opening accounts for high customers bsattsmedia.ttstrain.com/highriskcusthy080715.pdf · opening...

TRANSCRIPT

© gettechnical inc. 1

©Gettechnical Inc. 1

Opening Accounts for High Risk CustomersBSA Series2015

The material used in this text has been drawn from sources believed to be reliable. Every effort has been made to assure the accuracy of thematerial; however, the accuracy of this information is not guaranteed. The laws are often changed without prior notice from the government.The publisher and the editor are not engaging in the practice of law or accounting. We are not responsible for the actions of your company'semployees.

Instructor Deborah L Crawford • Debbie is the President of Gettechnical

Inc, a Virginia based training company. Her combined banking and training experience began in 1984 and she is a deposit side expert. She received her Bachelors and Masters degrees from Louisiana State University.

• If you have any questions just call 1‐800‐354‐3051 or email us at [email protected].

• You can find our state law chart at gettechnicalinc.com under resource tab. These resources are free and will help you to locate your state law issues.

©Gettechnical Inc. 2

© gettechnical inc. 2

3

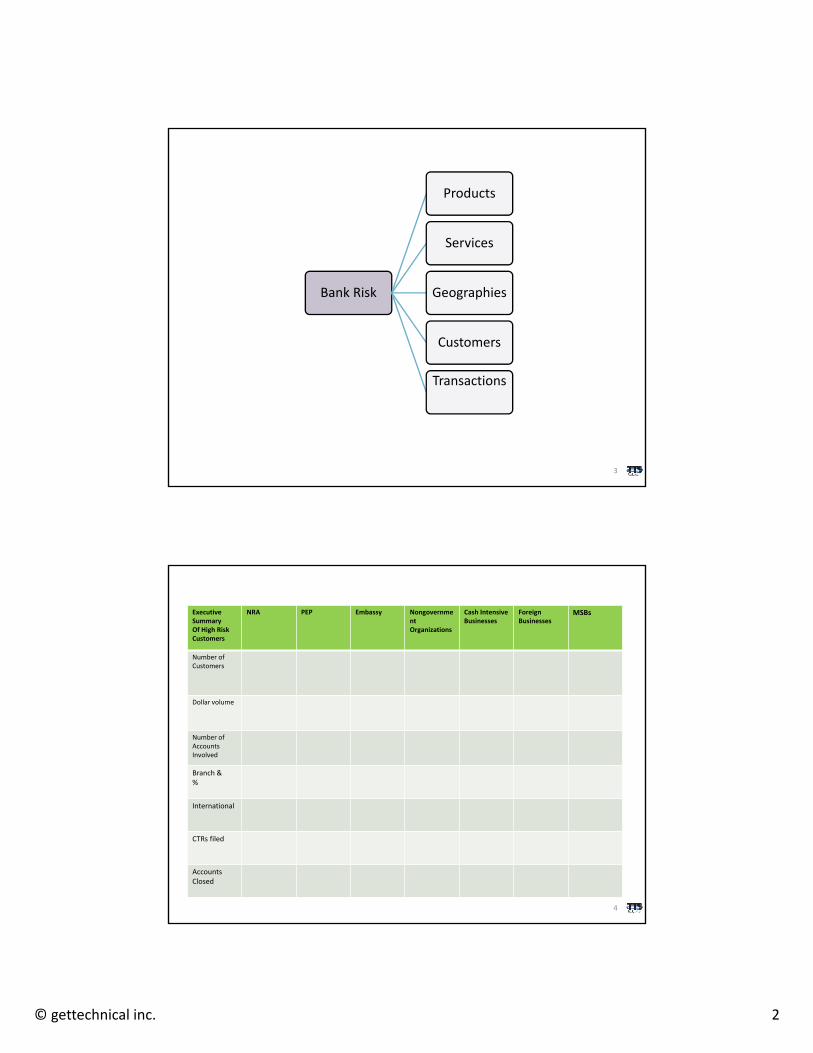

Bank Risk

Products

Services

Geographies

Customers

Transactions

4

ExecutiveSummaryOf High RiskCustomers

NRA PEP Embassy NongovernmentOrganizations

Cash Intensive Businesses

ForeignBusinesses

MSBs

Number of Customers

Dollar volume

Number of Accounts Involved

Branch &%

International

CTRs filed

Accounts Closed

© gettechnical inc. 3

5

Nonresident Alien (NRA) Inherent Risk# of Customers Involved, # of Transactions, Fee Income andDollar Volume

Risk MitigationSafe guards in place

Residual RiskWhat’s left

Legal Risk

Compliance Risk

Consumer Risk

Reputational Risk

IT Risk

Thirty Party Risk

Transaction Risk

Should be one of these on every Customer Group

It’s funny how things time out…

• In preparing for this program, a FIL was issued by the FDIC.

• Whether your examined by the FDIC or another examining body there is something to be learned from the recent FIL coming out from the FDIC….

• Blanket de‐risking may not be the best idea ever.

6

© gettechnical inc. 4

FDIC FIL 5‐2015

• The FDIC encourages insured depository institutions to serve their communities and recognizes the importance of services they provide.

• The FDIC encourages institutions to take a risk‐based approach in assessing individual customer relationships rather than declining to provide banking services to entire categories of customers without regard to the risks presented by an individual customer or the bank’s ability to manage the risk.

• Individual customers within broader customer categories present varying degrees of risk.

• Institutions are expected to assess the risks posed by an individual customer on a case‐by‐case basis and to implement controls to manage the relationship commensurate with the risks associated with each customer.

7

8

Base questions ask every customer

Low Risk

Medium Risk

High Risk

Very High Risk

Instead of de‐risking an entire group…you can possibly bank within the group the types of customers that may meet your risk profile

© gettechnical inc. 5

Risk

• Compliance Risk• Legal Risk• Transactional Risk• Consumer Risk• Credit Risk • Geographic Risk• Third Party Risk (KYCC)• Third Party Vendor Risk• OFAC Risk • IT Risk

9

Look at..

• Inherent Risk

• Risk Mitigation

• Residual Risk

10

© gettechnical inc. 6

11

Current CIP

(a) Customer Identification Program: minimum requirements—

1) In general. A bank must implement a written Customer Identification Program (CIP) appropriate for its size and type of business that, at a minimum, includes each of the requirements of paragraphs (a)(1) through (5) of this section. If a bank is required to have an anti‐money laundering compliance program under the regulations implementing 31 U.S.C. 5318(h), 12 U.S.C. 1818(s), or 12 U.S.C. 1786(q)(1), then the CIP must be a part of the anti‐money laundering compliance program. Until such time as credit unions, private banks, and trust companies without a Federal functional regulator are subject to such a program, their CIPs must be approved by their boards of directors.

12

© gettechnical inc. 7

IDENTIFY THE CUSTOMER

13

• (2) Identity verification procedures. The CIP must include risk‐based procedures for verifying the identity of each customer to the extent reasonable and practicable. The procedures must enable the bank to form a reasonable belief that it knows the true identity of each customer. These procedures must be based on the bank's assessment of the relevant risks, including those presented by the various types of accounts maintained by the bank, the various methods of opening accounts provided by the bank, the various types of identifying information available, and the bank's size, location, and customer base. At a minimum, these procedures must contain the elements described in this paragraph (a)(2).

14

© gettechnical inc. 8

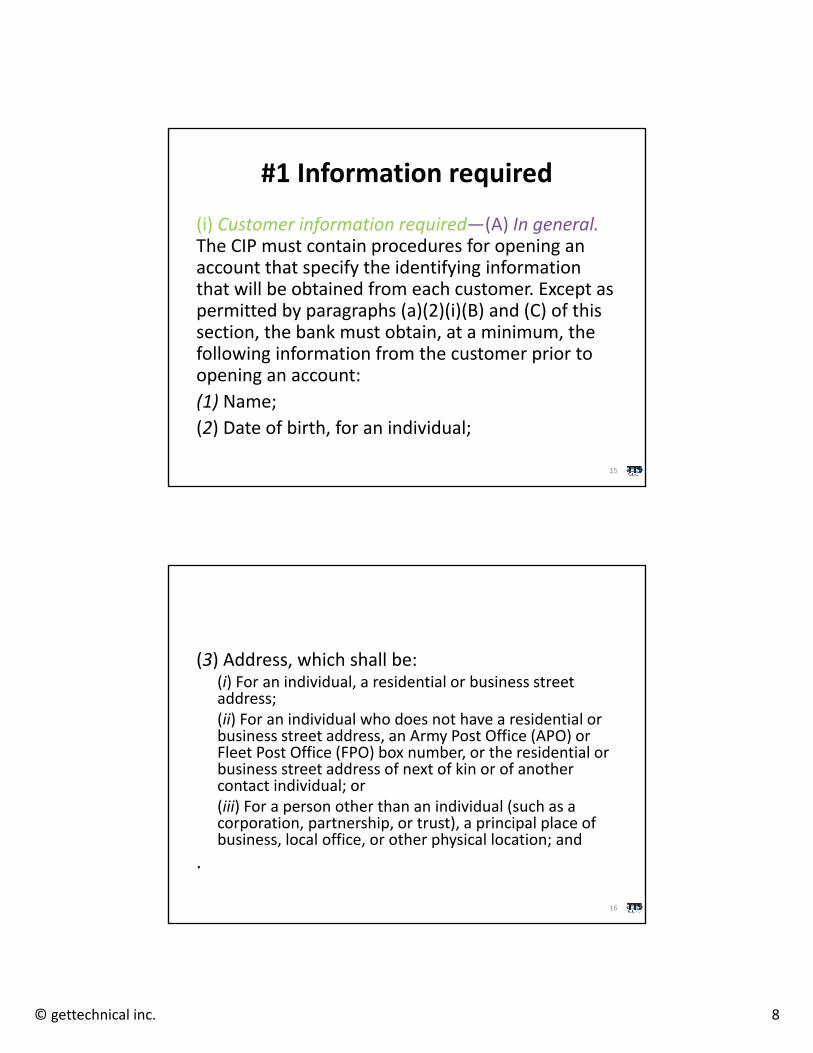

#1 Information required

(i) Customer information required—(A) In general.The CIP must contain procedures for opening an account that specify the identifying information that will be obtained from each customer. Except as permitted by paragraphs (a)(2)(i)(B) and (C) of this section, the bank must obtain, at a minimum, the following information from the customer prior to opening an account:

(1) Name;

(2) Date of birth, for an individual;

15

(3) Address, which shall be:(i) For an individual, a residential or business street address;(ii) For an individual who does not have a residential or business street address, an Army Post Office (APO) or Fleet Post Office (FPO) box number, or the residential or business street address of next of kin or of another contact individual; or(iii) For a person other than an individual (such as a corporation, partnership, or trust), a principal place of business, local office, or other physical location; and

.

16

© gettechnical inc. 9

(4) Identification number, which shall be:(i) For a U.S. person, a taxpayer identification number; or(ii) For a non‐U.S. person, one or more of the following: A taxpayer identification number; passport number and country of issuance; alien identification card number; or number and country of issuance of any other government‐issued document evidencing nationality or residence and bearing a photograph or similar safeguard.

NOTE TO PARAGRAPH a)(2)(i)(A)(4)(II): When opening an account for a foreign business or enterprise that does not have an identification number, the bank must request alternative government‐issued documentation certifying the existence of the business or enterprise

17

(B) Exception for persons applying for a taxpayer identification number.Instead of obtaining a taxpayer identification number from a customer prior to opening the account, the CIP may include procedures for opening an account for a customer that has applied for, but has not received, a taxpayer identification number. In this case, the CIP must include procedures to confirm that the application was filed before the customer opens the account and to obtain the taxpayer identification number within a reasonable period of time after the account is opened.(C) Credit card accounts. In connection with a customer who opens a credit card account, a bank may obtain the identifying information about a customer required under paragraph (a)(2)(i)(A) by acquiring it from a third‐party source prior to extending credit to the customer.

18

© gettechnical inc. 10

#2 Verification—document and Nondocument

(ii) Customer verification. The CIP must contain procedures for verifying the identity of the customer, using information obtained in accordance with paragraph (a)(2)(i) of this section, within a reasonable time after the account is opened. The procedures must describe when the bank will use documents, non‐documentary methods, or a combination of both methods as described in this paragraph (a)(2)(ii).(A) Verification through documents. For a bank relying on documents, the CIP must contain procedures that set forth the documents that the bank will use. These documents may include:

(1) For an individual, unexpired government‐issued identification evidencing nationality or residence and bearing a photograph or similar safeguard, such as a driver's license or passport; and(2) For a person other than an individual (such as a corporation, partnership, or trust), documents showing the existence of the entity, such as certified articles of incorporation, a government‐issued business license, a partnership agreement, or trust instrument.

19

(B) Verification through non‐documentary methods. For a bank relying on non‐documentary methods, the CIP must contain procedures that describe the non‐documentary methods the bank will use.

(1) These methods may include contacting a customer; independently verifying the customer's identity through the comparison of information provided by the customer with information obtained from a consumer reporting agency, public database, or other source; checking references with other financial institutions; and obtaining a financial statement.(2) The bank's non‐documentary procedures must address situations where an individual is unable to present an unexpired government‐issued identification document that bears a photograph or similar safeguard; the bank is not familiar with the documents presented; the account is opened without obtaining documents; the customer opens the account without appearing in person at the bank; and where the bank is otherwise presented with circumstances that increase the risk that the bank will be unable to verify the true identity of a customer through documents.

20

© gettechnical inc. 11

(C) Additional verification for certain customers. The CIP must address situations where, based on the bank's risk assessment of a new account opened by a customer that is not an individual, the bank will obtain information about individuals with authority or control over such account, including signatories, in order to verify the customer's identity. This verification method applies only when the bank cannot verify the customer's true identity using the verification methods described in paragraphs (a)(2)(ii)(A) and (B) of this section.

21

#3 Lack of verification

(iii) Lack of verification. The CIP must include procedures for responding to circumstances in which the bank cannot form a reasonable belief that it knows the true identity of a customer. These procedures should describe:

(A) When the bank should not open an account;

(B) The terms under which a customer may use an account while the bank attempts to verify the customer's identity;

(C) When the bank should close an account, after attempts to verify a customer's identity have failed; and

(D) When the bank should file a Suspicious Activity Report in accordance with applicable law and regulation.

22

© gettechnical inc. 12

OTHER PROVISIONS OF CIP

23

• (3) Recordkeeping. The CIP must include procedures for making and maintaining a record of all information obtained under the procedures implementing paragraph (a) of this section.

24

© gettechnical inc. 13

• (4) Comparison with government lists. The CIP must include procedures for determining whether the customer appears on any list of known or suspected terrorists or terrorist organizations issued by any Federal government agency and designated as such by Treasury in consultation with the Federal functional regulators. The procedures must require the bank to make such a determination within a reasonable period of time after the account is opened, or earlier, if required by another Federal law or regulation or Federal directive issued in connection with the applicable list. The procedures must also require the bank to follow all Federal directives issued in connection with such lists.

25

(5)(i) Customer notice. The CIP must include procedures for providing bank customers with adequate notice that the bank is requesting information to verify their identities.(ii) Adequate notice. Notice is adequate if the bank generally describes the identification requirements of this section and provides the notice in a manner reasonably designed to ensure that a customer is able to view the notice, or is otherwise given notice, before opening an account. For example, depending upon the manner in which the account is opened, a bank may post a notice in the lobby or on its Web site, include the notice on its account applications, or use any other form of written or oral notice.

26

© gettechnical inc. 14

(iii) Sample notice. If appropriate, a bank may use the following sample language to provide notice to its customers:Important Information About Procedures for Opening a New AccountTo help the government fight the funding of terrorism and money laundering activities, Federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an account.What this means for you: When you open an account, we will ask for your name, address, date of birth, and other information that will allow us to identify you. We may also ask to see your driver's license or other identifying documents.

27

(6) Reliance on another financial institution. The CIP may include procedures specifying when a bank will rely on the performance by another financial institution (including an affiliate) of any procedures of the bank's CIP, with respect to any customer of the bank that is opening, or has opened, an account or has established a similar formal banking or business relationship with the other financial institution to provide or engage in services, dealings, or other financial transactions, provided that:(i) Such reliance is reasonable under the circumstances;(ii) The other financial institution is subject to a rule implementing 31 U.S.C. 5318(h) and is regulated by a Federal functional regulator; and(iii) The other financial institution enters into a contract requiring it to certify annually to the bank that it has implemented its anti‐money laundering program, and that it will perform (or its agent will perform) the specified requirements of the bank's CIP.

28

© gettechnical inc. 15

29

Impact of CDD

For FinCEN, the key elements of CDD include:

(i) identifying and verifying the identity of customers;(ii) identifying and verifying the identity of beneficial owners of legal entity customers (i.e., the natural persons who own or control legal entities); (iii) understanding the nature and purpose of customer relationships; and (iv) conducting ongoing monitoring to maintain and update customer information and to identify and report suspicious transactions.

30

© gettechnical inc. 16

CDD FOUR ELEMENTS

31

32

Open Business Account

4 Elements of CDD

CIP: Identifying and Verifying the Identity of

Customers

CIP Entity

(If Agent then CIP person acting for business)

CIP Signatories if in Your Policy

CIP Exemptions

Identifying and Verifying the Identity of Beneficial Owners of Legal Entity

Customers

CIP Beneficial Owners of Legal Entities Customers

CIP Exemptions plus those for Beneficial ownership

Understanding the Nature and Purpose of Customer

Relationships

Base transactional questions and more detailed questions for high risk accounts

Assign Risk

Conducting On‐Going Monitoring

© gettechnical inc. 17

Information Required(Prior to opening an account)

+Verification through documents

(Reasonable time after opening account) +

Nondocumentary verification(Reasonable time after opening account)

+CIP Recordkeeping

+ Customer Notice

=CIP COMPLIANCE

33

Element One

Establish a CIP Procedurefor all “customers”

Legal Entity Customers

Ask for 25% Beneficial Owners+

Ask for Controlling Person+

Run Your Institution’s CIP+

CDD Recordkeeping

34

Element Two

Establish beneficial ownership on legal entity customers

© gettechnical inc. 18

Beneficial Ownership

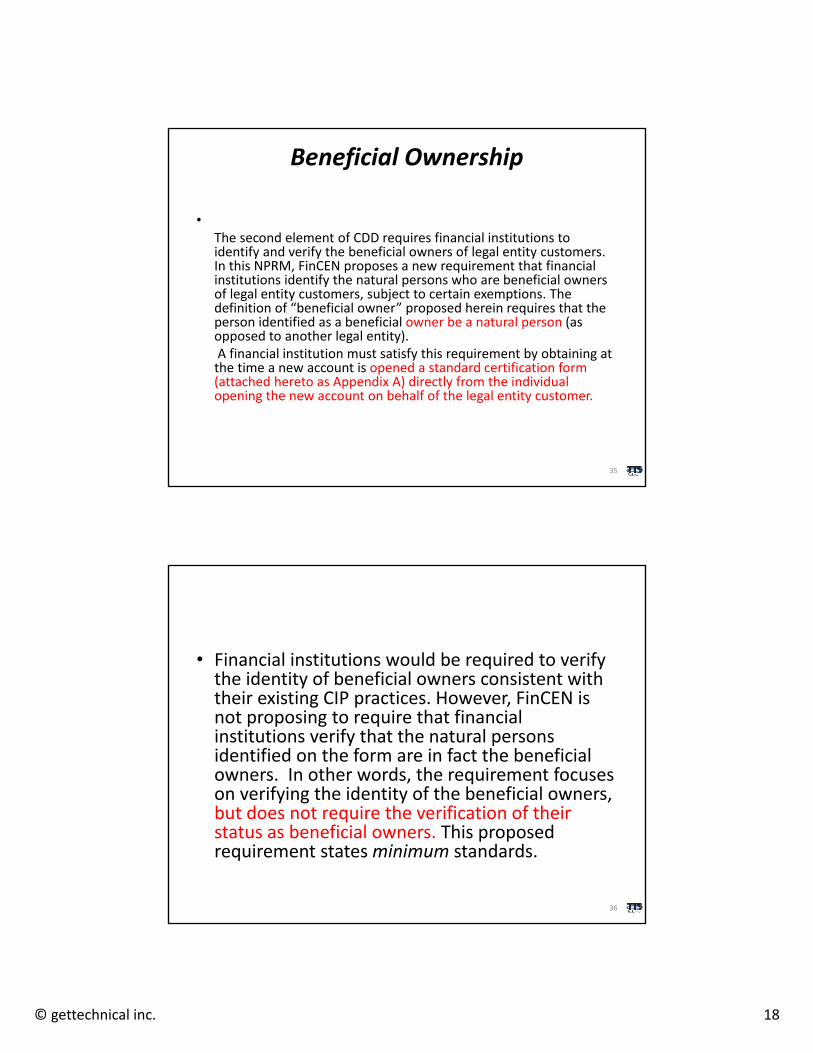

•The second element of CDD requires financial institutions to identify and verify the beneficial owners of legal entity customers. In this NPRM, FinCEN proposes a new requirement that financial institutions identify the natural persons who are beneficial owners of legal entity customers, subject to certain exemptions. The definition of “beneficial owner” proposed herein requires that the person identified as a beneficial owner be a natural person (as opposed to another legal entity). A financial institution must satisfy this requirement by obtaining at the time a new account is opened a standard certification form (attached hereto as Appendix A) directly from the individual opening the new account on behalf of the legal entity customer.

35

• Financial institutions would be required to verify the identity of beneficial owners consistent with their existing CIP practices. However, FinCEN is not proposing to require that financial institutions verify that the natural persons identified on the form are in fact the beneficial owners. In other words, the requirement focuses on verifying the identity of the beneficial owners, but does not require the verification of their status as beneficial owners. This proposed requirement states minimum standards.

36

© gettechnical inc. 19

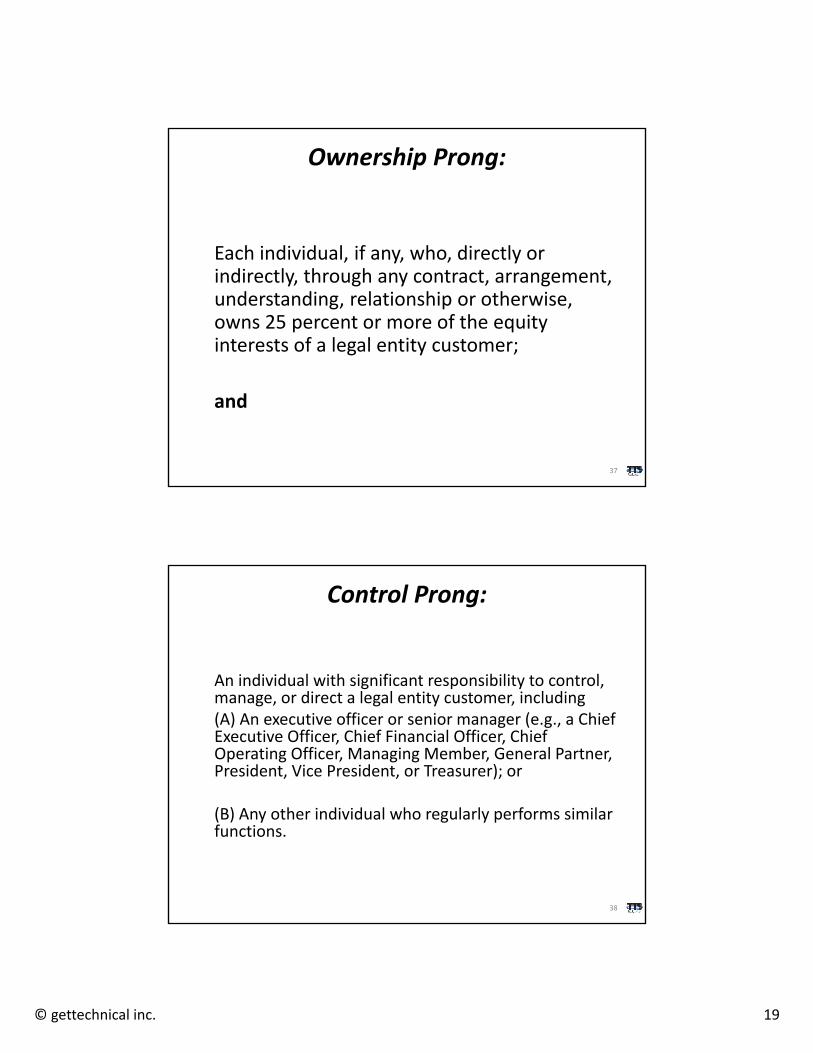

Ownership Prong:

Each individual, if any, who, directly or indirectly, through any contract, arrangement, understanding, relationship or otherwise, owns 25 percent or more of the equity interests of a legal entity customer;

and

37

Control Prong:

An individual with significant responsibility to control, manage, or direct a legal entity customer, including(A) An executive officer or senior manager (e.g., a Chief Executive Officer, Chief Financial Officer, Chief Operating Officer, Managing Member, General Partner, President, Vice President, or Treasurer); or

(B) Any other individual who regularly performs similar functions.

38

© gettechnical inc. 20

Exemptions from beneficial ownership requirement

• Customers Exempt from CIP– Same as CIP except existing customers (financial institutions regulated

by a federal functional regulator, publicly held companies traded on certain US stock exchanges, domestic government agencies and instrumentalities and certain legal entities that exercise governmental authority)

– Plus some new exemptions

• Existing and New Customers– Applies to legal entity customer that open a new account after the

implementation date

39

Plus these new exemptions…

FinCEN proposes that the following entities also be exempt from the beneficial ownership requirement when opening a new account because their beneficial ownership information is generally available from other credible sources:

• An issuer of a class of securities registered under Section 12 of the Securities Exchange Act of 1934 or that is required to file reports under Section 15(d) of that Act;

• Any majority‐owned domestic subsidiary of any entity whose securities are listed on a U.S. stock exchange;• An investment company, as defined in Section 3 of the Investment Company Act of 1940, that is registered with

the SEC under that Act;• An investment adviser, as defined in Section 202(a)(11) of the Investment Advisers Act of 1940, that is registered

with the SEC under that Act;• An exchange or clearing agency, as defined in Section 3 of the Securities Exchange Act of 1934, that is registered

under Section 6 or 17A of that Act;• Any other entity registered with the Securities and Exchange Commission under the Securities and Exchange Act

of 1934.• A registered entity, commodity pool operator, commodity trading advisor, retail foreign exchange dealer, swap

dealer, or major swap participant, each as defined in section 1a of the Commodity Exchange Act, that is registered with the CFTC;

• A public accounting firm registered under section 102 of the Sarbanes‐Oxley Act; and• A charity or nonprofit entity that is described in Sections 501(c), 527, or 4947(a)(1) of the Internal Revenue Code

of 1986, that has not been denied tax exempt status, and that is required to and has filed the most recently required annual information return with the Internal Revenue Service.

40

© gettechnical inc. 21

Verification of Beneficial Owners

• Standard Certification Form

• Verification of Beneficial Owners

– Do not have to verify status

– Do have to verify identity like CIP

41

Updating Beneficial Ownership Information

• No specific requirement to update periodically

• Update when open new account

• Update when activity changes with on‐going monitoring

42

© gettechnical inc. 22

43

44

© gettechnical inc. 23

45

Nature and Purpose: Ask Transactional questions

The third element of CDD requires financial institutions to understand the nature and purpose of customer relationships

in order to develop a customer risk profile.

A bank should obtain information at account opening sufficient to develop an understanding of normal and expected activity

for the customer’s occupation or business operations.

In addition, because this is a necessary step to identifying and reporting suspicious activities, which obligation applies to all “transactions…conducted or attempted by, at or through” the covered financial institution, its scope should not be limited to “customers” for purposes of the CIP rules, but rather should

extend more broadly to encompass all accounts established by the institution

46

Element ThreeAsk Nature, Purpose and Transactional QuestionsApplies to all customers on a risk basis

© gettechnical inc. 24

47

Go further for high risk customers:MSBs+

MRBs+

Cash Intensive Businesses+

Third Party Payment Processors+

Embassy, Foreign Missions and Consulates+

Pay day Lenders+

Nongovernment Organizations+

Professional Service Providers

And many more…

Monitoring

Conduct on‐going monitoring+

Refresh Customer information when necessary+

Must apply not only to “customers” for purposes of the CIP rules, but more broadly to all account relationships maintained by the

covered financial institution

48

Element Four

MonitoringPart of SAR programApplies to everyone

© gettechnical inc. 25

Nonresident Aliens

49

Tax Home

• Your customer's tax home is the general area of your customer's main place of business, employment, or post of duty, regardless of where your customer maintains his or her family home. Your customer's tax home is the place where he or she permanently or indefinitely works as an employee or a self‐employed individual. If your customer does not have a regular or main place of business because of the nature of the customer's work, then your customer's tax home is the place where he/she regularly live. If your customer does not fit either of these categories, he or she is considered an itinerant and your customer's tax home is wherever he or she works.

• For determining whether your customer has a closer connection to a foreign country, your customer's tax home must also be in existence for the entire current year, and must be located in the same foreign country to which he or she are claiming to have a closer connection.

50

© gettechnical inc. 26

Opening of a deposit account

Withholding agent

W‐9 US Person

W‐8BEN or W‐8BENE

Nonresident alien

51

W‐ 8 BEN

Generally, a Form W‐8 BEN provided without a U.S. taxpayer ID number (TIN) will remain in effect for a period starting on the date the form is signed and ending on the last day of the third succeeding calendar year, unless a change in circumstances makes any information on the form incorrect. For example, a Form W‐8 BEN signed on Sept. 30, 2011 remains valid through December 31, 2014. A Form W‐8 BEN furnished with a U.S. TIN will remain in effect until a change in circumstances makes any information on the form incorrect, provided that the withholding agent reports on Form 1042‐S at least one payment annually to the beneficial owner who provided the Form W‐8 BEN.

52

© gettechnical inc. 27

Nonresident Aliens If your customer is an alien (not a U.S. citizen), he or she is considered a nonresident alien unless the customer meets one of the two tests described next under Resident Aliens.

Resident Aliens Your customer is a resident alien of the United States for tax purposes if he/she meets either the green card test or the substantial presence test for calendar year 2015 (January 1‐December 31). Even if he/she does not meet either of these tests, he/she may be able to choose to be treated as a U.S. resident for part of the year.

53

Resident Alien?

#1 Substantial Presence Test

#2 Green Card Test

54

© gettechnical inc. 28

#1 Substantial Presence

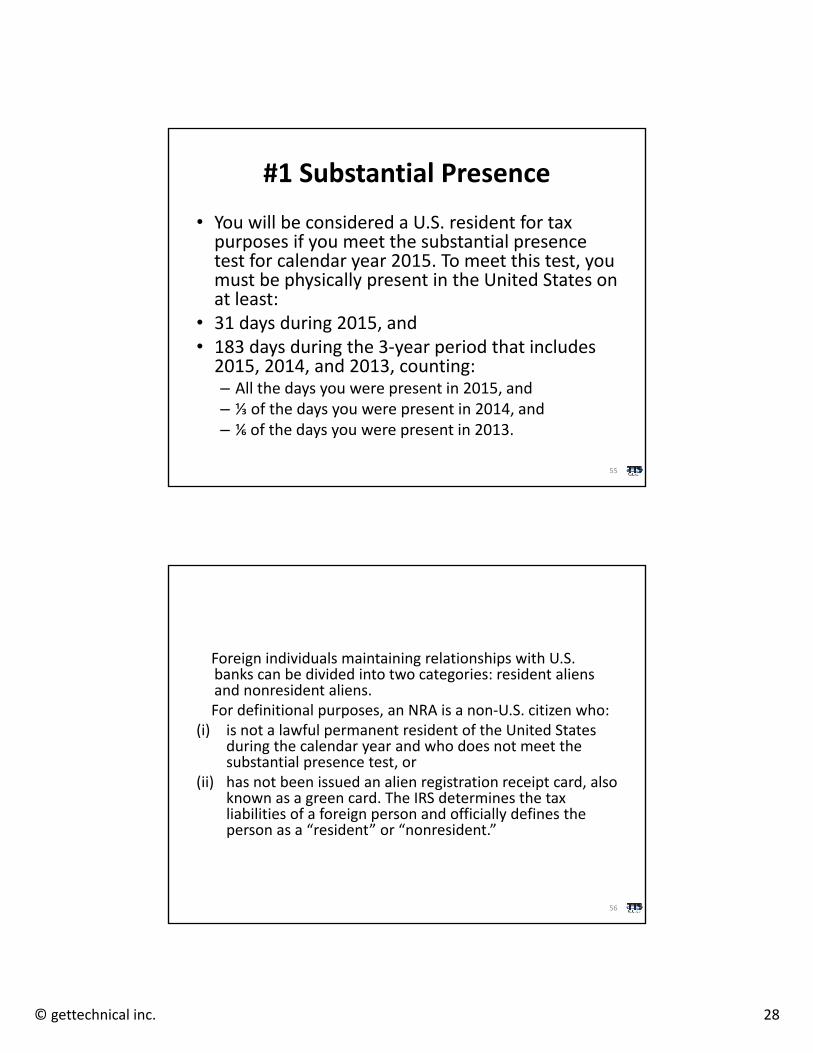

• You will be considered a U.S. resident for tax purposes if you meet the substantial presence test for calendar year 2015. To meet this test, you must be physically present in the United States on at least:

• 31 days during 2015, and • 183 days during the 3‐year period that includes 2015, 2014, and 2013, counting: – All the days you were present in 2015, and– ⅓ of the days you were present in 2014, and– ⅙ of the days you were present in 2013.

55

Foreign individuals maintaining relationships with U.S. banks can be divided into two categories: resident aliens and nonresident aliens. For definitional purposes, an NRA is a non‐U.S. citizen who:

(i) is not a lawful permanent resident of the United States during the calendar year and who does not meet the substantial presence test, or

(ii) has not been issued an alien registration receipt card, also known as a green card. The IRS determines the tax liabilities of a foreign person and officially defines the person as a “resident” or “nonresident.”

56

© gettechnical inc. 29

Although NRAs are not permanent residents, they may have a legitimate need to establish an account relationship with a U.S. bank. NRAs use bank products and services for asset preservation (e.g., mitigating losses due to exchange rates), business expansion, and investments.

The amount of NRA deposits in the U.S. banking system has been estimated to range from hundreds of billions of dollars to about $1 trillion. Even at the low end of the range, the magnitude is substantial, both in terms of the U.S. banking system and the economy.

57

Your customer can still …

Closer Connection to Foreign country

Present Less than 183 days during the year

Maintain a tax home in a foreign country

Have a closer connection during the year to one foreign country

58

© gettechnical inc. 30

# 2 Green Card Test

59

Requirements NRA1. Required Information on Entity:

(Before opening account) Name

Address—Permanent home address

required

Taxpayer identification—US TIN (SSN or

ITIN), TIN of home country and if none date

of birth on W‐8BEN and Passport number

for CIP

Date of Birth

2. IRS Reporting: Report in TIN of owner on 1042S, if any

All NRAs sign a W‐8BEN on the account

3. Documentary Requirements:(Reasonable time after opening)

Valid identification on owners This could be passport, VISA, national

ID card, Driver’s License or Birth Certificates from home country. Whatever your financial institution has defined as acceptable government issued ID.

60

© gettechnical inc. 31

Requirements NRA4. Suggested Nondocument

Verification:(Reasonable time after opening)

A CIP program must also have nondocumentary verification. Suggestions include: Welcome letter Call to customer to thank for business Delivery of checks to location by account

officer Third party verification Previous financial institution references

5. Account Styling: Joseph Garcia6. Consult Government Lists: Section 326 List

OFAC List

7. Insurance: $250,000.

61

1OWNERSHIP Single Party

2TITLEJoseph Garcia

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

I am not a US Person see W-8BEN

4SIGNATURES (Access)

Joseph Garcia

Sample: Nonresident Alien

62

© gettechnical inc. 32

63

Tax treaties are listed in irs.gov Publication 515. But do not need part II for deposit interest.

Checklist for NRA

Required information on NRA owner(s) Report in TIN of owner, if any Valid identification on NRA W‐8BEN on every owner Account Styling: Joseph Garcia Account Ownership: Single or Multiple Party Nondocumentary verification Risk Questionnaire Signature Card Government Lists

64

© gettechnical inc. 33

Risk Questions

• Account holder’s home country

• Types of Products and Services used

• Forms of Identification

• Source of Funds and Wealth

• Usual account activity

65

66

The answers are in the 1042S instructions at irs.gov.

Pay attention to the types of codes going in the system because it will come out on the 1042S

© gettechnical inc. 34

67

68

© gettechnical inc. 35

PEPs

69

• The term “politically exposed person” generally includes a current or former senior foreign political figure, their immediate family, and their close associates. Interagency guidance issued in January 2001 offers banks resources that can help them to determine whether an individual is a PEP. More specifically:

• A “senior foreign political figure” is a senior official in the executive, legislative, administrative, military or judicial branches of a foreign government (whether elected or not), a senior official of a major foreign political party, or a senior executive of a foreign government‐owned corporation. In addition, a senior foreign political figure includes any corporation, business, or other entity that has been formed by, or for the benefit of, a senior foreign political figure.

• The “immediate family” of a senior foreign political figure typically includes the figure’s parents, siblings, spouse, children, and in‐laws.

• A “close associate” of a senior foreign political figure is a person who is widely and publicly known to maintain an unusually close relationship with the senior foreign political figure, and includes a person who is in a position to conduct substantial domestic and international financial transactions on behalf of the senior foreign political figure.

70

© gettechnical inc. 36

Requirements PEP1. Required Information on Entity:

(Before opening account) Name

Address—Permanent home address

required

Taxpayer identification—US TIN (SSN or

ITIN), TIN of home country and if none date

of birth on W‐8BEN and Passport number

for CIP

Date of Birth

2. IRS Reporting: Report in TIN of owner on 1042S, if any

All NRAs sign a W‐8BEN on the account

3. Documentary Requirements:(Reasonable time after opening)

Valid identification on owners This could be passport, VISA, national

ID card, Driver’s License or Birth Certificates from home country. Whatever your financial institution has defined as acceptable government issued ID.

71

Requirements PEP4. Suggested Nondocument

Verification:(Reasonable time after opening)

A CIP program must also have nondocumentary verification. Suggestions include: Welcome letter Call to customer to thank for business Delivery of checks to location by account

officer Third party verification Previous financial institution references

5. Account Styling: Joseph Garcia6. Consult Government Lists: Section 326 List

OFAC List

7. Insurance: $250,000.

72

© gettechnical inc. 37

1OWNERSHIP Single Party

2TITLEJoseph Garcia

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

I am not a US Person see W-8BEN

4SIGNATURES (Access)

Joseph Garcia

Sample: PEP

73

FORM W‐8BEN CERTIFICATE OF FOREIGN STATUS OF BENEFICIAL OWNER FOR U.S. TAX WITHHOLDING

74

© gettechnical inc. 38

Checklist for PEP

Required information on PEP owner(s) Report in TIN of owner, if any Valid identification on PEP W‐8BEN on every owner Account Styling: Joseph Garcia Account Ownership: Single or Multiple Party Nondocumentary verification Risk Questionnaire Signature Card Government Lists

75

These issues are important…

• Official responsibilities of the individual’s office

• Nature and title (e.g. honorary or salaried)

• Level and nature of authority or influence over government activities or other officials

• Access to significant government assets or funds

• Geographic region, industry or sector

76

© gettechnical inc. 39

To open these accounts you must…

• Identify the accountholder and beneficial owner, including the nominal and beneficial owners of companies, trusts, partnerships, private investment companies, or other legal entities that are accountholders.

• Seek information directly from the account holder and beneficial owner regarding possible PEP status.

• Identify the account holder’s and beneficial owner’s country(ies) of residence and the level of risk for corruption and money laundering associated with these jurisdictions.

• Obtain information regarding employment, including industry and sector and the level of risk for corruption associated with the industries and sectors.

77

• Check references, as appropriate, to determine whether the account holder and beneficial owner is or has been a PEP.

• Identify the account holder’s and beneficial owner’s source of wealth and funds.

• Obtain information on immediate family members or close associates either having transaction authority over the account or benefiting from transactions conducted through the account.

• Determine the purpose of the account and the expected volume and nature of account activity.

78

© gettechnical inc. 40

• Make reasonable efforts to review public sources of information. These sources vary depending on each situation; however, banks should check the accountholder and any beneficial owners of legal entities against reasonably accessible public sources of information (e.g., government databases, major news publications, commercial databases and other databases available on the Internet, as appropriate).

79

Embassy, Foreign Consulate and Foreign Mission Accounts

80

© gettechnical inc. 41

• Embassies contain the offices of the foreign ambassador, the diplomatic representative, and their staff. The embassy, led by the ambassador, is a foreign government’s official representation in the United States (or other country). Foreign consulate offices act as branches of the embassy and perform various administrative and governmental functions (e.g., issuing visas and handling immigration matters). Foreign consulate offices are typically located in major metropolitan areas. In addition, foreign ambassadors’ diplomatic representatives, their families, and their associates may be considered politically exposed persons (PEP) in certain circumstances.

81

• Embassies and foreign consulates in the United States require access to the banking system to meet many of their day‐to‐day financial responsibilities. Such services can range from account relationships for operational expenses (e.g., payroll, rent, and utilities) to inter‐ and intra‐governmental transactions (e.g., commercial and military purchases). In addition to official embassy accounts, some banks provide ancillary services or accounts to embassy staff, families, and current or prior foreign government officials. Each of these relationships poses different levels of risk to the bank.

82

© gettechnical inc. 42

83

84

© gettechnical inc. 43

FinCEN

• Guidance on Accepting Accounts from Foreign Governments, Foreign Embassies and Foreign Political Figures (June 15, 2004); Updated Guidance on Accepting Accounts from Foreign Embassies, Consulates and Missions (March 24, 2011).

85

Requirements Embassy

1. Required Information on

Entity:

(Before opening account)

Name

Address

Taxpayer identification— The account will

use the employer identification number

of the corporation.

2. IRS Reporting:Report in TIN of Entity

86

© gettechnical inc. 44

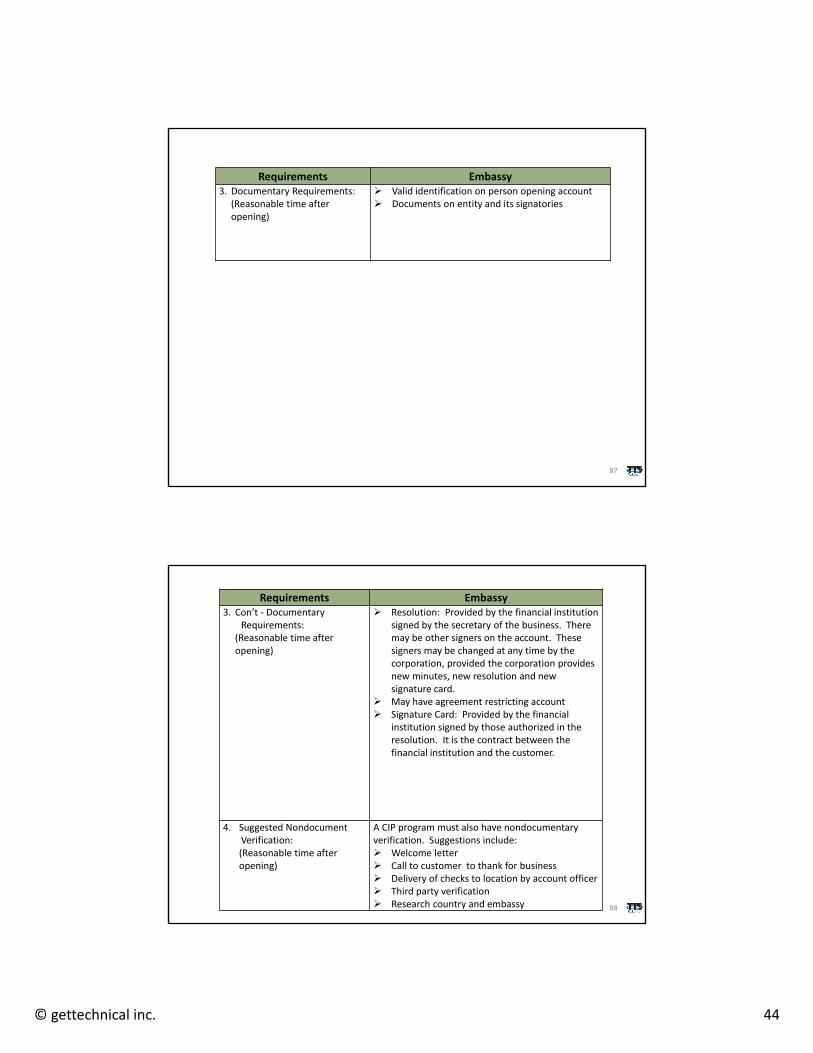

Requirements Embassy3. Documentary Requirements:

(Reasonable time after opening)

Valid identification on person opening account Documents on entity and its signatories

87

Requirements Embassy3. Con’t ‐ Documentary

Requirements:(Reasonable time after opening)

Resolution: Provided by the financial institution signed by the secretary of the business. There may be other signers on the account. These signers may be changed at any time by the corporation, provided the corporation provides new minutes, new resolution and new signature card.

May have agreement restricting account Signature Card: Provided by the financial

institution signed by those authorized in the resolution. It is the contract between the financial institution and the customer.

4. Suggested Nondocument Verification:(Reasonable time after opening)

A CIP program must also have nondocumentary verification. Suggestions include: Welcome letter Call to customer to thank for business Delivery of checks to location by account officer Third party verification Research country and embassy 88

© gettechnical inc. 45

Requirements Embassy

5. Account Styling: The Embassy of the United Kingdom of Great Britain

and Northern Ireland

6. Consult Government Lists: Section 326 List

OFAC List

7. Insurance: Each entity is separately insured for $250,000.

8. Miscellaneous: These accounts may have restricted agreements or

limited purpose accounts

89

1OWNERSHIP Embassy

2TITLE

The Embassy of the United Kingdom of Great Britain and Northern Ireland

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

TIN of Embassy, if any

4SIGNATURES (Access)

Joe SmithMary Smith

Sample: Corporation

90

© gettechnical inc. 46

Checklist for Embassy, Foreign Consulate and Foreign Mission Accounts

Name, address, TIN of embassy

Complete W‐8BEN E ( should be exempt)

Valid identification on Person Opening the Account

Document from Embassy establishing authority

Signature Card

Resolution

Account Styling: The Embassy of the United Kingdom of Great Britain and Northern Ireland

Government lists

91

• Accounts are from countries that have been designated as higher risk.

• Substantial currency transactions take place in the accounts.

• Account activity is not consistent with the purpose of the account (e.g., pouch activity or payable upon proper identification transactions) or account transactions are in unusual amounts.

• Accounts directly fund personal expenses of foreign nationals, including but not limited to expenses for college students.

• Official embassy business is conducted through personal accounts.

92

© gettechnical inc. 47

• Banks may also mitigate risk by entering into a written agreement that clearly defines the terms of use for the account(s), setting forth available services, acceptable transactions and access limitations. Written agreements to provide ancillary services or accounts to embassy, foreign consulate, and foreign mission personnel and their families may also assist in mitigating the varying degrees of risk.

93

• Similarly, the bank could offer limited purpose accounts, such as those used to facilitate operational expense payments (e.g., payroll, rent and utilities, routine maintenance), which are generally considered lower risk and allow the implementation of customary functions in the United States. The type and volume of transactions should be commensurate with the purpose of the limited access account. Account monitoring to ensure compliance with account limitations and the terms of any service agreements is essential to mitigate risks associated with these accounts.

94

© gettechnical inc. 48

Nonbank Financial InstitutionsMSBs Specifically

95

• Casinos and card clubs.• Securities and commodities firms (e.g., brokers/dealers, investment advisers, mutual funds, hedge funds, or commodity traders).

• Money services businesses (MSB).• Insurance companies.• Loan or finance companies.• Operators of credit card systems.• Other financial institutions (e.g., dealers in precious metals, stones, or jewels; pawnbrokers).

96

© gettechnical inc. 49

MSBs include five distinct types of financial services providers and the U.S. Postal Service:

(1) dealers in foreign exchange ;

(2) check cashers;

(3) issuers or sellers of traveler’s checks or money orders,

(4) providers or sellers of prepaid access; and

(5) money transmitters. FinCEN routinely publishes administrative letter rulings that address inquiries regarding whether persons who engage in certain specific business activities are MSBs.

97

Requirements MSB1. Required Information on

Entity:(Before opening account)

Name Address Taxpayer identification— The account can

use the Social Security number of owner if a one person LLC or employer identification number of the business.

2. IRS Reporting: Report in EIN of LLC or may use SSN of member if the LLC is one person.

LLC that is an MSB

98

© gettechnical inc. 50

Requirements MSB3. Documentary

Requirements:(Reasonable time after opening)

Valid identification on person opening the account

My financial institution does/does not require all signers to Complete CIP. Operating Agreement, if any: Provided by the

customer, the agreement between the members of the LLC. It usually names the managing member.

Domestic: Government Issued Document Foreign: Government Issued Document FinCEN Registration State registration(s)

Certification of Beneficial Owner(s), if applicable

Resolution: Provided by financial institution and signed by managing member authorizing others in organization to sign on accounts.

Signature Card: Provided by financial institution; it is the contract between financial institution and customer.

99

Requirements MSB4. Suggested Nondocument

Verification:(Reasonable time after opening)

A CIP program must also have nondocumentary verification. Suggestions include: Welcome letter Call to customer to thank for business Delivery of checks to location by account

officer Third party verification Check with Secretary of State’s Office

5. Account Styling: Name of business:Examples:

Smith Electronics, LLCIf a one person LLC using a Social Security number :

Joe Smith Smith Electronics, LLC

6. Consult Government Lists: Section 326 List OFAC List

7. Insurance: $250,000 per Entity

8. Miscellaneous:

100

© gettechnical inc. 51

Additional requirements

• Review the MSB’s BSA/AML program.• Review results of the MSB’s independent testing of its AML program.• Review written procedures for the operation of the MSB.• Conduct on‐site visits.• Review list of agents, including locations, within or outside the United

States, which receive services directly or indirectly through the MSB account.

• Determine whether the MSB has performed due diligence on any third‐party servicers or paying agents.

• Review written agent management and termination practices for the MSB.• Review written employee screening practices for the MSB.

FinCEN and the federal banking agencies do not expect banks to uniformly require any or all of the actions identified above for all MSBs.

101

Limited Liability Company Resolution

Names the Limited Liability Company: Floral Enterprises, LLC

Lists who can sign What their job is

Joe Smith Managing MemberMary Smith MemberBetty Smith Authorized Signer

Usually a list of what they can and cannot do

Make deposits and WithdrawalsMake loans Other

Joe Smith, Managing MemberAttested to by:Mary Smith, Member

102

© gettechnical inc. 52

1OWNERSHIP Limited Liability Company

2TITLEFloral Enterprises, LLC

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

EIN of LLC

4SIGNATURES (Access)

Joe Smith, Managing memberMary Smith, Member

Betty Smith, Authorized signer

Sample: Multiple Member LLC

103

104

Joe Smith

Floral Enterprises, LLC

Joe Smith

Joe Smith 01/06/2015

Joe Smith 08/14/1977 123 Main Street 439‐00‐9999Monroe, LA xxxxx

Mary Smith 09/15/1976 123 Main Street 439‐11‐0000Monroe, LA xxxxx

Joe Smith 08/14/1977 123 Main Street 439‐00‐9999Monroe, LA xxxxx

© gettechnical inc. 53

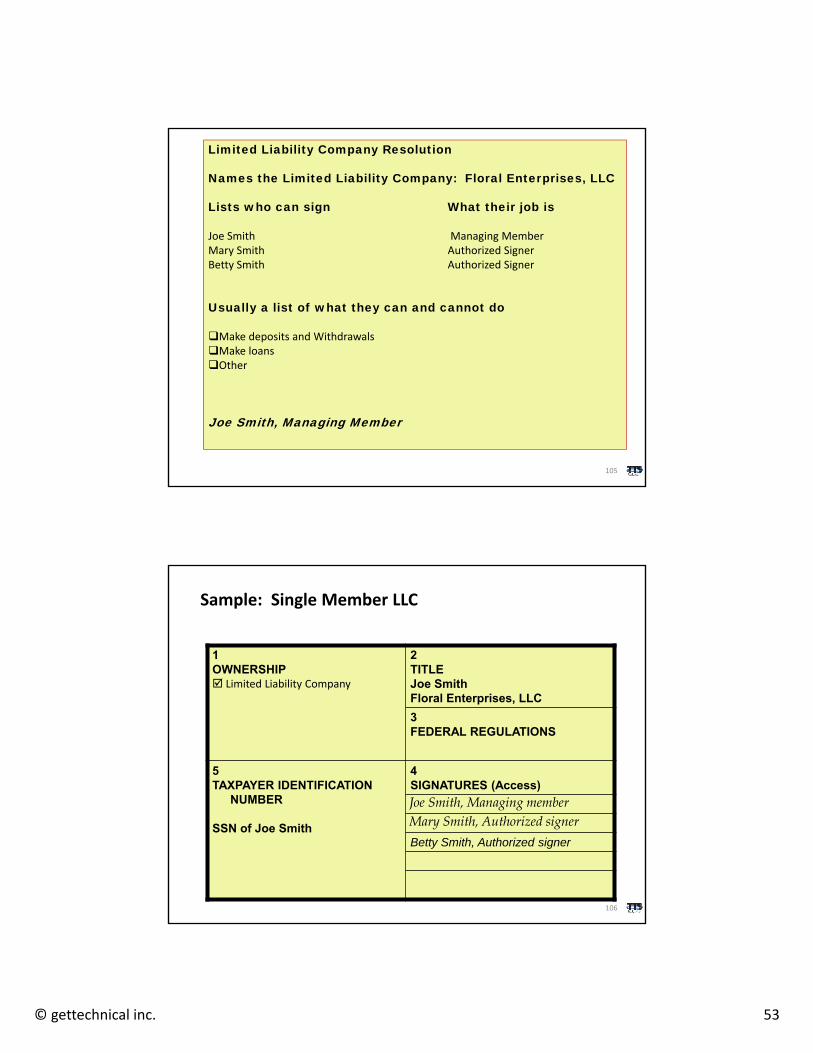

Limited Liability Company Resolution

Names the Limited Liability Company: Floral Enterprises, LLC

Lists who can sign What their job is

Joe Smith Managing MemberMary Smith Authorized SignerBetty Smith Authorized Signer

Usually a list of what they can and cannot do

Make deposits and WithdrawalsMake loans Other

Joe Smith, Managing Member

105

1OWNERSHIP Limited Liability Company

2TITLEJoe SmithFloral Enterprises, LLC

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

SSN of Joe Smith

4SIGNATURES (Access)

Joe Smith, Managing memberMary Smith, Authorized signer

Betty Smith, Authorized signer

Sample: Single Member LLC

106

© gettechnical inc. 54

107

Joe Smith

Floral Enterprises, LLC

Joe Smith

Joe Smith 01/06/2015

Joe Smith 08/14/1977 123 Main Street 439‐00‐9999Monroe, LA xxxxx

Joe Smith 08/14/1977 123 Main Street 439‐00‐9999Monroe, LA xxxxx

Checklist for Limited Liability Company that is a MSB

Required information on LLC Report to IRS in EIN (or SSN if one person LLC) Valid identification on managing member Operating Agreement, if any Documentation

Domestic: Government Issued Document Foreign: Government Issued Document FinCEN registration State registration Any additional documents that your financial institution requires

Account Styling: Smith Electronics, LLC OR Joe Smith, Smith Electronics, LLC

Nondocumentary verification Certification of Beneficial Owner(s) Resolution Signature Card Government lists

108

© gettechnical inc. 55

Professional Service Providers

109

• A professional service provider acts as an intermediary between its client and the bank. Professional service providers include lawyers, accountants, investment brokers, and other third parties that act as financial liaisons for their clients. These providers may conduct financial dealings for their clients. For example, an attorney may perform services for a client, or arrange for services to be performed on the client’s behalf, such as settlement of real estate transactions, asset transfers, management of client monies, investment services, and trust arrangements.

• A typical example is interest on lawyers’ trust accounts (IOLTA). These accounts contain funds for a lawyer’s various clients, and act as a standard bank account with one unique feature: The interest earned on the account is ceded to the state bar association or another entity for public interest and pro bono purposes.

110

© gettechnical inc. 56

• At account opening, the bank should have an understanding of the intended use of the account, including anticipated transaction volume, products and services used, and geographic locations involved in the relationship.

• Professional service providers cannot be exempted from currency transaction reporting requirements.

111

Professional Service Providers (IOLTA is our example)

Requirements Professional Service Providers

1. Required Information:(Before opening account)

Name Address Taxpayer identification— The account will use

the employer identification number of the organization.

2. IRS Reporting: Report in EIN of IOLTA

3. Documentary Requirements:(Reasonable time after opening)

Valid identification on person opening the account.

IOLTA documents required in your state

112

© gettechnical inc. 57

Requirements Professional Service Providers

3. Doc. Requirements(Continued)

Financial Institution Provided Signature Card

4. Suggested nondocument verification:(Reasonable time after opening)

A CIP program must also have nondocumentary verification. Suggestions include: Welcome letter Call to customer to thank for business Delivery of checks to location by account officer Third party verification Previous financial institution references

5. Account Styling: IOLTAJack Smith Law Firm

113

Requirements Professional Service Providers

6. Consult Government Lists: Section 326 List OFAC List

7. Insurance: $250,000 per Owner

8. Miscellaneous: Do not set up online banking between personal accounts and clients funds

114

© gettechnical inc. 58

1OWNERSHIP

IOLTA

2TITLEIOLTAJack Smith Attorney at Law

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

EIN of IOLTA

4SIGNATURES (Access)

Jack Smith, Attorney At Law

Example of Professional Service Providers

115

Checklist for IOLTA

Required information on attorney

Report to IRS in EIN of IOLTA

Valid identification Operating Agreement, if any

DocumentationAny additional documents that your financial institution requires

Account Styling: IOLTA, Jack Smith Law Firm

Nondocumentary verification

Signature Card

Government lists116

© gettechnical inc. 59

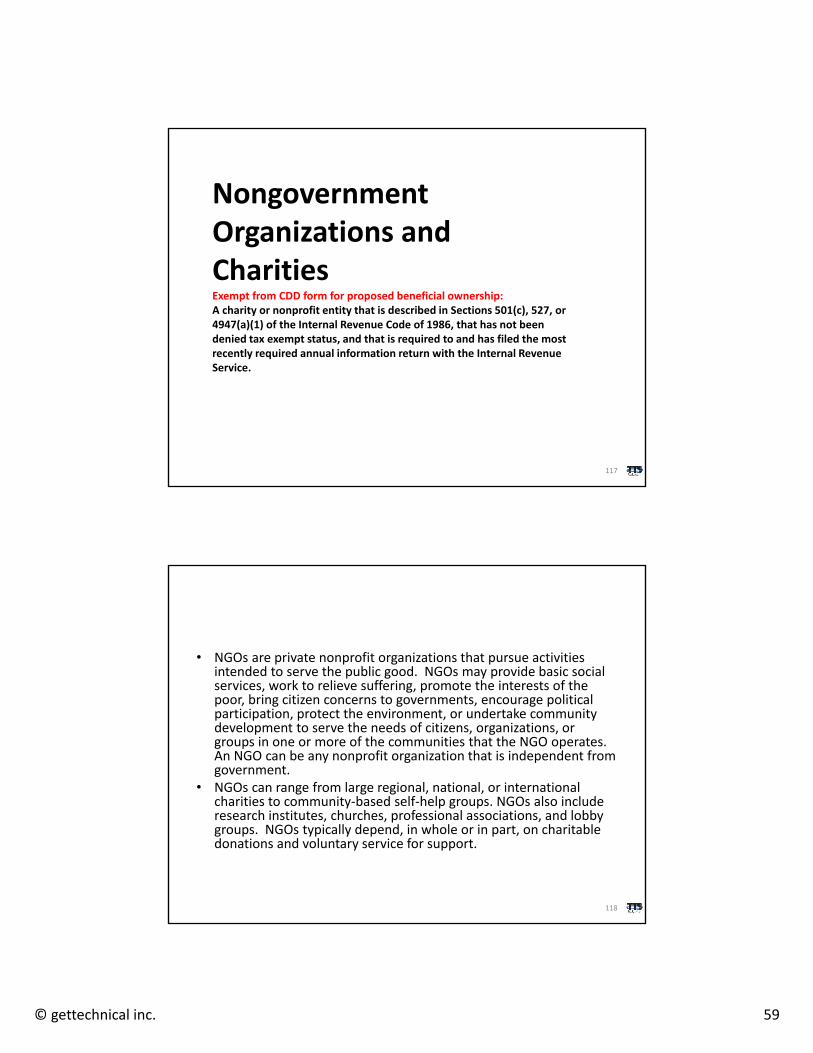

Nongovernment Organizations and CharitiesExempt from CDD form for proposed beneficial ownership:A charity or nonprofit entity that is described in Sections 501(c), 527, or 4947(a)(1) of the Internal Revenue Code of 1986, that has not been denied tax exempt status, and that is required to and has filed the most recently required annual information return with the Internal Revenue Service.

117

• NGOs are private nonprofit organizations that pursue activities intended to serve the public good. NGOs may provide basic social services, work to relieve suffering, promote the interests of the poor, bring citizen concerns to governments, encourage political participation, protect the environment, or undertake community development to serve the needs of citizens, organizations, or groups in one or more of the communities that the NGO operates. An NGO can be any nonprofit organization that is independent from government.

• NGOs can range from large regional, national, or international charities to community‐based self‐help groups. NGOs also include research institutes, churches, professional associations, and lobby groups. NGOs typically depend, in whole or in part, on charitable donations and voluntary service for support.

118

© gettechnical inc. 60

REQUIREMENTS FOR FORMAL NONPROFIT OR UNINCORPORATED ASSOCIATIONS

Requirements Formal Nonprofit Or Unincorporated Associations

1. Required Information:(Before opening account)

Name Address Taxpayer identification— The account will use

the employer identification number of the organization.

2. IRS Reporting: Report in EIN of Organization

3. Documentary Requirements:(Reasonable time after opening)

Valid identification on person opening the account. Sometime financial institutions require identification on all signatories.

My financial institution does/does not require all signers to complete CIP Charter, By‐laws —provided by customer. Minutes of Meeting authorizing account

opening

119

Requirements Formal Nonprofit Or Unincorporated Associations

3. Doc. Requirements(Continued)

Financial Institution Provided ResolutionFinancial Institution Provided Signature CardCertification of Beneficial Owner(s)

4. Suggested nondocument verification:(Reasonable time after opening)

A CIP program must also have nondocumentary verification. Suggestions include: Welcome letter Call to customer to thank for business Delivery of checks to location by account officer Third party verification Previous financial institution references

5. Account Styling: Name of organization. Examples: Rotary Lions Club Kiwanis

120

© gettechnical inc. 61

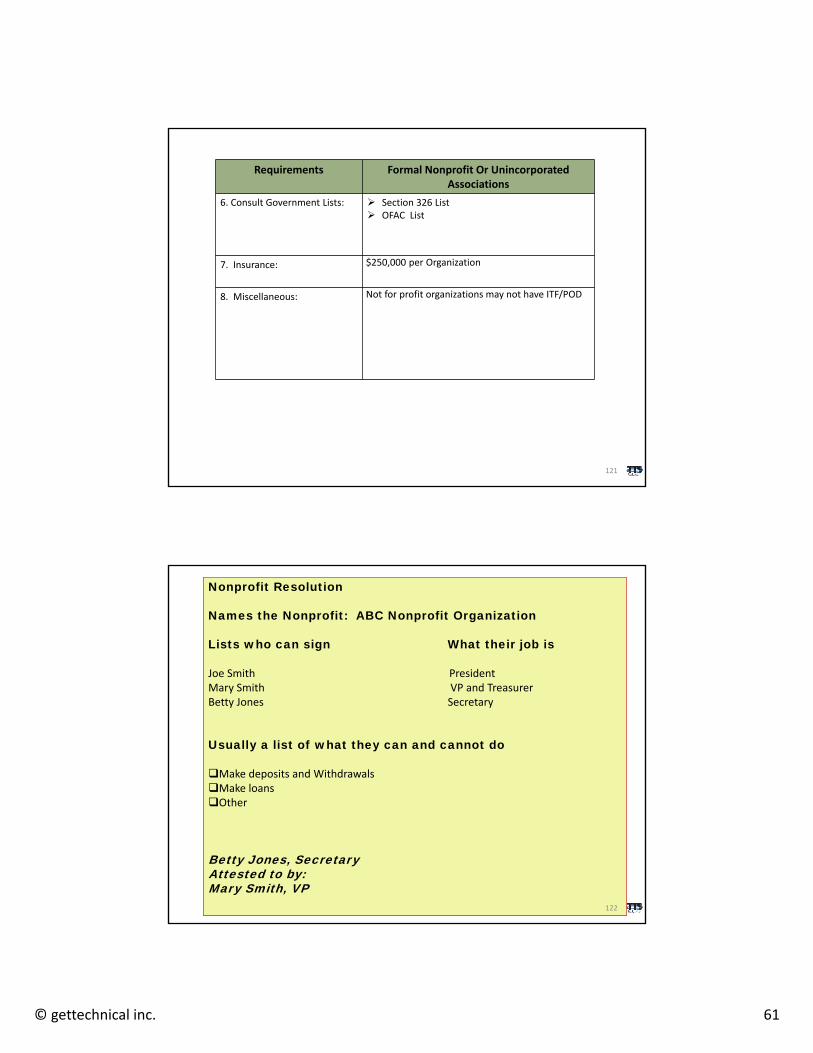

Requirements Formal Nonprofit Or Unincorporated Associations

6. Consult Government Lists: Section 326 List OFAC List

7. Insurance: $250,000 per Organization

8. Miscellaneous: Not for profit organizations may not have ITF/POD

121

Nonprofit Resolution

Names the Nonprofit: ABC Nonprofit Organization

Lists who can sign What their job is

Joe Smith PresidentMary Smith VP and TreasurerBetty Jones Secretary

Usually a list of what they can and cannot do

Make deposits and WithdrawalsMake loans Other

Betty Jones, SecretaryAttested to by:Mary Smith, VP

122

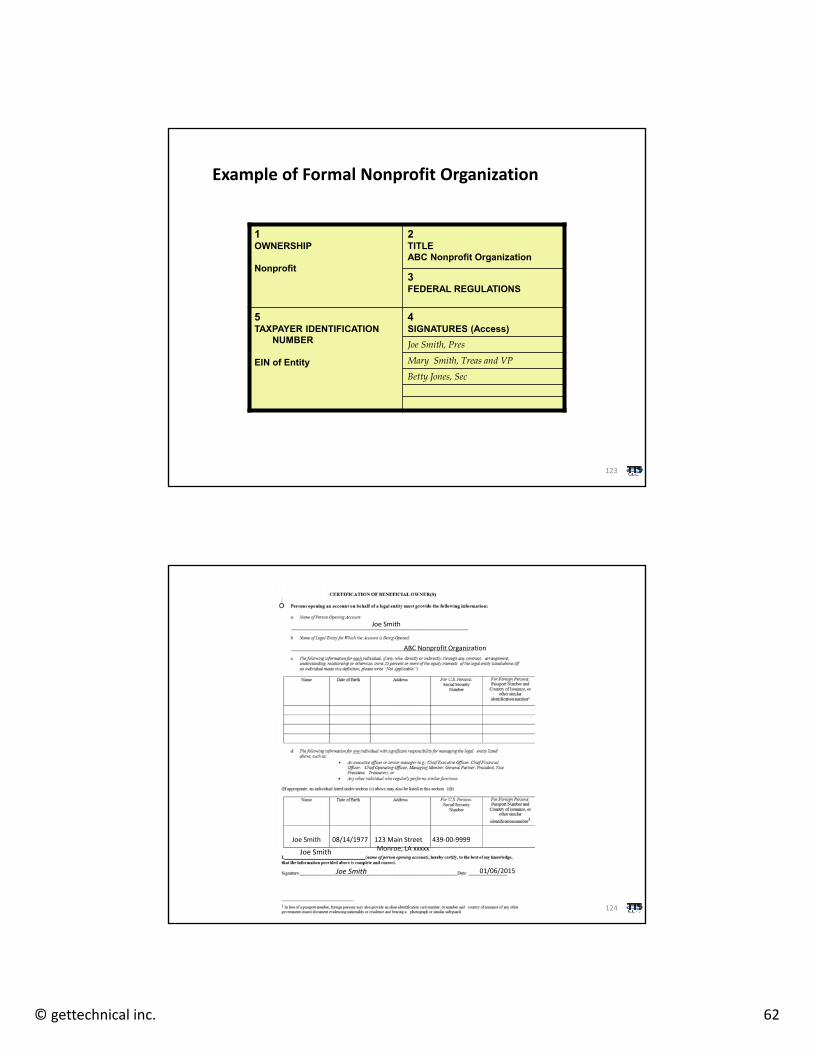

© gettechnical inc. 62

1OWNERSHIP

Nonprofit

2TITLEABC Nonprofit Organization

3FEDERAL REGULATIONS

5TAXPAYER IDENTIFICATION

NUMBER

EIN of Entity

4SIGNATURES (Access)

Joe Smith, Pres

Mary Smith, Treas and VP

Betty Jones, Sec

Example of Formal Nonprofit Organization

123

124

Joe Smith

ABC Nonprofit Organization

Joe Smith

Joe Smith 01/06/2015

Joe Smith 08/14/1977 123 Main Street 439‐00‐9999Monroe, LA xxxxx

© gettechnical inc. 63

Checklist for Formal Nonprofit Association

Required information on nonprofit association Valid identification on signers as required in your CIP Charter, By‐laws Minutes Report to IRS in EIN of Association Account Styling: ABC Nonprofit Organization Account Ownership: Nonprofit Nondocumentary verification Certification of Beneficial Owner(s) unless exempt Resolution Signature Card Government lists

125

Plus ask more about..

• Purpose and objectives of their stated activities.• Geographic locations served (including headquarters and operational areas).

• Organizational structure.• Donor and volunteer base.• Funding and disbursement criteria (including basic beneficiary information).

• Recordkeeping requirements.• Its affiliation with other NGOs, governments, or groups.

• Internal controls and audits.

126

© gettechnical inc. 64

• NGO accounts that are at higher risk for BSA/AML concerns include those operating or providing services internationally, conducting unusual or suspicious activities, or lacking proper documentation. EDD for these accounts should include:– Evaluating the principals.

– Obtaining and reviewing the financial statements and audits.

– Verifying the source and use of funds.

– Evaluating large contributors or grantors of the NGO.

– Conducting reference checks.

127

Cash Intensive Businesses

128

© gettechnical inc. 65

Cash‐intensive businesses and entities cover various industry sectors. Most of these businesses are conducting legitimate business; however, some aspects of these businesses may be susceptible to money laundering or terrorist financing. Common examples include, but are not limited to, the following:• Convenience stores.• Restaurants.• Retail stores.• Liquor stores.• Cigarette distributors.• Privately owned automated teller machines (ATM).• Vending machine operators.• Parking garages.

129

Risk Mitigation

• Purpose of the account.• Volume, frequency, and nature of currency transactions.• Customer history (e.g., length of relationship, CTR filings,300 and

SAR filings).• Primary business activity, products, and services offered.• Business or business structure.• Geographic locations and jurisdictions of operations.• Availability of information and cooperation of the business in

providing information.For those customers deemed to be particularly higher risk, bank management may consider implementing sound practices, such as periodic on‐site visits, interviews with the business’s management, or closer reviews of transactional activity.

130

© gettechnical inc. 66

Pay Day Lenders

131

What Are Payday Loans?

Payday loans are small‐dollar, short‐term, unsecured loans that borrowers promise to repay out of their next paycheck or regular income payment. Payday loans are usually priced at a fixed‐dollar fee, which represents the finance charge to the borrower. Because these loans have such short terms to maturity, the cost of borrowing, expressed as an annual percentage rate, can range from 300 percent to 1,000 percent, or more.

132

© gettechnical inc. 67

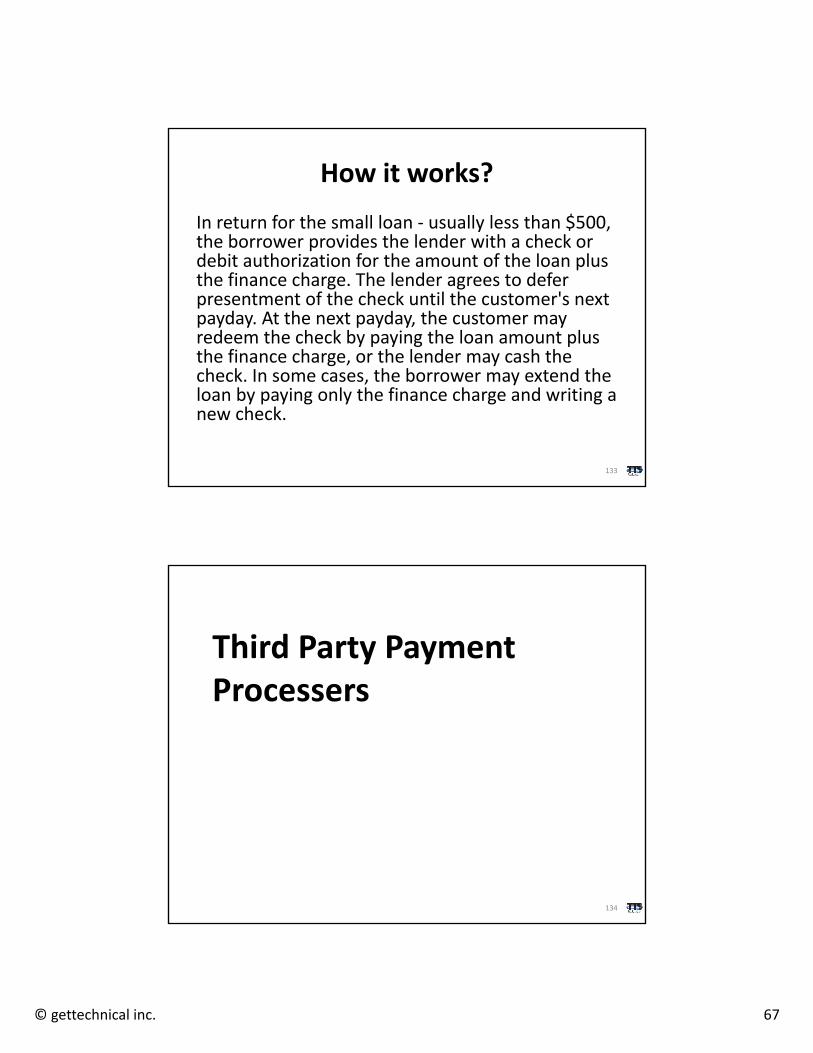

How it works?

In return for the small loan ‐ usually less than $500, the borrower provides the lender with a check or debit authorization for the amount of the loan plus the finance charge. The lender agrees to defer presentment of the check until the customer's next payday. At the next payday, the customer may redeem the check by paying the loan amount plus the finance charge, or the lender may cash the check. In some cases, the borrower may extend the loan by paying only the finance charge and writing a new check.

133

Third Party Payment Processers

134

© gettechnical inc. 68

Nonbank or third‐party payment processors (processors) are bank customers that provide payment‐processing services to merchants and other business entities. Traditionally, processors contracted primarily with retailers that had physical locations in order to process the retailers’ transactions. These merchant transactions primarily included credit card payments but also covered automated clearing house (ACH) transactions, remotely created checks (RCC), and debit and prepaid cards transactions.

135

Third‐party payment processors often use their commercial bank accounts to conduct payment processing for their merchant clients. For example, the processor may deposit into its account RCCs generated on behalf of a merchant client, or process ACH transactions on behalf of a merchant client. In either case, the bank does not have a direct relationship with the merchant. The increased use of RCCs by processor customers also raises the risk of fraudulent payments being processed through the processor’s bank account. The Federal Deposit Insurance Corporation (FDIC), Office of the Comptroller of the Currency (OCC), and Financial Crimes Enforcement Network (FinCEN) have issued guidance regarding the risks, including the BSA/AML risks, associated with banking third‐party processors.

136

© gettechnical inc. 69

FDIC Clarifying Supervisory Approach to Institutions Establishing Account Relationships with Third‐Party Payment Processors, FDIC FIL‐41‐2014, July 28, 2014; Payment Processor Relationships Revised Guidance, FDIC FIL‐3‐2012, January 31, 2012; Risk Management Guidance: Payment Processors, OCC Bulletin 2008‐ 12, April 24, 2008; Risk Management Guidance: Third Party Relationships, OCC Bulletin 2013‐29, October 30, 2013; and Risk Associated with Third‐Party Payment Processors, FinCEN Advisory FIN‐2012‐A010, October 22, 2012.

137

Account opening…

• Merchant base.• Merchant activities.• Average dollar volume and number of transactions.• “Swiping” versus “keying” volume for credit card transactions.

• Charge‐back history, including rates of return for ACH debit transactions and RCCs.

• Consumer complaints or other documentation that suggest a payment processor’s merchant clients are inappropriately obtaining personal account information and using it to create unauthorized RCCs or ACH debits.

138

© gettechnical inc. 70

Before on boarding

• Implementing a policy that requires an initial background check of the processor (using, for example, the Federal Trade Commission Web site, Better Business Bureau, Nationwide Multi‐State Licensing System & Registry (NMLS), NACHA, state incorporation departments, Internet searches, and other investigative processes), its principal owners, and of the processor’s underlying merchants, on a risk‐adjusted basis in order to verify their creditworthiness and general business practices.

• Reviewing the processor’s promotional materials, including its Web site, to determine the target clientele. A bank may develop policies, procedures, and processes that restrict the types of entities for which it allows processing services. These restrictions should be clearly communicated to the processor at account opening.

• Determining whether the processor re‐sells its services to a third party who may be referred to as an “agent or provider of Independent Sales Organization (ISO) opportunities” or “gateway” arrangements.224

• Reviewing the processor’s policies, procedures, and processes to determine the adequacy of its due diligence standards for new merchants.

139

• Requiring the processor to identify its major customers by providing information such as the merchant’s name, principal business activity, geographic location, and transaction volume.

• Verifying directly, or through the processor, that the merchant is operating a legitimate business by comparing the merchant’s identifying information against public record databases, and fraud and bank check databases.

• Reviewing corporate documentation including independent reporting services and, if applicable, documentation on principal owners.

• Visiting the processor’s business operations center.• Reviewing appropriate databases to ensure that the processor and

its principal owners and operators have not been subject to law enforcement actions.

140

© gettechnical inc. 71

Marijuana Related Businesses (MRBs)

141

Risk

In assessing the risk of providing services to a marijuana‐related business, a financial institution should conduct customer due diligence that includes:

(i) verifying with the appropriate state authorities whether the business is duly licensed and registered;

(ii) reviewing the license application (and related documentation) submitted by the business for obtaining a state license to operate its marijuana‐related business;

(iii) requesting from state licensing and enforcement authorities available information about the business and related parties;

142

© gettechnical inc. 72

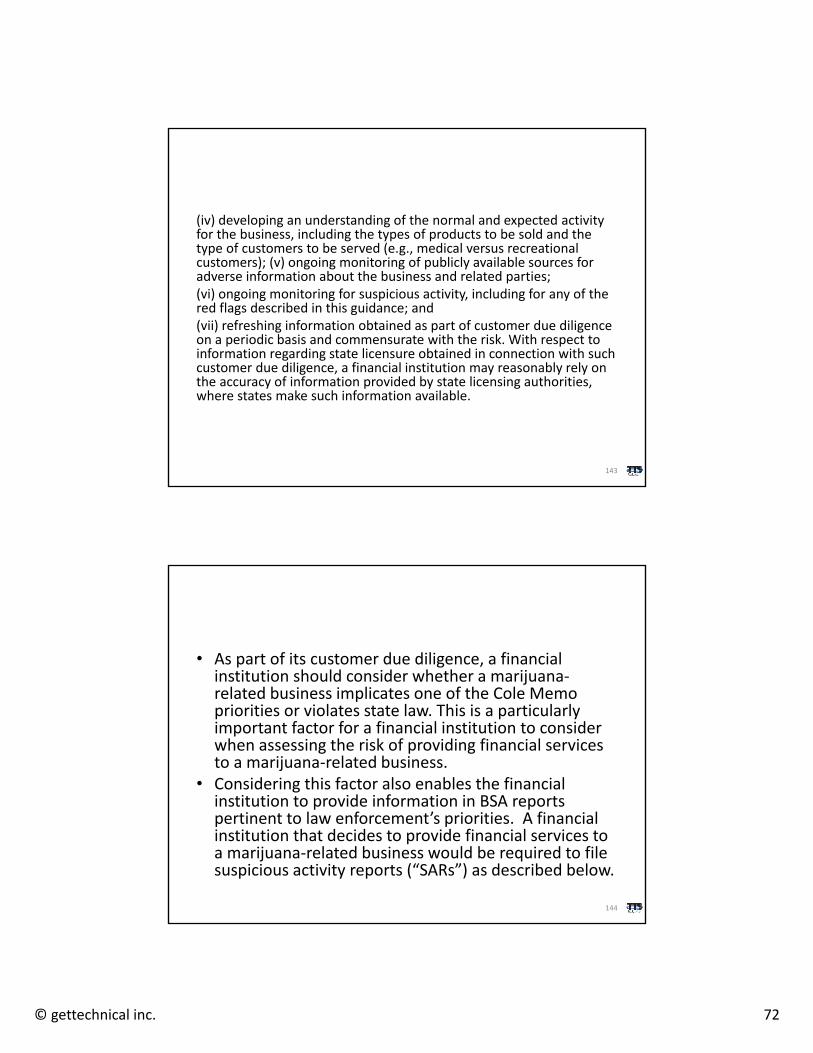

(iv) developing an understanding of the normal and expected activity for the business, including the types of products to be sold and the type of customers to be served (e.g., medical versus recreational customers); (v) ongoing monitoring of publicly available sources for adverse information about the business and related parties; (vi) ongoing monitoring for suspicious activity, including for any of the red flags described in this guidance; and (vii) refreshing information obtained as part of customer due diligence on a periodic basis and commensurate with the risk. With respect to information regarding state licensure obtained in connection with such customer due diligence, a financial institution may reasonably rely on the accuracy of information provided by state licensing authorities, where states make such information available.

143

• As part of its customer due diligence, a financial institution should consider whether a marijuana‐related business implicates one of the Cole Memo priorities or violates state law. This is a particularly important factor for a financial institution to consider when assessing the risk of providing financial services to a marijuana‐related business.

• Considering this factor also enables the financial institution to provide information in BSA reports pertinent to law enforcement’s priorities. A financial institution that decides to provide financial services to a marijuana‐related business would be required to file suspicious activity reports (“SARs”) as described below.

144

© gettechnical inc. 73

Cole Memo

• Preventing the distribution of marijuana to minors;

• Preventing revenue from the sale of marijuana from going to criminal enterprises, gangs, and cartels;

• Preventing the diversion of marijuana from states where it is legal under state law in some form to other states;

• Preventing state‐authorized marijuana activity from being used as a cover or pretext for the trafficking of other illegal drugs or other illegal activity;

145

• Preventing violence and the use of firearms in the cultivation and distribution of marijuana;

• Preventing drugged driving and the exacerbation of other adverse public health consequences associated with marijuana use;

• Preventing the growing of marijuana on public lands and the attendant public safety and environmental dangers posed by marijuana production on public lands; and

• Preventing marijuana possession or use on federal property.

146

© gettechnical inc. 74

SARS

• Limited

• Priority

• Termination

147

Activities that Can Make Your Customer High Risk

148

© gettechnical inc. 75

• Bulk Shipments of Currency

• Payable Through accounts

• Pouch Activities

• Electronic Banking

• Funds Transfers

• ACH

• Prepaid Access

• Privately held ATMs

149

FFI and NFFE

150

© gettechnical inc. 76

©Gettechnical Inc. 151

©Gettechnical Inc. 152

© gettechnical inc. 77

©Gettechnical Inc. 153

©Gettechnical Inc. 154

© gettechnical inc. 78

©Gettechnical Inc. 155

©Gettechnical Inc. 156

© gettechnical inc. 79

©Gettechnical Inc. 157

©Gettechnical Inc. 158

© gettechnical inc. 80

The CTR rules give more hints:

159

Certain businesses are ineligible for treatment as an exempt non‐listed business (31 CFR 1020.315(e)(8)). An ineligible business is defined as a business engaged primarily in one or more of the following specified activities:• Serving as a financial institution or as agents for a financial institution of any type.

• Purchasing or selling motor vehicles of any kind, vessels, aircraft, farm equipment, or mobile homes.

• Practicing law, accounting, or medicine.• Auctioning of goods.• Chartering or operation of ships, buses, or aircraft.

160

© gettechnical inc. 81

• Operating a pawn brokerage.• Engaging in gaming of any kind (other than licensed pari‐mutuel betting at race

tracks).• Engaging in investment advisory services or investment banking services.• Operating a real estate brokerage.• Operating in title insurance activities and real estate closings.• Engaging in trade union activities.• Engaging in any other activity that may, from time to time, be specified by FinCEN,

such as marijuana‐related businesses.A business that engages in multiple business activities may qualify for an exemption as a non‐listed business as long as no more than 50 percent of its gross revenues per year are derived from one or more of the ineligible business activities listed in the rule.

For additional details, refer to Guidance on Supporting Information Suitable for Determining the Portion of a Business Customer's Annual Gross Revenues that is Derived from Activities Ineligible for Exemption from Currency Transaction Reporting Requirements, FIN‐2009‐G001, April 27, 2009.

161

Business and Entity Script

162

© gettechnical inc. 82

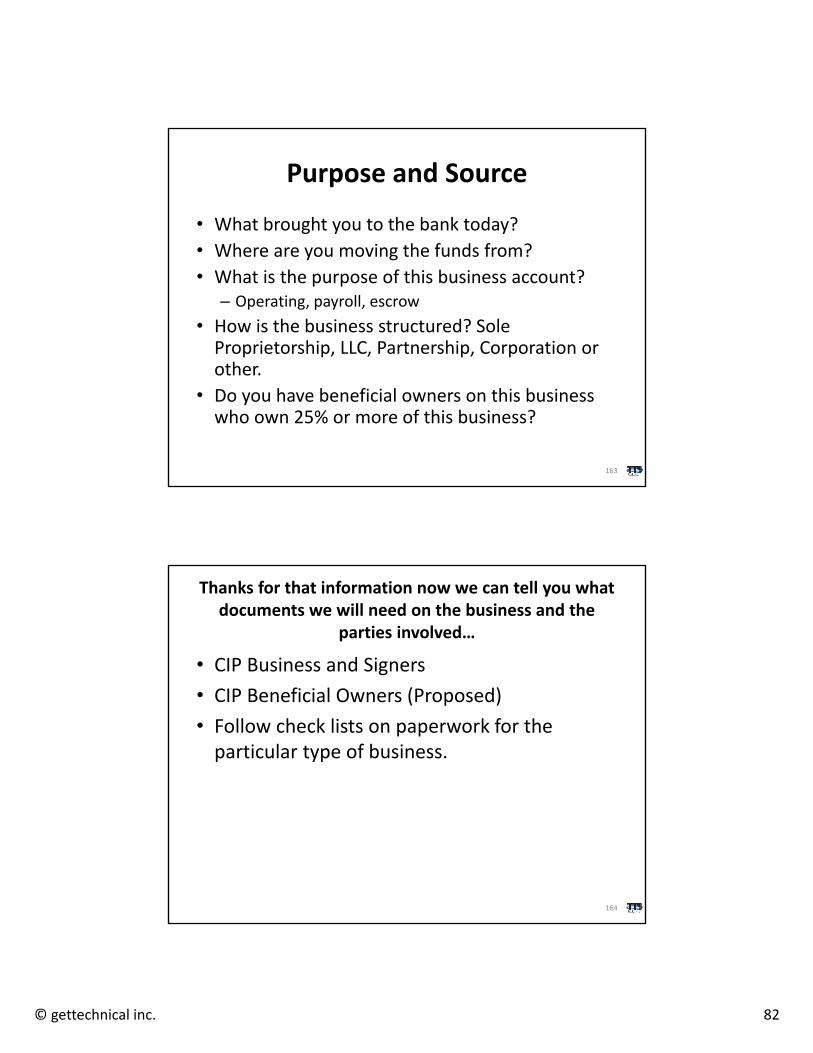

Purpose and Source

• What brought you to the bank today?

• Where are you moving the funds from?

• What is the purpose of this business account? – Operating, payroll, escrow

• How is the business structured? Sole Proprietorship, LLC, Partnership, Corporation or other.

• Do you have beneficial owners on this business who own 25% or more of this business?

163

Thanks for that information now we can tell you what documents we will need on the business and the

parties involved…

• CIP Business and Signers

• CIP Beneficial Owners (Proposed)

• Follow check lists on paperwork for the particular type of business.

164

© gettechnical inc. 83

Geography

• Can you tell me the service area of your business?

• Do all of the principals live in the same geographic region?

165

Transactional questions

Now to get you in the right product, we will have to ask a few transactional questions.

Expected Annual Deposits _______________________________________________________________

Types of banking services used_____________________________________________________________________________________________________________________________________________________________________________________________Expected International Services____________________________________________________________________________________________________________________________________________________________________________________________

166

© gettechnical inc. 84

Products and Services

• We have several options for the account that might work for you. Let me go over them with you.

• We have some additional services that I can also offer you. – Remote Deposit Capture

– Debit Cards

– Online banking

– Bill Pay

• Now let’s make sure you understand all the benefits and fees of the choices you have made….

167

Money Service Business

• Does your company cash checks over $1000?• Does your company issue cashier’s checks or money orders over $1000?• Does your company exchange currency over $1000?• Do you transmit currency even virtual currency at any dollar amount?• Do you provide or sell prepaid cards?• ‐Over $2000 Closed loop• ‐Not for HSA, Government Benefits or Employee Benefits• ‐Over $1000 • ‐At any amount if allow for reloads from nonfinancial institutions or

internationally• ‐If a seller, if you do not CIP or sell under $10,000• If yes, then we will need your FinCEN Registration and state registration

when applicable unless you are acting as an agent solely and can provide proof of the agency status.

168

© gettechnical inc. 85

Unlawful or lawful internet gambling

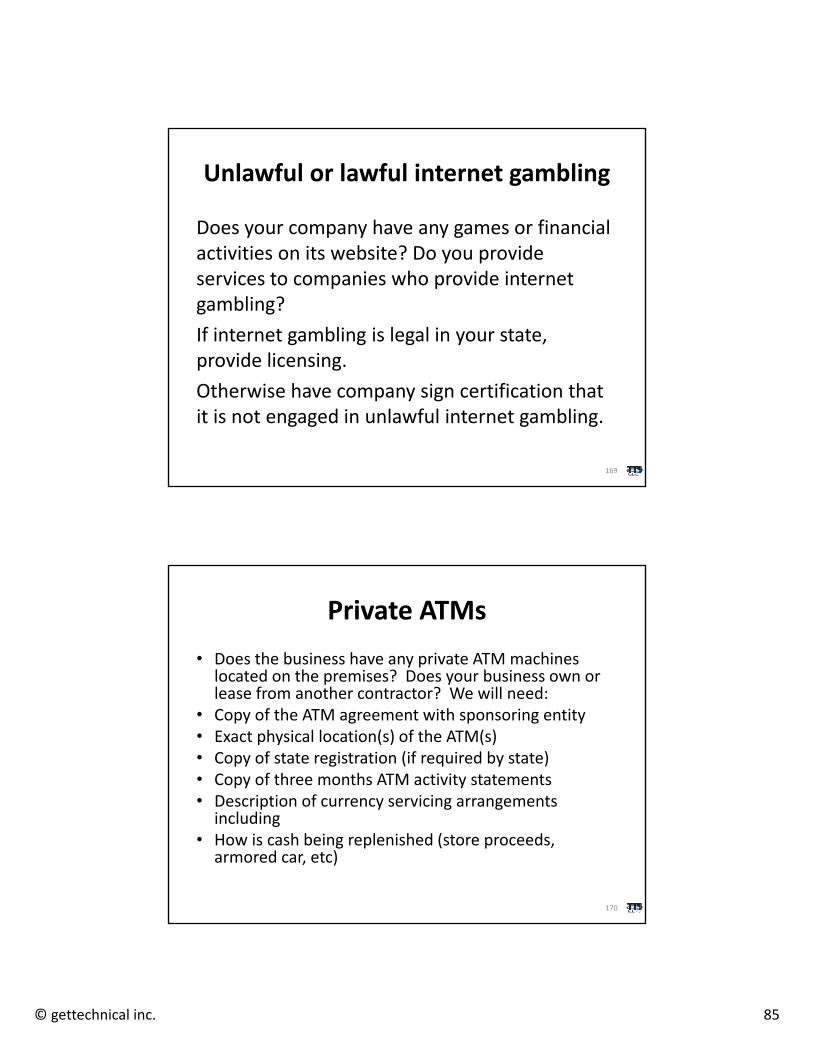

Does your company have any games or financial activities on its website? Do you provide services to companies who provide internet gambling?

If internet gambling is legal in your state, provide licensing.

Otherwise have company sign certification that it is not engaged in unlawful internet gambling.

169

Private ATMs

• Does the business have any private ATM machines located on the premises? Does your business own or lease from another contractor? We will need:

• Copy of the ATM agreement with sponsoring entity• Exact physical location(s) of the ATM(s)• Copy of state registration (if required by state)• Copy of three months ATM activity statements• Description of currency servicing arrangements including

• How is cash being replenished (store proceeds, armored car, etc)

170

© gettechnical inc. 86

Funds Availability on Checking

• Here is our funds availability policy. You will notice that our funds are generally next day available but cash is available on the same day.

• You can make a deposit from 9‐5 at the teller window and it will be available generally by the next morning.

171

Debit Cards

• We do issue debit cards for business accounts. Is this something that you are interested in?

• You can order these for employees but I want to take a minute to go over the limits and what happens if there is an unauthorized transaction on you business debit card it is a little different than a personal account.

• Explain

172

© gettechnical inc. 87

Marijuana Related Businesses

Are you a producer, processor or retailer of marijuana?Yes/No If yes, obtain copy of license

What is your annual revenue? ________________________________If a retailer, you agree that there is:

‐No employee under the age of 21 or allow anyone under the age of 21 on the premisesNo signage is visible from the public right of way ‐No display is visible from the public right of way‐No employee or owner shall use the product on the premises

Is this business a marijuana‐related business?Type of Business ____________________________ (Example Insurance company, landlord,security systems etc.

Approximate Annual Revenue ____________________________________________What percentage of your business is directly tied to marijuana business? __________%What process do you have in place to make sure the marijuana business is licensed? ___________________________________________________________________________

173

Checklist

• Customer Profile• Resolution • Signature Card• W‐9 or W‐8Bene• Documentation on Business• Documentation on Signers and 25% Beneficial owners• OFAC• Business Debit Card Agreement, Online banking and Remote

Deposit Capture• Funds availability and unlawful internet gambling • Registration for MSBs and state law registration• State registration and licensing for marijuana businesses• Risk rating of business

174

© gettechnical inc. 88

The CTR rules give more hints:

175

Certain businesses are ineligible for treatment as an exempt non‐listed business (31 CFR 1020.315(e)(8)). An ineligible business is defined as a business engaged primarily in one or more of the following specified activities:• Serving as a financial institution or as agents for a financial institution of any type.

• Purchasing or selling motor vehicles of any kind, vessels, aircraft, farm equipment, or mobile homes.

• Practicing law, accounting, or medicine.• Auctioning of goods.• Chartering or operation of ships, buses, or aircraft.

176

© gettechnical inc. 89

• Operating a pawn brokerage.• Engaging in gaming of any kind (other than licensed pari‐mutuel betting at race

tracks).• Engaging in investment advisory services or investment banking services.• Operating a real estate brokerage.• Operating in title insurance activities and real estate closings.• Engaging in trade union activities.• Engaging in any other activity that may, from time to time, be specified by FinCEN,

such as marijuana‐related businesses.A business that engages in multiple business activities may qualify for an exemption as a non‐listed business as long as no more than 50 percent of its gross revenues per year are derived from one or more of the ineligible business activities listed in the rule.

For additional details, refer to Guidance on Supporting Information Suitable for Determining the Portion of a Business Customer's Annual Gross Revenues that is Derived from Activities Ineligible for Exemption from Currency Transaction Reporting Requirements, FIN‐2009‐G001, April 27, 2009.

177

©Gettechnical Inc. 178

Thanks for participating!Debbie Crawford

Gettechnical Inc

1‐800‐354‐3051

www.gettechnicalinc.com

©Gettechnical Inc.

© gettechnical inc. 90

Thanks for participating!

Debbie CrawfordGettechnical Inc1‐800‐354‐[email protected]

Kyle BennettTotal Training [email protected]‐831‐0678

Upcoming Webinars

August 11th ‐Writing Teller Training and Procedures

August 18th ‐Mortgage Loan Originator Required

Training Series ‐ Part 2

August 18th ‐ Virtual issues on Cashier’s Checks

August 19th ‐ Flood Insurance Fundamentals – What

do you need to know?

August 20th ‐ Basic Cash Flow Analysis

August 20th ‐ Compliance Perspectives: A Monthly

Update

August 25th ‐ All About the New FFIEC Cybersecurity

Assessment Tool

August 27th ‐ Appraisal Review for Mortgage

Decisions

179