overtime, exempt and non-exempt: 2016 wage … · overtime, exempt and non-exempt: 2016 wage and...

TRANSCRIPT

OVERTIME, EXEMPT AND NON-EXEMPT: 2016 WAGE AND HOUR UPDATE,

PART 1 & PART 2

First Run Broadcast: March 2 & 3, 2016

1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00a.m. P.T. (60 minutes each day)

Every employer must properly classify all employees as “exempt” or “non-exempt” for overtime

purposes. If an employer gets it wrong, it exposes itself to litigation, Department of Labor

complaints, and substantial financial liability for unpaid overtime. Classification is no easy

matter of separating employees into “manager” and “non-manager” categories. Moreover, the

changing nature of the workplace, including how technology allows us to work, has significantly

altered when a work day begins and ends, and thus the overtime payments to which non-exempt

employees are entitled. This program will provide you with a real-world guide to the rules and

principles governing worker classification, trends in DOL audits and private independent

contractor litigation, and best practices for avoiding liability.

Day 1 – March 2, 2016:

Review of new wage and hour regulations, including changes to salary threshold for

overtime purposes

Trends in hybrid federal/state litigation

“Fissured” industries and non-traditional employer-employee arrangements

Independent contractors, subcontractors, and franchised employees

Review of DOL enforcement priorities and trends in settlements and penalties

Day 2 – March 3, 2016:

Determining when an employee has managerial or administrative functions

Treatment of “inside” and “outside” sales people

Smartphones, technology and the “constant communications” rule

Working remotely – when does the workday begin and end?

How to handle meals and rest time

Donning and doffing of uniforms

Off-the-clock time

Speaker:

Raymond W. Bertrand is a partner in the San Diego office of Paul, Hastings LLP, where he

represents employers in a wide range of employment matters. His litigation practice includes

wage and hour, discrimination, harassment, retaliation, leaves of absence, contract disputes,

wrongful discharge, whistleblower, trade secrets and other types of employment-related matters.

In the wage and hour context, he also represents clients before the U.S. Department of Labor and

state regulators. He also authors the wage and hour section of Matthew Bender’s “California

Labor & Employment Bulletin” and has authored various articles on wage and hour matters. Mr.

Bertrand received his B.A. from State University of New York Binghamton and his J.D. from

Albany Law School.

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name ________________________ Middle Initial____Last Name___________________________

Firm/Organization _____________________________________________________________________

Address ______________________________________________________________________________

City _________________________________ State ____________ ZIP Code ______________________

Phone # ____________________________Fax # ______________________

E-Mail Address ________________________________________________________________________

Overtime, Exempt & Non-Exempt: 2016 Wage & Hour Update, Part 1

Teleseminar March 2, 2016 1:00PM – 2:00PM

1.0 MCLE GENERAL CREDITS

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association) Amount: _________ Credit Card (American Express, Discover, Visa or Mastercard) Credit Card # _______________________________________ Exp. Date _______________ Cardholder: __________________________________________________________________

VBA Members $75 Non-VBA Members $115

NO REFUNDS AFTER February 24, 2016

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name ________________________ Middle Initial____Last Name___________________________

Firm/Organization _____________________________________________________________________

Address ______________________________________________________________________________

City _________________________________ State ____________ ZIP Code ______________________

Phone # ____________________________Fax # ______________________

E-Mail Address ________________________________________________________________________

Overtime, Exempt & Non-Exempt: 2016 Wage & Hour Update, Part 2

Teleseminar March 3, 2016 1:00PM – 2:00PM

1.0 MCLE GENERAL CREDITS

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association) Amount: _________ Credit Card (American Express, Discover, Visa or Mastercard) Credit Card # _______________________________________ Exp. Date _______________ Cardholder: __________________________________________________________________

VBA Members $75 Non-VBA Members $115

NO REFUNDS AFTER February 25, 2016

Vermont Bar Association

CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: March 2, 2016 Seminar Title: Overtime, Exempt & Non-Exempt: 2016 Wage & Hour Update, Part 1 Location: Teleseminar - LIVE Credits: 1.0 MCLE General Credit Program Minutes: 60 General Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

Vermont Bar Association

CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: March 3, 2016 Seminar Title: Overtime, Exempt & Non-Exempt: 2016 Wage & Hour Update, Part 2 Location: Teleseminar - LIVE Credits: 1.0 MCLE General Credit Program Minutes: 60 General Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

2016 WAGE-HOUR UPDATE, PART 1 & PART 2

Raymond Bertrand, San Diego(o) (858) 458-3013

Blake Bertagna, Orange County(o) (714) 668-6208

Taylor Wemmer, San Diego(o) (858) 458-3065

2

OVERVIEW

Current Developments (Day 1)

DOL’s proposed revisions to the overtime regulations

DOL’s guidance on the joint employment test

DOL’s interpretation on the misclassification of independentcontractors

Case law update

Recent settlements

Mitigating Wage-Hour Risks (Day 2)

Off the clock claims (donning and doffing & training time)

Smartphones, technology and the “constant communications”rule

Meal and rest breaks

Telecommuting

Regular rate of pay

Preserving independent contractor status

DEPARTMENT OF LABOR’S PROPOSEDREVISIONS TO OVERTIME REGULATIONS

4

Enacted in 1938, the FLSA establishes

minimum wage, overtime pay,

recordkeeping, and youth employment

standards.

The most common FLSA minimum wage

and overtime exemptions – often called

the “white collar” exemptions – applies to

certain

Executives

Administrative employees

Professionals

FAIR LABOR STANDARDS ACT

5

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Federal Judicial Caseload Statistics 1995-2014

FLSA Cases (1995-2014)

6

THREE TESTS FOR EXEMPTION

Salary level

Salary basis

Job duties

7

PRESIDENT’S DIRECTIVE TO THE DEPARTMENT OF LABOR

President Obama, declaring that

the FLSA’s overtime regulations

“have not kept up with our

modern economy,” instructed the

Secretary of Labor in March

2014 to “consider how the

regulations could be revised to

update existing protections

consistent with the intent of the

Act; address the changing nature

of the workplace; and simplify the

regulations to make them easier

for both workers and businesses

to understand and apply.”

8

SALARY LEVEL – HISTORICAL VIEW

Year Salary Level

1938 • $ 30 for all exemptions

1940 • $30 for executive / $50 for administrative and professional

1949 • $55 for executive / $75 for administrative and professional

• $100 with a new “short test”

1958 • $80 for executive / $95 for administrative and professional

• $125 for the “short test”

1963 • $100 for executive and administrative / $115 for professionals

• $150 for the short test

1970 • $100 for executive and administrative / $115 for professionals

• $150 for the short test

1975 • $125 for executive and administrative / $140 for professionals

• $200 for the short test

2004 • $455 for all exemptions

• $100,000 annually for highly compensated employees

9

SALARY LEVEL – PROPOSED RULE

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

EAP HCE

Current

Proposed

Proposed rule would increase the

minimum salary required to qualify

as an exempt white collar employee

from $455/week ($23,660/year) to

approximately $970/week

($50,440/year).

Increase the total annual

compensation requirement needed

to exempt highly compensated

employees from $100,000/year to

approximately $122,148/year.

Establish a mechanism for

automatically updating the salary

and compensation levels going

forward.

10THE JOB DUTIES REQUIREMENTS FOR EXEMPTIONWOULD REMAIN UNCHANGED – MAYBE

Employees must meet certainrequirements as to their job duties toqualify for exempt status.

Employers must be able to establishthat the employee’s “primary duty” isthe performance of exempt work inorder for an exemption to apply.

“Primary duty” means the principal,main, major or most important dutythat the employee performs.

The DOL did not propose specificregulatory changes to the dutiestests, but did request comments onthe current requirements in responseto certain concerns the agency haswith the existing regulations.

11UNDER FURTHER REVIEW:THE “PRIMARY DUTIES” STANDARD

In the proposed regulations, the DOL states that it is

“concerned that employees in lower-level managementpositions may be classified as exempt and thus ineligible forovertime pay even though they are spending a significantamount of their work time performing nonexempt work.”

The DOL notes “that the removal of the more protective longduties test in 2004 has exacerbated these concerns and led to[] inappropriate classification[s].”

12UNDER FURTHER REVIEW:THE “CONCURRENT DUTIES DOCTRINE”

The DOL also questions the appropriateness of maintaining

the “concurrent duties doctrine,” which recognizes that exempt

executives often perform exempt duties concurrently with

nonexempt duties.

The DOL views this doctrine as “difficult to apply” and believes

it leads to inconsistent results.

The DOL specifically notes that “California has addressed thisissue by requiring that exempt [executive, administrative andprofessional] employees spend at least 50 percent of theirtime performing their primary duty, and not counting timeduring which nonexempt work is performed concurrently.”

13

DUTIES TEST: DOL SOUGHT COMMENTS

What, if any, changes should be made to the duties tests?

Should employees be required to spend a minimum amount of

time performing work that is their primary duty in order to qualify

for exemption? If so, what should that minimum amount be?

Should the DOL look to California’s law (requiring that 50 percent

of an employee’s time be spent exclusively on work that is the

employee’s primary duty) as a model?

Does the single standard duties test for each exemption category

appropriately distinguish between exempt and nonexempt

employees?

Is the concurrent duties regulation for executive employees

(allowing the performance of both exempt and nonexempt duties

concurrently) working appropriately or does it need to be

modified to avoid sweeping nonexempt employees into the

exemption?

14

ADMINISTRATIVE PROCESS

Notice of Proposed Rulemaking

60-Day Comment Period

Ended on September 4, 2015

DOL received roughly 270,000 comments

Final Rule

Solicitor of Labor M. Patricia Smith stated in November 2015 that

the finalized changes to the overtime eligibility rules likely will not

be released until late 2016.

Significant rules and major rules are required to have a 60 day

delayed effective date.

Query what effect the upcoming presidential election will have on

the rulemaking process.

15

STEPS EMPLOYERS SHOULD TAKE

Identify the salary levels ofexempt employees todetermine whether theymeet the DOL’s proposed$50,440 annual minimumthreshold.

Determine whether to adjustthe salaries of or reclassifyas non-exempt employeeswho fall below the proposedminimum salary threshold.

If employees are reclassifiedfrom exempt to non-exempt,determine an appropriatehourly rate.

16

EVOLUTION OF THE JOINT EMPLOYER TEST

17

BROWNING-FERRIS INDUSTRIES

Expanded the definition of a joint employer under the NationalLabor Relations Act.

Issue: Whether Browning-Ferris was the joint employer ofworkers provided by a staffing agency under a temporarylabor services agreement.

The Board abandoned the longstanding “direct and immediatecontrol” requirement for a finding of joint employment.

The Board will now consider “indirect” control exercisedthrough an intermediary employer such as a staffing agency.

Browning-Ferris has appealed to the D.C. Circuit.

18

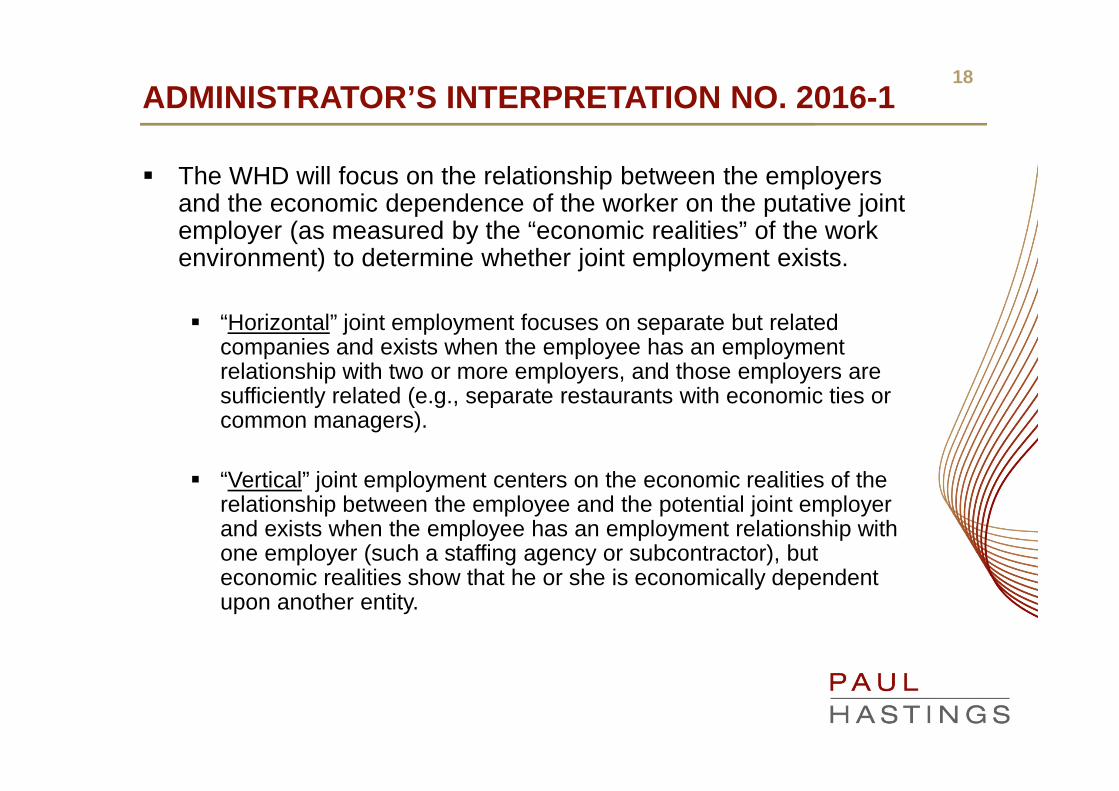

ADMINISTRATOR’S INTERPRETATION NO. 2016-1

The WHD will focus on the relationship between the employersand the economic dependence of the worker on the putative jointemployer (as measured by the “economic realities” of the workenvironment) to determine whether joint employment exists.

“Horizontal” joint employment focuses on separate but relatedcompanies and exists when the employee has an employmentrelationship with two or more employers, and those employers aresufficiently related (e.g., separate restaurants with economic ties orcommon managers).

“Vertical” joint employment centers on the economic realities of therelationship between the employee and the potential joint employerand exists when the employee has an employment relationship withone employer (such a staffing agency or subcontractor), buteconomic realities show that he or she is economically dependentupon another entity.

19

HORIZONTAL JOINT EMPLOYMENT

Nine facts may be relevant when analyzing the degree ofassociation between, and sharing of control by, potentialhorizontal joint employers:

(1) who owns the potential joint employers;

(2) do the potential joint employers have any overlappingofficers, directors, executives, or managers;

(3) do the potential joint employers share control over operations;

(4) are the potential joint employers’ operations inter-mingled;

(5) does one potential joint employer supervise the work of theother;

(6) do the potential joint employers share supervisory authorityfor the employee;

(7) do the potential joint employers treat the employees as a poolof employees available to both of them;

(8) do the potential joint employers share clients or customers;and

(9) are there any agreements between the potential jointemployers?

20

VERTICAL JOINT EMPLOYMENT

The AI lists seven factors from the MSPA regulations to determinevertical joint employment exists:

(1) Whether the potential joint employer directs, controls orsupervises the work performed;

(2) Whether the potential joint employer has the power to hire or firethe employee, modify employment conditions, or determine the rateor method of pay;

(3) Whether the potential joint employer had an indefinite, permanent,full-time, or long-term relationship with the subject employee(s);

(4) Whether the joint employee’s work for the potential joint employeris repetitive and rote, is relatively unskilled, and/or requires little or notraining;

(5) Whether the employee’s work is an integral part of the potentialjoint employer’s business;

(6) Where the work is performed on premises owned or controlled bythe potential joint employer indicates that the employee iseconomically dependent on the potential joint employer; and

(7) Whether common HR or labor relations functions exist.

U.S. LABOR DEPARTMENT'S INTERPRETATION ONMISCLASSIFICATION OF INDEPENDENT

CONTRACTORS UNDER THE FLSA

22

INTRODUCTION

In order for the FLSA to apply, there must be

an employment relationship between the

“employer” and the “employee.”

The FLSA defines employee as "any individual

employed by an employer" and employ is

defined as including "to suffer or permit to

work."

The concept of employment in the FLSA is

tested by "economic reality," a common-law,

multi-factored analysis.

On July 15, 2015, the U.S. Department of

Labor’s Wage and Hour Division (WHD)

issued a new interpretive paper entitled

“Administrator’s Interpretation No. 2015-1: The

Application of the Fair Labor Standards Act’s

‘Suffer or Permit’ Standard in the Identification

of Employees Who Are Misclassified as

Independent Contractors.”

23A CLOSE REVIEW OF THE ADMINISTRATOR’SAPPROACH TO DECIDING FLSA “EMPLOYEE” STATUS

Administrative Interpretations are intended to assist

employers (the regulated community) to comply with the law.

Per the WHD, they “provide meaningful and comprehensive

guidance and compliance assistance to the broadest number

of employers and employees.”

Administrator’s Interpretation No. 2015-1 devotes the majority

of its content to educating the reader on the WHD’s views as

to how to apply economic realities test’s factors.

The Administrator’s Interpretation represents that its depiction

of the test and its factors comes straight from established

Supreme Court and federal appellate court jurisprudence.

24

THE “ECONOMIC REALITIES” TEST

The “economic realities” factors typically include:

the extent to which the work performed isan integral part of the employer’s business;

the worker’s opportunity for profit or lossdepending on his or her managerial skill;

the extent of the relative investments of theemployer and the worker;

whether the work performed requiresspecial skills and initiative;

the permanency of the relationship; and

the degree of control exercised or retainedby the employer.

EE IC

25THE FACTORS PURPORTEDLY ARE NOT A FIXED SET - YET THE SIXDISCUSSED IN THE INTERPRETATION ARE DEPICTED AS MANDATORY

On one hand, the Interpretation states that the factors that

make up the economic realities test under federal case law

are not static.

Yet on the other hand, the Interpretation posits a rigid, fixed

set of economic reality test factors mandated for every FLSA

“employee” analysis.

As for the six factors detailed in the Interpretation, the

Administrator directs: “All of the factors must be considered in

each case.”

26NO ONE FACTOR IS DISPOSITIVE, BUT THE SPECIAL“INTEGRAL” FACTOR IS “COMPELLING”

The Interpretation is replete with warnings that no one factor

should be accorded greater importance than the others.

Yet the Interpretation singles out the “integral” factor as

“particularly” important. (The “integral” factor examines the

extent to which the work performed by the individual is “an

integral part of the employer’s business.”)

The Interpretation features the “integral” factor as the very first of

the six factors to be recited and discussed.

The Interpretation states that due to its special importance, this

factor “should always be analyzed in misclassification cases.”

The “integral” factor above all is depicted as “compelling.”

The result is conflicting guidance: No one factor should be

accorded greater importance, but the integral factor is

“compelling.”

27THE “CONTROL” FACTOR “SHOULD NOT PLAY ANOVERSIZED ROLE” IN THE ANALYSIS

The “control” factor looks to the level of control over a worker

by the alleged employer.

The Interpretation repeatedly downplays this factor:

[N]o one factor (particularly the control factor) isdeterminative of whether a worker is an employee.

The “control” factor, for example, should not be given undueweight.

[T]he “control” factor should not play an oversized role in theanalysis of whether a worker is an employee or anindependent contractor.

The control factor should not overtake the other factors of theeconomic realities test . . . .

Conclusion: . . . and no single factor, including control, shouldbe over-emphasized.

28THE “CONTROL” FACTOR “SHOULD NOT PLAY ANOVERSIZED ROLE” IN THE ANALYSIS (CONTINUED)

The “control” factor has long been given relatively greater weight by

the courts and the WHD.

The WHD’s Field Operations Handbook (Handbook) elevates the

“control” test above other factors:

The principal test relied upon by the courts for determiningwhether an employment relationship exists has been whetherthe possible employer controls or has the right to controlthe work to be done by the possible employee to the extentof prescribing how the work shall be performed.

Further, the Handbook depicts other factors as secondary to control:

If the possible employer has control over the manner in whichthe work is to be performed the absence of any or all of theforegoing factors will not indicate an absence of the employer-employee relationship. However, where the element of controlcannot be firmly established, they will help in determiningwhether the relationship is one of employer and employee[.]

Case law authorities also show special deference to the control

analysis.

29THE NATURE OF THE ADMINISTRATOR’S“INTERPRETATION” AND ITS LEGAL WEIGHT

Courts accord varying legal weight to WHDwork product. Administrator’s Interpretationsare not “controlling.”

They may be deemed persuasive, however,and earn deference by courts, depending oncertain factors identified by the Supreme Court:

[T]he thoroughness evident in itsconsideration, the validity of itsreasoning, its consistency with earlierand later pronouncements, and all thosefactors which give it power to persuade, iflacking power to control.

See Perez v. Mortgage Bankers Assoc., 135S. Ct. 1199, 1203-04 (2015).

Open question whether courts will affordAdministrator’s Interpretation No. 2015-1deference or whether it will be found to beinternally inconsistent in its approach, andirreconcilable with well-established,contradictory legal authorities.

30

CASE LAW UPDATE

31PEREZ V. MORTGAGE BANKERS ASS’N, 135 S. CT. 1199(2015)

Paralyzed Veterans held that an agency must use APA’s notice-

and-comment procedure when issuing a new interpretation of a

regulation that deviates significantly from a previous

interpretation.

In 2010, DOL withdrew a 2006 opinion letter stating that

mortgage-loan officers qualified for the FLSA administrative

exemption under the DOL’s 2004 regulations. At the same time,

the DOL issued its first AI, stating that mortgage-loan officers are

not exempt.

Mortgage Bankers Association argued the new AI was invalid.

The Supreme Court unanimously held that Paralyzed Veteranswas wrongly decided: the DOL could issue new interpretations

without being subject to notice-and-comment rulemaking

procedures.

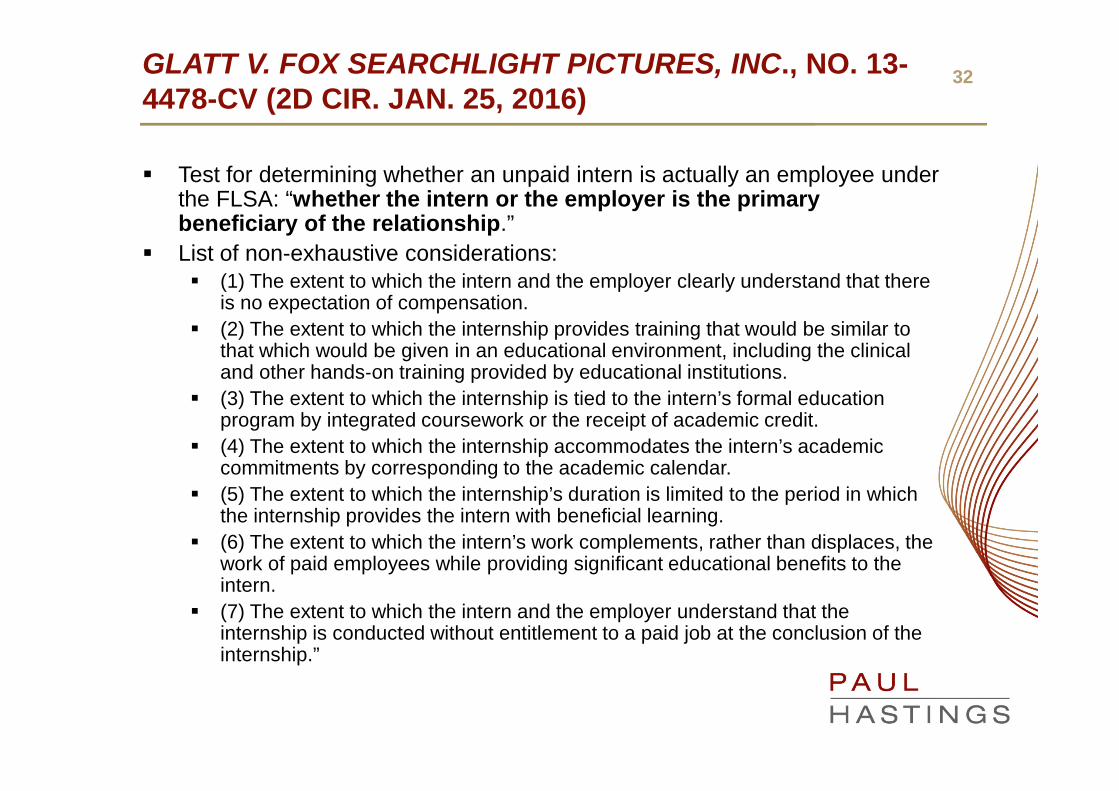

32GLATT V. FOX SEARCHLIGHT PICTURES, INC., NO. 13-4478-CV (2D CIR. JAN. 25, 2016)

Test for determining whether an unpaid intern is actually an employee underthe FLSA: “whether the intern or the employer is the primarybeneficiary of the relationship.”

List of non-exhaustive considerations:

(1) The extent to which the intern and the employer clearly understand that thereis no expectation of compensation.

(2) The extent to which the internship provides training that would be similar tothat which would be given in an educational environment, including the clinicaland other hands‐on training provided by educational institutions.

(3) The extent to which the internship is tied to the intern’s formal educationprogram by integrated coursework or the receipt of academic credit.

(4) The extent to which the internship accommodates the intern’s academiccommitments by corresponding to the academic calendar.

(5) The extent to which the internship’s duration is limited to the period in whichthe internship provides the intern with beneficial learning.

(6) The extent to which the intern’s work complements, rather than displaces, thework of paid employees while providing significant educational benefits to theintern.

(7) The extent to which the intern and the employer understand that theinternship is conducted without entitlement to a paid job at the conclusion of theinternship.”

33SAKKAB V. LUXOTTICA RETAIL N. AM., INC., 803 F.3D425, 428 (9TH CIR. 2015)

The district court, which acknowledged a split in California

authority, ruled that the Federal Arbitration Act (“FAA”)

preempted any California rule that barred waiver of PAGA

claims in arbitration agreements.

The California Supreme Court announced its decision in

Iskanian v. CLS Transportation Los Angeles, LLC, 59 Cal. 4th

348 (2014) (“Iskanian”), which held that employees could notwaive their right to bring representative claims under PAGA.

The Ninth Circuit followed the Iskanian decision -- an

arbitration agreement that requires individual arbitration of all

claims arising out of employment is unenforceable as applied

to PAGA claims.

34CHEEKS V. FREEPORT PANCAKE HOUSE, INC., 796 F.3D 199(2D CIR. 2015)

Generally, when parties settle a federal court action, they

simply file a stipulation that dismisses the case with prejudice.

By filing such a stipulation, the parties do not have to provide

the court with a copy of their settlement agreement and the

terms of any such agreement can remain private and

confidential.

The Second Circuit held that parties cannot dismiss FLSA

cases by stipulation and instead the parties must submit their

settlement agreement to the District Court for review so that

the District Court can determine whether the settlement is fair

and equitable.

35HOME CARE ASS'N OF AM. V. WEIL, 799 F.3D 1084 (D.C.CIR. 2015)

The FLSA has long exempted certain categories of “domestic

service” workers from the FLSA’s minimum wage and/or

overtime protections, including for domestic-service workers

providing either (1) companionship services or (2) live-in care

for the elderly, ill, or disabled.

In October 2013, the DOL issued its Final Rule seeking to

eliminate the FLSA’s “companionship services” exemption for

third-party providers, and to limit the definition of

“companionship services.”

The D.C. Circuit Court concluded that the DOL had the

authority to limit the exemptions and that its construction of

the exemptions here was entirely reasonable.

36OREGON REST. & LODGING ASS'N V. PEREZ, NO. 13-35765, 2016 WL 706678 (9TH CIR. FEB. 23, 2016)

Under the FLSA, where an employer claims a tip credit towardthe federal minimum wage, the employer may only require thatemployees pool tips with other employees who customarily andregularly receive tips. The FLSA is silent about who mayparticipate in a mandatory tip pool if the employer does not claima tip credit against the minimum wage.

In Cumbie v. Woody Woo, Inc., dba Vita Cafe, 596 P.2d 577 (9thCir. 2010), the court held that the FLSA’s restriction on tip sharingamong customarily and regularly tipped employees applies onlywhen their employer claims the federal tip credit.

In May 2011, DOL rejected Woody Woo and stated that tips arethe property of the employee whether or not the employer hastaken a tip credit and that a valid tip pool may only include “thoseemployees who customarily and regularly receive tips.”

A divided three judge panel held the DOL’s interpretation of theFLSA was “reasonable” and decided that the DOL may regulatetip pooling even when the employer does not use the FLSA’s tipcredit.

37

RECENT SETTLEMENTS

Alexander v. FedEx Ground Package System, No. 3:05-cv-00038-EMC (N.D.Cal.). Class of 2300 drivers in California alleged they’d been misclassified as independent

contractors.

Settlement of $227 million approved in October 2015.

Verderame vs. RadioShack Corp., No. 2:13-cv-02539, (E.D. Pa.) Class of 569 former store managers claimed they had not received proper overtime

pay.

In February 2016, the liquidating trustee overseeing RadioShack's bankruptcyagreed to pay $5.5 million in unsecured claims.

Brandon v. 3PD Inc., No.1:13-CV-03745 (N.D. Ill.) 115 of 258 eligible delivery drivers opted into action, claiming misclassification as

independent contractors.

In January 2016, court approved $3 million settlement.

Rite Aid Wage and Hour Cases, No. JCCP4583 (Los Angeles Sup. Ct.) 2775-member class of current and former pharmacists claimed to have been denied

meal and rest breaks.

Court indicated it would approve $9.7 million settlement.

Bararsani v. Coldwell Banker, No.BC495767 (Los Angeles Sup. Ct.) Certified class of approximately 5600 California real estate agents claiming

misclassification as independent contractors.

Court approved $4.5 million settlement in January 2016.

38

RECENT SETTLEMENTS (CONT.)

Dicks Sporting Goods cases (multi-district) Class of about 2,200 assistant store managers alleged they were misclassified as

exempt.

Proposed settlement of $10 million announced in December 2015.

Encarnacion v. J.W. Lee Inc., No. 0:14-cv-61927 (S.D. Fla.) Class of 4,709 exotic dancers claimed they had been misclassified as independent

contractors by a chain of clubs in Florida and Ohio.

Proposed settlement of $6 million announced in June 2015.

Awuah v. Coverall North America Inc., No. 1:07-cv-10287 (D. Mass.) Custodial “franchisees” alleged they should have been classified as employees.

Court approved $5.5 million settlement in May 2015.

Taylor v. Shippers Transport Express Inc., No. 2:13-cv-02092 (C.D. Cal) Certified class of 540 truck drivers alleged they had been misclassified as

independent contractors.

Court approved $11 million settlement in May 2015.

Fuentes v. Macy’s West Stores Inc., No. 2:14-cv-00790 (C.D. Cal.) Plaintiffs alleged that Macy’s and the department store’s logistics management

company, Joseph Eletto Transfer Inc., had misclassified as independentcontractors more than 600 drivers and helpers.

Settlement reached in 2015 provided that Macy’s would pay $3 million and Eletto $1million.

39

MANAGING WAGE-HOUR RISKS

© 2015 Paul Hastings LLP. CONFIDENTIAL

40

OFF THE CLOCK CLAIMS

© 2015 Paul Hastings LLP. CONFIDENTIAL

Donning and Doffing Time

Training Time

41

FLSA

Time spent changing into clothes required for the performance of

the principal activity is compensable as an integral part of that

activity, but changing clothes merely for the convenience of the

employee is considered a noncompensable "preliminary'' or

"postliminary'' activity. 29 CFR § 785.24

Changing clothes as a cautionary measure after working in a

toxic environment has been deemed an integral part of a

principal activity and therefore compensable under the FLSA.

Steiner v. Mitchell (1956) 350 U.S. 247, 252, 100 L. Ed. 267, 76

S. Ct. 330

Special exception for express terms of or by custom or practice

under a bona fide collective bargaining agreement applicable to

the employee. 29 U.S.C. § 203(o)

DONNING AND DOFFING TIME

42

FLSA

Special Rule for Changing Clothes at Home: “Employees who dress to

go to work in the morning are not working while dressing even though

the uniforms they put on at home are required to be used in the plant

during working hours. Similarly, any changing which takes place at

home at the end of the day would not be an integral part of the

employee’s employment and is not working time.” DOL Field

Operations Handbook § 31b13

DONNING AND DOFFING TIME

43

FLSA

IBP, Inc. v. Alvarez, 546 U.S. 21 (2005): Time spent walking between changing and production areas is

compensable.

Because donning and doffing gear that is “integral andindispensable” to employees’ work is a “principal activity,” thecontinuous workday rule mandates that the time spent walkingto and from the production floor after donning and beforedoffing, as well as the time spent waiting to doff, arecompensable.

Under the “continuous workday rule, . . . the ‘workday’ isgenerally defined as the period between the commencementand completion on the same workday of an employee’sprincipal activity or activities. 29 C.F.R. § 790.6(b) (2005).”Id. at 521.

Time spent waiting to don the first piece of gear that marks thebeginning of the continuous work day is not compensable.

“[Section] 4(a)(2) excludes from the scope of the FLSA thetime employees spend waiting to don the first piece of gearthat marks the beginning of the continuous workday.” Id. at528.

DONNING AND DOFFING TIME

44

FLSA

“Attendance at lectures, meetings, training programs and similar

activities need not be counted as working time if the following four

criteria are met:

Attendance is outside of the employee’s regular working hours;

Attendance is in fact voluntary;

The course, lecture, or meeting is not directly related to the

employee’s job; and

The employee does not perform any productive work during such

attendance.” 29 C.F.R. § 785.27

TRAINING TIME

45

FLSA

What is voluntary?

“Attendance is not voluntary, of course, if it is required by the

employer. It is not voluntary in fact if the employee is given to

understand or led to believe that his present working conditions or

the continuance of his employment would be adversely affected by

nonattendance.” 29 C.F.R. § 785.28.

TRAINING TIME

46

FLSA

What is directly related to the employee’s job?

“The training is directly related to the employee’s job if it

is designed to make the employee handle his job more

effectively as distinguished from training him for another

job, or to a new or additional skill. . . . Where a training

course is instituted for the bona fide purpose of

preparing for advancement through upgrading the

employee to a higher skill, and is not intended to make

the employee more efficient in his present job, the

training is not considered directly related to the

employee’s job even though the course incidentally

improves his skill in doing his regular job.” 29 CFR §

785.29

TRAINING TIME

47

SMARTPHONES, TECHNOLOGY AND THE

“CONSTANT COMMUNICATIONS” RULE

48

POTENTIAL FLSA VIOLATIONS

Today’s office culture is increasingly “smart-phone” oriented

Employees may feel pressured to stay in contact with the

office after they have clocked out for the day by checking text

messages or emails

Does an employee’s use of a cell phone after hours constitute

“hours worked” under the FLSA?

49

CASES

Agui v. T-Mobile USA, Inc. (E.D.N.Y. 2009)

T-Mobile employees, who were nonexempt sales

representatives, alleged that they were required to check work

related emails and texts even when not clocked in

Rulli v. CB Richard Ellis, Inc. (E.D. Wis. 2009)

Employees filed collective action claim for unpaid overtime

compensation based upon a company requirement to use

company-issued smart phone devices after hours and respond to

messages within 15 minutes

50

FACTORS TO CONSIDER

Is this activity an “integral and indispensable” part of theemployee’s “principal activity”?

Does the activity qualify as “work”?

Does the employer “permit” the employee to perform theactivity?

Is it necessary to perform a task?

Does it primarily benefit the employer?

On call time: engaged to wait or waiting to be engaged?

Employers cannot deny compensation to an employee if theemployer knows or has reason to know that an employee isworking overtime

51

POSSIBLE SOLUTIONS

Do not issue smartphones to non-exempt employees or do

not permit them to use them without prior authorization

Implement policies prohibiting smartphone use after hours

Require that employees record their time spent after hours

checking/responding to emails and voicemails

Might be able to track time worked through apps

Companies may wish to “audit” their nonexempt employees’

use of cell phones after work hours

52

CELL PHONE POLICIES: THINGS TO CONSIDER

Recording hours worked while using the company issued cell

phone

Expectations of privacy

Confidentiality

Who owns the device/information on the device

53

MEAL AND REST BREAKS

Steps Employers Can Take to Mitigate Risk

54

MEAL PERIODS – FLSA (29 C.F.R. 785.19)

Bona fide meal periods are not worktime.

Bona fide meal periods do not include coffee breaks or time forsnacks. These are rest periods.

The employee must be completely relieved from duty for thepurposes of eating regular meals.

The employee is not relieved if [the employee] is required toperform any duties, whether active or inactive, while eating.

For example, an office employee who is required to eat at [his/her]desk or a factory worker who is require to be at [his/her] machine isworking while eating.

It is not necessary that an employee be permitted to leave thepremises if [the employee] is otherwise completely freed from dutiesduring the meal period.

Ordinarily 30 minutes or more is long enough for a bona fidemeal period. A shorter period may be long enough under specialconditions.

55

Rest periods of short duration, running from 5 minutes to about 20minutes, are common in industry.

They promote the efficiency of the employee and are customarilypaid as working time.

They must be counted as hours worked.

REST PERIODS – FLSA (29 C.F.R. 785.18)

56

STATE SPECIFIC REQUIREMENTS

General: At least 21 states have general provisions requiring

employers to provide employees meal periods, and at least 7

states also have rest period requirements

Specific: 35 jurisdictions also have separate specific

provisions requiring meal periods specifically for minors.

Various states also have requirements for certain types of

workers (e.g., seasonal farm workers)

Exemptions:

State law exemptions for executive, administrative and

professional employees, and for outside salespersons

vary

Other state law exemptions may exist for certain types of

workers if the employees are covered by a valid collective

bargaining agreement

57

MAINTENANCE OF A WRITTEN POLICY

Number: the number of meal and rest breaks allowed

Timing: when the meal and rest breaks can be taken

Recording: how the meal breaks are to be recorded

Compliance: statement that employees are expected to take

their breaks

Complaint Process: employees are required to report to a

supervisors if they feel that they were denied their entitled

meal or rest break

Definition:

Key is to authorize and permit an employee to take all entitled

breaks.

Meal/rest periods are duty-free

58

COMMUNICATE POLICY

Obtain a signed acknowledgement from employees

Explain the meal and rest policy during the orientation process

Periodically remind employees about the policy through

announcements and/or employee trainings

59

TIME AND PAY SYSTEMS

Timekeeping system should record the start and end time of

meal periods

Affirmation by employee acknowledging that the employee

was provided the breaks he/she was entitled to

If state law provides for penalties for missed meal and/or rest

breaks, establish process for payment of such penalties

© 2015 Paul Hastings LLP. CONFIDENTIAL

60

INVESTIGATE MISSED MEAL/REST PERIODS

Establish processes for:

Investigating employee claims that a meal or rest period was not

provided in accordance with company policy

Flagging when an employee has not taken a meal period, and

investigate such incidents

61

SPECIAL MEAL AND REST PERIOD ISSUES

Meal period waivers

On-duty meal periods

Special/unique positions

62

TELECOMMUTING

How To Make Telecommuting Arrangements Work ForEveryone

63

Telecommuting is a work arrangement under which employees

are allowed to work from home or another non-company

location for all or part of their workday

Not every position is suitable for telecommuting. The employer

needs to consider:

Job duties – interaction with other employees required? Or is

the majority of the work able to be performed through

electronic/telephonic means?

What level of supervision is required?

What type of technology support/equipment is needed to

perform the job?

Does this employee work with highly sensitive/confidential

company materials?

HOW DOES TELECOMMUTING WORK?

64

© 2015 Paul Hastings LLP. CONFIDENTIAL

Although the position may be suitable for telecommuting, the

employer must also consider each employee on an individual

basis:

How long has the employee been with the company?

Can the employee work independently and without close

supervision?

How is the employee’s performance? Any discipline?

Does the employee have strong written and oral

communication skills?

Interaction with other laws:

ADA – Americans with Disabilities Act

OSHA – Workplace Safety

Workers’ Compensation

TELECOMMUTING IS NOT FOR EVERY EMPLOYEE

65

POTENTIAL WAGE AND HOUR ISSUES

Reporting and monitoring of hours

Working “off-the-clock”

Overtime

Portal to Portal Act

66

TELECOMMUTING POLICIES

It is important to have a written, comprehensive policy that

outlines the rules and procedures for telecommuters:

Telecommuting is not an entitlement and must be authorized by

the company

Outline eligible job positions/employees

Telecommuters have the same expectations as employees

working in the office; it is not a flex-schedule program

The company has the right to monitor all data and activity on

company systems, even for work performed while telecommuting

Dedicated work space in the home, especially when employee

works with/has access to confidential company data

67

TELECOMMUTING POLICES (CONTINUED)

Recording Work Time:

Clearly outline the hours the employee is expected to be

working/available during the workday

Telecommuting employees must keep a complete and accurate

record of the hours worked each day

Company should provide time sheets or an online system for

recording hours worked

Pre-approval of overtime for nonexempt employees

68

TELECOMMUTING ACKNOWLEDGMENT

In addition to a written policy, prepare a comprehensive

acknowledgement for each employee who is permitted to

participate in the company’s telecommuting program that is to

be signed by the employee

Define the employee’s working hours

Make clear that the telecommuting relationship can be

revoked by the company at any time

Outline if/how often the employee is required to check in with

supervisors

69

THE REGULAR RATE OF PAY

70

What Is the Regular Rate of Pay?

The Rate Used to Calculate Overtime: The Regular Rate ofpay is the rate that employers must use to calculate overtime.

An Hourly Rate: The Regular Rate is an hourly rate.Therefore, even though employers have the right to pay non-exempt employees other than by the hour (e.g., by salary, bycommission, and by piece), they must reduce all non-hourlyforms of pay to an hourly rate for overtime calculations.

Unique to Each Work Week: The Regular Rate is an hourlyrate that an employer must calculate work week by work week,not pay period by pay period.

Calculation Method (Outside California): All pay for hoursworked divided by all hours worked.

Calculation Method (Inside California): All pay for hoursworked divided by all hours worked, except that the divisor forfixed sums such as salaries and fixed-rate bonuses cannotexceed 40.

REGULAR RATE OF PAY

71

What Must Employers Include in the Regular Rate of Pay?

All Pay for All Hours Worked: The regular rate includes “allremuneration for employment paid to, or on behalf of, theemployee.” 29 USC § 207(e)

An All-Inclusive Rate: Courts resolve all doubts in favor ofinclusion.

The regular rate includes premiums for non-overtimework:

Night shift differentials

Premiums paid for hazardous, arduous or dirty work

Incentives for the rapid performance of work

Lump sum premiums which are paid without regard tothe number of hours worked

The regular rate also includes overtime premiums thatdo not conform to the overtime premiums authorizedby the Act.

REGULAR RATE OF PAY – INCLUSIONS

72

What May Employers Exclude from the Regular Rate of Pay?

Gifts: For example, gifts at year-end or other specialoccasions, rewards for service – as long as an employer doesnot measure the amount the amounts of which are notmeasured by or dependent on hours worked, production, orefficiency.

Payments that Are Not Compensation for Work Performed:For example, vacation pay, holiday pay, sick leave pay, andexpense reimbursements.

Certain Bonus Payments: For example, those for which thereis no prior announcement of an amount or a program.

Contributions to Health and Welfare Trusts

REGULAR RATE OF PAY - EXCLUSIONS

73

Daily or Weekly Premiums: For example, premiums forworking more than 8 hours in a day or more than 40 hoursin a week. (This rule exists to avoid pyramiding ofstatutory overtime and contractually promised premiums.)

Saturday, Sunday, Holiday and Similar Premiums: Forexample, premiums for working on a Saturday, Sunday,Holiday, Day of Rest, Sixth Day or Seventh Day, as longas the premium is at least 1.5 times the rate establishedfor similar work during non-overtime hours.

Premiums for Work Outside Specified Hours: Forexample, if an employer promises to establish all 8-hourwork schedules between 6:00 AM and 6:00 PM andfurther promises a premium of at least 1.5 times theRegular Rate for all work outside those hours, thosepremiums are excludable.

The Value of Income Derived from Stock Options,Stock Appreciation Rights and Stock Purchase Plans

REGULAR RATE OF PAY – EXCLUSIONS

74

PRESERVING INDEPENDENT CONTRACTORSTATUS

75

IRS TEST: OVERVIEW

For federal tax purposes, the usual common law rules are

applicable to determine whether a worker is an independent

contractor or an employee.

Under the common law, you must examine the relationship

between the worker and the business. All evidence of the

degree of control and independence in this relationship should

be considered.

The facts that provide this evidence fall into three categories:

Behavioral Control

Financial Control

The Relationship of the Parties.

76

FLSA: ECONOMIC REALITIES TEST

The “economic realities” factors typically include:

the extent to which the work performed is an integral part of the

employer’s business;

the worker’s opportunity for profit or loss depending on his or her

managerial skill;

the extent of the relative investments of the employer and the

worker;

whether the work performed requires special skills and initiative;

the permanency of the relationship; and

the degree of control exercised or retained by the employer.

77PRESERVING INDEPENDENT CONTRACTOR STATUS:PRACTICES TO AVOID

Do not utilize independent contractors who perform the same

duties as company employees.

Do not convert contractors to employees doing the same job.

Do not hire former employees as independent contractors

and, if you do, establish restrictions on their engagement that

prohibit them from performing the same work as when they

were employees.

78PRESERVING INDEPENDENT CONTRACTOR STATUS:PRACTICES TO AVOID (cont’d)

Do not provide independent contractors with employee

benefits.

Not only access to benefit plans but things like vacation,

access to employee discounts, invitations to employee

events.

Do not pay independent contractors in the same manner as

employees – no Christmas Bonus.

Limit training provided to the independent contractor to “need

to know” items that are related to a specific project. Do not

provide a new independent contractor with the full panoply of

training or orientation you would provide to a new employee.

79PRESERVING INDEPENDENT CONTRACTOR STATUS:PRACTICES TO AVOID (cont’d)

Do not require independent contractors to work a particular

schedule or hours of work. It is also important to avoid

tracking independent contractor hours or whereabouts.

Independent contractors should have far greater flexibility to

come and go as needed to complete the assigned project.

80PRESERVING INDEPENDENT CONTRACTOR STATUS:PRACTICES TO AVOID (cont’d)

Place limits on direction given to independent contractors.

Although some degree of communication regarding the

execution of a project is acceptable, you should avoid

controlling the way in which the goals of the independent

contractor are accomplished. Consider financial penalties in

the independent contractor agreement for failure to achieve

goals.

81

PRACTICES TO AVOID (cont’d)

Limit the length and scope of independent contractor projects.

Do not retain the independent contractors on an open ended

basis.

Do not use one independent contractor agreement to cover a

lengthy or open ended retention. Enter into new independent

contractor agreements for each significant project. Defining

the scope of the work to be performed and the length of the

engagement in the agreement are important.

Do not prohibit the independent contractor from working for

more than one client at a time.

20 OfficesACROSS ASIA, EUROPEAND NORTH AMERICA

1 Legal TeamTO INTEGRATE WITH THE STRATEGIC

GOALS OF YOUR BUSINESS

NORTH AMERICA

Atlanta

Chicago

Houston

Los Angeles

New York

Orange County

Palo Alto

San Diego

San Francisco

Washington, D.C.

EUROPE

Brussels

Frankfurt

London

Milan

Paris

ASIA

Beijing

Hong Kong

Seoul

Shanghai

Tokyo

82

For further information, you may visit our home page at

www.paulhastings.com or email us at [email protected]

www.paulhastings.com ©2015 Paul Hastings LLP

NORTH AMERICA EUROPE ASIA

Atlanta1170 Peachtree Street, N.E.

Suite 100

Atlanta, GA 30309

t: +1.404.815.2400

f: +1.404.815.2424

Chicago71 S. Wacker Drive

Forty-Fifth Floor

Chicago, IL 60606

t: +1.312.499.6000

f: +1.312.499.6100

Houston600 Travis Street

Fifty-Eighth Floor

Houston, TX 77002

t: +1.713.860.7300

f: +1.713.353.3100

Los Angeles515 South Flower Street

Twenty-Fifth Floor

Los Angeles, CA 90071

t: +1.213.683.6000

f: +1.213.627.0705

New York75 East 55th Street

First Floor

New York, NY 10022

t: +1.212.318.6000

f: +1.212.319.4090

Orange County695 Town Center Drive

Seventeenth Floor

Costa Mesa, CA 92626

t: +1.714.668.6200

f: +1.714.979.1921

Palo Alto1117 S. California Avenue

Palo Alto, CA 94304

t: +1.650.320.1800

f: +1.650.320.1900

San Diego4747 Executive Drive

Twelfth Floor

San Diego, CA 92121

t: +1.858.458.3000

f: +1.858.458.3005

San Francisco55 Second Street

Twenty-Fourth Floor

San Francisco, CA 94105

t: +1.415.856.7000

f: +1.415.856.7100

Washington, D.C.875 15th Street, N.W.

Washington, D.C. 20005

t: +1.202.551.1700

f: +1.202.551.1705

BrusselsAvenue Louise 480-5B

1050 Brussels

Belgium

t: +32.2.641.7460

f: +32.2.641.7461

FrankfurtSiesmayerstrasse 21

D-60323 Frankfurt am Main

Germany

t: +49.69.907485.0

f: +49.69.907485.499

LondonTen Bishops Square

Eighth Floor

London E1 6EG

United Kingdom

t: +44.20.3023.5100

f: +44.20.3023.5109

MilanVia Rovello, 1

20121 Milano

Italy

t: +39.02.30414.000

f: +39.02.30414.005

Paris96, boulevard Haussmann

75008 Paris

France

t: +33.1.42.99.04.50

f: +33.1.45.63.91.49

Beijing19/F Yintai Center Office Tower

2 Jianguomenwai Avenue

Chaoyang District

Beijing 100022, PRC

t: +86.10.8567.5300

f: +86.10.8567.5400

Hong Kong21-22/F Bank of China Tower

1 Garden Road

Central Hong Kong

t: +852.2867.1288

f: +852.2526.2119

Seoul33/F West Tower

Mirae Asset Center1

26, Eulji-ro 5-gil, Jung-gu,

Seoul, 04539, Korea

t: +82.2.6321.3800

f: +82.2.6321.3900

Shanghai43/F Jing An Kerry Center Tower II

1539 Nanjing West Road

Shanghai 200040, PRC

t: +86.21.6103.2900

f: +86.21.6103.2990

TokyoArk Hills Sengokuyama Mori Tower

40th Floor, 1-9-10 Roppongi

Minato-ku, Tokyo 106-0032

Japan

t: +81.3.6229.6100

f: +81.3.6229.7100

OUR OFFICES83