outline - iabciabc.or.id/download/conference/hermantodardak.pdf · papua ng sumber ... mp3ei...

TRANSCRIPT

MINISTRY OF PUBLIC WORKS

Well Connected and Reliable Infrastructure to Support Economic Development

PRESENTATION OF VICE MINISTER OF PUBLIC WORKSREPUBLIC OF INDONESIA

Indonesia Australia Business Council (IABC)Bali, November 2013

Outline• Introduction on APEC

• APEC 2013 and Bogor Goals

• Indonesia – Australia connection

• Countries Outlook

• Indonesia current condition

• Road Infrastructure Development Plan

• Infrastructure Investment Requirement

• Innovative delivery in toll road development

• New models for government co‐funding in Infrastructure Development

• Conclusion

Introduction on APECAPEC’s economic trade and highlights

14.8

46.6

0

10

20

30

40

50

1992 2012

GDP (PPP)Percentage of the world’s GDP (PPP)

6.0%

5.6%

5.8%

5.0%

5.5%

6.0%

6.5%

APEC Non‐APECCountries

World

GDP (PPP) average growth

0.9%

1.3%

0.0%

0.5%

1.0%

1.5%

APEC World

Population growth per annum

67514008 5113

16760

8624

11847

0

5000

10000

15000

20000

25000

APEC Non‐APECCountries

World

20121992

GDP (PPP) per capita

APEC’s GDP in Purchasing Power Parity (PPP)terms has increased almost 3x from 1992 to 2012

APEC accounted for 39.6% of world population in 2012

APEC was established in 1989 to furtherenhance economic growth andprosperity for the region and tostrengthen the Asia‐Pacific community.

Since its inception, APEC has worked toreduce tariffs and other trade barriersacross the Asia‐Pacific region by creatingefficient domestic economies anddramatically increasing exports.

APEC also works to create an environmentfor the safe and efficient movement ofgoods, services and people acrossborders in the region through policyalignment and economic and technicalcooperation.

*) Values in international dollars. Source: IMFWEO, April 2013.

53.20%

56%

50%

55%

60%

1992 2012

Resilient Asia‐Pacific, Engine of Global Growth

Attaining the Bogor Goals

Regional Economic Integration: Reducing barriers to trade and

investment

Revisiting Bogor Declaration: Promoting the free flow of goods, services and capital

among economies

Structural Reform,

Trade Facilitation,

Long Term Planning

Sustainable Growth with Equity

Reducing vulnerability through economic empowerment

Unlocking Economic potentials

Promoting Connectivity

Connecting the region

Strengthening Network for Development

ECONOMIC AND TECHNICAL COOPERATION

SMEs Competitiveness

Food Security

Financial Inclusion

Health

Physical

Institutional

People‐to‐people

The efforts to attain the Bogor Goals willbe done through continued efforts tocreate deeper regional economicintegration.

Allignment of efforts will be focused oneconomic empowerment, engagement ofstakeholders and utilization of untappedpotential.

Concrete efforts to linking growth centersand developing new growth centers in theregion to increase output andproductivity.

2013 APEC Priorities

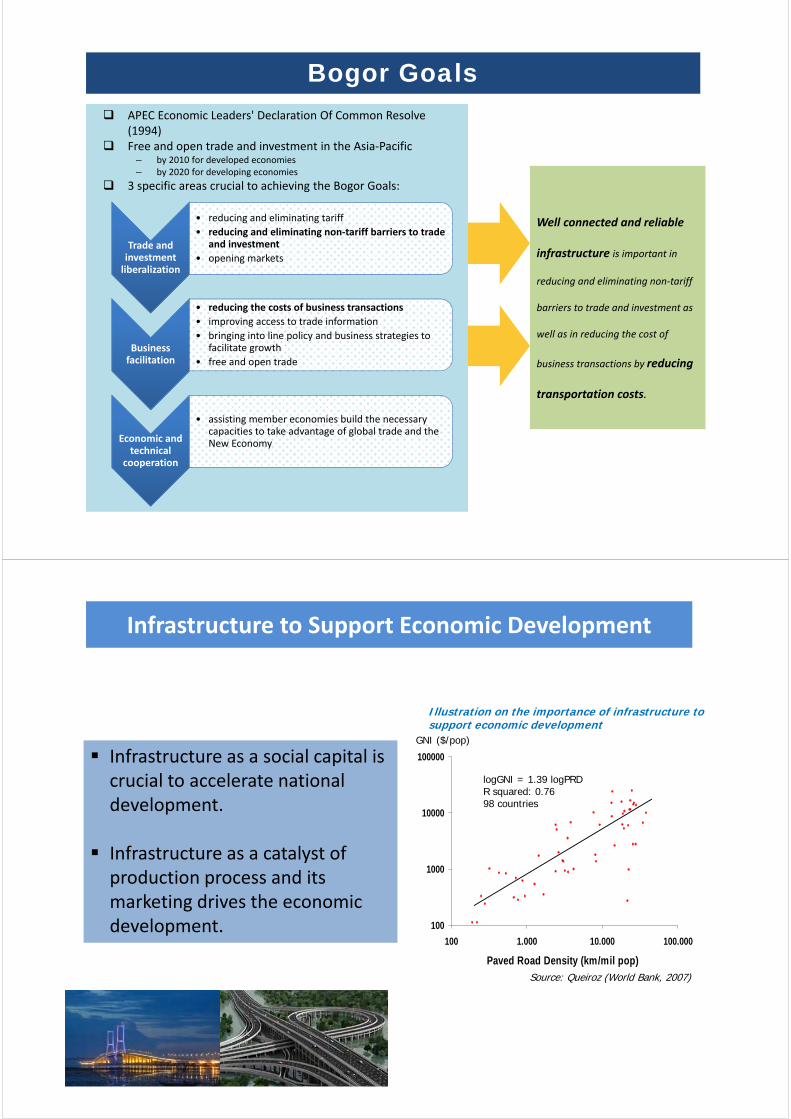

Trade and Trade and investment liberalization

• reducing and eliminating tariff

• reducing and eliminating non‐tariff barriers to trade and investment

• opening markets

Business facilitation

• reducing the costs of business transactions

• improving access to trade information

• bringing into line policy and business strategies to facilitate growth

• free and open trade

Economic and Economic and technical

cooperation

• assisting member economies build the necessary capacities to take advantage of global trade and the New Economy

APEC Economic Leaders' Declaration Of Common Resolve (1994)Free and open trade and investment in the Asia‐Pacific

– by 2010 for developed economies– by 2020 for developing economies

3 specific areas crucial to achieving the Bogor Goals:

Bogor Goals

Well connected and reliable

infrastructure is important in

reducing and eliminating non‐tariff

barriers to trade and investment as

well as in reducing the cost of

business transactions by reducing

transportation costs.

100

1000

10000

100000

100 1.000 10.000 100.000

Paved Road Density (km/mil pop)

GNI ($/pop)

Source: Queiroz (World Bank, 2007)

logGNI = 1.39 logPRDR squared: 0.7698 countries

Infrastructure as a social capital is crucial to accelerate national development.

Infrastructure as a catalyst of production process and its marketing drives the economic development.

Illustration on the importance of infrastructure to support economic development

Infrastructure to Support Economic Development

The Australian and Indonesian economies are the largest in the region.

Significantly, both contries recorded growth in the post‐(2008‐09) Global Financial Crisis period.

Indonesia is one of Australia’s most important bilateral relationships on almost all fronts.

Indonesia – Australia Connection

Indicator Indonesia Australia

GDP(USD Mill.)

846,832 1,379,382

GDP per Capita(USD Mill.)

3,495 61,790

Population 242,325,600 22,323,900

Area (km2) 1,904,569 7,692,024

Density (person/km2) 127 3

Source: values in 2011 (statistics.apec.org; 2013)

Countries Outlook

Indonesia’s economic makes up 47% of ASEAN economy, 46% of population, and half of the landmass

Challenge in Connectivity

Connectivity across main corridors is low compared to other countries

0.00 1.00 2.00 3.00

Trip time (hr/100 km)

Vietnam

Indonesia

China

Thailand

Malaysia

High land transport costs – low connectivity of economic centres

Demand growing 8‐10% pa to support growth

Key centres congested, large areas under‐developed

0 0.2 0.4 0.6 0.8

Malaysia

China

Philippines

Thailand

Indonesia

Vietnam

Expressway Density (km/1000 population)

Backlog in Expressway Development

Indonesia

Indonesia

0 1 2 3 4 5 6 7

Developing Asia

ASEAN

Indonesia

China

Thailand

Malaysia

Singapore

Brunei Darussalam

Cambodia

Philippines

Indonesia

Low Competitiveness in InfrastructureQuality of Roads Score (GCI 2013‐2014)

Indonesia

2013‐2014: rank 38

2012‐2013: rank 50

Singapore

2013‐2014: rank 2

2012‐2013: rank 2

Competitiveness ranking (GCI)

Malaysia

2013‐2014: rank 24

2012‐2013: rank 25

Thailand

2013‐2014: rank 37

2012‐2013: rank 38

3.0

3.5

4.0

4.5

5.0

5.5

6.0Institutions

Infrastructure

Macroeconomic

environment

Health andprimaryeducation

Highereducationand training

Goodsmarketefficiency

Labor marketefficiency

Financialmarket

development

Technological readiness

Market size

Businesssophisticatio

n

Innovation

Score 2013‐2014 Score 2012‐2013

• Indonesia’s rank according to GCI 2013‐2014 is improved (rank 38) fromlast year (rank 50).

• Infrastructure rank is also improved (rank 61) from last year (rank 78).

• Quality of overall infrastructure is improved (score 4,0) from last year(score 3,4).

• However, quality of roads score is still below quality of overallinfrastructure score as well as overall competitiveness score.

• Road infrastructure in Indonesia needs to be improved in order toincrease competitiveness.

2012‐20132013‐2014

Challenge in Competitiveness

Reliable Infrastructure is Crucial to Improve Competitiveness

Challenge in Logistics Performance

1

8

18

21

26

29

31

38

46

52

53

59101

109

128

Singapore

Japan

Australia

Korea

China

Malaysia

New Zealand

Thailand

India

Philippines

Vietnam

Indonesia

Cambodia

Laos

Papua NG

Sumber: Logistic Performance Index (The World Bank)

Road infrastructure holds an important role to ensure logistics servicesdelivery.Reliable road infrastructure reduces transportation costs.Road infrastructure development is one of the indicators of logisticsperfomance index and global competitiveness.

The World Bank’s Logistics Performance index (LPi) analyzes countries in six components:1. The efficiency of customs and border management

clearance.2. The quality of trade and transport infrastructure.3. The ease of arranging competitively priced

shipments.4. The competence and quality of logistics services.5. The ability to track and trace consignments.6. The frequency with which shipments reach

consignees within scheduled or expected delivery times.

0

1

2

3

4LPI Score

Customs

Infrastructure

ShipmentsCompetence

Tracking

Timeless

LPI 2012 RANKING

National Connectivity

zzzz

Production center and natural resources processing and national energy resources

Production center and mining product processing

and national energy resources

National production center and agriculture, fishery,

plantation, oil, gas and mining products processing

National industrial and services support National tourism gate and

national consumable goods support

National energy, consumable goods, fishery and mining development

STATUS

GROUND BREAKINGUP TO JULY 2013

TOTAL

Investment Cost : USD 64.746 Bill

No. of Project : 240 Projects

SECTOR

Investment Cost : USD 36.446 Bill

No. of Project : 94 Projects

INFRASTRUCTURE

Investment Cost : USD 28.300 Bill

No. of Project : 146 Projects

VALIDATION RESULTUP TO JULY 2013

TOTAL

Investment Cost : USD 448,100 Bill

No. of Project : 1,568 Projects

SECTOR

Investment Cost : USD 217,700 Bill

No. of Project : 583 Projects

INFRASTRUCTURE

Investment Cost : USD 230,400 Bill

No. of Project : 985 Projects

MP3EI LAUNCHING27 MAY 2011

TOTAL

Investment Cost : USD 401,200 Bill

No. of Project : 1,264 Projects

SECTOR

Investment Cost : USD 222,600 Bill

No. of Project : 639 Projects

INFRASTRUCTURE

Investment Cost : USD 178,600 Bill

No. of Project : 625 Projects

VALIDATION

Validation result exclude Human Resources Investment in Science and Technology with total amount of USD 2,170 Mill.

PROGRESS OF MP3EI

Ferry AH-2 to AH-25 Sumatera to Java Island

= 14 mile, served by max of 24 Ro-Ro Ferrys

(±3.5 trip time)

Ferry to/from Singapore (Efficiency and

CompetitivesnessProposed to be studied)

AH Route

Width (KM)

< 6 M6 – 7 M

7 – 14 M

>14 M Total

AH‐2 16 573 676 420 1685

AH‐25 512 1836 318 98 2764

AH‐150 2779 342 291 52 3464

AH Route

Condition (%)

Good Fair Bad

AH‐2 58 38 4

AH‐25 61 35 4

AH‐150 78 17 5

Progress per December 2012

Current Progress on ASEAN Highways Network

Route ItineraryLength

(km)Transit Route

Sumatera Island

AH-25 Banda Aceh-Medan-Dumai-Pekanbaru-Jambi-Palembang-Bakauheni.Ferry:Bakauheni-Merak

2,746.57 non-toll roadwith 42.7 toll road as

alternative route

Y

AH-151 Tebing Tinggi-Pematang siantar-Bukit Tinggi-Padang-Muara Bango-Sarolangun-Lubuk Linggau-Lahat-BatuRaja-Bandar Lampung

1,968.42 N

Java Island

AH-2 Merak – Jakarta – Semarang – Surakarta – Surabaya – Ketapang, Cikampek – Bandung.Ferry:Ketapang-Gilimanuk

1,525.862 non-toll roadWith 541,16 toll road as

alternative route

Y

AH-152 Jakarta – Sukabumi – Bandung – Cilacap –Yogyakarta - Kertosono

833.766 N

Bali Island

AH-2 Gilimanuk - Tabanan – Denpasar – Tuban 159.334 Y

Kalimantan Island

AH-150 Pontianak-Pangkalanbun-Palangkaraya-Banjarmasin-Balikpapan-Samarinda-Bontang-Tanjung Selor-Malinau-Simanggaris

3,390.742 N

ASEAN and Asian Highways Routes

16

Bandung

Jawa Barat

JakartaSerang

Surabaya

Yogyakarta

Semarang

DKI

Banten

DIY

Jawa Tengah

Jawa Timur

Kertosono

Mojokerto

Pejagan Pemalang

Batang

Cikampek

Palimanan

Solo

Ngawi

Pasuruan

Probolinggo

Banyuwangi

Kanci

SukabumiCiranjang Demak

Malang

Pandaan

Gempol

Bogor

288 KM 177,12 KM 76,77 KM

(K)

TRANS JAVA TOLL ROAD

73 KM

1

243

6

57

8

9Legend:: Operated: Land Acquisition and Construction: Preparation

Total investment cost : USD 5,141 Mill.Total land acquisition cost : USD 509 Mill.Total length : 615 Km

Section Number

Toll Road Cikampek – Palimanan Pejagan -Pemalang

Pemalang -Batang

Batang -Semarang

Semarang - Solo Solo - Ngawi Ngawi - Kertosono Kertosono -Mojokerto

Mojokerto -Surabaya

Toll Road Company PT.Lintas Marga Sedaya

PT. Pejagan Pemalang Toll

Road

PT. Pemalang Batang Toll

Road

PT. Marga Setia Puritama

PT. Trans Marga Jateng

PT. Solo Ngawi Jaya PT. Ngawi Kertosono Jaya

PT. Marga Harjaya

Infrastruktur

PT. Marga Nujyasumo

Agung

Length (km)/No. of Section 116/6 58/4 39/2 75/5 73/5 90/4 87/4 41/4 36/5

Investment Cost (USD Mill.) 1,260 552 408 723 621 514 383 348 340

Land Acquisition Cost (USD Mill)

55 25.4 18 58.4 92.7 99.5 86.4 29.7 46.1

Target Operation 2014 2014 2014 2015 2014 2014 2014 2014 2014

Concession period (year) 35 45 45 45 45 35 35 35 42

Progress

Land Acq. *) 100,00% 28,72% 1,86% 3,33% 38,95% 82,67% 51,27% 87,00% 64,71%

Construction 2,90% - - - 30,18%Total GOI TRC Total GOI TRC

38,55% 31,06% 11,98% 48% -. - - -

1 2 3 4 5 6 7 8 9

*) Status: 23 August 2013*) Assumption: 1 USD = Rp. 10,000

Trans Java Toll Road

Bakaheuni ‐ Indralaya

Indralaya ‐ Pekanbaru

Pekanbaru ‐Medan

Medan ‐ Aceh

PKN

HGH Sumatera consists of:Bakauheni‐ Banda Aceh corridor (Eastern Corridor, total length of ±2.017 Km)Feeder, total length of +720 Km

Connecting 8 cities (National Activity Center/PKN), 8 airports, 6 international portsConnected to Sunda Strait Bridge and Trans Java Toll RoadPart of ASEAN/ASIAN HighwaysOperation of Trans Sumatera Toll Road will reduce traffic load and road maintenance costs

High Grade Highway Sumatera

Sunda Strait Infrastructure and Strategic Region Development

Sunda Strait Infrastructure and Strategic Region Development

Sunda Strait Bridge Construction

No Bridge Components Unit Quantity

1 Steel Pilon ton 139,800

2 Main Cable ton 176,864

3 Hanger ton 8,810

4 Steel Box Girder ton 145,920

5 Structural Part of Caison for Pilon m3

1,925,316

6 Lean Concrete of Caison for Pilon m3

1,005,092

7 Anchor Block m3

462,488

8 Structural Part of Caison for Anchor Block m3

1,274,597

9 Lean Concrete of Caison for Anchor Block m3

951,003

10 Pavement, darinage, etc m2

430,160

11 SHMS unit 2

1 Concrete Box Girder m3

1,033,560

2 Concrete Deck m3

43,656

3 Pier m3

219,959

4 Capping Beam m3

187,715

5 Pile Cap m3

588,861

6 Bored Pile dia. 2.4 m m' 248,977

7 Pavement, darinage, etc m2

1,001,520

JEMBATAN GANTUNG ULTRA PANJANG

VIADUCT

Total Steel Requirement = ± 472,000 tonTotal Concrete Requirement = ± 7.7 mill. m3

Integrated Coastal Infrastructure

NCICD is one of the efforts to cope with flooding problem in Jakarta as well as to create opportunities for integrated coastal regional development

Integrated Coastal Infrastructure

ELEVATED ROAD AND BRIDGE PRE‐CAST

IMPLEMENTATION ELEVATED ROAD INTERMODA

(Non Toll Fly Over Antasari – Blok M)

BALI MANDARA TOLL ROAD AND DEWARUCI INTERCHANGE (UNDERPASS AND FLYOVER)

Dewaruci Interchange (Underpass and Fly over)

BALI MANDARA TOLL ROAD

Infrastructure Investment Requirement (2010-2014)

(Gap)

Source: Bappenas 2011

Initial Target: ID

R 1,429 Trillion

Investment Requirement and Funding Sources (2010‐2014)

IDR Trillion

Total : ID

R 1.429 Trillion

National BudgetIDR 559.5 Trillion

Local Govt. BudgetIDR 355 Trillion

Private SectorIDR 344.7 Trillion

State Owned CompanyIDR 340.8 Trillion

Total Investment Requirement Estimated Financing Capacity Gap

Infrastructure Investment Gap (2010-2014)

2009 2010 2011 2012 2013 2014Total

2010‐2014

Growth (%)1)

4.6 6.2 6.5 6.2 6.3 6.4

GDP (IDR Trillion)1)

5.606,2 6.436,3 7.427,1 8.179 9.284 10.583 41.909,4

Total Infrastructure Allocation1)

218,65 263,9 314,1 385,2 438,1 469,15 1.870,42

Infrastructure Investment Requirement 5% of GDP (IDR Trillion)

3) 280,3 321,8 371,4 409 464,2 529,2 2.095,64)

Infrastructure Investment Requirement 7% of GDP (IDR Trillion)

2) 392,4 450,5 519,9 572,5 649,9 740,8 2.933,6

Requirement Gap of Infrastructure Investment 5% of GDP (IDR Trillion)

3) 61,65 57,9 57,3 23,8 26,1 60,05 225,18

Requirement Gap of Infrastructure Investment 7% of GDP (IDR Trillion)

3) 173,75 186,6 205,8 187,3 211,8 271,65 1.123,18

Allocation for Ministry of Public Works36,1

16,51%37,7

14,29%56,9

18,12%75,5

19,6%83,2

19,17%84,1

17,93%337,4

18,04%

Remarks:1)Source: National Budget Plan 2014

2) Minimum requirement of 7% based on RPJMN 2010‐2014

3)Analysis Result

4) Analysis in year 2011 = IDR 1,923 Trillion and has been reviewed to IDR 2,095 Trillion

Innovative Delivery in Toll Road Development

Land Acquisition

New InnitiativeCurrent Practice

Financing Facilities

PPP Modality

Procurement

Concession Agreement and Contingent Liability

• Presidential Decree No. 36/2005 as amended with Presidential Decree No. 65/2006

• Financed by TRC (pre financed by BLU)• Implemented by Government

• UU Pengadaan Tanah Bagi Kepentingan Umum No.2/2012

• Dibiayai dan dilaksanakan oleh Pemerintah

• TRC and bank syndication • TRC and bank syndication• SMII/IIF

• BOT • BOT• SBOT• Annuity Based Project• Leasing• Outsourcing

• Mainly solicited• Solicited• Unsolicited

• Standard minimum• No government guarantee

•Better risk allocation•Government guarantee by PT.PII

Government support

• From sector (related Ministry) • Sectoral contribution from related Ministry

• VGF by Ministry of Finance

New Models for Government co‐funding in Infrastructure Development

• Enhanced financial Impact (retain risks, achieve cost efficiency and apply user charges)

• Increased leverage (impact on balance sheet and ability to attract private sector capital)

Model 1: Public sector subordinated notes

Transfer of demand risk to private sector with defined public sector support (subordinate loan) for any funding gapSubordinated loans are repaid after debt service on senior loans but before returns to equity

Model 2:Public sector debt capital

Government co‐lending on equal basis with commercial debt

Model 3:Public sector minimum guarantees

Government support for demand risk until a threshold is metGovernment would provide minimum patronage or revenue guarantees for a defined period

Model 4:Public sector development company (with traditionally

delivered infrastructure)Government through public sector development company would design, finance, and build the asset and maintain and operate it in the initial years Government retains substantially all project risks (until divested)

Model 5:Public sector development company (with availability based

PPP delivered infrastructure)Government retains demand risk (until divested) Payment by the government to the Concessionaire based on the availability of the asset after construction

Model 6:Alternative new funding models

Tax Increment Financing: Use the revenue generated by infrastructure development, specifically an increase in local/state taxes due to increase in property values to repay loan used to fund new infrastructureInfrastructure bonds has focused on leveraging private investment through: i) Create a tax incentive by allowing interest in infrastructure bonds to be tax deductible for issuers but tax exempt for investors and ii) provide some form of credit enhancement through government guarantees

Source: Funding Infrastructure: Time For A New Approach? (pwc.com.au/industry, 2013)

Reliable infrastructure is prerequisite to improveIndonesia’s competitiveness in the global world.

To support Bogor Goals, Ministry of Public Works supportsinfrastructure connectivity as one of crucial aspects inreducing and eliminating non‐tariff barriers to trade andinvestment.

The efforts are among others in form of ASEAN and AsianHighway development, Trans Sumatera Toll Road, TransJava Toll Road and Sunda Strait Bridge Development Plan.

In realizing such programs, the main issues faced today arerelated to the land acquisition process and low feasibility ofthe projects (the need for Government support andguarantee to increase the project’s attractiveness to theprivate sector).

Innovative delivery is needed in infrastructure funding tosupport Public Private Partnership in infrastructureprovision.

Conclusion

THANK YOU

MINISTRY OF PUBLIC WORKS