opportunities in the uk cherry market: a supply chain audit · consumer response (ecr) and category...

TRANSCRIPT

Opportunities in the UK Cherry Market: A Supply Chain Audit

U. Wermund, A. Fearne and S. Hornibrook

Department of Agricultural Sciences

Imperial College at Wye

Abstract

The paper presents the results of a study designed to explore the opportunities for UK

cherry growers to gain a bigger and more profitable share of the UK cherry market. The

study is the first to take a holistic view of the cherry supply chain, from growers through

to the final consumer. The results suggest that, in common with other UK fruit there is a

need for investment in new varieties, improved post-harvest technology and a more

effective and efficient flow of physical product and knowledge within the cherry supply

chain. In order for this to happen greater co-ordination is required within the cherry

supply chain, to exploit market intelligence, reduce costs and develop distinct products

for different market segments.

Keywords: UK Cherry market, supply chain audit, vertical co-ordination

1. INTRODUCTION

UK food retailers are amongst the most sophisticated in the world and the demands which

they place on their suppliers, particularly their suppliers of fresh produce (fruit,

vegetables, meat and fish) render the British food industry one of the most efficient and

innovative in the world (Fearne & Hughes, 2000). The implementation of Efficient

Consumer Response (ECR) and Category Management (CM) heralds the dawn of a new

era in which value creation is the priority, with supermarkets and their suppliers working

together to exploit the diverse opportunities which exist in a cosmopolitan marketplace in

which (relatively) affluent and increasingly diligent consumers are running out of time to

purchase, prepare, cook and consume their food.

2

2

Historically, the fresh produce industry has lagged some way behind the manufacturers of

fast moving consumer goods (fmcg) in its approach to marketing and merchandising,

seemingly resigned to the status of commodity traders. However, the ascendancy of the

multiple retailers and the key strategic importance of own label fresh produce presents

suppliers with a genuine opportunity to break out of the commodity trap and take the

fresh produce category out of the trading environment.

Grasping this opportunity is not easy, particularly in sectors where the commodity status

is particularly difficult to change (eg potatoes, brassicas, apples, pears) but for those

sectors that already hold a niche status within the fresh produce category (eg exotic fruit

and vegetables, berry fruit and stone fruit at different times of the year) the challenge is,

arguably, less daunting and the rewards more attractive as the consumer resistance to

price premiums for product differentiation is much less than it is for staple, commodity

lines. Cherries are a good example – limited domestic production, seasonal consumption,

untapped health benefits (cherries are high in perillul alcohol, a naturally existing

chemical which flushes cancer-causing substances from the body, and at the same time,

prevents growth of cancerous cells) and positive consumer perceptions – yet the UK

cherry market is dominated by imports and UK growers have struggled to penetrate the

most profitable marketing channel, the retail multiples.

This study was commissioned1 specifically to explore the key issues facing UK cherry

growers and marketing organizations looking forward to the long term development and

sustainability of the UK cherry industry. The dominance of the multiple retailers across

all food categories in the UK is beyond question and the UK cherry industry will be

unable to develop for as long as it remains focused on the requirements of wholesale

markets, let alone farm shops and roadside stalls. The volume and value growth that is

essential for investment and innovation can only come if the UK cherry industry rises to

the challenge of the multiple retailers. This paper aims to highlight the key issues which

1 The authors would like to thank the Mount Trust for commissioning the study.

3

3

growers and marketing organizations need to address if they are to succeed in meeting the

challenge, by examining the problems and opportunities at each point in the supply chain,

from growers to final consumers.

The paper is in five parts. Part two outlines the research methodology. Part three

summarises the key characteristics of the UK cherry market. Part four then presents the

key findings in three sub-sections, each covering the key issues (problems and

opportunities) relating to production (growers), marketing and distribution (agents,

importers and retailers), purchasing and consumption (final consumers). The final section

draws conclusions from the study and makes recommendations for further research.

2. Research Methodology

Previous research (Fearne & Hughes, 2000) has identified the growing importance of

vertical co-ordination in the food supply chain, as supermarkets compete for an increased

share of a mature market. Destination categories (food categories that have a significant

influence on a shopper’s choice of store), such as fresh produce and meat, are almost

exclusively own label and UK retailers are increasingly looking to their dedicated, often

exclusive, suppliers to deliver the unique selling proposition that will attract and/or retain

customers. Thus, any research into developing market opportunities within the UK food

retail sector must take a holistic supply chain perspective, with a view to understanding

customer needs at each point in the supply chain and the issues that prevent stakeholders

from meeting those needs. If UK cherry growers are to increase their share of the retail

market, it is essential that they identify customer needs more accurately and deliver

solutions (products and services) more efficiently and more effectively than their

competitors overseas, who continue to take the lion’s share of the supermarket business

even during the peak UK season.

Between September 1999 and April 2000 semi-structured interviews were conducted

with key industry representatives from each link in the cherry supply chain. Specifically,

interviews were conducted with ten growers, five importers/marketing organizations, five

4

4

major retailers and three research organizations. The interviews conducted a wide range

of issues, given the exploratory nature of the research, including production techniques,

post-harvest technology and marketing. Finally, qualitative consumer research in the

form of focus groups, was undertaken in the Spring 2000, which provided the basis for a

nationwide survey of cherry consumers which was undertaken in June/July, 2000.

3. Key characteristics of the UK cherry market

There is a dearth of information on the UK cherry market, but the key characteristics are

outlined below.

Cherries account for around five per cent of the UK fruit market and retail sales are worth

around £40 million (Checkout Fresh, 2000). However, household penetration is low

compared to other UK fruit, with 25% of households having purchased cherries during

the fifty two weeks ending April 28th, 2002, compared to 92% apples, 67% strawberries,

62% pears, 50% plums (Taylor Nelson SOFRES).

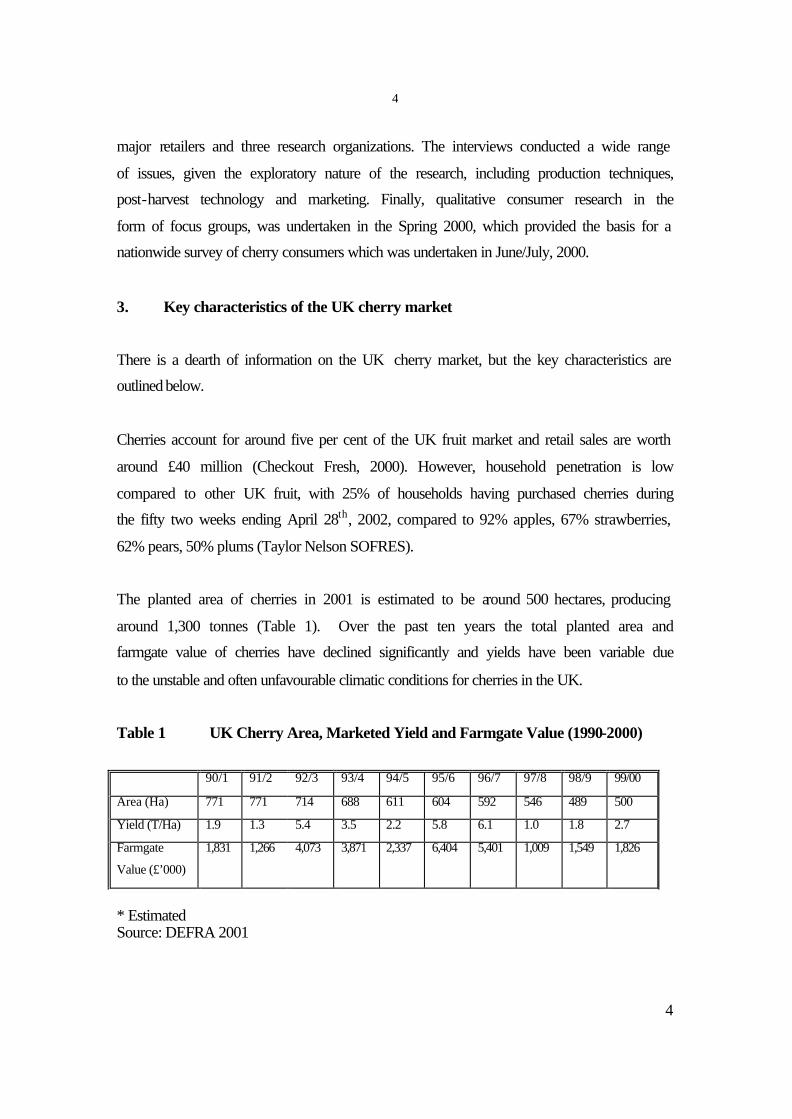

The planted area of cherries in 2001 is estimated to be around 500 hectares, producing

around 1,300 tonnes (Table 1). Over the past ten years the total planted area and

farmgate value of cherries have declined significantly and yields have been variable due

to the unstable and often unfavourable climatic conditions for cherries in the UK.

Table 1 UK Cherry Area, Marketed Yield and Farmgate Value (1990-2000)

90/1 91/2 92/3 93/4 94/5 95/6 96/7 97/8 98/9 99/00

Area (Ha) 771 771 714 688 611 604 592 546 489 500

Yield (T/Ha) 1.9 1.3 5.4 3.5 2.2 5.8 6.1 1.0 1.8 2.7

Farmgate

Value (£’000)

1,831 1,266 4,073 3,871 2,337 6,404 5,401 1,009 1,549 1,826

* Estimated Source: DEFRA 2001

5

5

Cherry production in the UK is concentrated in the South East, which accounts for 88%

of production, with the remainder split between the South West and, to a decreasing

extent, the West Midlands. The UK season is extremely short, lasting between five and

eight weeks, so the market is heavily dependent on imports (Figure 1). Over the last ten

years UK cherry imports have doubled in volume, from 7,500 tonnes in 1990 to 14,700

tonnes in 2000, and trebled in value, from £7.2 million to £21.8 million (Table 2).

Figure 1 The UK Annual Calendar for Cherries: Sources of Supply

Source: Fresh Produce Journal ( 2000) Table 2 UK Cherry Imports (1990-2000)

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000*

000 t 7.5 7.3 9.2 9.5 11.8 12.6 14.8 16.4 11.7 16.2 14.7

£000 7267 8090 9206 14405 13492 16723 19139 23789 21758 23793 21760

* Estimated Source: DEFRA 2001

Cherries are imported from around the world but the majority within season come from

Spain, Turkey and France. In 1999 the value of Spanish cherries rose to £10 million,

double the value for 1998. Demand for cherries outside the summer season are met

primarily from Chile and in 1999 were worth around £1 million (The Grower, 2000).

The UK is a lucrative market for overseas suppliers but the process is both capital and

MONTHS January February March April May June July August September October November December

WEEKS 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

Tasmania

Australia

New Zealand

Chile

Argentina

South Africa

California

Oregon

Washington

Spain

Italy

France

Portugal

Turkey

UK

Norway

6

6

labour intensive. Imported cherries are cooled to 40C in the packing house, typically

within four hours of harvest and subsequently hydrocooled at 00C. Fruit is typically

packed within twenty four hours into modified atmosphere packaging, for shipment either

by plane or boat, the latter requiring up to thirty five days from packhouse to retail store.

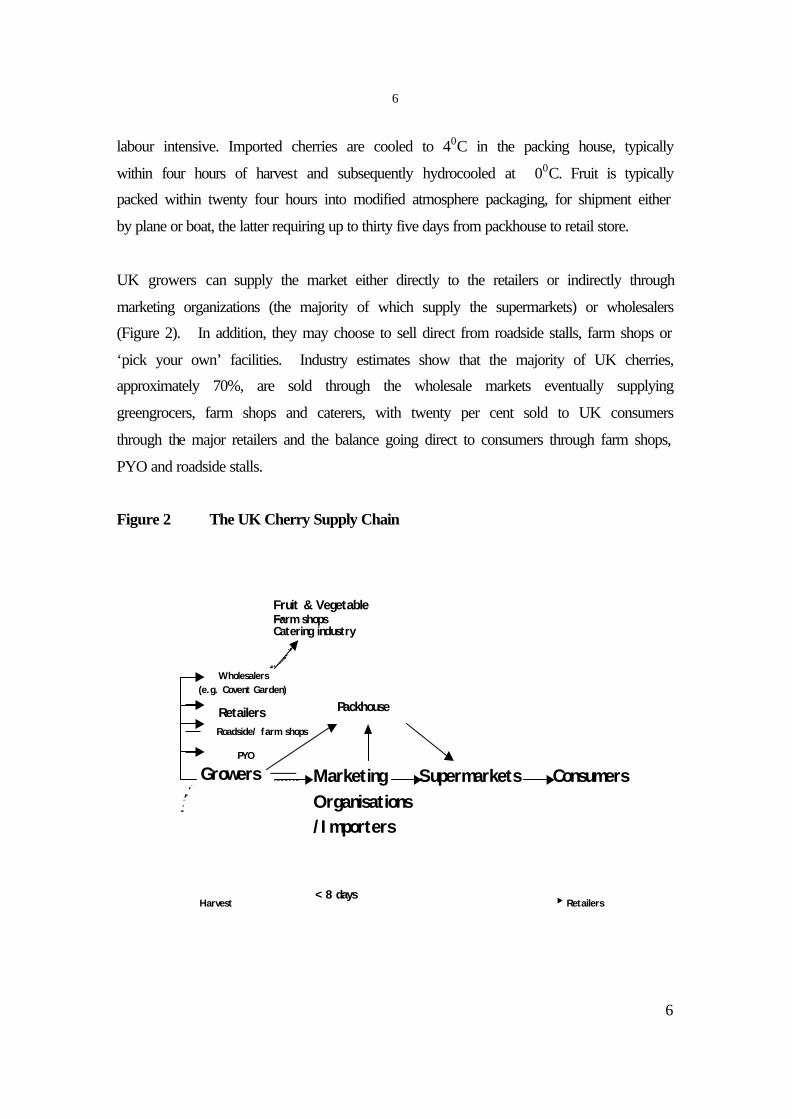

UK growers can supply the market either directly to the retailers or indirectly through

marketing organizations (the majority of which supply the supermarkets) or wholesalers

(Figure 2). In addition, they may choose to sell direct from roadside stalls, farm shops or

‘pick your own’ facilities. Industry estimates show that the majority of UK cherries,

approximately 70%, are sold through the wholesale markets eventually supplying

greengrocers, farm shops and caterers, with twenty per cent sold to UK consumers

through the major retailers and the balance going direct to consumers through farm shops,

PYO and roadside stalls.

Figure 2 The UK Cherry Supply Chain

ConsumersMarketingOrganisations/Importers

Supermarkets

Roadside/ farm shops

Packhouse

Harvest< 8 days

Retailers

Catering industryFarm shopsFruit & VegetableShops

Growers

Wholesalers(e.g. Covent Garden)

PYO

Retailers

7

7

The reliance of UK growers on the wholesale market is a major reason for the decline in

the production of UK cherries over the past ten years, in that wholesale prices are, on

average, 30% lower than retail prices and the wholesale share of the market has been

declining consistently as retailers have moved to central buying and now purchase all

produce directly from suppliers.

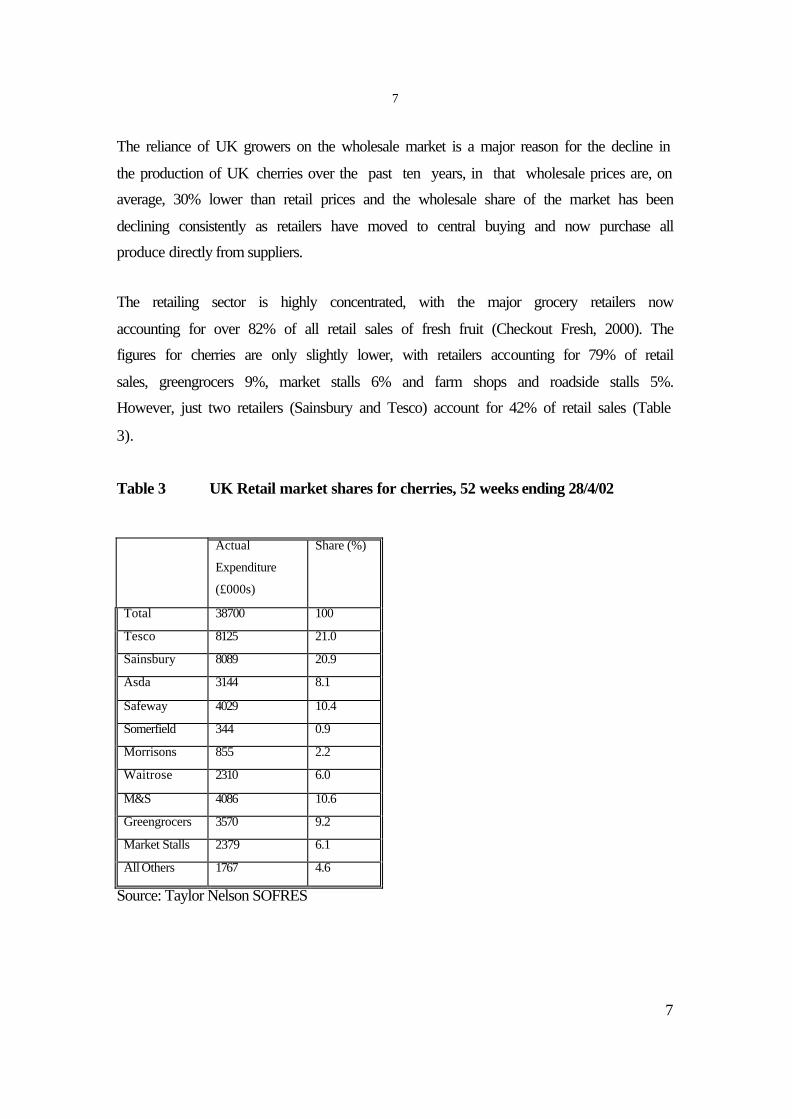

The retailing sector is highly concentrated, with the major grocery retailers now

accounting for over 82% of all retail sales of fresh fruit (Checkout Fresh, 2000). The

figures for cherries are only slightly lower, with retailers accounting for 79% of retail

sales, greengrocers 9%, market stalls 6% and farm shops and roadside stalls 5%.

However, just two retailers (Sainsbury and Tesco) account for 42% of retail sales (Table

3).

Table 3 UK Retail market shares for cherries, 52 weeks ending 28/4/02

Actual

Expenditure

(£000s)

Share (%)

Total 38700 100

Tesco 8125 21.0

Sainsbury 8089 20.9

Asda 3144 8.1

Safeway 4029 10.4

Somerfield 344 0.9

Morrisons 855 2.2

Waitrose 2310 6.0

M&S 4086 10.6

Greengrocers 3570 9.2

Market Stalls 2379 6.1

All Others 1767 4.6

Source: Taylor Nelson SOFRES

8

8

The role of fresh produce in the strategies of the major supermarkets has changed

dramatically over the past ten years, as they seek to gain competitive advantage through

the range and quality of fresh produce offered. Retail concentration, together with the

strategic importance of the fresh produce sector, has led to an increased demand for

efficiency and innovation from suppliers. The supply base has been rationalised, with the

main retailers reducing the number of fresh produce suppliers to two or less, a trend that

is now driving consolidation in the production sector. Cherries are no exception: of the

eight organizations (importers, grower/packers) that currently supply cherries to the UK

supermarkets, two account for around 80%. Similarly, while the UK production base for

cherries remains fragmented, with over 150 growers, industry observers estimate that

85% of UK production is produced by a few large growers (The Grower, 2001).

4. Key issues for stakeholders within the UK cherry supply chain

In this section we present the key findings from the semi-structured interviews

conducted with representatives from the key links in the cherry supply chain – growers,

importers/marketing organizations, retailers and a survey of final consumers.

4.1 The Growers

Cherries are mainly grown as a lucrative sideline by growers who also produce apples,

plums and pears, with an average cherry acreage of between ten and twelve hectares. The

fragmented nature of cherry production is exacerbated by a proliferation of varieties,

many of which are grown on rootstock dating back twenty five years. The short UK

cherry season lasts approximately five weeks, with the first harvest of the season starting

at the middle of June with early varieties such as ‘Early Rivers’, ‘Merchant’, ‘Sasha’,

followed by mid season varieties such as ‘Hertford’, ‘Van’, ‘Stella’, ‘Inga’. The main

production is in July when later varieties such as ‘Sunburst’, ‘Summit’, ‘Lapins’,

‘Colney’ and ‘Summersun’ are harvested and the season is now further extended into

early August with the variety ‘Sweetheart’. Rootstocks include ‘Colt’ which has been

9

9

used for 25 years, the seedling rootstock ‘Edabriz’, and on recent semi-intensive orchards

‘Gisella 5’.

The irregular cropping of cherries is considered to be the main problem with cherry

production in the UK, which is mainly due to fluctuations in the weather, soil quality,

water availability, and varietal performance. The lack of winter chilling is also considered

to be a major contributing factor to erratic cropping, given the trend towards mild

winters.

Growers first began to invest in new cherry varieties, including dwarf systems, in 1978.

With a five year lag between planting and production, environmental risk and the

increased investment required in pre-harvest technology, such as netting, covers, or wind

machines in tunnels, the production of cherries is viewed as a long term, high risk

venture.

One grower observed that larger fruit tend to taste sweeter but suffer from a shorter shelf

life. Thus, investment in post harvest technologies and the chill chain is becoming

increasingly important, and growers in the UK are aware that cherry exporting countries

have become more sophisticated, using post harvest technology such as hydrocooling and

modified atmosphere packing (MAP) to improve picking, grading, storage and

distribution.

Several growers said they preferred to sell their produce through the wholesale markets

because of the increase in picking costs and wastage associated with the quality standards

demanded by the supermarkets. They also stated that they found it very difficult to

produce cherries economically to the specifications set by marketing organisations, in

accordance with retailers’ requirements. The general perception was that picking and

wastage costs increase significantly when supplying the major retailers (one grower

suggested by as much as £0.5/lb), due to the higher standards of grading and packaging

required compared to supplying the wholesale market or the local farmer’s market. As a

result, many growers prefer to supply to the wholesale market or to regional farmer

10

10

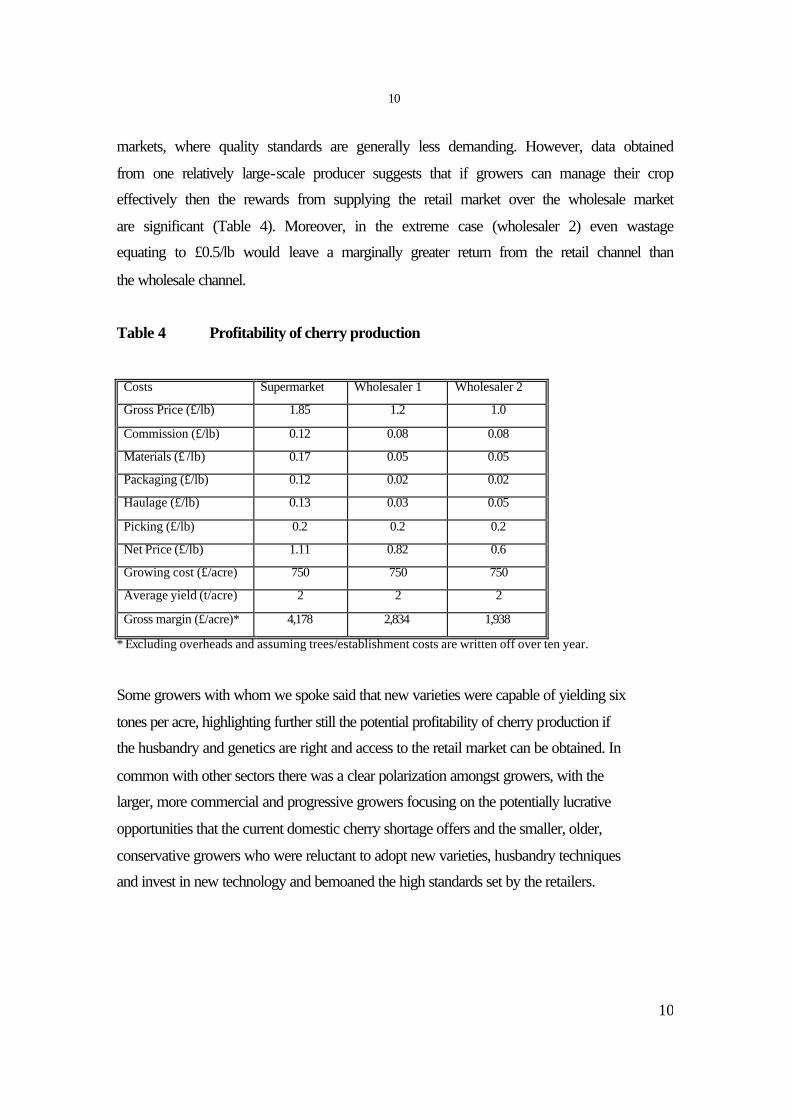

markets, where quality standards are generally less demanding. However, data obtained

from one relatively large-scale producer suggests that if growers can manage their crop

effectively then the rewards from supplying the retail market over the wholesale market

are significant (Table 4). Moreover, in the extreme case (wholesaler 2) even wastage

equating to £0.5/lb would leave a marginally greater return from the retail channel than

the wholesale channel.

Table 4 Profitability of cherry production

Costs Supermarket Wholesaler 1 Wholesaler 2

Gross Price (£/lb) 1.85 1.2 1.0

Commission (£/lb) 0.12 0.08 0.08

Materials (£ /lb) 0.17 0.05 0.05

Packaging (£/lb) 0.12 0.02 0.02

Haulage (£/lb) 0.13 0.03 0.05

Picking (£/lb) 0.2 0.2 0.2

Net Price (£/lb) 1.11 0.82 0.6

Growing cost (£/acre) 750 750 750

Average yield (t/acre) 2 2 2

Gross margin (£/acre)* 4,178 2,834 1,938

* Excluding overheads and assuming trees/establishment costs are written off over ten year.

Some growers with whom we spoke said that new varieties were capable of yielding six

tones per acre, highlighting further still the potential profitability of cherry production if

the husbandry and genetics are right and access to the retail market can be obtained. In

common with other sectors there was a clear polarization amongst growers, with the

larger, more commercial and progressive growers focusing on the potentially lucrative

opportunities that the current domestic cherry shortage offers and the smaller, older,

conservative growers who were reluctant to adopt new varieties, husbandry techniques

and invest in new technology and bemoaned the high standards set by the retailers.

11

11

4.2 Marketing Groups

The main problems with cherries, as perceived by the marketing organisations, are the

irregular cropping patterns and problems in the cool chain, including the lack of

hydrocooling. It was also observed that more accurate crop forecasting could help to

counteract imports during the UK season and that price competitiveness should not be a

critical factor.

The National Summer Fruits Association (NSFA) acts as an umbrella organisation to co-

ordinate all of the marketing groups in the interest of British summer fruit growers and

provides retailers with crop forecasts, as judged by visual inspections by individual

growers. However, these forecasts are notoriously inaccurate, which can have serious

knock-on effects on demand for the following season at the retail level. For example,

during 1997 and following a wet June, the UK industry could only supply thirty per cent

of volume demanded by the major retailers instead of the forecasted 70%. The following

year, the retailers assumed only forty per cent UK production and imported the remaining

60 per cent in order to maintain consistent supply.

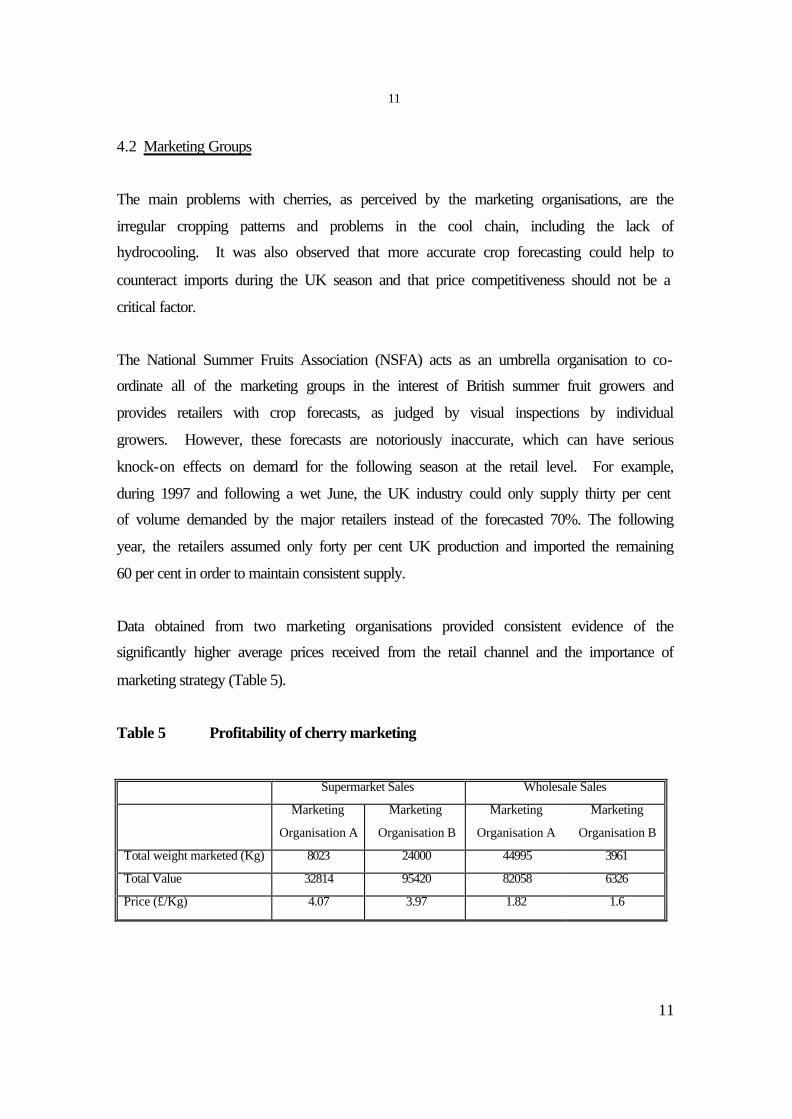

Data obtained from two marketing organisations provided consistent evidence of the

significantly higher average prices received from the retail channel and the importance of

marketing strategy (Table 5).

Table 5 Profitability of cherry marketing

Supermarket Sales Wholesale Sales

Marketing

Organisation A

Marketing

Organisation B

Marketing

Organisation A

Marketing

Organisation B

Total weight marketed (Kg) 8023 24000 44995 3961

Total Value 32814 95420 82058 6326

Price (£/Kg) 4.07 3.97 1.82 1.6

12

12

Organization A sold 83.5% of its cherries to the supermarkets compared to just 18% for

organization B, with the resulting difference in the weighted average price obtained of

£1.47/lb. Organisation B sold 11% fewer cherries in total but due to its ability to achieve

a much higher share of retail sales, the weighted average price obtained was 68% higher

than that obtained by organization A.

Effective stock rotation and presentation at the retail level were perceived as being of

great importance in any attempt to increase cherry sales. In addition, the on-going

rationalisation and concentration at the marketing organisation level was viewed as

necessary in order to achieve a more co-ordinated and focused approach in terms of

uniform marketing strategies within the UK cherry industry.

4.3 Retailers

Retailers were confident that UK customers are prepared to pay a premium for UK

cherries and that when available, UK cherries are good quality and that August is the

peak month, with consumers exhibiting a strong preference for large black cherries.

Specifications vary between retailers in terms of the tolerance for splitting, bruising,

mechanical damage, colour requirement of fruit and stalks, shelf life, pesticide useage,

age, Class, and size (24-26 mm, 26mm+). Specifications are also dependent on the

season. Retailers are supplied by between three and 15 suppliers, although one third

account for approximately 90 per cent of the total cherry market. Importers and

marketing organisations work closely together with retailer technologists and advise them

on new varieties. If importers and marketing organisations do not meet the

specifications, then the fruit is rejected by the retailers and has to be re-packed in the

packhouse and sent to the wholesale market, at considerable cost and loss of revenue to

the supplier. The costs of third party auditing are also the responsibility of the supplier.

Irregular cropping in the UK cherry industry, unreliable forecasting of volumes, inability

to meet and improve upon specifications, inconsistent eating quality and problems in the

cool chain were all identified by the retailers as issues which needed to be overcome in

13

13

order to develop the domestic industry. One retailer identified that inconsistent eating

quality due to differences in sugar level and colour negatively affected repeat purchases.

The costs associated with produce returns by consumers is met by the retailers, but

suppliers can be fined a fee for reimbursement of administration costs. This mechanism

helps monitor customer satisfaction and highlight problems, which are then

communicated along the supply chain. Some retailers also accepted that whilst produce

managers were trained in the handling and display of cherries in store, such training was

not always available for ‘front line’ produce staff.

Retailers also identified that sales of fresh fruit, including cherries, are dependent on the

weather, and that sales of soft fruit increase in hot weather, but can fall by 60% if the

weather is cold and wet, in which case promotions are critical. Sales based ordering

systems for cherries include the weather factor and previous sales volumes, but also

depend on the size of the store and the characteristics of the customer base.

We found limited evidence of a desire to develop long-term relationship between retailers

and growers although initiatives had been made by two retailers who had subsidised

investment in new varieties with selected growers, giving them greater control on quality,

varieties and a guaranteed UK supply.

4.4 Consumers

The consumer is typically portrayed as the final link in the supply chain (figure 1), as it is

at this point that the product is finally consumed. However, in a demand-driven supply

chain the consumer should also be the first link in the supply chain, as it is the wants and

needs of the consumer that should ultimately shape the decisions of all industry

stakeholders (nurserymen, growers, importers, distributors and retailers). However, in

common with most of the sectors within the fresh produce industry, and most notably

fruit, there has been very little consumer research undertaken by any stakeholders in the

cherry supply chain, to determine the extent to which their offering is consistent with

14

14

consumer needs and wants. From the perspective of UK growers this reflects the small-

scale and fragmented nature of cherry cultivation and a production orientated approach

which fails to recognize the need to effectively target consumers, particularly in the face

of such strong competition from overseas. Thus, in this penultimate section of the paper

we turn to the cherry consumer and present the key findings from our consumer research,

designed to identify the potential for developing a commercially viable niche market for

UK cherries and regaining market share from imported cherries in the highest value

supply chain – the supermarkets.

Initial qualitative research was undertaken in the Spring of 2000, in the form of consumer

focus groups, which indicated that consumers would pay a premium price for home

grown cherries, and that there was a distinct preference for large, dark, full red or black

glossy cherries, with taste being the most important attribute (Wermund & Fearne, 2000).

Subsequently, 479 face-to-face interviews with purchasers of cherries were conducted in

four regions (Manchester, Newcastle, Nottingham and the South East), with shoppers

from three supermarkets (Marks and Spencer n=163, J. Sainsbury n=162 and Asda

n=155). The questionnaire was administered2 within or at the entrance to selected stores

in each region during June and July 2000. In terms of age, 29% of the sample were less

than 34 years old, 45% were aged between 35 and 54, and 26% were 55 years and older.

The discussion of the survey results is presented in three sections: purchasing behaviour,

consumption behaviour and marketing mix.

Purchasing Behaviour

Consumers were asked when and where they usually bought cherries during the summer.

The majority of respondents, namely 62%, bought cherries on a weekly basis during the

season; 30% every two or three weeks and only eight per cent bought cherries for special

occasions. In addition, the majority of respondents (81%) had never bought cherries

2 The authors would like to thank Rodolphe Boulen, a former MSc student at Imperial College at Wye, for his contribution to the consumer research.

15

15

during the winter. Demand for cherries is therefore associated with seasonality, and is

consistently high during the main summer season. When asked where they usually

purchased their cherries during the summer, 65% of respondents bought cherries from

their usual supermarket, while just over a quarter bought cherries from the greengrocer.

The remainder bought cherries from market stalls, ‘pick your own’ venues and from other

outlets. In general, these figures reflect consumers’ shopping habits for fresh produce,

given that the supermarkets account for the majority of the retail market. In particular,

they confirm the major role played by the supermarkets in the supply chain for fresh

cherries.

In order to gain some insights into the importance consumers attach to the different

attributes of cherries, respondents were asked to select their preferred attributes for an

ideal cherry from a list of attributes generated from the focus groups. More than three

quarters of the sample preferred large cherries, whereas 21% claimed to have no

preference and only two per cent preferred small cherries. The majority of respondents

(80%) preferred cherries which were black in colour, 15% had no preference as far as

colour was concerned, and five per cent preferred red or yellow cherries. For the

overwhelming majority (88%), the sweet taste of cherries was chosen as a preferred

attribute, with nine per cent declaring they had no preference and the remaining three per

cent preferring sharp tasting cherries.

The preference for the appearance attribute of cherries was less clearly expressed, with

60% choosing ‘glossy’ and one per cent choosing ‘matt’, but 39% had no preference for

either glossy or matt cherries. Considering the results overall, it would appear that the

vast majority of consumers surveyed preferred large, black cherries that are sweet tasting,

although the preference for a glossy cherry was less evident from the survey than

indicated by the focus groups.

Significantly, given the strong preference for home-grown cherries expressed in the focus

groups, less than one third of consumer claimed that home grown cherries would be a

feature of their ideal product. The majority (60%) claimed they had no preference, and

16

16

nearly nine per cent said they would prefer imported cherries. However, it is important to

note that there were (statistically) significant regional differences, with half of the

shoppers interviewed in the South-East stating a preference for home-grown cherries,

compared to 30% in both Manchester and Nottingham and 25% in Newcastle. This is not

surprising given that the bulk of the cherry crop is produced in Kent, but it does highlight

the potential for market segmentation. Further research is needed into identifying the

desirability of other attributes such as organic production and the environmental costs

associated with air freighted fruit, which may permit more effective promotion of the

benefits of home grown fruit.

Consumption Behaviour

The majority of respondents (65%) bought cherries in punnets, with the remainder buying

loose cherries. Over 94% of the sample stated that they usually bought cherries for

themselves. Just under half also purchased them for their partner and just over a quarter

said they bought cherries for their children. This emphasizes the indulgence nature of

cherry consumption, seen by most people as a personal treat. However, the limited

exposure to children is cause for concern, as they represent the consumers of tomorrow

and may have distinctly different preferences to adults.

The manner in which cherries are consumed was also explored, and respondents

indicated that by far the most popular way to eat cherries was to eat them on their own.

In light of this, one way of adding value and increasing sales would be to offer smaller,

durable packs of cherries suitable for lunchboxes, with promotional campaigns designed

to target both adults and children. Among the 13% who claimed to enjoy cherries in a

fruit salad, the vast majority had retired and belonged to the higher socio-economic

groups, suggesting that there is scope for promotional and marketing strategies targeting

such segments with end-use in mind rather than price.

Respondents were asked why they had bought cherries on the day of the interview (Table

6). The main reason given was ‘because they tasted good the last time’, which highlights

the importance of the taste attribute in securing repeat purchases. In-store promotions

17

17

offering free tasting of cherries would appear to be the most effective way of ensuring

consumers can sample the product, and use that experience to inform their purchasing

decisions. The second most cited reason was ‘as a treat’, closely followed by

‘promotional offer’. The appearance of cherries is also an important attribute, with just

under a quarter stating the main reason for buying cherries is ‘because they look good’.

Table 6 Reasons for Buying Cherries

Reasons % of Respondents

Because they tasted good the last time 53.9

As a treat 30.9

Promotional offer 28.5

Because they look so good 24.1

Part of a healthy diet 22.8

Special occasions 1.1

Sunny weather 0.6

Part of a special diet (e.g. medicinal) 1.7

Developments in technology and packaging should be explored in order to protect the

appearance and maintain the eating quality of cherries from the point of harvest. The

health aspect of cherries was ranked fifth, with nearly 23% stating that they buy cherries

as ‘part of a healthy diet’. This latent awareness of a health aspect indicates that there is

potential for promoting the specific benefits to health of increased consumption of

perillul alcohol, a chemical that occurs naturally in cherries.

Marketing mix

Respondents were asked how likely they were to buy more cherries if their chosen

supermarket undertook certain promotional or added-value activities. The mean scores

are presented in Table 7. The results show overwhelmingly that the factor most likely to

increase consumption is a reduction in price, with more than 80% of respondents giving

this a score of 8 or above, on a scale of 1 to 10 (1 = definitely would not buy more

10 = definitely would buy more). Link promotions would also seem an effective way for

retailers to increase sales, perhaps with yoghurts and other seasonal or stone fruits. In

18

18

contrast, offering stoneless, stalkless or organic cherries, and increased product

information would appear to have no effect on increasing the amount of cherries bought

within the chosen supermarket. However, there were still in excess of fifteen per cent of

respondents who did view an organic offering as important, a result which may well

signal niche opportunities for some growers wishing to invest in organic production.

Further research is needed to determine whether such a target market would be willing to

pay an adequate price premium.

Table 7 Mean Score of Factors likely to increase Consumption of Cherries

Possible Actions Mean Score

Reduce the price 8.4

Promote cherries as a link purchase 5.3

Offer stoneless cherries 3.6

Offer organic cherries 3.2

Give new serving suggestions 3.2

Offer stalkless cherries 2.2

1 = definitely would not buy more, 10 = definitely would buy more

The final section of the questionnaire contained a series of statements, against which

respondents were asked to indicate their level of agreement/disagreement on a Likert

scale (1=strongly disagree, 5=strongly agree). The mean scores are presented in Table 8.

With a mean score in excess of 4, 90% of the sample agreed or strongly agreed with the

statement ‘I enjoy buying fruit’ and three quarters of the sample agreed with the

statement ‘I buy cherries as a treat for myself’. Over two thirds of the sample agreed and

only 23% disagreed with the statement ‘I would never buy cherries with blemishes’,

indicating the need for all members of the supply chain to work together to produce

blemish-free products. Three quarters of respondents disagreed with the statement ‘I

would never buy cherries with brown stalks’ but just over a quarter did agree.

19

19

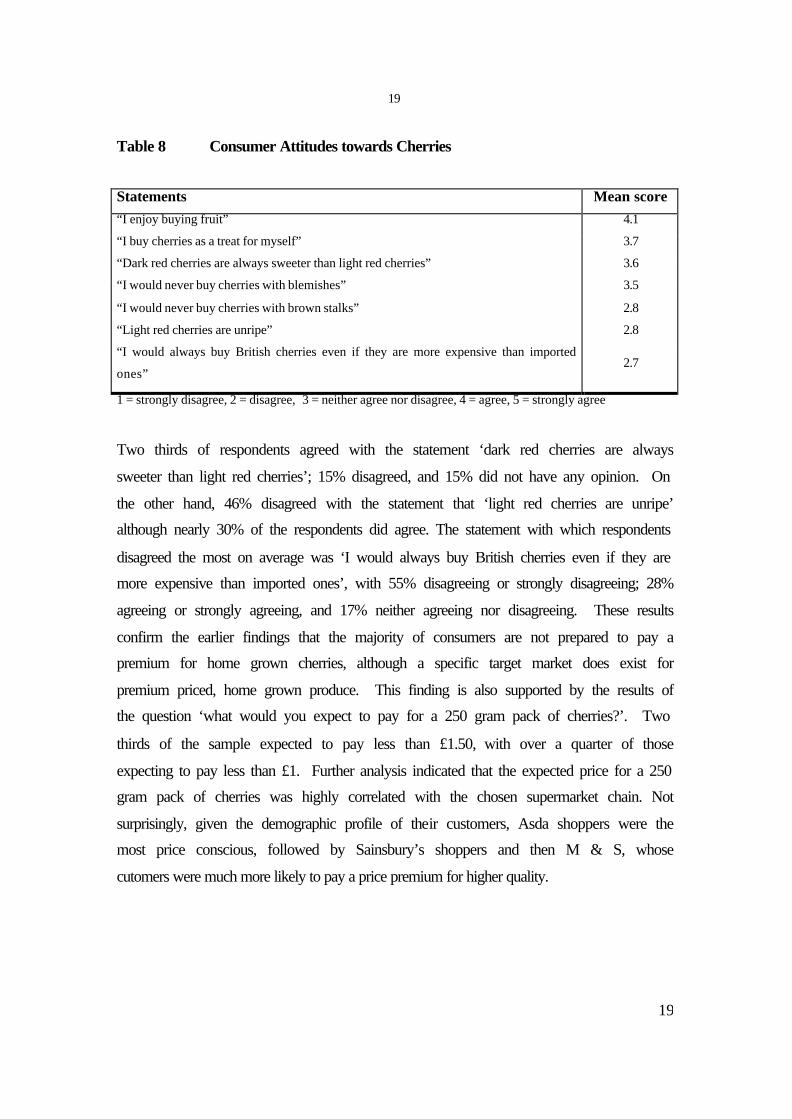

Table 8 Consumer Attitudes towards Cherries

Statements Mean score

“I enjoy buying fruit” 4.1

“I buy cherries as a treat for myself” 3.7

“Dark red cherries are always sweeter than light red cherries” 3.6

“I would never buy cherries with blemishes” 3.5

“I would never buy cherries with brown stalks” 2.8

“Light red cherries are unripe” 2.8

“I would always buy British cherries even if they are more expensive than imported

ones” 2.7

1 = strongly disagree, 2 = disagree, 3 = neither agree nor disagree, 4 = agree, 5 = strongly agree

Two thirds of respondents agreed with the statement ‘dark red cherries are always

sweeter than light red cherries’; 15% disagreed, and 15% did not have any opinion. On

the other hand, 46% disagreed with the statement that ‘light red cherries are unripe’

although nearly 30% of the respondents did agree. The statement with which respondents

disagreed the most on average was ‘I would always buy British cherries even if they are

more expensive than imported ones’, with 55% disagreeing or strongly disagreeing; 28%

agreeing or strongly agreeing, and 17% neither agreeing nor disagreeing. These results

confirm the earlier findings that the majority of consumers are not prepared to pay a

premium for home grown cherries, although a specific target market does exist for

premium priced, home grown produce. This finding is also supported by the results of

the question ‘what would you expect to pay for a 250 gram pack of cherries?’. Two

thirds of the sample expected to pay less than £1.50, with over a quarter of those

expecting to pay less than £1. Further analysis indicated that the expected price for a 250

gram pack of cherries was highly correlated with the chosen supermarket chain. Not

surprisingly, given the demographic profile of their customers, Asda shoppers were the

most price conscious, followed by Sainsbury’s shoppers and then M & S, whose

cutomers were much more likely to pay a price premium for higher quality.

20

20

5. Conclusions

This exploratory study – the first of its kind to focus specifically on the cherry supply

chain, has revealed a number of key challenges which need to be overcome by the UK

cherry industry if UK growers are to gain a greater share of the UK retail market. The

main problem associated with the production of cherries in the UK is irregular cropping,

mainly due to fluctuations in the weather and varietal performance. Cherries are highly

perishable, and fast handling is required. In the UK, the time window between harvest

and supply to the retailer or wholesale market is between one and two days. The

development of new varieties to extend the season for home grown produce, together

with pre-harvest innovations and improvements in post harvest technologies and the cool

chain, are viewed as key requirements to withstand the competition from imports during

the peak season in July/August. Closer co-operation and co-ordination between all

stakeholders is also viewed as a key challenge for the industry, to improve supply

forecasts and demand management – more effectively and efficiently meeting the needs

of UK consumers to the benefit of all stakeholders in the supply chain.

It would appear that consumers view cherries as an indulgence, a summer treat for

everyone in the family. The preferred cherry is large, black and sweet, with taste

considered paramount, but the results show that, contrary to industry assumptions, the

majority of consumers are not prepared to pay a price premium for home grown cherries.

In addition, competitive pricing would appear to be the most effective way of increasing

consumption. However, consumers are not homogeneous, and the survey suggests that

different market segments could be developed. Furthermore, effective promotions which

form part of a targeted marketing strategy should be designed in order to target different

market segments, with price just one of many instruments that can be used to stimulate

demand.

The implications for the supply chain for cherries are clear, and reflect the changes

already taking place elsewhere in the fresh produce industry. The production base is

fragmented and investment is needed to fund research in new varieties to minimise

21

21

environmental risk, improve technology and material flow within the supply chain. The

preferred distribution channel for cherries would appear to be the multiple retailers, but

only approximately one fifth of current production is reaching consumers direct through

the retail market, with the majority sold via wholesale. The major multiples view fresh

produce as a destination category, and have invested heavily in information technology

systems, and extensive and integrated chill chain operations in order to reduce costs in

the supply chain, and increase the quality of the product at the point of sale. In order to

take advantage of such investment, there is an urgent need for closer and more co-

ordinated relationships throughout the domestic supply chain, but particular at the

production level. Larger, specialised cherry growers, or groups of growers, who are

dedicated to trial and produce crops destined for specific supermarkets will be best placed

to respond to this challenge and capture the benefits.

22

22

REFERENCES

Checkout Fresh (2000). Market Review 1999-2000.

Department of the Environment, Food and Rural Affairs. 2001. Basic Horticultural

Statistics for the UK – Calendar and Crop Years 1990/91 – 2000/01.

Fearne, A. and Hughes, D. (2000) Success factors in the fresh produce supply chain,

British Food Journal, Vol. 102, No. 10, p. 760-772

Fresh Produce Journal, (2000). Desk Book 2000

The Grower. 2000. 8 June, Week 23, p.8.

The Grower. 2001. 16 August, p.3.

Wermund, U. & Fearne, A. 2000. Key challenges facing the cherry supply chain in the

UK, Paper presented at the 14th International Symposium of Horticultural Economics,

Guernsey, September 12-15, 2000, published by the ISHS, Acta Horticulturae, No.536,

pp613-624.