online onboarding metrics that matter: how do you measure up?

TRANSCRIPT

WWW.SIGNiX.COM

JOHN B. HARRISSVP, PRODUCT MANAGEMENT

ONLINE ONBOARDING

METRICS THAT MATTER:

How Do You Measure Up?

DARRIN COURTNEYRESEARCH DIRECTOR

#signixlearning

.

.

©2015. All Rights Reserved

AGENDA

• Client Preferences for Digital Transactions

• Advisor Needs for Onboarding Technologies

• Firm Adoption and Approaches to Onboarding

• E-Signatures As An Essential Foundation for Digital

Onboarding

• Discussion – Q & A

#signixlearning

3© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

ROADMAP TO PRESENTATION

Firm Adoption and

Approaches to

Onboarding

Client Preferences

for Digital

Interactions

Advisor Needs for

Onboarding

Technologies

#signixlearning

4© 2015 CEB. All Rights Reserved.

ACCESS REQUIREMENTS ARE CHANGING

Clients are looking for

enhancements to

traditional financial

benchmark reporting

and are looking for

mobile access

N = 420 (Global)

Source: CEB TowerGroup Wealth Management Client Experience Survey, 2013.

Ownership of Tablets and Smartphones

Percentage of Respondents, 2013

Financial Measurement Preferences

Percentage of High-Net-Worth Respondents, 2013

Source: CEB TowerGroup Research, Capgemini and RBC Wealth Management, “World Wealth Report: 2013”.

Have a tablet,

but no Smartphone

15%

Have a

Smartphone,

but no tablet

20%

Do not have a

Smartphone or

tablet

14%

Have both a

tablet and a

smartphone

51%

No strong

preference

42%

Strongly prefer

financial

benchmark

measurement

23%

Strongly prefer

financial and life

goals measurement

35%

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

5© 2015 CEB. All Rights Reserved.

HNW WEBSITE USAGE GROWING

Contrary to popular

belief, HNW clients are

more likely to use the

website, and more likely

to use it often, than are

their mass affluent

counterparts. 19%17% 17%

10%

15%

22%

15%13%

25%

16%18%

13%

>Weekly About weekly About monthly 3 to 5 times 1 to 2 times Never

2011

2013

30%41%

24%

53%

34%

13%

>6 Times 1-5 Times Never

Mass affluent HNW

Website Usage by Asset Segment

Percentage of HNW and Mass Affluent Respondents, 2013

Frequency of visiting primary wealth management firm’s website in the past 12

months

Percentage of HNW Respondents, 2011 and 2013

N = 376 (Mass Affluent) 139 (HNW)

Source: CEB TowerGroup Wealth Management Client Experience Survey, 2013.

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

6

N = 141 (United States)

Source: 2013 Client Experience Survey, CEB TowerGroup Research

Interactions every few months or more

Percent of clients by activity, 2013

18%

42%

25%

59%

25%

39% 40%

70%

18-37 38-46 47-57 58+

Visit Website Interact with Advisor

SILVERS HIGHEST, HAPPIEST WEBSITE USERS

HNWs over the age of 58

are most likely to visit

the website and interact

with their advisor at least

every few months.

© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

34%

52%

34%

60%

82%

54%

62%

81%

18-37 38-46 47-57 58+

Web Satisfaction Advisor Satisfaction

#signixlearning

7

0%

61%

41% 44%

53%

73%

Not at all Once a year Twice a year 3 to 5 times a year

About every couple of months

About once a month or more

Pe

rce

nt

Vis

itin

g W

eb

sit

eM

on

thly

or

Mo

re

Frequency of Advisor Contact

N = 141 (United States)

Source: 2013 Client Experience Survey, CEB TowerGroup Research

ADVISOR CONTACT AND FREQUENT WEB VISITS

UNCORRELATED Regardless of the

frequency of advisor

meetings, at least 40%

of respondents go

online at least monthly.

Frequent website usage versus advisor contact

Percentage of respondents, 2013

© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

100%

0%

#signixlearning

8

70%

60%

32%

21% 17%

11% 9%

1%

3%

1%

1%

Accessaccounts,

products, and services

Access news and insights on financialmarkets

Trade stocks, bonds, mutual funds, or other investments

Purchaseadditionalaccounts,

products, and services

Get help with a simple

question about personalfinances

Receiveassistance with an account or

productproblem

Obtain financial guidance

Mobile Device

Online

N = 139 (United States)

Source: 2013 Client Experience Survey, CEB TowerGroup Research

A majority of

respondents prefer to

use a portal for account

data and news and also

wish to process

transactions.

© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

CHANNEL PREFERENCES VARY BY ACTIVITY

Preferred Channel for Financial Activities

Percentage of respondents, 2013

#signixlearning

9© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

ROADMAP TO PRESENTATION

Firm Adoption and

Approaches to

Onboarding

Client Preferences for

Digital Interactions

Advisor Needs for

Onboarding

Technologies

#signixlearning

10

19%

1%

16%

58%

5%

20%

2%

25%

47%

5%

Yes, my advisorpresented information

to me on a laptopcomputer

Yes, my advisorpresented information

to me on a tabletcomputer

Yes, my advisorpresented informationto me using a desktop

No, my advisor did notpresent information to

me on a computer

Unsure

2011 2013

DIGITAL DOESN’T ALWAYS MEAN SELF SERVICE

Wealth firms will look to

make it easier for

advisors to utilize digital

presentations with

clients and thus make

them more industry

prevalent.

N = 1117; 28

Source: CEB TowerGroup Wealth Management Client Experience Surveys, 2011 and 2013.

2011: Quality of digital presentation

Percentage Respondents, 2011

2013: Quality of digital presentation

Percentage Respondents, 2013

Positive

77%

Negative

23%

Positive

91%

Negative

9%

In the last 12 months, has your primary wealth manager presented information to you

on a computer instead of paper during an in-person meeting?

Percentage of Respondents, 2013

© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

11© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

N = 55,854.

Source: CEB Information Risk Leadership Council End-User Awareness Survey, 2012.

BETTER TECHNOLOGY NEEDED FOR ALL ADVISORS

Wealth firms need to

provide advisors with

more effective

onboarding technology

solutions.

Effectiveness of Technology1

Mean Response of Respondents, 2012

Percentage of Employees Describing Themselves as Technology-Embracing

Percentage of Respondents, 2013

4.334.66 4.68 4.87 4.89

5.18 5.24 5.33

Mobile AdvisorTools

CustomerRelationshipManagement

DocumentManagementand Workflow

ClientReporting/Account

Aggregation

Client WebPortal

PortfolioManagement/

Recordkeeping

Research andAnalytics

FinancialPlanning

1Effectiveness scores were calculated by assigning the following numerical values to responses: 1 = Very ineffective, 2 = Ineffective, 3 =

Somewhat ineffective, 4 = Neither ineffective nor effective, 5 = Somewhat effective, 6 = Effective, 7 = Very effective.

N = 1004.

Source: CEB TowerGroup Wealth Management Advisor Benchmarking Survey, 2012.

85% 79% 73%56%

25-39 40-49 50-59 60+

#signixlearning

12© 2015 CEB. All Rights Reserved.

CLIENTS EXPECTING DIGITAL INTERACTIONS

More than 6 out of 10

Gen X/Y Clients believe

technology helps them

better collaborate with

their advisor.

Client Agreement with the Statement, “My Advisor and I Collaborate More

Effectively Through Technology,” by Age

Millionaire Investors, United States, 2012

Improving

client experience

27%

Enabling

employees

and improving

client experience

36%

Marketing

8%

Other

3%

Enabling

employees

26%

Mobility Strategy: Wealth Management Firms

Percentage of Respondents, 2012- 2013

33%

62%

Boomer/Retiree (48and Older)

Gen X/Y (47 andYounger)

Source: Fidelity Investments, Insights on Advice, 2012

N = 752

Source: CEB TowerGroup FSI Technology Survey, 2012-2013CEB TOWERGROUP WEALTH MANAGEMENT

#signixlearning

13© 2015 CEB. All Rights Reserved.

CLIENT FACING TOOLS TAKING ON IMPORTANCE

Different technologies

support different advisor

needs.

Areas Where Applications Help Advisors the Most

Percentage of Respondents, 2012

N = 709

Respondents permitted to select one or two choices

Source: CEB Wealth Management 2012 Advisor Benchmarking SurveyCEB TOWERGROUP WEALTH MANAGEMENT

Saves

Time

Improves

Sales

Process

Improves

Advice

Quality

Improves

Service

Quality

None of

the Above

CRM 9% 35% 6% 28% 22%

Financial Planning 1% 20% 53% 14% 13%

Portfolio Management &

Recordkeeping11% 9% 27% 33% 20%

Client Reporting & Account

Aggregation10% 12% 26% 34% 17%

Document Management &

Workflow42% 7% 6% 23% 23%

Mobile Advisor Tools 21% 8% 7% 20% 44%

Research & Analytics 3% 18% 49% 12% 18%

Client Web Portal 15% 8% 10% 39% 28%

#signixlearning

© 2015 CEB. All Rights Reserved. 14

14%

Not concerned at all that

robo-advisors will

negatively impacting

business

COMPETITION FROM NON-TRADITIONAL THREATS

Self-service tools and

online advisory services

put consumers in direct

control of achieving their

financial goals with

minimal advisor input.

Threat Posed by "Robo-Advisors“ Over Next Five Years

Percentage of Respondents, 2014

59%

Very concerned to somewhat

concerned that robo-advisors

will negatively impacting

business

28%

Slightly concerned that

robo-advisors will

negatively impacting

business

n = 22

Source: CEB Wealth Management Forum Polling, 2014.

CEB TOWERGROUP WEALTH MANAGEMENT#signixlearning

15© 2015 CEB. All Rights Reserved.

CEB TOWERGROUP WEALTH MANAGEMENT

ROADMAP TO PRESENTATION

Onboarding

Adoption and

Approaches at

Wealth Firms

Client Preferences for

Digital Interactions

Advisor Needs for

Onboarding

Technologies

#signixlearning

© 2015 CEB. All Rights Reserved. 16

A GOAL OF HOLISTIC ADVICE

Nearly two-thirds of

wealth executives report

building holistic advisory

relationships is critical to

their business

performance.

Wealth Management Firms Ranking Each as Very Important for Business

Performance in the Next 18 Months

Global, 2014

27%

34%

34%

36%

41%

57%

64%

64%

Managing organizational change effectively

Implementing goal-based planning strategies

Improving financial planning capabilities

Managing large-scale technology investments

Recruiting and hiring frontline staff

Coaching and training frontline staff

Improving clients’ perception of value of our advice

Building holistic advisory relationships with clients

N = 44

Source: CEB 2014 Advisory Experience Diagnostic

High-Net-Worth Client Preference for Personal Financial Guidance

Global, 2014

38%62%Advice about a specific,

immediate needAdvice to help you

better manage your

overall financial

situation

N = 593

Source: CEB 2014 Small Business Owner SurveyCEB TOWERGROUP WEALTH MANAGEMENT

#signixlearning

17© 2015 CEB. All Rights Reserved. © 2015 CEB. All Rights Reserved.

DIGITAL AND ONBOARDING ON THE RISE

TOP TWO areas that are most CRITICAL during the next 12 months

Percentage of Respondents, 2014

N =28

Source: CEB TowerGroup Technology Outlook Poll 2015

36%

32%

32%

25%

21%

18%

14%

11%

7%

4%

0%

0%

Preparing systems for upcoming regulatory deadlines

Applying technology to improve multi-channel (portal,mobile, branch, etc.) client engagement

Improving client onboarding from front to back office

Making goals-based planning and reporting the center ofyour value proposition

Integrating core advisor desktop components to increaseadvisor productivity

Assessing/defining strategies for core platform (trust,brokerage, etc.) conversion

Organizing data for actionable business analytics

Aggregating client data from inside and outside yourinstitution

Developing/enhancing the vendor oversight process

Developing a mobile technology solution/platform foradvisors

Adopting cloud technology and solutions

Enhancing social media compliance, engagement, andadoption

CEB TOWERGROUP WEALTH MANAGEMENT

Second only to regulatory

preparedness, onboarding

and collaboration

technologies are most

critical.

#signixlearning

© 2015 CEB. All Rights Reserved.

86%

75% 75%71%

57%54%

46%43%

64%

32%

21%

32%

18%

39%

25%

11%

Preparingsystems forupcomingregulatorydeadlines

Improvingclient

onboardingfrom front toback office

Organizingdata for

actionablebusinessanalytics

Applyingtechnology toimprove multi-

channel(portal, mobile,branch, etc.)

clientengagement

Aggregatingclient datafrom insideand outside

your institution

Making goals-based planningand reportingthe center ofyour valueproposition

Integratingcore advisor

desktopcomponents to

increaseadvisor

productivity

Developing amobile

technologysolution/

platform foradvisors

18

LARGEST GAPS SEEN IN DATA AND ONBOARDING

Priority versus Confidence Scores

“”High/Critical Importance” and “High/Complete Confidence” Responses, 2014Regulatory issues were

rated as most important,

with a modest majority of

executives having

confidence in execution,

as opposed to data and

onboarding-related

issues, which were also

important, but garnered

less confidence.

N = 28

Source: CEB TowerGroup Technology Outlook Poll 2015

CEB TOWERGROUP WEALTH MANAGEMENT#signixlearning

19© 2015 CEB. All Rights Reserved.

ONBOARDING RELATED TECH GAINS INVESTMENT

What are the TOP THREE areas of technology investment during the next 12 months

Percentage of Respondents, 2014BPM and ECM technologies have

risen steadily over the last few

years as areas of investment

0%

4%

4%

7%

7%

7%

11%

18%

21%

32%

36%

43%

54%

57%

Social Networking Technologies

Mutual Fund & Retirement Plan…

Cloud Solutions

Advisor Technology From…

Securities Processing

Outsourcing

Trust Accounting

Account Aggregation

Client Reporting

Advisor Desktop

Financial Planning

BPM & ECM

Portfolio Management/…

Customer Relationship…

N = 28

Source: CEB TowerGroup Wealth Management Agenda Poll 2014CEB TOWERGROUP WEALTH MANAGEMENT

#signixlearning

© 2015 CEB. All Rights Reserved. 20

BPM AND ECM AN AREA OF FOCUS

Most firms either have,

are adopting, or are

replacing existing BPM

and ECM Solutions.

13% 16%

31%

41%

Adopting Replacing Installed Unsure

17%14%

42%

27%

Adopting Replacing Installed Unsure

Current State of BPM

Percentage of respondents, 2014-2015

Current State of ECM

Percentage of respondents, 2015

n =199

Source: CEB FSI Technology Survey, 2014- 2015.

n =196

Source: CEB FSI Technology Survey, 2014- 2015.CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

© 2015 CEB. All Rights Reserved. 21

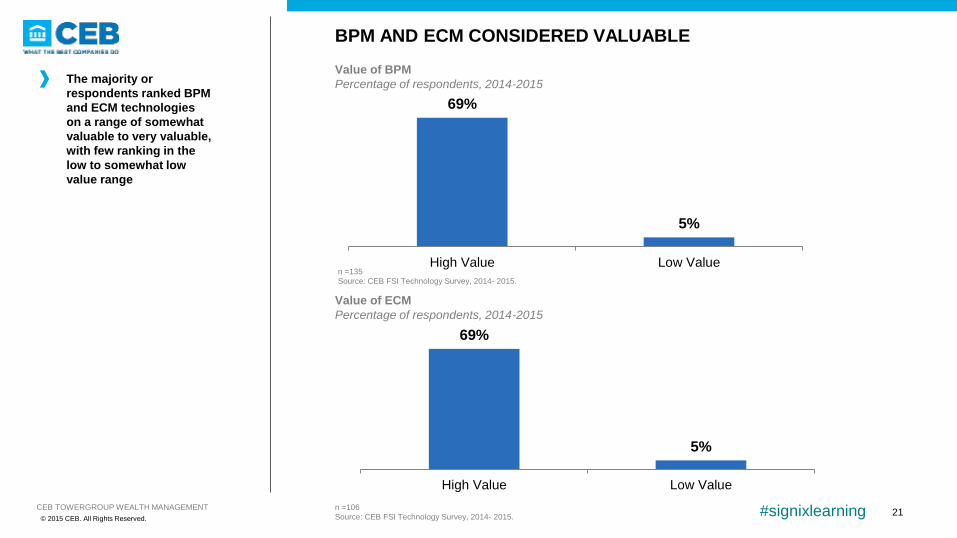

BPM AND ECM CONSIDERED VALUABLE

The majority or

respondents ranked BPM

and ECM technologies

on a range of somewhat

valuable to very valuable,

with few ranking in the

low to somewhat low

value range

69%

5%

High Value Low Value

69%

5%

High Value Low Value

n =135

Source: CEB FSI Technology Survey, 2014- 2015.

n =106

Source: CEB FSI Technology Survey, 2014- 2015.

Value of BPM

Percentage of respondents, 2014-2015

Value of ECM

Percentage of respondents, 2014-2015

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

© 2015 CEB. All Rights Reserved. 22

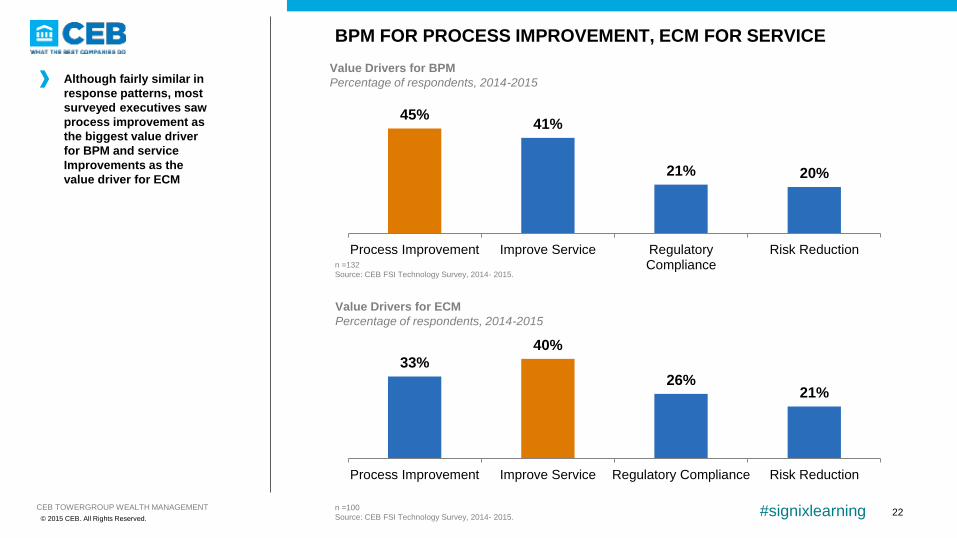

BPM FOR PROCESS IMPROVEMENT, ECM FOR SERVICE

Although fairly similar in

response patterns, most

surveyed executives saw

process improvement as

the biggest value driver

for BPM and service

Improvements as the

value driver for ECM

33%

40%

26%21%

Process Improvement Improve Service Regulatory Compliance Risk Reduction

45%41%

21% 20%

Process Improvement Improve Service RegulatoryCompliance

Risk Reductionn =132

Source: CEB FSI Technology Survey, 2014- 2015.

n =100

Source: CEB FSI Technology Survey, 2014- 2015.

Value Drivers for BPM

Percentage of respondents, 2014-2015

Value Drivers for ECM

Percentage of respondents, 2014-2015

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

© 2015 CEB. All Rights Reserved. 23

ONBOARDING TECH SEEN AS MODERATELY RISKY

Compared to other

technologies, BPM and

ECM are considered

moderate risk

technologies

37%

46%

14%

Low Risk Moderate Risk High Risk

32%

42%

22%

Low Risk Moderate Risk High Risk

n =100

Source: CEB FSI Technology Survey, 2014- 2015.

n =131

Source: CEB FSI Technology Survey, 2014- 2015.

Risk of BPM

Percentage of respondents, 2014-2015

Risk of ECM

Percentage of respondents, 2014-2015

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

© 2015 CEB. All Rights Reserved. 24

SCALABILITY IS THE GREATEST RISK

Although integration

difficulty, risk of

catastrophic failure and

information security fears

are all areas of concern,

most executives worry

about the ability of

onboarding solutions to

scale as volume demand

grows

43%

29%23% 22%

Scalability to Volume Information Security Catastrophic Failure Difficult Integrations

30%27%

23% 24%

Scalability to Volume Information Security Catastrophic Failure Difficult Integrations

Risk Factors for BPM

Percentage of respondents, 2014-2015

Risk Factors for ECM

Percentage of respondents, 2014-2015

n =127

Source: CEB FSI Technology Survey, 2014- 2015.

n =97

Source: CEB FSI Technology Survey, 2014- 2015.CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

© 2015 CEB. All Rights Reserved.

EXCELLENT ONBOARDING HELPS REFERRALS

Clients with favorable

ratings of initial

interactions are more

likely to recommend

their firm to others.

New Clients* Who Recommended Their Firm, by Rating of Initial Interactions

Past 12 Months, April 2011

33%

48%

63%

Fair to Good Very Good Excellent

Sample Average, 53%

N = 132Source: CEB 2011 High-Net Worth Client Experience Survey. * New Clients are defined as those with three years or less of advisor and firm tenure.

CEB TOWERGROUP WEALTH MANAGEMENT #signixlearning

26

Clients are not only looking for holistic advice, but they are also looking

to have digital interactions with their advisors and wealth firms using the

devices of their choosing.

Advisors see the value in onboarding technologies but aren’t receiving

the solutions they require to meet the demands of clients in an omni-

channel world.

Forward thinking firms will focus on ECM and BPM investments that not

only expedite the onboarding process and ongoing advisory experience

in a scalable way, but that do so on a platform that supports multiple

devices and channel preferences.

CONCLUSIONS

#signixlearning

.

.

©2015. All Rights Reserved

Designed for

Security

Sign Everywhere

Cost-Effective

True Partner Focus & Philosophy

Focused Features

Standards-based

Powerful Integration

Legal Evidence

Easy-to-Use

Delivering Independent eSignatures and Independence from Paper for over 12 years.

Vertical Expertise

Superior Pricing

Independent eSignatures™

WHO IS SIGNiX?Faster

Revenue Turnaround

Improved User

Experience

#signixlearning

.

.

©2015. All Rights Reserved

WHY USE E-SIGNATURES?

SpeedSign online,

anywhere, anytime = faster onboarding

No NIGOClients & advisors can’t finish signing

without filling mandatory fields.

LegalSEC/FINRA-compliant

signatures produce legally defensible proof of signing

CostNo more overnight deliveries, no staff opening envelopes

ExperienceNo obstacle

onboarding = happy clients, happy

employees.

#signixlearning

.

.

©2015. All Rights Reserved

INDEPENDENCE FROM PAPER = STREAMLINED PROCESS

Built-in online signatures as part of the client onboarding process

PROBLEM: Burdensome onboarding processSOLUTION: Integrated signing, eliminating NIGO

“Security and compliance are two driving concerns for our clients, and SIGNiX put those concerns to rest [with an] easy-to-use service…”

#signixlearning

.

.

©2015. All Rights Reserved

EASY FOR ADVISORS!

Who needs to sign?In what order?

What do they need to sign?

Where do they need to sign?

…and we do the rest!

#signixlearning

.

.

©2015. All Rights Reserved

INTEGRATION: DOCUPACE

#signixlearning

.

.

©2015. All Rights Reserved

SIGN EASILY ON SMARTPHONES

#signixlearning

.

.

©2015. All Rights Reserved

SIGN EASILY ON TABLETS

#signixlearning

.

.

©2015. All Rights Reserved

SIGN EASILY ON LARGE SCREENS

#signixlearning

.

.

©2015. All Rights Reserved

A TRUTH WE HOLD SELF-EVIDENT...

Buyer Beware – Not Every eSignature Is The Same.

#signixlearning

.

.

©2015. All Rights Reserved

INDEPENDENTeSIGNATURES™

DEPENDENTeSIGNATURES™

You own the signatures, docs & evidence. Vendor-linked signatures, docs & evidence.

#signixlearning

.

.

©2015. All Rights Reserved

SIGNiX = NO PEN (OR SERVICE) REQUIRED

#signixlearning

.

.

©2015. All Rights Reserved

PEACE OF MIND, DELIVERED

Signed PDF Document(s)

Each Independent eSignature™ Is:

• Verifiable off-line, without SIGNiX.com

• Based on open, published standards

• Tamper-Evident

• Linked to a snapshot of the document

.

.

©2015. All Rights Reserved

PEACE OF MIND, DELIVERED Signed PDF Document(s)

• Fully transparent signing process

• Rich metadata for each event

• Complete record of the transaction

• Consistent proof of intent to sign

TotalAudit™

TransactionalAudit Trail (XML, PDF)

TotalAudit™ Means Independent Evidence:

.

.

©2015. All Rights Reserved

MAKING YOUR SIGNATURES COUNT

PAPER DEPENDENT eSIGNATURES

OTHERE-SIGNATURE SERVICE

Independently verifiable, embedded signatures…

in wet ink.

TotalAudit™

Independently verifiable, transparent signatures & process…in digital form.

Future-proof.

Lightweight Audit Trail

OTHERE-SIGNATURE SERVICE

Signing process inside black box. Image of signatures linked to vendor

website. Subject to future link rot.

INDEPENDENT eSIGNATURES™

#signixlearning

.

.

©2015. All Rights Reserved

HOW MUCH MONEY COULD YOU SAVE?

Visit: http://www.signix.com/digital-signature-roi-worksheet

• Find out how much you're spending on paper processes

• Discover the ROI of digital signatures for your business

#signixlearning

.

.

©2015. All Rights Reserved

THANKS! CONTACTUSWe’re headquartered in charming Chattanooga, TN

Address1110 Market Street, Suite 402 Chattanooga, TN 37402

Phone423-305-7052

Email – John [email protected]

@signixsolutions

SIGNiXDigitalSignatures

DigitallySigned www.SIGNiX.com