opec extended production cuts: why prices fell consulting services, inc. artberman.com slide 1 opec...

TRANSCRIPT

Slide1LabyrinthConsultingServices,Inc. artberman.com

OPECExtendedProductionCuts:WhyPricesFell

• Lastweek’spriceplungewasthethirdtimein2017thatpriceshaveadjusteddownwardtowardthe$45perbarrellevelsuggestedbymarketfundamentals.

• IEAcalculatedthatrecentproductioncutsearnedthecartelanadditional$75millionperdayyear-over-yearinthefirstquarterof2017.

• OPEC’sgoalhasbeentokeepafloorundercurrentpricesbutthemarketexpectedthecarteltomovepriceshigherthroughinventoryreduction.

• OPECwassatisfiedwithgreaterrevenuesfromhigherpricescomparedtoayearago,butthemarketwanteddeeperproductioncuts.

• OPECtakesthelongviewbutthemarketisconcernedwiththenearterm.• OPECextendedthecutsandthemarketreactedwithlowerprices.

$40

$41

$42

$43

$44

$45

$46

$47

$48

$49

$50

$51

$52

$53

$54

$55

$56

$57

$58

$59

$60

11/1/

16

11/8/

16

11/15

/16

11/22

/16

11/29

/16

12/6/

16

12/13

/16

12/20

/16

12/27

/16

1/3/17

1/10/1

7

1/17/1

7

1/24/1

7

1/31/1

7

2/7/17

2/14/1

7

2/21/1

7

2/28/1

7

3/7/17

3/14/1

7

3/21/1

7

3/28/1

7

4/4/17

4/11/1

7

4/18/1

7

4/25/1

7

5/2/17

5/9/17

5/16/1

7

5/23/1

7

NYMEXW

TIFuturesPrice($/barrel)

ThirdDeflationoftheOPECExpectationPremiumin2017

The OPECExpectationPremium

Source:EIA,Bloomberg &Labyrinth Consulting Services,Inc.

$45PerBarrel

February-MarchDeflation

April- EarlyMay Deflation

LateMay

Deflation

Slide2LabyrinthConsultingServices,Inc. artberman.com

OPEC’sGoal:KeepaFloorUnderOilPricesWithoutHelpingCompetitionTooMuch

• Atfirst,OPECdidnothingafteroilpricescollapsedin2014.• Whenpricesfellto$26perbarrelinearly2016,OPECfloatedtheideaofaproductionfreezeandthat

establishedafloorfromwhichpricesincreasedtomorethan$50perbarrelduringthefirsthalfoftheyear.

• InJune2016,marketslostfaithinOPEC’sresolveandpricesfellfrom$51tobelow$40perbarrel.• OPECthensetanotherpricefloorbyannouncingtentativeagreementonaproductioncut.• Whenpricesfellbelow$43inNovember,anotherpricefloorwascreatedwhenOPECenacted

productioncuts.• Theworldpricefloormovedupalmost75%from$26to$45perbarrelinjustoverayear.• Productioncutswereextendedlastweektoreinforcethecurrent$45floorwithouthelpingthe

competitiontoomuch—nottomeetmarketexpectationsofhigherprices.

0

20

40

60

80

100

120

$0$2$4$6$8$10$12$14$16$18$20$22$24$26$28$30$32$34$36$38$40$42$44$46$48$50$52$54$56$58$60$62$64$66

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-1

5 Au

g-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-1

6 Au

g-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Oil-PriceVo

latilityIndex

NYM

EXW

TIFuturesPrices($

/Barrel)

OilMarketsContinueTesting$55Ceiling&$45Floor

NYMEXFutures

Price(LHS)

Oil-PriceVolatilityIndex(RHS)

$62

$55PerBarrelCeiling

Source:EIA,CBOE,Bloomberg &Labyrinth Consulting Services,Inc.

OPEC"Freeze"ProposedFeb2016

$43OPECCutNov2016

$26

$45Floor

$40OPECCutAnnouncedSept2016

Slide3LabyrinthConsultingServices,Inc. artberman.com

OiltradersBeganUnwindingLongPositionsinFebruary

• OiltradersunderstandthisbetterthananalystsandtheybeganunwindingtheirlongpositionsinFebruary.

• NetlongpositionsonWTIfutureshavefallen25%sincethenbutmostofthesell-offhasbeensinceApril2017.

• Longpositionscommonlyover-shootpricetrendsandpricesfallafterhighestlevels.• TermstructureofWTIfuturescontractsinfairlysteepbackwardationsincemid-April.• Priceslessthan$50/barreluntil2020.

$25

$30

$35

$40

$45

$50

$55

$60

0

50

100

150

200

250

300

350

400

1/5/16

1/1

9/16

2/2/16

2/1

6/16

3/1/16

3/1

5/16

3/29/1

6 4/1

2/16

4/26/1

6 5/1

0/16

5/24/1

6 6/7

/16

6/21/1

6 7/5

/16

7/19/1

6 8/2

/16

8/16/1

6 8/3

0/16

9/13/1

6 9/2

7/16

10/11

/16

10/25

/16

11/8/

16

11/22

/16

12/6/

16

12/20

/16

1/3/17

1/1

7/17

1/31/1

7 2/1

4/17

2/28/1

7 3/1

4/17

3/28/1

7 4/1

1/17

4/25/1

7 5/9

/17

NYM

EXW

ITPrice($/barrel)

NetLongPositions(MillionsofBarrelsofW

IT)

NetLongFuturesPostionsHaveFallen17%SinceMid-April2017

NetLongPositions(LHS)

NYMEXPrice(RHS)

Source:CFTC, EIA&LabyrinthConsultingServices,Inc.

NetLongPositions(LHS)

NYMEXPrice(RHS)

Source:CFTC, EIA&LabyrinthConsultingServices,Inc.

&25%SinceMarch2017FebruaryPeak

AprilPeak

$45

$47

$49

$51

$53

$55

$57

Jan-17

Mar-17

May-17

Jul-1

7 Sep-17

Nov-17

Jan-18

Mar-18

May-18

Jul-1

8 Sep-18

Nov-18

Jan-19

Mar-19

May-19

Jul-1

9 Sep-19

Nov-19

Jan-20

Mar-20

May-20

Jul-2

0 Sep-20

Nov-20

Jan-21

Mar-21

May-21

Jul-2

1 Sep-21

Nov-21

Jan-22

Mar-22

May-22

Jul-2

2 Sep-22

Nov-22

NYMEXW

TIIPrice($/barrel)

TheTermStructureofFuturesContractsChangedAfterOPECProductionCuts

NOV302016

MAR242018

APR132017

May52017

MAY192017

25-May2017

Source:CME& LabyrinthConsultingServices,Inc.

Mar24

May5

May19May26

Slide4LabyrinthConsultingServices,Inc. artberman.com

ReasonsforLowerOilPrices

• ManyanalystsproclaimthatBrentpriceswillbenear$65bytheendoftheyear.• AlthoughIEAandEIAproductiondatasuggestsgoodOPECcompliancewiththeNovemberagreement.• IraqwillhaveahardtimemaintainingcutswithISISwarandotherfiscalpressures.• Russiaproductioncurrentlyinaseasonallowthatincreased500kb/din2H2016.

36.5

37.5

38.5

39.5

40.5

41.5

42.5

43.5

Jan-14 Mar-14 May-14 Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17

MillionsofBarrelsofCrudeO

ilPerDay

OPEC- NOPECCrudeOilProductionAtLowestLevelSinceJune2015

Venezuela

Iran

Iraq

Libya

Nigeria

UAE

SaudiArabia

Qatar

Kuwait

Angola

BaseAlgeria

Gabon-Ecuador Mexico

Russia

June2015

Source:EIAMaySTEO,EIAInternationalData&La

byrinthConsultingServices,Inc.

9.6

9.8

10

10.2

10.4

10.6

10.8

11

Jan Feb Mar Ap May June July Aug Sept Oct Nov Dec

CrudeOilProduction(m

mb/d)

RussiaCrudeProductionIncreasesSeasonallyEspeciallyin2016

2017

Source:EIAM

aySTEO,EIAInternationalData&LabyrinthConsultingServices,Inc.

2016

2015

2014

Slide5LabyrinthConsultingServices,Inc. artberman.com

ReasonsforLowerOilPrices

• Still,globalmarketsremainwellsupplied.• OPECshipmentstoitsbiggestcustomers—theU.S.andChina—aremorethan10%higherthanayear

ago.• Productioncutsarenotreflectedinwell-suppliedmarketsnorareglobalinventoriesfallingmuch.

Slide6LabyrinthConsultingServices,Inc. artberman.com

U.S.ProductionConcernsAreReal

• MarketconcernsarevalidthatU.S.tightoiloutputmaycancelOPECproductioncuts.• Despitefrackcrewshortagesandlimitstopressurepumpingequipment,2017wellcompletionrates

appearstrongintheBakken,EagleFordandPermianbasinplays.• EIAforecastisfortotalcrudeoilproductiontoincrease0.96mmb/din2017,another0.61mmb/din

2018(1.57mmb/dtotal2017-2018increase).• Mostofthedecreaseinbreak-evenpricesisbecauseofloweroil-fieldservicecostsandnotefficiency

andtechnology.

-

100

200

300

400

500

600

700

0

50

100

150

200

250

300

350

400

450

500

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Jul-1

4

Aug-14

Sep-14

Oct-14

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-1

5

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-1

6

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

MonthlyPermianWellCom

pletions

Bakken&EagleFordMonthlyW

ellCom

pletions

IncreasedTightOilWellCompletionsin2017

Permian

EagleFord

Bakken

Source:EIA&LabyrinthConsultingServices,Inc.

9.63

8.57

9.15

9.74 10

.35

$0

$20

$40

$60

$80

$100

$120

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Jan-14

Feb-14

Mar-14

Apr-14

May-14

Jun-14

Jul-14

Aug-14

Sep-14

Oct-14

Nov-14

Dec-14

Jan-15

Feb-15

Mar-15

Apr-15

May-15

Jun-15

Jul-15

Aug-15

Sep-15

Oct-15

Nov-15

Dec-15

Jan-16

Feb-16

Mar-16

Apr-16

May-16

Jun-16

Jul-16

Aug-16

Sep-16

Oct-16

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-18

Jul-18

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

WTIPrice($/Barrel)

MillionsofB

arrelsofCrudeOilPerD

ay

U.S.Output9.15mmb/dUp58kb/dInApril

April

2015

Source: EIASTEOMay2017&LabyrinthConsulting Services,Inc.

-1.06mmb/d

OilProduction(LHS)

WTIPrice(RHS)

Apr2

017

Dec2

017

+0.58mmb/d

Sept

2017

Dec2

018

+1.2mmb/dApr2017-Dec2018

ForecastIs10.35 mmb/dand$57/barrelbyDecember2018+0.96mmb/d in2017,+0.61in2018,+1.57total2017-18

0

0.2

0.4

0.6

0.8

1

Dec-85

Sep-86

Jun-87

Mar-88

Dec-88

Sep-89

Jun-90

Mar-91

Dec-91

Sep-92

Jun-93

Mar-94

Dec-94

Sep-95

Jun-96

Mar-97

Dec-97

Sep-98

Jun-99

Mar-00

Dec-00

Sep-01

Jun-02

Mar-03

Dec-03

Sep-04

Jun-05

Mar-06

Dec-06

Sep-07

Jun-08

Mar-09

Dec-09

Sep-10

Jun-11

Mar-12

Dec-12

Sep-13

Jun-14

Mar-15

Dec-15

Sep-16

Norm

alize

dWTI&ProducerPrice

Index

TheCostofDrillingOilandGasWellsFell45%AfterTheOil-PriceCollapse;UnconventionalPlaysResultedIna4-foldIncreaseinDrillingCosts

Source:U.S.Federal ReserveBank,EIA&LabyrinthConsulting Services,Inc.

WTIPrice

OIl&GasWell DrillingProducer PriceIndex

Source:U.S.Federal ReserveBank,EIA&LabyrinthConsulting Services,Inc.

4-FoldIncreaseinO&GPPI

45%Decrease

Slide7LabyrinthConsultingServices,Inc. artberman.com

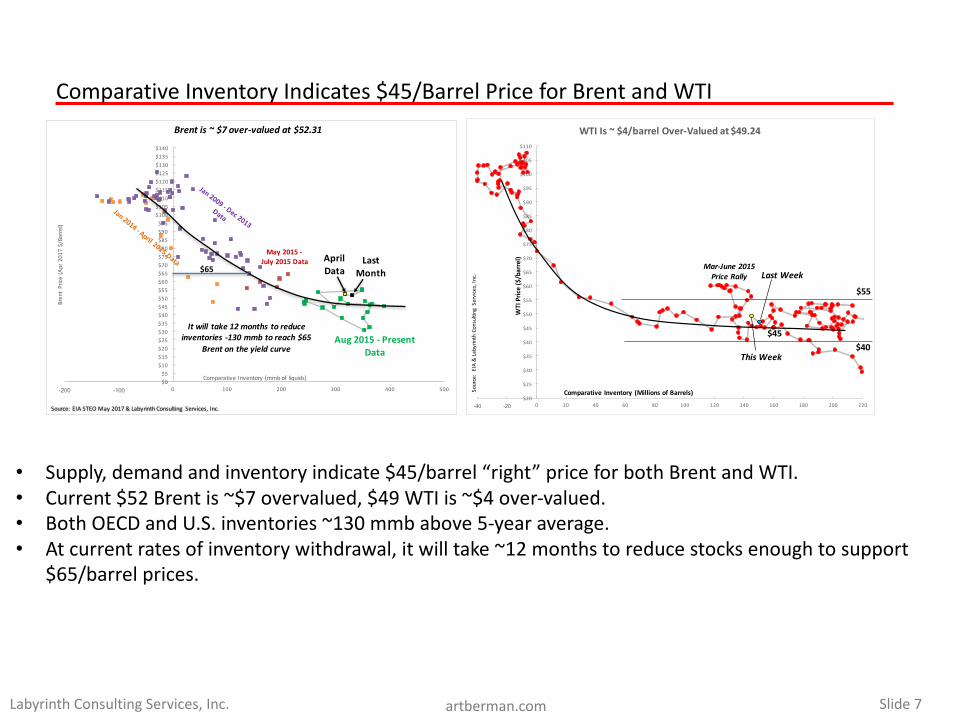

ComparativeInventoryIndicates$45/BarrelPriceforBrentandWTI

$0$5

$10$15$20$25$30$35$40$45$50$55$60$65$70$75$80$85$90$95$100$105$110$115$120$125$130$135$140

-200 -100 0 100 200 300 400 500

BrentPrice

(Apr2017$/Barre

l)

ComparativeInventory(mmbofliquids)

Aug2015- PresentData

May2015-July2015Data April

Data

Brentis~$7 over-valuedat$52.31

LastMonth$65

Itwill take12monthstoreduceinventories -130mmbtoreach$65

Brentontheyieldcurve

Source: EIASTEOMay2017&LabyrinthConsulting Services,Inc.

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

$100

$105

$110

-40 -20 0 20 40 60 80 100 120 140 160 180 200 220

WTIIs~$4/barrelOver-Valuedat$49.24

Comparative Inventory (Millionsof Barrels)

WTIPrice($/barrel)

ThisWeek$40

$55

Source:EIA&La

byrinthConsultingServices,Inc.

Mar-June 2015PriceRally

$45

LastWeek

• Supply,demandandinventoryindicate$45/barrel“right”priceforbothBrentandWTI.• Current$52Brentis~$7overvalued,$49WTIis~$4over-valued.• BothOECDandU.S.inventories~130mmb above5-yearaverage.• Atcurrentratesofinventorywithdrawal,itwilltake~12monthstoreducestocksenoughtosupport

$65/barrelprices.

Slide8LabyrinthConsultingServices,Inc. artberman.com

ComparativeInventoryIndicates$45/BarrelPriceforBrentandWTI

1.27

1.28

1.29

1.30

1.31

1.32

1.33

1.34

1.35

1.36

1.37

3.0

3.0

3.0

3.0

3.1

3.1

3.1

3.1

3.1

May-17

Jun-17

Jul-1

7

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-18

Jul-1

8

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

U.S.Stocks(bblliquids)

OECDStocks(bbliquids)

OECDInventoriesFlatin2017,Increasein2018U.S.InventoriesFallin2017,Increasein2018

U.S.Stocks(RHS)

Source: EIAMay2017STEO&LabyrinthConsulting Services,Inc.

OECDStocks(LHS)

• WorldproductionsurpluseshavebeenfallingforthelastyearbutEIAexpectsthesetostartincreasingasearlyasMay.

• Surplusesmaypersistthroughthemiddleof2018beforedecreasingagain.• ItsforecastisforBrentpricestoremainlessthan$60perbarrelthroughtheendof2018.• EIAforecastisforflatOECDinventoriesthrough2017,thenincreasein2018.• U.S.inventoriespredictedtofallin2018then,increasein2018.• MacquarieResearch

$0

$20

$40

$60

$80

$100

$120

$140

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Jul-16

Oct-16

Jan-17

Apr-17

Jul-17

Oct-17

Jan-18

Apr-18

Jul-18

Oct-18

Bren

tPric

e(Feb

ruary2

017Do

llarsPerBarrel)

WorldLiqu

idsP

rodu

ctionminusCon

sumption(M

illionsofBarrelsPe

rDay)

EIAForecastsProduction SurplusToIncrease2H2017-1H2018

Source: EIASTEOMay2017&LabyrinthConsulting Services,Inc.

ProductionSurplus(LHS)

BrentPrice(RHS)

IncreasingSurplus

DecreasingSurplusThru

1H2017

DecreasingSurplus2H2018

IncreasingSurplus2H2017-1H2018

ProdDeficit(LHS)

Slide9LabyrinthConsultingServices,Inc. artberman.com

$56 $5

6

$59

$59

$57

$56

$55

$56

$59

$60

$61

$63

$50

$52

$54

$56

$58

$60

$62

$64

Q117 Q217 Q317 Q417 Q118 Q218 Q318 Q418 Q119 Q219 Q319 Q419

BrentPrice

($/Barrel)

MacquarieForecastsBrentPricesBelow$60Through2Q2019

Source:M

acquarie&La

byrinthConsultingServices,Inc.

MacquarieResearchPredictsSub-$60BrentThrough2Q2019

• RecentmodelingbyMacquarieResearchsupportsthisviewandpredictssub-$60Brentpricesthroughthesecondquarterof2019.

• AlthoughOPECcutsappeartobereal,MacquarieseesU.S.,RussiaandBrazilproductiongrowthasbearishdriversonprice.

• MaintainingOPECcutsbeyondtheendof2017willbedifficult.• RecenttalkofsellinghalfofU.S.strategicreservespotentiallyputsanadditional300millionbarrelsofoil

onanalreadyover-suppliedmarket.• Termstructureoffuturestripinbackwardationwithpriceslessthan$51/barreluntilAugust2021.

$45

$47

$49

$51

$53

$55

$57

Jan-17

Mar-17

May-17

Jul-1

7 Sep-17

Nov-17

Jan-18

Mar-18

May-18

Jul-1

8 Sep-18

Nov-18

Jan-19

Mar-19

May-19

Jul-1

9 Sep-19

Nov-19

Jan-20

Mar-20

May-20

Jul-2

0 Sep-20

Nov-20

Jan-21

Mar-21

May-21

Jul-2

1 Sep-21

Nov-21

Jan-22

Mar-22

May-22

Jul-2

2 Sep-22

Nov-22

NYMEXW

TIIPrice($/barrel)

WTIFuturesHaveBeenBackwardatedSinceApril2017

NOV302016

MAR242018

APR132017

May52017

MAY192017

25-May2017

Source:CME& LabyrinthConsultingServices,Inc.

Mar24

May5

May19May26

Slide10LabyrinthConsultingServices,Inc. artberman.com

MacquarieResearchPredictsSub-$60BrentThrough2Q2019$56 $5

6

$59

$59

$57

$56

$55

$56

$59

$60

$61

$63

$50

$52

$54

$56

$58

$60

$62

$64

Q117 Q217 Q317 Q417 Q118 Q218 Q318 Q418 Q119 Q219 Q319 Q419

BrentPrice

($/Barrel)

MacquarieForecastsBrentPricesBelow$60Through2Q2019

Source:M

acquarie&La

byrinthConsultingServices,Inc.

• RecentmodelingbyMacquarieResearchsupportsthisviewandpredictssub-$60Brentpricesthroughthesecondquarterof2019.

• AlthoughOPECcutsappeartobereal,MacquarieseesU.S.,RussiaandBrazilproductiongrowthasbearishdriversonprice--maintainingOPECcutsbeyondtheendof2017willbedifficult.

• RecenttalkofsellinghalfofU.S.strategicreservespotentiallyputsanadditional300millionbarrelsofoilonanalreadyover-suppliedmarket.

• Worldliquidsproductionwillincrease4millionbarrelsperdaybytheendof2018.• 62%ofincreasefromU.S.,28%fromOPEC—capitalmarkets¢ralbankskeytocapitalavailability.• Thatwillmeanrelativelylowoilprices,arequisitefortheglobaleconomytomuddleforward.

Slide11LabyrinthConsultingServices,Inc. artberman.com

Oil & Gas Company Return on Capital Employed

Oil & Gas Company Stock Performance

MajorPriceSpikeSometimeintheNext5Years

• Under-investmentwillensuretightersupplyinthefuture.• Reservereplacementata70-yearlow.• DespitegoodheadlinesaboutE&Pbreak-evenprices,ROCEisdeclining.• Oil&gascompanystockperformancewellbelowS&P500returns.

Slide12LabyrinthConsultingServices,Inc. artberman.com

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160

Jan-70

Jan-71

Jan-72

Jan-73

Jan-74

Jan-75

Jan-76

Jan-77

Jan-78

Jan-79

Jan-80

Jan-81

Jan-82

Jan-83

Jan-84

Jan-85

Jan-86

Jan-87

Jan-88

Jan-89

Jan-90

Jan-91

Jan-92

Jan-93

Jan-94

Jan-95

Jan-96

Jan-97

Jan-98

Jan-99

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

CPIA

djustedWTIPrice

s(Ja

nuary2017DollarsPe

rBarrel)

Oil Shocks-->

Massive E&PInvestment(North

Sea,Mexico,Siberia)

Over-Supply, DemandDestruction&PriceDeflation

Debt-FueledEconomicExpansion&Rapid

GrowthinChina&EastAsia

MassiveE&PInvestment(Shale, DeepWater,Heavy

Oil)

Over-Supply, DemandDestruction&Price

Deflation

Current$51OilPrice>40%HigherThanJan1986- Dec2004AverageinApril2017Dollars

Source:EIA, U.S.Bureau ofLaborStatistics &LabyrinthConsulting Services,Inc.

Avg1986-2004 $36/barrel Avg2005-2014$91/barrel

All PricesinConstant April 2017Dollars

Avg1974-1985 $71/barrel<$23/barrel

$50/barrel

1stBubble:1974-1980

2ndBubble:1999-2014

$48/barrel

OilMarketsinEarlyRecoveryFromOilPriceCollapse

• Secondmajorbubblesince1970.• Whenoilpricesgottoohighin2008,thesystemcrashed.Realestateandbankingaretheexplanation

butthecostofenergywasaconstantunderlaying thosefactors.• Whenoilpricesgottoohighagainfrom2011-2014,therewasnofinancialcollapsebuttherewasanoil-

pricecollapse.Itdoesnotfeelascataclysmicas2008forthoseoutsidetheoilindustrybecauseitmadeenergymoreaffordable.

• Oilpricesstill40%higherthanduringperiodofGDPgrowthin1980sand1990s.• Averagepriceofoilsince1950inconstant2016dollarswas$46/barrel.

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

$0

$20

$40

$60

$80

$100

$120

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

E

U.S.G

DP(2016$Trillions)

CPI-AdjustedW

TIPrice(2016$/Barrel)

GDPGenerallyIncreasesWhenOilPricesAreLow

andIsFlatWhenOilPricesAreHigh

OilPrice

GDP

GDP 5Yr

MovingAvg

Source:WorldBank,EIA,U.S.Bureau ofLabor Statistics&Labyrinth Consulting Services,Inc.

Avg1986-2004 $36/barrel Avg2005-2014

$91/barrel

GDP&Oil PricesInConstant2016Dollars

$48/

barrel

Avg1974-1985 $71/barrel<$23/

barrel

Slide13LabyrinthConsultingServices,Inc. artberman.com

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

$20

$22

$24

$26

$28

$30

$32

$34

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

U.S.Public,Corporate&

HouseholdDebt($Trillions)

FederalFundsEffectiveRate(Percent)

U.S.PublicandConsumerDebt&InterestRates

Reagan

Bush

Clinton

Bush

Obama

PublicDebt(RHS)

Source:U.S.Treasury,U.S.FederalReserveBankandLabyrinthConsultingServices,Inc.

InterestRates(LHS)

Carter

Nixon-FordKennedy-Johnson

Eisen-hower

AllDebt(RHS)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jan-00

Jun-00

Nov-00

Apr-01

Sep-01

Feb-02

Jul-0

2 Dec-02

May-03

Oct-03

Mar-04

Aug-04

Jan-05

Jun-05

Nov-05

Apr-06

Sep-06

Feb-07

Jul-0

7 Dec-07

May-08

Oct-08

Mar-09

Aug-09

Jan-10

Jun-10

Nov-10

Apr-11

Sep-11

Feb-12

Jul-1

2 Dec-12

May-13

Oct-13

Mar-14

Aug-14

Jan-15

Jun-15

Nov-15

Apr-16

Sep-16

MillionsofBarrelsofCrudeO

ilPerDay

UnconventionalOilAccountsFor63%ofU.S.Production

Conventional

Unconventional

Source:Drilling Info,EIA,LabyrinthConsulting Services,Inc.&Crude OilPeak

U.S.DebtandTightOil

• U.S.hasbeenfundinggrowthwithdebtsincetheearly1970safterU.S.oilproductionpeaked.• Highinterestratesintheearly1980smadetheTreasurybondthereserveassetoftheworldandallowed

theU.S.toputgrowthonacreditcard.• Lowenergycoststhroughlate1990shelpedgrowth.• LowinterestratesanddollardevaluationaftertheFinancialCollapseproducedcapitalflowtotightoil

plays.• Now,tightoilismorethan50%ofU.S.oiloutputandincreasing.• BakkenandEagleFordplaysareprobablyinslowterminaldecline.• ThismeansthatthePermianbasinisthesolegrowtharea.• Furtherreasonforapricespikeinthecoming5years.