openness to experience in managers and company … · web viewthis research aims to link the...

TRANSCRIPT

Openness to experience in managers and company performance

To what extent exerts the Big Five personality factor Openness to Experience an influence on the

financial performance of the company?

Department of Economics

Supervisor: Dr. Kapoor

Ingeborg de Graaf

368462

8/3/2015

Content

This research aims to link the personality factor Openness to Experience (as a facet of the Big Five personality measures) to company performance. The relationship was investigated by multiple regression, controlling for all other Big Five factors, as well as job tenure. The results showed that Openness to Experience has a significant positive influence on company performance. However, this relation was moderated negatively by the Big Five factor Agreeableness.

2

s

1. Introduction.......................................................................................................................4

2. Theoretical framework......................................................................................................6

2.1 Personality; the Big Five..........................................................................................6

2.2 Personality as performance indicator......................................................................7

2.3 Company success.....................................................................................................8

2.4 Hypothesis:..............................................................................................................9

3. Data and Methodology....................................................................................................10

3.1 Research design.....................................................................................................10

3.2 Data collection.......................................................................................................10

3.3 Analysis techniques...............................................................................................12

3.4 Sample strategy.....................................................................................................12

3.5 Quality indicators..................................................................................................13

3.5.1 Validity....................................................................................................13

4. Results.............................................................................................................................14

4.1 Differences in average Openness to Experience....................................................14

4.2 Multiple regression analysis..................................................................................15

4.3 Regression estimates Revenues............................................................................16

4.3.1 Model 1...................................................................................................16

4.3.2 Model 2...................................................................................................18

4.3.3 Model 3...................................................................................................18

4.3.4 Model 4...................................................................................................19

4.3.5 Model 5...................................................................................................20

4.3.6 Model 6...................................................................................................21

4.3.7 Model 7...................................................................................................22

4.3.8 Model 8...................................................................................................24

5. Conclusion.......................................................................................................................25

6. Discussion & limitations..................................................................................................27

7. References.......................................................................................................................29

8. Appendices......................................................................................................................31

8.1 Appendix 1: survey in Dutch (as distributed to the respondents).........................31

3

8.2 Appendix 2: survey translated to English...............................................................41

8.3 Excluded regression models..................................................................................44

4

1. Introduction

Hiring the right people for the right job is something that has gotten quite some attention

over the years. Since there are a lot of aspects to this process, I will focus on one aspect:

employee personality. In a simple Web of Science™ search for the words "personality" and

"job performance" in the title resulted in 101 scientific publications.

Financial performance as a stand-alone topic is a widely discussed topic as well, as is

mentioned by Capon et al. (1990), who reviewed 320 empirical studies in their meta-analysis

of financial performance.

However, a search for personality and company/business/financial performance in the title

resulted in only four publications, two of which two addressed company performance, the

other two both addressed job performance. Moreover, a search for papers which addressed

manager's job performance and a search for personality and company/business/financial

performance resulted in only one paper for the former and only two for the latter, both not

relevant for the research I am proposing. In this research, I will take on a different

perspective on hiring and company performance. I will investigate whether the personality

of the manager has an influence on financial performance.

For the measurement of the managers' personalities, I will make use of the Big Five

construct (IPIP). This is a fifty-item questionnaire which addresses the five key personality

traits: Openness to experience, Extraversion, Emotional Stability, Agreeableness and

Conscientiousness. This is in accordance with Chiavarella et al. (2004), who argued that the

Big Five model "has been found to be a robust indicator of an individual's personality".

The other aspect of this research is company performance. Since performance has a lot of

different measurements, I opted for the simplest measure, revenues. The choice was made

because revenues are the number of sales times the price of that what is sold. This is

universal and makes sure that the values for both companies comprehend the exact same

things.

Two organizations have been approached for this study, one in the carpentry industry and

one in the logistics industry. More information is not disclosed, because they requested to

stay anonymous. Besides the different industries, the most important distinction is the fact

5

that the carpentry company is in bad financial shape, whereas the logistics company is

performing well.

This leads to the research question: "Does Openness to Experience (as part of a manager's

personality) have an influence on the financial performance of the company?"

In this paper, I will examine this linkage in a (non-random) sample of managers from both a

successful and an unsuccessful company. A simple comparison of average scores for the Big

Five traits will show whether or not this difference is apparent. I suspect there will be a

difference for the factor openness to experience and possibly in conscientiousness. If this

does occur, I will try to investigate the causality of this difference. By estimating a regression

where financial performance of a company is regressed on the manager's score on each of

the Big Five characteristics (either per company or department). If the coefficient of the

openness factor is significant from zero, there might be an effect of the personality of the

managers on the company performance.

From a company perspective, this research is an interesting subject when companies are

faced with deteriorating financial health, provided that the causality leads from the

personality traits to the company performance. For the investigated companies especially,

this information could lead to better financial performance when the hiring processes are

adapted to take personality into account (if an effect of personality on company financial

performance is found).

Furthermore, this research contributes to the current literature by examining managers'

personalities as a variable which might influence company performance. Moreover, this is a

link that has not been studied before and might provide a useful insight in the realization of

financial goals. This research aims to provide a helpful notion for those examining the

determinants of financial performance. Future research can either replicate or evaluate this

research, or use it as a starting point for new studies.

I will proceed with the theoretical framework on which this research is based, followed by a

description of the data, the methodology and the results. The conclusion will relate these

results to the research question and the before mentioned theories. Finally, the implications

of the findings, as well as limitations of this research are discussed.

6

2. Theoretical framework

2.1 Personality; the Big Five

The Big Five personality dimensions addressed a need in the field of personality research, by

integrating the numerous and divergent ways of studying and/or describing personality in

one framework (John, 2001). The starting point of the Big Five lies with the lexical approach

of personality research, which posits that “most of the socially relevant and salient

personality characteristics have become encoded in the natural language” (John, 2001). Over

the course of the 20th century, all the words that could be used to describe any human’s

behavior as differing from the behavior of another. The amount of categories of words

differed per researcher, as well as the vision of the boundaries used (mutually exclusive an

clear, or overlapping and fuzzy). Over time, the amount of describing terms was reduced

more and more, from almost 18.000 terms (Allport, 1936) of which Cattell picked 4.500 to

reduce further to only 35 in 1943 and 1945 researches to arrive at 12 personality factors,

which were eventually included in his 16 Personality Factors survey. The work of Cattell

(both the outcomes and the reduction of the amount of variables used) inspired other

researchers to investigate personality. (Fiske, 1949) simplified 22 of the 35 variables of

Cattell and constructed a 5-factor structure which came close to the Big Five. When

reanalyzing the correlation matrices from eight samples (which ranged from people with no

more than high school education to graduate students), they found that the five factors

emerged clearly and frequent, across self-ratings, peer, supervisor, teacher and clinician

ratings (John, 2001).

In accordance with Norman (1963), the factors were initially named Extraversion (or

Surgency), Agreeableness, Conscientiousness, Emotional Stability versus Neuroticism and

Culture. The name Big Five came to be because of the broad scope of the factors (Goldberg,

1981). However, the Big Five does not suggest that that personality differences can be

captured in just five traits, but rather that personality can be represented by five dimensions

at the highest level of abstraction.

An important note to be made, is that an individual's personality obtains its final form

between the ages of 21 and 30, changes in personality traits after the age of 30 are therefore

7

rare (Costa & McCrae, 1994). Since the average age of the respondents is higher than 30,

reverse causality seems highly unlikely.

2.2 Personality as performance indicator

The link between personality and company success has been investigated by Chiavarella et

al. (2004), who found that the personality of the entrepreneur had an effect on venture

survival. They characterized the personality through the Big Five (Openness to experience,

Extraversion, Emotional Stability, Agreeableness and Conscientiousness) and venture

survival. They defined entrepreneurs as "those that have decided to launch a small business

by forgoing all other career alternatives and without the safety net of a professional license

in case of failure". For these entrepreneurs, extraversion, emotional stability and

agreeableness had no effect. Survival of a company was defined as the company still existing

after 8 years. Conscientiousness had a significant and positive effect on the life span of the

venture (p<.01), whereas openness to experience was expected to have a positive effect, it

had a significant negative effect (p<.10). They reason that openness to experience might be a

factor in starting a business, but over time, the job may require a shift from creative and

broad-mindedness to a managerial approach.

A paper by Barrick & Mount (1991) found that conscientiousness had a positive effect on

the job performance of managers as well, However, they found that openness to experience

had a weak and positive effect on managerial performance, contrasting the above reasoning.

A logical conclusion of this latter result would be that higher openness to experience in

managers leads to better company performance through better job performance.

The personality of managers will be assessed through the Big Five personality factors.

Ciavarella et al. (2003) have constructed the following overview of the Big Five based on the

descriptions in Barrick & Mount's 1991 paper, in their attempt to uncover the relationship

between an entrepreneurs personality and venture survival:

8

Big Five Factor Traits Components

Extraversion Sociable, gregarious,

assertive, talkative, active

ambition—initiative, surgency, impetuous,

likes to be in charge, seeks leadership roles,

persuasive

sociability—talkative, gregarious, enjoys

meeting people

individuality—shows off, enjoys taking

chances and stirring up excitement

Emotional

Stability

Calm, even-tempered, self-

satisfied, comfortable,

unemotional, hardy, stable,

confident, effective

Steady —even-tempered, steady emotionally

Security — feels secure about self, not

bothered by criticism

Agreeableness Being courteous, flexible,

trusting, good-natured,

cooperative, forgiving,

soft-hearted, tolerant

Cooperative — likes to help others and does

things for friends, trusting of others

Considerate — good-natured, cheerful,

forgives others easily

Conscientiousness Responsible, well-

organized, planful,

hardworking,

achievement-oriented,

persevering

Dependability — thorough, careful

Industriousness — strives to do best, does

more than planned, hardworking, persistent

Efficiency — neat and orderly, plans in

advance, rarely late for appointments

Openness to

experience

Being imaginative,

creative, cultured, curious,

original, broadminded,

intelligent, artistically

sensitive

Intellect — imaginative, likes abstract ideas

and concepts, analytical and introspective,

enjoys philosophical debates

Open — cultured, likes to try new and

different things, enjoys art, music, literature

Table 1: The Big Five Factors, Traits and Components (Ciavarella et al., 2003)

Despite the fact that openness to experience the interesting factor is in this case, all factors

are assessed in the survey, providing data for both control and interaction variables.

2.3 Company success

The dependent variable in my research question is company performance. However, this

term is very broad (and broadly used as well). Moreover, the ways to measure it are

numerous and ranging from extremely simple to complicated formulas. In this research, I

will focus on the simplest measure of company success: revenues. The choice for this

9

measure comes down to the fact that calculating revenues is straightforward and there is

only one way to do it, which makes sure that the measures are performed (and thus are

measuring) exactly the same in both companies (in accordance with Dutch tax policies).

2.4 Hypothesis:

Reasoning from the arguments posited in the previous paragraphs, I pose the following

hypothesis, which is the research question of this paper:

Average managers' openness to experience will have a positive influence on company

revenues.

The following chapter will elaborate on the methodology of this research, as well as

information concerning the data.

Company RevenuesManager's Openness to Experience

10

3. Data and Methodology

In this section, the data collection and the methodology of this paper is explained. This

research aims to uncover the relationship between the Openness to Experience of managers

and the consecutive financial performance of their company.

3.1 Research design

As mentioned, I will focus on managers from both successful and unsuccessful companies,

and I will define a company as unsuccessful when the bank has declared that the company is

under "Bijzonder Beheer" or, in English: Special Asset Management (SAM). This means that

the bank has serious doubts whether or not the company is able to keep paying its bills and

thus decides that the company needs help in becoming financially healthy again or help

concerning termination, to ensure that the loss is kept to a minimum (Rabobank, n.d.).

Unfortunately, I was not allowed to get more information about which criteria are used to

determine whether or not a company should be under SAM. However, the binary division of

successful and unsuccessful is sufficient for this research, for it is only used to determine the

type of company that is studied.

The factor Openness to Experience is part of the Big Five Factor model, which is the reason I

chose the standard IPIP 50-item questionnaire to use in my survey. To study the outcomes

appropriately, the survey responses will be aggregated per company.

3.2 Data collection

The data are obtained from two companies. The company under SAM is a manufacturer of

wooden window frames (carpentry industry). The company that is financially sound, is a

provider of value-added logistics and warehousing (transportation and storage industry). The

survey was distributed to the managers of the two companies, which amounted to 11

managers of the company under SAM and five managers of the financially healthy company.

All subjects responded, totaling 16 surveys in total. Personality was assessed by the 50-item

set of IPIP Big Five Factor Markers (IPIP). The answers to the questions concerning the Big

Five consisted of a five-point Likert scale, which makes it easier to fill in the questionnaire

and will reduce possible errors due to inattentiveness. The questionnaire can be found in

appendix 2 (this is the translated version, the version that was send out was in Dutch and

11

can be found in appendix 1). The answers ranged from "strongly disagree" to "strongly

agree", expressing neutrality towards the question was possible as well.

Financial performance will be measured by the revenues of the year 2013. Control variables

will consist of: the remaining four of the Big Five personality factors, which have been found

to be predictors of job performance in managers (Rothmann, 2003). Logical reasoning leads

me to think that good job performance should lead to better financial results. However, as I

mentioned before, this relationship has not yet been investigated. Continuing on this view, I

accounted for job tenure, which was found to have a positive (but diminishing over time)

effect on job performance (Hg, 2010). These variables were reported in the survey.

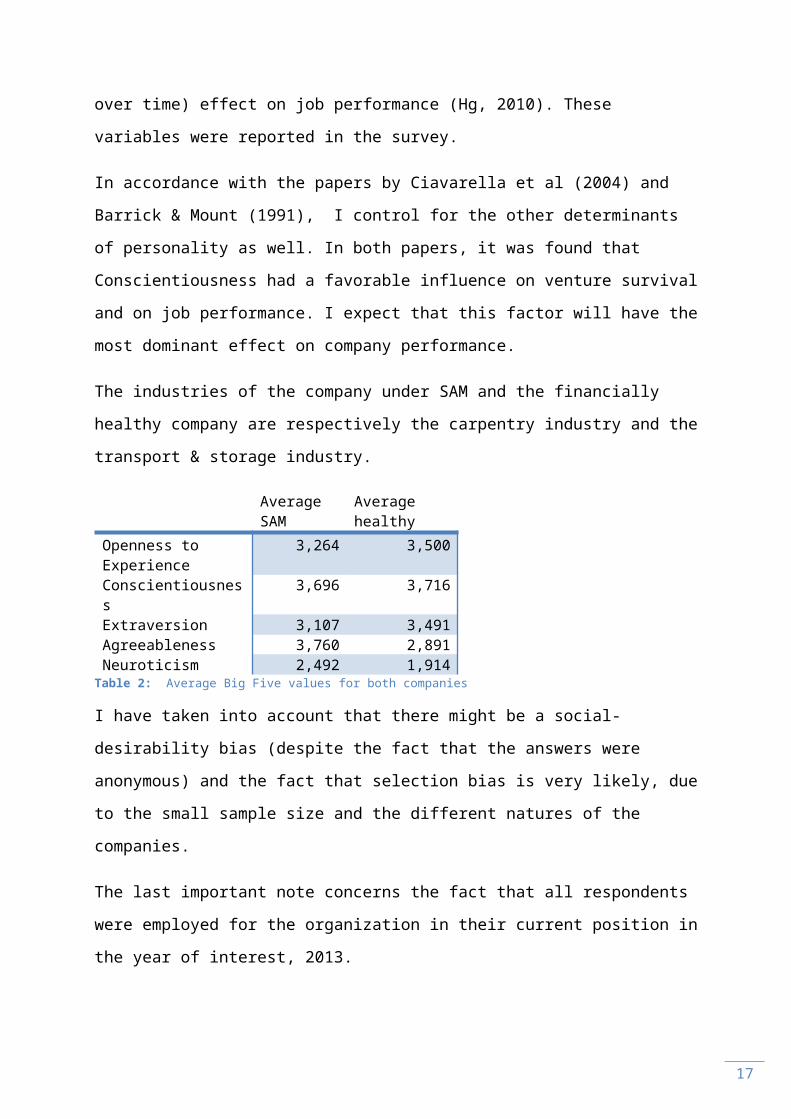

In accordance with the papers by Ciavarella et al (2004) and Barrick & Mount (1991), I

control for the other determinants of personality as well. In both papers, it was found that

Conscientiousness had a favorable influence on venture survival and on job performance. I

expect that this factor will have the most dominant effect on company performance.

The industries of the company under SAM and the financially healthy company are

respectively the carpentry industry and the transport & storage industry.

Average SAM Average healthyOpenness to Experience 3,264 3,500Conscientiousness 3,696 3,716Extraversion 3,107 3,491Agreeableness 3,760 2,891Neuroticism 2,492 1,914

Table 2: Average Big Five values for both companies

I have taken into account that there might be a social-desirability bias (despite the fact that

the answers were anonymous) and the fact that selection bias is very likely, due to the small

sample size and the different natures of the companies.

The last important note concerns the fact that all respondents were employed for the

organization in their current position in the year of interest, 2013.

12

3.3 Analysis techniques

After the collection of data was completed, an independent t-test was run to see if the mean

values of Openness to Experience differed between the two groups. The choice for an

independent t-test was made because of the small sample size and the fact that the samples

were drawn from two different groups. This is an important step, because in order to prove

a causal relationship between the Openness to Experience factor and company

performance, there must be a difference in Openness to Experience, as well as in company

performance.

After this comparison, a normal quantile plot was constructed, to check if Openness to

Experience is distributed normally.

Finally, several multiple regression models were estimated. I have disclosed eight models,

the first five adding the Big Five factors step-by-step, starting with Openness to Experience,

then Conscientiousness, followed by Extraversion, Agreeableness and Neuroticism (forming

OCEAN). In the sixth model, the variable job tenure was added, and in the seventh, the

interaction between Openness to Experience and Agreeableness. In the final model, the

variable Extraversion is deleted, to arrive at the model with both the highest explanatory

value (as depicted by the Adjusted R-square) and the most significant estimates of the

coefficients of the included variables. For some models, residual plots are provided, to see if

the assumption of homoscedasticy of the errors is satisfied.

3.4 Sample strategy

The sample was purposely created, which means that only managers of the companies were

asked to fill in a survey. The choice for managers was made because the results of Barrick &

Mount (1991) indicated that Openness to Experience was a significant indicator of

manager’s job performance. In the carpentry company, the managers belonged to either

one of tree management groups: Owner-managers, Management Team and Operations

Management. In the transport & storage company, all managers were partial owners,

resulting in only one group. Convenience sampling was only the case in the carpentry

company, because two managers were on holiday during the time the survey was available.

Because this information was available prior to the sending out of the survey, they have not

been approached.

13

3.5 Quality indicators

3.5.1 ValidityTo enhance the validity of this research, I included some control variables. The first four

control variables concern the Big Five factors of Conscientiousness, Extraversion,

Agreeableness and Neuroticism. These were taken into account because all of them have an

influence on managerial job performance (Rothmann, 2003), and thus logically on company

performance as well.

The fifth control variable is the job tenure of the managers. This control might prove to be

important, because a manager with a longer time on the job might understand the processes

in the company better, and therefore be more able to interpret correctly what influence his

or her actions indirectly have on other parts of the company. Hg & Feldman (2010) found

that job tenure had a positive (but diminishing) effect on job performance. Again, this

variable is included because of the effect that job performance is logically thought to have

on company performance.

The sixth control variable indicates the size of the companies, as measured by the average

number of employees per year. This was in accordance with Ciavarella et al (2004), who

examined different companies in different industries as well.

The seventh, and last, control variable concerns the performance per industry. This is in

accordance with the meta-analysis performed by Capon & Hoenig (1990), which was aimed

to discover the determinants of financial performance.

The validity of the survey was secured, because it is widely used, supported widely, as well

as plenteously used in personality-related research (Gosling, 2003).

14

4. Results

4.1 Differences in average Openness to Experience

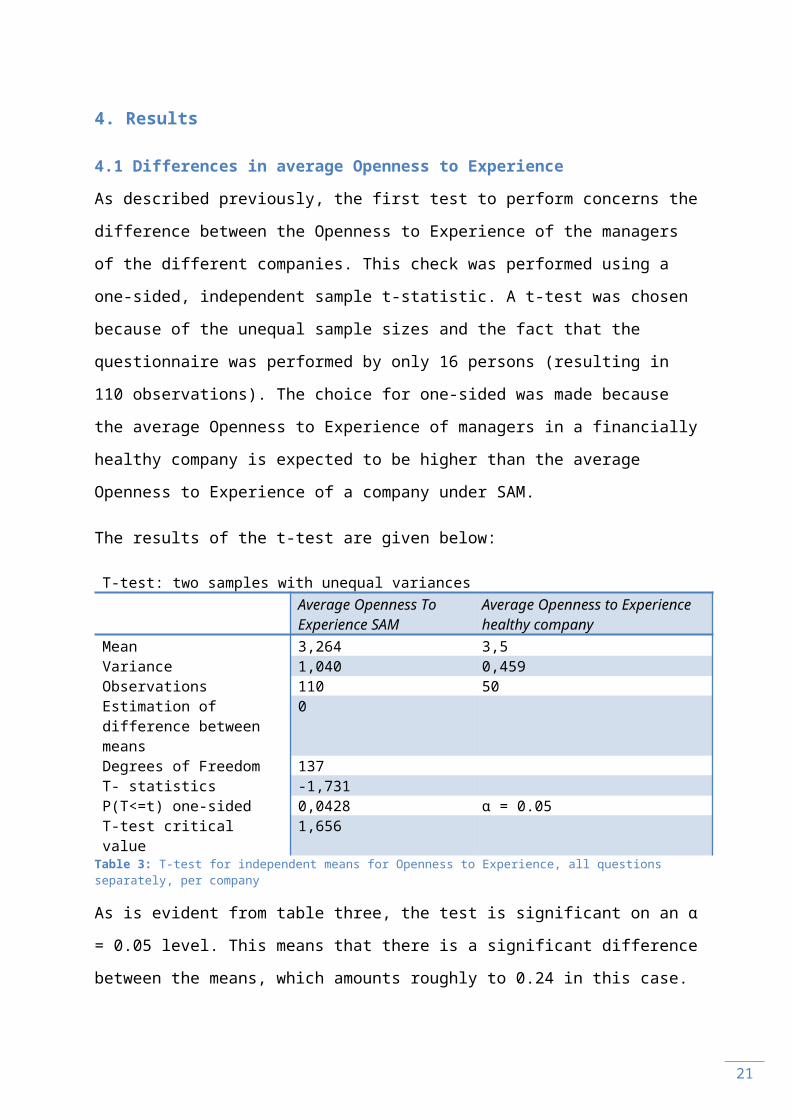

As described previously, the first test to perform concerns the difference between the

Openness to Experience of the managers of the different companies. This check was

performed using a one-sided, independent sample t-statistic. A t-test was chosen because of

the unequal sample sizes and the fact that the questionnaire was performed by only 16

persons (resulting in 110 observations). The choice for one-sided was made because the

average Openness to Experience of managers in a financially healthy company is expected to

be higher than the average Openness to Experience of a company under SAM.

The results of the t-test are given below:

T-test: two samples with unequal variancesAverage Openness To Experience SAM

Average Openness to Experience healthy company

Mean 3,264 3,5Variance 1,040 0,459Observations 110 50Estimation of difference between means

0

Degrees of Freedom 137T- statistics -1,731P(T<=t) one-sided 0,0428 α = 0.05T-test critical value 1,656

Table 3: T-test for independent means for Openness to Experience, all questions separately, per company

As is evident from table three, the test is significant on an α = 0.05 level. This means that

there is a significant difference between the means, which amounts roughly to 0.24 in this

case.

However, since the results of the test would yield an average score per respondent, The

same test was performed on the much smaller observation of the score on Openness to

Experience per respondent. The independent samples t-test yielded the following results:

15

T-test: two samples with unequal variances

Average Openness To Experience SAM

Average Openness to Experience healthy company

Mean 3,5 3,264Variance 0,065 0,152Observations 5 11Estimation of difference between means

0

Degrees of Freedom 12T- statistics 1,441P(T<=t) one-sided 0,0874 α = 0.10T-test critical value 1,782

Table 4: T-test for independent means for the variable Openness to Experience per manager, per company

Again, the difference is visible, however the significance has decreased a little, to α = 0.10.

With the difference between levels of Openness to Experience apparent, it is possible to

advance to the next section of the results.

4.2 Multiple regression analysis

One of the assumptions of regression is normality. The below Normal Quantile Plot shows

the dispersion of the data against the normal line. As is visible, there are outliers in the

middle, but the deviation seems small and the overall pattern has a reasonable fit with the

line, as is indicated by the R-square of approximately 0.73.

-2.5 -2 -1.5 -1 -0.5 0 0.5 1 1.5 2 2.50

0.5

1

1.5

2

2.5

3

3.5

4

f(x) = 0.297183646480822 x + 3.275R² = 0.729186581045192

Normal Quantile Plot

Rank-based Z-score

Ope

nnes

s to

Expe

rienc

e

Figure 1: Normal Quantile Plot for the variable Openness to Experience

16

4.3 Regression estimates Revenues

A significance level of α = 0.10 is used, unless specified otherwise.

I will first provide a short overview of the regressions performed:

Model R-

squared

Adjusted R-

squared

Variables used

1 0,0971 0,0326 Openness to Experience

2 0,106 -0,031 Openness to Experience and Conscientiousness

3 0,179 -0,026 Openness to Experience, Conscientiousness and

Agreeableness

4 0,746 0,654 Openness to Experience, Conscientiousness, Agreeableness

and Extraversion

5 0,829 0,743 Openness to Experience, Conscientiousness, Agreeableness,

Extraversion and Neuroticism

6 0,830 0,717 Openness to Experience, Conscientiousness, Agreeableness,

Extraversion, Neuroticism and job tenure

7 0,893 0,799 Openness to Experience, Conscientiousness, Agreeableness,

Extraversion, Neuroticism, job tenure and Openness to

Experience*Agreeableness

8 0,883 0,806 Openness to Experience, Conscientiousness, Agreeableness,

Extraversion, Neuroticism, job tenure and Openness to

Experience*Agreeableness

Table 5: Overview of the regression models

4.3.1 Model 1

In order to estimate the effect of Openness to Experience on company performance more

clearly, I will show six regression models: three with revenues as dependent variable and

three with EBIT as dependent variable. I will start with the regression of revenues:

Regression StatisticsMultiple R - correlation coefficient 0,312R-square 0,097Adjusted R-square 0,033Standard error 154993,515Observations 16

Coefficients Standard t Stat P-

17

Error valueIntercept 12911337,58 369890,078 34,90

60.000

Openness to Experience -135253,003 110218,699 -1,227 0,240Table 6: Model 1, regression of company revenue on Openness to Experience

The estimation results in the following regression:

company revenue = 12911337,58 -135253,0025*(Openness to experience managers)

This regression, however, is not very accurate, as is depicted by the very low R-square (0.09).

Moreover, the effect of Openness to Experience is not significant, which means that there is

no evidence that it’s effect is different from zero.

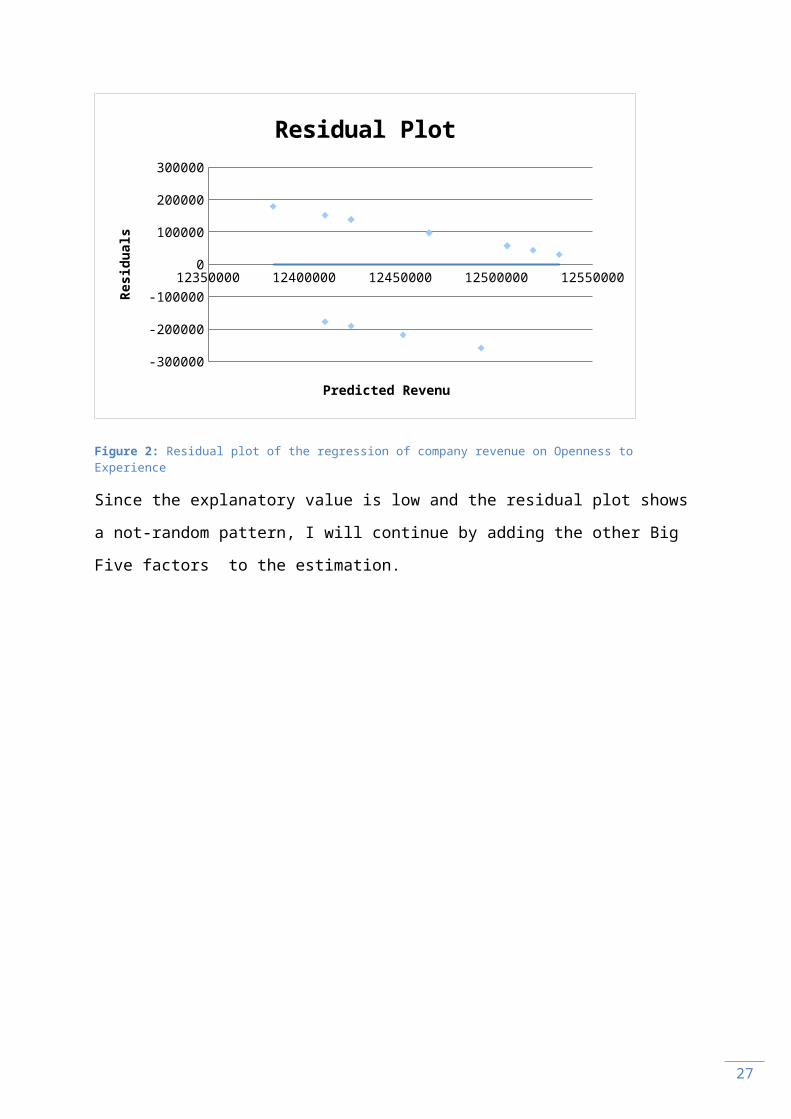

Since one of the assumptions of the regression model assume homoscedasticy, I will check

for this by using a residual plot. As is visible from the plot, the estimate is both biased and

heteroscedastic. The blue (horizontal) line depicts the linear trend line, or the regression line

of the data. This line is horizontal, even when there is a clear downward slope visible in the

plot, because the line does not follow the line the data appears to follow, the residuals are

biased. Moreover, the residuals are divided into two groups, indicating that there is

homoscedasticity.

12350000 12400000 12450000 12500000 12550000

-300000

-200000

-100000

0

100000

200000

300000

Residual Plot

Predicted Revenu

Resid

uals

Figure 2: Residual plot of the regression of company revenue on Openness to Experience

Since the explanatory value is low and the residual plot shows a not-random pattern, I will

continue by adding the other Big Five factors to the estimation.

18

19

4.3.2 Model 2

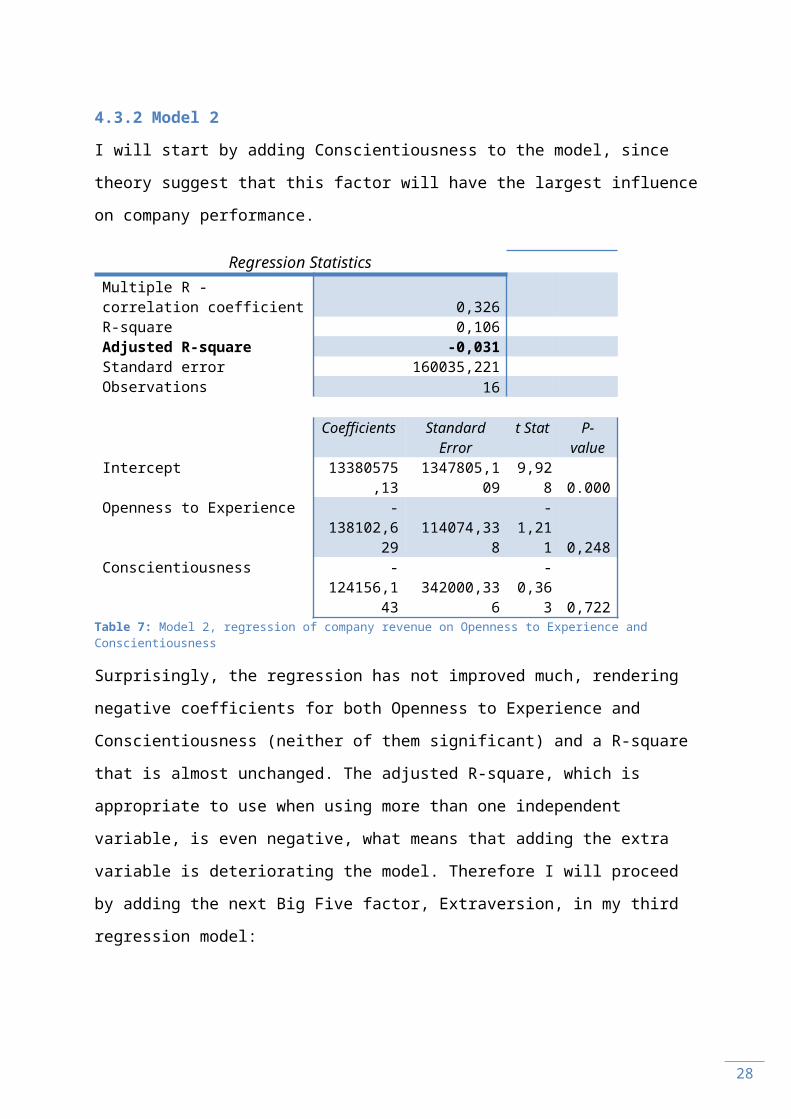

I will start by adding Conscientiousness to the model, since theory suggest that this factor

will have the largest influence on company performance.

Regression StatisticsMultiple R - correlation coefficient 0,326R-square 0,106Adjusted R-square -0,031Standard error 160035,221Observations 16

Coefficients Standard Error

t Stat P-value

Intercept 13380575,13 1347805,109 9,928 0.000Openness to Experience -138102,629 114074,338 -1,211 0,248Conscientiousness -124156,143 342000,336 -0,363 0,722

Table 7: Model 2, regression of company revenue on Openness to Experience and Conscientiousness

Surprisingly, the regression has not improved much, rendering negative coefficients for both

Openness to Experience and Conscientiousness (neither of them significant) and a R-square

that is almost unchanged. The adjusted R-square, which is appropriate to use when using

more than one independent variable, is even negative, what means that adding the extra

variable is deteriorating the model. Therefore I will proceed by adding the next Big Five

factor, Extraversion, in my third regression model:

4.3.3 Model 3

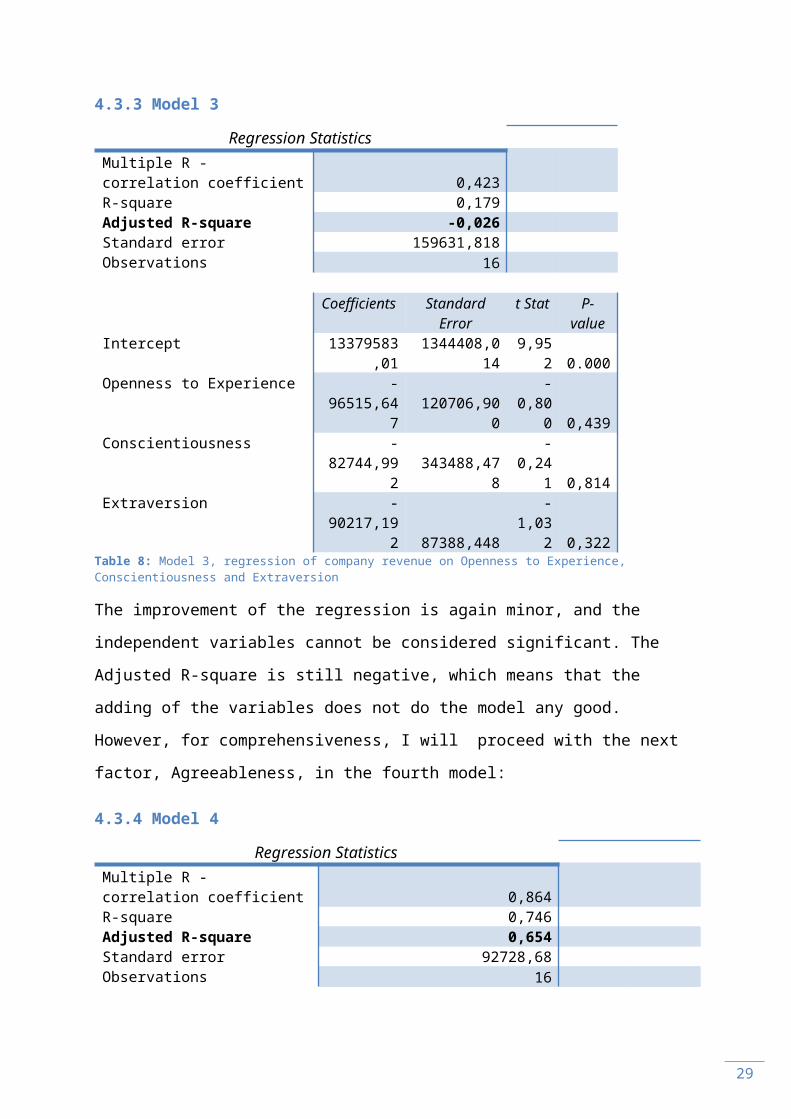

Regression StatisticsMultiple R - correlation coefficient 0,423R-square 0,179Adjusted R-square -0,026Standard error 159631,818Observations 16

Coefficients Standard Error

t Stat P-value

Intercept 13379583,01 1344408,014 9,952 0.000Openness to Experience -96515,647 120706,900 -0,800 0,439Conscientiousness -82744,992 343488,478 -0,241 0,814Extraversion -90217,192 87388,448 -1,032 0,322

Table 8: Model 3, regression of company revenue on Openness to Experience, Conscientiousness and Extraversion

The improvement of the regression is again minor, and the independent variables cannot be

considered significant. The Adjusted R-square is still negative, which means that the adding

20

of the variables does not do the model any good. However, for comprehensiveness, I will

proceed with the next factor, Agreeableness, in the fourth model:

4.3.4 Model 4

Regression StatisticsMultiple R - correlation coefficient 0,864R-square 0,746Adjusted R-square 0,654Standard error 92728,68Observations 16

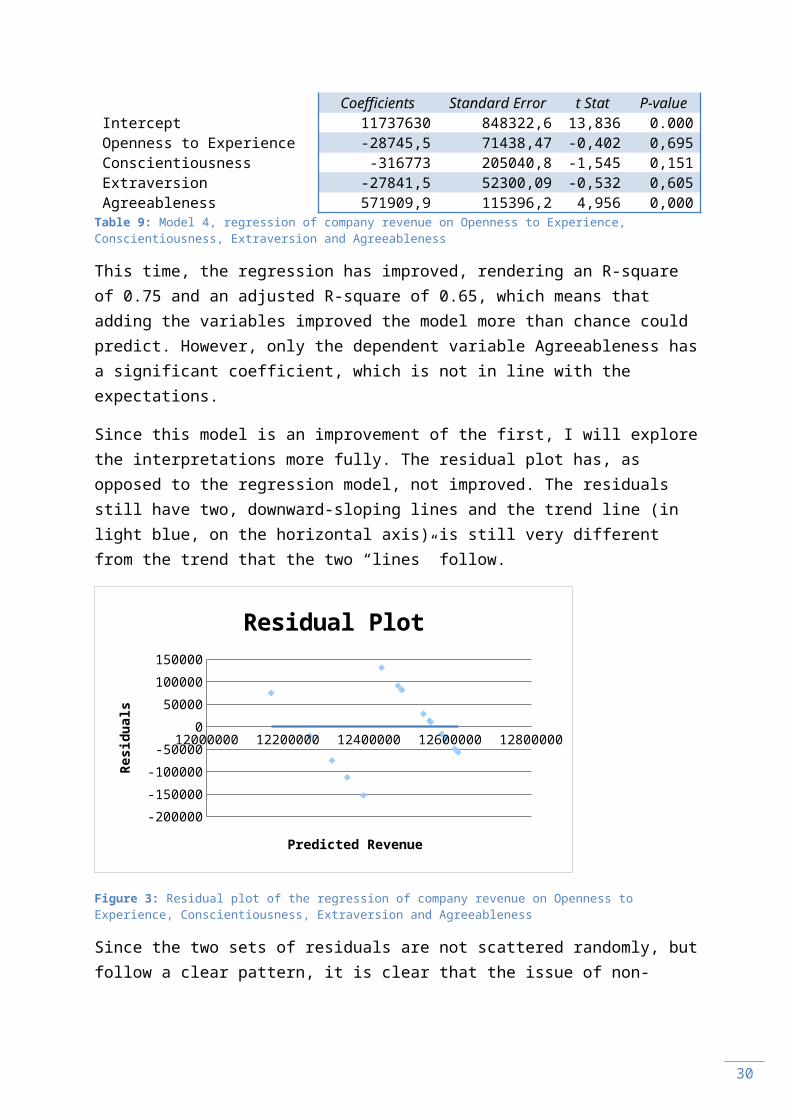

Coefficients Standard Error t Stat P-valueIntercept 11737630 848322,6 13,836 0.000Openness to Experience -28745,5 71438,47 -0,402 0,695Conscientiousness -316773 205040,8 -1,545 0,151Extraversion -27841,5 52300,09 -0,532 0,605Agreeableness 571909,9 115396,2 4,956 0,000

Table 9: Model 4, regression of company revenue on Openness to Experience, Conscientiousness, Extraversion and Agreeableness

This time, the regression has improved, rendering an R-square of 0.75 and an adjusted R-square of 0.65, which means that adding the variables improved the model more than chance could predict. However, only the dependent variable Agreeableness has a significant coefficient, which is not in line with the expectations.

Since this model is an improvement of the first, I will explore the interpretations more fully. The residual plot has, as opposed to the regression model, not improved. The residuals still have two, downward-sloping lines and the trend line (in light blue, on the horizontal axis) is still very different from the trend that the two “lines” follow.

21

12100000 12200000 12300000 12400000 12500000 12600000 12700000

-200000

-150000

-100000

-50000

0

50000

100000

150000

Residual Plot

Predicted Revenue

Resid

uals

Figure 3: Residual plot of the regression of company revenue on Openness to Experience, Conscientiousness, Extraversion and Agreeableness

Since the two sets of residuals are not scattered randomly, but follow a clear pattern, it is clear that the issue of non-normality of the sample is not resolved. However, this was to be expected, since the sample was not selected randomly.

Now, I will run a regression with all Big Five estimates:

4.3.5 Model 5

Regression StatisticsMultiple R - correlation coefficient 0,910R-square 0,829Adjusted R-square 0,743Standard error 79858,71Observations 16

Coefficients Standard Error t Stat P-valueIntercept 11266290 761403,6 14,797 0.000Openness to Experience -8336,7 62220,12 -0,134 0,896Conscientiousness 67887,35 248612,4 0,273 0,790Extraversion -49479,1 46104,5 -1,073 0,308Agreeableness 56072,32 254859,8 0,220 0,830Neuroticism 400479,1 182201,7 2,198 0,053

Table 10: Model 5, regression of company revenue on Openness to Experience, Conscientiousness, Extraversion, Agreeableness and Neuroticism

22

The regression formula generated by this model is the following:

company revenue = 11266290 -8336,7*(Openness to experience managers) +

67887,35* (conscientiousness managers) -49479,1*(extraversion managers) +

56072,32*(emotional stability managers) + 400479,1*(agreeableness managers)

The effect of Openness to Experience remains negative and insignificant and the coefficient

of Agreeableness has deteriorated, not even coming close to being statistically significant.

Another surprise is the significance of Neuroticism (significant at the 0.10 level). The

adjusted R-squared shows that this regression is preferable to the previous one (0.74 versus

0.65).

12100000 12200000 12300000 12400000 12500000 12600000 12700000

-200000

-150000

-100000

-50000

0

50000

100000

150000

Residual Plot

Predicted Revenue

Resid

uals

Figure 4: Residual plot of the regression of company revenue on Openness to Experience, Conscientiousness, Extraversion, Agreeableness and Neuroticism

The residual plot shows a similar pattern to the residual plot of the previous regression. Therefore, the interpretation stays the same: since there are two sets which appear to be following a clear pattern, means that the sample does not suffice the condition of normality.

A possible way to improve the normality is to take job tenure into account, which will be done in the next model:

4.3.6 Model 6

Regression StatisticsMultiple R - correlation coefficient 0,911R-square 0,830Adjusted R-square 0,717Standard error 83765,919

23

Observations 16

Coefficients Standard Error

t Stat P-value

Intercept11120538,04 936427,159

11,875 0.000

Job Tenure 1034,799 3471,202 0,298 0,772Openness to Experience -5265,119 66072,654 -0,080 0,938Conscientiousness 118288,100 310786,357 0,380 0,712Extraversion -40233,210 57451,315 -0,700 0,501Agreeableness 7623,277 312854,488 0,024 0,981Neuroticism 435663,151 224621,994 1,940 0,084

Table 11: Model 6, regression of company revenue on the Big Five and job tenure

This regression model has a lower adjusted square, which means that the previous model is

better at explaining the different revenues. Therefore, I will not elaborate further on this

specific model.

Another way for Openness to Experience to influence company revenue could be through

interactions with other variables. Because of the large amount of variables, I will only

present the variables that generated an adjusted R-square that was higher than the fifth

model:

4.3.7 Model 7

Regression StatisticsMultiple R - correlation coefficient 0,945R-square 0,893Adjusted R-square 0,799Standard error 70632,416Observations 16

Coefficients Standard Error t Stat P-valueIntercept -1135873,681 5733452,832 -0,198 0,848Job Tenure 3387,446 3123,352 1,085 0,310Openness to Experience 3377020,886 1568120,414 2,154 0,063Conscientiousness 385186,432 289771,260 1,329 0,220Extraversion -40892,882 48444,594 -0,844 0,423Agreeableness 2869370,088 1351934,18 2,122 0,066Neuroticism 711179,065 228407,359 3,114 0,014Openness to Experience * Agreeableness -915656,586 424255,448 -2,158 0,063

Table 12: regression of company revenue on the Big Five, job tenure and the interaction of Openness to Experience and Agreeableness

In this model, both Openness to Experience, Agreeableness and the interaction are

statistically significant at the 0.10 level, as well as Neuroticism (which is significant at the

24

0.05 level). The interaction means that for a given value of Agreeableness, say, 3, the effect

of Openness to Experience does not only incorporate the coefficient of Openness to

Experience, but the coefficient of the interaction as well. This means that for a higher value

of Agreeableness, the effect of Openness to Experience diminishes.

For the average levels of the manager's Agreeableness of the both companies, the effect of

Openness to Experience amounts to:

For the company under SAM, the effect amounts to:

3377020.886−915656.586∗3.714=−23269.846

For the financially healthy company, the effect amounts to:

3377020.886−915656.586∗3.372=289793.141

This small mathematical example shows the magnitude of the interaction on the effect that

is examined in the paper. This is yet another confirmation that the interaction is a factor that

should not be left out.

Unfortunately, but unsurprisingly, the residual plot still shows the non-normality because of

the non-random selection of the sample.

12100000 12200000 12300000 12400000 12500000 12600000 12700000

-200000

-150000

-100000

-50000

0

50000

100000

Residual Plot

Predicted Revenue

Resid

uals

Figure 5: Residual plot of the regression of company revenue on the Big Five, job tenure and the interaction of Openness to Experience and Agreeableness

25

Looking at the other factors, it is visible that job tenure, Conscientiousness and Extraversion

are not statistically significant. Because Neuroticism is statistically significant, it might be

useful to see if the interaction effect of Neuroticism with Openness to Experience is an

improvement over the sixth model. However, neither the model where this interaction was

added to the sixth model, nor the one where it was added to the seventh were an

improvement of the seventh model with respect to the adjusted R-square. Therefore, I will

not include them. These excluded regression models can be found in appendix three.

4.3.8 Model 8

In this model, I will delete the variable with the highest p-value, Extraversion:

Regression StatisticsMultiple R - correlation coefficient 0,940R-square 0,883Adjusted R-square 0,806Standard error 69495,233Observations 16

Coefficients Standard Error t Stat P-valueIntercept -1306586,869 5637633,674 -0,232 0,822Job Tenure 4715,422 2654,766 1,776 0,109Openness to Experience 3361118,873 1542762,316 2,179 0,057Conscientiousness 408041,550 283858,616 1,437 0,184Agreeableness 2846034,943 1329889,908 2,140 0,061Neuroticism 731400,322 223490,569 3,273 0,010Openness to Experience * Agreeableness -913397,110 417416,622 -2,188 0,056

Table 13: regression of company revenue on the Openness to Experience, Conscientiousness, Agreeableness, Neuroticism, job tenure and the interaction of Openness to Experience and Agreeableness

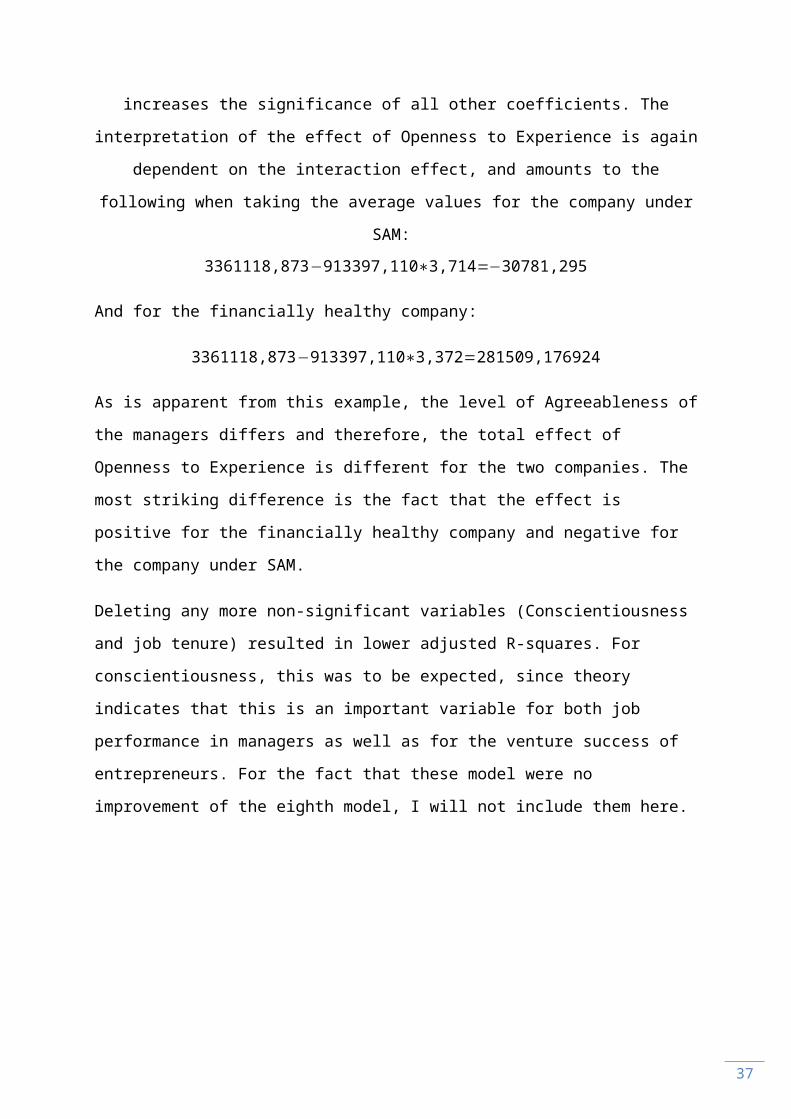

Deleting this variable from the equation has improved the model (as indicated by a higher

adjusted R-squared). It also increases the significance of all other coefficients. The

interpretation of the effect of Openness to Experience is again dependent on the interaction

effect, and amounts to the following when taking the average values for the company under

SAM:

3361118,873−913397,110∗3,714=−30781,295

And for the financially healthy company:

3361118,873−913397,110∗3,372=281509,176924

26

As is apparent from this example, the level of Agreeableness of the managers differs and

therefore, the total effect of Openness to Experience is different for the two companies. The

most striking difference is the fact that the effect is positive for the financially healthy

company and negative for the company under SAM.

Deleting any more non-significant variables (Conscientiousness and job tenure) resulted in

lower adjusted R-squares. For conscientiousness, this was to be expected, since theory

indicates that this is an important variable for both job performance in managers as well as

for the venture success of entrepreneurs. For the fact that these model were no

improvement of the eighth model, I will not include them here.

Since this model is the model with the highest explanatory value (as indicated by the

Adjusted R-squared), I will discuss the residual plot:

12100000 12200000 12300000 12400000 12500000 12600000 12700000

-150000

-100000

-50000

0

50000

100000

Residual Plot

Predicted Revenue

Resid

uals

Figure 6: Residual plot of the regression of company revenue on the Openness to Experience, Conscientiousness, Agreeableness, Neuroticism, job tenure and the interaction of Openness to Experience and Agreeableness

The division into two groups of the sample is very clear, indication non-normality of the data.

However, when comparing to the previous residual plots, the residuals have decreased in

seze, indicating a better-fitting model.

5. Conclusion

To answer the research question "Does Openness to Experience (as part of a manager's

personality) have an influence on the financial performance of the company?", the regression

models show that Openness to Experience has a significant (p value 0.057) and positive

27

influence on company performance as measured by revenues. Moreover, the interaction

effect between Openness to Experience and Agreeableness is negative, which means that

the effect of Openness to Experience decreased when the value of Agreeableness increases.

This effect was very visible in both companies as well, the company under SAM for instance,

had a higher value for Agreeableness than the financially healthy company, which resulted in

a negative overall effect of Openness to Experience for this company. For the financially

healthy company, which had a lower value of Agreeableness, the overall effect was positive.

Therefore, the hypothesis "Average managers' openness to experience will have a positive

influence on company revenues" is rejected. From the results it has become clear that the

interaction between Openness to Experience and Agreeableness has a significant effect on

the overall effect of Openness to Experience. The model which was presented in the theory

section, must be adjusted.

Now, the model visualizes the direct effect of Openness to Experience (as indicated by the

horizontal arrow), which is positive, and the interaction effect (as represented by the vertical

arrow), which is negative. Despite the fact that the coefficient of the interaction is smaller

than the coefficient of Openness to Experience, it turns negative when the value of

Agreeableness exceeds 3.680.

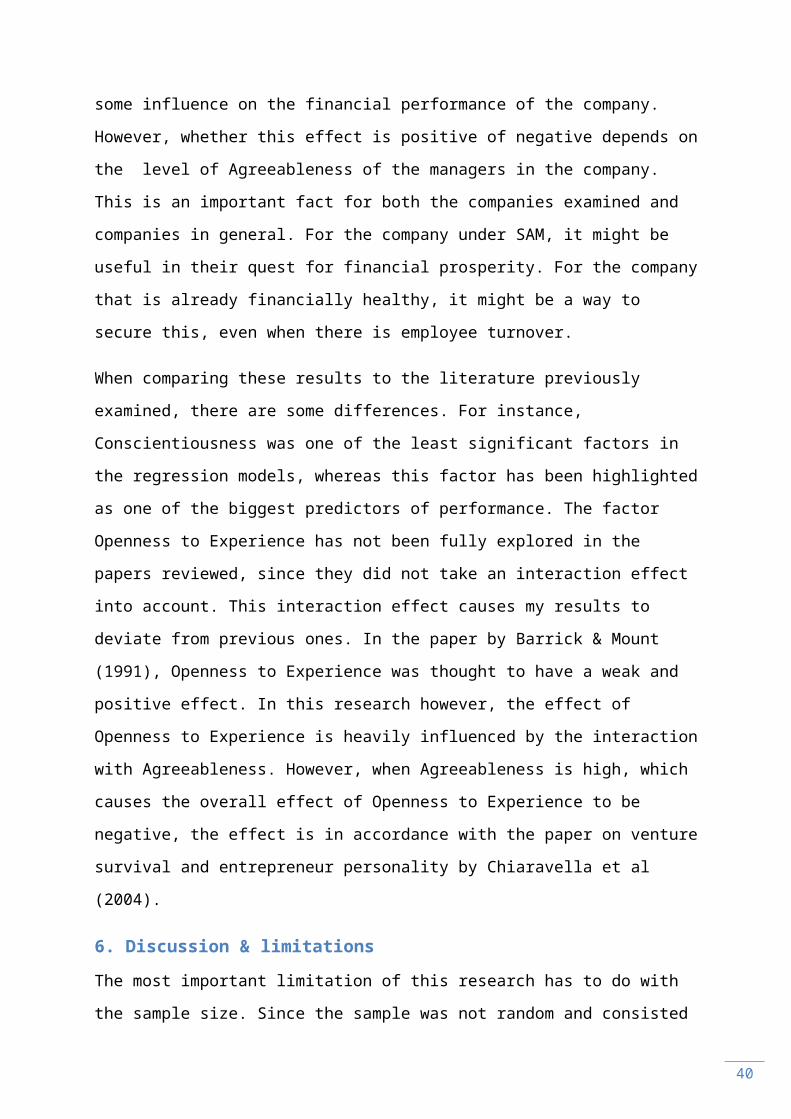

The implications of this research are the following: all in all, Openness to Experience seems

to be a factor that has quite some influence on the financial performance of the company.

However, whether this effect is positive of negative depends on the level of Agreeableness

of the managers in the company. This is an important fact for both the companies examined

and companies in general. For the company under SAM, it might be useful in their quest for

financial prosperity. For the company that is already financially healthy, it might be a way to

secure this, even when there is employee turnover.

(-)

(+)Company RevenuesManager's Openness to Experience

Manager's Agreeableness

28

When comparing these results to the literature previously examined, there are some

differences. For instance, Conscientiousness was one of the least significant factors in the

regression models, whereas this factor has been highlighted as one of the biggest predictors

of performance. The factor Openness to Experience has not been fully explored in the

papers reviewed, since they did not take an interaction effect into account. This interaction

effect causes my results to deviate from previous ones. In the paper by Barrick & Mount

(1991), Openness to Experience was thought to have a weak and positive effect. In this

research however, the effect of Openness to Experience is heavily influenced by the

interaction with Agreeableness. However, when Agreeableness is high, which causes the

overall effect of Openness to Experience to be negative, the effect is in accordance with the

paper on venture survival and entrepreneur personality by Chiaravella et al (2004).

6. Discussion & limitations

The most important limitation of this research has to do with the sample size. Since the

sample was not random and consisted of only 16 people, the representativeness of this

research is very limited. Moreover, since this paper has focused on the data from a survey,

the typical survey limitations apply:

- Common method bias, the potential inflation of correlations between measures that are

computed via the same method (e.g., self-report) (Meade, Watson, & Kroustalis, 2007).

However, this bias is likely to be small to moderate in organizational research (Meade,

Watson, & Kroustalis, 2007).

- Social desirability (or self-deception) bias, the possibility that respondents answer the

questions in a way that portrays them as nicer, better persons. However, this effect is

expected to be small, because the stakes are low with regard to the outcomes of this paper.

- The possibility that the Big Five personality factors are not comprehensive enough. This

topic has been investigated by Judge et al (1991), claiming that the evidence suggests that

virtually all personality measures can be categorized or led back to the Big Five.

- Survey outcomes can be seen as a snapshot, it might be that something that happened

before taking the survey has influenced the respondent, inducing them to answer in a way

that is not representative of their normal behavior or feelings.

29

There are multiple recommendations for future research. I will start with the most common

and most obvious: a bigger, randomly selected sample. With regard to sample size, this

research can be pegged as more exploratory than explanatory. However, since the results

indicated an effect, true explanatory research is recommended.

Secondly, it might be interesting if the relations found in these two Dutch companies can be

confirmed in different countries.

All in all, this research has contributed to research regarding financial performance, which

tends to focus on other financial indicators. This research shows that the personalities in a

company are forces to reckon with. Moreover, this research seems to indicate that the

different aspects have a different influence than expected, because of interaction effects.

30

7. References

Airioldi, M. (2013). Disinvestments in Practice: Overcoming Resistance to Change through a Sociotechnical Approach with Local Stakeholders. Journal of Health Polotics Policy and Law (38), 1149-1171.

Allport, G. W. (1936). Trait-names: A psycho-lexical study. Psychological Monographs , i-171.

Barrick, M. R., & Mount, M. K. (1991). The Big Five Personality Dimensions and Job Performance: A Meta-Analysis. Personnel Psychology (44), 1-26.

Capon, N. F. (1990). Determinants of Financial Performance: a Meta-Analysis. Journal of Management Science , 1143-1159.

Cattell, R. B. (1943). The description of personality: basic traits resolved into clusters. The Journal of Abnormal and Social Psychology , 476-506.

Cattell, R. B. (1945). The Description of Personality: Principles and Findings in a Factor Analysis. The American Journal of Psychology , 69-90.

Centraal Bureau voor de Statistiek. (2015, April 15). Bedrijfsleven; arbeids- en financiële gegevens, per branche, SBI 2008. Retrieved Juli 15, 2015, from Statline; Centraal Bureau voor de Statistiek: http://statline.cbs.nl/Statweb/publication/?DM=SLNL&PA=81156NED&D1=1,3-21&D2=38,228&D3=3-4&HDR=G2,G1&STB=T&VW=T

Choe, & Yongduk. (2013). Resistance to Organizational Change and Organizational Commitment: The Mediating Role of Job Stress and the Moderating Roles of Union Instrumentality and Procedural Justice. Korean Journal of Management (21), 1-36.

Ciavarella, M. A., Buchholtz, A. K., Riordan, C. M., Gatewood, R. D., & Stokes, G. S. (2004). The Big Five and Venture Survival: Is there a linkage? Journal of Business Venturing (19), 465-483.

Costa, J. P., & McCrae, R. R. (1994). Set like plaster? Evidence for the stability of adult personality. American Psychological Association , 21-40.

Fiske, D. W. (1949). Consistency of the factorial structures of personality ratings from diffent sources. The Journal of Abnormal and Social Psychology , 329-344.

Goldberg, L. R. (1981). Language and Individual differences: the search for universals in personality lexicons. Review of personality and social psychology , 141-165.

Gosling, S. D. (2003). A very brief measure of the Pig-Five personality domains. Journal of Research in Personality , 504-528.

Hg, T. W. (2010). Organizational Tenure and Job Performance. Journal of Management , 1220-1250.

Hurtz, G. M., & Donovan, J. J. (2000). Personality and Job Performance: The Big Five Revisited. Journal of Applied Psychology (85), 869-879.

31

IPIP. (n.d.). A Scientific Collaboratory for the Development of Advanced Measures of Personality Traits and Other Individual Differences. Retrieved 6 19, 2015, from International Personality Item Pool: http://ipip.ori.org/

John, O. P. (2001). The Big Five Trait Taxonomy: History, Measurement, and Theoretical Perspectives. In O. P. John, Handbook of personality: Theory and research. New York: The Guilford Press.

Lundy, V., & Morin, P.-P. (2013). Project Leadership Influences Resistance to Change: The Case of the Canadian Public Service. Project Management Journal (44), 45-64.

McCrae, R. R. (1994). Openness to Experience: expanding the boundaries of Factor V. European Journal of Personality (8), 251-272.

Meade, A. W., Watson, A. M., & Kroustalis, C. M. (2007). Assessing Common Methods Bias in Organizational Research. 22nd Annual Meeting of the Society for Industrial and Organizational Psychology (pp. 1-10). New York: .

Rabobank. (n.d.). Our aim is to enable a business to survive. Retrieved April 29, 2015, from Background stories: Cooperative, Special Asset Management: https://www.rabobank.com/en/about-rabobank/background-stories/cooperative/our-aim-is-to-enable-a-business-to-survive.html

Rothmann, S. C. (2003). The Big Five Personality Dimensions and Job Performance. Journal of Industrial Psychology , 68-74.

32

8. Appendices

8.1 Appendix 1: survey in Dutch (as distributed to the respondents)

Welkom en bij voorbaat dank voor uw participatie in deze enquête. Wij willen graag benadrukken dat het van groot belang is dat u het antwoord kiest dat het dichtste bij uzelf staat. Wij willen u erop attent maken dat er geen 'vorige'-knop is. Wees dus alstublieft zeker over uw antwoord voordat u naar de volgende vraag gaat!

Er is geen vastgestelde tijd waarbinnen u de vragenlijst moet beantwoorden.

Mocht u vragen en/of opmerkingen hebben tijdens de enquête, pauzeer deze, dan kunt u uw vraag sturen naar het volgende e-mail adres:[email protected]. Zou u ons willen vertellen hoeveel jaar u uw huidige functie vervult?

Als u dit niet zeker weet, geef dit dan als volgt aan: "schatting: # jaar"Q1. Kunt u aangeven in hoeverre u het eens bent met de volgende zinnen?Ik heb moeite met het begrijpen van abstracte ideeën.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ2.Ik ben niet geïnteresseerd in abstracte ideeën.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ41.Ik heb een grote woordenschat.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eens

33

Q3.Ik heb geen grote verbeeldingskracht.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ4.Ik zit vol met ideeën.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ5.Ik begrijp zaken snel.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ6.Ik gebruik moeilijke woorden.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ7.Ik besteed tijd aan reflectie.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ8.Ik heb uitstekende ideeën.

34

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ9.Ik heb een levendige fantasie.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ10.Ik ben de gangmaker op een feest.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ11.Ik praat niet zo veel.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ12.Ik blijf op de achtergrond.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ13.Ik praat met veel verschillende mensen op feesten.

Sterk mee oneens

Mee oneens

35

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ14.Ik ben stil in het gezelschap van vreemden.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ15.Ik vind het niet erg om het middelpunt van de aandacht te zijn.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ16.Ik vind het niet leuk om de aandacht op mezelf te vestigen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ17.Ik heb niet zo veel te zeggen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ18.Ik start conversaties.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

36

Sterk mee eensQ19.Ik voel me comfortabel in het gezelschap van anderen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ20.Ik vergeet vaak dingen op de juiste plek terug te leggen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ21.Ik ontloop het werk dat ik moet doen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ22.Ik houd van orde.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ23.Ik ga grondig te werk.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ24.

37

Ik volg het plan.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ25.Ik besteed aandacht aan details.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ26.Ik voer mijn klusjes meteen uit.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ27.Ik maak rommel.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ28.Ik laat mijn eigendommen slingeren.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ29.Ik ben altijd voorbereid.

Sterk mee oneens

38

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ30.Ik ben snel gestrest.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ31.Ik ben meestal relaxed.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ32.Ik maak me zorgen over dingen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ33.Ik voel me zelden verdrietig.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ34.Ik ben snel verontrust.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

39

Mee eens

Sterk mee eensQ35.Ik ben snel van streek.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ36.Ik wissel vaak van stemming.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ37.Ik heb regelmatig stemmingswisselingen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ38.Ik ben snel geïrriteerd.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ39.Ik voel me vaak verdrietig.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eens

40

Q40.Ik voel weinig bezorgdheid om anderen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ42.Ik ben teerhartig.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ43.Ik ben niet geïnteresseerd in anderen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ44.Ik voel andermans emoties aan.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ45.Ik zorg ervoor dat anderen zich op hun gemak voelen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ46.Ik doe moeite voor anderen.

41

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ47.Ik ben niet geïnteresseerd in andermans problemen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ48.Ik voel mee met andermans gevoelens.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ49.Ik beledig mensen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ50.Ik ben geïnteresseerd in mensen.

Sterk mee oneens

Mee oneens

Niet mee eens niet mee oneens

Mee eens

Sterk mee eensQ51. Zouden wij uw naam en/of e-mail adres mogen weten?(De antwoorden op deze enquête zullen geanonimiseerd worden en kunnen niet naar u worden teruggeleid)

Mocht u deze informatie liever niet geven, vul dan in:

42

"Zeg ik liever niet"

8.2 Appendix 2: survey translated to English

Welcome and thank you in advance for participating in this survey. We would like to stress that it is imperative that you choose the answer which is closes to your person. Please take notice of the fact that there is no "previous" button. Please be sure of your answer before you proceed to the next question.

There is no time limit for this survey.

If you have any questions or remarks during the time that you are making this survey, please pause your survey response and send your question to the following e-mail address:

Please indicate how much you agree with the following statements:I …

Am the life of the party.Strongly agree / agree / don’t know / disagree / strongly disagree

Feel little concern for others.Strongly agree / agree / don’t know / disagree / strongly disagree

Am always prepared.Strongly agree / agree / don’t know / disagree / strongly disagree

Get stressed out easily.Strongly agree / agree / don’t know / disagree / strongly disagree

Have a rich vocabulary.Strongly agree / agree / don’t know / disagree / strongly disagree

Don't talk a lot.Strongly agree / agree / don’t know / disagree / strongly disagree

Am interested in people.Strongly agree / agree / don’t know / disagree / strongly disagree

Leave my belongings around.Strongly agree / agree / don’t know / disagree / strongly disagree

Am relaxed most of the time.Strongly agree / agree / don’t know / disagree / strongly disagree

Have difficulty understanding abstract ideas.Strongly agree / agree / don’t know / disagree / strongly disagree

Feel comfortable around people. Strongly agree / agree / don’t know /

43

disagree / strongly disagree

Insult people.Strongly agree / agree / don’t know / disagree / strongly disagree

Pay attention to details.Strongly agree / agree / don’t know / disagree / strongly disagree

Worry about things.Strongly agree / agree / don’t know / disagree / strongly disagree

Have a vivid imagination.Strongly agree / agree / don’t know / disagree / strongly disagree

Keep in the background.Strongly agree / agree / don’t know / disagree / strongly disagree

Sympathize with others' feelings.Strongly agree / agree / don’t know / disagree / strongly disagree

Make a mess of things.Strongly agree / agree / don’t know / disagree / strongly disagree

Seldom feel blue.Strongly agree / agree / don’t know / disagree / strongly disagree

Am not interested in abstract ideas.Strongly agree / agree / don’t know / disagree / strongly disagree

Start conversations.Strongly agree / agree / don’t know / disagree / strongly disagree

Am not interested in other people's problems.Strongly agree / agree / don’t know / disagree / strongly disagree

Get chores done right away.Strongly agree / agree / don’t know / disagree / strongly disagree

Am easily disturbed.Strongly agree / agree / don’t know / disagree / strongly disagree

Have excellent ideas.Strongly agree / agree / don’t know / disagree / strongly disagree

Have little to say.Strongly agree / agree / don’t know / disagree / strongly disagree

Have a soft heart.Strongly agree / agree / don’t know / disagree / strongly disagree

Often forget to put things back in their proper place.Strongly agree / agree / don’t know / disagree / strongly disagree

44

Get upset easily.Strongly agree / agree / don’t know / disagree / strongly disagree

Do not have a good imagination.Strongly agree / agree / don’t know / disagree / strongly disagree

Talk to a lot of different people at parties.Strongly agree / agree / don’t know / disagree / strongly disagree

Am not really interested in others.Strongly agree / agree / don’t know / disagree / strongly disagree

Like order.Strongly agree / agree / don’t know / disagree / strongly disagree

Change my mood a lot.Strongly agree / agree / don’t know / disagree / strongly disagree

Am quick to understand things.Strongly agree / agree / don’t know / disagree / strongly disagree

Don't like to draw attention to myself.Strongly agree / agree / don’t know / disagree / strongly disagree

Take time out for others.Strongly agree / agree / don’t know / disagree / strongly disagree

Shirk my duties.Strongly agree / agree / don’t know / disagree / strongly disagree

Have frequent mood swings.Strongly agree / agree / don’t know / disagree / strongly disagree

Use difficult words.Strongly agree / agree / don’t know / disagree / strongly disagree

Don't mind being the center of attention.Strongly agree / agree / don’t know / disagree / strongly disagree

Feel others' emotions.Strongly agree / agree / don’t know / disagree / strongly disagree

Follow a schedule.Strongly agree / agree / don’t know / disagree / strongly disagree

Get irritated easily.Strongly agree / agree / don’t know / disagree / strongly disagree

Spend time reflecting on things.Strongly agree / agree / don’t know / disagree / strongly disagree

45

Am quiet around strangers.Strongly agree / agree / don’t know / disagree / strongly disagree

Make people feel at ease.Strongly agree / agree / don’t know / disagree / strongly disagree

Am exacting in my work.Strongly agree / agree / don’t know / disagree / strongly disagree

Often feel blue.Strongly agree / agree / don’t know / disagree / strongly disagree

Am full of ideas.Strongly agree / agree / don’t know / disagree / strongly disagree

Could you tell us your name or e-mail address? (the answers to this survey will be kept anonymous and cannot be traced back to you)

If you would rather not provide this information, please write "I prefer not to"

Please note, since the Dutch survey was in a certain format and I did not send out an English version, the questions are presented in a different manner. However, the questions are exactly the same.

8.3 Excluded regression models

Regression of company revenue on all Big Five, job tenure and the interaction of Openness to Experience and Neuroticism:

Regression StatisticsMultiple R - correlation coefficient 0,943R-square 0,889Adjusted R-square 0,792Standard error 71953,956Observations 16

Coefficients Standard Error t Stat P-valueIntercept 5724868,891 2753728,066 2,079 0,071Job Tenure 1978,734 3017,109 0,656 0,530Openness to Experience 1384296,894 680615,950 2,034 0,076Conscientiousness 225623,669 272054,067 0,829 0,431Extraversion -32886,421 269464,812 -0,122 0,906Agreeableness -20288,542 50301,036 -0,403 0,697Neuroticism 2530764,890 1040662,971 2,432 0,041Openness to Experience * Agreeableness -574040,366 280189,191 -2,049 0,075

46

Regression of company revenue on all Big Five, job tenure, the interaction of Openness to Experience and Agreeableness and the interaction of Openness to Experience and Neuroticism

Regression StatisticsMultiple R - correlation coefficient 0,949R-square 0,900Adjusted R-square 0,785Standard error 73050,697Observations 16

Coefficients Standard Error t Stat P-valueIntercept 641027,194 6461592,398 0,099 0,924Job Tenure 2999,079 3278,655 0,915 0,391Openness to Experience 2835435,882 1800689,582 1,575 0,159Conscientiousness 341256,494 306338,915 1,114 0,302Extraversion -30371,266 52358,377 -0,580 0,580Agreeableness 1784489,290 2100389,943 0,850 0,424Neuroticism 1688227,444 1431200,702 1,180 0,277Openness to Experience * Agreeableness -575211,947 659124,853 -0,873 0,412Openness to Experience * Neuroticism -295770,212 427307,996 -0,692 0,511