on the calibration of the sabr–libor market model correlations · model of interest forward rates...

TRANSCRIPT

On the Calibration of the

SABR–Libor Market Model Correlations

Master’s Thesis

Dr. Elidon Dhamo

Christ Church College

University of Oxford

Submitted in Partial Fulfillment for the MSc in

Mathematical Finance

September 2011

To Migena ...

Abstract

This work is concerned with the SABR-LMM model. This is a term structuremodel of interest forward rates with stochastic volatility that is a naturalextension of both, the LIBOR market model (Brace-Gatarek-Musiela [1997])and the SABR stochastic volatility model of Hagan et al. [2002].

While the seminal approximation formula (developed by Hagan et al. [2002])to implied Black volatility using the SABR model parameters allows fora successful calibration of each forward rate dynamics to the volatilitysmile of the respective caplets/floorlets, an adequate calibration of the richcorrelation structure of SABR-LMM (correlations among the forward rates,the volatilities and the cross correlations) is a challenging topic and of greatinterest in practice. Although widely used for calibration, it is well knownthat swaptions’ volatilities carry only little information about correlationsamong the forward rates. As practically successful for the classical LMM,desirable would be to take the market swap rate correlations into account forthe model calibration.

In this study we develop a new approach of calibrating the model correlations,aiming at incorporating the market information about the forward rate corre-lations implied from more correlation-sensitive products such as CMS spreadderivatives, in which also swap rate correlations are involved. To this end wederive a displaced-diffusion model for the swap rate spreads with a SABRstochastic volatility. This we achieve by applying the Markovian projectiontechnique which approximates the dynamics of the basket of forward rates, interms of the terminal distribution, by a univariate displaced-diffusion. TheCMS spread derivatives can then be priced using the SABR formulas for theimplied volatility, taking the whole market smile of CMS spread options intoconsideration. For the ATM values in the payoff measure of the projectedSDE we use a standard smile-consistent replication of the necessary convexityadjustment with swaptions.

Numerical simulations conclude the work, giving a comparison between thismethod and the classical one of calibrating the model correlations to swaptionvolatilities. Furthermore, we study the performance of different parameteriza-tions of the correlation (sub-)matrices.

v

Acknowledgements

First of all, I would like to thank Dr. Christoph Reisinger for agreeing tosupervise this thesis, his support and his encouragements.

I would like to express my gratitude towards my former employer, d-fineGmbH, for offering me the opportunity to take part in the MathematicalFinance course at the University of Oxford, and for providing financial support.

Last but not least I am particularly indebted to my family for their understand-ing, their great moral support and their patience over the numerous weekendsI did not spend with them.

vii

Contents

Introduction 1

Chapter 1. Forward Libor and Swap Market Models 4

1.1 A Review of the Classical Libor and Swap Market Models . . . . . . 4

1.1.1 Libor Dynamics Under the Forward Measure . . . . . . . . . . 7

1.1.2 Valuation in LMM . . . . . . . . . . . . . . . . . . . . . . . . 8

1.1.3 Covariance and Correlations in LMM . . . . . . . . . . . . . . 9

1.1.4 Swap Rate Models and Measures . . . . . . . . . . . . . . . . 10

1.1.5 Incompatibility Between the LMM and the SMM . . . . . . . 11

1.2 The Convexity Adjustment and CMS Derivatives . . . . . . . . . . . 13

1.2.1 Constant Maturity Swaps and Related Derivatives . . . . . . . 14

1.2.2 Valuation of CMS Derivatives . . . . . . . . . . . . . . . . . . 16

1.3 Parameterization and Calibration . . . . . . . . . . . . . . . . . . . . 22

1.3.1 Parametric Forms of the Instantaneous Volatilities . . . . . . . 23

1.3.2 Calibration to the Cap/Floor Market . . . . . . . . . . . . . . 24

1.3.3 The Structure of Instantaneous Correlations . . . . . . . . . . 25

1.3.4 Calibration of LMM Correlations to Swaptions Volatilities . . 30

1.3.5 Calibration to Correlations Implied From CMS Spread Options 30

Chapter 2. The SABR Model of Forward Rates 32

2.1 General Model Dynamics . . . . . . . . . . . . . . . . . . . . . . . . . 32

2.1.1 The Time-Homogeneous Model . . . . . . . . . . . . . . . . . 34

2.1.2 Joint Dynamics of the SABR Forward Rates and Their Volatilities 35

2.2 Valuation in the SABR Model . . . . . . . . . . . . . . . . . . . . . . 36

Chapter 3. Pricing CMS Derivatives in SABR 37

3.1 The Markovian Projection Method . . . . . . . . . . . . . . . . . . . 37

3.2 A Displaced SABR Diffusion Model for CMS Derivatives . . . . . . . 38

3.2.1 Projection of CMS-Spreads to Displaced SABR Diffusion . . . 38

ix

Contents x

3.2.2 Pricing of CMS-Spread Options in a SABR Displaced DiffusionModel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Chapter 4. The SABR-LMM Model and Its Calibration 48

4.1 SABR–Consistent Extension of the LMM and Its Calibration . . . . . 48

4.2 Calibrating the Volatility Process . . . . . . . . . . . . . . . . . . . . 50

4.3 The SABR Correlation Structure . . . . . . . . . . . . . . . . . . . . 51

4.4 Calibration of the SABR–LMMCorrelations to Swaption Implied Volatil-ities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.5 Calibrating to Correlations Implied From CMS Spread Options . . . 55

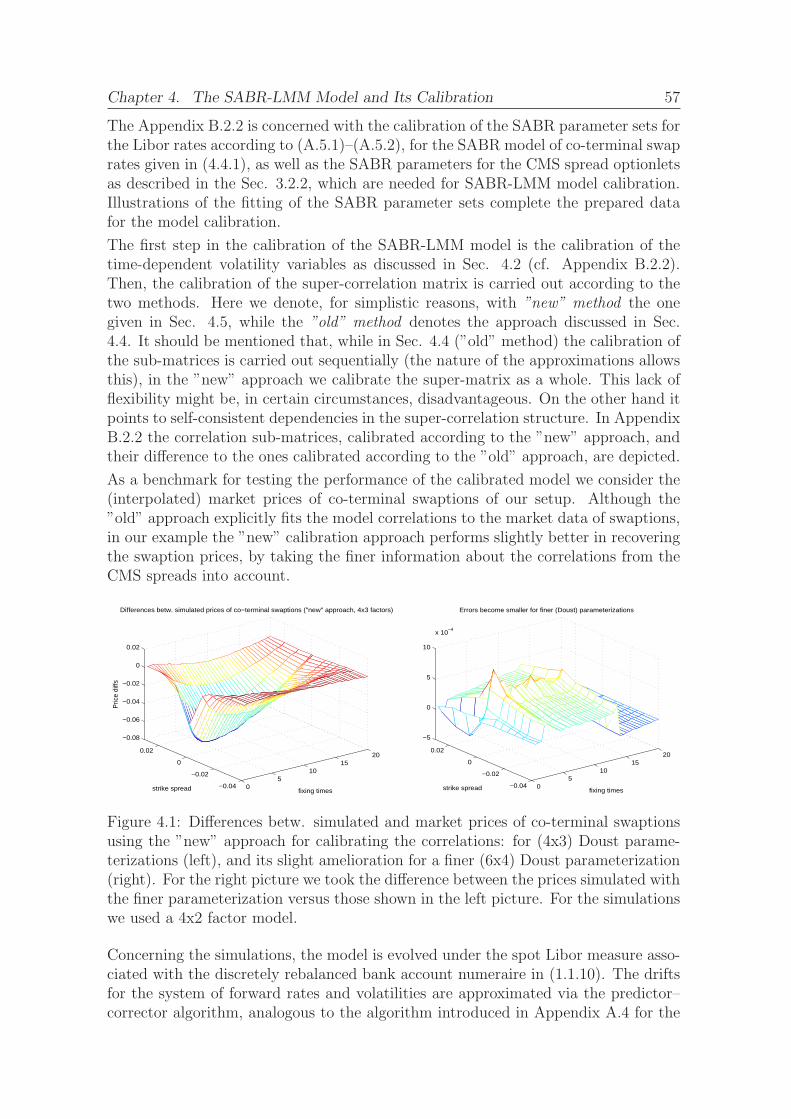

4.6 Numerical Simulations . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Chapter 5. Conclusion and Outlook 59

Appendix A. Classical Models and SABR-LMM 60

A.1 Valuation in LMM . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

A.2 Swap Rate Dynamics and the Choice of Numeraire . . . . . . . . . . 63

A.3 Valuation in the Log-Normal Swap Market Model . . . . . . . . . . . 64

A.4 Drift Approximation in LMM and Simulations . . . . . . . . . . . . . 65

A.5 SABR Implied Volatility . . . . . . . . . . . . . . . . . . . . . . . . . 66

Appendix B. Calibration Details 69

B.1 Bootstrapping the Market Data . . . . . . . . . . . . . . . . . . . . . 69

B.2 Parameterization of SABR–LMM and Its Calibration . . . . . . . . . 71

B.2.1 Parameterization of the SABR–LMM Model . . . . . . . . . . 71

B.2.2 Calibration Procedure . . . . . . . . . . . . . . . . . . . . . . 72

Bibliography 77

Introduction

While the Brace-Gatarek-Musiela (BGM) or Libor1 Market Model (LMM), based onthe assumption that forward term rates follow lognormal processes under their cor-responding forward measure, has established itself as a benchmark model for pricinginterest rate derivatives, it is less successful in recovering other essential characteris-tics of interest rate markets, particularly volatility skews and smiles. The presenceof these volatility skew and smiles in the market, however, indicates that a purelognormal forward rate dynamics is not appropriate.

In the last decade several extensions of the BGM model have been proposed, inwhich various versions of the volatility structures of forward Libor rates have beendesigned to match the observed volatility smile effects in the market. The set ofextensions covers local volatility, jump-diffusion and stochastic volatility models withand without time-dependent parameters. The calibration procedures in most of thesemodels are complicated and computationally expensive, and are performed on a best-fit basis.

One of the most successful and popular extensions of the LMM, the SABR2 model,models the forward rate process under its forward measure using a correlated log-normal stochastic volatility process. Its success is indebted to two main propertiesof the model: the crucial property of taking into account the quality of prediction ofthe future dynamics of the volatility smile, meeting the observations from the marketreality, and the seminal asymptotic expansion formula, developed by Hagan et al.[2002], to approximate the implied Black volatility using the SABR model parame-ters. Hence, prices of options, such as caps and floors, can be calculated using thewell known Black pricing framework but taking the volatility smile surface via theSABR parameters into account.

The SABR model and the LMM, although modeling the same assets, ”do not directlytalk to each other”3. The SABR does not link the snapshots of the caplet smiles intowell-defined joint dynamics. To overcome this Rebonato [2007] introduced a naturalextension of the LMM, the SABR-LMM, that recovers the SABR caplet prices almostexactly for all strikes and maturities. The dynamics of the volatility in this model ischosen so as to be consistent across expiries and to make the evolution of the impliedvolatilities as time-homogeneous as possible.

While the approximation to implied Black volatility using the SABR model parame-ters allows for a successful calibration of each forward rate dynamics to the volatility

1Libor = London Inter-Bank Offered Rates2Launched by Hagan et al. [2002]3Rebonato [2007]

1

Introduction 2

smile of the respective caplets and floorlets, an adequate calibration of the rich cor-relation structure of SABR-LMM (comprising correlations among the forward rates,the volatilities and the cross correlations) is a challenging topic and of great inter-est in practice. Although widely used for calibration, it is well known that swap-tion volatilities carry only little information about correlations among the forwardrates4. Facing the richness of the correlation structure of SABR-LMM, the needfor a calibration approach to more correlation-sensitive products is obvious and ofwide practical interest. As already successfully applied for the classical LMM5, it isdesirable to additionally take the swap rate correlations into account for the modelcalibration, which consistently are to be implied from the market prices of appropri-ate products. A broadly known and traded class of interest rate derivatives meetingthese requirements, particularly incorporating information about the swap rate cor-relations, is the one of Constant Maturity Swap (CMS) spread derivatives. Whilevaluation (in all the mentioned forward rate models) of these products is typicallydone straight-forwardly by Monte-Carlo simulation, the calibration of the models tothese products, by finding accurate and fast analytical approximations to reproducethe prices of these instruments, has been always subject to research6, even within thesimpler LMM framework7.

Scope of the Present Work and Contribution

In this work we develop a novel approach for the calibration of the rich correlationstructure in the SABR-LMM model of forward rates. Given the reasons above, ourscope is to extract the information about the forward rate correlations from themarket prices of correlation-sensitive derivatives, such as CMS spread options, andfit the model correlation parameters to those. To this end the derivation of analyticalpricing formulas for these products in the SABR framework is necessary.

The Markovian projection (MP) technique8 is an effective technique to volatilitycalibration that seeks to optimally approximate a complex underlying process witha simpler one, keeping essential properties of the initial process, and is, in principle,applicable to any diffusion model.

Starting with the SABR-LMM we apply the MP technique to the CMS spreads andderive a displaced–diffusion SABR model for the spread between the swap rates withdifferent maturities. To achieve this we adapt the recent work of Kienitz-Wittkey[2010], carried out in a SABR swap rate framework, to our SABR-LMM model.Consequently, we can price the CMS spread options in the resulting SABR swapspread model by making use of the seminal SABR formula of Hagan et al. [2002]. Inthis way we can calibrate the SABR swap spread model parameters to the marketimplied (normal) volatilities of the corresponding CMS spread options. For the ATM

4We refer at this point to the works of Alexander [2003], Brigo-Mercurio [2007], Rebonato[2002], Schoenmakers [2002, 2005], Schoenmakers-Coffey [2003].

5Borger-van Heys [2010].6Antonov-Arneguy [2009], Castagna-Mercurio-Tarenghi [2007], Lutz [2010], Kienitz-Wittkey

[2010], etc.7Belomestny-Kolodko-Schoenmakers [2010], Borger-van Heys [2010], etc.8MP has been introduced in this context by Piterbarg [2003, 2005a,b] and formalized in Piterbarg

[2007].

Introduction 3

values in the expiry forward measure of the projected SDE (i.e. expiry time of thecorresponding CMS spread option) we use a standard smile-consistent replication9 ofthe necessary convexity adjustment with swaptions. By this means we shall be able toimplicitly retrieve the important information about swap rate correlations containedin the market smile of CMS spread options and embed it into the SABR-LMM modelcorrelations.

This work is concluded with the numerical implementation of this new calibrationprocedure and some numerical simulations. We shall discuss different parameteri-zations of the sub-matrices of the model correlation matrix, in particular the Doustparameterizations, and study the performance of this calibration approach, in termsof pricing errors for swaptions, in comparison to the approach of calibrating the modelcorrelations to swaptions’ implied volatilities, given in Rebonato [2007].

The performed simulations shall also illustrate the effectiveness and robustness ofthis approach, and provide information about expected and possible drawbacks.

Outline

The thesis is organized as follows.

In the first chapter we review the classical forward LIBOR and swap rate marketmodels. Particular focus is set on the introduction of convexity and the differentapproaches to carry out the convexity correction. We incorporate these methods tothe pricing of CMS derivatives, in particular, the CMS caps and spread options. Wealso describe the calibration of LMM and introduce the different parameterizationsof the correlation matrix. At the end of the chapter a recent approach to implycorrelations from CMS spread options is presented.

The second chapter is devoted to introduction and general properties of the SABRmodel.

The application of the Markovian Projection (MP) method to the basket of forwardrates is carried out in the third chapter. Here we derive a displaced-diffusion modelfor the swap rate spread with a SABR stochastic volatility. For the pricing of CMSspread caplets in the payoff forward measure we use a smile-consistent replication ofthe convexity adjustment for the ATM spreads via swaptions, and apply the Haganet al. [2002] formulae.

The SABR-LMMmodel is introduced in the fourth chapter which is mainly concernedwith the parameterization and the calibration of the model. Two different approachesto correlation calibration are presented. Numerical simulations give a comparisonbetween the these approaches, taking different parameterizations of the sub-matricesof the correlation matrix into account.

We conclude the work by presenting a short summary of our analysis, and give anoutlook of possible future directions of the discussed topics.

9According to Hagan [2003].

Chapter 1

Forward Libor andSwap Market Models

1.1 A Review of the Classical Libor and Swap

Market Models

Over the past two decades the Brace-Gatarek-Musiela [1997] model (BGM) has es-tablished itself as a benchmark model for pricing and risk managing interest ratederivatives. It is based on the assumption that the forward rates follow lognormalprocesses with deterministic (time-dependent) volatilities under their correspond-ing measures, and it is widely known as the lognormal forward Libor Market Model(LMM). The popularity of this model is indebted to its compatibility with the seminalBlack model which establishes a direct relationship between caplets’ prices and local(implied) volatilities of forward rates and constitutes the standard market conventionfor quoting benchmark instruments.

While the LMM model has established a standard for incorporating all available at-the-money information, it is less successful in recovering other essential characteristicsof interest rate markets, particularly volatility skews and smiles1. Various extensionsof the LMM model, designed to incorporate skew and smile effects, have been pro-posed. The set of extensions covers local volatility, jump-diffusion and stochasticvolatility models with and without time-dependent parameters. In the next chap-ters we shall discuss one of the most successful extensions of the LMM, the SABRmodel, which enjoys increasing popularity among the practitioners and academicsalike, again due to its compatibility with the Black ’s framework.

Nevertheless, one of the biggest challenges in using these models is the calibrationof the forward rate correlations which are not covered by the caplets markets, butrather incorporated in other benchmark instruments, such as European swaptionsor CMS spread derivatives. While the valuation in all these forward rate models is

1The volatility tends to rise if the option is out of the money. This results in the so calledvolatility smile describing the fact that implied Black volatility is strike-dependent.

4

Chapter 1. Forward Libor and Swap Market Models 5

typically done straight-forwardly by Monte-Carlo simulation, calibration by findingaccurate and fast analytical approximations to prices of these benchmark instrumentshas always been subject to research.

In this chapter we briefly describe the construction of forward Libor models as givenin Brace-Gatarek-Musiela [1997] and Jamshidian [1997], whereby we follow theapproach proposed by Musiela-Rutkowski [2005]. Assuming, for the time being,that there are no smile effects present in the interest rate markets, the formal modelsetup we present here is based on assumptions made in Musiela-Rutkowski [2005].In the following sections we shall present some of the mostly used parameterizationsand calibration methods for the forward rate volatilities and their correlations, whichwill prepare the ground for introducing the SABR-LMM model in the next chaptersand its calibration approaches. We shall also briefly mention the lognormal swaprate model (SMM), putting emphasis on the incompatibility between the two models.Furthermore, a separate section is dedicated to the approximation and pricing of CMSderivatives via the convexity correction technique which paves the way to calibratingthe forward rate correlations to the prices of CMS spread derivatives.

Let T ∗ > 0 represent a fixed time horizon. Given a filtered probability space(

Ω, Ftt∈[0,T ∗],PT ∗)

which satisfies the basic assumptions made in Musiela-Rutkowski

[2005], let WT ∗

t t∈[0,T ∗] denote a d-dimensional standard Brownian motion (Wienerprocess) and assume that the filtration Ftt∈[0,T ∗] is the usual P

T ∗−augmentation of

the filtration generated by WT ∗

t (cf. Hunt-Kennedy [2004]).

In the given probability space an interest rate system formally consists of a systemof zero-coupon bonds B = B(t, T ) | 0 < t < T < T ∗ satisfying a set of stochasticdifferential equations (SDEs) and defined by the following assumptions:

• The system of zero-coupon bond prices B = B(t, T ) | 0 < t < T < T ∗ ismodeled as a strictly positive continuous semi-martingale under PT ∗

. A deter-ministic initial set of bond prices B(0, T ), T ∈ [0, T ∗], is exogenously givenand the bond price process satisfies the relationship B(t, T ) > B(t, S) for anyt ≤ T < S with B(t, T ) ≡ 1 for any t ≥ T.

• For any fixed T ∈ [0, T ∗) the forward rate process2

(1.1.1) F (t, T, T ∗) =B(t, T )− B(t, T ∗)

τB(t, T ∗), 0 < t < T, τ(T, T ∗) = T ∗−T,

is a strictly positive, continuous martingale under PT ∗

.

The equivalent martingale measure PT ∗

can be interpreted as the time T ∗-forwardmeasure and implies that the bond price dynamics is arbitrage-free.

It follows from the Martingale Representation Theorem (cf. Karatzas-Shreve [1991])that for every T ∈ [0, T ∗) the forward interest rate process F (t, T, T ∗) has the repre-sentation

(1.1.2) dF (t, T, T ∗) = F (t, T, T ∗)γ(t, T, T ∗) · dWT ∗

t , 0 ≤ t ≤ T,

2This definition is derived from the self-financing portfolio of zero bonds: at time t we sell B(t, T )

and buy B(t,T )B(t,T∗) ·B(t, T ∗) at total of zero, B(t, T )− B(t,T )

B(t,T∗) ·B(t, T ∗) = 0. This leads to the definition

of F (t, T, T ∗), satisfying 1+(T ∗−T )F (t, T, T ∗) = B(t,T )B(t,T∗) . The latter is the interest amount received

at time T ∗.

Chapter 1. Forward Libor and Swap Market Models 6

under PT ∗

, where WT ∗

t =(

W T ∗

t,1 , . . . ,WT ∗

t,d

)

is a Rd-valued (element-wise independent)

PT ∗

-Brownian motion and γ(t, T, T ∗) is a Rd-valued, Ft-adapted3 volatility process

satisfying the condition PT ∗

[

∫ T

0‖γ(u, T, T ∗)‖2d du < ∞

]

= 1.

Given these assumptions and the representation of the forward rate process (1.1.2),we can in principle construct an interest rate model with an exogenously specifiedvolatility structure process γ(t, T, T ∗).

The volatility structure γ(t, T, T ∗) might be, in general, a stochastic process. In thespecial case where γ(t, T, T ∗) is a deterministic, bounded, piecewise continuous func-tion, the forward Libor rate F (t, T, T ∗) is a lognormal martingale under its equivalentmartingale measure. The construction of a model of forward rates as presented byBrace-Gatarek-Musiela [1997] starts by postulating that the dynamics of the forwardrates F (t, T, T ∗) under the equivalent martingale measure P T ∗

are governed by thestochastic differential equation (1.1.2), where the deterministic volatility function isexogenously given. The model for the forward rates (1.1.2) is referred to in the liter-ature as BGM (Brace-Gatarek-Musiela) Model or the lognormal LiborMarket Model(LMM).

In practice, however, we do not model a continuum of forward rates with a fixedcompounding period τ but only a finite number of simple forward rates, which in thefollowing will be termed forward Libor rates.

Definition 1.1 (d-factor Libor Market Model). Let T0, . . . , TN be the set of ex-piries and B(t, T0), . . . , B(t, TN) the corresponding set of zero coupon bond prices.

Let d be the fixed number of independent driving Brownian motions in the model.For each i ∈ 0, . . . , N − 1 the d-factor Libor Market Model (LMM) assumes thefollowing GBM dynamics for forward rate Fi(t) := Fi(t, Ti, Ti+1), under its payoffmartingale measure P

i+1 := PTi+1:

(1.1.3) dFi(t) = Fi(t)γi(t) · dWi+1t , 0 ≤ t ≤ Ti,

where Wi+1t is a standard d-dimensional Brownian motion under the forward mea-

sure Pi+1, with d(W i+1

t,k ,W i+1t,l ) = δk,l dt, k, l ∈ 1, . . . , d (δk,l is the usual Kronecker

Delta). γi(t) is a deterministic vector process4 given by γi(t) = (σi,1(t), . . . , σi,d(t))T ,

with σi(t) := ‖γi(t)‖d.

Using the Ito’s lemma, the GBM equation (1.1.3) can be solved by

(1.1.4) Fi(t) = Fi(0) exp

(∫ t

0

γi(s) · dWi+1s ds− 1

2

∫ t

0

‖γi(s)‖2d ds)

, 0 ≤ t ≤ Ti.

The dynamics in (1.1.3) does not yet distinguish between the correlations and thevolatility of the forward rates. To make this clearer we re-formulate the equation(1.1.3) in the form (cf. Rebonato [1999a] for more details)

(1.1.5) dFi(t) = Fi(t)σi(t)bi(t) · dWi+1t ,

3The filtration Ft is consistently generated by WT∗

t .4The interpretation for γi(t) is that it contains the responsiveness of the i’th forward rate for d

different independent random shocks.

Chapter 1. Forward Libor and Swap Market Models 7

where bi(t) ∈ Sd ⊂ Rd (Sd the unit hypersphere in R

d) is given by

(1.1.6) bi,k(t) =σi,k(t)

‖γi(t)‖d,

d∑

k=1

b2i,k = 1.

In this way (1.1.5) formally separates the volatility σi of the forward rate Fi from thecorrelation structure ρ between the forward rates, which can be equivalently definedvia its pseudo square root b = b0, . . . ,bN−1, containing the vectors bi as columns:

(1.1.7) ρ(t) = b(t)⊥ b(t) =

(

γi(t) · γj(t)

‖γi(t)‖d‖γj(t)‖d

)

i,j

, 0 ≤ t ≤ minTi, Tj.

Rebonato [1999a] presented a significant and efficient way to reduce to a very largeextent the difficulties in the simultaneous calibration of the volatilities and the corre-lation matrix thanks to straightforward geometrical relationships and matrix theory.The notation so far with the introduction of loading vectors in (1.1.6) shall simplifythe understanding and the usage of these results.

Remark 1.2 Once the fixing time Ti is reached the forward rate becomes constant,which means that Fi(t) remains constant for all t ≥ Ti. Although obvious, let it bementioned that the instantaneous volatility function then satisfies

σi(t) = ‖γi(t)‖d ≡ 0, ∀ t ≥ Ti, i ∈ 1, . . . , N.

1.1.1 Libor Dynamics Under the Forward Measure

Of course, in order to use the LMM in practice the dynamics of all forward Liborrates have to be formulated in a single measure. In this respect convenient choicesare either the terminal measure PN which is induced by taking the terminal discountbond B(t, TN) as numeraire, or the spot measure which is defined by the numerairegiven in (1.1.10). As a consequence only one of the forward Libor rates is a martingaleand, according to Girsanov’s theorem, all other forward rate processes will have bemodified by additional drift terms (cf. Hunt-Kennedy [2004]).

In practice, the standard approaches to construct the system of forward Libor ratesrely either on the forward induction as in Brace-Gatarek-Musiela [1997] or on theso-called backward induction as in Musiela-Rutkowski [2005].

Concretely, under the measure Pk+1 the forward rate process Fj reads

(1.1.8) dFj(t) = µ(t, Tj, Tk) dt+ Fj(t)γj(t) · dWk+1t ,

where the drift term µ(t, Tj, Tk) is determined by requiring lack of arbitrage.

For 0 ≤ t ≤ Tj the drifts are given by (cf. Brace-Gatarek-Musiela [1997])(τi = Ti+1 − Ti):

(1.1.9) µ(t, Tj, Tk) = Fj(t) ·

−k∑

i=j+1

τiFi(t) σi(t)σj(t)ρi,j(t)

1+τiFi(t)for j < k

0 for j = kj∑

i=k+1

τiFi(t) σi(t)σj(t)ρi,j(t)

1+τiFi(t)for j > k.

Chapter 1. Forward Libor and Swap Market Models 8

The spot measure (cf. Jamshidian [1997]) is induced by the rolling bond numeraire5

Gt = B(t, Tξ(t))

ξ(t)−1∏

j=0

(1 + τjFj(t)),(1.1.10)

where the left-continuous function ξ : [0, TN ] → 1, . . . , N gives the next reset dateat time t:

(1.1.11) ξ(t) = inf

k ∈ N |T0 +k−1∑

i=0

τi ≥ t

= inf

k ∈ N |Tk ≥ t

.

The forward Libor process for Fj, j = 0, . . . , N − 1, is then given by

(1.1.12) dFj(t) = Fj(t)γj(t) · dW∗t + Fj(t)

j∑

i=ξ(t)

τiFi(t) σi(t)σj(t)ρi,j(t)

1 + τiFi(t)dt,

with W∗t denoting a standard Brownian motion under the spot measure P

∗.

We see that in the spot Libor measure Fj in (1.1.12) contains j− ξ(t)+1 drift terms,whereas in the terminal measure it contains N − j − 1 drift terms, cf. (1.1.9). Fornumerical reasons it is important to keep the calculation costs of the Libor drifts assmall as possible. Therefore, for products involving only short maturity Libors thedynamics in the spot Libor measure (1.1.12), involving repeatedly the rolling of thebond with the shortest time to maturity available, is preferable, whereas for longerdated products the representation in the terminal measure may be recommended.

In both cases the numeraire process remains alive throughout the time span of thetenor structure TnNn=0. This is particularly necessary for the evaluation of deriva-tive securities that involve random payoffs at any date in the tenor structure. Oursimulations in Sec. 4.6 are carried out by calculating the drifts with respect to thespot measure.

1.1.2 Valuation in LMM

The key advantage of LMM in regard to model calibration as well as to pricing of thefinancial interest rate products is its compatibility of the forward rates’ modeling tothe Black framework, due to the assumed lognormality of the forward rate dynamicsand, of course, to the assumed deterministic (time-dependent) volatility.

With regard to the scope of this work, we present in Appendix A.1 the valuationformulae of the basic benchmark instruments which will be used to calibrate theLMM and other models we will consider later in the next chapters.

The spectrum of interest rate products which can be priced with LMM is huge. Inpractice, a lot of products are being priced with LMM by taking into consideration

5Gt represents the wealth at the time t of a portfolio that starts at time 0 with one unit of cashinvested in a zero-coupon bond of maturity T0, and whose wealth is then reinvested at each timeTj in zero-coupon bonds maturing at the next date Tj+1, cf. Schoenmakers [2005]. The processGt is a continuous and completely determined by the Libors at the tenor dates, such that the spotmeasure P

∗ is then defined such that the relative bond prices B(t, Tj)/Gt, j = 1, . . . , N are localmartingales.

Chapter 1. Forward Libor and Swap Market Models 9

approximations. One family of popular approximations we shall discuss in detail inChap. 1.2.

Nevertheless, the main reason to develop a market model of forward rates is howeverto price exotic interest rate options, whose complex payoff can be expressed in termsof market observable Libor rates. In the most cases this is done by performingjoint Monte-Carlo simulations of the forward rates in a calibrated LMM. The jointdistributional evolution of the forward rates with respect to e.g. a payoff measure,though, results in solving a system of stochastic differential equations, as in (1.1.8)-(1.1.9), which involves state dependent drift terms. In Appendix A.4 we brieflypresent a standard method how to approximate the corresponding drifts in the jointevolution of forward rates.

1.1.3 Covariance and Correlations in LMM

In general, if one is interested in terminal correlations of forward rates at a futuretime instant (when pricing financial instruments with payoffs at future times), asimplied by the LMM model, then the computation has to be based on a MonteCarlo simulation technique. Following Brigo-Mercurio [2007], let us assume we areinterested in computing the terminal correlation between forward rates Fi and Fj attime Tk, k < i < j, say under the measure P

y, y > k. Then we need to compute theterminal covariance

Corry(Fi(Tk);Fj(Tk))(t)=E

yt

[

(Fi(Tk)− Eyt [Fi(Tk)]) (Fj(Tk)− E

yt [Fj(Tk)])

]

√

Eyt

[

(

Fi(Tk)− Eyt [Fi(Tk)]

)2]

Eyt

[

(

Fj(Tk)− Eyt [Fj(Tk)]

)2]

.

We notice that, while the instantaneous correlations do not depend on the partic-ular probability measure or numeraire under which we are working, the terminalcorrelations do.

Recalling the dynamics of Fi and Fj under Py, the expected values appearing in the

above expression can be obtained by simulating the above dynamics of Fi and Fj upto time Tk. Fortunately, there exist approximated formulas that allow us to deriveterminal correlations algebraically from the LMM parameters ρi,j(.) and σi(.). Bypartial freezing of the drift components in the log-normal dynamics of the forwardrates with respect to P

y, we can easily obtain (cf. Brigo-Mercurio [2007]):

Corry(Fi(Tk);Fj(Tk))(t) ≈exp

∫ Tk

tσi(s)σj(s)ρi,j(s) ds

− 1√

exp

∫ Tk

tσi(s)2 ds

− 1

√

exp

∫ Tk

tσj(s)2 ds

− 1

.

This approach makes the terminal correlations independent of the chosen probabil-ity measure. Notice that a first order expansion of the exponentials appearing inthe above formula yields a second formula for the terminal correlations (Rebonato[2004]):

(1.1.13) CorryRR(Fi(Tk);Fj(Tk))(t) =

∫ Tk

tσi(s)σj(s)ρi,j(s) ds

√

∫ Tk

tσi(s)2 ds

√

∫ Tk

tσj(s)2 ds

.

Chapter 1. Forward Libor and Swap Market Models 10

An immediate application of Schwartz’s inequality shows that terminal correlations,when computed via Rebonato’s formula, are always smaller, in absolute value, thaninstantaneous correlations. In agreement with this general observation, recall thatthrough a careful repartition of integrated volatilities (caplets) in instantaneous volatil-ities σi(t) and σj(t) we can make the terminal correlation Corry

RRarbitrarily close to

zero, even when the instantaneous correlation ρi,j is one.

1.1.4 Swap Rate Models and Measures

A probability measure Pm,n, induced by the annuity Bm,n(t) =

∑ni=m+1 τi−1B(t, Ti)

and equivalent to the measure PT ∗

, is said to be the forward swap probability mea-sure associated with the dates Tm and Tn, or simply the forward swap measure, iffor every i = 0, . . . , N the relative bond price B(t,Ti)

Bm,n(t), for all t ∈ [0, Ti ∧ Tm+1], fol-

lows a local martingale process under Pm,n. Thus, the forward swap rate Sm,n(t) =

B(t,Tm)−B(t,Tn)Bm,n(t)

, t ∈ [0, Tm], is a Pm,n-martingale (cf. Appendix A.2).

Definition 1.3 If the (vector-valued) volatility process t → γm,n(t) is a deterministicfunction we speak of a (lognormal) Swap Market Model (SMM) for Sm,n, assumingthat forward swap rates follow a lognormal diffusion process of type

(1.1.14) dSm,n(t) = Sm,n(t)γm,n(t) ·Wm,nt , 0 ≤ t ≤ Tm,

where Wm,n denotes the corresponding d-dimensional Brownian motion under Pm,n.

As the correlations between the forward swap rates will not be focused on in thissection, (1.1.14) can be alternatively expressed in an one-dimensional form6 as

(1.1.15) dSm,n(t) = Sm,n(t)σm,n(t)dWm,nt , 0 ≤ t ≤ Tm,

where σm,n(t) = ‖γm,n(t)‖d, and Wm,nt =

γm,n(t)

‖γm,n(t)‖d·Wm,n

t being an one-dimensional

Brownian motion under Pm,n.

As an important consequence, European options on swap contracts over [Tm, Tn],called swaptions, can be priced exactly with the Black-Scholes formula ( see AppendixA.3). Moreover, as we will show, there exist very accurate swaption approximationformulas for swaptions in the LMM.

While in the Libor model of forward rates there is only one degree of freedom forchoosing the numeraire, see (1.1.9)–(1.1.12), for swap market models in general thereare N degrees of freedom for a N+1 time grid. For instance, for a complete system ofstandard swaps it is possible to choose σ0,N , . . . , σN−1,N simultaneously deterministic(cf. discussions in Schoenmakers [2005]).

In Appendix A.2 we shall briefly present some of swap rate models mostly used inpractice: in particular, the co-terminal and the co-initial swap rate models. We referto Galluccio et al. [2006] for their extensive studies on these and further swap ratemodels and their adequateness in practice.

6We will consider the swap rate process Sm,n(t), if not otherwise explicitly specified, always inits ”natural” measure P

m,n.

Chapter 1. Forward Libor and Swap Market Models 11

1.1.5 Incompatibility Between the LMM and the SMM

The cap and swaption markets are underpinned by the same state variables, eitherforward rates or, equivalently, swap rates which can be transformed to each other bysimple bootstrapping methods. As a corollary, the instantaneous volatilities of for-ward rates and swaptions cannot be assigned independently. Once the instantaneousvolatilities of, and correlations among, forward rates are given, then the correlationsamong and volatilities of swap rates are completely specified (cf. Rebonato [1999b]).

It is market practice to price both sets of instruments (caps and swaptions) using theBlack [1976] formula which is inconsistent as lognormal forward and lognormal swaprate models are incompatible; if simple forward rates are lognormal, swap rates canonly be approximately so, and vice versa (cf. Brace [1997]). The Black model ceasesto be arbitrage–free when it is assumed that, at the same time, forward rates and swaprates are all lognormal. Further discussions about the effects of this incompatibilityin practice can be found in Rebonato [1999b], Brigo-Liinev [2005], Brigo-Mercurio[2007].

The next two paragraphs show how the two models interact with each other, andhow far they are compatible.

Swap rate dynamics under the forward measure. Following Brigo-Mercurio[2007], the dynamics of the forward swap rate Sm,n in the SMM model (cf. (1.1.14)),under the Libor forward measure numeraire B(t, Tm) is given (after lengthy calcula-tions) by

(1.1.16) dSm,n(t) = µmm,n(t)Sm,n(t)dt+ Sm,n(t)γm,n(t) ·Wm

t , 0 ≤ t ≤ Tm.

The drift is defined by(1.1.17)

µmm,n(t) =

n−1∑

i,j=m

νm,ni,j (t)τiτjB(t, Tm, Ti+1)B(t, Tm, Tj+1)ρi,j(t)σi(t)σj(t)Fi(t)Fj(t)

1− B(t, Tm, Tn),

where B(t, Tm, Tk) =B(t,Tk)B(t,Tm)

denotes the price of the zero-coupon bond at time t formaturity Tk, as seen from expiry Tm, hence the forward price of the zero bond fromTm to Tk as seen at time t.

The weights νm,ni,j are defined as

νm,ni,j (t) =

B(t, Tm, Tn)∑i

k=m+1 τk−1B(t, Tm, Tk) +∑n

k=i+1 τk−1B(t, Tm, Tk)(∑n

k=m+1 τk−1B(t, Tm, Tk))2

·n∑

k=j+1

τk−1B(t, Tm, Tk).

Forward rate dynamics under the annuity measure. Symmetrically, it is pos-sible to work out the dynamics of the forward Libor rates under the SMM numeraireBm,n. Applying the change-of-numeraire technique we have the following dynamics

Chapter 1. Forward Libor and Swap Market Models 12

for the forward rate Fi under Pm,n (cf. (1.1.15)):

(1.1.18) dFi(t) = σi(t)Fi(t) (µm,ni (t)dt+ Fi(t)σi(t)W

m,nt ) , 0 ≤ t ≤ Ti.

The drift is given by

(1.1.19) µm,ni (t) =

n∑

k=m+1

(

(2χk≤i − 1)

τk−1B(t, Tk)

Bm,n(t)

maxi,k−1∑

j=mini,k

τjFj(t)σj(t)ρi,j(t)

1 + τjFj(t)

.

The details of these derivations can be found in Brigo-Mercurio [2007].

Approximating the Swap Rate Volatility in LMM

The dynamics of swap rates in a Libor market model, as seen in (1.1.16), is rathercomplicated due to the stochastic factors involved in the drifts. Therefore, closedform pricing of swaptions in the LMM is in general not possible, nonetheless it ispossible to give surprisingly accurate swaption approximation formulas in LMM. Tothis end we write the swap rate again as a combination of forward rates and discountzero bonds (cf. (A.1.2))

(1.1.20) Sm,n(t) =

∑ni=m+1 τi−1B(t, Ti)Fi−1(t)

Bm,n(t)=

n−1∑

i=m

wm,ni (t)Fi(t), t ∈ [0, Tm],

with the stochastic weights wm,ni (t) = τiB(t,Ti+1)

Bm,n(t). The popular freezing of these weights,

which certainly simplifies the swap drifts in LMM, will also help us in approximatingthe swap rate variance in LMM.

Following Schoenmakers [2005], the swap rate variance σ2m,n(t) = ‖γm,n(t)‖2d may be

expressed in terms of the forward Libor volatilities by

(1.1.21) σm,n(t)2 =

1

S2m,n(t)

(

n−1∑

i=m

n−1∑

j=m

vm,ni (t)vm,n

j (t)Fi(t)Fj(t)γi(t) · γj(t)

)

,

with some weights vm,ni (t) whose distance to the swap weights wm,n

i (t) is given via

(1.1.22) vm,ni (t)− wm,n

i (t) = τiBi,n(t)

Bm,n(t)

S0m,n(t)− S0

i,n(t)

1 + τiFi(t)=: ym,n

i (t),

where m ≤ i < n and S0i,n denotes a system of virtual swap rates over a period [Ti, Tn]

defined as (see Schoenmakers [2005] for the details of derivation)

S0i,n(t) =

B(t, Ti)−B(t, Tn)

Bm,n(t)∑n−1

k=minl|m+l≥i wm,nk (t)

.

The terms ym,ni (t) have magnitudes comparable with differences of swap rates, hence,

they are usually rather small. They are zero when S0i,n(t) = S0

m,n(t) for m < i < n.

Chapter 1. Forward Libor and Swap Market Models 13

For example, this is the case for standard swaptions when the yield curve is flat (seealso Rebonato-Jaeckel [2003]). Integrating (1.1.21) over time to expiry we obtain(1.1.23)

1

Tm − t

∫ Tm

t

σm,n(s)2ds =

n−1∑

i,j=m

∫ Tm

t

vm,ni (s)vm,n

j (s)Fi(s)Fj(s)

S2m,n(s)

γi(s) · γj(s) ds.

We now note that the (stochastic) fractions in the r.h.s. of (1.1.23) add up to ap-proximately one and thus may be regarded as weights, tend to vary relatively slowin practice and therefore may be approximated by their values at t. Under this addi-tional assumption instantaneous swap volatilities may be considered as deterministic(though model inconsistent). This technique of ”freezing” all weights and forwardrates in (1.1.23) to their initial value leads to Rebonato’s formula (Rebonato [2002]):(1.1.24)

1

Tm − t

∫ Tm

t

σm,n(s)2ds =

n−1∑

i,j=m

vm,ni (t)vm,n

j (t)Fi(t)Fj(t)

S2m,n(t)

∫ Tm

t

γi(s) · γj(s) ds,

with vm,ni (t) = τiB(t,Ti+1)

Bm,n(t)+ ym,n

i (t). This formula can be used to calibrate of the model

parameters to implied swaption volatilities according to (A.3.3).

1.2 The Convexity Adjustment and CMS Deriva-

tives

In finance convexity is a broadly understood and non-specific term for nonlinear be-havior of the price of an instrument as a function of evolving markets. Such convexbehaviors manifest themselves as convexity corrections/adjustments to various pop-ular interest rate derivatives. From the perspective of financial modeling they ariseas the results of valuation done under the wrong martingale measure.

Practitioners use various ad hoc rules to calculate convexity corrections for differentproducts, often based on Taylor approximations (cf. Hunt-Pelsser [1998], Benhamou[2000], etc). However, Pelsser [2003] is the first to put convexity correction on afirm mathematical basis by showing that it can be interpreted as the side-effect of achange of numeraire. It can be understood as the expected value of an interest rateunder a different probability measure than its own martingale measure.

The well known Change of Numeraire Theorem, due to Geman et al. [1995], showshow in an arbitrage-free economy an expectation under a probability measure P

N ,generated by the numeraire N, can be represented as an expectation under a probabil-ity measure PM , generated by the numeraire M, times the Radon-Nikodym derivativedPN/dPM . For an expectation at time 0 of a random variable H at time T we have

(1.2.1) EN[

H(T )]

= EM

[

H(T )N(T )M(0)

N(0)M(T )

]

.

Following Pelsser [2003], suppose we are given a forward interest rate F (t, T, T ∗) withmaturity T < T ∗ and a numeraire B(t, T ∗) such that the forward rate is a martingale

Chapter 1. Forward Libor and Swap Market Models 14

under the associated probability measure PT ∗

. Now assume we have a contract wherethe interest rate F (T, T, T ∗) is observed at T but paid at a later date S ≥ T. At timeT the discounted interest payment is given by V (T ) = B(T, S)F (T, T, T ∗) and in P

S

(1.2.2) V (0) = B(0, S)ES0

[

F (T, T, T ∗)]

follows. However, under the measure PS the process F (t, T, T ∗) is in general not a

martingale such that the expectation (1.2.2) can be expressed as F (0, T, T ∗) timesa correction term. This correction term is known in the market as the convexitycorrection or convexity adjustment. Applying the change of numeraire technique(1.2.1) we can express (1.2.2) in terms of ET ∗

as follows

ES0

[

F (T, T, T ∗)]

= ET ∗

0

[

F (T, T, T ∗)dPS

dPT ∗

]

= ET ∗

0

[

F (T, T, T ∗)B(T, S)B(0, T ∗)

B(0, S)B(T, T ∗)

]

= ET ∗

0

[

F (T, T, T ∗)R(T )]

,

where R denotes the Radon-Nikodym derivative which is also a martingale underthe measure P

T ∗

. If we know the joint probability distribution of F (T, T, T ∗) andR(T ) the expectation can be calculated explicitly and we obtain an expression forthe convexity correction.

Only for very special cases exact expressions for the convexity correction can beobtained. In these special cases the Radon-Nikodym derivative of the change of mea-sure is equal to (a simple function of) the interest rate that determines the payoff. Aprominent example where an exact expression for the convexity correction is possibleis a Libor in Arrears contract, in which the payment is in arrears, i.e. at fixing time.Thus, we have for the Radon-Nikodym derivative dPT/dPT ∗

we have

(1.2.3)dPT

dPT ∗=

B(T, T )B(0, T ∗)

B(0, T )B(T, T ∗)=

1 + τF (T, T, T ∗)

1 + τF (0, T, T ∗), τ = T ∗ − T,

and hence,

ET0

[

F (T, T, T ∗)]

= F (0, T, T ∗)1 + τF (0, T, T ∗)e

∫ T

0σT (s)2ds

1 + τF (0, T, T ∗).(1.2.4)

1.2.1 Constant Maturity Swaps and Related Derivatives

The acronym CMS stands for constant maturity swap, and it refers to a swap ratewith a pre-defined length which fixes in the future. CMS rates provide a convenientalternative to Libor as a floating index, as they allow market participants to expresstheir views on the future levels of long term rates (for example, the 10 year swaprate). There are a variety of CMS based instruments, the simplest of them beingCMS swaps and CMS caps / floors.

A particularly known type of exotic European interest rate contract is a (fixed forfloating) CMS swap. This is a swap where at every payment date a payment calcu-lated from a swap rate is exchanged for a fixed rate. The floating leg pays periodicallya swap rate of fixed length (say, the 10 year swap rate) which fixes at the beginningof the accrual period.

Chapter 1. Forward Libor and Swap Market Models 15

A CMS cap or floor is a basket of calls or puts on a swap rate of fixed tenor (say, 10years) structured in analogy to a Libor cap or floor, cf. Sec. A.1. For example, a 5year cap on 10 year CMS struck at K is a basket of CMS caplets over 5 years, eachof which pays max(10 year CMS rate−K; 0), where the CMS rate fixes at the startof each accrual period.

Needless to say, a plethora of more sophisticated contracts are traded in the mar-kets, which may differ from the standard ones by differences in fixing and paymentfrequencies, whether the floating leg fixes in arrears or in advance, whether the termand payment frequency of the swap rate may be different from the specifications ofthe CMS swap itself and further market particularities. Moreover, the contracts canconsist of even more complicated formulas involving algebraic expressions of CMSrates of different lengths.

CMS Swaps

As mentioned above the floating payments of a CMS swap are not based on theLibor forward rates but on some swap rate. Formally, at the settlement dates Ti+1,i ∈ 0, . . . , N −m− 17, the fixed payment K is exchanged for the variable paymentSi,i+m(Ti) for a preassigned length m ≥ 1. Let us consider one CMS swaplet only,paying at Ti+1 and based on a notional of 1. The discounted payment on the fixedleg as of t is obviously given by B(t, Ti+1)τiK, while for the floating leg

(1.2.5) CMS(t, Ti,m) = B(t, Ti+1)τiEi+1t

[

Si,i+m(Ti)]

holds. Ei+1t denotes the expectation at time t with respect to the forward measure

Pi+1.

For a fixed natural number n ≤ N −m and k ∈ 0, . . . , N −m− 1, we denote withCMS(t, Tk,m, n), a n–period (forward starting) CMS swap rate which is defined by

K = CMS(t, Tk,m, n) =

∑n−1i=k CMS(t, Ti,m)

Bk,n(t).(1.2.6)

CMS Caps/Floors

The CMS caplets and CMS floorlets are built up analogously to their classical pen-dants, i.e. the interest rate caplets and floorlets. We can write

CMSCPL(t, Tk,m, κ) = B(t, Tk+1)τkEk+1t

[

(

Sk,k+m(Tk)− κ)+]

,(1.2.7)

CMSFLL(t, Tk,m, κ) = B(t, Tk+1)τkEk+1t

[

(

κ− Sk,k+m(Tk))+]

,(1.2.8)

where κ is obviously the optionlet strike. Not surprisingly, this implies a put-callparity relation for the CMS rate:

(1.2.9) CMSCPL(t, Tk,m, κ)−CMSFLL(t, Tk,m, κ) = CMS(t, Tk,m)− κ.

7We are assuming that the total time horizon in our economy is up to TN .

Chapter 1. Forward Libor and Swap Market Models 16

Analogously to the classical ones (Sec. A.1), for CMS caps (for CMS floors analo-gously) we have

CMSCAP(t, Tk,m, n, κ) =n−1∑

i=k

CMSCPL(t, Ti,m, κ).(1.2.10)

CMS Spread Options

A holder of a CMS spread option(let) has the right to exchange for one period of timethe difference between two CMS rates minus a spread κ. Hence, the payoff at expirytime Tk equals(1.2.11)

CMSSPO(Tk, Tk, n1, n2, κ) := τk

(

a1ωSk,k+n1(Tk) + a2ωSk,k+n2

(Tk)− ωκ)+

,

n1 6= n2, k + ni < N, a1, a2 ∈ R, ω ∈ −1, 1. A CMS spread option(let) can beseen as a special case of a CMS basket option(let). A generic CMS basket option(let),written on M CMS rates that reset at the option’s expiry date Tk, has the payoff

(1.2.12) CMSSPOB(Tk, Tk, miMi=1, κ) := τk

(

M∑

i=1

ωaiSk,k+mi(Tk)− ωκ

)+

,

where ai ∈ R denote weights and mi, i = 1, . . . ,M, (k + mi < N) are preassignedlengths of reference swaps.

A natural step further, far beyond the scope of this work, though, is to considercaps/floors of CMS spreads or even CMS basket options with periodic expiries/fixingswhose payoff at every fixing/expiry time Tk reads as in (1.2.12).

1.2.2 Valuation of CMS Derivatives

We now come to the point where we can examine the pricing of CMS productswe introduced previously. The most common characteristic of these products withrespect to pricing is that their payoffs are functions of one or more CMS ratesf(Si,i+m1

, Si,i+m2, . . .), which are usually fixed at Ti and paid at Ti+1. As we know

the swap rate Si,i+m(t) is a martingale with respect to the measure Pi,i+m, induced

by the annuity Bi,i+m(t). The forward measure Pi+1, associated with the payment

date Ti+1, is not its natural measure, i.e. Si,i+m(t) is not a martingale w.r.t. Pi+1.

Turning back to the CMS swaplet (1.2.5), by using the change of numeraire technique(1.2.1), we can write for i = 0, . . . , N −m− 1:

Ei+1t

[

Si,i+m(Ti)]

=Bi,i+m(t)

B(t, Ti+1)E

i,i+mt

[

Si,i+m(Ti)B(Ti, Ti+1)

Bi,i+m(Ti)

]

.(1.2.13)

They are basically two ways how to deal with the expectation: either find a lognormalapproximation for the CMS rate in the forward measure, by approximating the Libordrifts, or a convexity correction approach shall be applied by expressing the Radon-Nikodym derivative as a (simple) function of the interest rate that determines thepayoff, as, for instance, in the case of the Libor in Arrears in the LMM (cf. (1.2.3)).

Chapter 1. Forward Libor and Swap Market Models 17

In this section we want to discuss some of the methods used in the practice to ap-proximate (1.2.13). The first method exploits the idea of making the Radon-Nikodymderivative a function of the payout rate.

Approximating the Radon-Nikodym Derivative and the Convexity Cor-rection

For evaluating (1.2.13) we here recall the convexity approach in Pelsser [2003], basedon the assumption of a lognormal SMM, cf. Hunt-Kennedy [2004]:

B(Ti, Ti+1)

Bi,i+m(Ti)≈ a+ bi+1Si,i+m(Ti),(1.2.14)

where a and bi+1 are constants which are determined as follows. As the Radon-Nikodym derivative is a martingale w.r.t. to the annuity measure, by taking theexpectation we obtain

B(t, Ti+1)

Bi,i+m(t)= E

i,i+mt

[

B(Ti, Ti+1)

Bi,i+m(Ti)

]

= a+ bi+1Si,i+m(t).

Hence,

(1.2.15) bi+1 =1

Si,i+m(t)

(

B(t, Ti+1)

Bi,i+m(t)− a

)

.

On the other hand we have by summing up

1 =i+m−1∑

k=i

τkB(t, Tk+1)

Bi,i+m(t)=

i+m−1∑

k=i

τk (a+ bk+1Si,i+m(t)) .

Replacing bi+1 by (1.2.15),

a =1

∑i+m−1k=i τk

, bi+1 =Bi+1(t)− Bi,i+m(t)

∑i+m−1k=i

τk

Bi(t)−Bi+m(t)(1.2.16)

hold. Finally, we can rewrite (1.2.13) as

(1.2.17) Ei+1t

[

Si,i+m(Ti)]

= Si,i+m(t)

(

1 +bi+1Var

i,i+m[Si,i+m(Ti)]

Si,i+m(t)(a+ bi+1Si,i+m(t))

)

.

The linear approximation in (1.2.14) does seem very crude at first, but can be justifiedby the following argument (cf. Pelsser [2003]). Convexity corrections only becomesizable for large maturities. However, for large maturities the term structure almostmoves in parallel. Hence, a change in the level of the long end of the curve is welldescribed by the swap rate. Furthermore, for parallel moves in the curve, the ratioB(Ti, Ti+1)/Bi,i+m(Ti) is closely approximated by a linear function of the swap rate,which is exactly what the approach does. This leads to a good approximation of theconvexity correction for long maturities.

With these formulas we can easily price linear CMS products like in (1.2.5) – (1.2.6).

Chapter 1. Forward Libor and Swap Market Models 18

In his seminal work Hagan [2003] discusses general approximations of functionalform to the Radon-Nikodym derivative given through (1.2.13). He writes for theCMS caplets:

CMSCPL(t, Ti,m, κ) = B(t, Ti+1)τiEi,i+mt

[

(

Si,i+m(Ti)− κ)+B(Ti, Ti+1)/Bi,i+m(Ti)

B(t, Ti+1)/Bi,i+m(t)

]

= B(t, Ti+1)τiEi,i+mt

[

(

Si,i+m(Ti)− κ)+]

+ B(t, Ti+1)τiEi,i+mt

[

(

Si,i+m(Ti)− κ)+(

B(Ti, Ti+1)/Bi,i+m(Ti)

B(t, Ti+1)/Bi,i+m(t)− 1

)]

.

The first term is exactly the price of a European swaption (cf. (A.3.2)) with notionalB(t, Ti+1)/Bi,i+m(t), regardless of how the swap rate is modeled. The last term is theconvexity correction. Following the argumentation in Hagan [2003], since Si,i+m is a

martingale in the annuity measure andB(Ti,Ti+1)/Bi,i+m(Ti)

B(t,Ti+1)/Bi,i+m(t)− 1 is zero on average, this

term goes to zero linearly with the variance of the swap rate, and is much smallerthan the first term. Giving the ratio a general form

(1.2.18) B(Ti, Ti+1)/Bi,i+m(Ti) = G(Si,i+m(Ti)),

for some function G, we then have

CMSCPL(t, Ti,m, κ) = B(t, Ti+1)τiEi,i+mt

[

(

Si,i+m(Ti)− κ)+]

+ B(t, Ti+1)τiEi,i+mt

[

(

Si,i+m(Ti)− κ)+(

G(Si,i+m(Ti))

G(Si,i+m(t))− 1

)]

.

Using the general property for smooth functions f with f(κ) = 0 (integration byparts):

(1.2.19) f ′(κ)(

S − κ)+

+

∫ ∞

κ

(

S − x)+

f ′′(x) dx =

f(S) for S > κ0 for S < κ,

and choosing

(1.2.20) f(x) =(

x− κ)

(

G(x)

G(Si,i+m(t))− 1

)

,

we obtain by simple transformations

CMSCPL(t, Ti,m, κ) = τiB(t, Ti+1)

Bi,i+m(t)

[

1 + f ′(κ)]

PSWO(t, Ti, Ti+m, κ)

+

∫ ∞

κ

PSWO(t, Ti, Ti+m, x)f′′(x) dx

.(1.2.21)

This formula replicates the value of the CMS caplet in terms of European swaptionsat different strikes It takes into account the presence of a market smile, incorporatingconsistently the information coming from the quoted swaption Black -volatilities. Werefer to Mercurio-Pallavicini [2006] for discussions about the approximation of the

Chapter 1. Forward Libor and Swap Market Models 19

integral above on a practically plausible, in general not negligible, strike interval[0, K], with K ”large enough”. We will come back to this approximation of theconvexity adjustment when considering the SABR model.

The formula for CMS floorlets (1.2.8) is a slight adaption of (1.2.21), replacingPSWO with RSWO (cf. (A.3.4)):

CMSFLL(t, Ti,m, κ) = τiB(t, Ti+1)

Bi,i+m(t)

[

1 + f ′(κ)]

RSWO(t, Ti, Ti+m, κ)

−∫ κ

−∞RSWO(t, Ti, Ti+m, x)f

′′(x) dx

.(1.2.22)

The value of the CMS swaplet is easily derived from the CMS put-call parity (1.2.9).

The method of replicating the CMS caplets/floorlets by means of swaptions is opaqueand computationally intensive. Hagan [2003] gives simpler approximate formulas forthe convexity correction, as an alternative to the replication method. Expanding atfirst order the function G around Si,i+m(t) makes f quadratic

(1.2.23) f(x) ≈ G′(Si,i+m(t))

G(Si,i+m(t))(x− Si,i+m(t))(x− κ),

and f ′′(x) constant. Together with the equality

∫ ∞

κ

PSWO(t, Ti, Ti+m, x) dx = Bi,i+m(t)Ei,i+mt

[

∫ ∞

κ

(

Si,i+m(Ti)− x)+

dx

]

=1

2Bi,i+m(t)E

i,i+mt

[

(

Si,i+m(Ti)− κ)+)2]

,

we have, by considering (Si,i+m(Ti)− κ)(Si,i+m(Ti)− κ)+ =(

Si,i+m(Ti)− κ)+)2,

CMSCPL(t, Ti,m, κ) = τiB(t, Ti+1)

Bi,i+m(t)PSWO(t, Ti, Ti+m, κ)

+τiG′(Si,i+m(t))Bi,i+m(t)E

i,i+mt

[

(Si,i+m(Ti)− Si,i+m(t))(Si,i+m(Ti)− κ)+]

,

CMSFLL(t, Ti,m, κ) = τiB(t, Ti+1)

Bi,i+m(t)RSWO(t, Ti, Ti+m, κ)

−τiG′(Si,i+m(t))Bi,i+m(t)E

i,i+mt

[

(Si,i+m(t)− Si,i+m(Ti))(κ− Si,i+m(Ti))+]

.

For a CMS swaplet,

CMS(t, Ti,m) = τiB(t, Ti+1)Si,i+m(t)(1.2.24)

+τiG′(Si,i+m(t))Bi,i+m(t)E

i,i+mt

[

(Si,i+m(Ti)− Si,i+m(t))2]

holds. The SMM (cf. Hunt-Kennedy [2004]) gives

Ei,i+mt

[

(Si,i+m(Ti)− Si,i+m(t))2]

= Si,i+m(t)2[

e∫ Tit σ2

i,i+m(s)ds − 1]

.(1.2.25)

Chapter 1. Forward Libor and Swap Market Models 20

Given that G(Si,i+m(t)) approximates the ratio B(t, Ti+1)/Bi,i+m(t) (cf. (1.2.18))linear as in (1.2.14)), the equation (1.2.24) perfectly matches with (1.2.17).

Hagan [2003] suggests to use for CMS swaps the volatility of at-the-money swaptions,since the expected value includes high and low strike swaptions equally. For out-of-the-money CMS caplets and floorlets, the strike-specific volatility should be used,while for in-the-money options, the largest contributions come from swap rates nearthe mean value. Accordingly, call-put-parity should be used to evaluate in-the-moneycaplets and floorlets as a CMS swap payment plus an out-of-the-money CMS floorletor caplet.

The function G has been considered a general smooth and slowly varying function,regardless of the model used to obtain it. Hagan [2003] develops simpler approximateformulas for the convexity correction, by specifying G. We shall present here themarket standard method for computing convexity corrections which uses bond mathapproximations and goes as follows. Let the yield curve be flat, fixed at a level y.Then, given an equidistant time grid with step size ∆T and discrete discounting, wecan write

Bi,i+m(t) =i+m∑

k=i+1

τk−1B(t, Tk) =i+m∑

k=i+1

∆TB(t, Ti+1)

(1 + ∆Ty)k−i−1.

The standard formula for the geometric sum gives then

Bi,i+m(t) =B(t, Ti+1)

Si,i+m(t)

[

(1 + ∆TSi,i+m(t))−1

(1 + ∆TSi,i+m(t))m−1

]

,

where the par swap rate y = Si,i+m(t) was taken as discount rate, since it representsthe average rate over the life of the reference swap. Thus,

(1.2.26) Gstd(Si,i+m(t)) =Si,i+m(t)

(1 + ∆TSi,i+m(t))− 1(1+∆TSi,i+m(t))m−1

.

A more accurate lognormal approximation of the swap rates and their correlations inthe forward measure was introduced by Belomestny-Kolodko-Schoenmakers [2010],based on the method of freezing the weights (as in Section 1.1.5) but assuming amore sophisticated approximation.

The approximation (1.2.17) is model independent and quite accurate especially forflat yield curves and highly correlated rates. Such constraints are not necessarilyunrealistic, since adjustments are mostly relevant for long maturities (and tenors),where (forward) rates tend to be constant and to move in parallel fashion.

Assuming lognormal-type dynamics for the swap rates as in SMM we obtain theclassical Black-like adjustment with at-the-money implied volatilities given through(1.2.24)–(1.2.26).

Pricing CMS Spread Options

Once more than one CMS rate is part of a payoff, as in case of CMS spread options,the correlation between the CMS rates in the forward measure starts playing animportant role in pricing these products.

Chapter 1. Forward Libor and Swap Market Models 21

Let us first focus on CMS spread option(let)s with zero strike whose payoff at expirytime Ti equals (cf. (1.2.11))

(1.2.27) CMSSPO(Ti, Ti, n1, n2, 0) := τi

(

Si,i+n1(Ti)− Si,i+n2

(Ti))+

.

The arbitrage-free value of the payoff (1.2.27) at time t is given by

(1.2.28) CMSSPO(t, Ti, n1, n2, 0) := τiB(t, Ti)Eit

[(

Si,i+n1(Ti)− Si,i+n2

(Ti))+]

,

which can be calculated as soon as we know the joint distribution of the pair of swaprates Si,i+n1

and Si,i+n2under the forward measure P

i.

Apart from the fact that the expectation is taken in the non-natural forward mea-sure, this payoff is the one of an exchange option. Therefore, the simplest valuationprocedure is based on assuming that the logarithms of the swap rates are jointly nor-mally distributed as in the Black-Scholes model of two underlying assets. A formaljustification of this approach is given by resorting to the SMM (cf. Def. 1.3) andsuitable approximations. Thus, let assume that both swap rates evolve according to

dSi,i+n1= µi,i+n1

(t)Si,i+n1dt+ σi,i+n1

Si,i+n1dW i

t(1.2.29)

dSi,i+n2= µi,i+n2

(t)Si,i+n2dt+ σi,i+n2

Si,i+n2dW i

t ,(1.2.30)

where W it and W i

t are Brownian motions under Pi, correlated via d(W it , W

it ) = ρ(t)dt,

with ρ(t) assumed to be given (estimated historically or approximated, for instance,as in Belomestny-Kolodko-Schoenmakers [2010]. The drifts µi,i+n1

and µi,i+n2of the

corresponding swap rates with respect to Pi are motivated by (1.1.17) and assumed

to be frozen or deterministic.

The formula for pricing exchange options, developed by Margrabe [1978] using thechange of numeraire technique, can now be applied to obtain:(1.2.31)

Eit

[(

Si,i+n1(Ti)− Si,i+n2

(Ti))+]

= BS

(

Eit[Si,i+n1

(Ti)],Eit[Si,i+n2

(Ti)], σ√

Ti − t, 1)

.

With the swap rate dynamics given in (1.2.29)–(1.2.30) we obtain explicitly:

Eit[Si,i+nk

(Ti)] = Si,i+nk(t)e

∫ Tit µi,i+nk

(s)ds, k = 1, 2,

and

(1.2.32) σ2 =1

Ti − t

∫ Ti

t

(

σ2i,i+n1

(s) + σ2i,i+n2

(s)− 2ρ(s) σi,i+n1(s)σi,i+n2

(s))

ds.

There are several ways how to approximate drifts deterministically under Pi, for

instance:

• they can be inferred from the convexity adjustments, i.e. from the approxima-tions to E

it

[

Si,i+nk(Ti)

]

, k = 1, 2 (discussed in the previous section). We notethat the convexity adjustment technique does not give the correlation betweenthe swap rates w.r.t. Pi;

Chapter 1. Forward Libor and Swap Market Models 22

• the classical method of ”freezing the coefficients” can be applied to (1.1.17),to make the P

i-dynamics of the swap rates lognormal, i.e. Eit

[

Si,i+nk(Ti)

]

=

Si,i+nk(t)eµ

ii,i+nk

(t)(Ti−t), with µii,i+nk

(t) given in (1.1.17);

• complex lognormal approximations, as in Belomestny-Kolodko-Schoenmakers[2010] for instance, can be applied to the swap rates under Pi.

Assuming the dynamics (1.2.29)–(1.2.30) with drifts µii,i+nk

(t), k = 1, 2, and the cor-relation ρ(t) between the two swap rates frozen at evaluation time t, Brigo-Mercurio[2007] gives a formula for the more general case of a time Ti payoff (1.2.11) with astrike κ 6= 0:

(1.2.33) Eit

[(

aωSi,i+n1(Ti) + bωSi,i+n2

(Ti)− ωκ)+]

=

∫ +∞

−∞

1√2π

e−12v2f(v) dv,

where

f(v) = aωSi,i+n1(t) exp

(

µii,i+n1

(t)− 1

2ρ(t)2σ2

i,i+n1(t)

)

τ + ρ(t)σi,i+n1(t)

√τv

× Φ

ωln

aSi,i+n1(t)

h(v)+[

µi,i+n1(t) + (1

2− ρ(t)2)σ2

i,i+n1(t)]

τ + ρ(t)σi,i+n1(t)

√τv

σi,i+n1(t)

√τ√

1− ρ(t)2

− ωh(v)Φ

ωln

aSi,i+n1(t)

h(v)+[

µi,i+n1(t)− 1

2σ2i,i+n1

(t)]

τ + ρ(t)σi,i+n1(t)

√τv

σi,i+n1(t)

√τ√

1− ρ(t)2

,

h(v) = κ− bSi,i+n2(t)e(µi,i+n2

(t)− 12σ2i,i+n2

(t))τ+σi,i+n2(t)

√τv, τ = Ti − t.

A straight-forward calculation shows that for κ = 0 the equation (1.2.31) is recovered.

By no log-normality of the swap rates, an analytical solution for the case κ 6= 0 isonly feasible if the spread is modeled as a normal distributed random variable:

(1.2.34) Si,i+n1(t)− Si,i+n2

(t) = S(t) with dS(t) = σdW (t).

This framework is too simple to consistently price CMS spread options since implicitlya perfect correlation is assumed. And it is also not taking into account the smileand the skew effects. The market quotes spread options by their implied normalvolatilities, similar to swaptions which are quoted by their implied Black volatility.

1.3 Parameterization and Calibration

The general form of the forward Libor model (cf. Def. 1.1) is merely a frameworkwhich becomes a model once the forward volatility structure γi(t), i ∈ 0, . . . , N−1,is specified, which determines both the level of the forward rates and the correlationbetween the forward rates via

ρi,j(t) =γi(t) · γj(t)

‖γi(t)‖‖γj(t)‖, 0 ≤ t ≤ minTi, Tj.

Chapter 1. Forward Libor and Swap Market Models 23

The selected covariance structure should match the observable dynamics of the Liborrates, such as the number and the shape of the underlying principal components, cf.Rebonato [2002]. Once the forward volatility structure is specified, the chosen modelis calibrated to the current forward rate curve and to liquid market instruments.

Since the current (at t0) forward rates Fi(t0) are initial conditions, and hence inputsfor the forward LMM, the calibration to the current forward rate curve is automatic.Calibration to cap and European swaption prices is achieved by choosing the for-ward volatility structure such that the model prices of these derivatives match theirmarket prices as closely as possible. As shown in (A.1.3)–(A.1.7), the lognormal as-sumption in the forward Libor model allows for the pricing of caplets by the ”marketconvention” Black-Scholes formula, and, as we will see, it enables the derivation ofgood closed-form approximations of European swaption prices, which then leads toefficient calibration of the model correlations to swaption market prices.

Nevertheless, with regard to the valuation of correlation-sensitive products such asCMS spread options, the calibration of instantaneous Libor correlation has alwaysbeen a challenging point of the LMM which has not been satisfactorily fulfilled bythe classical way of approximating the swap rate implied volatilities.

At the end of this section we shall present two approaches to calibrate the LMMcorrelations:

• by approximating the swap rate volatilities implied from the swaption quotes,Sec. 1.3.4;

• by approximating the swap rate correlations implied from the prices of CMSspread options, Sec. 1.3.5.

1.3.1 Parametric Forms of the Instantaneous Volatilities

Driven by empirical observations many authors and practitioners put special emphasisto the desideratum that the term structure of instantaneous volatilities should evolvein a time–homogeneous manner, assuming ”by default” that it is desirable for ainstantaneous volatility function to be able to reproduce (at least approximately) thecurrent term structure of volatilities in the future (cf. Rebonato [2002]). As a resultthe instantaneous volatility function should be modeled not as a function of calendartime, but rather as a function of left time to maturity σi(t) = g(Ti−t). It is importantto point out that the result does not depend on the details of the functional form ofthe instantaneous volatility function; the future smile surface will exactly ”look like”today’s smile surface. Apart from the time-homogeneity, Rebonato [1998, 1999a]states that the volatility function should have a flexible functional form to be ableto reproduce either a humped or a monotonically decreasing instantaneous volatility,and allow for an easy analytical integration of its square (facilitating the evaluationof the necessary variance and covariance elements). Rebonato suggests in his worksthe following parametric form:

(1.3.1) g(Ti − t) = [a+ b(Ti − t)]exp−c(Ti − t)+ d, c, d > 0, a+ d > 0,

which fulfills these criteria to an acceptable degree (see Rebonato [2002] for examplesand further explanations).

Chapter 1. Forward Libor and Swap Market Models 24

(1.3.1) can be extended to a richer parametric form; the extended linear-exponentialvolatility model (cf. Rebonato [2002], Brigo-Capitani-Mercurio [2003]):

(1.3.2) gext(Ti − t) = kig(Ti − t), k(Ti) > 0.

Rebonato [2002] models the vector k ∈ RN as ki = 1 + ǫ(Ti), being ideally close to

one and flexible enough to allow for a better fit of volatility function to the marketimplied volatilities of different maturities.

Assuming no smile and skews in the caplet markets, any choice of the parametersa, b, c, d will only approximately satisfy the ATM caplet condition,

(1.3.3) (σBlack

i )2 (Ti − t) =

∫ Ti

t

g(u)2 du,

across all forward rates8. The parameters ki then allow for the Libor rate specificadjustment to exactly fit the market implied volatility:

(1.3.4) k2i =

(σBlack

i )2 (Ti − t)∫ Ti

tg(u)2 du

.

The caplet condition (1.3.3) is then fulfilled by construction everywhere along thecurve.

A good and extensive overview of the volatility parameterizations used in practicecan be found in Brigo-Mercurio [2007].

1.3.2 Calibration to the Cap/Floor Market

The market convention to quote caps and floors is to use the (implied) Black- volatilitywhich plugged into the Black formula gives the market price of the cap/floor. In asmile-less world, we know from the Black-Scholes theory that for the instantaneousvolatility function σi(t) of a forward rate Fi(t) in the lognormal LMM the impliedBlack volatility σBlack

i is given by (cf. (A.1.4)),

(1.3.5) (σBlack

i )2 (Ti − t) =

∫ Ti

t

σi(u)2 du.

Ideally, in case of given market prices of ATM caplets, their implied Black volatilityconstitutes the right value to fit with the model volatility parameters.

The market prices are unfortunately a bit more involved. The market quotes flatvolatilities for caps of different maturities, T and strikes, K. Thus, an implied volatil-ity surface σBlack

cap(T,K) is quoted at any point in time. So what are the implied

volatilities of the caplets that make up the caps with different strikes and maturi-ties that are consistent with the quoted cap volatility surface? Alexander [2003]gives a brief and good overview about the particularities in stripping the informationout of cap market prices. For instance, each fixed strike caplet in a cap with the

8Depending on the calibration target one can choose the model volatility parameters to meetcondition (1.3.3) even not (only) for ATM Black volatilities.

Chapter 1. Forward Libor and Swap Market Models 25

ATM strike K has a different moneyness. Each Ti maturing caplet is assumed to beATM if Fi(Ti) = K, but since each caplet has a different underlying forward rate, itwill have a different ATM strike. So the different caplets in an ATM cap are onlyapproximately ATM. One of the popular iterative methods, used to back out thesecaplet volatilities from the cap market implied volatility surface, is the vega-weightedinterpolation technique, for which we refer to Alexander [2003].

Several stripping algorithms9 to extracting caplet volatilities out of quoted cap volatil-ities are presented in detail in the technical work by Hagan-Konikov [2004].

Finally, in a smile-less world, the calibration to caplets’ and floorlets’ implied volatil-ities (once extracted from the market quotes of caps and floors) for the LMM model isstraight-forward via (1.3.5), and the correlations between forward Libor rates have noimpact on the cap/floor prices. The application of the calibration requirement (1.3.5)to the volatility parameterizations given above is straight-forward as well. Therefore,in the sequel we will focus on the parameterization given in (1.3.2)–(1.3.4). The firststep in the calibration procedure is to find the solution parameters a, b, c, d for theminimizing problem(1.3.6)

mina,b,c,d

N−1∑

i=0

[

σBlack

i

√

(Ti − t)−√

∫ Ti

t

[

[a+ b(Ti − t)]exp−c(Ti − t)+ d]2

du

]2

.

Additionally, the free Libor rate specific parameters ki in (1.3.4) can be used toexactly fit the respective (ATM) Black caplet volatilities.

1.3.3 The Structure of Instantaneous Correlations

As discussed in Sec. 1.1.3, both, the instantaneous volatility formulation as well asthe chosen instantaneous correlation, can contribute to terminal correlations. Thequalities and properties an instantaneous correlation matrix ρ associated with a LMMshould have are (cf. Brigo-Mercurio [2007]):

• Symmetry and ones on the diagonal:

ρi,j = ρj,i, ρi,i = 1, for all i, j ∈ 0, . . . , N − 110;

• ρi,j ≥ 0 for all i, j, and the map i 7→ ρi,j has to be decreasing for i ≥ j,thus, moving away from the diagonal along a column or row the entries becomemonotonically decreasing as joint movements of far away rates are less correlatedthan movements of the rates with close maturity;

• When moving along the yield curve, the larger the tenor, the more correlatedthe adjacent forward rates are. Hence, the sub-diagonals, i 7→ ρi+p,i, will beincreasing for a fixed p.

9The idea behind the boot-stripping algorithms is that if we know, for instance, the 1 and 2 yearflat volatilities we know the 1 year and 2 year cap prices. Their price difference is by no arbitragearguments the second caplet in 2 year cap contract. It is thus required to solve a volatility thatimplies this caplet price. The same procedure is continued iteratively further.

10For ease of notation we will be numbering the elements of the correlation matrix by beginningwith zero, ρ = ρi,jN−1

i,j=0, coinciding with the numbering of the forward rates and their expiries.

Chapter 1. Forward Libor and Swap Market Models 26

A variety of parameterization functions have been introduced over the past years thatallow for expressing a given correlation matrix of forward rates in a functional form.There are several advantages to this: of course, it is computationally convenientto work with an analytical formula. But also noise, such as bid-ask spreads, andilliquidity are removed by focusing on general properties of correlation. Furthermore,the rank and the positive semi-definiteness of the correlation matrix can be controlledthrough the functional form.

The parameterizations we shall present here are full-rank parameterizations. Wewill also discuss how to reduce their rank depending on the number of underlyingBrownian motions of the model. One property that is implicitly present in all pa-rameterizations is the desirable time-homogeneity of the correlations.

Full-rank correlation parameterization

In general, the full instantaneous correlation matrix is characterized by N(N − 1)/2entries, given the symmetry and the ones on the diagonal. This number of entriesmay be too high for practical purposes, thus, a parsimonious parametric form withreduced number of parameters has to be found. In the literature a vast number ofcorrelation parameterizations is presented; to be mentioned here are the works ofSchoenmakers-Coffey [2003], Wu-Zhang [2003], Morini-Webber [2006], and latelythe papers of Borger-van Heys [2010] and Lutz [2010].

We will focus in the sequel on some of the parameterizations which will be used inour model calibration later on.

Three-parameters full-rank exponential parameterization. For 0 ≤ t ≤minTi, Tj Rebonato [2004] proposed a parameterization of the form

(1.3.7) ρi,j(ρ∞, α, β; t) = ρ∞ + (1− ρ∞) exp[

− |Ti − Tj|(β − αmaxi, j)]

,

which fulfils the desirable properties given above. Thus, it may produce for a giventenor structure realistic market correlations for properly chosen ρ∞ ∈ (−1, 1), β > 0and (small) 0 ≤ α ≤ β/(N − 1) (cf. Rebonato [1999a]). A slight modification of(1.3.7), also given in Rebonato [2004], reads:

(1.3.8) ρi,j(ρ∞, α, β; t) = ρ∞ + (1− ρ∞) exp[

− β|Ti − Tj| exp

−αmaxi, j

]

,

with ρ∞ ∈ (−1, 1), β > 0 and α ∈ R.

A special case of (1.3.7) is the Rebonato’s two-parameters full-rank exponential pa-rameterization:

(1.3.9) ρi,j(ρ∞, β; t) = ρ∞ + (1− ρ∞) exp[

− β|Ti − Tj|]

, β > 0, ρ∞ ∈ (−1, 1).

However, it should be noted that for a particular choice of parameters it is not directlyguaranteed that (1.3.7) or (1.3.8) defines valid correlation structure indeed (it mightviolate the positive semi-definiteness of the correlation matrix). The special case withρ∞ = 1 (cf. Rebonato [2002]),

(1.3.10) ρi,j(β; t) = exp[

− β|Ti − Tj|]

, t ∈ [0, Ti ∧ Tj],

Chapter 1. Forward Libor and Swap Market Models 27

assures a symmetric correlation matrix with positive eigenvalues. This parameteri-zation is analytically very attractive and fulfills the basic modeling requirements.

Apart from their parameter poorness which might turn out to be a handicap whenfitting to market quotes, these parameterizations do not distinguish on the distancebetween two different forward rates such that different pairs of forward rates with thesame distance to each other are correlated to the same degree. Since an unconstrainedoptimization is preferable to a constrained one, Schoenmakers-Coffey [2003] param-eterizations might be preferred from this point of view. Nonetheless, the Rebonato’sparameterizations are widely used in practice because of their analytical tractabilityand the easy calibration.