outline - securing the future of philippine...

TRANSCRIPT

OutlineI. Introduction

I. Industry Profile

• Global

• Philippines

III. SWOT

IV. Vision, Mission and Targets

V. Conclusion and Recommendations

Objectives of the Study

• Prepare a sector snap shot to assess the currentlevel of delivery system for healthcare services tonon-Filipino nationals: health and wellness, dentaland medical services, as well the excess capacity ifany, to expand those services to a larger market.

• Based on the assessment, create a roadmap forthe development of the international medicaltravel sector.

Short-Term Expert

Ms. Elizabeth ZiembaPresident, Medical Tourism Training, Inc. (USA)

With funding from EU-TRTA Project 3

International Medical Travel Sector

Five Major Segments

• Tourists

• Medical Tourists

• Medical Travellers

• International Patients

• Accompanying Guests

Service

Coverage

Hospitals

Clinics

Associations, Retirement,

and Ancillary Services

Hotels, Spas and Resorts (Health and

Wellness Services)

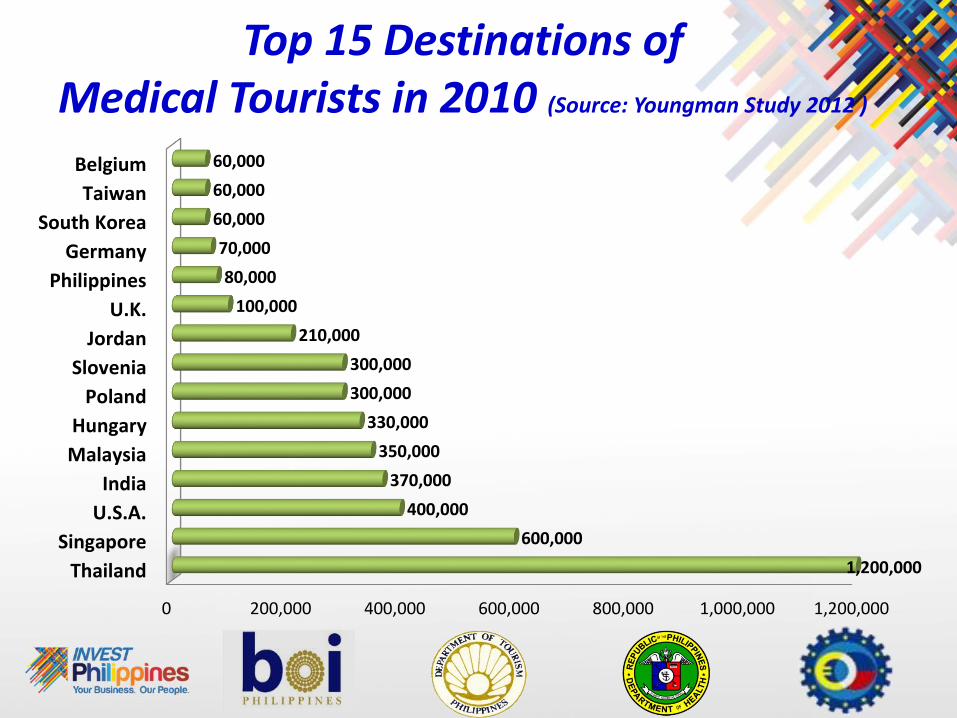

Top 15 Destinations of Medical Tourists in 2010 (Source: Youngman Study 2012 )

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000

Thailand

Singapore

U.S.A.

India

Malaysia

Hungary

Poland

Slovenia

Jordan

U.K.

Philippines

Germany

South Korea

Taiwan

Belgium

1,200,000

600,000

400,000

370,000

350,000

330,000

300,000

300,000

210,000

100,000

80,000

70,000

60,000

60,000

60,000

United States• No. of Tourist Arrivals : 2013 - 69.8 million• Top Markets : Canada, Mexico, UK, Japan

& China• Revenues Generated : 2013 - $140 billion• No. of Medical Travelers/Tourists : 2012 - 800,000

Singapore• No. of Tourist Arrivals : 2013 - 15.5 million• Top Markets : Indonesia, China, Malaysia,

Australia & India• Revenues Generated : 2013 - $23.5 billion• No. of Medical Travelers/Tourists : 2011 - 35,959• No. of JCI-Accredited Hospitals : 11

India• No. of Tourist Arrivals : 2013 - 6.97 million• Top Markets : 1M from US; UK & Bangladesh• Revenues Generated : 2013 - $18.455 billion• No. of Medical Travelers/Tourists : 2012 - 400,000• No. of JCI-Accredited Hospitals : 18

Korea• No. of International Patients : 2012 159,000 people from 189

countries• Revenues Generated : 2012 $ 138 M

2013 $ 187 M (11 months)• 25 international hospitals and 32 JCI - Accredited hospitals and clinics.• Leading Hospital Providers : Yonsei Severance Hospital, Wooridul

Hospital and Incheon St. Mary’s.

Malaysia• No. of JCI-Accredited hospitals : 9• No. of International Patients : 2010 - 392,956

2011 - 583, 2962012 - 671,7272013 - 770, 134

• Revenues Generated : 2010 - $378 M2011 $ 511 M

• Top five Markets (2010-2011) : Indonesia, India, Japan, United Kingdom,and China and Hong Kong

Thailand• No. of JCI-Accredited hospitals : 32• Bumrungrad Hospital - often considered the gold standard for clinical and

patient experience excellence in the international medical travel sector.• Top Markets : Middle East, Cambodia, Laos, Vietnam

Europe

General HospitalsLevel 1 : 1,016(70%)Level 2: 329 (23%)Level 3: 113 (7%)

Government-owned Hospitals: 551 (38%)

Privately-owned Hospitals: 912 (62%)

DOH Licensed

Hospitals: 1,463

Industry Profile – Philippines

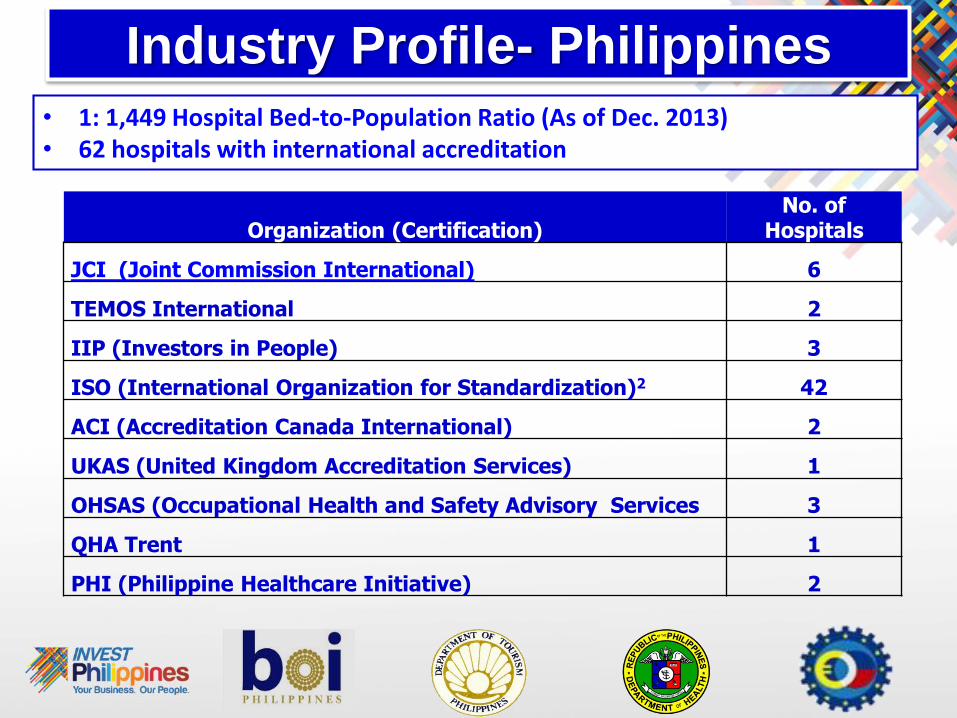

Industry Profile- Philippines • 1: 1,449 Hospital Bed-to-Population Ratio (As of Dec. 2013)• 62 hospitals with international accreditation

Organization (Certification)No. of

Hospitals

JCI (Joint Commission International) 6

TEMOS International 2

IIP (Investors in People) 3

ISO (International Organization for Standardization)2 42

ACI (Accreditation Canada International) 2

UKAS (United Kingdom Accreditation Services) 1

OHSAS (Occupational Health and Safety Advisory Services 3

QHA Trent 1

PHI (Philippine Healthcare Initiative) 2

Industry Profile- Philippines

• The private sector is leading the development of medical travelindustry by offering services that appeal to nationals and non-nationals:o Private hospitals and a handful of public hospitals are

delivering quality medical care, often in accordance withinternational accreditation standards, with well-trainedmedical personnel, state-of-the art medical devices inattractive physical settings;.

o Ambulatory clinics offer a variety of services to medicaltourists that are primarily drawn from the domestic market;

o Hotels, resorts and spas provide a variety of H&W services inaddition to tourist attraction ~~ in all price-points frombudget friendly to high end.

Industry Profile- Philippines

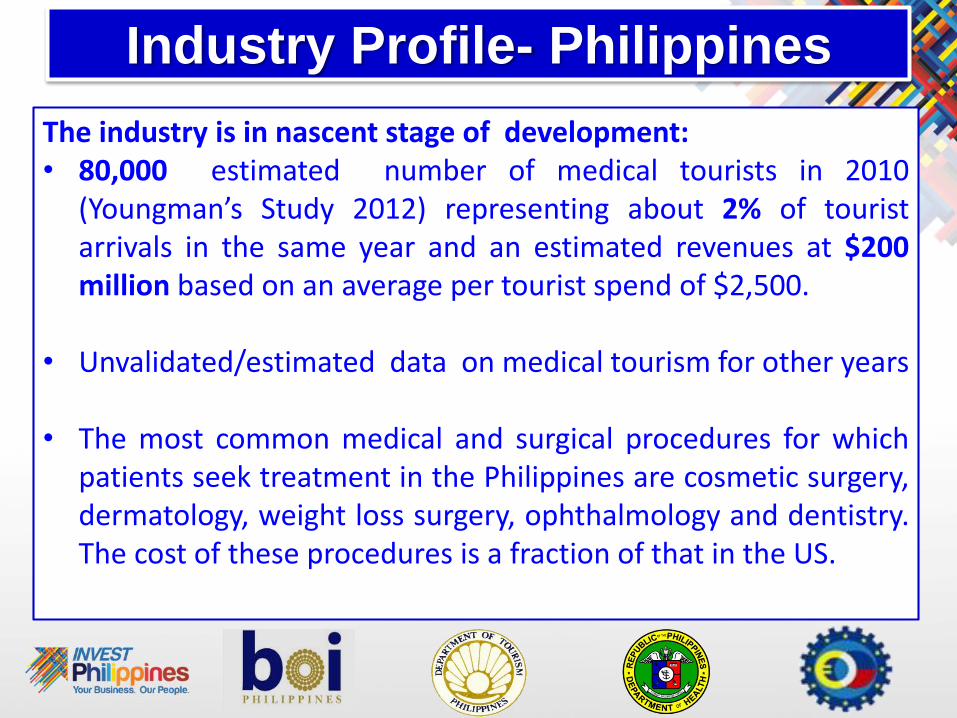

The industry is in nascent stage of development:• 80,000 estimated number of medical tourists in 2010

(Youngman’s Study 2012) representing about 2% of touristarrivals in the same year and an estimated revenues at $200million based on an average per tourist spend of $2,500.

• Unvalidated/estimated data on medical tourism for other years

• The most common medical and surgical procedures for whichpatients seek treatment in the Philippines are cosmetic surgery,dermatology, weight loss surgery, ophthalmology and dentistry.The cost of these procedures is a fraction of that in the US.

Industry Profile- Philippines

Revenues in Medical Tourism in the Philippines

Source: Euromonitor

Source: Euromonitor International Report

Year Revenues in Million US $

2009 66.6

2010 80

2011 96.8

2012 112.2

2013 126.8

2014 144.5

Industry Profile- Philippines

• Small but growing number of healthcare service providers engaging ininternational best business practices that appeal to individuals in everysegment of the international medical travel sectors.

• Hospital’s non-Filipino clients are drawn from:o China, Japan, Korea, Guam, Marianas Islands, and PNGo Small number of overseas Filipinos ( OFWs, 1st & 2nd generation)o Smaller number of Non-Filipinos from the US, Australia, Canada,

Netherlands and Vietnam; patients from North America and Europeare either diasporas or expats residing in the Philippines

Industry Profile- Philippines • Clinicso Treat international clients including Balikbayans while primarily serving the

domestic populationo Offer a range of services attractive to medical touristso Have contracts with local employers to provide variety of services including

ex-pats and international clientso Offer packages that have tie-ups with other businesses including hotelso Indicate strong interest in engaging more actively in the international

tourism market.

• Hotels, Resorts, Spaso Massages, facials , body wraps and related serviceso There are H&W facilities which represent international business

practices that reflect global trends in the H&W sectoro Traditional medicine and alterative medicine are included in the

definition of H&W services in the Philippines

STRENGTHS

• Well-educated, English-speaking, and compassionate healthcareprofessionals

• Hospitable, friendly and approachable citizenry that are able tounderstand and speak English fluently

• Growing number of healthcare providers with international bestbusiness practices

• Competitive pricing of healthcare and other services• Large overseas Filipinos including 1st and 2nd generation Filipinos,

returning nationals, and OFWs with strong country ties.• Access to numerous markets within a 3-5 hour flight time with

reasonable flight costs• Dollar exchange rate: extending the value of their money locally

SWOT Analysis

SWOT Analysis

STRENGTHS

• Culturally tolerant society• Tropical climate• Biodiversity• Strong complimentary industries (e.g. call centers and

back office solutions for healthcare services)• Strong social media presence• Robust Health and Human Resource that are willing to

provide quality services to all types of nationalities• Presence of International Patient Centers in JCI Hospitals

providing concierge services for clients• Hospital websites that provide information on services

being offered including costs for Executive Packages andnon-complicated procedures

SWOT Analysis

STRENGTHS

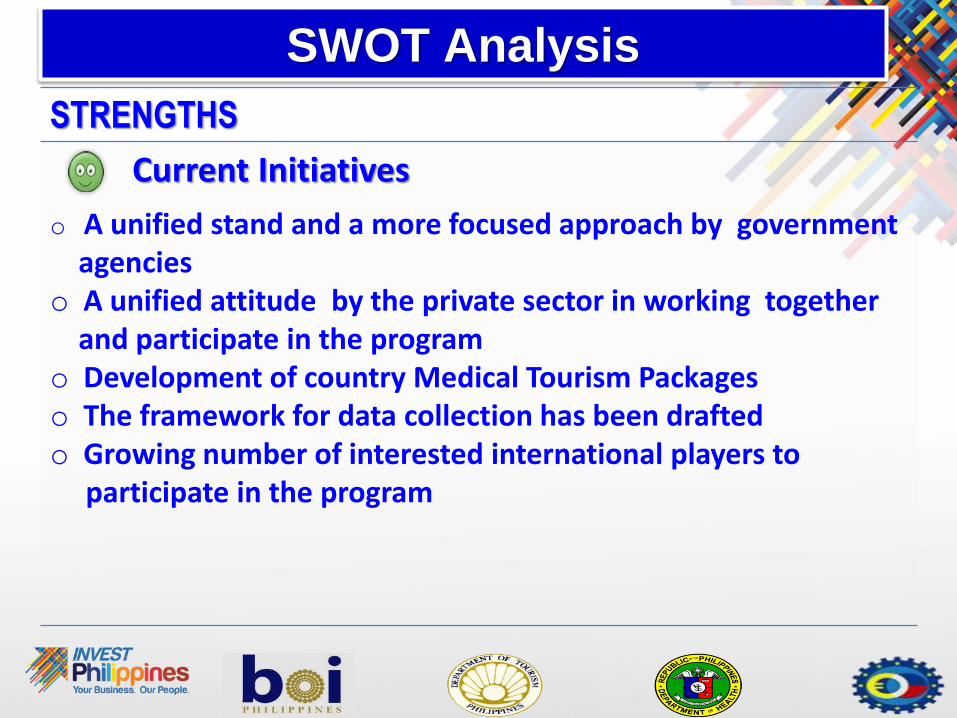

Current Initiatives

o A unified stand and a more focused approach by governmentagencies

o A unified attitude by the private sector in working togetherand participate in the program

o Development of country Medical Tourism Packageso The framework for data collection has been draftedo Growing number of interested international players to

participate in the program

SWOT Analysis

OPPORTUNITIES

• Improving global perception of the Philippines as a traveldestination

• Continued aging of target markets

• Continued high cost of healthcare services in certain markets

• Multi-sectoral cooperation among government agencies

• Strong willingness among private sector entities interested inengaging in international medical travel/tourism development

• Bi-lateral and intra-regional agreements to foster travel fortourism, medical tourist and medical travel.

SWOT Analysis

Weaknesses

Major infrastructure issues (e.g. need for a larger airport, help

desk/dedicated courtesy lane for medical travelers at the airport,traffic mismanagement, taxi drivers’ behaviour , etc.)

Lack of reliable data concerning services provided as part of thesector

Lack of Branding (No “Me Too!”)

Weak synergy between sectors involved in the international medicaltravel industry

SWOT Analysis

Weaknesses

Unpredictability of medical professional fees

Expensive flights to and from countries outside the 3-5 hour flight range

Lack of portability of insurance plans from several key potential markets

SWOT Analysis

Threats

• Strong global competition from current & emergingdestinations

• Uncertain climate for prosecution of medical malpracticecases that may discourage international travelers

• Challenges of pre- and post-operative care/discontinuity ofcare

• Perceived/actual challenges to social equity in delivery ofhealthcare services

SWOT Analysis

Threats

• Changing political objectives that redirect/undermineproject objectives

• International political wrangles and disputes that disruptrelations affecting tourism numbers

• Brain Drain- medical personnel seeking employmentoutside the Philippines

VISION, MISSION & TARGETS

• Being a clinical, policy, research, and opinion leader in theinternational medical travel sector.

• To foster economic development across the international medicaltravel sector to increase access to quality health and wellness,dental and medical services, both domestic and international.

• Short-term Target (By 2016): 2% of the 10 million tourist arrivals

• Medium-term Target (By 2022): 4% of the year’s total number of tourists

• Long-term Target (By 2026): 6% of the year’s total number of tourists

VISION

MISSION

TARGETS

PROPOSED TOP THREE MARKETS

The overseas Filipinos including Balikbayans andindividuals of Filipino descent.

Current markets ofa. Chinese, Japanese, and Korean;b. Guam, Micronesia, Papua New Guinea and other current

markets from the immediate geographic location.

Other markets that are under-represented in currenttourist/medical tourists/medical travelers numbers and thatfall within the 3-5 hour flight time radius.

Conclusion

The conclusion of this study is that intermediate stepsneed to be accomplished to support the currentefforts underway and to prepare for the future.

The Philippines needs to address certain weakness inthe current infrastructure systems before launching afull-scale initiative to enter the international medicaltravel sector.

Conclusion

The top recommendations are essential intermediate stepstowards building the medical travel infrastructure whilesupporting the growth of tourism:

(1) create a leadership council, and(2) improve data collection(3) develop brand strategy.

Once these three recommendations have been addressed aswell as any others that the Council chooses to implement, areassessment can be conducted (within 12-24 months) toprovide further guidance in launching a more comprehensivecampaign for the country.

Leadership Council

• A team led by the private sector withsupport from government to guide thesector;

• Provides accountability for theimplementation of the intermediate stepsand lay the foundation for future growth.

Data Collection

Improved data collection gives an accurate pictureof what is actually occurring in the country interms of individuals accessing medical, dental,wellness, etc. services. With more accurateinformation, fact-based decisions can be made asto what services can and should be offered to the

global market.

Country Brand Strategy

• Developing and implementing a brandstrategy will further identify the strengthsand weakness in the infrastructure neededto grow tourism industry and internationalmedical travel sector.

• The Philippines ranks 95 of 118 countries inthe Country Brand Index. Its weak brandequity is a disadvantage which needs to beovercome to be competitive.

ACTION PLAN/ACTIVITY

TWG / Convenors Meeting about Proposed Council and Membership

Review Vision and Mission

Statements Review of Targets Prioritize Action Points

#1 LEADERSHIP

ACTION PLAN / ACTIVITY

Conduct Intercept and/or Email Surveys

Establish a Uniform Data CollectionSystem

Provide Incentives to

Encourage Compliance

#2 DATA COLLECTION

ACTION PLAN/ACTIVITY

Creation of Brand Identity and Strategy tobe led by the Department of Tourism.

- Hire a Short Term Expert for Branding

#3 BRANDING

Other Recommendations

• Regulatory Issues

• Insurance Payments

• Workforce Development

• Sector Development through linkages with Institutions of Higher Learning

• Access

• Social Equity

• Public Relations

• Malpractice

• Natural Disasters

1st Medical Travel and Wellness Tourism

Convenors Meeting

• Small Group Clusters formed to implement the major recommendations identified in the roadmap:o Leadership Council Cluster o Data Collection Cluster o Market Development/Promotion and

International Patient Pathway Cluster o Branding Strategy Cluster

• Hospital MTWT Reporting Form - for finalization andpilot testing

• New Immigration Arrival and Departure Cards mayinclude among the purposes of travel : MedicalTourism

• Random Exit Surveys of foreign passengers at theairports.

• Review data fields of PSA’s Survey of TourismEstablishment in the Philippines (STEP) and TourismSatellite Accounts where MTWT data may possibly beextracted.

Data Collection Cluster Initiatives

• 7th World Medical Tourism and Global Healthcare Congress, 2014, USA

• Top Medical Product/Services Promoted with Country Packageso Executive check-upo Cardiologyo Orthopaedics o Aesthetics/cosmetic (including dental services)

o Ophthalmology

Market Development / Promotion

Cluster Initiatives

• International Medical Travel Exhibition and

Conference (IMTEC) in Dubai in October 7-8,

2015

• 8th World Medical Travel and Healthcare

Congress on September 27-30, 2015 in Orlando,

Florida

• Phil. Medical Tourism Mega FamTour and

Medical Travel Exchange (December 6-11, 2015)

Market Development / Promotion

Cluster Initiatives

Thank You

STRATEGY ACTION PLAN/ACTIVITY

Regulatory Issues

Review of rules and regulations issued byregulatory authorities

Consultation with representatives

Insurance and Payment Issues

Workshop with providers, administratorsinvolved with processing insurance claims,insurance companies, HMOs, and otherrelevant parties.

Public-Private Partnership between healthservice providers that offer back office solutions

Workforce Development

Improving Language SkillsCurriculum for Clinical Skills for Geriatric Care

STRATEGY ACTION PLAN/ACTIVITY

Sector Development thru linkages with Institutions of Higher Learning

Involve colleges and universities in developing the sector - Courses, degree programs, topics in subjects

pertaining to the international medical travel sector.- Engage in research

Involve medical professionals in developing the sector- Engage in medical research including clinical trials.- Publish in peer review journals- Attend medical conferences- Visit and invite colleagues in the same discipline

Access

Establishing a “Medical Travel Help Desk”Superior customer service of airport, customs and

immigration, airline, and other personnelProper training to address issues relating to medical

travelers

STRATEGY ACTION PLAN/ACTIVITY

Social Equity The DOH to develop a policy statement thatreflects the official position of the governmentconcerning this issue.

Public Relations

The DOH to provide announcement of activitiesassociated with the data collection and reportingsystem.

The DOT to regularly promote its activitiesincluding the social media campaign of “More funin the Philippines”.

STRATEGY ACTION PLAN/ACTIVITY

MalpracticeBoth DOT and DOH to establish a

calendar of regular communications toprovide updates, share information, andto inform the public and privatestakeholders about continuing efforts tosupport the sector.Establishment of an Ombudsman for

Medical Tourism

Natural Disasters

Elements of emergency disaster planinclude:

put patient safety first; defined emergency plans; and clear instructions on evacuation or

other steps to be taken in order toremain safe

Major ProductsMajor Surgeries • Orthopedic surgeries: hip replacement, hip resurfacing, knee

replacement•Spinal procedures: spinal fusion, spinal disc replacement•Limited cardiac procedures: angioplasty, cardiac diagnostic procedures•Gynecological surgeries: partial, total, or radical hysterectomies •Hysterectomy, bilateral salpingo oophorectomy•General surgeries: vascular, stomach and bowel, kidney and urinary, gallbladder removal, hernia repair, cataract surgery, Lasik surgery, hemorrhoid removal, Endo-laser vein surgery•Other medical procedures: bariatric surgery, fertility treatment, oncology, transplants, stem cell treatments, sex reassignment, addiction treatments

Minor Surgeries •Dental procedures: dental work, cosmetic dentistry, crowns, bonding, veneers, whitening, bridges, bone grafts, root canals, tooth extractions•Eye, ear, nose and throat treatments

Cosmetic/plastic surgeries

• Facial cosmetic surgery: rhytidectomy, eyelid surgery, nose reshaping, brow or forehead lift, ear surgery•Body contouring: liposuction including tummy tuck, breast augmentation, breast life, thigh lift, lower-body

Major Products

Diagnostic Services • Annual Checkups

Alternative TherapyTreatments

• Chinese medicine, acupuncture, herbal treatments, ayurvedictreatments•Pancha Karma, tai-chi

Wellbeing/lifestyleremodelling services

• Spa therapy, yoga therapy, meditation therapy, holistic therapy, thermal therapy (mineral springs, balneo therapy), thermo therapy, thalasso therapy•Algae therapy, aroma therapy, cryotherapy, electrotherapy, magnetotherapy, mud healing (fango therapy), occupational therapy (stress management), massage, diet and nutritional programs, detoxification, New Age, spiritual tourism