized

Decentralized

ManagementProcesses:

CoordinationConfiguration

Performance:Market share

Profits

Formalization:HighLow

111

Industry Analysis

Responsiveness/Integration Framework

GlobalCoordinationIntegration

High

High

Low

Low

Global

International

Transnational

Multi-national

Local responsiveness

112

Industry Analysis

Integration/Responsiveness Framework

GlobalCoordination,Integration

High

High

Low

Low

Global

International

TransnationalTransnational

Multi-national

Local responsiveness

Technology

Worldwidelearning

113

Industry Analysis

… But Remember, We Said There Are Two Major Schools of Thought

1. The strategic “positioning” school of strategy

Associated with Michael Porter

Select the right “position” in an “attractive” industry

2. The Resource Based View of the Firm (RBVF)

Originated with economist Edith Penrose; developed by strategy professors Jay Barney;

Dietricx & Cool

Recently popularized by Hamel & Prahalad, Competing for Time (1990) but re-named “core

competencies”

Develop and exploit your unique capabilities

114

Industry Analysis

What Do RBVF Strategists Say?

Innovative IT solutions are copied or imitatedMost IT applications are imitableSome exceptions exist when IT can’t be imitated

Unless the capabilities to create the innovative IT solution are unique and immobile, then second-movers may: copy your great ideas more cheaply learn from your mistakes

Customer “lock-in” does not really workCustomers are too smart and will avoid becoming over-committed to you ..

115

Industry Analysis

“IT and Sustained Competitive Advantage: A Resource Based Analysis,” MIS Quarterly 1995

Why do the authors argue that many of these resources can’t create sustainable advantage?Customer lock-inAccess to financial capitalProprietary technology (patents, copyrights, etc.)

Technical IT skills (e.g., software developers)

Managerial IT skills (e.g., IT managers, business unit managers, the ability to collaborate

in order to identify and deploy effective IT)

Collaborative Supply

Scheduling & Management

Supplier CustomerFirmCustomers

SourceX-Dock

Geo HubTransportation

ProviderTransportation

ProviderFab/Sort

TransportationProvider

AssemblyTransportation

ProviderTest

TransportationProvider

Box &FHS

TransportationProvider

CustomersMake

CustomersDeliver

SupplierSource

SupplierDeliver

SupplierMake

Exe

cuti

on

Exe

cuti

on

Sch

edu

lin

gS

ched

uli

ng

What Synchronized BusinessMight Look Like!

Dmd/SupplyPlanning

Collaborative Strategic Plg

Collaborative Supply

Scheduling & Management

Dmd/SupplyPlanning

Strategic Planning

Integrated Factory,Materials/Warehouse/Transportation Execution

Demand and Supply Planning

Integrated SN DetailedScheduling For

Factory/Materials/Warehouse/Transportation

Strategic Business Planning

Pla

nn

ing

Pla

nn

ing

Collaborative Planning

Collaborative Planning

WarehouseManagement

WarehouseManagement

Factory Execution

Factory Execution

Long Range Business/Capacity Planning Long Range Planning

Long Range Planning

ExternalCollaboration

End-to-EndSynchronization

InternalIntegration

Entry/Re-entryCycle

Focus on the Value Stream

InitialLean

Vision

Short Term Cycle

Create & Refine Transformation Plan

Lean Transformation

Framework

Adopt LeanParadigm

EnterpriseStrategicPlanning

Focus on Continuous Improvement

Outcomes on Enterprise

Metrics

Implement Lean Initiatives Enterprise

LevelTransformation

Plan

Develop Lean Structure & Behavior

Detailed Lean

Vision

Environmental Corrective

Action IndicatorsDetailed

Corrective Action Indicators

Decision to Pursue

Enterprise Transformation

•Build Vision•Convey Urgency•Foster Lean Learning•Make the Commitment•Obtain Senior Mgmt. Buy-in

•Map Value Stream•Internalize Vision•Set Goals & Metrics•Identify & Involve Key Stakeholders

•Organize for Lean Implementation•Identify & Empower Change Agents•Align Incentives•Adapt Structure & Systems

•Identify & Prioritize Activities•Commit Resources•Provide Education & Training

•Monitor Lean Progress•Nurture the Process•Refine the Plan•Capture & Adopt New Knowledge

•Develop Detailed Plans•Implement Lean Activities

Enterprise Level Roadmap

+

+

Long Term Cycle

118

Industry Analysis

One Last Important Concept

• Core Competencies

- Something a firm does well relative to its competitors

• Distinctive Competencies

- Something a firm does which makes it unique relative to its competitors

119

Industry Analysis

• While useful, the competitor table and the strategic groups are, like Porter’s Analysis, essentially static.

• Just as the Four-Arena Analysis is useful for using history to make guesses about the future -- especially about how trends might stop and the ground might shift --

• Hamilton et al’s Core Competency Strategic Intent matrix is useful for tracing -- and predicting -- shifts in competitors’ relative power.

Dynamic Competitor Analysis

120

Industry Analysis

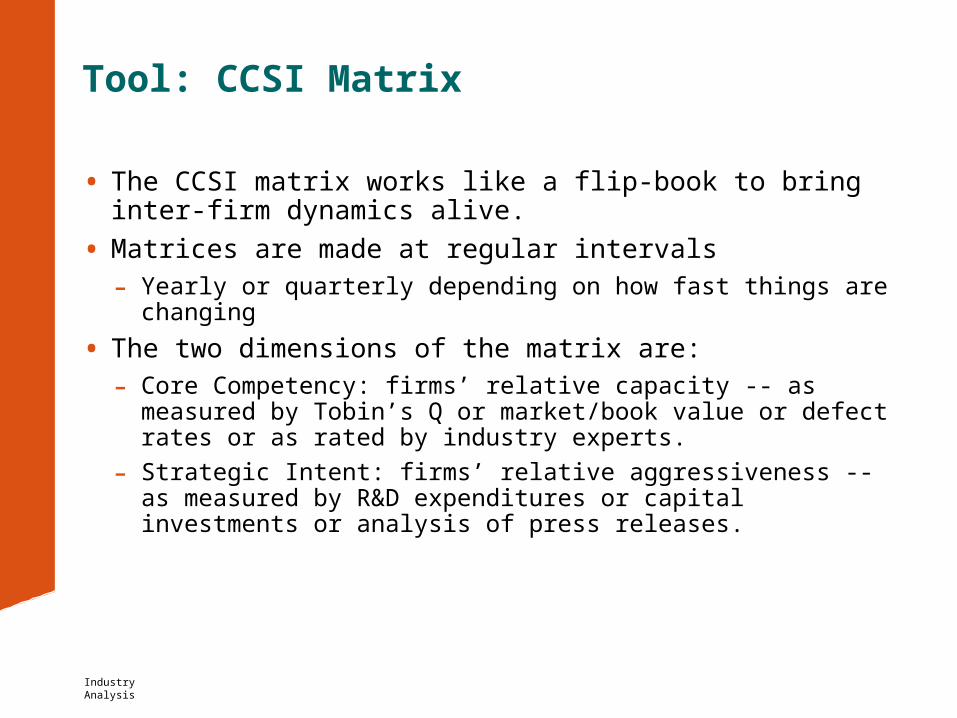

Tool: CCSI Matrix

• The CCSI matrix works like a flip-book to bring inter-firm dynamics alive.

• Matrices are made at regular intervals

- Yearly or quarterly depending on how fast things are changing

• The two dimensions of the matrix are:

- Core Competency: firms’ relative capacity -- as measured by Tobin’s Q or market/book value or defect rates or as rated by industry experts.

- Strategic Intent: firms’ relative aggressiveness -- as measured by R&D expenditures or capital investments or analysis of press releases.

121

Industry Analysis Strategic IntentPassiv

eAverag

eAggressiv

e

Low

Avera

ge

Hig

h

Core

C

ap

ab

ilit

ies

Tool: CCSI Matrix

122

Industry Analysis

• Each competitor is mapped as a circle:

- the size of which reflects sales or capitalization or assets

- and the pie slice in which reflects free cash or other available resources

Tool: CCSI Matrix

123

Industry Analysis

Case: CCSI Analysis of the early 90s Automobile Industry

• Flip the through the following three slides fast, noting:

- The decline of Honda & Toyota

- The ascendancy of Ford

- General Motors unsucessful run at leadership

- Chrysler’s repositioning as an up and coming star.

124

Industry Analysis

Passive

AggressiveStrategic Intent

Core

C

ap

ab

ilit

ies

Automobile Industry 1990

Honda

General Motors

Ford

Toyota

Chrysler

1.0

.5

1.5

(1.0)

(1.5)

(.50)

1.04 1.08 1.12.88 .92 .96

Figure 1

Low

Hig

h

125

Industry Analysis

Strategic IntentPassiv

eAggressiv

e

Core

C

ap

ab

ilit

ies

Automobile Industry 1991

1.0

.5

1.5

(1.0)

(1.5)

(.50)

1.04 1.08 1.12.88 .92 .96

General Motors

Toyota

Chrysler

Honda

Ford

Figure 2

Low

Hig

h

126

Industry Analysis

Passive

Aggressive

Core

C

ap

ab

ilit

ies

Automobile Industry 1992

1.0

.5

1.5

(1.0)

(1.5)

(.50)

1.04 1.08 1.12.88 .92 .96

General Motors

Ford

Toyota

Chrysler

Honda

Strategic IntentFigure 3

Low

Hig

h

Industry Analysis www. wai .bangkaew.comDate

Managing disruptions means managing the dynamics of the value chain

Performance

Time

Ferment

Takeoff

Maturity

Disruption

Can I reshape the dynamics ofpower in the value chain?

Industry Analysis www. wai .bangkaew.comDate

Making money from Innovation: Summary

• Creating value is not enough:

• It is important to capture value as well

• Value can be captured through a variety of mechanisms, including uniqueness and complementary assets

• Value capture strategies change over the life cycle

• Technology strategy and business strategy should thus be intimately linked

129

Industry Analysis

Industry Equilibrium

• Industry structure reinforces power relationships and patterns of competition.

• The nature of industries is to resist change and maintain stability.

• Periods of instability provide both significant threats and opportunities for organizations.

130

Industry Analysis

Stages of Industry Transformation

• The Trigger - an event that significantly alters the way business has been done before, major impact on cost or buyer value.

- Change in technology

- Change in customer needs or wants

- Change in regulation

131

Industry Analysis

Stages of Industry Transformation

• Experimentation - a widespread “trial and error” search for a winning response to a triggering event.

- Period of high risk and uncertainty

- Imitation is a popular response

- Access to capital vital

132

Industry Analysis

Stages of Industry Transformation

• Convergence - marks the emergence of “dominant” business models as unsuccessful experiments are shaken out of the industry.

- Industry life cycles have gotten much shorter

- Convergence begins to return industry to equilibrium

133

Industry Analysis

• Why don’t the 5 competitive forces affect businesses equally?

- Strategic Groups

- Industry Differences

134

Industry Analysis

Competitor Analysis

(-) After sales services (+)

(+)

Speedto

market

(-)

“Strategic Groups”

Competitor Analysis“Mapping”

By identifying important competitive factors you may effectivelymap your competitive position

135

Industry Analysis

Spe

cial

izat

ion

Vertical Integration

NarrowLine

FullLine

High VerticalIntegration

Assembler

Full line, vertically integratedlow manufacturing costs,

low service,moderate quality

Moderate line, assemblermedium price, very highcustomer service, low

quality, low price

Group C

Group A

Narrow line, assembler,high price,high tech, high quality

Group B

Group DNarrow line, highly

automated, low price,low service

136

Industry Analysis

Example: Strategic Group Map of the Video Game Industry

Typ

es o

f V

ideo

Gam

e S

up

pli

ers/

Dis

trib

uti

on

Ch

ann

els

Overall Cost to Players of Video Games

Low(Coin-operated

equipment)

Medium (Console players cost

$100-$300)

High (Use PC)

Arcades

Home PCs

Video game consoles

Online/Internet

Sony, Sega, Nintendo, several

others

Arcade operators Publishers

of games on CD-ROMs

MSN Gaming Zone, Pogo.com,

America Online, HEAT, Engage, Oceanline, TEN

137

Industry Analysis

Strategic Groups

• A group of firms in an industry following the same or a similar strategy.

• Present a more detailed analysis of the structure of an industry and help explain differences in performance of individual companies within the same industry.

• Companies within groups are limited in their ability to adopt the strategies of companies in other groups due to “mobility barriers”.

138

Industry Analysis

Industry Differences

• Industry Life Cycle Model

- Embryonic

- Growth

- Shakeout

- Mature

- Declining

139

Industry Analysis

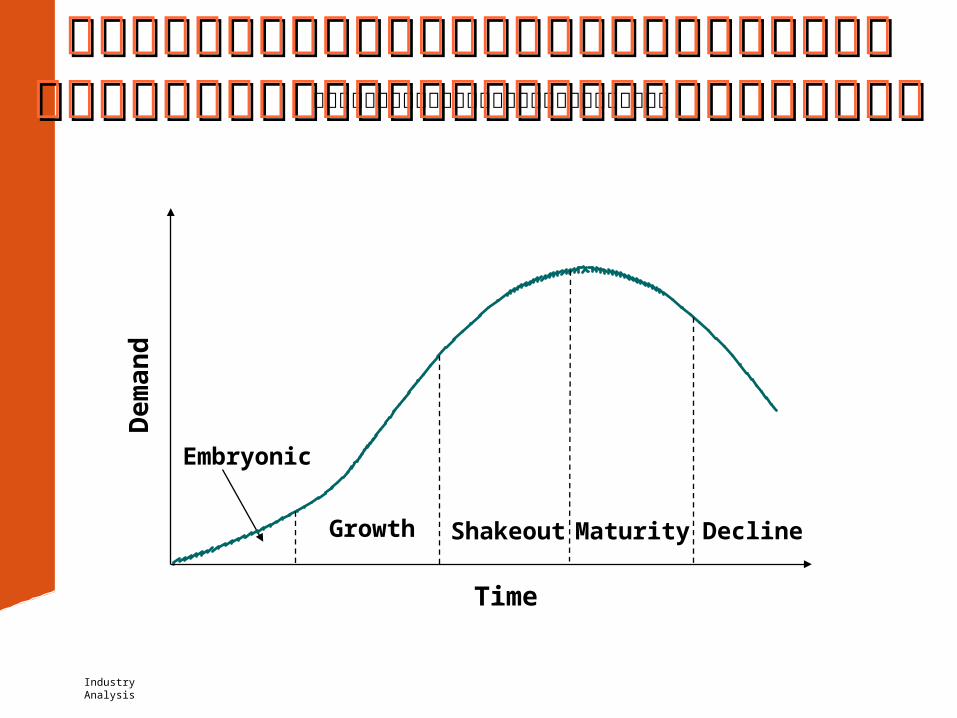

ขั้��นตอนพั�ฒนาการขั้องอ ตสาหกรรม

การเปลี่��ยนแปลี่งการแขั้�งขั้�นในช่�วงการการเปลี่��ยนแปลี่งการแขั้�งขั้�นในช่�วงการเปลี่��ยนแปลี่งอ ตสาหกรรมเปลี่��ยนแปลี่งอ ตสาหกรรม

Time

Embryonic

Growth Shakeout Maturity Decline

De

ma

nd

140

Industry Analysis

An Action-Based Model of the An Action-Based Model of the Industry Life CycleIndustry Life Cycle

Key TaskKey Task

Exploiting Open Exploiting Open Niches (Blind Spots) Niches (Blind Spots)

and Competitive and Competitive UncertaintyUncertainty

Entrepreneurial Entrepreneurial ActionsActions

Key TaskKey Task

Growth-OrientedGrowth-OrientedActionsActions

Exploiting Factors Exploiting Factors of Productionof Production

Key TaskKey Task

Market-PowerMarket-PowerActionsActions

Exploiting Market Exploiting Market PositionPosition

Firm Resource Firm Resource &&

Market StrengthMarket Strength

Emerging StageEmerging Stage Growth StageGrowth Stage Mature StageMature Stage

TimeTime

Industry Analysis www. wai .bangkaew.comDate

A Key Framework: The industry life cycle

Era of Ferment/Disruption

“Dominant design” emerges

Maturity

IncrementalInnovation

Industry Analysis www. wai .bangkaew.comDate

The S-curve Maps Major Transitions

Performance

Time

Ferment

Takeoff

Maturity

Disruption

143

Industry Analysis

145

Industry Analysis

S curve

• Can the S curve be predicted?

- The product/process transition

- Technological “exhaustion”

• How do markets evolve as technologies change?

- Basic segmentation

- Crossing the chasm

- New technologies, new needs

146

Industry Analysis

Can the Life Cycle be Predicted?The product/process transition

Focus of attention

Time

Product innovation

ProcessInnovation

Industry Analysis www. wai .bangkaew.comDate

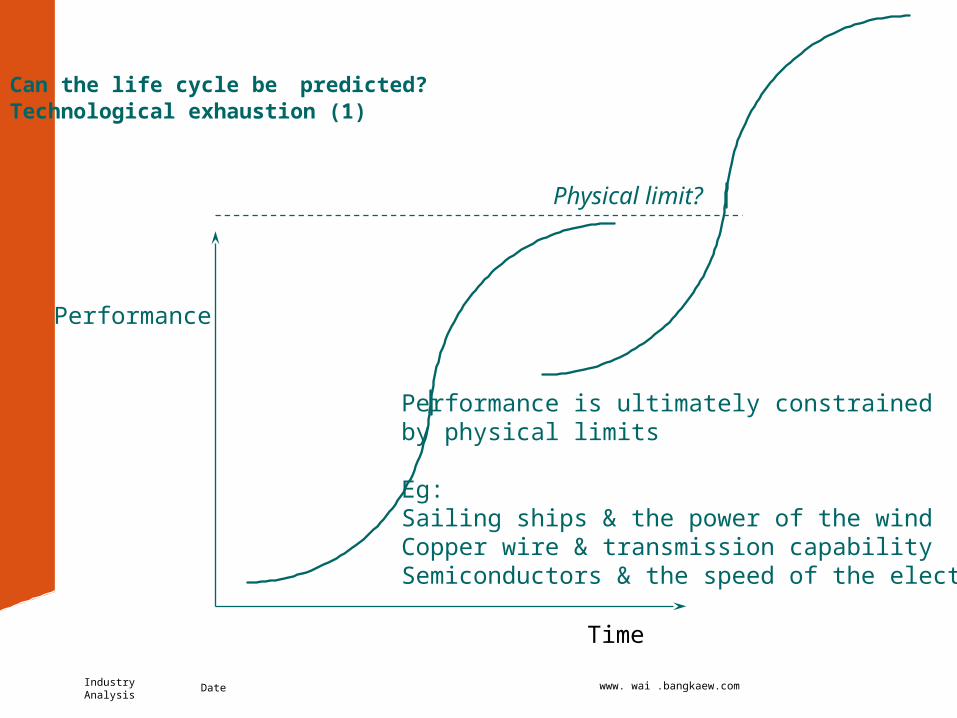

Can the life cycle be predicted?Technological exhaustion (1)

Performance

Time

Physical limit?

Performance is ultimately constrainedby physical limits

Eg:Sailing ships & the power of the windCopper wire & transmission capabilitySemiconductors & the speed of the electron

Industry Analysis www. wai .bangkaew.comDate

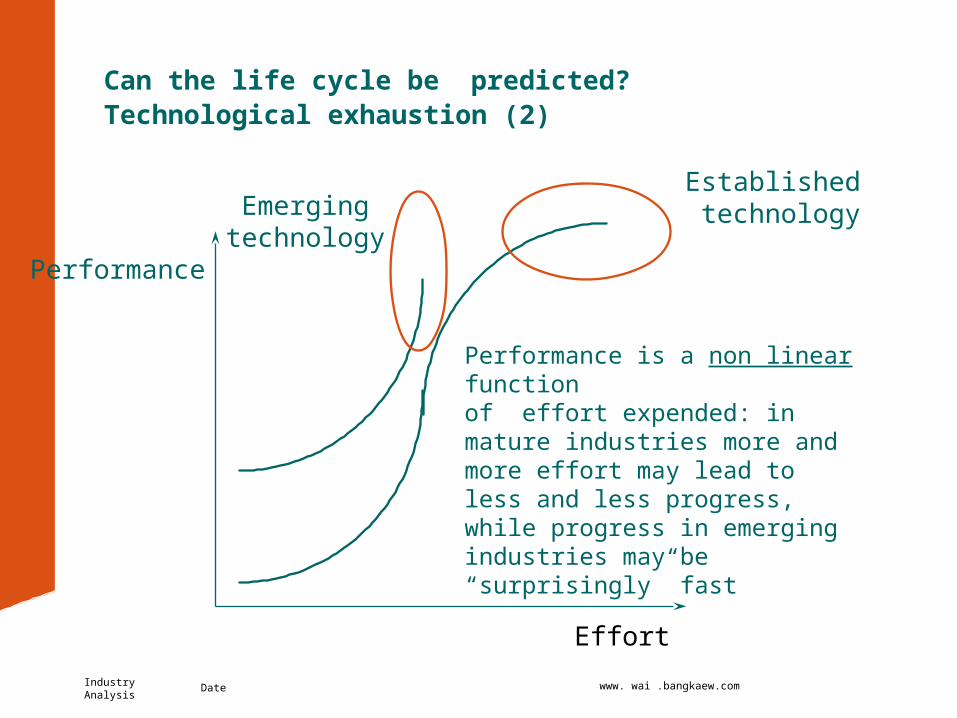

Can the life cycle be predicted?Technological exhaustion (2)

Performance

Effort

Performance is a non linear functionof effort expended: in mature industries more and more effort may lead to less and less progress, while progress in emerging industries may be “surprisingly” fast

Established technologyEmerging

technology

Industry Analysis www. wai .bangkaew.comDate

Market Evolution over the Life Cycle

• Market segmentation

• Crossing the chasm

• New markets, new needs: The Innovator’s Dilemma

Industry Analysis www. wai .bangkaew.comDate

Who buys a technology as it evolves?

Performance

Time

Industry Analysis www. wai .bangkaew.comDate

Understanding market dynamics:Basic segmentation (Rogers)

UnitsBought

Time

Innovators

EarlyAdopters

EarlyMajority

LateMajority

Laggards

Adopters differ by, for example, social, economic status -- particularly resources, affinity for risk,knowledge, complementary assets, interest in the product

Industry Analysis www. wai .bangkaew.comDate

Understanding market dynamics:Crossing the chasm: (Moore)

Time

Innovators

EarlyAdopters

EarlyMajority

LateMajority

Laggards

Making the transition from “early adopters” to “early majority” users oftenrequires the development of quite different competencies: e.g. service, support capabilities, much more extensive training.

Crossing the chasm?

UnitsBought

Industry Analysis www. wai .bangkaew.comDate

New Customers, New Needs

Performance

Time

Who buys a technologywhen it is firstintroduced?

New technologies sell to:- New customers- With new needs- Often at lower margins

154

Industry Analysis

New markets can be harder to manage than new technologies

Old technologyCompetencies

New technologyCompetencies

New customerNeeds

Old customerNeeds

Industry Analysis www. wai .bangkaew.comDate

Managing the change in customer groups may be the hardest task!

Performance

Effort

Leading edge customerfocused research may be a critical capability

Industry Analysis www. wai .bangkaew.comDate

Exercise: Market Evolution

• Consider the three industries:

- Ready to eat frozen dinners

- Publishing (Books or music)

- Handheld cameras for consumers

• For each industry:

- What was the dominant performance metric under the “old regime”?

- What is the dominant metric under the new?

- Is the discontinuity a new market, or does it represent a threat to the core business?

• Choose one industry and be prepared to present your results to the group

157

Industry Analysis

Hypercompetition

HypercompetitionHypercompetition

A condition of rapidly escalatingcompetition based on

• Price-quality positioning

• Competition to create new know-how and establish first-mover advantage

• Competition to protect or invade established product or geographic markets

158

Industry Analysis

Hypercompetition

First mover advantage eroded through:rapid response and innovation;

enhancement of product features; niche attacks

Advantage by building barriers eroded by:technological advances; building on home-based

economies of scale; buying share;

different distribution channels (e.g. e-business); niche attacks

Industry Analysis www. wai .bangkaew.comDate

The PLC Phase

Focus on the firm andits strategies at different

stages of the PLCSWOT framework

Hypercompetition Phase

Focus on the competitiveinteractions w.r.t. the four

competitive arenasC-Q/T-K/S/D framework

ValueNet Phase

Focus on all the playersrelevant to your operations

PARTS framework

Number of Players

Com

plex

ity o

f A

naly

sis

Industry Analysis www. wai .bangkaew.comDate

Price-Quality Maneuvers

Price War

Full line Producers

Niching & Outflanking

Move to Ultimate Value

Attempt to redefine Quality

Commodity like Market

Return to Price Wars

Move to the next Arena

The Cycle of Price-Quality Competition - MovingUp the Escalation Ladder

Industry Analysis www. wai .bangkaew.comDate

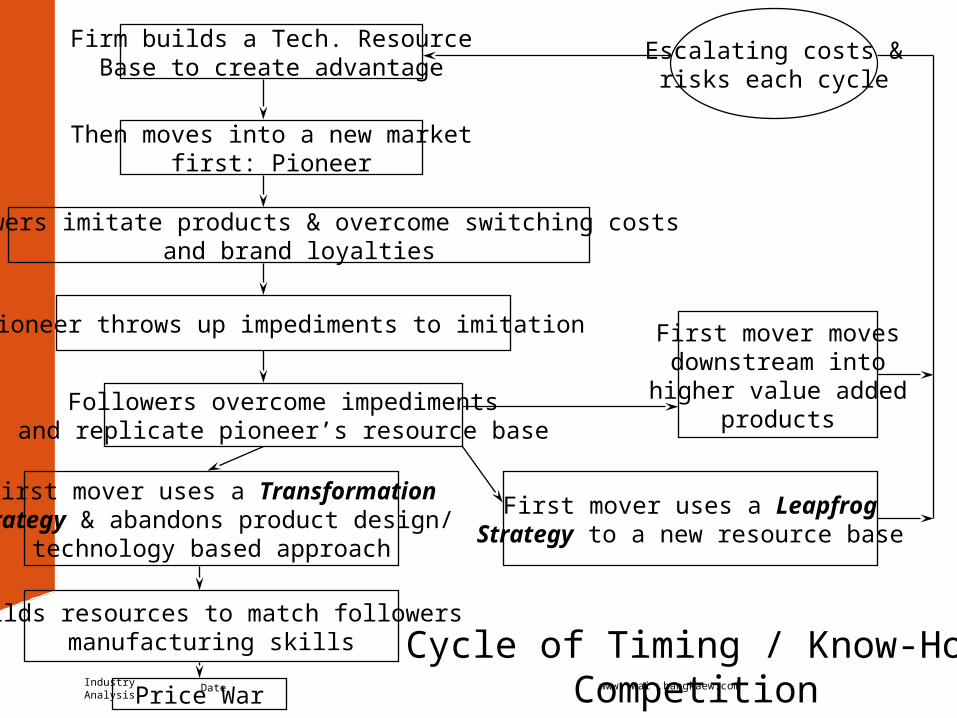

Firm builds a Tech. ResourceBase to create advantage

Then moves into a new marketfirst: Pioneer

Followers imitate products & overcome switching costsand brand loyalties

Pioneer throws up impediments to imitation

Followers overcome impedimentsand replicate pioneer’s resource base

First mover uses a TransformationStrategy & abandons product design/

technology based approach

Builds resources to match followersmanufacturing skills

Price War

First mover uses a LeapfrogStrategy to a new resource base

First mover movesdownstream into

higher value addedproducts

Escalating costs &risks each cycle

Cycle of Timing / Know-HowCompetition

Industry Analysis www. wai .bangkaew.comDate

Build entry barrier around market Ato exclude competition

Build entry barrier around market Bto exclude competition

Circumvent barriers and attackniche in market B

Short Run: Withdraw from niche or fail to respond

Delayed Response: Barriers to contain entrant to a segment of B

Entrant breaches barriersor triggers price war in B

Incumbent’s stronghold in B weak-ens as it grows more competitive

Long Run:Incumbent attacks entrant’s market A to punish

Entrant responds in market A or inmarket B

Standoff until one party gains theupper hand in market A or B

Both strongholds erodeor merge into one

market

Price WarOther firmdivests

One firm builds newstronghold

Cyclerestarts withentry into anew market

If one firm dominates

STRONG-HOLDSARENA

Industry Analysis www. wai .bangkaew.comDate

Deep pocket develops

Launches attack todrive out small firms

Antitrust laws invoked - work

occasionally

Small firms forcedto outmaneuver

deep pocket

Hostile takeoverof large firm

Small firm escalatesown resource base

Cooperative strategy develops

Avoidance strategyniching, etc.

Large scalealliances form with equally deep pockets

Deep pocket advantage is elim

inated or neutralizedBuyers or

suppliers develop acountervailing

force

New attempt to escalate resources

Cycle of DeepPockets Competition

Industry Analysis www. wai .bangkaew.comDate

Kroger becomeslarge & powerful

Drops prices

Antitrust suitsfiled by rivals

Kroger winssuits

Many takeover attempts from outside industrylead to high leverage

Mergers

Acquisitions

Small chains seekniches. Kroger also

niches geographicallyto avoid competition

Industryconsolidation

Deep pocket advantage is elim

inated or neutralizedLarge wholesalersprovide economies

to smaller stores

Continued M&A in industry

Cycle of DeepPockets Competition

Industry Analysis www. wai .bangkaew.comDate

Vision for DisruptionIdentifying and creating

opportunities for temporaryadvantage via understanding•Stakeholder satisfaction• Strategic soothsaying

to ID new ways to serve current customers better or serve

those not being served

Capability for DisruptionSustaining the momentum by

developing abilities for:• Speed

• Surprisethat can be applied across

many actions to builda series of temporary

advantages

Tactics for DisruptionSeizing the initiative to

gain advantage by• Shifting the rules

• Signaling• Strategic thrusts

with actions that shape,mould or influence

the direction or nature ofcompetitors’ responses

MarketDisruption

Industry Analysis www. wai .bangkaew.comDate

A 4 Arena Analysis

Arena Key Success Factors Critical 7S

Cost / Quality Understandingcustomer needsCost reduction

S1: StakeholdersatisfactionS3: Speed

Know-how / Timing Foster innovationQuick marketpenetration

S3: SpeedS4: Surprise

S2: Soothsaying

Stronghold creation /invasion

DeterrenceAggression

S6: SignalsS7: Strategic thrusts

Deep pockets Brute forceOut-maneuvering big

opponents

S7: Strategic thrustsS5: Shifting rules

Industry Analysis www. wai .bangkaew.comDate

Limitations of the Hypercompetition Perspective

• Ignores the point that competition and co-operation can co-exist.

• may be in the best interests of players not to jump to the next level of dynamic competitive interaction but into co-operative competition - coopetition

• requires looking at the firm’s valuenet

Industry Analysis www. wai .bangkaew.comDate

The ValueNet

Customers

Company

Suppliers

ComplementorsSubstitutors

170

Industry Analysis

Intel - A Partial ValueNet

HP; Compaq; IBM

INTEL

Suppliers

MicrosoftHP (Merced)Sun (Solaris + Merced)Compaq (Digital TV standards with M’Soft)

NatSem / CyrixAMD / IBMMicrosoft

IBM manufactures AMD

Digital CableTV StandardsNetPC StandardsSolaris Compatibility of NetPC design & Merced Limits Microsoft power in ValueNet

Limit customerpower & competitorresponse via Mother-board manufacture

Customers limitdependence - alternativesuppliers

171

Industry Analysis

How can the game be changed?

The game can be changed by changing• Players• Added value• Rules of the game• Tactics employed• Scope of the game

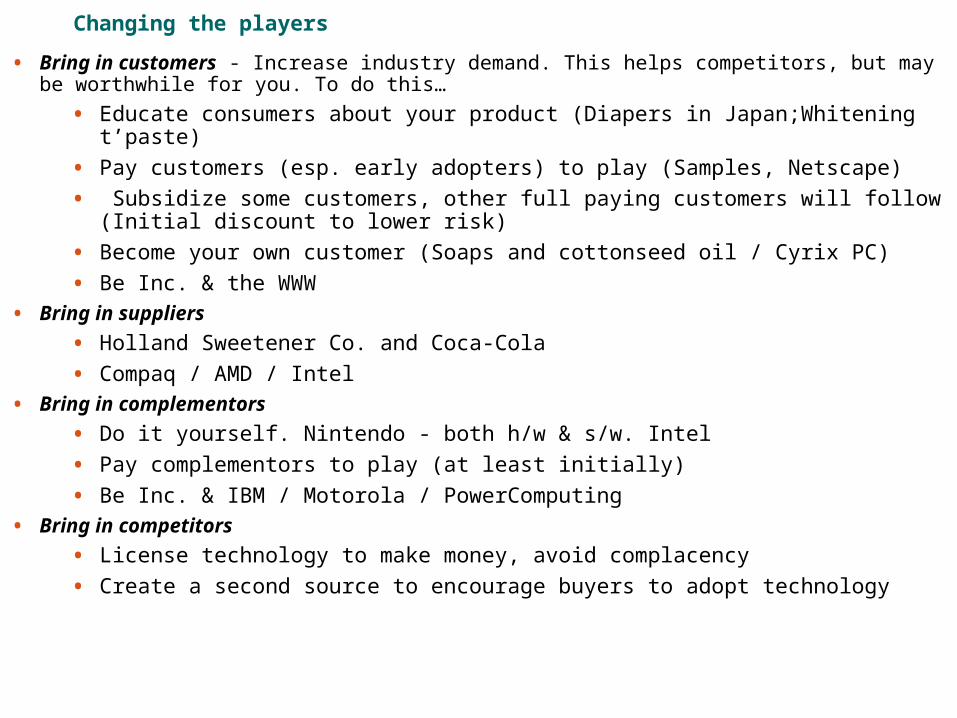

Changing the players

• Bring in customers - Increase industry demand. This helps competitors, but may be worthwhile for you. To do this…

• Educate consumers about your product (Diapers in Japan;Whitening t’paste)

• Pay customers (esp. early adopters) to play (Samples, Netscape)

• Subsidize some customers, other full paying customers will follow (Initial discount to lower risk)

• Become your own customer (Soaps and cottonseed oil / Cyrix PC)

• Be Inc. & the WWW

• Bring in suppliers

• Holland Sweetener Co. and Coca-Cola

• Compaq / AMD / Intel

• Bring in complementors

• Do it yourself. Nintendo - both h/w & s/w. Intel

• Pay complementors to play (at least initially)

• Be Inc. & IBM / Motorola / PowerComputing

• Bring in competitors

• License technology to make money, avoid complacency

• Create a second source to encourage buyers to adopt technology

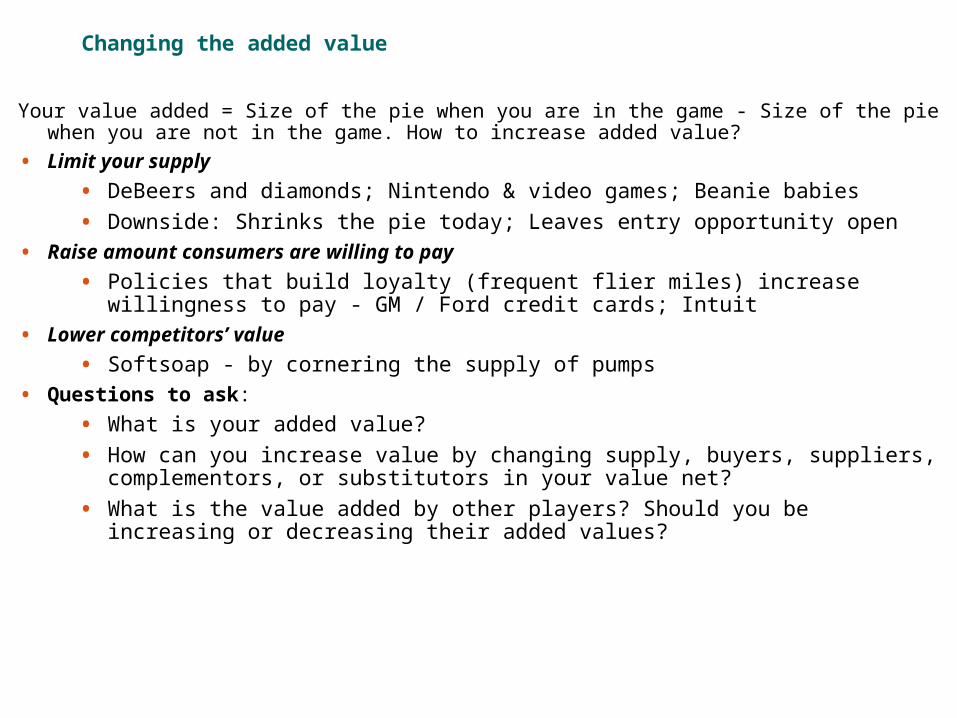

Changing the added value

Your value added = Size of the pie when you are in the game - Size of the pie when you are not in the game. How to increase added value?

• Limit your supply

• DeBeers and diamonds; Nintendo & video games; Beanie babies

• Downside: Shrinks the pie today; Leaves entry opportunity open

• Raise amount consumers are willing to pay

• Policies that build loyalty (frequent flier miles) increase willingness to pay - GM / Ford credit cards; Intuit

• Lower competitors’ value

• Softsoap - by cornering the supply of pumps

• Questions to ask:

• What is your added value?

• How can you increase value by changing supply, buyers, suppliers, complementors, or substitutors in your value net?

• What is the value added by other players? Should you be increasing or decreasing their added values?

Changing the rules

Questions to ask are:

• Which rules are helping you?

• Which ones are hurting you?

• Rules can be for pricing, advertising, product variety, satisfaction, etc.

• What kinds of contracts are you willing to write with your buyers and suppliers?

• Do you want Match Competition Clauses?

• What does this do for you?

• Do you have the power to change the rules?

• Does someone else have the power to overturn them?

• Can you signal your commitment credibly (Kiwi Air)

Changing tactics

Questions to ask are:

• How do other players perceive the game? How do these perceptions affect the play of the game? (NY Post vs. Daily News)

• Which perception do you want to keep, which to change?

• Do you want the game to be transparent or opaque (fee negotiation between investment banker and firm - guarantee / % fee)? When do you want to send signals that benefit you? When do you want to preserve the fog?

• To establish credibility (clear the fog)

- Accept a pay-for-performance contract

- Offer guarantees or advertise

- Ask others to demonstrate their credibility to you

• To preserve the fog

- Create complexity (long distance calling rates)

- Bluff: Ask yourself whether you will be believed and under what circumstances

- Ask what others stand to gain by preserving the fog, and what they could be bluffing about

Industry Analysis www. wai .bangkaew.comDate

Changing the scope

Questions to ask are:

• What is the current scope of the game?

• Do you want to change it?

• Games are linked over time and across markets (geographic and product markets)

• Do you want to link the current game to other games?

• When multi-market contact could be beneficial

• Do you want to delink the current game from other games?

177

Industry Analysis

Co-opetition

• More about forming alliances to better compete.

• Companies, competitors, customers and suppliers are participate in (and compete in) “the value net”.

• Key concept is “complementors”, companies that sell complementary products and services.

• These can often gain advantage by forming an alliance to provide a more competitive

178

Industry Analysis

การแข่�งข่�นค�อุการต�อุส��ที่��เคลื่��อุนไห์วิอุยู่��ตลื่อุดเวิลื่า

Industry Analysis www. wai .bangkaew.comDate

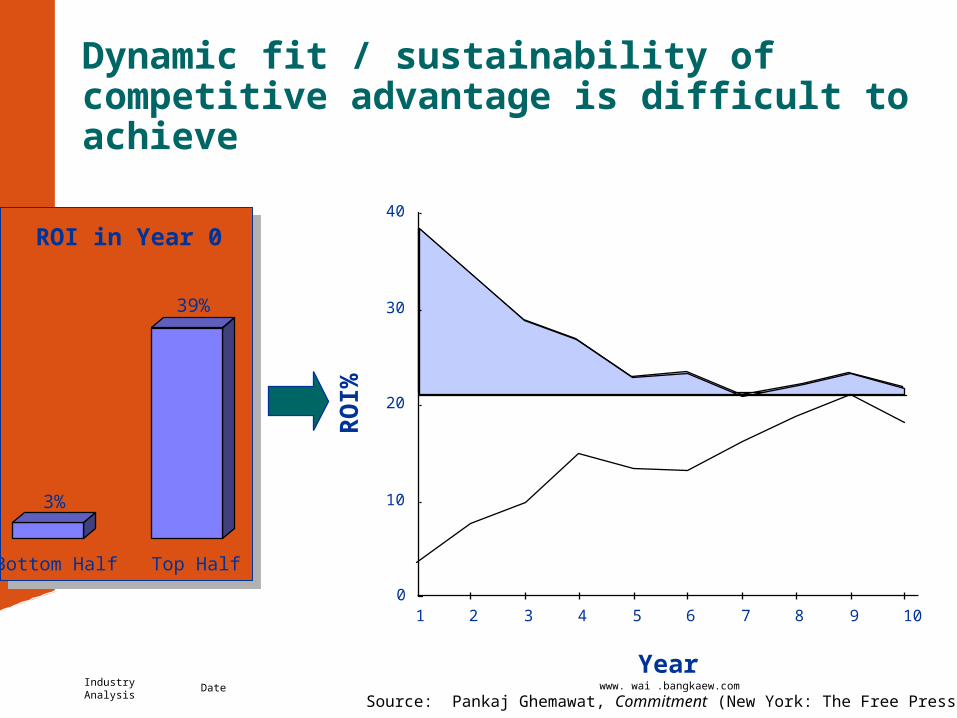

Building sustainable advantages

• Understand your own uniqueness

• Scan the environment for

- Technological changes

- Variations in input supply

- Demand shifts

• Invest in opportunities that fit

Source: Ghemawat, 1999

Industry Analysis www. wai .bangkaew.comDate

Building sustainable advantages (II)

• The best defense is a good offense, i.e., defend your advantage by continually upgrading it

- Seek out ways to increase willingness to pay without incurring commensurate supplier opportunity costs

- Seek out ways to reduce supplier opportunity costs without sacrificing commensurate willingness to pay

• Make yourself a moving target

• Remember that the landscape can shift under your feet

Source: Ghemawat, 1999

181

Industry Analysis

In many situations anticipating competitors moves can critical to building and sustaining competitive advantage

• Where in the course do we see the importance of interactive incentives?

- HSC vs. Nutrasweet

- Barnesandnoble vs. Amazon.com

- War of Attrition

- Intel vs. OEMs

• Interactive incentives tool kit

- Game theory

- Competitor analysis

182

Industry Analysis

A solution concept: the Nash Equilibrium

• Fundamental tool for examining non-cooperative games

- Idea: Every player does the best that he/she can, given that the other players are also doing the best that they can

• Definition

- a Nash equilibrium is a set of strategies for each player in which no player can improve his/her situation by choosing a different strategy, given the choices of the other players

• Testing for a Nash equilibrium

- Does any player have a profitable deviation? I.e., could any player improve his / her payoffs by choosing a different strategy?

• If there is a profitable deviation from a set of strategies, then this is not a Nash equilibrium

183

Industry Analysis

A famous example: The Prisoner’s Dilemma

Don’t Confess Confess

Don’t Confess

Confess

Prisoner A

Prisoner B

1 year 10 year

No prison 9 years

1 year No prison

10 years 9 years

184

Industry Analysis

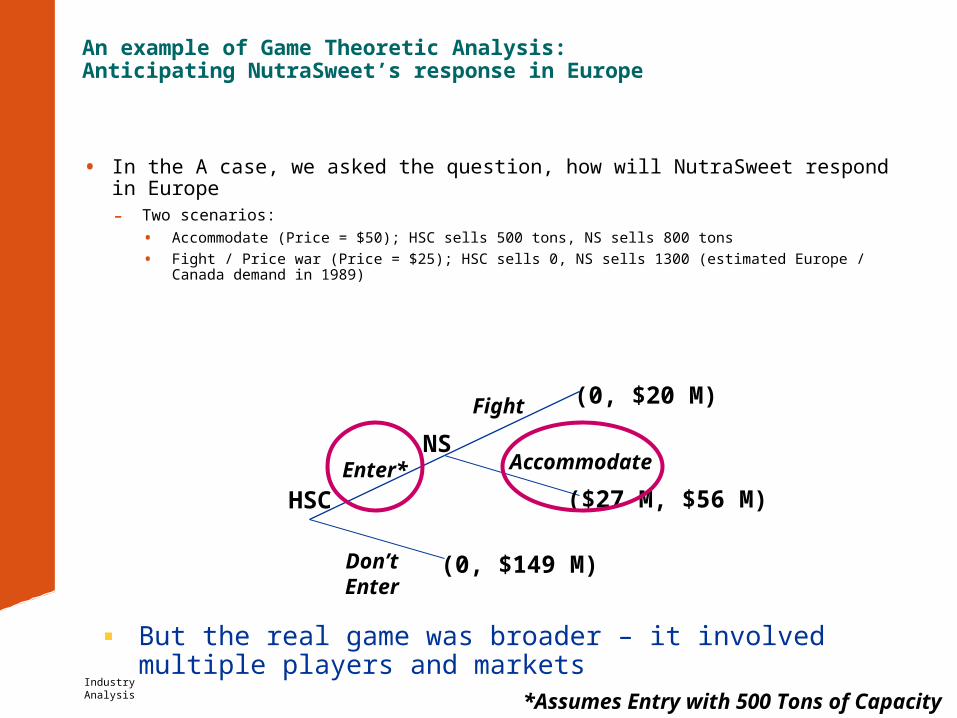

An example of Game Theoretic Analysis: Anticipating NutraSweet’s response in Europe

• In the A case, we asked the question, how will NutraSweet respond in Europe- Two scenarios:

• Accommodate (Price = $50); HSC sells 500 tons, NS sells 800 tons

• Fight / Price war (Price = $25); HSC sells 0, NS sells 1300 (estimated Europe / Canada demand in 1989)

(0, $20 M)

($27 M, $56 M)

(0, $149 M)

Fight

Enter*

Don’tEnter

Accommodate

HSC

NS

*Assumes Entry with 500 Tons of Capacity

But the real game was broader – it involved multiple players and markets

185

Industry Analysis

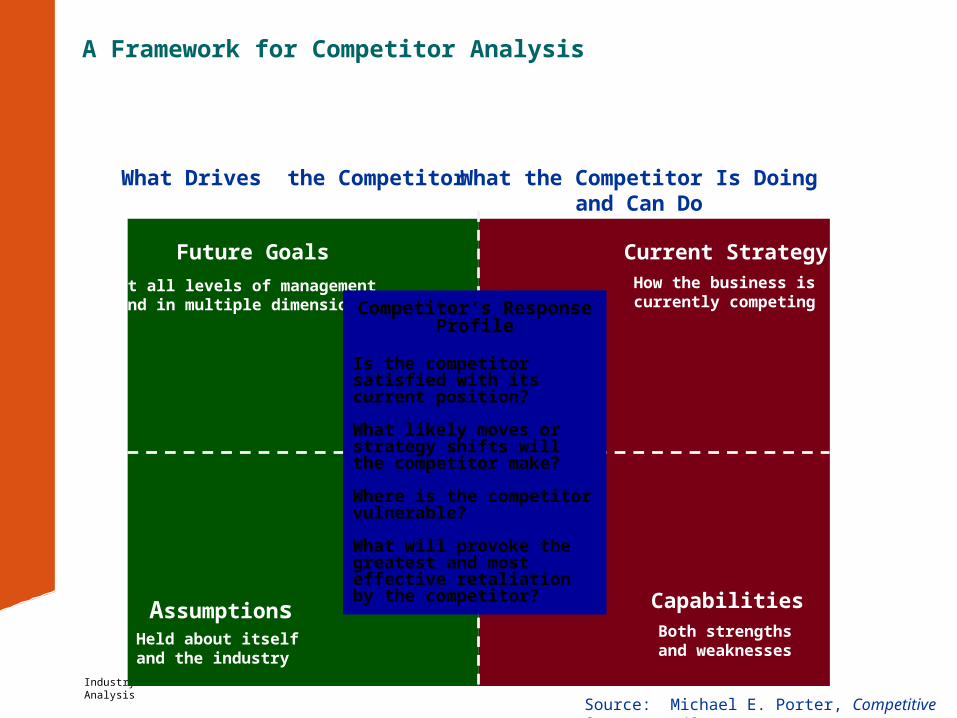

A Framework for Competitor Analysis

Source: Michael E. Porter, Competitive Strategy, p. 49

What the Competitor Is Doing and Can Do

What Drives the Competitor

Future Goals

At all levels of managementand in multiple dimensions

Current StrategyHow the business iscurrently competing

CapabilitiesBoth strengthsand weaknesses

AssumptionsHeld about itselfand the industry

Competitor’s Response Profile

Is the competitor satisfied with its current position?

What likely moves or strategy shifts will the competitor make?

Where is the competitor vulnerable?

What will provoke the greatest and most effective retaliation by the competitor?

Industry Analysis www. wai .bangkaew.comDate

Classic Good Moves ...

• Hard to match; cost them more than it costs you -- builds on strategic asymmetries

• Have commitment value; costly to reverse, so intentions will be believed

• Help\improve industry structure

• Lower costs and\or create value for customers

• Aim at competitor’s blind spots

• Anticipate the competition (it is easier to keep them out than kick them out)

Industry Analysis www. wai .bangkaew.comDate

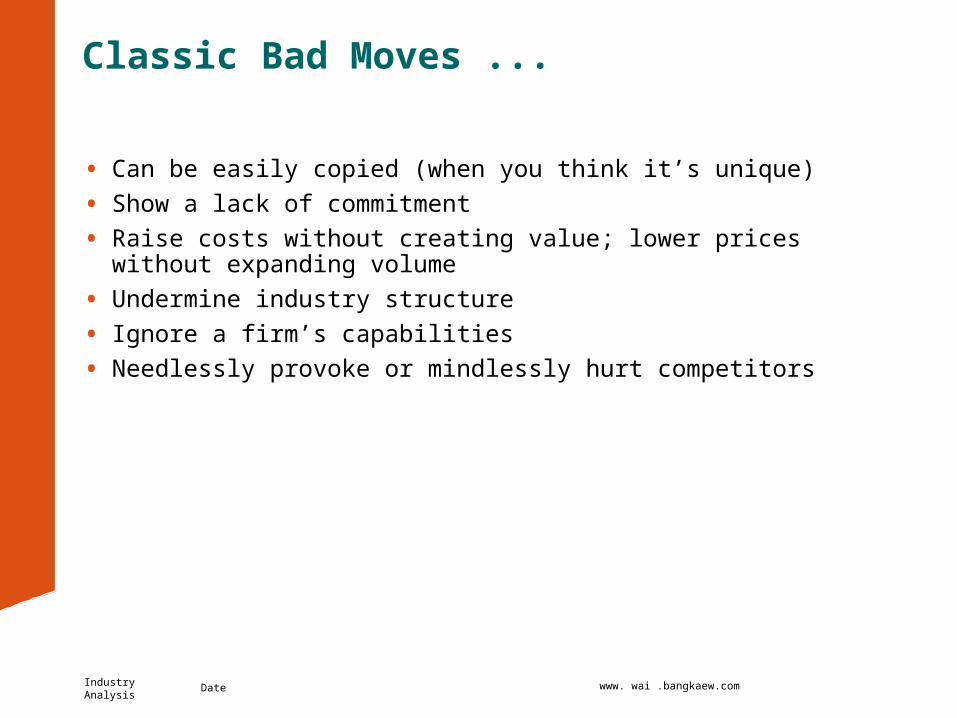

Classic Bad Moves ...

• Can be easily copied (when you think it’s unique)

• Show a lack of commitment

• Raise costs without creating value; lower prices without expanding volume

• Undermine industry structure

• Ignore a firm’s capabilities

• Needlessly provoke or mindlessly hurt competitors

Industry Analysis www. wai .bangkaew.comDate

Strategy

Capabilities& Resources

Industry /Business

Environment

Internal consistencyFit among strategicchoices and policies

External consistencyFit between the strategyand the outside world

Dynamic consistencyFit between the strategy and thefirm’s capabilities and resourcesover time

So what can we say about making these strategic choices and how they should fit together?

189

Industry Analysis

Internal, external, and dynamic consistency at Coors

BackwardIntegration Cans Other inputs

PlantScale

Procurement Manufacturing

OneProduct

IntermediatePrice

LimitedAdvertising

Product• Attributes• Rocky Mount. Image

Marketing

OneLocation

Unique Process• Asset-Intensive• Long• Unpasteurized

HighCapacity

Utilization

DistributionControls

RegionalDistribution

Distribution

Pre-1980s Post-1980s

• Regional / Local Advertising•Capacity Shortfall in the West

Internal

External • National Advertising• Incursion of competitors in the West

Dynamic

190

Industry Analysis

Internal consistency

• Activity maps can be helpful in assessing internal consistency of a strategy

• Question: Are activities chosen in such a way that they reinforce one another, or do they work at cross purposes?

- which are the key choices

• are they consistent with one another

- which are the links between choices?

• if there aren’t a lot of links, or if the links are very tenuous, this raises questions about the internal consistency of the firm’s strategy

Industry Analysis www. wai .bangkaew.comDate

Source: Michael E. Porter “What is Strategy” Harvard Business Review, Nov-Dec 1966

Limitedpassengeramenities

Short-haul,point-to-pointroutes betweenmidsize cities

and secondaryairports

Highaircraft

utilization

Frequent,reliable

departures

Lean, highlyproductiveground andgate crews

Very lowticket prices

No meals

No seatassignments

No baggagetransfers

No connectionswith other

airlines

15-minutegate

turnarounds

Limited useof travelagents

Automaticticketingmachines

Standardizedfleet of 737

aircraft

Flexibleunion

contracts

High levelof employee

stockownership

“Southwest,the low-fare

airline”

Highcompensationof employees

Southwest Airlines’ Activity Map

© 1999 Pankaj Ghemawat

192

Industry Analysis

External consistency: The manager’s problem

• To craft an effective strategy, you must take account of the external environment

- To decide whether to put your firm in an environment (entry)

- To decide whether to extricate your firm from an environment (exit)

- To position your firm to succeed in a given environment

- To assess the effect of a major change (e.g., deregulation)

- To shape the environment

• But the environment is enormously complex

Need structured ways of thinking about the environment– …that capture the richness of the real business world

– …but separate signal from noise

Threat of New Entry

Rivalry Among Existing Competitors

Bargaining Powerof Customers

Threat of Substitutes

Bargaining Powerof Suppliers

• Economies of scale• Proprietary product

differences• Brand identity• Switching costs

• Capital requirements• Access to distribution• Absolute cost advantages• Government policy• Expected retaliation

• Relative price performance of substitutes• Switching costs• Buyer propensity to substitute

• Industry growth• Fixed costs / value

added• Overcapacity• Product differences• Brand identity