operational risk (e) subgroup of the capital … · alan seeley, chair new mexico richard ford...

TRANSCRIPT

© 2016 National Association of Insurance Commissioners

2/2/17 Conference Call

OPERATIONAL RISK (E) SUBGROUP

OF THE CAPITAL ADEQUACY (E) TASK FORCE Monday, February 13, 2017

Noon ET / 11:00 AM CT / 10:00 AM MT / 9:00AM PT

ROLL CALL

Alan Seeley, Chair New Mexico Richard Ford Alabama Ron Dahlquist California Chris Buchanan John Robinson

Kansas Minnesota

Anna Taam/Stephen Wiest New York John Doak/Joel Sander Oklahoma Steven Drutz/Patrick McNaughton Washington Tom Houston Wisconsin

AGENDA

1. Continue discussion of structural changes and factor for basic operational risk “add-on” a. Exposed structure for “add-on” Attachment 1 b. Treatment of affiliate risk Attachment 2 c. Treatment of growth risk Attachment 2

2. Further discussion of deleting the informational P/C RBC growth risk page Attachments 3 & 4

3. Other matters brought before the Subgroup 4. Adjournment

w:\qa\rbc\oprsg\2017\Feb\2_23 open call\op risk agenda.docx

2016 National Association of Insurance Commissioners

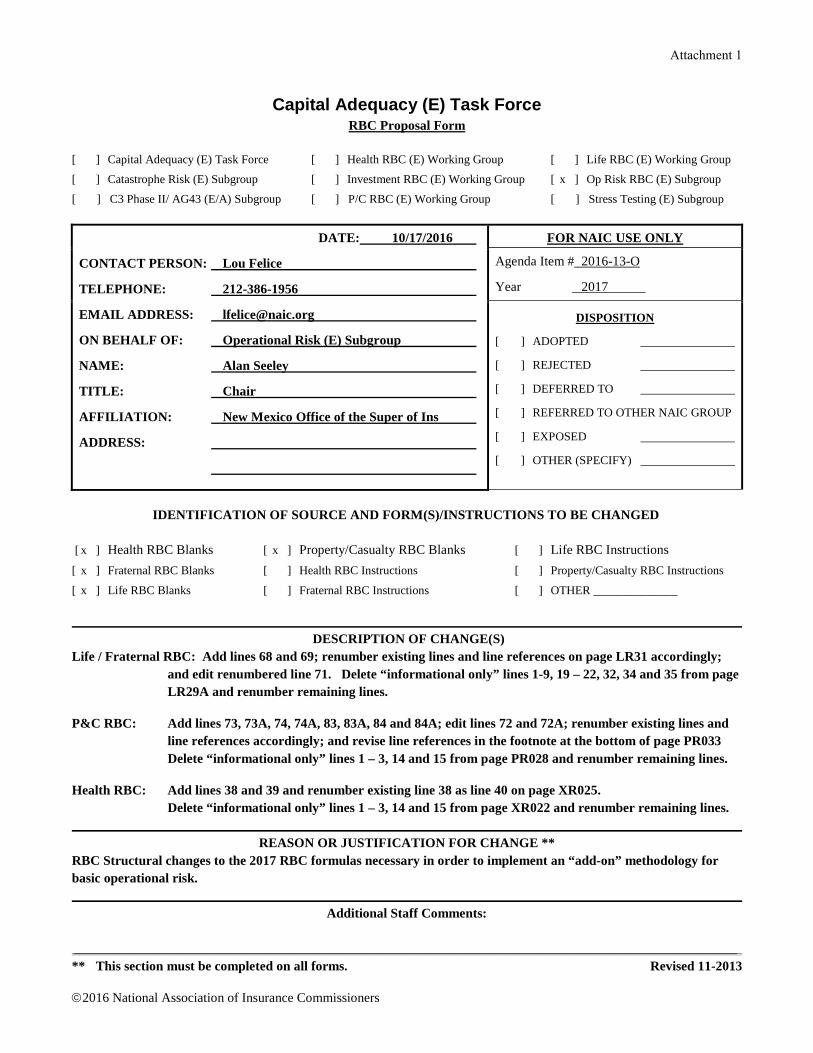

Capital Adequacy (E) Task Force

RBC Proposal Form [ ] Capital Adequacy (E) Task Force [ ] Health RBC (E) Working Group [ ] Life RBC (E) Working Group

[ ] Catastrophe Risk (E) Subgroup [ ] Investment RBC (E) Working Group [ x ] Op Risk RBC (E) Subgroup

[ ] C3 Phase II/ AG43 (E/A) Subgroup [ ] P/C RBC (E) Working Group [ ] Stress Testing (E) Subgroup

DATE: 10/17/2016

CONTACT PERSON: Lou Felice

TELEPHONE: 212-386-1956

EMAIL ADDRESS: [email protected]

ON BEHALF OF: Operational Risk (E) Subgroup

NAME: Alan Seeley

TITLE: Chair

AFFILIATION: New Mexico Office of the Super of Ins

ADDRESS:

FOR NAIC USE ONLY

Agenda Item # 2016-13-O

Year 2017

DISPOSITION

[ ] ADOPTED

[ ] REJECTED

[ ] DEFERRED TO

[ ] REFERRED TO OTHER NAIC GROUP

[ ] EXPOSED

[ ] OTHER (SPECIFY)

IDENTIFICATION OF SOURCE AND FORM(S)/INSTRUCTIONS TO BE CHANGED [ x ] Health RBC Blanks [ x ] Property/Casualty RBC Blanks [ ] Life RBC Instructions

[ x ] Fraternal RBC Blanks [ ] Health RBC Instructions [ ] Property/Casualty RBC Instructions

[ x ] Life RBC Blanks [ ] Fraternal RBC Instructions [ ] OTHER ______________

DESCRIPTION OF CHANGE(S) Life / Fraternal RBC: Add lines 68 and 69; renumber existing lines and line references on page LR31 accordingly;

and edit renumbered line 71. Delete “informational only” lines 1-9, 19 – 22, 32, 34 and 35 from page LR29A and renumber remaining lines.

P&C RBC: Add lines 73, 73A, 74, 74A, 83, 83A, 84 and 84A; edit lines 72 and 72A; renumber existing lines and

line references accordingly; and revise line references in the footnote at the bottom of page PR033 Delete “informational only” lines 1 – 3, 14 and 15 from page PR028 and renumber remaining lines.

Health RBC: Add lines 38 and 39 and renumber existing line 38 as line 40 on page XR025.

Delete “informational only” lines 1 – 3, 14 and 15 from page XR022 and renumber remaining lines.

REASON OR JUSTIFICATION FOR CHANGE ** RBC Structural changes to the 2017 RBC formulas necessary in order to implement an “add-on” methodology for basic operational risk.

Additional Staff Comments:

___________________________________________________________________________________________________ ** This section must be completed on all forms. Revised 11-2013

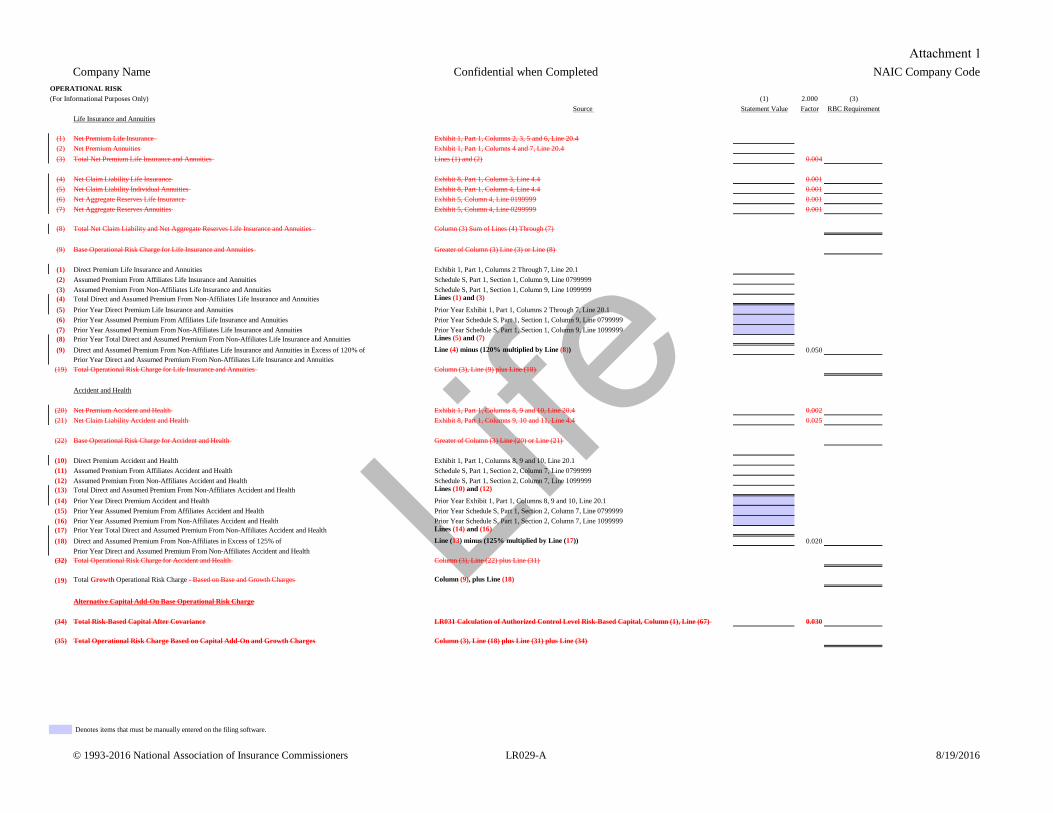

Attachment 1

Life

Company Name Confidential when Completed NAIC Company Code

© 1993-2016 National Association of Insurance Commissioners LR029-A 8/19/2016

OPERATIONAL RISK (For Informational Purposes Only) (1) 2.000 (3)

Source Statement Value Factor RBC RequirementLife Insurance and Annuities

(1) Net Premium Life Insurance Exhibit 1, Part 1, Columns 2, 3, 5 and 6, Line 20.4(2) Net Premium Annuities Exhibit 1, Part 1, Columns 4 and 7, Line 20.4(3) Total Net Premium Life Insurance and Annuities Lines (1) and (2) 0.004

(4) Net Claim Liability Life Insurance Exhibit 8, Part 1, Column 3, Line 4.4 0.001(5) Net Claim Liability Individual Annuities Exhibit 8, Part 1, Column 4, Line 4.4 0.001(6) Net Aggregate Reserves Life Insurance Exhibit 5, Column 4, Line 0199999 0.001(7) Net Aggregate Reserves Annuities Exhibit 5, Column 4, Line 0299999 0.001

(8) Total Net Claim Liability and Net Aggregate Reserves Life Insurance and Annuities Column (3) Sum of Lines (4) Through (7)

(9) Base Operational Risk Charge for Life Insurance and Annuities Greater of Column (3) Line (3) or Line (8)

(1) Direct Premium Life Insurance and Annuities Exhibit 1, Part 1, Columns 2 Through 7, Line 20.1(2) Assumed Premium From Affiliates Life Insurance and Annuities Schedule S, Part 1, Section 1, Column 9, Line 0799999(3) Assumed Premium From Non-Affiliates Life Insurance and Annuities Schedule S, Part 1, Section 1, Column 9, Line 1099999(4) Total Direct and Assumed Premium From Non-Affiliates Life Insurance and Annuities Lines (1) and (3)

(5) Prior Year Direct Premium Life Insurance and Annuities Prior Year Exhibit 1, Part 1, Columns 2 Through 7, Line 20.1(6) Prior Year Assumed Premium From Affiliates Life Insurance and Annuities Prior Year Schedule S, Part 1, Section 1, Column 9, Line 0799999(7) Prior Year Assumed Premium From Non-Affiliates Life Insurance and Annuities Prior Year Schedule S, Part 1, Section 1, Column 9, Line 1099999(8) Prior Year Total Direct and Assumed Premium From Non-Affiliates Life Insurance and Annuities Lines (5) and (7)

(9) Direct and Assumed Premium From Non-Affiliates Life Insurance and Annuities in Excess of 120% of Line (4) minus (120% multiplied by Line (8)) 0.050Prior Year Direct and Assumed Premium From Non-Affiliates Life Insurance and Annuities

(19) Total Operational Risk Charge for Life Insurance and Annuities Column (3), Line (9) plus Line (18)

Accident and Health

(20) Net Premium Accident and Health Exhibit 1, Part 1, Columns 8, 9 and 10, Line 20.4 0.002(21) Net Claim Liability Accident and Health Exhibit 8, Part 1, Columns 9, 10 and 11, Line 4.4 0.025

(22) Base Operational Risk Charge for Accident and Health Greater of Column (3) Line (20) or Line (21)

(10) Direct Premium Accident and Health Exhibit 1, Part 1, Columns 8, 9 and 10, Line 20.1(11) Assumed Premium From Affiliates Accident and Health Schedule S, Part 1, Section 2, Column 7, Line 0799999(12) Assumed Premium From Non-Affiliates Accident and Health Schedule S, Part 1, Section 2, Column 7, Line 1099999(13) Total Direct and Assumed Premium From Non-Affiliates Accident and Health Lines (10) and (12)

(14) Prior Year Direct Premium Accident and Health Prior Year Exhibit 1, Part 1, Columns 8, 9 and 10, Line 20.1(15) Prior Year Assumed Premium From Affiliates Accident and Health Prior Year Schedule S, Part 1, Section 2, Column 7, Line 0799999(16) Prior Year Assumed Premium From Non-Affiliates Accident and Health Prior Year Schedule S, Part 1, Section 2, Column 7, Line 1099999(17) Prior Year Total Direct and Assumed Premium From Non-Affiliates Accident and Health Lines (14) and (16)

(18) Direct and Assumed Premium From Non-Affiliates in Excess of 125% of Line (13) minus (125% multiplied by Line (17)) 0.020Prior Year Direct and Assumed Premium From Non-Affiliates Accident and Health

(32) Total Operational Risk Charge for Accident and Health Column (3), Line (22) plus Line (31)

(19) Total Growth Operational Risk Charge - Based on Base and Growth Charges Column (9), plus Line (18)

Alternative Capital Add-On Base Operational Risk Charge

(34) Total Risk-Based Capital After Covariance LR031 Calculation of Authorized Control Level Risk-Based Capital, Column (1), Line (67) 0.030

(35) Total Operational Risk Charge Based on Capital Add-On and Growth Charges Column (3), Line (18) plus Line (31) plus Line (34)

Denotes items that must be manually entered on the filing software.

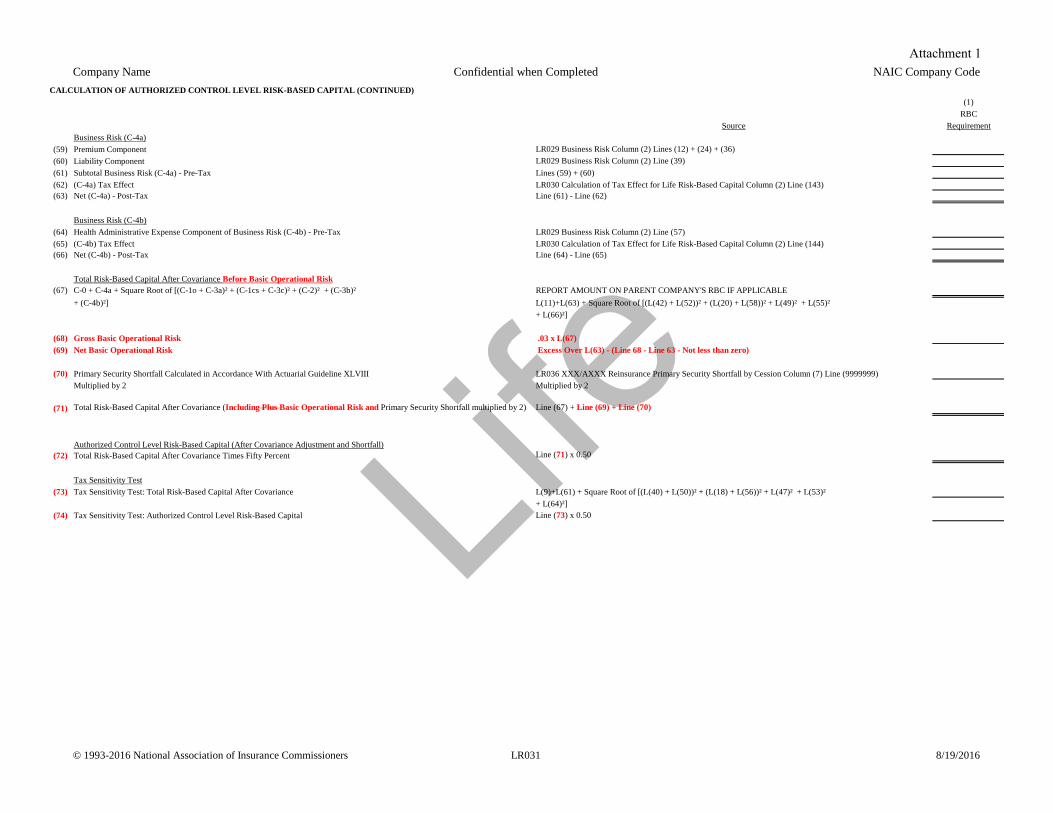

Attachment 1

Life

Company Name Confidential when Completed NAIC Company Code

© 1993-2016 National Association of Insurance Commissioners LR031 8/19/2016

CALCULATION OF AUTHORIZED CONTROL LEVEL RISK-BASED CAPITAL (CONTINUED)(1)

RBCSource Requirement

Business Risk (C-4a)(59) Premium Component LR029 Business Risk Column (2) Lines (12) + (24) + (36)(60) Liability Component LR029 Business Risk Column (2) Line (39)(61) Subtotal Business Risk (C-4a) - Pre-Tax Lines (59) + (60) (62) (C-4a) Tax Effect LR030 Calculation of Tax Effect for Life Risk-Based Capital Column (2) Line (143)(63) Net (C-4a) - Post-Tax Line (61) - Line (62)

Business Risk (C-4b)(64) Health Administrative Expense Component of Business Risk (C-4b) - Pre-Tax LR029 Business Risk Column (2) Line (57)(65) (C-4b) Tax Effect LR030 Calculation of Tax Effect for Life Risk-Based Capital Column (2) Line (144)(66) Net (C-4b) - Post-Tax Line (64) - Line (65)

Total Risk-Based Capital After Covariance Before Basic Operational Risk(67) C-0 + C-4a + Square Root of [(C-1o + C-3a)² + (C-1cs + C-3c)² + (C-2)² + (C-3b)² REPORT AMOUNT ON PARENT COMPANY'S RBC IF APPLICABLE

+ (C-4b)²] L(11)+L(63) + Square Root of [(L(42) + L(52))² + (L(20) + L(58))² + L(49)² + L(55)² + L(66)²]

(68) Gross Basic Operational Risk .03 x L(67)(69) Net Basic Operational Risk Excess Over L(63) - (Line 68 - Line 63 - Not less than zero)

(70) Primary Security Shortfall Calculated in Accordance With Actuarial Guideline XLVIII LR036 XXX/AXXX Reinsurance Primary Security Shortfall by Cession Column (7) Line (9999999)Multiplied by 2 Multiplied by 2

(71) Total Risk-Based Capital After Covariance (Including Plus Basic Operational Risk and Primary Security Shortfall multiplied by 2) Line (67) + Line (69) + Line (70)

Authorized Control Level Risk-Based Capital (After Covariance Adjustment and Shortfall)(72) Total Risk-Based Capital After Covariance Times Fifty Percent Line (71) x 0.50

Tax Sensitivity Test(73) Tax Sensitivity Test: Total Risk-Based Capital After Covariance L(9)+L(61) + Square Root of [(L(40) + L(50))² + (L(18) + L(56))² + L(47)² + L(53)²

+ L(64)²](74) Tax Sensitivity Test: Authorized Control Level Risk-Based Capital Line (73) x 0.50

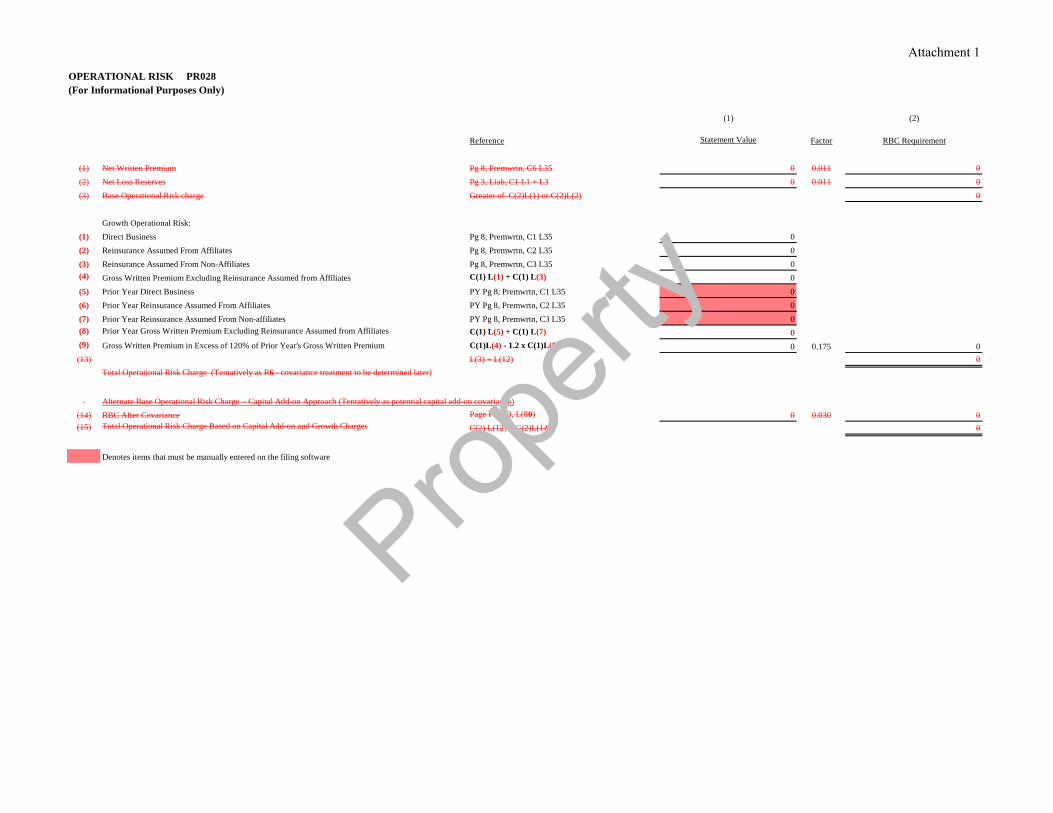

Attachment 1

OPERATIONAL RISK PR028(For Informational Purposes Only)

(1) (2)

Reference Statement Value Factor RBC Requirement

(1) Net Written Premium Pg 8, Premwrtn, C6 L35 0 0.011 0(2) Net Loss Reserves Pg 3, Liab, C1 L1 + L3 0 0.011 0(3) Base Operational Risk charge Greater of C(2)L(1) or C(2)L(2) 0

Growth Operational Risk:(1) Direct Business Pg 8, Premwrtn, C1 L35 0(2) Reinsurance Assumed From Affiliates Pg 8, Premwrtn, C2 L35 0(3) Reinsurance Assumed From Non-Affiliates Pg 8, Premwrtn, C3 L35 0(4) Gross Written Premium Excluding Reinsurance Assumed from Affiliates C(1) L(1) + C(1) L(3) 0(5) Prior Year Direct Business PY Pg 8, Premwrtn, C1 L35 0(6) Prior Year Reinsurance Assumed From Affiliates PY Pg 8, Premwrtn, C2 L35 0(7) Prior Year Reinsurance Assumed From Non-affiliates PY Pg 8, Premwrtn, C3 L35 0(8) Prior Year Gross Written Premium Excluding Reinsurance Assumed from Affiliates C(1) L(5) + C(1) L(7) 0(9) Gross Written Premium in Excess of 120% of Prior Year's Gross Written Premium C(1)L(4) - 1.2 x C(1)L(8) 0 0.175 0(13) L(3) + L(12) 0

Alternate Base Operational Risk Charge - Capital Add-on Approach (Tentatively as potential capital add-on covariance)(14) RBC After Covariance Page PR033, L(80) 0 0.030 0(15) Total Operational Risk Charge Based on Capital Add-on and Growth Charges C(2) L(12) + C(2)L(14) 0

Denotes items that must be manually entered on the filing software

Total Operational Risk Charge (Tentatively as R6 - covariance treatment to be determined later)

Propert

y

Attachment 1

Calculation of Total Risk-Based Capital After Covariance PR033 R4-Rcat(1)

R4 - Underwriting Risk - Reserves PRBC O&I Reference RBC Amount(62) One half of Reinsurance RBC If R4 L(63)>(R3 L(57) + R3 L(58)), R3 L(58), otherwise, 0 0

(62A) One half of Reinsurance RBC (For Informational Puposes Only) If R4 L(63)>(R3 L(57) + R3 L(58A)), R3 L(58A), otherwise, 0 0(63) 'Total Adjusted Unpaid Loss/Expense Reserve RBC 'PR017 L(15)C(20)(64) Excessive Premium Growth - Loss/Expense Reserve PR016 L(13) C(8) 0(65) A&H Claims Reserves Adjusted for LCF PR024 L(5) C(2) + PR023 L(6) C(4) 0

(66) Total R4 L(62)+L(63)+L(64)+L(65) 0(66A) L(62A)+L(63)+L(64)+L(65) 0

R5 - Underwriting Risk - Net Written Premium(67) Total Adjusted NWP RBC PR018 L(15)C(20) 0(68) Excessive Premium Growth - Written Premiums Charge PR016 L(14)C(8) 0(69) Total Net Health Premium RBC PR022 L(21)C(2) 0(70) Health Stabilization Reserves PR025 L(8)C(2) + PR023 L(3) C(2) 0

(71) Total R5 L(67)+L(68)+L(69)+L(70) 0

(72) Total RBC After Covariance excluding Catastrophe Risk Before Basic Operational Risk = R0+SQRT(R1^2+R2^2+R3^2+R4^2+R5^2) 0(72A)* Total RBC After Covariance excluding Catastrophe Risk Before Basic Operational Risk = R0+SQRT(R1^2+R2^2+R3A^2+R4A^2+R5^2) (For Informational Puposes Only) 0

(73) Basic Operational Risk = .03 x L(72) 0(73A)* Basic Operational Risk = .03 x L(72A) (For Informational Puposes Only) 0

(74) Total RBC After Covariance excluding Catastrophe Risk and Including Basic Operational Risk = L72 + L73(74A)* Total RBC After Covariance excluding Catastrophe Risk and Including Basic Operational Risk = L72A + L73A 0

(75) Authorized Control Level RBC excluding Catastrophe Risk = .5 x L(74) 0(75A)* Authorized Control Level RBC excluding Catastrophe Risk = .5 x (L74A) (For Informational Puposes Only) 0

For Informational Purposes Only

R5A - Underwriting Risk - Net Written Premium(76) Total Adjusted NWP RBC PR018A L(15)C(20) 0(77) Excessive Premium Growth - Written Premiums Charge PR016 L(14)C(8) 0(78) Total Net Health Premium RBC PR022 L(21)C(2) 0(79) Health Stabilization Reserves PR025 L(8)C(2) + PR023 L(3) C(2) 0

(80) Total R5A L(76)+L(77)+L(78)+L(79) 0

Rcat - Catastrophe Risk (81) Total Rcat PR027 L(3) C(1) 0

(82) Total RBC After Covariance including Catastrophe Risk Before Basic Operational risk = R0A+SQRT(R1A^2+R2A^2+R3^2+R4^2+R5A^2+Rcat^2) 0(82A)* Total RBC After Covariance including Catastrophe Risk Before Basic Operational Risk = R0A+SQRT(R1A^2+R2A^2+R3A^2+R4A^2+R5A^2+Rcat^2) 0

(83) BasicOperational Risk = .03 x L(82) 0(83A)* Basic Operational Risk = .03 x L(82A) 0

(84) Total RBC After Covariance including Catastrophe Risk and Basic Operational risk = L82 + L83 lop 0(84A)* Total RBC After Covariance including Catastrophe Risk and Basic Operational Risk = L82A + L83A 0

(85) Authorized Control Level RBC including Catastrophe Risk = .5 x L84 0(85A)* Authorized Control Level RBC including Catastrophe Risk = .5 x L84A 0

* Lines 72A, 73A, 74A, 75A, 82A, 83A, 84A and Line 85A reflect the implementation of recently approved credit risk charges for reinsurance recoverable

Total R4A (For Informational Puposes Only)

Propert

y

Attachment 1

Health

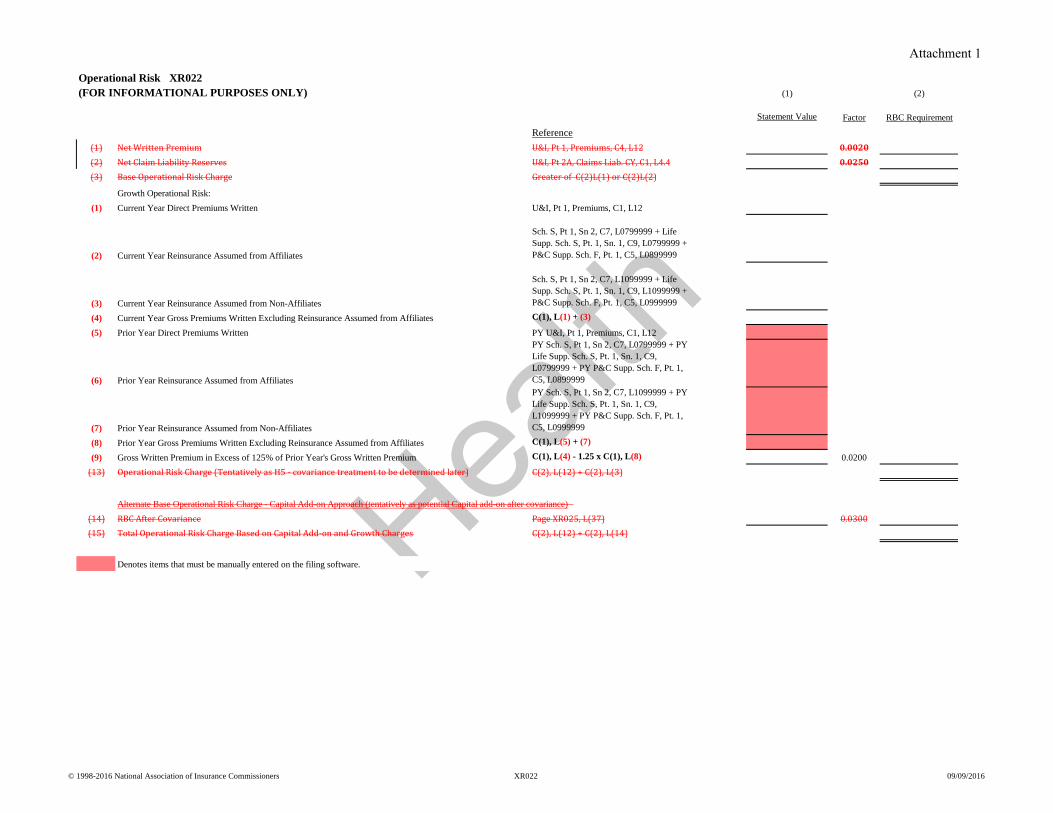

© 1998-2016 National Association of Insurance Commissioners XR022 09/09/2016

Operational Risk XR022(FOR INFORMATIONAL PURPOSES ONLY) (1) (2)

Statement Value Factor RBC Requirement

Reference(1) Net Written Premium U&I, Pt 1, Premiums, C4, L12 0.0020(2) Net Claim Liability Reserves U&I, Pt 2A, Claims Liab. CY, C1, L4.4 0.0250(3) Base Operational Risk Charge Greater of C(2)L(1) or C(2)L(2)

Growth Operational Risk:(1) Current Year Direct Premiums Written U&I, Pt 1, Premiums, C1, L12

(2) Current Year Reinsurance Assumed from Affiliates

Sch. S, Pt 1, Sn 2, C7, L0799999 + Life Supp. Sch. S, Pt. 1, Sn. 1, C9, L0799999 + P&C Supp. Sch. F, Pt. 1, C5, L0899999

(3) Current Year Reinsurance Assumed from Non-Affiliates

Sch. S, Pt 1, Sn 2, C7, L1099999 + Life Supp. Sch. S, Pt. 1, Sn. 1, C9, L1099999 + P&C Supp. Sch. F, Pt. 1, C5, L0999999

(4) Current Year Gross Premiums Written Excluding Reinsurance Assumed from Affiliates C(1), L(1) + (3)

(5) Prior Year Direct Premiums Written PY U&I, Pt 1, Premiums, C1, L12

(6) Prior Year Reinsurance Assumed from Affiliates

PY Sch. S, Pt 1, Sn 2, C7, L0799999 + PY Life Supp. Sch. S, Pt. 1, Sn. 1, C9, L0799999 + PY P&C Supp. Sch. F, Pt. 1, C5, L0899999

(7) Prior Year Reinsurance Assumed from Non-Affiliates

PY Sch. S, Pt 1, Sn 2, C7, L1099999 + PY Life Supp. Sch. S, Pt. 1, Sn. 1, C9, L1099999 + PY P&C Supp. Sch. F, Pt. 1, C5, L0999999

(8) Prior Year Gross Premiums Written Excluding Reinsurance Assumed from Affiliates C(1), L(5) + (7)

(9) Gross Written Premium in Excess of 125% of Prior Year's Gross Written Premium C(1), L(4) - 1.25 x C(1), L(8) 0.0200(13) Operational Risk Charge (Tentatively as H5 - covariance treatment to be determined later) C(2), L(12) + C(2), L(3)

Alternate Base Operational Risk Charge - Capital Add-on Approach (tentatively as potential Capital add-on after covariance)(14) RBC After Covariance Page XR025, L(37) 0.0300(15) Total Operational Risk Charge Based on Capital Add-on and Growth Charges C(2), L(12) + C(2), L(14)

Denotes items that must be manually entered on the filing software.

Attachment 1

Health

© 1998-2016 National Association of Insurance Commissioners XR025 09/09/2016

CALCULATION OF TOTAL RISK-BASED CAPITAL AFTER COVARIANCE(1)

RBC AmountH3 - CREDIT RISK

(28) Total Reinsurance RBC XR019, Credit Risk Page, L(21)(29) Intermediaries Credit Risk RBC XR019, Credit Risk Page, L(28)(30) Total Other Receivables RBC XR020, Credit Risk Page, L(34)(31) Total H3 Sum L(28) through L(30)

H4 - BUSINESS RISK(32) Administrative Expense RBC XR021, Business Risk Page, L(7)(33) Non-Underwritten and Limited Risk Business RBC XR021, Business Risk Page, L(11)(34) Premiums Subject to Guaranty Fund Assessments XR021, Business Risk Page, L(12)

(35) Excessive Growth RBC XR021, Business Risk Page, L(19)(36) Total H4 Sum L(32) through L(35)

(37) RBC after Covariance Before Basic Operational Risk H0 + Square Root of (H12+H22+H32+H42)(38) Basic Operational Risk .03 x Line (37)(39) RBC After Covariance Including Basic Operational Risk Line (37) x Line (38)(40) Authorized Control Level RBC .50 x Line (39)

Denotes items that must be manually entered on filing software.

Attachment 1

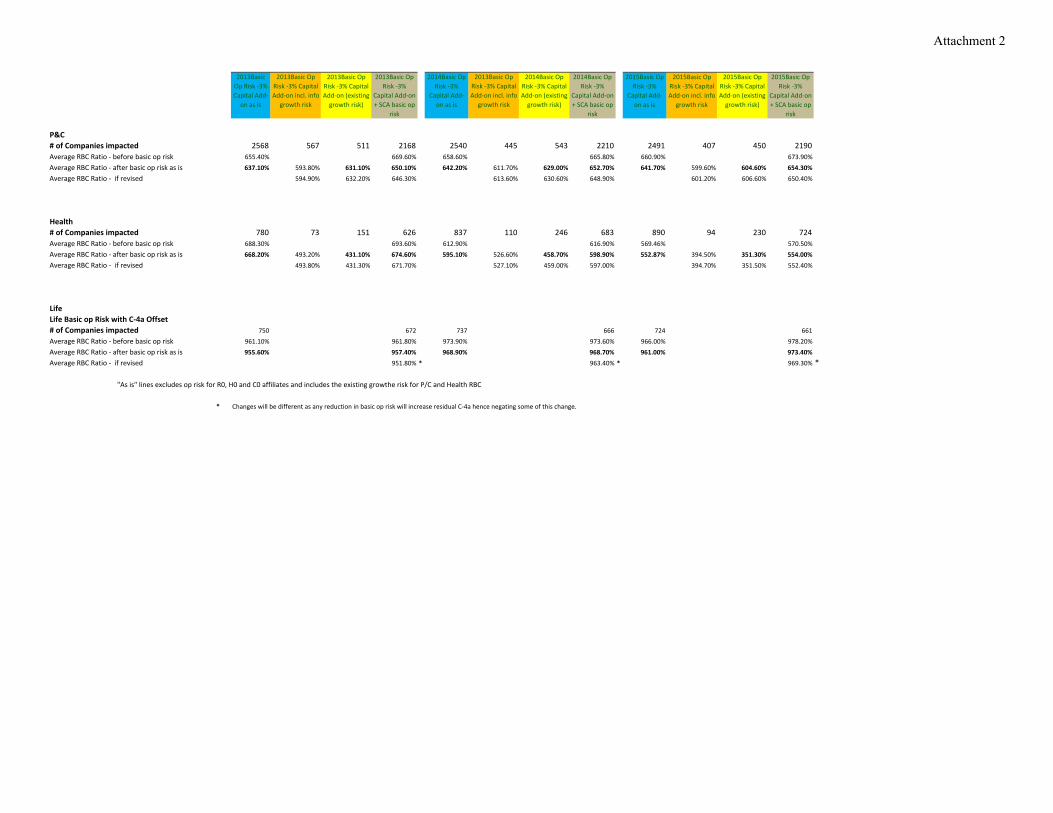

P&C# of Companies impacted 2568 567 511 2168 2540 445 543 2210 2491 407 450 2190

655.40% 669.60% 658.60% 665.80% 660.90% 673.90%637.10% 593.80% 631.10% 650.10% 642.20% 611.70% 629.00% 652.70% 641.70% 599.60% 604.60% 654.30%

594.90% 632.20% 646.30% 613.60% 630.60% 648.90% 601.20% 606.60% 650.40%

Health# of Companies impacted 780 73 151 626 837 110 246 683 890 94 230 724

688.30% 693.60% 612.90% 616.90% 569.46% 570.50%668.20% 493.20% 431.10% 674.60% 595.10% 526.60% 458.70% 598.90% 552.87% 394.50% 351.30% 554.00%

493.80% 431.30% 671.70% 527.10% 459.00% 597.00% 394.70% 351.50% 552.40%

LifeLife Basic op Risk with C‐4a Offset# of Companies impacted 750 672 737 666 724 661

961.10% 961.80% 973.90% 973.60% 966.00% 978.20%955.60% 957.40% 968.90% 968.70% 961.00% 973.40%

951.80% * 963.40% * 969.30% *

"As is" lines excludes op risk for R0, H0 and C0 affiliates and includes the existing growthe risk for P/C and Health RBC

* Changes will be different as any reduction in basic op risk will increase residual C‐4a hence negating some of this change.

Average RBC Ratio ‐ if revised

2015Basic Op Risk ‐3% Capital Add‐on incl. info

growth risk

Average RBC Ratio ‐ if revised

2015Basic Op Risk ‐3%

Capital Add‐on + SCA basic op

risk

2015Basic Op Risk ‐3%

Capital Add‐on as is

2015Basic Op Risk ‐3% Capital Add‐on (existing growth risk)

2014Basic Op Risk ‐3%

Capital Add‐on + SCA basic op

risk

2014Basic Op Risk ‐3% Capital Add‐on (existing growth risk)

2014Basic Op Risk ‐3%

Capital Add‐on as is

2013Basic Op Risk ‐3%

Capital Add‐on + SCA basic op

risk

2013Basic Op Risk ‐3% Capital Add‐on as is

2013Basic Op Risk ‐3% Capital Add‐on incl. info

growth risk

2013Basic Op Risk ‐3% Capital Add‐on incl. info

growth risk

Average RBC Ratio ‐ before basic op risk

2013Basic Op Risk ‐3% Capital Add‐on (existing growth risk)

Average RBC Ratio ‐ after basic op risk as is

Average RBC Ratio ‐ after basic op risk as is

Average RBC Ratio ‐ before basic op riskAverage RBC Ratio ‐ after basic op risk as isAverage RBC Ratio ‐ if revised

Average RBC Ratio ‐ before basic op risk

Attachment 2

ATTACHMENT 3

Operational Risk – Growth Risk Additional P/C RBC Feedback

Alan Seeley, Chair

Outreach: As Subgroup Chair, I reached out to a current regulator, a former regulator and three non-regulators, all of whom are “experts” familiar with the development of the growth risk charge currently used in the P/C RBC formula. Staff support Lou Felice also attended the calls. The following main questions were posed and discussed (main points from the responses are posted below each question):

1. It would seem less likely that there would be excessive growth at the group level than at the entity level. Why is using group growth is appropriate for entity based RBC?

Responses:

• Group growth is more appropriate for P/C where quota share pooling occurs within the group. The group calculation may not be as important for small simple group structures.

• Groups often distribute incoming business to their member companies by lines of business or quality of business, which makes group growth more relevant than individual company growth

2. What is the reason for applying a growth risk factor to loss and expense reserves?

Responses:

• Applying a factor to reserves recognizes potential understatement resulting from excessive growth

• Factors were developed based on a comparison of loss ratios at different company growth rates.

• In addition to operational risk, excessive growth increases underwriting risk, including the risk of inadequate loss reserves.

3. Why are the growth risk factors applied to net exposures for premiums and reserves rather than gross (consistent with how the growth threshold is measured)? Responses: • Applying the factors to net proxies is consistent with extra underwriting risk to the

entity that is associated with excessive growth. • Growth risk is picked up in Schedule P

ATTACHMENT 3

2

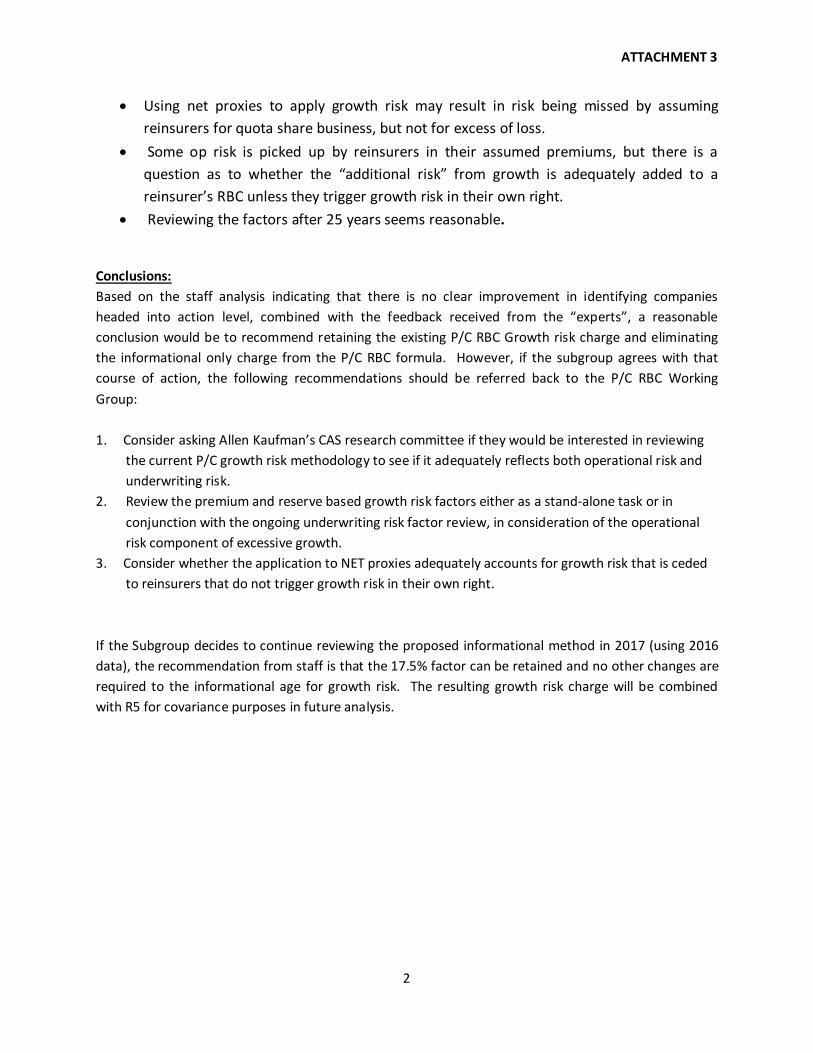

• Using net proxies to apply growth risk may result in risk being missed by assuming reinsurers for quota share business, but not for excess of loss.

• Some op risk is picked up by reinsurers in their assumed premiums, but there is a question as to whether the “additional risk” from growth is adequately added to a reinsurer’s RBC unless they trigger growth risk in their own right.

• Reviewing the factors after 25 years seems reasonable.

Conclusions: Based on the staff analysis indicating that there is no clear improvement in identifying companies headed into action level, combined with the feedback received from the “experts”, a reasonable conclusion would be to recommend retaining the existing P/C RBC Growth risk charge and eliminating the informational only charge from the P/C RBC formula. However, if the subgroup agrees with that course of action, the following recommendations should be referred back to the P/C RBC Working Group: 1. Consider asking Allen Kaufman’s CAS research committee if they would be interested in reviewing

the current P/C growth risk methodology to see if it adequately reflects both operational risk and underwriting risk.

2. Review the premium and reserve based growth risk factors either as a stand-alone task or in conjunction with the ongoing underwriting risk factor review, in consideration of the operational risk component of excessive growth.

3. Consider whether the application to NET proxies adequately accounts for growth risk that is ceded to reinsurers that do not trigger growth risk in their own right.

If the Subgroup decides to continue reviewing the proposed informational method in 2017 (using 2016 data), the recommendation from staff is that the 17.5% factor can be retained and no other changes are required to the informational age for growth risk. The resulting growth risk charge will be combined with R5 for covariance purposes in future analysis.

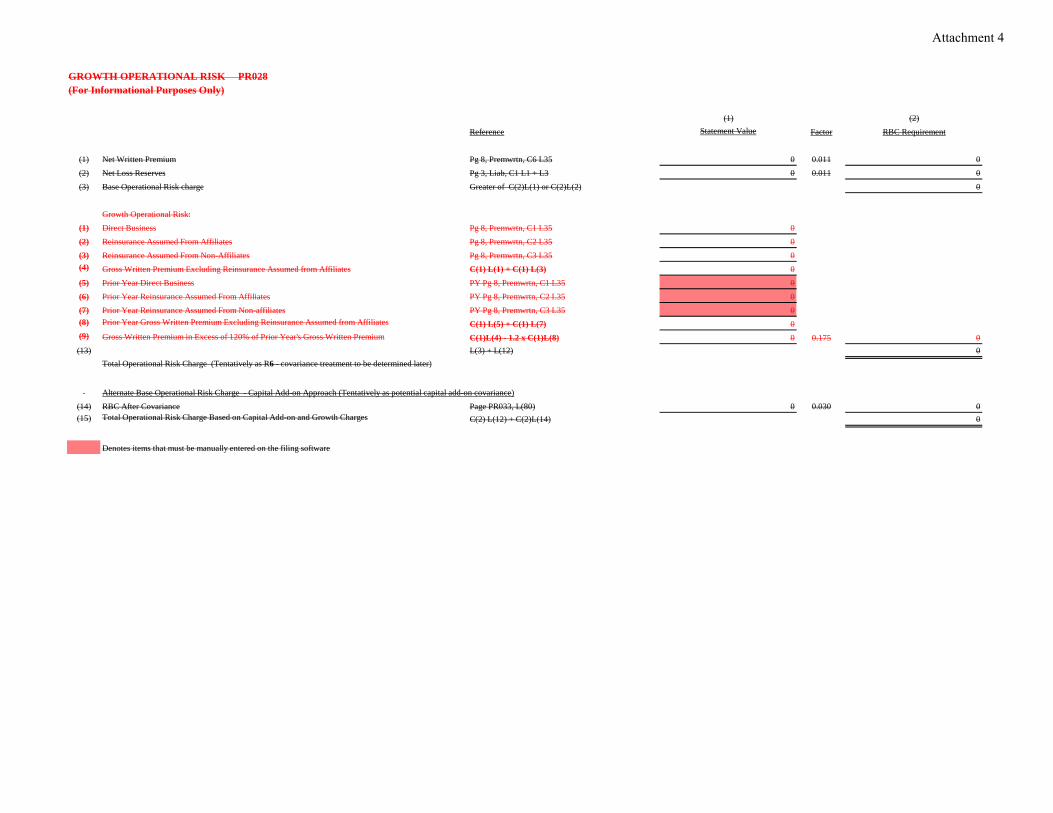

GROWTH OPERATIONAL RISK PR028(For Informational Purposes Only)

(1) (2)Reference Statement Value Factor RBC Requirement

(1) Net Written Premium Pg 8, Premwrtn, C6 L35 0 0.011 0(2) Net Loss Reserves Pg 3, Liab, C1 L1 + L3 0 0.011 0(3) Base Operational Risk charge Greater of C(2)L(1) or C(2)L(2) 0

Growth Operational Risk:(1) Direct Business Pg 8, Premwrtn, C1 L35 0(2) Reinsurance Assumed From Affiliates Pg 8, Premwrtn, C2 L35 0(3) Reinsurance Assumed From Non-Affiliates Pg 8, Premwrtn, C3 L35 0(4) Gross Written Premium Excluding Reinsurance Assumed from Affiliates C(1) L(1) + C(1) L(3) 0(5) Prior Year Direct Business PY Pg 8, Premwrtn, C1 L35 0(6) Prior Year Reinsurance Assumed From Affiliates PY Pg 8, Premwrtn, C2 L35 0(7) Prior Year Reinsurance Assumed From Non-affiliates PY Pg 8, Premwrtn, C3 L35 0(8) Prior Year Gross Written Premium Excluding Reinsurance Assumed from Affiliates C(1) L(5) + C(1) L(7) 0(9) Gross Written Premium in Excess of 120% of Prior Year's Gross Written Premium C(1)L(4) - 1.2 x C(1)L(8) 0 0.175 0(13) L(3) + L(12) 0

Alternate Base Operational Risk Charge - Capital Add-on Approach (Tentatively as potential capital add-on covariance)(14) RBC After Covariance Page PR033, L(80) 0 0.030 0(15) Total Operational Risk Charge Based on Capital Add-on and Growth Charges C(2) L(12) + C(2)L(14) 0

Denotes items that must be manually entered on the filing software

Total Operational Risk Charge (Tentatively as R6 - covariance treatment to be determined later)

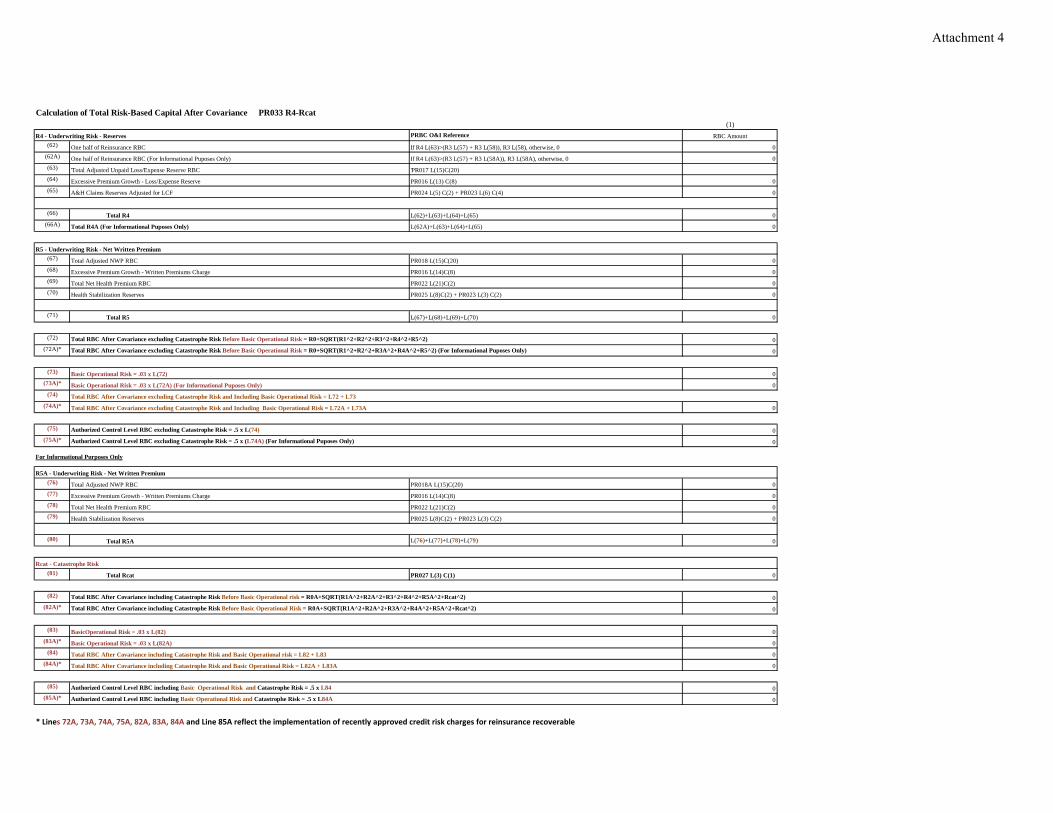

Attachment 4

Calculation of Total Risk-Based Capital After Covariance PR033 R4-Rcat(1)

R4 - Underwriting Risk - Reserves PRBC O&I Reference RBC Amount(62) One half of Reinsurance RBC If R4 L(63)>(R3 L(57) + R3 L(58)), R3 L(58), otherwise, 0 0

(62A) One half of Reinsurance RBC (For Informational Puposes Only) If R4 L(63)>(R3 L(57) + R3 L(58A)), R3 L(58A), otherwise, 0 0(63) 'Total Adjusted Unpaid Loss/Expense Reserve RBC 'PR017 L(15)C(20)(64) Excessive Premium Growth - Loss/Expense Reserve PR016 L(13) C(8) 0(65) A&H Claims Reserves Adjusted for LCF PR024 L(5) C(2) + PR023 L(6) C(4) 0

(66) Total R4 L(62)+L(63)+L(64)+L(65) 0(66A) L(62A)+L(63)+L(64)+L(65) 0

R5 - Underwriting Risk - Net Written Premium(67) Total Adjusted NWP RBC PR018 L(15)C(20) 0(68) Excessive Premium Growth - Written Premiums Charge PR016 L(14)C(8) 0(69) Total Net Health Premium RBC PR022 L(21)C(2) 0(70) Health Stabilization Reserves PR025 L(8)C(2) + PR023 L(3) C(2) 0

(71) Total R5 L(67)+L(68)+L(69)+L(70) 0

(72) Total RBC After Covariance excluding Catastrophe Risk Before Basic Operational Risk = R0+SQRT(R1^2+R2^2+R3^2+R4^2+R5^2) 0(72A)* Total RBC After Covariance excluding Catastrophe Risk Before Basic Operational Risk = R0+SQRT(R1^2+R2^2+R3A^2+R4A^2+R5^2) (For Informational Puposes Only) 0

(73) Basic Operational Risk = .03 x L(72) 0(73A)* Basic Operational Risk = .03 x L(72A) (For Informational Puposes Only) 0

(74) Total RBC After Covariance excluding Catastrophe Risk and Including Basic Operational Risk = L72 + L73(74A)* Total RBC After Covariance excluding Catastrophe Risk and Including Basic Operational Risk = L72A + L73A 0

(75) Authorized Control Level RBC excluding Catastrophe Risk = .5 x L(74) 0(75A)* Authorized Control Level RBC excluding Catastrophe Risk = .5 x (L74A) (For Informational Puposes Only) 0

For Informational Purposes Only

R5A - Underwriting Risk - Net Written Premium(76) Total Adjusted NWP RBC PR018A L(15)C(20) 0(77) Excessive Premium Growth - Written Premiums Charge PR016 L(14)C(8) 0(78) Total Net Health Premium RBC PR022 L(21)C(2) 0(79) Health Stabilization Reserves PR025 L(8)C(2) + PR023 L(3) C(2) 0

(80) Total R5A L(76)+L(77)+L(78)+L(79) 0

Rcat - Catastrophe Risk (81) Total Rcat PR027 L(3) C(1) 0

(82) Total RBC After Covariance including Catastrophe Risk Before Basic Operational risk = R0A+SQRT(R1A^2+R2A^2+R3^2+R4^2+R5A^2+Rcat^2) 0(82A)* Total RBC After Covariance including Catastrophe Risk Before Basic Operational Risk = R0A+SQRT(R1A^2+R2A^2+R3A^2+R4A^2+R5A^2+Rcat^2) 0

(83) BasicOperational Risk = .03 x L(82) 0(83A)* Basic Operational Risk = .03 x L(82A) 0

(84) Total RBC After Covariance including Catastrophe Risk and Basic Operational risk = L82 + L83 0(84A)* Total RBC After Covariance including Catastrophe Risk and Basic Operational Risk = L82A + L83A 0

(85) Authorized Control Level RBC including Basic Operational Risk and Catastrophe Risk = .5 x L84 0(85A)* Authorized Control Level RBC including Basic Operational Risk and Catastrophe Risk = .5 x L84A 0

* Lines 72A, 73A, 74A, 75A, 82A, 83A, 84A and Line 85A reflect the implementation of recently approved credit risk charges for reinsurance recoverable

Total R4A (For Informational Puposes Only)

Attachment 4