option pricing models: the black-scholes-merton model aka black – scholes option pricing model...

TRANSCRIPT

Option Pricing Models:The Black-Scholes-Merton Model aka Black – Scholes

Option Pricing Model (BSOPM)

Important Concepts

• The Black-Scholes-Merton option pricing model• The relationship of the model’s inputs to the

option price• How to adjust the model to accommodate

dividends and put options• The concepts of historical and implied volatility• Hedging an option position

The Black-Scholes-Merton Formula

• Brownian motion and the works of Einstein, Bachelier, Wiener, Itô

• Black, Scholes, Merton and the 1997 Nobel Prize• Recall the binomial model and the notion of a

dynamic risk-free hedge in which no arbitrage opportunities are available.

• The binomial model is in discrete time. As you decrease the length of each time step, it converges to continuous time.

Some Assumptions of the Model

• Stock prices behave randomly and evolve according to a lognormal distribution.

• The risk-free rate and volatility of the log return on the stock are constant throughout the option’s life

• There are no taxes or transaction costs• The stock pays no dividends• The options are European

Background

• Put and call prices are affected by– Price of underlying asset

– Option’s exercise price

– Length of time until expiration of option

– Volatility of underlying asset

– Risk-free interest rate

– Cash flows such as dividends

• Premiums can be derived from the above factors

Option Valuation

• The value of an option is the present value of its intrinsic value at expiration. Unfortunately, there is no way to know this intrinsic value in advance.

• Black & Scholes developed a formula to price call options

• This most famous option pricing model is the often referred to as “Black-Scholes OPM”.

The Concepts Underlying Black-Scholes

• The option price and the stock price depend on the same underlying source of uncertainty

• We can form a portfolio consisting of the stock and the option which eliminates this source of uncertainty

• The portfolio is instantaneously riskless and must instantaneously earn the risk-free rate

Option Valuation Variables

• There are five variables in the Black-Scholes OPM (in order of importance):– Price of underlying security– Strike price– Annual volatility (standard deviation)– Time to expiration– Risk-free interest rate

Option Valuation Variables: Underlying Price

• The current price of the underlying security is the most important variable.

• For a call option, the higher the price of the underlying security, the higher the value of the call.

• For a put option, the lower the price of the underlying security, the higher the value of the put.

Option Valuation Variables: Strike Price

• The strike (exercise) price is fixed for the life of the option, but every underlying security has several strikes for each expiration month

• For a call, the higher the strike price, the lower the value of the call.

• For a put, the higher the strike price, the higher the value of the put.

Option Valuation Variables: Volatility

• Volatility is measured as the annualized standard deviation of the returns on the underlying security.

• All options increase in value as volatility increases.

• This is due to the fact that options with higher volatility have a greater chance of expiring in-the-money.

Option Valuation Variables: Time to Expiration

• The time to expiration is measured as the fraction of a year.

• As with volatility, longer times to expiration increase the value of all options.

• This is because there is a greater chance that the option will expire in-the-money with a longer time to expiration.

Option Valuation Variables: Risk-free Rate

• The risk-free rate of interest is the least important of the variables.

• It is used to discount the strike price• The risk-free rate, when it increases,

effectively decreases the strike price. Therefore, when interest rates rise, call options increase in value and put options decrease in value.

Implied Volatility

• The implied volatility of an option is the volatility for which the Black-Scholes price equals the market price

• The is a one-to-one correspondence between prices and implied volatilities

• Traders and brokers often quote implied volatilities rather than dollar prices

Nature of Volatility

• Volatility is usually much greater when the market is open (i.e. the asset is trading) than when it is closed

• For this reason time is usually measured in “trading days” not calendar days when options are valued

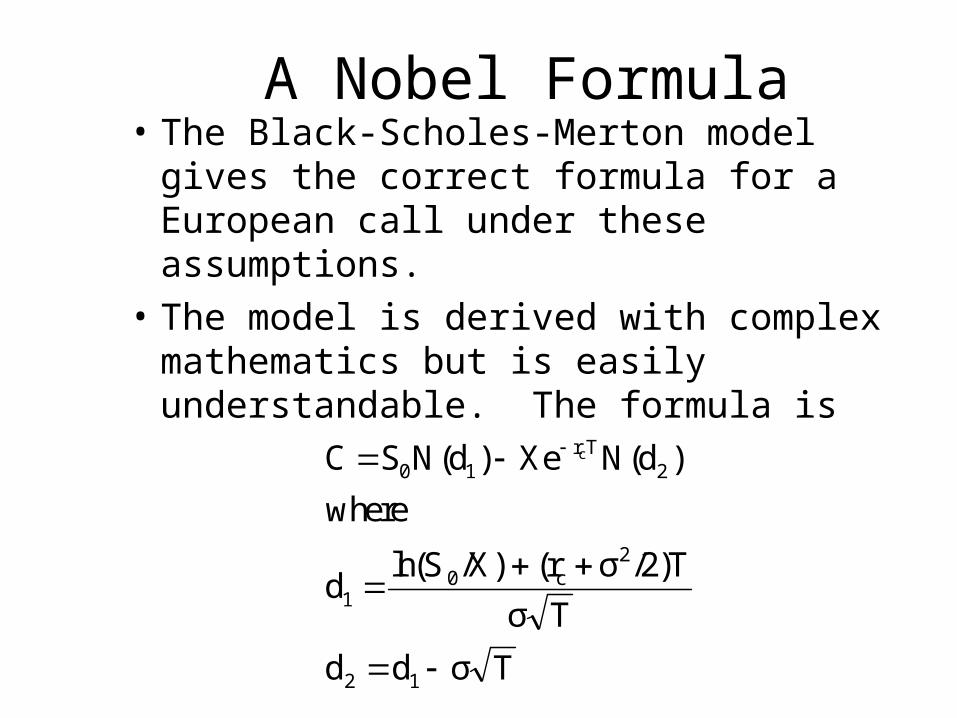

A Nobel Formula• The Black-Scholes-Merton model gives the

correct formula for a European call under these assumptions.

• The model is derived with complex mathematics but is easily understandable. The formula is

Tσdd

Tσ

/2)Tσ(r/X)ln(Sd

where

)N(dXe)N(dSC

12

2c0

1

2Tr

10c

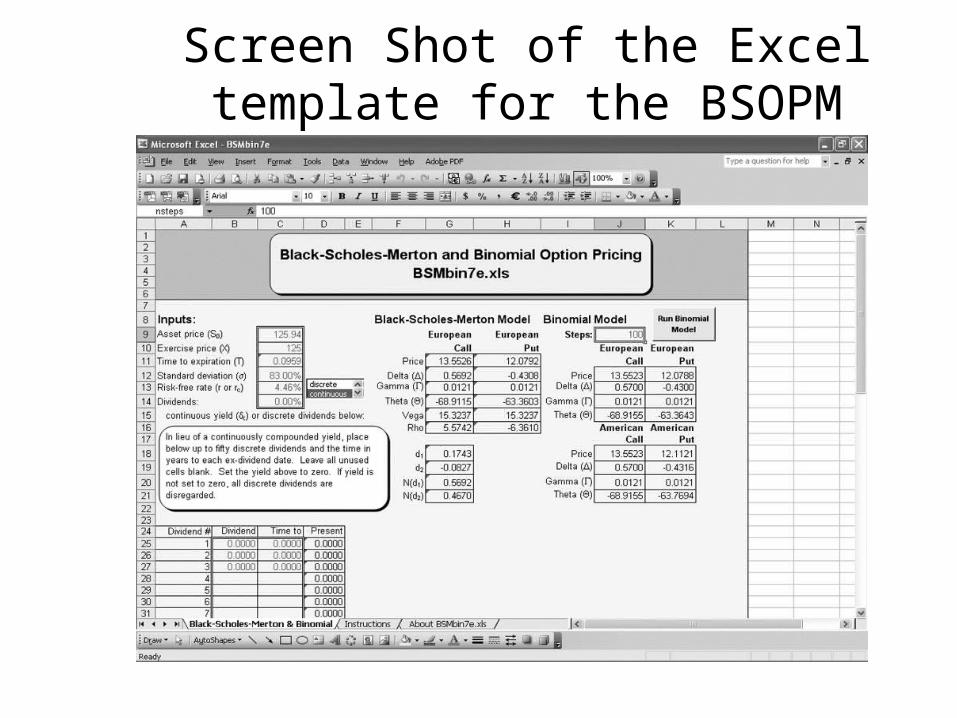

Screen Shot of the Excel template for the BSOPM

OPM & The Measurement of Portfolio Risk Exposure

• Because BS OPM isolates the effects of each variable’s effect on pricing, it is said that these isolated, independent effects measure the sensitivity of the options value to changes in the underlying variables.

The Greeks

Greeks are derivatives of the option price function :

• Delta• Gamma• Theta• Vega• Rho

The Greeks are also called hedge parameters as they are often used in hedging operations by big financial institutions

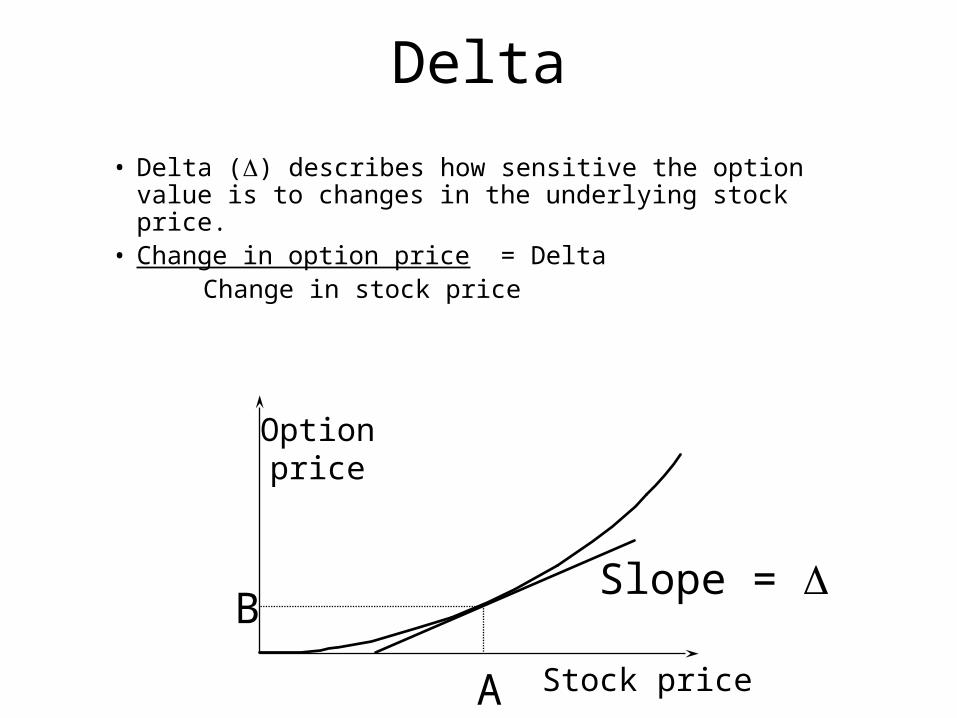

Delta

• Delta () describes how sensitive the option value is to changes in the underlying stock price.

• Change in option price = Delta Change in stock price

Optionprice

A

BSlope =

Stock price

Delta Application

• Suppose that the delta of a call is .8944.

• What does this mean????

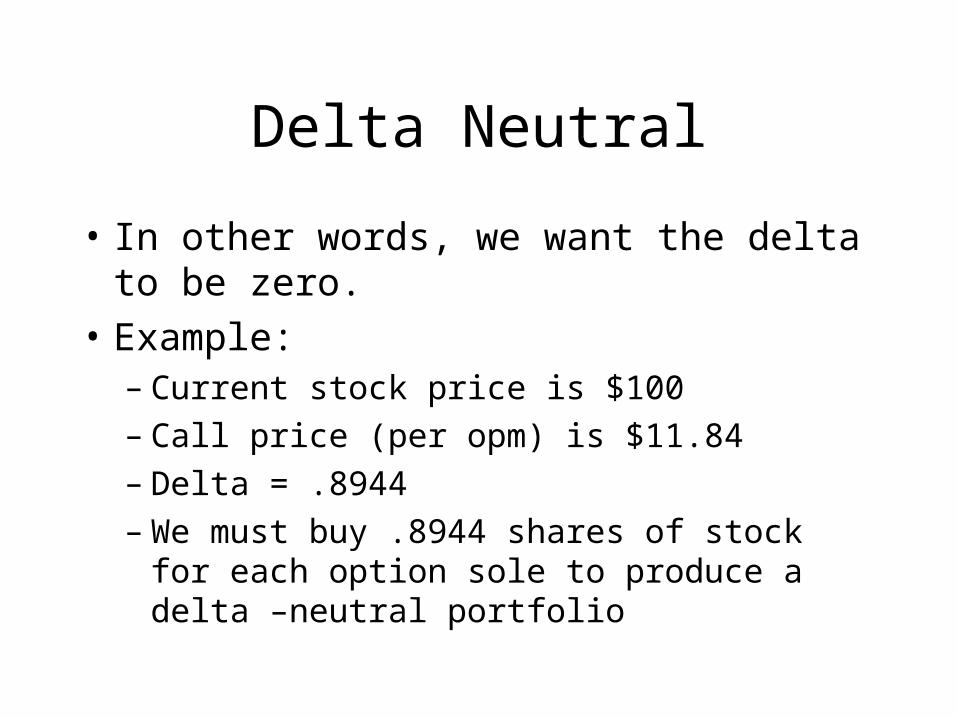

Delta Neutral

• In other words, we want the delta to be zero.

• Example:– Current stock price is $100– Call price (per opm) is $11.84– Delta = .8944– We must buy .8944 shares of stock for each

option sole to produce a delta –neutral portfolio

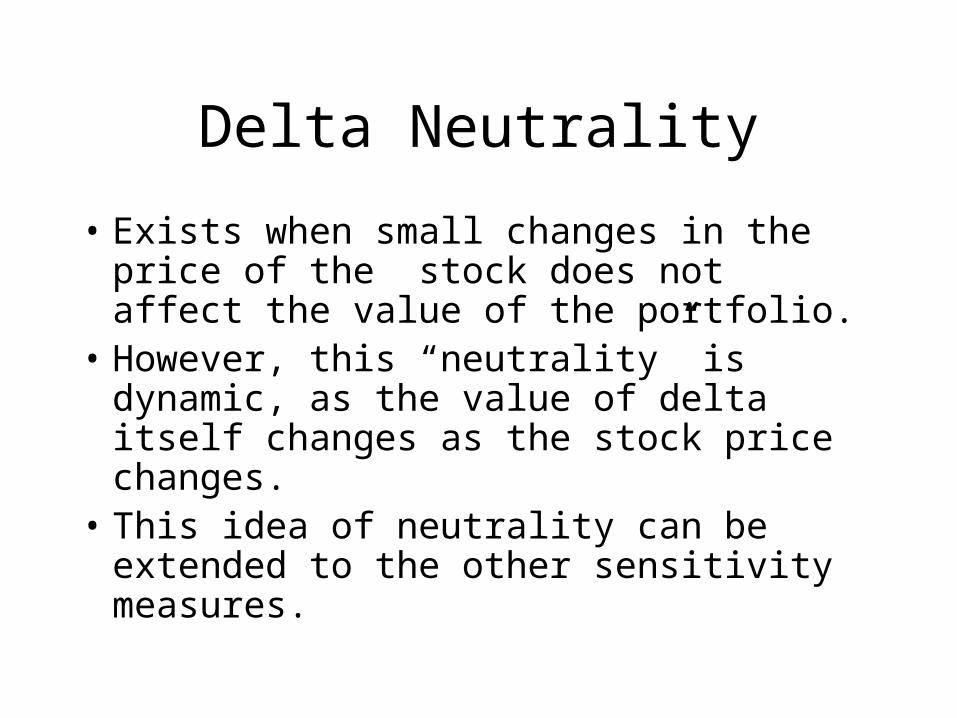

Delta Neutrality

• Exists when small changes in the price of the stock does not affect the value of the portfolio.

• However, this “neutrality” is dynamic, as the value of delta itself changes as the stock price changes.

• This idea of neutrality can be extended to the other sensitivity measures.

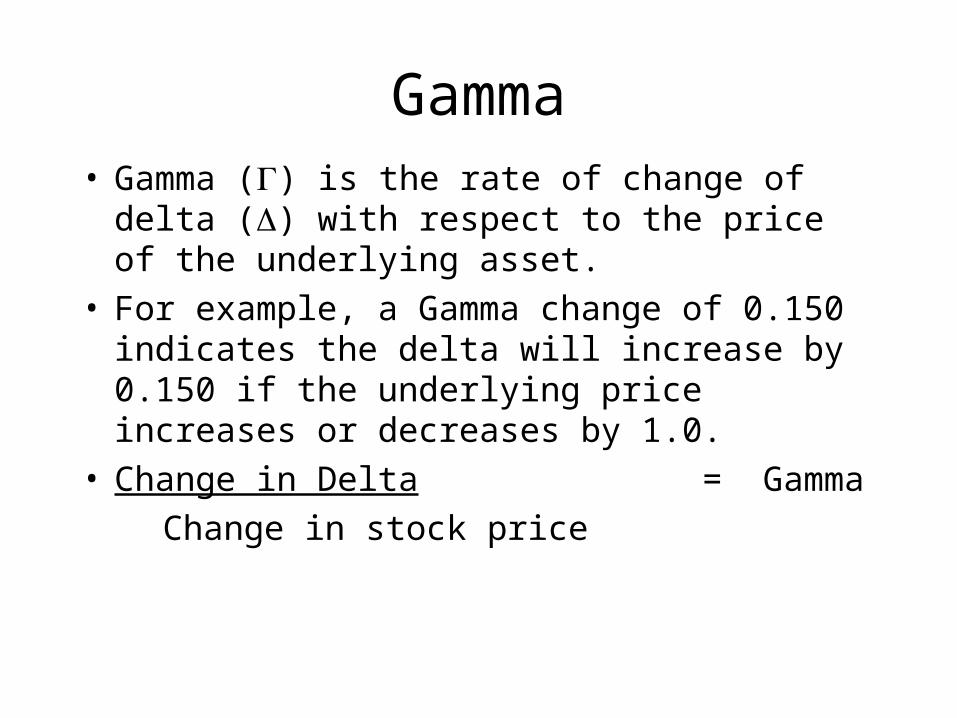

Gamma• Gamma () is the rate of change of delta () with

respect to the price of the underlying asset.

• For example, a Gamma change of 0.150 indicates the delta will increase by 0.150 if the underlying price increases or decreases by 1.0.

• Change in Delta = Gamma

Change in stock price

Gamma Application

• Can be either positive or negative

• The only Greek that does not measure the sensitivity of an option to one of the underlying assets. – it measures changes to its Greek brother – Delta, as a result of changes to the stock price.

Theta

• Theta () of a derivative is the rate of change of the value with respect to the passage of time.

• Or sensitivity of option value to change in time

• Change in Option Price = THETA

Change in time to Expiration

Theta Application

• If time is measured in years and value in dollars, then a theta value of –10 means that as time to option expiration declines by .1 years, option value falls by $1.

• AKA Time decay: – A term used to describe how the

theoretical value of an option "erodes" or reduces with the passage of time.

Vega

• Vega () is the rate of change of the value of a derivatives portfolio with respect to volatility

• For example:– a Vega of .090 indicates an absolute change in the option's theoretical value will increase by .090 if the volatility percentage is increased by 1.0 or decreased by .090 if the volatility percentage is decreased by 1.0.

• Change in Option Price = Vega

Change in volatility

Vega Application

• Proves to us that the more volatile the underlying stock, the more volatile the option price.

• Vega is always a positive number.

Rho

• Rho is the rate of change of the value of a derivative with respect to the interest rate

• For example:– a Rho of .060 indicates the option's theoretical value will increase by .060 if the interest rate is decreased by 1.0.

• Change in option price = RHO Change in interest rate

Rho Application

• Rho for calls is always positive

• Rho for puts is always negative

• A Rho of 25 means that a 1% increase in the interest rate would:– Increase the value of a call by $.25– Decrease the value of a put by $.25