op georgia petworth doc

TRANSCRIPT

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 1/40

December, 2009

DC Retail Action Strategy

SWOT Analysis, Retail Demand Analysis, Strategy and Preliminary Planning DiagramsGeorgia Avenue-Petworth

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 2/40

Georgia Avenue-Petworth SWOT Analysis

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 3/40

The expansive Georgia Avenue-Petworth corridor possesses a unique urban vitality, with an

acve street life despite its outdated shops. Although the area has suered from deferred

maintenance and neglect, a recent urry of residenal and commercial development around

the Georgia-Petworth Metro staon has turned this into a transional community. The area

benets from a strategic locaon: in addion to having a central Metro staon, Georgia Avenue

itself is a major trac corridor. The area is also close to Howard University, Columbia Heights,

the U.S. Soldiers’ & Airmen’s Home (slated for major redevelopment), and several hospitals.

Overview

Introduction

The Georgia Avenue-Petworth corridor is zoned

enrely as commercial. At the top of this

corridor, there is a small area of commercial light-

manufacturing on the west side of Upshur Street

(the east side is commercial for a block). The

surrounding area is zoned mostly as residenal.

A major excepon is 14th Street, which is another

commercial corridor running parallel to Georgia

Ave. In addion to this commercial strip, there

are large amounts of land zoned as government-

owned property, including the U.S. Soldiers’ &

Airmen’s Home and its surrounding area east to

North Capitol Street.

Zoning

Boundaries

Georgia Avenue NW from Upshur Street NW

south to Columbia Road NW

= Core commercial area

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 4/40

Retail Opportunity

Upper Georgia Ave

This area is predominantly

residenal and has a loose urban

fabric. Anchored by Safeway,

apartments dominate. Mom-and-

pop shops are dispersed, except for

a cluster on the east side of Upshur

Street. Projects in the pipeline

reinforce this area’s residenal

character.

Central Georgia Ave (Metro)This central node, anchored by

the Georgia Ave-Petworth Metro

staon, is poised to become theheart of this secon of Georgia

Ave. Because of its accessibility by

Metro and car (it is located at the

intersecon of Georgia and New

Hampshire Aves), this area is primed

for transit-oriented development.

Fingly, several lots by the Metro

are currently under construcon

with mixed-use developments.

Lower Georgia AveThis large area, anchored by

Howard University to the south, has

a high concentraon of price-point

sensive retail in poor condion.

Although it is currently the liveliest

part of this submarket, its shallow

depth limits anchor locaons and

makes it ill-suited for larger-scale

redevelopment.

1

2NODE 2

Ace’s Cash Express

King’s Deli

Temperance Hall

Pipeline Projects:

-Park Place Petworth

Metrorail Development

3

Note: Tenant lists do not include all businesses located in the submarket.

3B

1A

1B

3A

2

1

2

NODE 1

Hair Impressions

Beer and Wine

King’s Nails

Merrell Realtors

ShellWendy’s

Safeway

Pipeline Projects:

-Georgia Commons

-Residences at

Georgia Ave

NODE 3

Car wash

BP

Chinese carryout

Pawnbrokers

Home Improvements

Lion’s LiquorBell Corner Stop

Small Smiles Dental

clinic

Goodies Carry-Out

Super Value

Cleaners-Laundromat

Sunray Market

Universal Madness

Jackson Hewi Tax

Service

Rich Convenient Store

Cluck U Chicken

South Food

3

1A

3B

1B

3A

2

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 5/40

Retail Node 1: Upper Georgia Ave-Petworth

The Upper Georgia Avenue-Petworth corridor can be

divided into 2 sub-nodes: Upshur Street Shops and

Grocery-Anchored Apartments.

B - Grocery-Anchored Apartmentsdescribes a 4-block

area of apartments anchored by a 22,000sf Safewaygrocery store (at the southwest corner of Georgia

Ave and Randolph St). The intersecons south of

Upshur Street (Taylor Street to Randolph Street)

show more potenal to create a disncve character

for Upper Georgia Avenue, as they do not have an

overwhelming amount of infrastructure. Although

retail could cluster around these intersecons, it is

currently dispersed and secondary to residences.

Projects in the pipeline include large apartment

houses like the Residences at Georgia Avenue as wellas approximately 30,000 square feet of retail.

A - Upshur Street Shops is a one-block cluster of shops

directly east of residenal Upper Georgia Avenue.

The intersecon at Upshur Street is currently one of

the largest in this submarket. However, the exisng

infrastructure limits the ability to create an authenc,

pedestrian-centered retail experience (Kansas Street

intersects very close-by, breaking up the lots and

creang huge gaps from a retail perspecve).

9 t h S t r e e

t

K a n s a

s S t

r e e t

= Minor Intersecon

= Neighborhood Intersecon

= Sub-node A

= Sub-node B

= Public open space

A

B

= Major Intersecon

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 6/40

Retail Node 2: Georgia Ave-Petworth Metro

A - Central Georgia Ave, which

includes the area around the

Georgia Ave-Petworth Metro

staon, is poised to catalyze the

redevelopment of this submarket.

The intersecon of Georgia and

New Hampshire Avenues showspotenal to be a very strong

anchor for the area. Although the

intersecon is extremely large, the

Metro acvates it with pedestrians

so that it can funcon well from

a retail perspecve. Fingly, the

area is quickly being redeveloped

with mixed-use projects. Of these

developments, the most signicant

is Park Place, which will add 156

mostly market-rate condos and

townhouses, as well as 17,000sf of

retail, at the Metro staon. This

project, as well as nearby buildings

such as Temperance Hall (a sit-down

restaurant/bar), oer glimpses into

Georgia Avenue’s thriving future.

The Georgia Avenue-Petworth

Metro corridor can be considered a

node unto itself.

R o c k C r

e e k C h u r c h R

o a d

Q u e b e c

P l a c e N o

r t h w e s t

Quincy Street NW

= Major Intersecon

= Neighborhood Intersecon

= Sub-node A

A

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 7/40

Retail Node 3: Lower Georgia Ave-Petworth

The Lower Georgia Avenue corridor can be divided

into 2 sub-nodes with disnct characters: Small Shops

and Schools and Homes.

B - Schools and Homes occupy the boom part of

Lower Georgia Avenue. Bruce Monroe Elementary

School anchors the northern end at Irving Street,

while Howard University is to the south. Although

Howard is a major anchor, its real presence lies further

south of this submarket’s boundaries. Howard’s

Metro stop provides momentum southward for

Lower Georgia Avenue’s redevelopment, just as theGeorgia Ave-Petworth Metro stop pulls northward.

A - Small Shops with neighborhood-serving retail

line this somewhat griy, but lively secon of Lower

Georgia Avenue. There are no obvious anchors or

hierarchy of streets; the exisng retail is small-scale

and generally in poor condion. There is also a small

strip mall between Morton and Lamont Streets withsimilar retail opons (cleaners, laundromat, carry-

out, tax service). Shops in this secon have very

shallow depths because they are adjacent to densely

packed rowhouses with ght alleys for service and

loading. This underlying bone structure makes this

secon unlikely to change from its current live-work

set-up.

= Neighborhood Intersecon

= Sub-node A

= Sub-node B

A

B

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 8/40

Retail Inrastructure

The streetscape along Georgia

Ave is mostly stark, with narrow

concrete sidewalks next to

rundown buildings. Lower GeorgiaAvenue is the main retail corridor,

but has suburban-sized sidewalks.

This small scale occasionally

creates a charming inmacy; for

example, between Harvard and

Hobart Streets, the sidewalk is

paved with brick and has regular

tree planngs. However, this small

scale also makes Lower Georgia

Avenue’s blocks indisnguishable

from each other, as there is no

hierarchy of streets or blocks.

Oddly, the widest sidewalks exist

o of Georgia Avenue on Upshur

Street, where there is a small row of

shops. In terms of trac, Georgia

Avenue is a very busy street.

There are 2 lanes of trac in each

direcon, with an occasional thirdlane occupied by parking.

Streets & Blocks Intersections Buildings Alleys & Service

The main intersecon, located

at Georgia and New Hampshire

Avenues, is large and inmidang

to pedestrians (who are secondaryto auto trac). The intersecon is

also out-of-scale with its current

context of 1-story retail, but the

new Park Place development will

be a more appropriate anchor.

Another signicant intersecon

occurs where Georgia Avenue hits

Upshur Street’s small retail strip;

this smaller intersecon shows

promise as a pedestrian crossing

because of its adjacent grassy

open space. Georgia Avenue’s

intersecon with Randolph Street

is notable because of Safeway.

Lower Georgia Avenue, where the

area’s retail is concentrated, does

not have any major intersecons

and, therefore, seems like one

connuous block because there isno hierarchy of streets.

Georgia Avenue has very limited

space dedicated to service and

loading. Most stores do not have

service alleys; trash cans areplaced outside stores for garbage

collecon, much like they are for

homes. When stores are slightly

larger and set back behind a parking

lot (e.g. Safeway, U-Like Carry-

Out), dumpsters are visible in front

set against the building. General-

use trash cans line Georgia Ave,

but lier is noceable, parcularly

around the Metro staon and

construcon areas. When

redeveloping this submarket, it will

be crical to improve back areas

for service and loading to make

them safe and clean for adjacent

residences.

Buildings on Georgia Avenue

are generally older and have

small footprints. They tend to

be 1-story retail shops or 2-story residenal buildings with

ground-oor retail. With the

excepon of new construcon like

Temperance Hall, these buildings

are mostly rundown. In general,

building facades lack transparency

and oen appear as solid walls

disengaged from the street. This

is especially noceable in the civic

instuons on Lower Georgia Ave,such as Bruce Monroe Elementary

School and Howard University, and

in the large apartments on Upper

Georgia Ave.

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 9/40

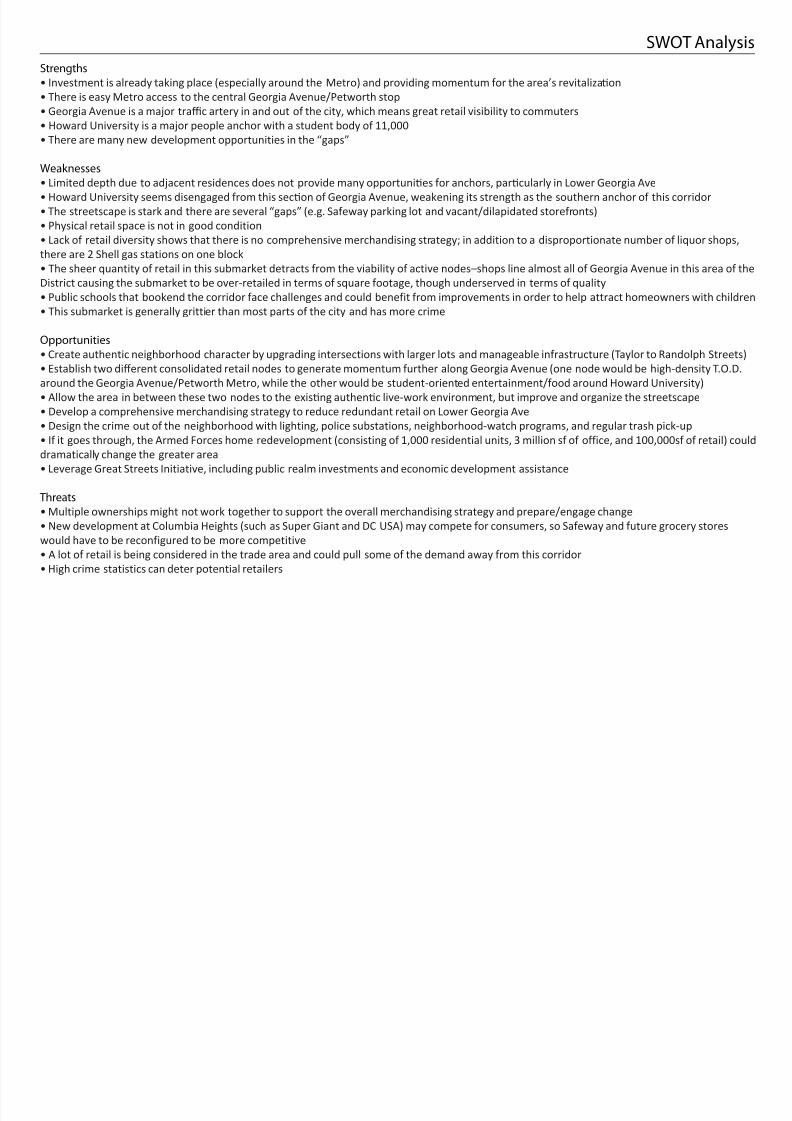

Strengths• Investment is already taking place (especially around the Metro) and providing momentum for the area’s revitalizaon

• There is easy Metro access to the central Georgia Avenue/Petworth stop

• Georgia Avenue is a major trac artery in and out of the city, which means great retail visibility to commuters

• Howard University is a major people anchor with a student body of 11,000

• There are many new development opportunities in the “gaps”

Weaknesses• Limited depth due to adjacent residences does not provide many opportunies for anchors, parcularly in Lower Georgia Ave

• Howard University seems disengaged from this secon of Georgia Avenue, weakening its strength as the southern anchor of this corridor

• The streetscape is stark and there are several “gaps” (e.g. Safeway parking lot and vacant/dilapidated storefronts)

• Physical retail space is not in good condition

• Lack of retail diversity shows that there is no comprehensive merchandising strategy; in addition to a disproportionate number of liquor shops,

there are 2 Shell gas stations on one block

• The sheer quantity of retail in this submarket detracts from the viability of active nodes–shops line almost all of Georgia Avenue in this area of the

District causing the submarket to be over-retailed in terms of square footage, though underserved in terms of quality

• Public schools that bookend the corridor face challenges and could benefit from improvements in order to help attract homeowners with children

• This submarket is generally grittier than most parts of the city and has more crime

Opportunities• Create authentic neighborhood character by upgrading intersections with larger lots and manageable infrastructure (Taylor to Randolph Streets)

• Establish two dierent consolidated retail nodes to generate momentum further along Georgia Avenue (one node would be high-density T.O.D.

around the Georgia Avenue/Petworth Metro, while the other would be student-oriented entertainment/food around Howard University)

• Allow the area in between these two nodes to the exisng authenc live-work environment, but improve and organize the streetscape

• Develop a comprehensive merchandising strategy to reduce redundant retail on Lower Georgia Ave• Design the crime out of the neighborhood with lighting, police substations, neighborhood-watch programs, and regular trash pick-up

• If it goes through, the Armed Forces home redevelopment (consisting of 1,000 residential units, 3 million sf of office, and 100,000sf of retail) could

dramatically change the greater area

• Leverage Great Streets Initiative, including public realm investments and economic development assistance

Threats• Multiple ownerships might not work together to support the overall merchandising strategy and prepare/engage change

• New development at Columbia Heights (such as Super Giant and DC USA) may compete for consumers, so Safeway and future grocery stores

would have to be reconfigured to be more competitive

• A lot of retail is being considered in the trade area and could pull some of the demand away from this corridor• High crime statistics can deter potential retailers

SWOT Analysis

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 10/40

Georgia Avenue-Petworth Preliminary Planning Diagrams

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 11/40

Planning Analysis Node 1: Upper Georgia Ave-Petworth

9 t h S t r e e

t

K a n

s a s

S t r e

e t

General Observaons about Exisng Area:

1) Upshur Street, Georgia Avenue, and Kansas Avenue meet to

create a mega-intersecon that is dominated by vehicular trac

and inmidang to pedestrians. Small, awkwardly shaped

blocks also make this intersecon dysfunconal for retail.

2) A concentraon of large leasing depths near the exisng

Safeway grocery make way for a successful retail and mixed-use

clustering at the intersecon of Georgia Avenue and Randolph

Street.

3) The setback of the exisng Safeway from the street

contradicts the city’s vision of Georgia Avenue as a pedestrian-

friendly retail experience.

Retail Planning Principles:

1) Take advantage of large, vacant, and single-owned parcels

for mixed-use development.

2) Focus on revitalizing the streets, sidewalks, and storefronts

in areas with exisng businesses and limited site depth for

redevelopment.

3) Design high-density, mixed-use buildings that are sensive to

the character of adjacent low-scale residenal buildings.

= Major Intersecon

= Neighborhood Intersecon

= Node 1

= Minor Intersecon

= Prime Corner

= Neighborhood Intersecon

= Minor Intersecon

= Major Intersecon= Major Intersecon

= Neighborhood Intersecon

= Node 1

= Minor Intersecon

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 12/40

Planning Concepts Node 1: Upper Georgia Ave-Petworth

The following concept diagram is intended to be used as a general guide for retail improvement opportunies.

Actual building conguraons and mix of uses should be reviewed on a parcel-by-parcel basis.

HIGH-DENSITY, MIXED-USE AND LOW-DENSITY, SINGLE-USE

DEVELOPMENT OPPORTUNITIES

Consolidang derelict and vacant properes creates favorable

dimensions for developing high-density, mixed-use buildings.

Capitalizing on the opportunity to consolidate and introduce a

mixed-use product would ensure that Georgia Avenue becomes

the transit-oriented development the city has envisioned.

Adjacent to the triangular park and setback from Georgia Avenue,

this locaon is ripe for low-scale, residenal inll development.

Where retail can suer from a lack of visibility, residenal uses

prosper from the privacy of neighborhood streets.

5

Redevelopment Opon 1

= Prime Corner

= Major Intersecon

= Neighborhood Intersecon

= Minor Intersecon

= Mixed-Use Opportunity

= Single-Use Opportunity

= Reinvestment Opportunity

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 13/40

Planning Concepts Node 1: Upper Georgia Ave-Petworth

The following concept diagram is intended to be used as a general guide for retail improvement opportunies.

Actual building conguraons and mix of uses should be reviewed on a parcel-by-parcel basis.

REINVESTMENT/REPOSITIONING OPPORTUNITIES

Street-calming techniques should be considered at the intersecon

of Upshur Street and Georgia Avenue to create a more pedestrian-

friendly crossing; however, focusing energy and eorts to produce

strong retail experiences at other intersecons is advised. The

intersecons between Taylor and Randolph Streets should be

upgraded in scale to become authenc neighborhood-dening

intersecons.

Streetscape and storefront incenves will improve the two-sided

retail experience along Upshur Street. Taking advantage of the

large sidewalk depths to create disnguishable zones that describe

a storefront zone, a pedestrian zone, and an amenity zone is one of

the possible strategies to consider.

Reposioning Safeway, located at the southwest corner of Randolph

and Georgia Avenue, to beer engage the street and updang it toa higher-quality oering is necessary to respond to the changing

demographics and demand of the area.

5

Redevelopment Opon 1

= Prime Corner

= Major Intersecon

= Neighborhood Intersecon

= Minor Intersecon

= Mixed-Use Opportunity

= Single-Use Opportunity

= Reinvestment Opportunity

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 14/40

General Observaons about Exisng Area:

1) Several new mixed-use projects have come to

dene this area as the transit-oriented core of

Georgia Avenue.

2) Awkward-shaped blocks at the intersecon of

New Hampshire Ave, Georgia Avenue, and Rock

Creek Church Road create a hosle pedestrian

environment.

3) New investment into some of the exisng

storefronts along Georgia Avenue highlights the

potenal for local retailers in this area.

Retail Planning Principles:

1) Embrace the momentum of the current mix-

use, transit-oriented developments.

2) Design high-density, mixed-use buildings that

are sensive to the character of adjacent low-

scale residenal buildings.

3) Cherish the exisng building stock through

restoraon and preservaon eorts.

Planning Analysis Node 2: Georgia Ave-Petworth Metro

G e

o r g i a A v e n u e

N e w

H a m

p s h i r e A v

e

Quinc y S tree t Nor th wes t

R o c k C r

e e k C h u

r c h R o a d

Q u e b e c

P l a c e N o

r t h -

= Prime Corner

= Neighborhood Intersecon

= Minor Intersecon

= Major Intersecon= Major Intersecon

= Neighborhood Intersecon

= Node 2

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 15/40

The following concept diagram is intended to be used as a general guide for retail improvement opportunies.

Actual building conguraons and mix of uses should be reviewed on a parcel-by-parcel basis.

HIGH-DENSITY, MIXED-USE DEVELOPMENT OPPORTUNITIES

Parcels bordering the Metro should be considered as part of a

transit-oriented, mixed-use strategy. Respecul consideraon

to the low-scale residenal properes that surround the

potenal mixed-use density will produce a more posive and

integrated community

REINVESTMENT/REPOSITIONING OPPORTUNITIES

Preserving good building stock along Georgia Avenue will

reinforce the established character of the neighborhood.

Introducing neighborhood-serving retail within these blocks

will beer dene the Georgia and New Hampshire Avenue

intersecon as the focal point of this trade area.

Planning Concepts Node 2: Georgia Ave-Petworth Metro

= Prime Corner

= Major Intersecon

= Neighborhood Intersecon

= Mixed-Use Opportunity

= Reinvestment Opportunity

Redevelopment Opon 1

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 16/40

Planning Analysis Node 3: Lower Georgia Ave-Petworth

3

General Observaons about Exisng Area:

1) Short blocks, shallow leasing depths, and mulple

ownerships limit future expansion of retail in this

submarket south of Os Place.

2) Howard University serves as a “people anchor”

for the corridor.

3) While the University’s inuence extends both

to the north and south along Georgia Avenue,

momentum around the Shaw-Howard University

Metro staon to the south has detracted aenon

and investment from the northern part of the

neighborhood.

Retail Planning Principles:

1) Focus on making exisng retail beer rather than

creang addional retail.

2) Tailor merchandising to reduce redundant retail.

3) Devise a branding strategy that denes the

character of retail in this node as something unique

to the Georgia Avenue corridor.

= Prime Corner

= Neighborhood Intersecon

= Minor Intersecon

= Major Intersecon= Neighborhood Intersecon

= Node 3

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 17/40

= Prime Corner

= Neighborhood Intersecon

= Reinvestment Opportunity The following concept diagram is intended to be used as a general guide for retail improvement opportunies.

Actual building conguraons and mix of uses should be reviewed on a parcel-by-parcel basis.

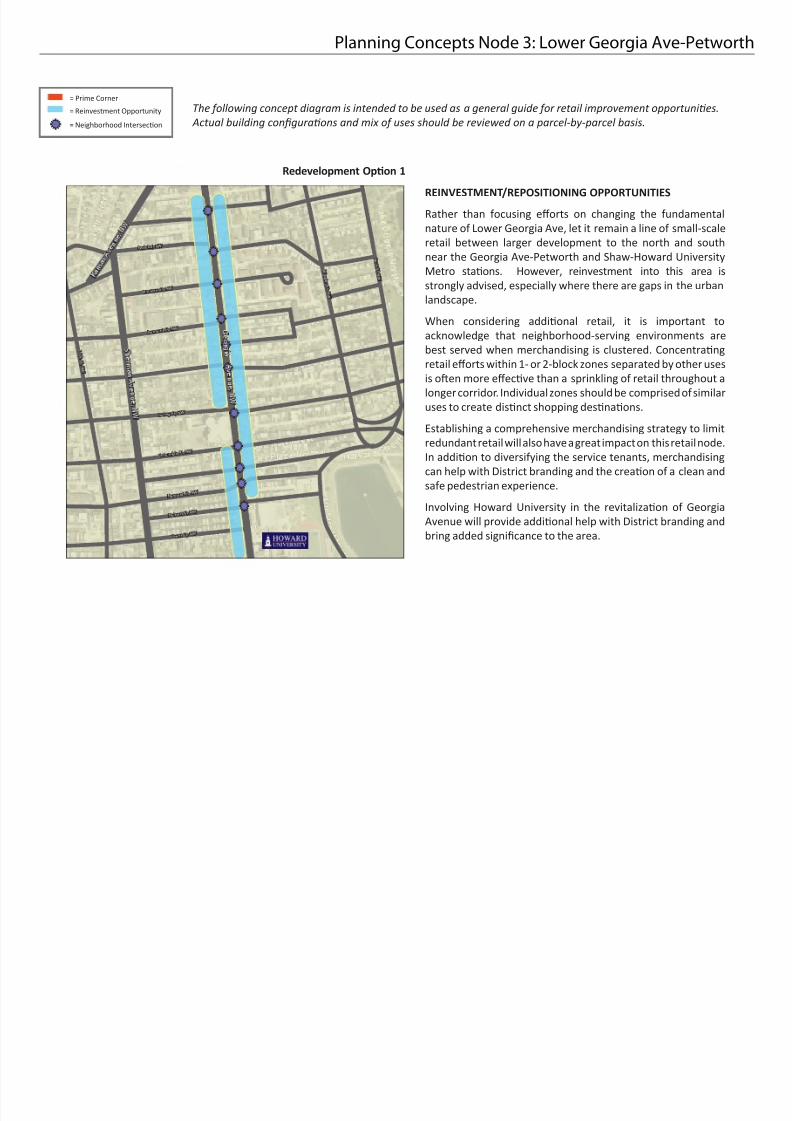

Planning Concepts Node 3: Lower Georgia Ave-Petworth

REINVESTMENT/REPOSITIONING OPPORTUNITIES

Rather than focusing eorts on changing the fundamental

nature of Lower Georgia Ave, let it remain a line of small-scale

retail between larger development to the north and south

near the Georgia Ave-Petworth and Shaw-Howard University

Metro staons. However, reinvestment into this area is

strongly advised, especially where there are gaps in the urban

landscape.

When considering addional retail, it is important to

acknowledge that neighborhood-serving environments are

best served when merchandising is clustered. Concentrang

retail eorts within 1- or 2-block zones separated by other uses

is oen more eecve than a sprinkling of retail throughout a

longer corridor. Individual zones should be comprised of similar

uses to create disnct shopping desnaons.

Establishing a comprehensive merchandising strategy to limit

redundant retail will also have a great impact on this retail node.

In addion to diversifying the service tenants, merchandising

can help with District branding and the creaon of a clean and

safe pedestrian experience.

Involving Howard University in the revitalizaon of Georgia

Avenue will provide addional help with District branding and

bring added signicance to the area.

Redevelopment Opon 1

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 18/40

The retail submarket is located along Georgia Avenue NW rom Upshur Street NW south to Colum-bia Road NW.

Key Elements

• Theretailsubmarketissituatedalongamajor

north-south artery, Georgia Avenue NW. Develop-ment trends are centered at the Georgia Avenue-

Petworth Metro Station (green line)

• Tradeareasassessresidentsandotherpotential

customers that could be drawn to the site

• Theprimarytradeareaencompassestheblock

groups within a ¼ mile o the retail submarket; the

secondary trade area includes the block groups

within a ½ mile o the retail submarket (reasonablewalking distances or pedestrian shopping)

• Primarytradearearesidentsareexpectedtobe

requent customers, with a ocus on those living clos-

esttothesite;secondarytradearearesidentsareex-

pected to be consistent, but not requent customers

• Potentialcustomerswhoarenotprimaryorsec-

ondary trade area residents are accounted or by an

“inow” actor; this is a percentage applied to poten-tialexpendituresatthesite

• ThetradeareaisboundedontheeastbytheUS

Soldiers’ and Airmen’s Home

• TradeareaincludesaSafewaysupermarketand

small, independent retail and service outlets

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 19/40

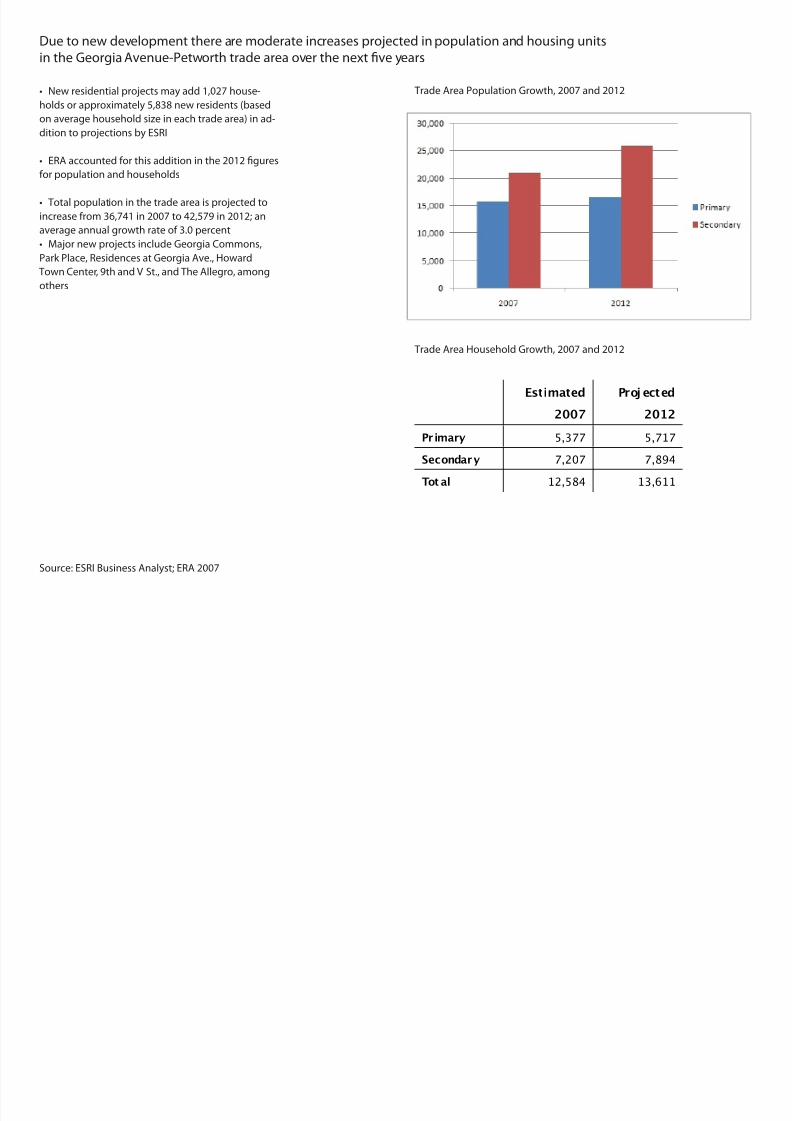

DuetonewdevelopmenttherearemoderateincreasesprojectedinpopulationandhousingunitsintheGeorgiaAvenue-Petworthtradeareaoverthenextveyears

• Newresidentialprojectsmayadd1,027house-

holdsorapproximately5,838newresidents(based

on average household size in each trade area) in ad-

ditiontoprojectionsbyESRI

• ERAaccountedforthisadditioninthe2012gures

or population and households

• Totalpopulationinthetradeareaisprojectedto

increasefrom36,741in2007to42,579in2012;an

averageannualgrowthrateof3.0percent

• MajornewprojectsincludeGeorgiaCommons,

Park Place, Residences at Georgia Ave., Howard

Town Center, 9th and V St., and The Allegro, among

others

Source:ESRIBusinessAnalyst;ERA2007

TradeAreaPopulationGrowth,2007and2012

TradeAreaHouseholdGrowth,2007and2012

Estimated

2007

Projected

2012

Primary 5,377 5,717

Secondary 7,207 7,894

Total 12,584 13,611

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 20/40

GeorgiaAvenue-PetworthKeyDemographics:TradeAreaHouseholdProle

• TheGeorgiaAvenue-Petworthtradeareamaybegenerallycharac-

terized as a working class neighborhood. The primary and secondary

tradeareashaveamedianhouseholdincomeof$38,808and$38,944

respectively

• Medianfamilyincomeis$46,731and$48,148intheprimaryandsec-

ondary trade areas

• Mediannetworthincludeshomevalues.Thetradearea’spopulationis

61% Arican-American. “Other” groups make up 26% o the population*

*“Other”includesmixedracialpopulationsorself-identiedassuch.Thegroupmay

include Latinos or Hispanics who do not identiy with another race. Latino and Hispanic

are ethnic groups, not racial, but may include people o several racial groups

Source:ESRIBusinessAnalyst;ERA2007

IncomeStatistics,2007

RacialandEthnicGroups,2007

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 21/40

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 22/40

GeorgiaAvenue-PetworthKeyDemographics:TradeAreaHouseholdProle

• Homeownershippatternsinthetradeareaareabout

evenlysplit,with53%ofhouseholdsrentingtheirhomes

and47%ofhouseholdsowningtheirresidences

• Asignicantnumberofhomeownersisgenerally

considered a positive indicator o neighborhood stability.

Home ownership rates also impact the median house-

hold net worth

• In2007tradearearesidentsspentatotalof$203.8

million on products and services in the categories repre-

sented on the graph. This is total spending everywhere,

notjustinthetradearea

• Householdexpendituresinthetradeareashowlower

amounts being spent or personal care and household

urnishings. The stronger perorming categories are gro-

cery, entertainment and ood & drink away rom home.

Aspreviouslynoted,projectedagecohortchanges

will continue to support entertainment and oodservice

businesses, but personal care may increase as the area

includes more “empty nest” households

Source:ESRIBusinessAnalyst;ERA2007

HomeOwnership,2007

HouseholdExpenditures(InMillions)byCategory,2007

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 23/40

Development Pipeline

PipelineProjects

• Multiplenewandplannedprojectsinthe

Georgia Avenue-Petworth trade area will deliverresidential and retail space

• Therearecurrently6projectsunderconstruc-

tion in the Georgia Avenue-Petworth trade area.

Theseprojectswilldeliver:

• 37,827squarefeetofretailspace

•556residentialunits

• Thereareanother6projectsplannedinthe

Georgia Avenue-Petworth trade area that may

deliver :

•21,400squarefeetofretailspace

•463residentialunits

Source:ESRIBusinessAnalyst;ERA2007

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 24/40

Overview o Market Demand Analysis

The purpose o the market analysis is to provide quantitative data that, combined with qualitative analysis in the Strengths-Weaknesses-Opportunities-

Threats (SWOT) section, inorm the retail development strategy or the submarket and provide a tool to DC government, private developers, retailers,

and community organizations or developing retail business opportunities.

Developing Estimates o Supportable Square Footage

A key component o the quantitative analysis is the determination o the quantity o retail space supportable in each submarket. To calculate this, retail

demand or spending within the trade area along with an estimate o the spending that the submarket could capture are measured. Various actors are

takenintoaccountindevelopingsubmarketcapturerates,suchasthequalityofexistingretailoeringsandtradeareacompetition.Retailspending

potentialforeachmajorretailcategory(ConvenienceRetail,SpecialtyRetailandFood&Beverage/RestaurantsotherFoodService)isdividedbythe

retail industry standard or sales-per-square oot (sometimes called retail sales productivity) to arrive at an estimate o retail square ootage that the

submarketcansupport.Submarketdemandiscomparedtosupplybysubtractingtheexistingretailinventorytodeterminethenetsupportablesquare

eet or retail space.

Forpotentialfuturedevelopmentin2012,pipelineresidentialandcommercialprojects,andassociatedincreasesintradeareaexpenditures,arefactored

intofuturedemand.Onthesupplyside,thepipelineof“underconstruction”and“planned”retailprojectsissubtractedfromtheestimateofsupportable

retail space, as it is assumed that the new space will absorb an equivalent amount o space at the threshold productivity levels.

Generally speaking, retail market demand analysis should not be considered conclusive, as it combines “typical” and “industry average” perormance

measureswithprofessionaljudgmentbasedonlocalconditionsandknowledgeofthemarketandretailindustry.Thereareseveralfactorsthatwilldeter-

mine the success or ailure o any individual retail business; that is why the industry is constantly changing. This analysis is intended to guide the Retail

Action Strategy to opportunities to recruit potential successul retail categories based on estimated demand potential.

*Estimatedretailspendingpotentialisbasedonhouseholdspendingpatterns,householdincomeandhouseholdcompositionasreportedbytheConsumerExpen-

diture Survey prepared by the US Census or the US Bureau o labor Statistics. For retail sales productivity rates, ERA used a range o retail industry-based sales per

squarefootestimatesbasedonthecompany’sexperienceinurbancommercialdistrictssimilartoeachindividualsubmarket,asshoppingcenterindustrystandardsdo

notalwaysreectcomparableperformanceineithermarketorientationornancialstructurebylocally-ownedbusinessesorbysmaller/oldercommercialbuildings.

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 25/40

Retail Demand: Primary Trade Area Supportable Retail Space

Retailersmeasurebusinesssuccessbycomparingtheirsalespersquarefootorproductivityagainsttheircostsandrevenueobjectivesaswellas

reportedretailindustrystandardsforcomparabletypesofstores.Theamountretailerscanaordtospendforrentisalsodeterminedbyannualsales

(boththetotalamountandsalespersquarefootperyear).Retailrentsusuallyrangebetween8percentand12percentoftotalannualsales.

This industry standard is a benchmark by which retail per ormance can be determined.

Local retailers whose sales all below these industry standards may be considered to be underperorming; the reasons or underperormance may

be a result o the size o the market, stronger competitors with better merchandise, merchandising, and/or better pricing, or undercapitalization. Under-

perorming retailers may cause the analysis o supportable square ootage to be underestimated. The higher perorming operators can capture market

sharefromexistingretailersaswellasnewcustomersnotcurrentlypatronizingacommercialdistrict.Whenconsideringacommerciallocationordistrict

such as the submarkets included in this analysis, retailers oten review the levels o rent achieved by property owners as an indication o the level o sales

that other retailers are generating.

Loweraveragerentlevelsalsoinuencetheamountthatpropertyownerscanaordtoinvestinpropertyimprovementstoretainexistingtenantsor

recruitnewones.Ifpropertyownersareunabletooertenantimprovementsbecauserentsaretoolow,theretailersarethenrequiredtoincreasethe

amount they must spend to prepare a building to become a store, caé, or consumer service business. The greater the amount the retailer is required to

investinspaceimprovements,thegreaterthenancialrisk,resultinginadditionalnancialpressuresduringtheearlyyearswhiletheretailerisbecoming

established and building a customer base. Districts presenting a higher risk o ailure have difculty attracting well managed, well capitalized businesses.

Thisrelationshipestablishestheconnectionbetweenthetotalsalesthatretailerscanachieve,theamounttheycanaordtopayinrent,andwhether

thepropertyownerswillbewilling(orable)toinvestinmajorneededbuildingupgrades(electricalsystems,HVAC,ortenantimprovements)toattractor

retain retail tenants.

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 26/40

Trade Area Resident Spending

• Retailopportunitiesaremeasuredusingtradearearetail

expenditures,whichdescribeconsumerspendingpatterns

• Expenditurestypicallycoverresidentspending,buthave

beenadjustedtoincludeworker,visitor,andotherspend-

ing, as appropriate

• Keycategoriesinclude:

•ApparelandApparelSer vices

•Enter tainmentandRecreation

•PersonalCare

• HouseholdFurnishingandEquipment

•Grocery

•FoodandDrinkAwayfromHome

• EntertainmentandRecreationincludesexpenditures

such as ees and admissions, TV/video/sound equipment,

pets, toys, recreational vehicles, sports equipment, photo

accessories, and reading

•PersonalCareincludesstoressuchas,drugstores(ex-

cluding prescription drugs) cosmetic stores, and services

(nail salons, hair salons, shoe repair, etc.)

•Grocery(foodanddrinkforconsumptionathome)

absorbsthemostexpendituresforthehouseholdsinthe

trade area

Source:ESRIBusinessAnalyst;ERA2007

TradeAreaExpendituresByCategory(InMillions),2007

$204MillionTotal

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 27/40

Captureratesareappliedtototaltradeareaexpendituresinordertoestimatepotentialexpendi-tures within the retail submarket

A capture rate is calculated as a percentage o sales

expectedfromhouseholdsorinowshoppersintheentire

trade area.

Therateisdevelopedbyexaminingthetradearea’sex-

istingretailoerings,qualityofretailers,thepotentialfor

increased sales with improved retail operations, size o the

tradeareaandaprofessionaljudgmentconsideringnearby

competition and other available retail purchasing opportuni-

ties or customers.

Theanalysisutilizescaptureratesspecictothetradearea

to calculate likely on-site spending within the retail submar-

ket.Forexample:

• A10%capturerate=$10ofevery$100spentwilloccur

in the retail submarket

• Notethat100%capturerateisnotpossible,astherate

reects all retail purchasing opportunities available to the

shoppers in the trade area

• Thecapturerateisgenerallyamajordeterminateofa

retail submarket’s viability

Source:ESRIBusinessAnalyst;ERA2007

Georgia Ave.– Petworth Submarket Capture Rates By Category

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 28/40

Estimated Captured Spending within the Retail Market

• CapturedspendingintheGeorgiaAvenue-Petworth

tradeareawasestimatedtobe$42.6millionin2007com-

paredtototaltradeareaspendingof$204millioninthe

same year

• CapturedspendingintheGeorgiaAvenue-Petworth

tradeareaisexpectedtobe$46.2millionin2012com-

pared to total trade area spending o $223 million in the

same year

• IntheGeorgiaAvenue-Petworthtradeareathereare

signicantalternativeshoppingalternativesatDCUSAon

14thStreetNW.Althoughoutsideofthesecondarytrade

area, these alternatives restrict the retail submarket’s ability

tocapturesignicantexpenditures

• ERAestimatesby2012thatGroceryspendingwillac-

countformorethan$35.8millionannuallyandFoodand

Drink(awayfromhome)willaccountforalittleover$5mil-

lion annually

• Capturedspendingintheretailtradeareaisexpected

toincreasebymorethan$3.6between2007and2012,

due mostly to moderate changes in population and income

levels

Source:ESRIBusinessAnalyst;ERA2007

EstimatedCapturedRetailTradeAreaSpending,2007

EstimatedCapturedRetailTradeAreaSpending,2012

$42.6Million

$46.2Million

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 29/40

Productivity and Typical Store Size

• Acalculationofstoreproductivityistypicallybasedon

optimal perormance o quality retailers, not actual opera-

tors

• Howeverthelowerqualityoftheretailspaceavailablein

this retail submarket requires that a lower than “optimal”

productivityratemustbeusedtoadjustthesupportable

square ootage calculation

• Thesquarefootageofretailtypedoesnotindicatenum-

ber o stores since stores sizes vary

“Typical” stores sizes might be:

•Apparel3,500SF

•Accessories2,000–10,000SF

• PersonalCare2,000–10,000SF

•HouseholdFurnishings3,500–10,000SF

• GroceryStores-30,000to65,000

• Restaurants3,000–6,000+SF

• QuickServicefood1,200–3,500SF

• Theretailsubmarketoeringscouldbeanchoredbya

supermarket, a collection o restaurants and neighbor-

hood-ocused goods and services

• Thebestwaytoestimateasite’sproductivityistoassessannuals

salespersquarefootforcomparableprojects

• Thetypeofretailoftenimpactsthesalespersquarefoot(i.e.jewelry

versus urniture)

While the productivity rates used or this submarket were based on

national averages as reported by the International Council o Shopping

Centers (ICSC), ERA used the lower national rates to reect space limi-

tations and likely perormance in the submarket. The rate still reects the

minimum productivity that would be needed or a quality retail operation

return on investment.

Source:ESRIBusinessAnalyst;ERA2007

Georgia Ave.- Petworth Submarket Comparable Productivity

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 30/40

2007NetSupportableSquareFeet

• Basedonthecurrentandprojectedlevelof

households in the trade area and their spending

patterns, the Georgia Ave-Petworth submarket

cansupportbetween88,100and117,300square

feetofretailin2007

• Theexistingretailinventorytotals127,037

square eet within the retail submarket. In order to

take into account the lower quality space it was

discountedto40,652squarefeet(seedetailed

explanationonpage17)

•Theretailsubmarkethasanetsupportablesquarefootrangebetween47,448and76,648

in2007

• Basedontypicalstoresizeandspendingpat-

terns,thesitecansupport,agrocerystore(ex-

pansion o the current Saeway plus planned Yes!

Organic), one to two restaurants, and one or more

entertainment/recreation stores such as a gym or

book store

• Whilethereisevidencesuggestingsupportfora

couple o apparel stores, such businesses perormbest in a larger cluster

Source:ESRIBusinessAnalyst;ERA2007

EstimatedNetSupportableSquareFeet2007

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 31/40

2012NetSupportableSquareFeet

• Basedonestimatedtradeareaexpenditures

and capture rates, the Georgia Ave-Petworth

submarketcansupportbetween95,400and

127,100squarefeetofretailin2012

• Thereisapproximately59,227squarefeetof

new retail planned or under construction in the

trade area including the space at Park Place and

the Residences at Georgia Avenue

• Theexistingretailsquarefootageandplanned

newprojectsaresubtractedfromthesubtotalto

arriveatnetsupportablesquarefootagefor2012

•TheGeorgiaAvenue-Petworthsubmarkethas a net supportable square ootage rangebetween(4,479)and27,221in2012

Source:ESRIBusinessAnalyst;ERA2007

EstimatedSupportableSquareFeet2012

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 32/40

Commentary on the Current Retail Inventory

According to CoStar Group Real Estate Inormation Services, there is

211,450squarefeetofretailspaceintheGeorgiaAvenue-Petworth

tradearea.Withintheretailsubmarketitself,thereare127,037square

feetofretailspace.Todeterminenetsupportablesquarefeet,theexist-

ing retail space is subtracted rom the gross supportable square eet.

Onemajordeterminantofopportunityreliesonthequalityoftheexisting

space – how competitive is the space relative to the rest o the trade

area and other competitive districts?

A recent study o Great Streets neighborhood retail or the Ofce o the

Deputy Mayor or Planning & Economic Development studied the quality

oftheexistingretailspaceinseveralcommercialdistrictstodetermine

thefeasibilityofataxincrementnance(TIF)district,includingGeorgia

Avenue – Petworth. While the study area did not coincide directly with

thetradearea,theassessmentoftherelativequalityoftheexisting

building stock suggests the general condition o the property inventory

in the area.

Thestudyconcludedthat68%oftheretailinventoryinthetradearea

was Grade “C”, or inadequate, or contemporary retailing needs. It also

statedthat22%ofspacewasclassiedas“buildtosuit”(BTS),mean-

ingspaceconstructedforaspecicpurposeortenantinsuchamanner

that makes conversion to another use or tenant impractical. Only 2%

and8%wereratedClassAandB,respectively.Inordertocalculate

supportablesquarefootage,theexistingspacewasdiscountedby

removing the Grade “C” inventory rom the equation. The average age o

theinventoryis79years.

Inaddition,theretailsubmarketisadjacenttoconsiderablenewre-

taildevelopmenttothesouthalongGeorgiaAvenueandeaston14th

Street immediately beyond the secondary trade area.

Retail opportunities are limited in the retail submarket partially due to

poorqualityofexistingretailspace,limitedhouseholdincomes,anda

lower concentration o households.

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 33/40

Multiplefactorswillultimatelyaectthesupportablesquarefeetandsuccessoftheretailsub-market’soeringsoverthelong-term

The success and appeal o a retail district is directly linked

toitsmerchandisemixanditsfunctionasadestination

Incorporating other uses and programs may limit retail

space,butcomplementoverallproject

The trade areas are capable o spending a certain amount.I more $$ are spent in one store less $$ will be spent

elsewhere

A store’s size, placement within the district, interior and

storeront design are part o total appeal or customers

Price-points and merchandise should accurately reect the

demographics and liestyle characteristics o the customers

Merchandise quality/price positioning/merchandising/mark-

up relative to cost o goods, as well as store size and other

operatingfactors,inuencearetailers’protability(Sales/

SF)

FactorsAectingStoreSupportableSquareFeet,2007

FactorsAectingStoreProductivity

Well-formedMerchandise Mix

Higher Store Productivity

Incorporation of OtherUses

24,848 SF 46,748 SF32,148 SF

Stores Cater to MarketCharacteristics

Location, Design, &Configuration

Type of Store

Low Sales / SF High Sales / SF

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 34/40

Detailed captured retail spending on site by category and market

2007PotentialCapturedSpendingonSite 2012PotentialCapturedSpendingonSite

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 35/40

Georgia Avenue-Petworth Strategy

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 36/40

Georgia Avenue Petworth

Introduction

TheGeorgiaAvenuePetworthsubmarketisalongcorridorofapproximatelysixteenblocksextendingfromjustbelowGirardStreetonthesouth

to a location north o Upshur Street on the northern boundary; the central part o the corridor includes the Metro station at Georgia and New

HampshireAvenues,thecorridor’smajorintersection.Accordingtocensusdata,theprimaryandsecondarymarketincludedabout12,600residentsin2007,andisprojectedtoaddapproximately1,000newresidentsby2012.Theaveragehouseholdincomesareincreasingover

thesameperiodbyapproximately18%intheprimaryandsecondarymarketsduehigherincomeresidentsinnewpipelineprojects,proximity

to Metro and the area’s central location in the District o Columbia. Median household incomes, the primary ocus in determining retail viabil-

ityin2012,areprojectedtoincreasemoremodestly(fromabout$38,800to$39,950intheprimarytradeareaand$45,150to$46,300inthe

secondarytradearea,orabout3.0%to3.5%,respectively).Thissuggeststhatthemajorityofhouseholdswillremaininsolidlower-middleto

middle-income ranges. The primary land uses around the corridor are residential, much o it in blocks o rowhouses and single amily homes

that characterize traditional, pedestrian-scaled DC neighborhoods. Howard University abuts the southern boundaries o the Georgia Avenue

Petworthstudyarea,butits11,000studentsarenotcurrentlyaprimarymarketopportunityforthecorridorduetofragmentedoeringsandthe

other competiting areas.

Based on the SWOT Analysis, Retail Demand Analysis and Preliminary Planning Diagrams completed as part o this submarket analysis, the

mostecientapproachtomaximizingthevalue,mixandappropriatenessofretailinthissubmarketrequiresacknowledgingthefollowingbasic

assessmentsoftheareaandthentakingthespecicactionslistedbelow.

Merchandising Concepts

The submarket is comprised o three separate nodes, each o which is a distinct neighborhood-serving retail area. With new competition rom the

SuperGiantsupermarketandDCUSAprojectsinColumbiaHeightsnearthesouthernendofthecorridorandpotentialcompetitionfromafutureredevelopment o the U.S. Soldier’s and Airmen’s Home site at the northern end o the corridor, the Georgia Avenue Petworth submarket should

continue to ocus on serving neighborhood needs rather than attempting to compete with nearby destination retail. Neighborhood-serving retail

functionsbestwhenconcentratedinclusters,andthethreeexistingnodesalongGeorgiaAvenueprovideafoundationuponwhichthisstrategycan

bedevelopedasappropriatefortheirrespectivepopulations,locationsinproximitytotheMetroandpipelineprojects,andqualityofavailableretail

spaces.GeorgiaAvenue’sdailyautocommutervolumesaresignicant,but,otherthanthegrocerystores,mostcommutertracpassesthrough

thecorridoranddoesnotstop:bothcommuterbehaviors(inwhichconsumer-spendingpatternsaremoreaectedbyproximitytohome)andthe

more modest market potential along this portion o Georgia Avenue will limit the degree to which the commuter market can be captured by Georgia

AvenuePetworth’sretailoeringinthenextveyears.

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 37/40

ThethreenodesidentiedintheSWOTarebasedonanassessmentofhowshoppingpatternsarelikelytooccurovertime.TheParkPlacedevelop-

mentwilladdretailactivity,squarefootageandapproximately160residentialunitsasaTransitOrientedDevelopment(TOD)attheMetrostationin

the central node. Merchandising niches or the northern and southern nodes should ocus on more neighborhood serving need or ood, pharmacy,

and convience needs. The relatively small resident population will make it more difcult to recruit a critical mass o apparel and accessories shops.

Professionalservices(suchasaccountants,taxservices,spas,attorneys,insuranceoces,etc.)averaging1,000to3,000squarefeetwillroundoutthe

consumer services category

Node1-UpperGeorgiaAvenueNW:TheretailpositioningopportunityforGeorgiaAvenuePetworthwillevolveovertimeasexistingusesare

upgraded and new uses are introduced. These uses will provide or incremental grocery sales and will draw some inow trafc rom the second-

arytradeareamarket.Whilehavingbeenalong-termpartofretailmixinthePetwortharea,theexistingSafewaystoreinNode1isanolder,

smallerstore(at22,000squarefeet)andisplannedtoberenovatedinresponsetothenewcompetitiveenvironment.TheretailclusteratUp-

shur continues to be a good location or independent businesses serving neighborhood needs. These businesses should be ostered and sup-

ported as the market changes.

Node 2- Central Georgia Avenue (Metro): The Metro station and Metro bus stops in Node 2 strengthens the central zone as an intermodal transit

connection,andcouldencouragenewretailservices.RetailerswhohavebecomeestablishedintheUStreetCorridorwouldbeagoodtforthe

Petworthareaasitsresidentialbasegrows;examplesincludespecialtystoressuchasHomeRulekitchen/homeproducts(approximately850to1,000square eet). Other retail uses oriented toward a primarily residential consumer base include casual dining and bars (to complement Domku Bar &

Cafe,TheLookingGlassLounge,andotherexistinglocations).ExamplesincludeHardTimesCaféorSalaThai(approximately1,500to1,800square

eet). The CVS planned near the Park Place development above the Metro Station will address convenience and pharmacy needs or the submarket.

Neighborhooddemandsupportsasupermarket-andoneisplanned,(anew5,000squarefootYes!OrganicMarket)thatwillcompetewiththe

redeveloped Saeway in Node 1. As a DC-based local retailer, the Yes! Organic Market may require support in its market positioning to distin-

guishitselffromanynewoeringsatSafeway.Arecreationaluselikeagym(examplesincludeGold’sGymorWashingtonSportsClubat8,000

to20,000squarefeet)couldbesupported,butthearea’sdemographicsandavailablecommercialfootprintsmaymoreappropriatelysupport

thetypeoftnesstrainingfacilitiessuchasResultsGymonUStreetnear16th.Theneighborhoodcouldsupportacoeeshopforcommunity

gatherings;examplesincludecoeebarssuchasTrystorMayorgaandlocalcafesandentertainmentvenuessuchasSaint-Ex.Typicalleasedspacesforthesecategoriesoffoodservicewouldrangefrom850squarefeetto2,500squarefeet.Amulti-useoptionmodelmaybeBusboys

&Poetson14thStreetwhichcombinesarestaurant,acoeehouse,abookstoreoralivemusic/performancevenueinasinglelocation.W

Domku and the Looking Glass Lounge have provided popular dining places in their respective locations; the uture retail strategy should support

existingcafesandrecruitmissingconceptssuchasacoeeshoptobroadentheoeringsofcommunitygatheringplaces.

Node 3- Lower Georgia Avenue: There are retail space constraints in the lower area o the submarket resulting rom shallow lot and building depths.

Thesewilllimitexpansion/recruitmentopportunitiesinthisnode,andmanyretailspacesalsoneedsubstantialrehabilitationtobecompetitive.In

the Lower Georgia Avenue node south o Otis Place, multiple ownership o shallow lots limits the long-term prospect or development o new retail

in this area, but the area could build on its growing identity as a neighborhood serving retail node. This node currently includes carry-out ood and

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 38/40

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 39/40

calming measures at the intersection o Georgia and Upshur. In the long-term, any potential uture streetcare route running along Georgia Avenue

would contribute to easier movement within and along the lengthy corridor and allow residents to move toward the central node/Metro or con-

venience goods. Current Metrobus service is adequate along Georgia Avenue. The addition o Smart Bike bicycle-sharing locations at the Metro

station and bus stops could be helpul in linking portions o this long commercial corridor with the others.

Retail Support

AsthecentralnodeisalreadyexperiencingredevelopmentduetothecatalyticaectofnewbuildingsandtenantsneartheMetrostation,retail

supportinthissubmarketshouldfocusonimprovingthequality,appearanceandfunctionalityoftheexistingretailinthenorthernandsouthern

nodes, rather than attempt to attract new retail to the area. Such a plan could be best coordinated by a local merchants association, eith the

support o both the Department o Small Local Business Development (DSLBD), restore DC, DC Main Streets (potentially) and neighboring How-

ardUniversity.Theareawouldbenettotheextentthatitcouldbebrandedasauniquecollectionofretailersnotfoundinothersectionsofthe

GeorgiaAvenuecorridor.ThiseortcouldbuildonstrengthentheproximityrelationshiptoHowardUniversitybyfocusingonAfrican-American

themed bookstores, academic goods and services, galleries and imported artwork and the presence o education and activism-oriented non-

protsandbusinesses(includingacoeehouse,barbershoporartgalleries).Retailmerchandisinginthisareashouldbesupportedwithinll

development that closes gaps in the pedestrian-oriented landscape. Because o the location near Howard University and the concentration o

institutional uses in this part o the corridor, a more ocused concept retail management approach celebrating the Arican American heritage o

Howard is suggested or this submarket.

Key Recommendations

Treat the Georgia Avenue Corridor as three separate nodes, each with a distinct strategy.

1.Createorsupportexistingmerchantassociationsthatwillfocusonleasingissuesandmerchandisingbynode.

2. Leverage Great Streets Initiative , Department o Housing and Community Development (DHCD), and reStore DC resources or streetscaping and

storefrontimprovementsbetweenretailnodestoenhancethequalityofexistingcommercialspacethatisnotlikelytoberedeveloped.

3. Market storeront commercial space along the corridor to ofce users (not retailers) in need o relatively low rents and able to unction outside

the central business district.

4.UpperGeorgiaAvenueNode:

a. Implement trafc calming at intersection with Kansas Avenue and Upshur Street to create a clear, sae northern edge to the commer

cial area.

b.Promoteinlldevelopmentthatclosesgapsinthepedestrian-orientedlandscape.

8/6/2019 OP Georgia Petworth Doc

http://slidepdf.com/reader/full/op-georgia-petworth-doc 40/40

c.Supportmixed-useredevelopmentoftheSafewayparcelthatbringsbuildingstothesidewalktoanimatethestreetscapeforpedestri

ans.

d.Attractsuccessfullocal,independentretailerstoprovidesuchneededservicesasrestaurants,tnesstraining,coeeshops,galleries

and bookstores, with combined use o retail space where possible to help incubate each use.

5.CentralGeorgiaAvenue(Metro)Node:Providezoningsupportforlarger-scaletransit-orienteddevelopmentwithmulti-familyresidentialinthenode surrounding the Georgia Avenue – Petworth Metro Station. This should ollow the Gerogia Avenue Petworth Metro Statio corridor Plan. The

Georgia Avenue Small Area Plan reviews orienting the area south o the Petworth Metro to TOD principles and creating a pedestrian/bike riendly

environment.

6. Lower Georgia Avenue Node:

a.Improvethequality,appearanceandfunctionalityoftheexistingretailasarststep,whilealsoseekingtoattractselectednewretail

usestotheareathatimprovethebusinessmix.

b.Providenecessarytechnicaland,asavailable,nancialsupporttoexistingmerchantsassociations,withthesupportofneighboringHoward University.

c.Completearetailrecruitment/managementanalysisbasedonexistingandpotentialnewretailusesthatwouldidentifythisareaand

determine how to attract a unique collection o retailers not ound in other sections o the Georgia Avenue corridor, such as the

Arican-American ocused businesses suggested near Howard University.

d.Promoteinlldevelopmentthatclosesgapsinthepedestrian-orientedlandscape.UsetheGeorgiaAvenueSmallAreaPlanguidelinesto

enhance pedestrian and bicycle inrastructure.