outlook for airline markets and industry performance - · pdf file ·...

TRANSCRIPT

Outlook for airline

markets and industry

performance

June 2016

Brian Pearce

Chief Economist

International Air Transport Association

The already weak economic cycle is slowing

www.iata.org/economics 2 Source: Netherlands CPB, Markit

30

35

40

45

50

55

60

65

70

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Co

nfi

den

ce in

dex

. 5

0 =

no

ch

ange

% c

han

ge o

ver

pre

vio

us

year

Global economic cycle indicators

International trade growth

Industrial production growth

Business confidence

Now both developed and emerging economies weaker

www.iata.org/economics 3 Source: IATA Economics using Markit data

35

40

45

50

55

60

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

PM

I, 5

0 =

no

ch

ange

Business confidence

Developed economies

Emerging economies

Globalization is still paused

www.iata.org/economics 4 Sources: IATA, Netherlands CPB, OECD-WTO TiVA database

30

32

34

36

38

40

42

44

46

48

50

52

50

60

70

80

90

100

110

120

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Index (Oct 2008=100)

World trade/IP ratio vs. measure of global supply chainsShare (%)

World trade/IP ratio

Ratio of foreign value added to domestic value added in world gross exports

International trade growth has slowed to a stop

www.iata.org/economics 5 Source: IATA using Netherlands CPB data

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Ch

ange

ove

r p

revi

ou

s ye

ar

Contributions to growth in international trade volumes

Emerging economies contribution

Advanced economies contribution

So cargo is weak…but air travel is still booming

Source: ICAO, IATA

Passenger RPKs

www.iata.org/economics 5

2,000

3,000

4,000

5,000

6,000

7,000

80

130

180

230

280

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

RP

Ks

bill

ion

FTK

s b

illio

n

Air travel and cargo volumes

Cargo FTKs

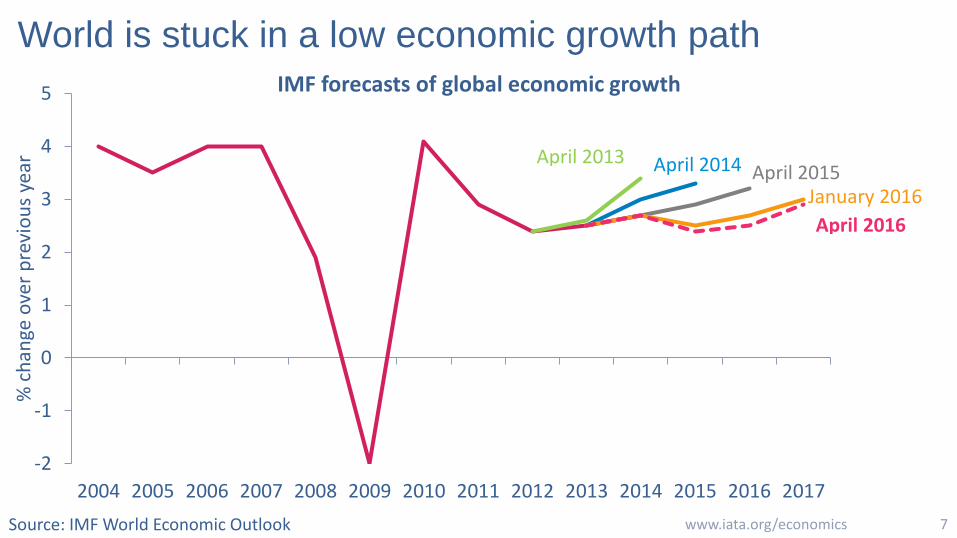

World is stuck in a low economic growth path

www.iata.org/economics 7 Source: IMF World Economic Outlook

-2

-1

0

1

2

3

4

5

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% c

han

ge o

ver

pre

vio

us

year

IMF forecasts of global economic growth

April 2016

January 2016April 2015April 2014April 2013

Yet air travel growth has remained strong

www.iata.org/economics 8 Source: IATA Economic Performance of the Airline Industry

-2

0

2

4

6

8

10

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

% c

han

ge o

ver

pre

vio

us

year

IATA forecasts of global RPK growth

Dec 2012Dec 2013

Dec 2015Dec 2014

Cargo revenues significantly lag passenger business

www.iata.org/economics 9 Source: ICAO, IATA

30

40

50

60

70

80

90

200

250

300

350

400

450

500

550

600

2000 2002 2004 2006 2008 2010 2012 2014 2016

US

$ b

illio

n

US

$ b

illio

n

Revenues from passengers and cargo

Passenger revenue

Cargo revenue

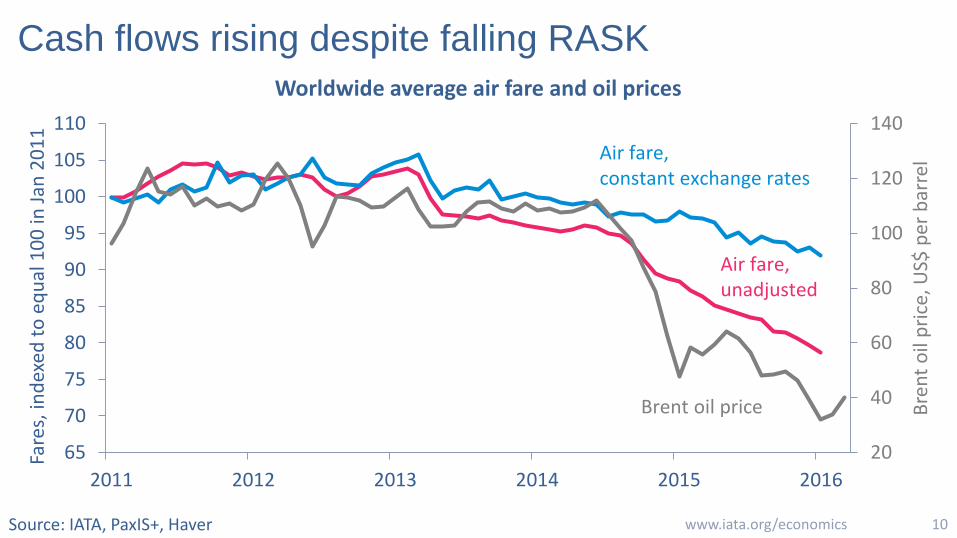

Cash flows rising despite falling RASK

www.iata.org/economics 10 Source: IATA, PaxIS+, Haver

20

40

60

80

100

120

140

65

70

75

80

85

90

95

100

105

110

2011 2012 2013 2014 2015 2016

Bre

nt

oil

pri

ce, U

S$ p

er b

arre

l

Fare

s, in

dex

ed t

o e

qu

al 1

00

in J

an 2

01

1

Worldwide average air fare and oil prices

Air fare, constant exchange rates

Air fare,unadjusted

Brent oil price

Widening asset utilization gap driving returns

www.iata.org/economics 11 Source: ICAO, IATA

58

60

62

64

66

68

2000 2002 2004 2006 2008 2010 2012 2014 2016

% A

TKs

Breakeven and achieved weight load factor

Achieved LF

Breakeven LF

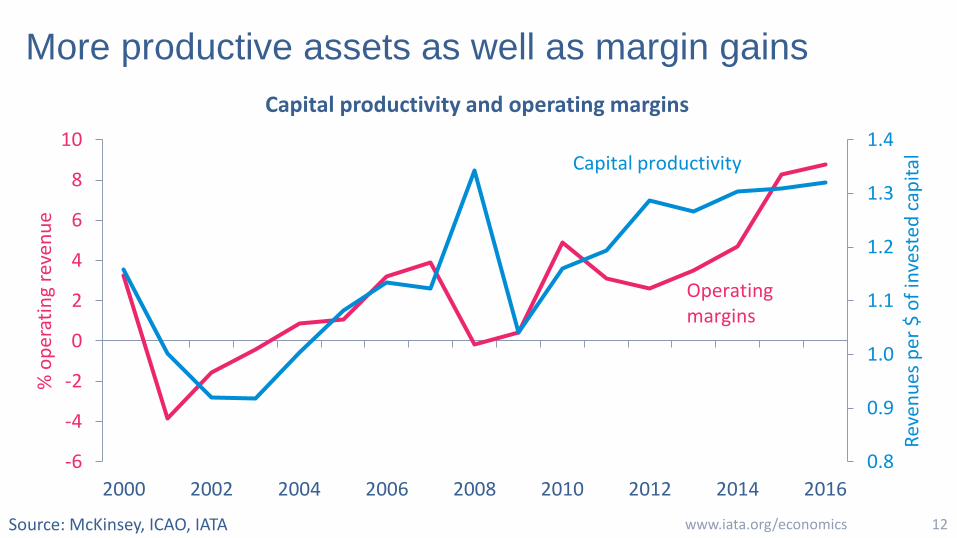

More productive assets as well as margin gains

www.iata.org/economics 12 Source: McKinsey, ICAO, IATA

0.8

0.9

1.0

1.1

1.2

1.3

1.4

-6

-4

-2

0

2

4

6

8

10

2000 2002 2004 2006 2008 2010 2012 2014 2016

Rev

enu

es p

er $

of

inve

sted

cap

ital

% o

per

atin

g re

ven

ue

Capital productivity and operating margins

Operating margins

Capital productivity

Return on airline capital now rising in most regions

www.iata.org/economics 13 Source: IATA calculations from The Airline Analyst

0%

2%

4%

6%

8%

10%

12%

14%

16%

2010 2011 2012 2013 2014 2015

% o

f in

vest

ed c

apit

al

Return on invested capital by region

North America

Europe

Asia Pacific

Latin America

Better performance is spread more widely now

www.iata.org/economics 14 Source: IATA calculations from The Airline Analyst

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

ROIC in 2015 by region and airline

North America Europe Asia PacificMiddle East

Latin America

Africa

Average cost of capital

Balance sheets improved except in L America

www.iata.org/economics 15 Source: IATA calculations from The Airline Analyst

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

2011 2012 2013 2014 2015

Ad

just

ed n

et d

ebt/

EBIT

DA

R

Adjusted net debt/EBITDAR by region

North America

Europe

Asia Pacific

Latin America

We forecast a 2nd year of above WACC returns

Source: McKinsey, IATA 16 www.iata.org/economics

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

% o

f in

vest

ed c

apit

alReturn on capital invested in airlines

Cost of capital (WACC)

Return on capital (ROIC)

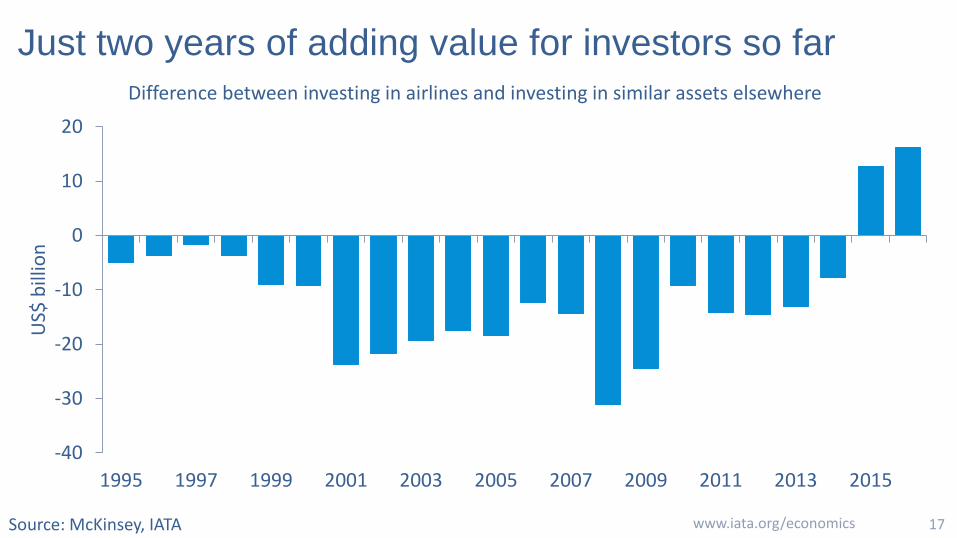

Just two years of adding value for investors so far

www.iata.org/economics 17 Source: McKinsey, IATA

-40

-30

-20

-10

0

10

20

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

US$

bill

ion

Difference between investing in airlines and investing in similar assets elsewhere

Net post-tax profits of $39.4 billion forecast this year

www.iata.org/economics 18 Source: ICAO, IATA

-40

-30

-20

-10

0

10

20

30

40

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

2000 2002 2004 2006 2008 2010 2012 2014 2016

US$

bill

ion

% r

even

ues

Global commercial airline profitability

Net post-tax

EBIT margin

Driven largely by N America, but also Europe & Asia

www.iata.org/economics 19 Source: ICAO, IATA

-10

0

10

20

30

40

50

2010 2011 2012 2013 2014 2015 2016

US$

bill

ion

Net post-tax profit by region

Africa

L America

Middle East

Asia Pacific

Europe

N America

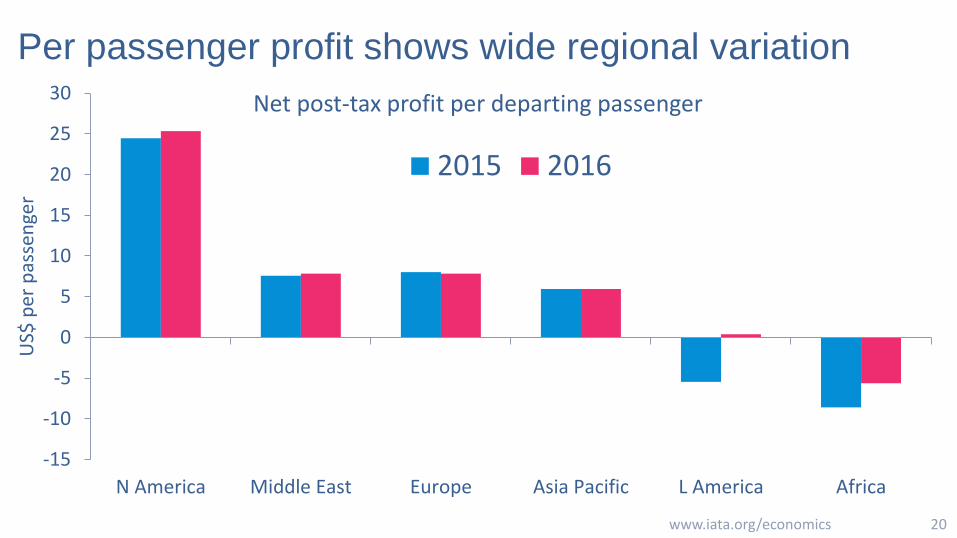

Per passenger profit shows wide regional variation

www.iata.org/economics 20

-15

-10

-5

0

5

10

15

20

25

30

N America Middle East Europe Asia Pacific L America Africa

US$

per

pas

sen

ger

Net post-tax profit per departing passenger

2015 2016

Net profit margins show a rather narrower variation

www.iata.org/economics 21

-10%

-5%

0%

5%

10%

15%

N America Europe Asia Pacific Midle East L America Africa

Net post-tax profit margins

2015 2016