outlook for us dried fruit & tree nuts ......outlook for us dried fruit & tree nuts:...

TRANSCRIPT

© Euromonitor International

1

OUTLOOK FOR US DRIED FRUIT & TREE NUTS: CONSUMPTION & EXPORT TRENDS

DFA OF CALIFORNIA AND SPECIALTY CROP TRADE COUNCIL 2012 ANNUAL

CONFERENCE: BEYOND GRAVITY, CATCH FIRE

© Euromonitor International

2

About Euromonitor International

Global & Regional Market Overview

US Exports & Opportunity Zones

Drivers, Constraints & Trends

© Euromonitor International

3

EUROMONITOR INTERNATIONAL OVERVIEW

Business information provider since 1972

Global strategic information tools and services to understand industry performance trends, drivers and market opportunities

World’s leading governments, manufacturers, academic institutions, retailers, banks, and suppliers among our clients

Cover 205 markets with 1400+ employees and on-the-ground research teams in 80 countries

Award-winning online databases, market reports, statistical reference books, and custom information tools and research services

Offices in London, Chicago, Santiago, Singapore, Shanghai, Vilnius, Cape Town, Dubai, Tokyo, Bangladesh and Sydney

© Euromonitor International

4

About Euromonitor International

Global Market Overview

US Exports & Opportunity Zones

Drivers, Constraints & Trends

© Euromonitor International

5

KEY FACTS

GLOBAL OVERVIEW

Market performance

• The global processed food market approached $3.4 trillion in 2011; global consumer foodservice is estimated to have topped $2.3 trillion.

• US tree nut exports neared $5 billion, while dried fruit exports approached $710 million.

• Consumption generally climbing with populations, rising disposable incomes, and desires for increased health & wellness, convenience and indulgence.

• Developing regions with rising populations, GDP, and shifting per capita consumption are helping to drive significant growth.

Largest Categories • Almonds

• Walnuts

• Pistachios

• Grapes, Dried

• Prunes

Historical US growth categories • Almonds

• Pistachios

• Walnuts

• Grapes, Dried

• Mixtures of Nuts

Fastest growing US exports • Brazil Nuts (no shell)

• Macadamia Nuts

• Cashew Nuts (in shell)

• Walnuts (in shell)

• Almonds (in shell)

Largest US export sectors

© Euromonitor International

6

PROCESSED FOOD: GLOBAL RETAIL VALUE PERFORMANCE

Processed food consumption neared $3.4 trillion in 2011 – many of food categories within Packaged Food utilize tree nuts / dried fruits as inputs.

Global value growth from 2011-2015 of $890 billion is expected, representing a 27% surge from 2011 levels -- this is expected to vary widely by region and country.

BROAD CATEGORY RETAIL SALES

© Euromonitor International

7

WORLDWIDE RETAIL SALES BY PACKAGED FOOD CATEGORY

CATEGORIES INCLUDING STAPLES, INDULGENCE, CONVENIENCE AND

© Euromonitor International

8

MAJOR GROWTH CONTRIBUTORS: DEVELOPING REGIONS

Asia-Pacific, Western Europe, and Latin America with largest value growth since 2007; North America trails most other regions in value growth.

Asia-Pacific & Latin American combined for 44% of global value growth since 2007; Asia-Pacific’s value growth for the period is expected to be more than twice that of North America by year’s end.

The same regions also showed the greatest growth in volume terms -- marking them as potential opportunity zones for US exports.

ASIA-PACIFIC AND LATIN AMERICA NOTABLE

© Euromonitor International

9

FUTURE GROWTH TIED MOSTLY TO DEVELOPING REGIONS

Western Europe represents the largest sales with $605 billion in 2011.

But greatest percentage and “absolute” value growth is coming from developing regions.

North America and Western Europe are expected to grow by 11% in value terms, while all other regions are growing at 2-5 times that rate.

FORECASTS FURTHER EMPHASIZE IMPORTANCE OF DEVELOPING REGIONS

0%

10%

20%

30%

40%

50%

60%

$0$100$200$300$400$500$600$700$800

Regional Packaged Food Value Sales: 2011-15 & Growth Rate - US$ bn - Fixed 2011 Ex. Rates

2011

2015

% Growth

© Euromonitor International

10

VOLUME EXPANSION ALSO IN DEVELOPING MARKETS

SIZEABLE GAINS IN VOLUME

Asia-Pacific, Middle East & Africa and Latin America are expected to combine for approximately 83% global volume growth in packaged foods from 2011-2015.

Asia-Pacific is expected to be 54% of total global volume growth during this period.

Western Europe and North America are projected to be 7% and 3% of global volume growth and are experiencing flat (or diminishing) per capita consumption.

© Euromonitor International

11

COUNTRY CAGR: PACKAGED FOODS FORECAST

DEVELOPING MARKETS ARE KEY TO GLOBAL GROWTH IN PROCESSED PRODUCTS

© Euromonitor International

12

ANTICIPATED VOLUME GROWTH IN PACKAGED FOOD

CHINA EATING UP COMMANDING SHARE IN PACKAGED FOOD

© Euromonitor International

13

ASIA PACIFIC CONSUMES MOST OF WORLD’S FRESH FOOD

Global consumption of fresh foods reached 1.85 billion tonnes in 2010.

Asia Pacific consumed 65% of the global total and, on a per capita basis, 16% more than those in North America.

ASIA PACIFIC PUSHING UP GLOBAL DEMAND

Asia Pacific 65%

Latin America 8%

Middle East and Africa 8%

Western Europe 8%

Eastern Europe 6%

North America 5% Australasia

0%

2010 World Fresh Food Consumption by Region

Asia Pacific

Latin America

Middle East and Africa

Western Europe

Eastern Europe

North America

Australasia

© Euromonitor International

14

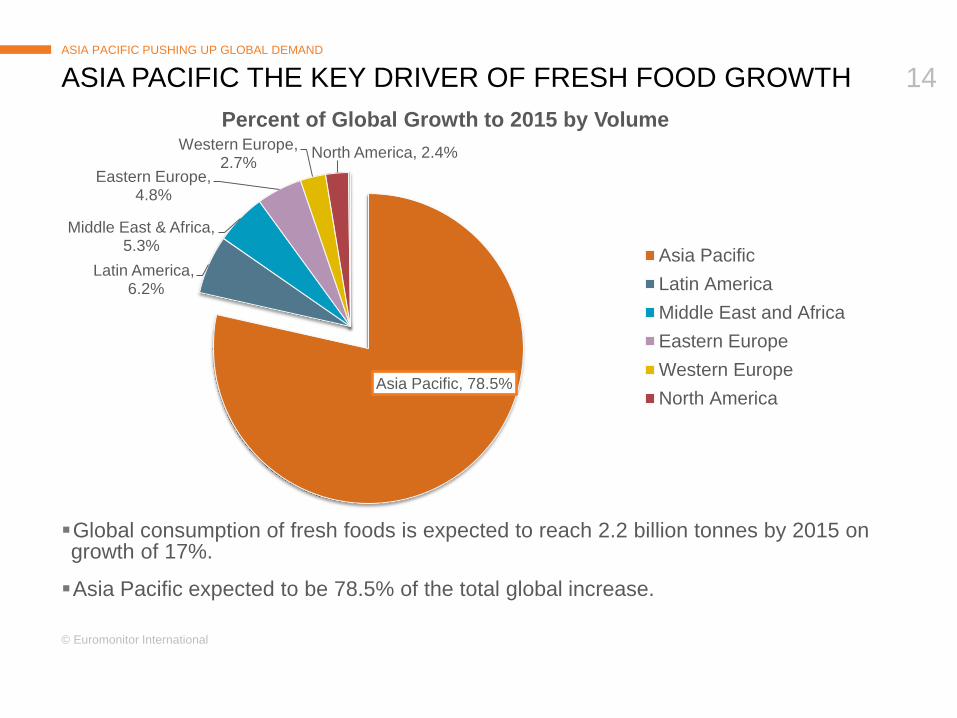

ASIA PACIFIC THE KEY DRIVER OF FRESH FOOD GROWTH

Global consumption of fresh foods is expected to reach 2.2 billion tonnes by 2015 on growth of 17%.

Asia Pacific expected to be 78.5% of the total global increase.

ASIA PACIFIC PUSHING UP GLOBAL DEMAND

Asia Pacific, 78.5%

Latin America, 6.2%

Middle East & Africa, 5.3%

Eastern Europe, 4.8%

Western Europe, 2.7%

North America, 2.4%

Percent of Global Growth to 2015 by Volume

Asia Pacific

Latin America

Middle East and Africa

Eastern Europe

Western Europe

North America

© Euromonitor International

15

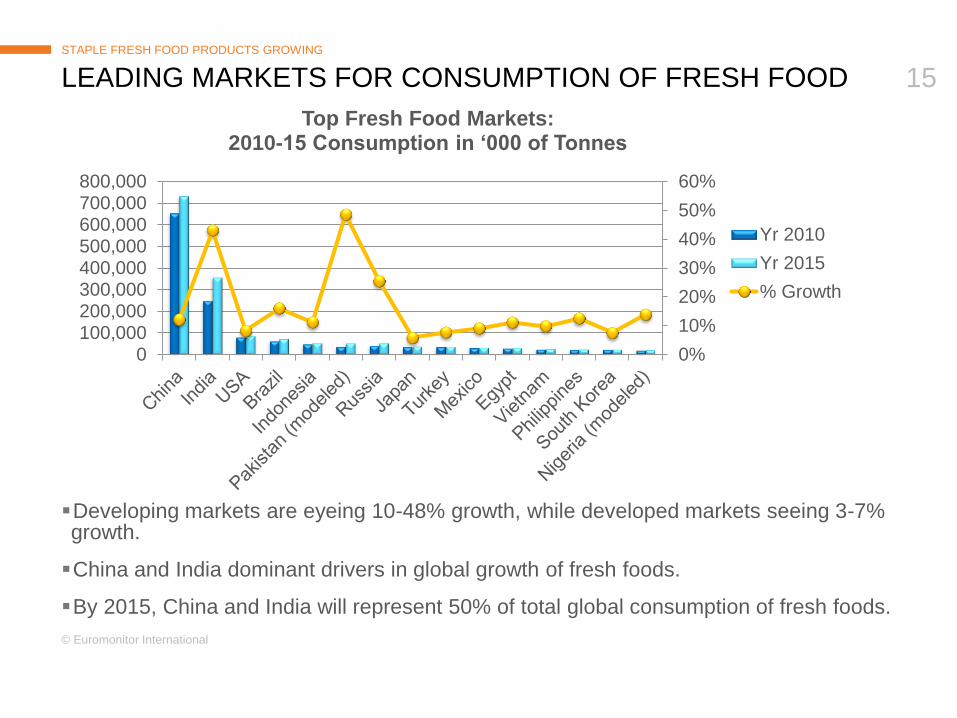

LEADING MARKETS FOR CONSUMPTION OF FRESH FOOD

Developing markets are eyeing 10-48% growth, while developed markets seeing 3-7% growth.

China and India dominant drivers in global growth of fresh foods.

By 2015, China and India will represent 50% of total global consumption of fresh foods.

STAPLE FRESH FOOD PRODUCTS GROWING

0%

10%

20%

30%

40%

50%

60%

0100,000200,000300,000400,000500,000600,000700,000800,000

Top Fresh Food Markets: 2010-15 Consumption in ‘000 of Tonnes

Yr 2010

Yr 2015

% Growth

© Euromonitor International

16

Global consumer foodservice estimated to have topped $2.3 trillion in 2011.

The global foodservice industry saw a return to growth in 2010, following a miserable 2009.

Growth was far from evenly distributed, with strong growth in Asia Pacific and Latin America offset by continued weakness in North America and Western Europe.

Relatively strong growth in quick-service categories, like fast food and street stalls/kiosks, as consumer desire for value and convenience remained strong.

Growth in Western Europe, above all, is expected to remain weak amid continued talk of austerity, with further government budget cuts expected to act as a brake on overall demand.

A TENTATIVE RETURN TO GROWTH IN 2010

CONSUMER FOODSERVICE: GLOBAL PERFORMANCE

© Euromonitor International

17

A RETURN TO GROWTH IN 2010

CONSUMER FOODSERVICE: GLOBAL PERFORMANCE

Full-service restaurants continue to account for around half of all foodservice demand globally

China remains home to the majority of the world's full-service restaurant outlets, with the format serving as the centre of social life for many Chinese consumers.

Several of the most important emerging markets – Brazil in particular – boast strong full-service restaurant categories, ensuring the category's overall dominance for years ahead.

© Euromonitor International

18

Asia Pacific accounted for around 40% of global foodservice spending in 2010, and saw rapid growth in that year.

China, India and Indonesia continue to expand in step with rising disposable incomes.

While both North America and Western Europe remain large, many operators cut back on outlet growth in favour of measures designed to increase same-store sales and eating frequency.

GLOBAL PERFORMANCE ASIA PACIFIC DOMINANT BY WIDE MARGIN

© Euromonitor International

19

Asia Pacific had four markets in the global top 10 in 2010, the same as Western Europe, with growth rates far in excess of any major European market.

Emerging markets have become well-established as key global markets.

China is now firmly entrenched as the world's number two consumer foodservice market.

Latin America also continues to see significant growth

Brazil, Argentina and Colombia now the key growth markets on the continent, spurred by a combination of growing consumer spending and relative financial stability on the continent.

Asian Markets Now Key 2010

Market 2010 sales (US$ billion)

US 436.9

China 333.4

Japan 240.5

Brazil 128.2

Spain 110.5

Italy 101.8

India 87.4

UK 83.4

France 62.1

South Korea 58.9

EMERGING MARKETS CONTINUE TO TAKE SHARE

ASIA PACIFIC AND LATIN AMERICA CONTINUE TO RESHAPE LANDSCAPE

© Euromonitor International

20

About Euromonitor International

Global Market Overview

US Exports & Opportunity Zones

Drivers, Constraints & Trends

© Euromonitor International

21

US PROCESSED PRODUCT EXPORTS SET RECORD IN 2011

US PROCESSED PRODUCT EXPORTS SEEING REMARKABLE GROWTH

US processed product exports topped US$58 billion in 2011.

This represents growth of nearly 80% within the five-year period from 2006-2011.

© Euromonitor International

22

EXPORT VOLUME IS ALSO GROWING – BUT NOT AS QUICKLY

VOLUME TRAILS

The upward trend from 2006-2011 result in overall volume growth of 16%.

Through February 2012, volume is up this year by 16% over last year.

© Euromonitor International

23

THE STORY SHOWN IN EXPORTS

STAPLES, CONVENIENCE, INDULGENCE, HEALTH…

0%

20%

40%

60%

80%

100%

120%

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

2006-2010: US Exports in ‘000 Dollars and Growth

Yr 2006

Yr 2010

% Growth2006-10

© Euromonitor International

24

EXPORTS TO DEVELOPING MARKETS HAVE LEAPED AHEAD

DEVELOPED VS. DEVELOPING MARKETS

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

Yr 2006 Yr 2010

2006 & 2010: US Exports of Processed Food Products - Developing vs. Developed Economies in US$ ‘000

Developing Economies

Developed Economies

Overall exports to developing markets

grew 67%, while those to developed

markets grew 37%.

© Euromonitor International

25

SURGING EXPORT GROWTH IN DEVELOPING REGIONS

PROCESSED FOOD PRODUCTS

-20%

0%

20%

40%

60%

80%

100%

120%

140%

$-

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

$18,000,000

$20,000,000

2006-2010: US Exports of Processed Food Products

Yr 2006

Yr 2010

% Growth

© Euromonitor International

26

EXPORTS IN DRIED HAVE SURGED AS WELL

DRIED GROWING AT ALL BROAD LEVELS

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

Nuts Dried Fruit Dried Vegetables

2007-2011: US Exports of Tree Nuts & Dried Products – US$ ‘000 & Growth Rate

Yr 2007

Yr 2011

% Growth

NOTE: “Nuts” excludes Coconuts, Brazilian and Cashew Nuts

© Euromonitor International

27

EAST ASIA & MIDDLE EAST PRIMARY DRIVERS OF GROWTH

REGIONAL GROWTH OF US TREE NUT EXPORTS

0%

50%

100%

150%

200%

250%

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

$1,800,000

2007-2011: US Tree Nut Exports - US$ '000 & Growth Rate

Yr 2007

Yr 2011

% Growth

Exports of Tree Nuts are up

74% to East Asia from Jan-

Feb vs same period last

year, while EU is up 14%.

© Euromonitor International

28

MAJOR TREE NUT EXPORTS SEEING SOLID GROWTH

EXPORT TOTALS HAVE SURGED FOR MOST TREE NUTS WITH ALMONDS LEADING

0%

50%

100%

150%

200%

250%

300%

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

2007-2011: Leading US Tree Nut Exports – US$ ‘000 & Growth Rate

Yr 2007

Yr 2011

% Growth

© Euromonitor International

29

HONG KONG KEY MARKET, SEEN RE-EXPORTING TO CHINA

EXPORT SURGE TIED PRIMARILY TO ASIA PACIFIC MARKETS

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000

$900,000H

on

g K

on

g

Spain

Ge

rma

ny

India

Ca

na

da

Un

ite

d A

rab

Em

ira

tes

Ja

pa

n

Tu

rke

y

Ne

the

rla

nd

s

Ch

ina

Ko

rea

, S

ou

th

Ita

ly

Me

xic

o

Be

lgiu

m-L

uxe

mb

ou

rg

Un

ite

d K

ing

do

m

Fra

nce

Isra

el

Ru

ssia

Vie

tnam

Au

str

alia

2007-2011: Top Markets for US Tree Nut Exports – US$ '000 & Growth Rates

Yr 2007

Yr 2011

% Growth

© Euromonitor International

30

EXPORT VOLUME GAINS DRIVEN BY DEVELOPING MARKETS

VOLUME IN TREE NUTS

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000H

on

g K

on

g

Spain

Ind

ia

Ge

rma

ny

Tu

rke

y

Un

ite

d A

rab

Em

ira

tes

Ch

ina

Ca

na

da

Ja

pa

n

Ita

ly

Ne

the

rla

nd

s

Ko

rea

, S

ou

th

Me

xic

o

Be

lgiu

m-L

uxe

mb

ou

rg

Vie

tna

m

Fra

nce

Ru

ssia

Un

ite

d K

ing

do

m

Isra

el

Au

str

alia

2007-2011: US Volume Exports of Tree Nuts in Metric Tonnes

Yr 2007

Yr 2011

© Euromonitor International

31

EXPORTS TO EAST ASIA TO ECLIPSE EUROPEAN UNION

REGIONAL GROWTH OF DRIED FRUIT EXPORTS

0%

50%

100%

150%

200%

250%

300%

350%

400%

$0

$50,000

$100,000

$150,000

$200,000

$250,000

2007-2011: US Dried Fruit Exports – US$ ‘000 & Growth

Yr 2007

Yr 2011

% Growth

Exports of Dried Fruit are up

7% to East Asia from Jan-

Feb vs same period last

year, while EU is up 2%.

© Euromonitor International

32

DRIED FRUITS POSITIVE BUT NOT WITHOUT CHALLENGES

RAISINS REMAIN SIGNIFICANT GROWTH FACTOR FOR THE CATEGORY

-50%

0%

50%

100%

150%

200%

250%

300%

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

2007-2011: Leading US Dried Fruit Export Categories – US$ '000 & Growth Rate

Yr 2007

Yr 2011

% Growth

Cult. Blueberries:

7800% growth from

$0 to $7.8 mn.

© Euromonitor International

33

VALUE UP IN MOST LEADING MARKETS

VALUE GROWTH WIDELY SEEN

-50%

0%

50%

100%

150%

200%

250%

300%

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

Ja

pa

n

Canada

Ge

rma

ny

Un

ite

d K

ing

do

m

Au

str

alia

Ko

rea

, S

ou

th

Ch

ina

Me

xic

o

Ma

laysia

Sw

ed

en

Ho

ng

Ko

ng

Ta

iwa

n

Isra

el

Sw

itze

rla

nd

De

nm

ark

Ru

ssia

No

rwa

y

Ne

the

rla

nd

s

Italy

Sa

udi A

rab

ia

2007-2011: Top Markets for US Exports of Dried Fruit – US$ '000 & Growth Rate

Yr 2007

Yr 2011

% Growth

© Euromonitor International

34

VOLUME GROWTH LARGELY IN DEVELOPING MARKETS

VOLUME SHIFTING

-40%-20%0%20%40%60%80%100%120%140%160%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Ja

pa

n

Ca

na

da

Ge

rma

ny

United K

ingdom

Ko

rea

, S

ou

th

Au

str

alia

Me

xic

o

Ch

ina

Ma

laysia

Ho

ng

Ko

ng

Sw

ed

en

Ta

iwa

n

Ru

ssia

Sw

itze

rla

nd

Isra

el

De

nm

ark

Sa

udi A

rab

ia

Ne

the

rla

nd

s

No

rwa

y

New

Zeala

nd

2007-2011: Top Markets and Growth Rates for US Dried Fruit Exports by Volume (Metric Tonnes)

Yr 2007

Yr 2011

% Growth

© Euromonitor International

35

About Euromonitor International

Global Market Overview

US Exports & Opportunity Zones

Drivers, Constraints & Trends

© Euromonitor International

36

GROWTH IN DISPOSABLE INCOME PLAYING A ROLE

DEVELOPING MARKETS WITH MORE MONEY

18% 14%

33%

40%

26%

35%

17%

Per capita disposable income of developing markets is greatly below that of developed.

An increase of $823 per capita in disposable income is expected in Asia-Pacific by 2015.

Asia-Pacific’s total disposable expected to eclipse all other regions by 2013.

© Euromonitor International

37

DEVELOPING MARKETS HOLD MAMMOTH POTENTIAL

PER CAPITA CONSUMPTION RELATIVELY LOW IN DEVELOPING MARKETS

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Yr 2006 Yr 2007 Yr 2008 Yr 2009 Yr 2010

2006-10 Regional Per Capita Consumption of Packaged in kg

Western Europe

Australasia

North America

Eastern Europe

Latin America

World

Middle East and Africa

Asia Pacific

© Euromonitor International

38

AP & MEA’S POPULATION TO EXPAND BY OVER 633 MILLION

SIGNIFICANT POPULATION SHIFTS

Population expansion of nearly 350 million is forecasted for Asia-Pacific from 2010-20.

Middle East & Africa is expected to expand by nearly 275 million during the same period.

Eastern Europe is expected to post a loss of nearly 5 million.

© Euromonitor International

39

Asia-Pacific is predicted to add 184 million people to the global population between 2010 and 2015, followed by the Middle East and Africa at 139 million over the same period.

Asia-Pacific’s population growth is predicted to stem entirely from urban areas, while Middle East & Africa’s will be 35% rural growth.

Asia-Pacific’s extraordinary urban population growth should result in strong consumer demand for processed food in the short to medium term.

Greater spending power among middle-income consumers in countries such as China and India will also underpin strong growth in fresh meat consumption and associated foods.

Eastern Europe’s population is projected to fall by 3.3 million, due to emigration and cases of falling life expectancies but will still see value and volume increases.

POPULATION GROWTH UNDERPINS DEMAND FOR COMMODITIES

URBANIZATION TO FURTHER SUPPORT CONSUMPTION

© Euromonitor International

40

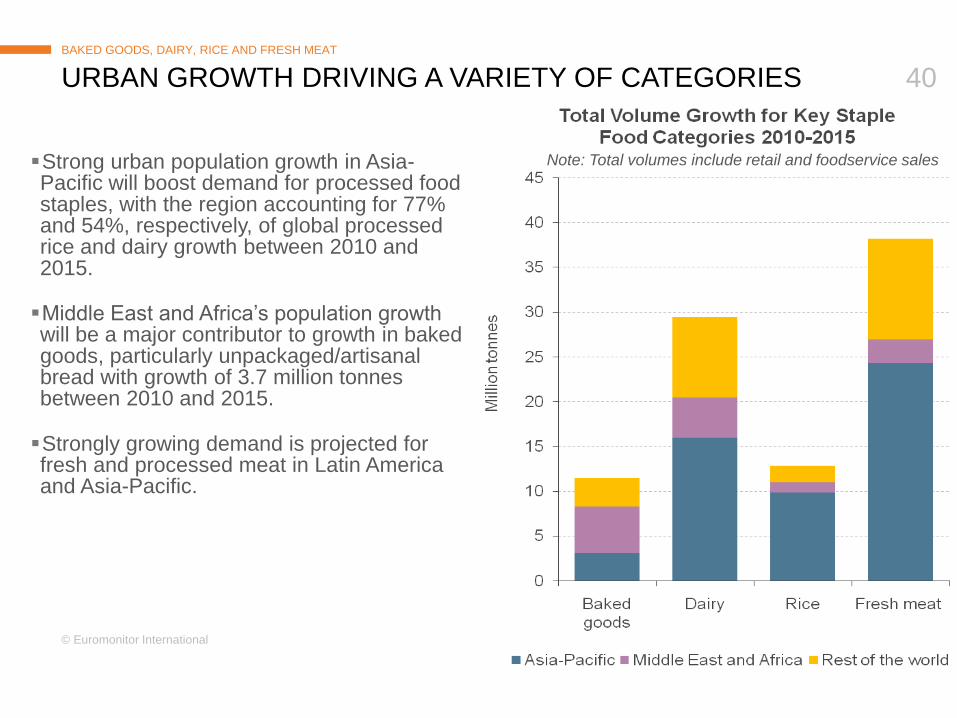

Strong urban population growth in Asia-Pacific will boost demand for processed food staples, with the region accounting for 77% and 54%, respectively, of global processed rice and dairy growth between 2010 and 2015.

Middle East and Africa’s population growth will be a major contributor to growth in baked goods, particularly unpackaged/artisanal bread with growth of 3.7 million tonnes between 2010 and 2015.

Strongly growing demand is projected for fresh and processed meat in Latin America and Asia-Pacific.

Note: Total volumes include retail and foodservice sales

BAKED GOODS, DAIRY, RICE AND FRESH MEAT

URBAN GROWTH URBAN GROWTH DRIVING A VARIETY OF CATEGORIES

© Euromonitor International

41

PACKAGED FOOD PRODUCTS GROWING IN ALL CATEGORIES

INCOMES, HEALTH, CONVENIENCE AND INDULGENCE

Dairy to add over $85 billion in growth through 2015.

Bakery, confectionery, chilled/dried/ and frozen processed foods to see growth ranging from 3-5% in value terms.

Growth is being led by increased desire for staple food products, food safety, indulgence, convenience.

© Euromonitor International

42

Industry prediction:

Exceptionally slow

economic recovery

European markets are now facing significant public spending cuts and the USA

continues to struggle with 8-9% unemployment.

Industry response:

Emerging markets and

‘hot’ growth prospects

To stave off the constraining effects of economic uncertainty in increasingly mature

developed packaged food markets, aggressive and sustained expansion into

emerging markets, especially Asia-Pacific, will be essential to future success.

Industry prediction:

Commodity prices

Commodity prices face volatility, which will put pressure on manufacturers and the

broader supply chain. However, a repeat of the rapid food price inflation seen from

mid-2007 to mid-2008 remains unlikely.

Industry response:

Managing volatile

commodity prices

Nevertheless, manufacturers that anticipate any increases to commodity costs will be

in a stronger position, especially as cost savings and effective supply chain

management become more important in the face of mounting retailer consolidation.

Industry prediction:

Innovation

Packaged food manufacturers will increase investment in new product developments

in light of better economic prospects, particularly in fast-growing regions such as

Asia-Pacific. Innovation crucial to staving off private label encroachment.

Industry response: Don’t

stop adding value

Manufacturers must become bolder and even more compelling in adding value to

their new product launches, while resisting the temptation to retreat into a single-

minded value-for-money proposition as they try to compete against private label.

Industry prediction:

Private label

Even though economic prospects are gradually improving, there is no guarantee that

consumers, especially those in developed markets, will return en masse to branded

products, especially now that private label has become more adept at adding value.

FINAL CONCLUSIONS

INDUSTRY DRIVERS & CONSTRAINTS CONTINUED

DEALING WITH CHALLENGING FACTORS

© Euromonitor International

43

Convenience remained one of the key consumer drivers in 2010, as consumers sought cost-effective alternatives to eating out.

Value for money, traditionally a prime concern for most consumers, has also become more important given lingering economic uncertainty. Still, premium products benefitted from a decline in foodservice expenditure.

Health considerations remain another key factor -- the use of “all natural” ingredients is expanding to emerging regions such as Eastern Europe and is underpinned by the growing number of middle-class consumers developing preferences close to those

that are already firmly established in mature economies. That said, health alone is not enough to increase consumer demand for established brands. Manufacturers are thus opting to advertise new offerings as meals offering both health and indulgence.

From a strategic point of view, food manufacturers are focusing their efforts on growth niches, especially in emerging economies. This trend is particularly relevant to Asia-Pacific and Latin America, where some chilled processed lines and other packaged food categories are being introduced for the very first time.

Convenience

Price / Value for Money

Health

Indulgence

KEY TRENDS AND DEVELOPMENTS

CONSUMERS DRIVERS

© Euromonitor International

44

THANK YOU FOR YOUR ATTENTION.

Matt Tripodi Government & Trade Relations Manager Phone: +1 312-922-1115 x 8205 [email protected]