opportunity day ' 2009.ppt - set.or.th · pdf filethroughout the nation covering both...

TRANSCRIPT

1

OOpportunity Day

PREMIER MARKETING PUBLIC CO.,LTD.CO.,LTD.

2009 PERFORMANCE

2

A dAgenda COMPANY OVERVIEW

INDUSTRY OVERVIEW

FINANCIAL HIGHLIGHTS

FUTURE BUSINESS DIRECTION

SHARE PRICE PERFORMANCE

3

COMPANY OVERVIEWCOMPANY OVERVIEW

4

Business Group Structure

Premier Group Of Companies

Support Functions1. Accounting & Investment

2 Human Resources2. Human Resources

3. Corporate Core Value

4. Internal Audit

5 Communication & PR5. Communication & PR

Consumer Products

Business GroupFinancial Services

Business Group

Information Technology

Business Group

Trading & Manufacturing

Business Group

Real Estate Development

Business GroupNew Business

5

Premier VisionPremier Vision

กลุ่มบริษัทไทยที่เป็นผู้นําในการทาํธุรกิจที่ประสบความสาํเร็จ

ทัง้ในด้านสังคม องค์กร และ พนักงานทงในดานสงคม องคกร และ พนกงาน

เพื่อสร้างความสุขที่ยั่งยืนร่วมกัน

To be leading Thai conglomerate that drivesTo be leading Thai conglomerate that drives success of society, organization and staff to create sustainable and harmonious happiness

6

The Premier ValueThe Premier Value

The Premier Business ธรกจิก้าวหน้าThe Premier Business

The Premier People

ธุรกจกาวหนา

พนักงานมั่นคงp

The Premier Society สังคมยั่งยืน

“THE HARMONIOUS SUCCESS”

7

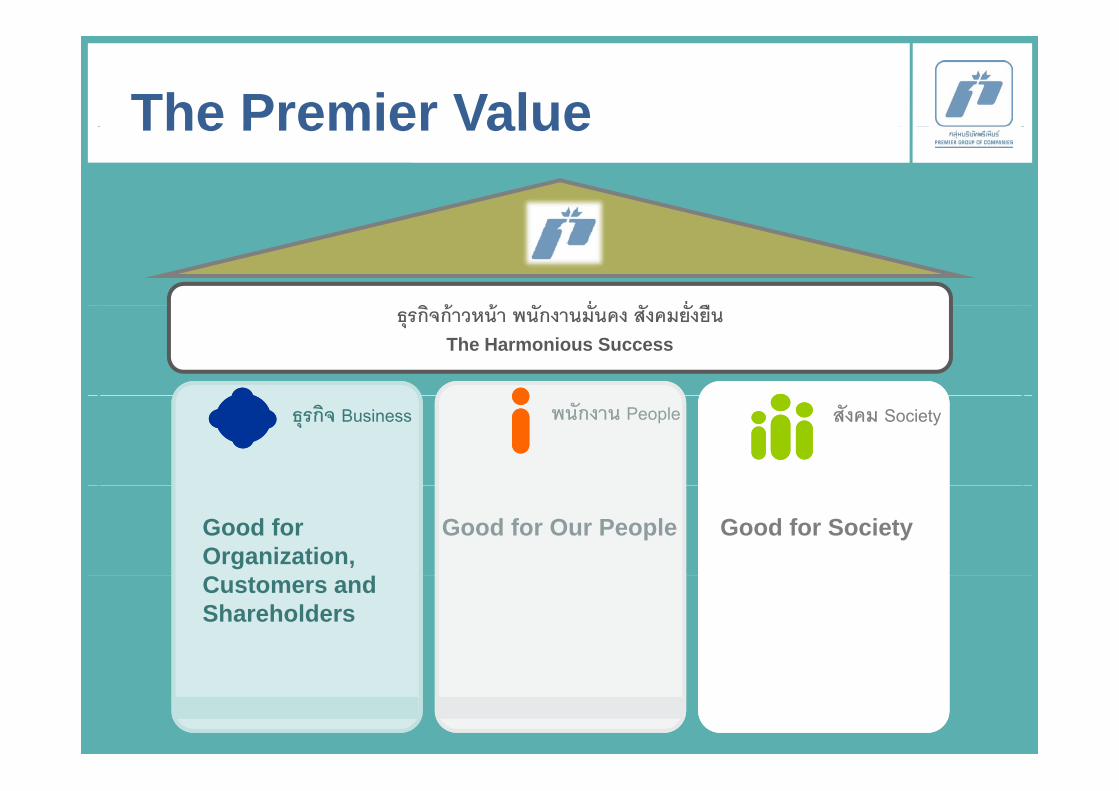

The Premier ValueThe Premier Value

ิ ้ ้ ั ั่ ั ั่ ืธุรกจิก้าวหน้า พนักงานมันคง สังคมยังยืนThe Harmonious Success

พนักงาน People สังคม Societyธุรกจิ Business

Good for Organization,

Good for SocietyGood for Our People

Customers and Shareholders

8

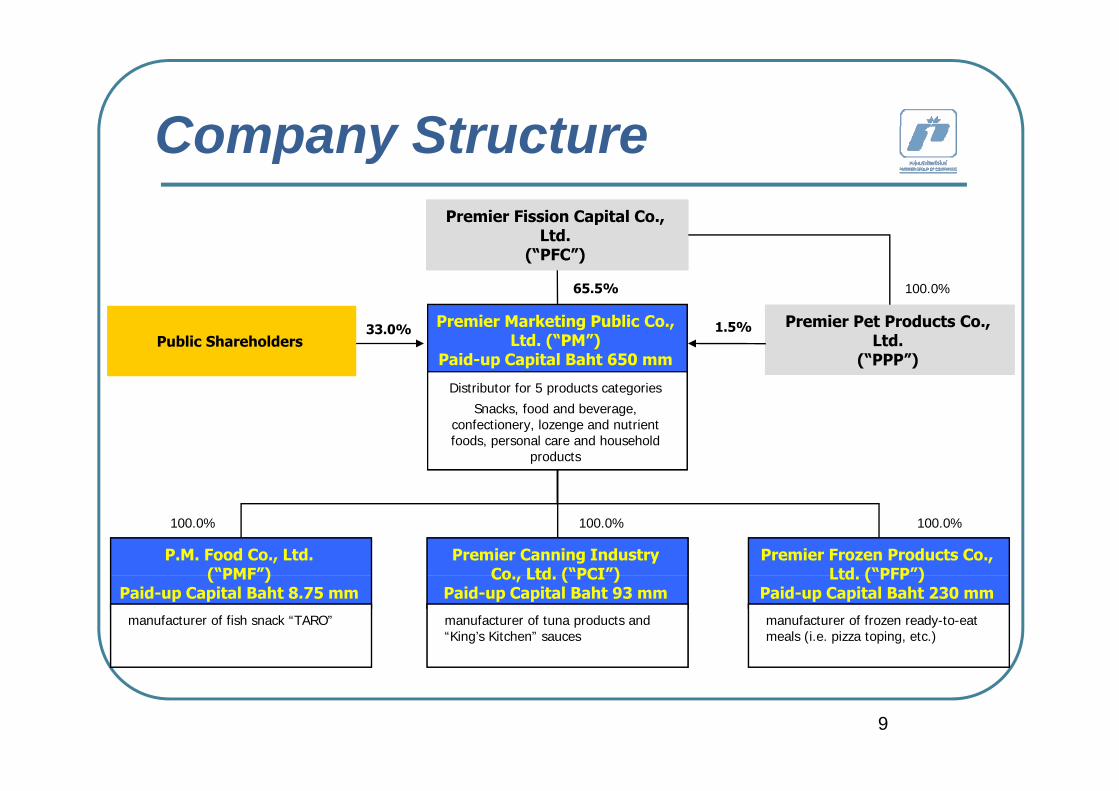

Company StructurePremier Fission Capital CoPremier Fission Capital Co

Company StructurePremier Fission Capital Co.,

Ltd.(“PFC”)

Premier Fission Capital Co., Ltd.

(“PFC”)

65.5% 100.0%

Public ShareholdersPublic Shareholders33.0% Premier Marketing Public Co.,

Ltd. (“PM”)Paid-up Capital Baht 650 mm

Premier Pet Products Co., Ltd.

(“PPP”)

Premier Pet Products Co., Ltd.

(“PPP”)

1.5%

Distributor for 5 products categoriesSnacks, food and beverage,

confectionery, lozenge and nutrient foods, personal care and household

products

P.M. Food Co., Ltd.(“PMF”)

Premier Canning Industry Co Ltd (“PCI”)

Premier Frozen Products Co., Ltd (“PFP”)

100.0% 100.0% 100.0%

( PMF )Paid-up Capital Baht 8.75 mm

Co., Ltd. ( PCI )Paid-up Capital Baht 93 mm

Ltd. ( PFP )Paid-up Capital Baht 230 mm

manufacturer of tuna products and “King’s Kitchen” sauces

manufacturer of frozen ready-to-eat meals (i.e. pizza toping, etc.)

manufacturer of fish snack “TARO”

9

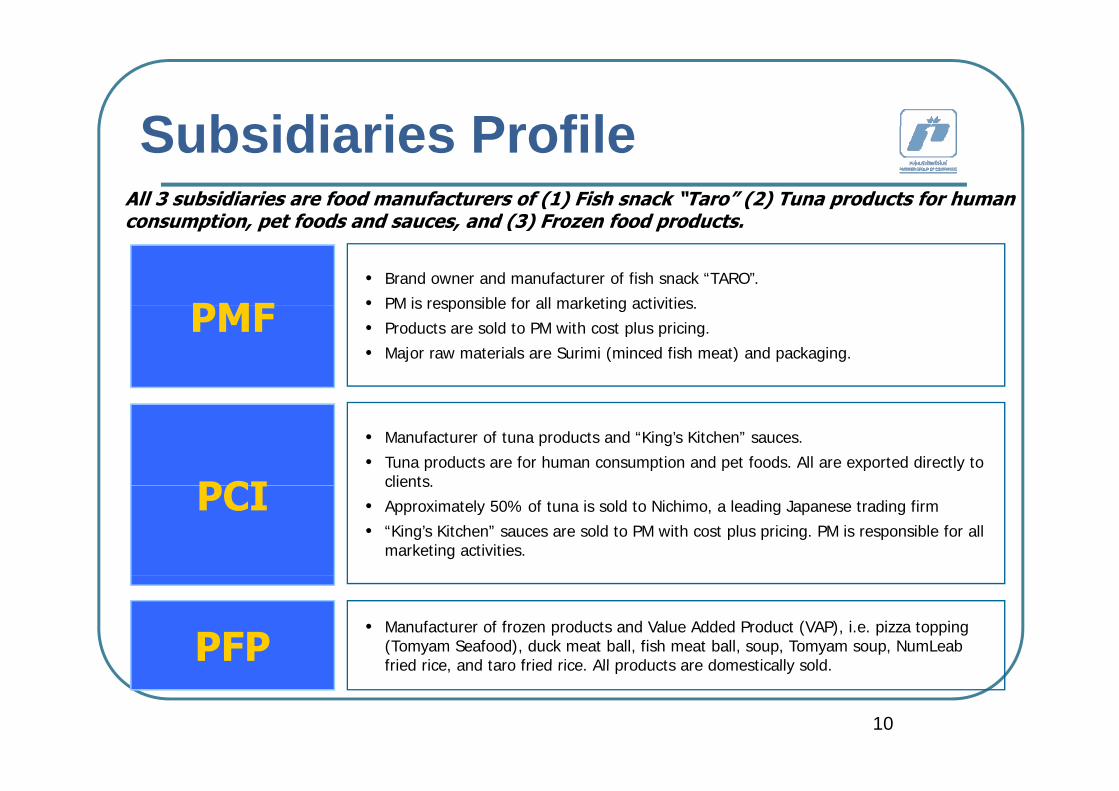

Subsidiaries ProfileAll 3 subsidiaries are food manufacturers of (1) Fish snack “Taro” (2) Tuna products for human

ti t f d d d (3) F f d d t

Subsidiaries Profileconsumption, pet foods and sauces, and (3) Frozen food products.

PMF• Brand owner and manufacturer of fish snack “TARO”.• PM is responsible for all marketing activitiesPMF • PM is responsible for all marketing activities.• Products are sold to PM with cost plus pricing.• Major raw materials are Surimi (minced fish meat) and packaging.

PCI

• Manufacturer of tuna products and “King’s Kitchen” sauces.• Tuna products are for human consumption and pet foods. All are exported directly to

clients.PCI clients.• Approximately 50% of tuna is sold to Nichimo, a leading Japanese trading firm• “King’s Kitchen” sauces are sold to PM with cost plus pricing. PM is responsible for all

marketing activities.

PFP• Manufacturer of frozen products and Value Added Product (VAP), i.e. pizza topping

(Tomyam Seafood), duck meat ball, fish meat ball, soup, Tomyam soup, NumLeab fried rice and taro fried rice All products are domestically sold

10

fried rice, and taro fried rice. All products are domestically sold.

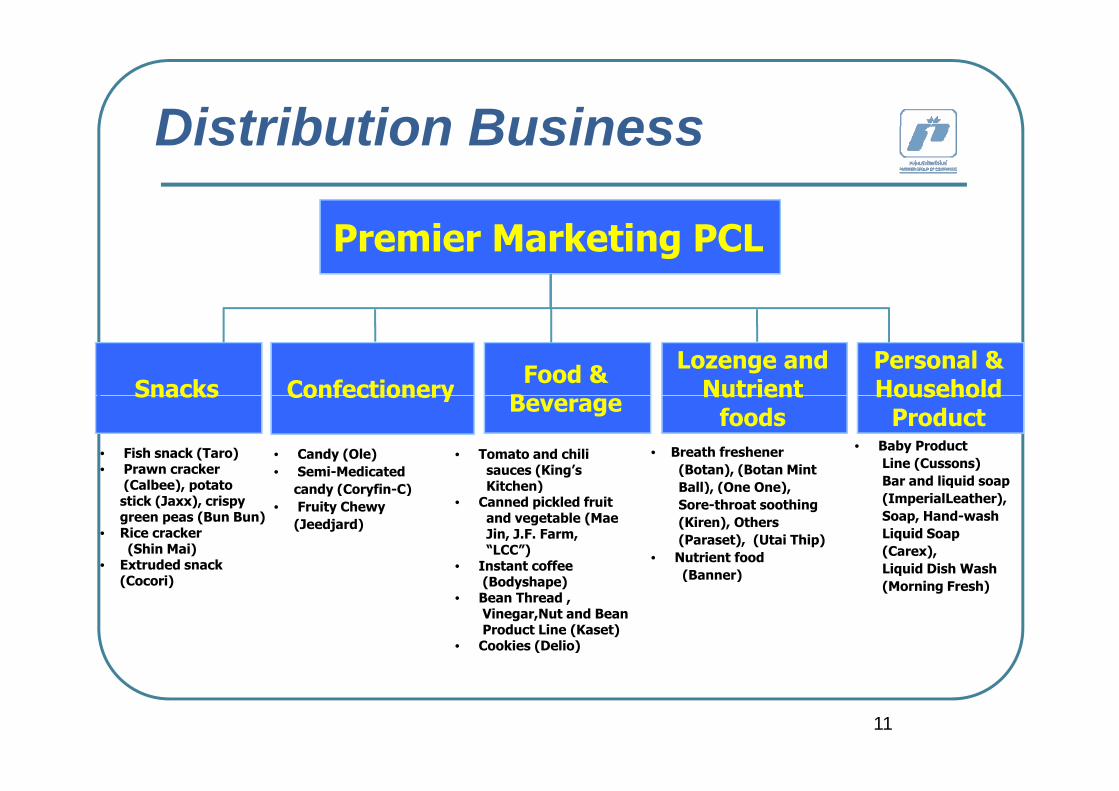

Distribution BusinessDistribution Business

Premier Marketing PCL

Snacks Confectionery Food & B

Lozenge and Nutrient

Personal & HouseholdSnacks Confectionery Beverage Nutrient

foodsHousehold

Product• Fish snack (Taro)• Prawn cracker

(Calbee) potato

• Candy (Ole)• Semi-Medicated

d (C fi C)

• Tomato and chili sauces (King’s Kitchen)

• Breath freshener (Botan), (Botan Mint Ball) (One One)

• Baby Product Line (Cussons) Bar and liquid soap(Calbee), potato

stick (Jaxx), crispy green peas (Bun Bun)

• Rice cracker (Shin Mai)

• Extruded snack

candy (Coryfin-C)• Fruity Chewy

(Jeedjard)

Kitchen)• Canned pickled fruit

and vegetable (Mae Jin, J.F. Farm, “LCC”)

• Instant coffee

Ball), (One One), Sore-throat soothing (Kiren), Others (Paraset), (Utai Thip)

• Nutrient food (Banner)

Bar and liquid soap (ImperialLeather), Soap, Hand-wash Liquid Soap (Carex),Liquid Dish Wash

(Cocori) (Bodyshape)• Bean Thread ,

Vinegar,Nut and Bean Product Line (Kaset)

• Cookies (Delio)

(Banner) q(Morning Fresh)

11

Distribution ChannelsDistribution Channels

1. Modern Trade

Distribution Channels Distribution Channels Nationwide OutletsNationwide Outlets

• Direct distribution to more than 30,000 outlets throughout the nation covering both modern Supermarket, Hypermarket,

Convenience store, and Gas station store by delivering to clients’ Distribution Centers

throughout the nation covering both modern trade retailers and traditional channels

• In 2009, Bangkok metropolitan and suburb areas represented 62.4% of PM sales and

2. Traditional TradeWholesalers and Local

37.6 % for upcountry

Supermarkets

3. Cash VanDirect visits to small retail shops,

Up-country37.6 %

Bangkok

Metropolitan62.4 %

orders are taken and goods delivered from company sales van

12

INDUSTRY OVERVIEWINDUSTRY OVERVIEW

13

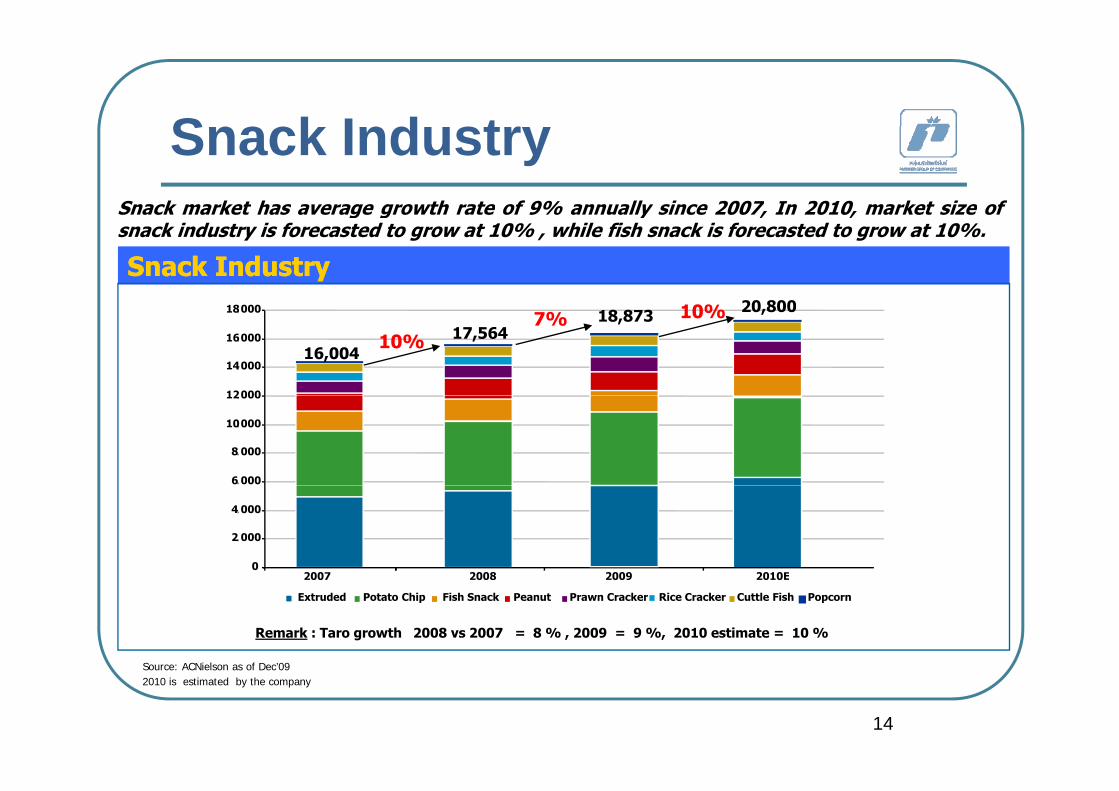

S k I d tSnack market has average growth rate of 9% annually since 2007, In 2010, market size of

Snack Industryg g y , ,

snack industry is forecasted to grow at 10% , while fish snack is forecasted to grow at 10%.

Snack IndustrySnack Industry18000 20 80010%

12000

14, 000

16, 000

18, 000

16,00417,564

7% 18,873

10%

20,80010%

6, 000

8, 000

10, 000

12, 000

0

2, 000

4, 000

2010E2007 2008 2009

Source: ACNielson as of Dec’09

Extruded Potato Chip Fish Snack Peanut Prawn Cracker Rice Cracker Cuttle Fish Popcorn

2010E2007 2008 2009

Remark : Taro growth 2008 vs 2007 = 8 % , 2009 = 9 %, 2010 estimate = 10 %

14

Source: ACNielson as of Dec’092010 is estimated by the company

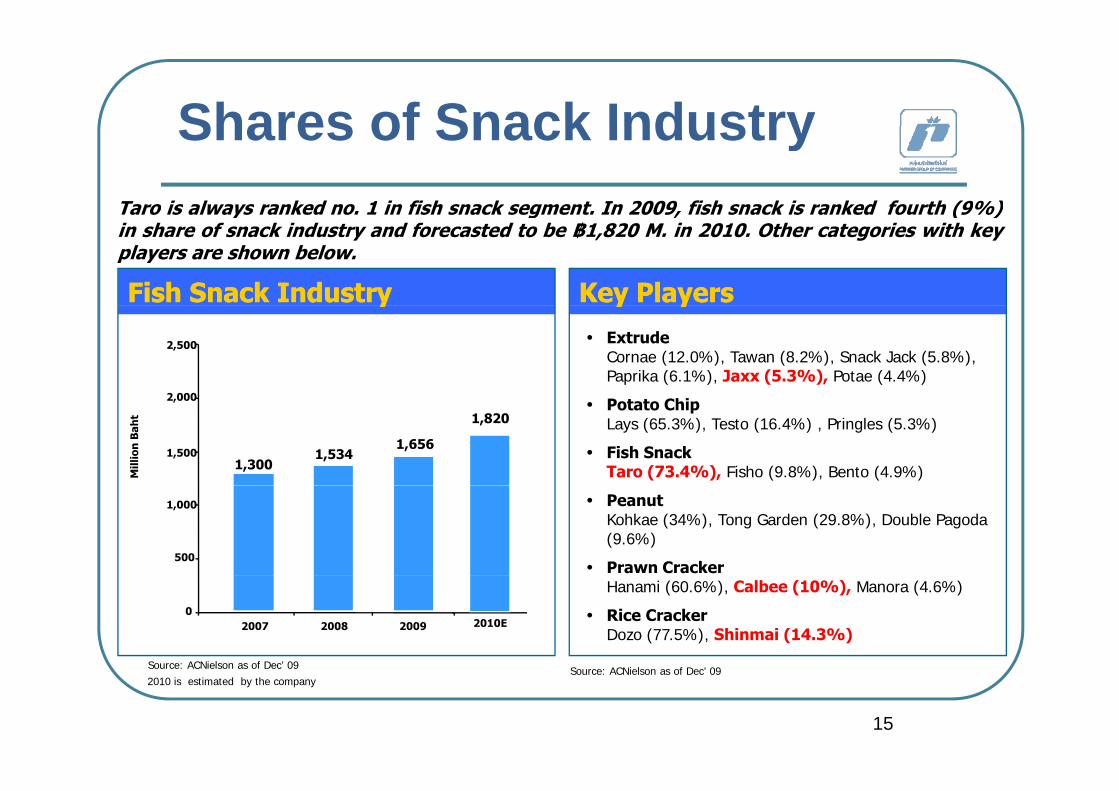

Shares of Snack IndustryTaro is always ranked no. 1 in fish snack segment. In 2009, fish snack is ranked fourth (9%)

Shares of Snack Industryy g , ( )

in share of snack industry and forecasted to be ฿1,820 M. in 2010. Other categories with keyplayers are shown below.

Key PlayersKey PlayersFish Snack IndustryFish Snack Industry y yy y• Extrude

Cornae (12.0%), Tawan (8.2%), Snack Jack (5.8%), Paprika (6.1%), Jaxx (5.3%), Potae (4.4%)

yy

2 000

2,500

• Potato ChipLays (65.3%), Testo (16.4%) , Pringles (5.3%)

• Fish SnackTaro (73.4%), Fisho (9.8%), Bento (4.9%)M

illio

n B

aht

1,656

1,820

1,3001,5341,500

2,000

• PeanutKohkae (34%), Tong Garden (29.8%), Double Pagoda (9.6%)

• Prawn Cracker500

1,000

Hanami (60.6%), Calbee (10%), Manora (4.6%)

• Rice CrackerDozo (77.5%), Shinmai (14.3%)

Source: ACNielson as of Dec’ 09

020092007 2008 2010E

15

Source: ACNielson as of Dec’ 09Source: ACNielson as of Dec 092010 is estimated by the company

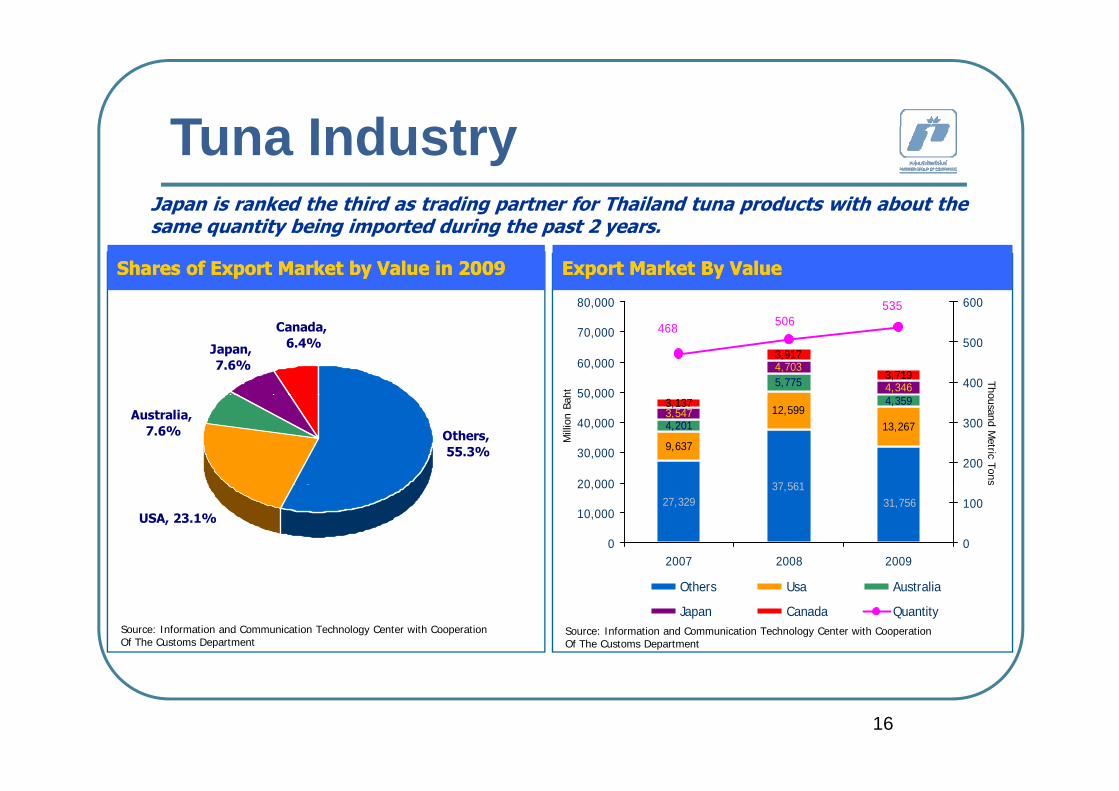

T I d tJapan is ranked the third as trading partner for Thailand tuna products with about the

Tuna Industrysame quantity being imported during the past 2 years.

Shares of Export Market by Value in Shares of Export Market by Value in 20092009

53580,000 600

Export Market By ValueExport Market By Value

Canada, 6.4%Japan,

7.6%5,7754,703

4,346

3,917

3,719

535506468

50 000

60,000

70,000

80,000

400

500

600

ht

Tho

Others, 55.3%

Australia, 7.6%

37 561

9,637

12,59913,2674,201

4,3593,5473,137

20 000

30,000

40,000

50,000

200

300

Mill

ion

Bah ousand M

etric Tons

USA, 23.1%27,329

37,56131,756

0

10,000

20,000

2007 2008 20090

100

Source: Information and Communication Technology Center with CooperationOf The Customs Department

Others Usa Australia

Japan Canada QuantitySource: Information and Communication Technology Center with CooperationOf The Customs Department

16

FINANCIAL HIGHLIGHTSFINANCIAL HIGHLIGHTS

17

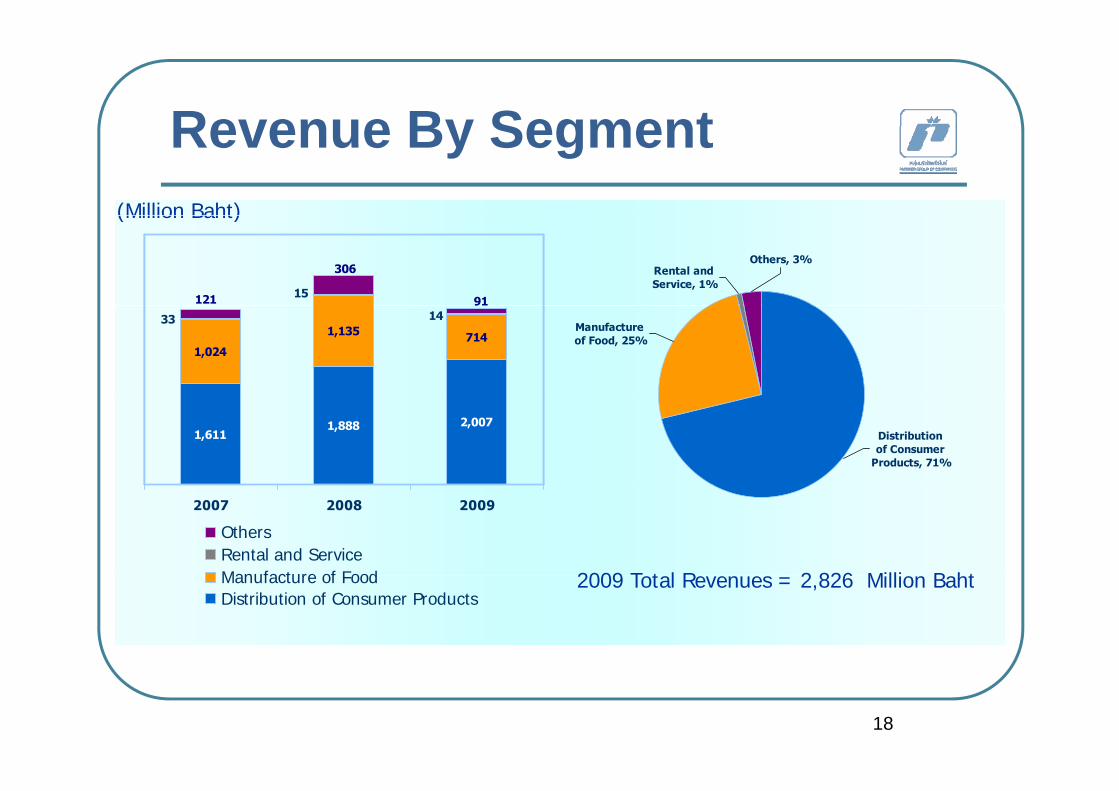

Revenue By SegmentRevenue By Segment(Million Baht)

Others, 3%Rental and Service, 1%

15

306

121 91

(Million Baht)

Manufacture of Food, 25%

1,024

1,135 71433 14

Distribution of Consumer

Products, 71%

1,6111,888 2,007

2009 T t l R 2 826 Milli B ht

2007 2008 2009

OthersRental and ServiceManufacture of Food 2009 Total Revenues = 2,826 Million BahtManufacture of FoodDistribution of Consumer Products

18

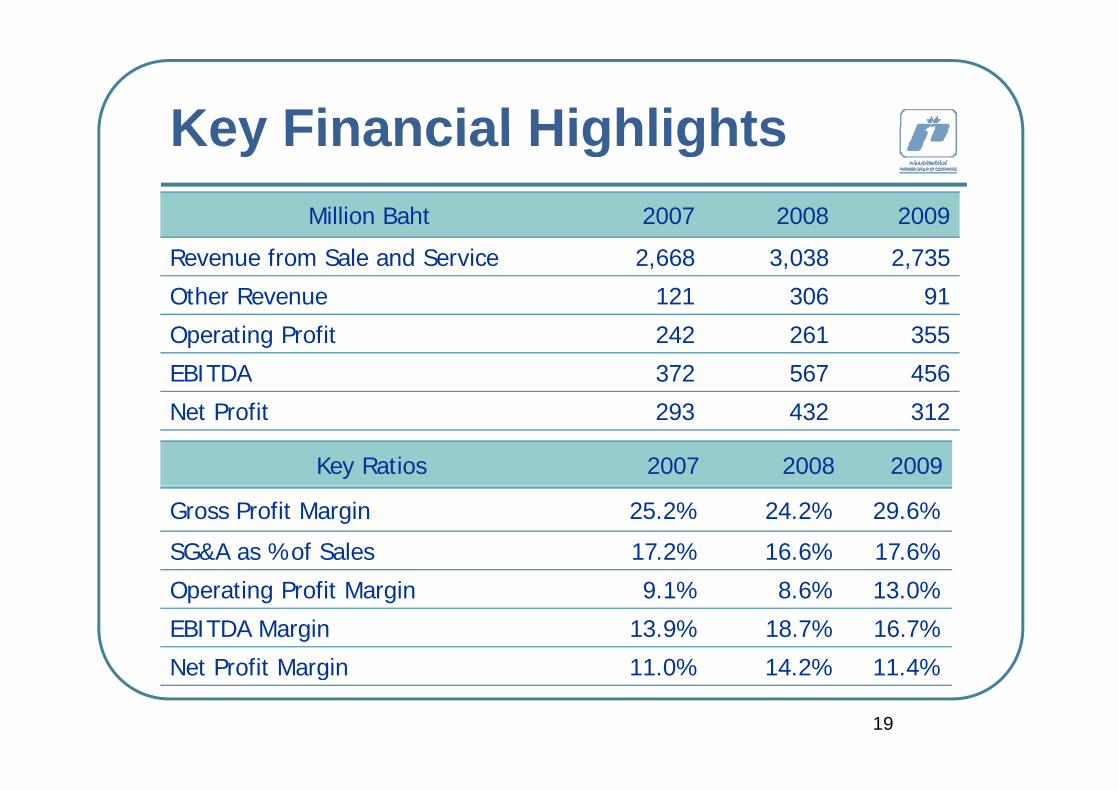

Key Financial HighlightsKey Financial HighlightsMillion Baht 2007 2008 2009Million Baht 2007 2008 2009

Revenue from Sale and Service 2,668 3,038 2,735

Other Revenue 121 306 91

Operating Profit 242 261 355

EBITDA 372 567 456

Net Profit 293 432 312

Key Ratios 2007 2008 2009

Gross Profit Margin 25.2% 24.2% 29.6%

SG&A as %of Sales 17.2% 16.6% 17.6%

Operating Profit Margin 9.1% 8.6% 13.0%

EBITDA Margin 13.9% 18.7% 16.7%

Net Profit Margin 11 0% 14 2% 11 4%

19

Net Profit Margin 11.0% 14.2% 11.4%

P f5,000

100.0%

PerformanceSales and Service & Gross Margin Operating Profit & Margin

242 261

355

200

300

400

500

40.0%

60.0%

80.0%

100.0%

2,6683,038

2,735

24.2%25.2%29.6%2,000

3,000

4,000

40.0%

60.0%

80.0%

00.0%Sales and Service & Gross Margin Operating Profit & Margin

ht)

8.6%9.1%13.0%

0

100

200

2007 2008 2009

0.0%

20.0%

40.0%

0

1,000

2007 2008 2009

0.0%

20.0%

(Mill

ion

Ba

Operating Profit Operating Profit MarginSale and Service Gross Margin

600 100 0%Net Profit & Margin

293

432

312300

400

500

600

40.0%

60.0%

80.0%

100.0%

14.2%11.0%11.4%

0

100

200

2007 2008 2009

0.0%

20.0%

20

Net Profit Net Profit Margin

FUTURE BUSINESSFUTURE BUSINESS

DIRECTIONDIRECTION

21

F t B i Di tiFuture Business Direction

Develop more premium snack food product lines

Focus on quality / premium ready to eat items Focus on quality / premium ready-to-eat items

Seek additional trading partner for export g p pmarkets

Closer cooperation with existing business Closer cooperation with existing business partners for future expansion

Explore opportunities for joint venture & business acquisition

22

q

SHARE PRICE PERFORMANCE

23

Sh P i P fShare Price PerformanceYTD Sh P i P f

2.30

2.50

YTD Share Price Performance

1.70

1.90

2.10

)

1 10

1.30

1.50

1.70

30/12/2009

(Bah

t)

0 50

0.70

0.90

1.10 Close = 2.20 Bt.

0.50

Jan-09 Feb-09 Mar-09 Apr -09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09

24

Q & AQ

DiscussionDiscussion

25