ohlone college 2019-2020 tentative budget · ohlone college 2019-2020 tentative budget ... stock...

TRANSCRIPT

OHLONE COLLEGE 2019-2020

TENTATIVE BUDGET

Presented to the Board of Trustees June 12, 2019

2

Agenda

• State Budget Update

• Community Colleges Proposals

• Ohlone College Tentative Budget

• CCC Sound Fiscal Management Self Assessment Checklist

• Q&A

State Budget Process

January Release of

Governor’s Budget

Jan thru May Legislature Budget

Subcommittee Hearings

May Governor’s May

Revisions

By June 15 Legislature agrees

on a Final State Budget Bill

By June 30 Governor acts on

State Budget

3

State Economic Outlook

• Economic growth expected to slow down

• California remained the 5th largest economy in 2018

• Main risks to outlook include: Stock Market Correction

Global Slow-down

Natural Disasters

Aging Population

Increasing Consumer debt level

• Emphasizes the need for fiscal prudence 4

State Budget Priorities Include:

• Building Rainy Day Reserves • Education • Early Childhood Education • Paying Down Debt/Liabilities • Housing Affordability • Earned Income Tax Credit • Fighting Homelessness

5

California State Budget Proposition 98 Funding

$49.7 $47.3

$58.1 $59.0

$67.1 $69.1 $71.6

$75.5 $78.1

$81.1

$45.0

$50.0

$55.0

$60.0

$65.0

$70.0

$75.0

$80.0

$85.0

Dol

lars

in B

illion

Community Colleges will receive 10.93% of total Prop 98 Funding 6

Community College Proposals

8

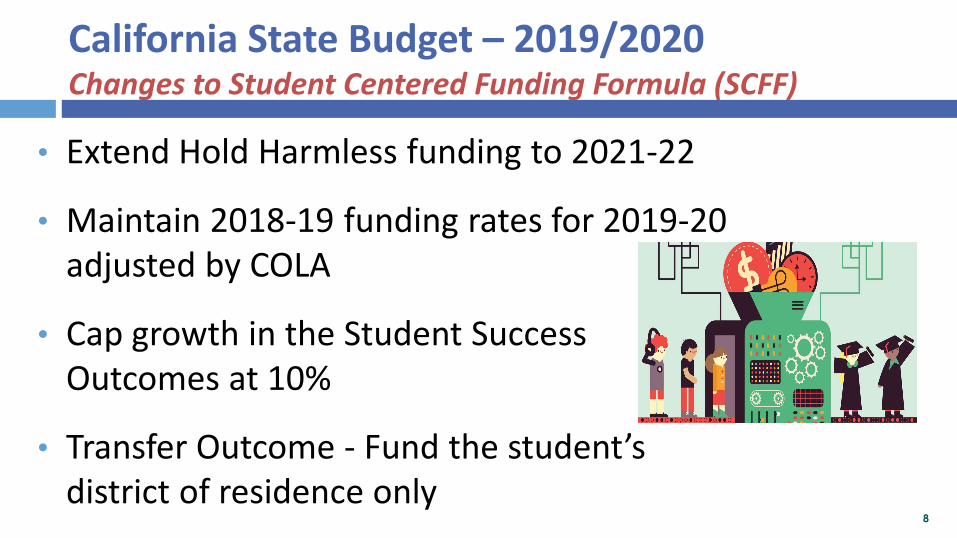

California State Budget – 2019/2020 Changes to Student Centered Funding Formula (SCFF)

• Extend Hold Harmless funding to 2021-22

• Maintain 2018-19 funding rates for 2019-20adjusted by COLA

• Cap growth in the Student SuccessOutcomes at 10%

• Transfer Outcome - Fund the student’sdistrict of residence only

8

The latest on SCFF- Compromise between Legislature and the Governor

Cap the student success allocation to 10% of the total formula allocation

For 2018-19, transfer data is based on publicly available info

Effective 2019-20, transfer data is based on recently enrolled students

Three-year rolling average for the student success metrics

Unduplicated count for the highest award obtained

*Source: School Services of California 9

California State Budget - 2019/2020 Major Revenue Assumptions

Unrestricted Programs State

Proposed Ohlone

Estimates

• Growth (0.55%)• COLA (3.26%)• Mandate Block Grant• Full Time Faculty Funding• Lottery Revenue

$25M $230M

$33M $50M

$151/FTES

∅

$1.6M $240K $324K $1.1M

10

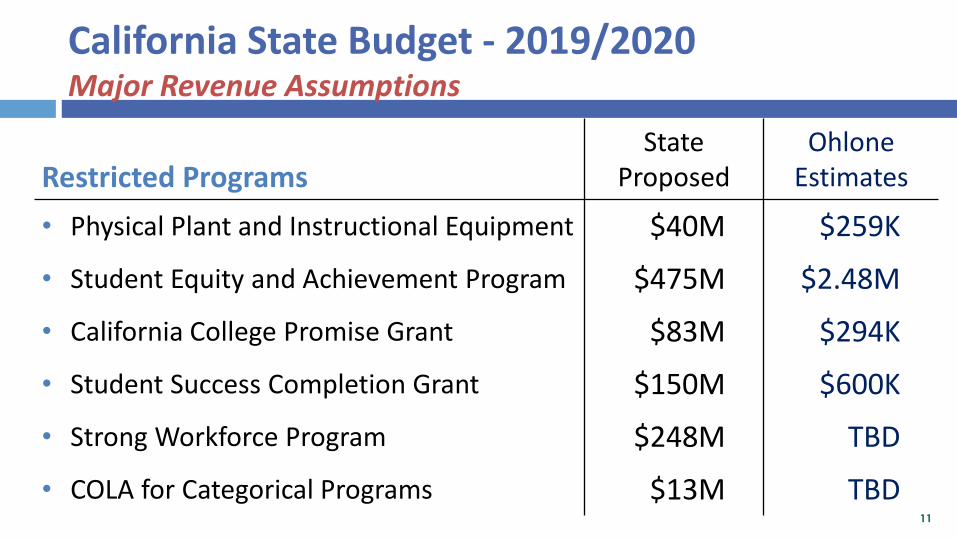

California State Budget - 2019/2020 Major Revenue Assumptions

Restricted Programs State

Proposed Ohlone

Estimates

• Physical Plant and Instructional Equipment

• Student Equity and Achievement Program

• California College Promise Grant

• Student Success Completion Grant

• Strong Workforce Program

• COLA for Categorical Programs

$40M

$475M

$83M

$150M

$248M

$13M

$259K

$2.48M

$294K

$600K

TBD

TBD 11

OHLONE COLLEGE 2019-20 TENTATIVE BUDGET

2019-20 Tentative Budget Major Revenue Assumptions – Unrestricted General Fund (Fund 10)

Categories 2019/20 2020/21 2021/22 2022/23

Base Allocation:

FTES Target

Enrollment Growth

7,303

∅

7,522

3%

7,673

2%

7,673

∅

Supplemental Allocation - Growth ∅ 3% 2% ∅

Student Success Allocation - Growth ∅ 3% 2% ∅

13

2019-20 Tentative Budget Major Expenditures Assumptions – Unrestricted General Fund (Fund 10)

• Steps, Column and Longevity costs $429K

• PERS/STRS rate increases $560K

• Temporary expenditures reduction ($2.3M)

• OPEB cost charged 100% to Fund 10 $503K

• DSPS program backfill $930K

• Parking Fund backfill $200K 14

2019-2020 Tentative Budget Institutional Improvements Objectives (IIOs)

• General Fund (Fund 10): Noncredit Programs Program Review/Planning Tool

• Restricted Funds: First Year Student Experience Noncredit Programs Integrated Professional Development Planning Program Review/Planning Tool

Cost

$25,000 $25,000

TBD $75,000

TBD $25,000

15

Retirement Contributions (STRS/PERS) Unrestricted General Fund (Fund 10)

1.47M 1.87M

2.22M 2.66M

2.71M 2.98M 2.96M 3.00M 3.03M 3.07M 3.11M

1.27M 1.67M

2.04M 2.54M

3.05M 3.56M

3.81M 3.98M 4.14M 4.23M 4.26M

2.74M

3.53M

4.26M

5.20M

5.76M

6.54M 6.77M 6.98M 7.18M 7.30M 7.37M

1.00M

2.00M

3.00M

4.00M

5.00M

6.00M

7.00M

8.00M

0.00M

2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22 2022-23 2023-24 2024-25 2025-26 STRS PERS Total

16 *Based on tentative 2019/20 staffing levels and annual step/column increases. Amounts subject to change.

2019-20 Tentative Budget - Unrestricted General Fund (Fund 10) Description

2019-2020 2020-2021 Projected Budget

2021-2022 Projected Budget

2022-2023 Projected Budget Tentative Budget

17Revenue: Apportionment per SCFF Hold Harmless One-time Funds Other Sources

43,814,606 46,818,212 6,452,145 7,655,752

48,295,593 6,466,334 7,690,864

50,479,527 -

7,699,380 7,904,187 7,608,004

Revenue Total 59,326,797 60,926,109 62,452,791 58,178,908

Expenditures Temporary Exp. Reduction

60,353,504 61,785,802 (3,758,727)

62,373,878 (3,758,727)

63,257,351 (3,758,727) (2,349,872)

Expenditures Total 58,003,632 58,027,075 58,615,151 59,498,624

Net Increase/Decrease 1,323,164 2,899,034 3,837,640 (1,319,717)

Beginning Fund Balance 9,975,317 11,298,482 14,197,516 18,035,156

Ending Fund Balance 11,298,482 14,197,516 18,035,156 16,715,440

Fund Balance % of Expenditures 19.48% 24.47% 30.77% 28.09% *Expenditures does not include negotiated settlements. 17

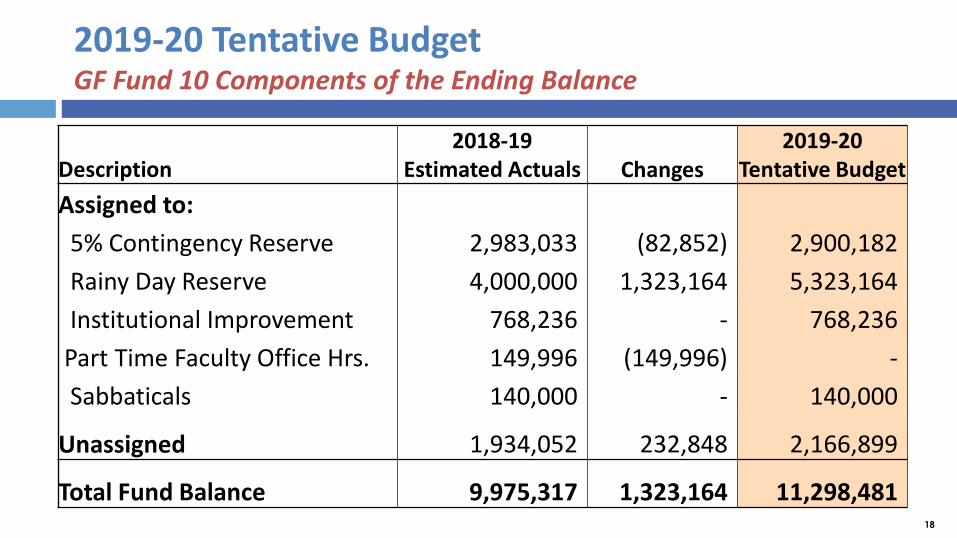

2019-20 Tentative Budget GF Fund 10 Components of the Ending Balance

Description 2018-19

Estimated Actuals Changes 2019-20

Tentative Budget Assigned to: 5% Contingency Reserve 2,983,033 (82,852) 2,900,182 Rainy Day Reserve 4,000,000 1,323,164 5,323,164 Institutional Improvement 768,236 - 768,236

Part Time Faculty Office Hrs. 149,996 (149,996) -Sabbaticals 140,000 - 140,000

Unassigned 1,934,052 232,848 2,166,899

Total Fund Balance 9,975,317 1,323,164 11,298,481 18

2019-20 Tentative Budget Unrestricted General Fund (Fund 10-18) Summary

Fund 10 Fund 12 Unrestricted Program

Description General Distribution

Fund 13 Community Education

Fund 14 Contract

Education

Fund 15 Smith Center

Fund 18 Civic Center

Rentals

Total Unrestricted General Fund

Revenues 59,326,797 15,000 1,521,164 100,000 262,500 358,800 61,584,261

Expenditures 58,003,632 23,942 1,483,036 89,100 262,250 227,000 60,088,960

Net Activity 1,323,164 (8,942)

Beginning Fund Balance 9,975,317 8,942

38,128

204,902

10,900

411,117

250

61,330

131,800

1,039,677

1,495,301

11,701,284

Ending Fund Balance 11,298,481 - 243,030 422,017 61,580 1,171,477 13,196,584

19.48% 21.96% 19

2019-20 Tentative Budget Restricted General Fund and All Other Funds (Fund 20-69) Summary

Description

Fund 20 Categorical

Fund 21 Grants

Fund 25 Parking

Fund 26 Health

Services

Fund 41 Capital Outlay

Fund 43 Measure G

Bond

Fund 69 Internal

Services Fund

Revenues 10,850,735 10,606,354 861,776 325,000 159,500 350,000 503,196

Expenditures 10,850,735 10,606,354 861,776 341,222 279,500 39,700,000 503,196

- - - (16,222) (120,000) (39,350,000) -

- - 136,728 47,488 3,600,217 39,350,000 3,707,038

Net Activity

Beginning FB Ending

Fund Balance - - 136,728 31,266 3,480,217 - 3,707,03820

21

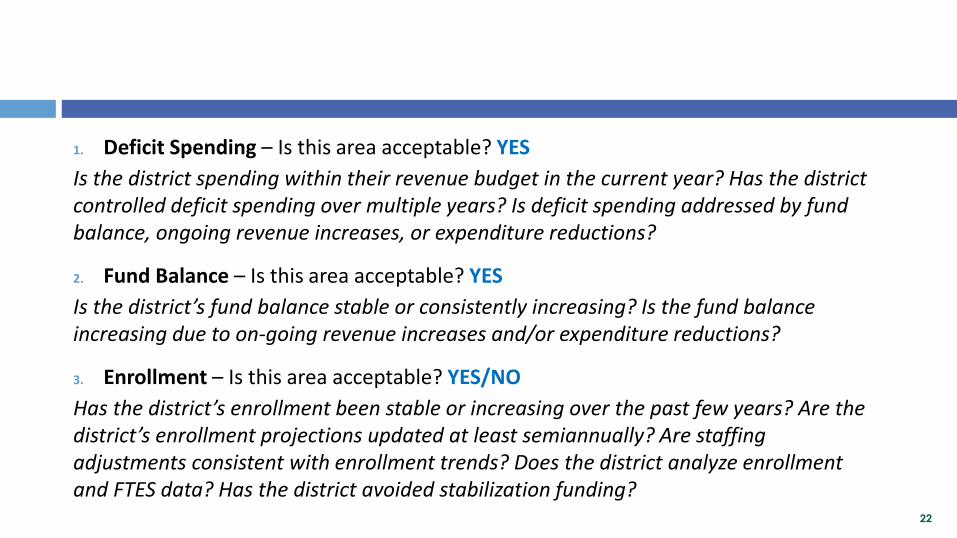

CCC Sound Fiscal Management Self Assessment Checklist

1. Deficit Spending – Is this area acceptable? YES Is the district spending within their revenue budget in the current year? Has the district controlled deficit spending over multiple years? Is deficit spending addressed by fund balance, ongoing revenue increases, or expenditure reductions?

2. Fund Balance – Is this area acceptable? YES Is the district’s fund balance stable or consistently increasing? Is the fund balance increasing due to on-going revenue increases and/or expenditure reductions?

3. Enrollment – Is this area acceptable? YES/NO Has the district’s enrollment been stable or increasing over the past few years? Are the district’s enrollment projections updated at least semiannually? Are staffing adjustments consistent with enrollment trends? Does the district analyze enrollment and FTES data? Has the district avoided stabilization funding?

22

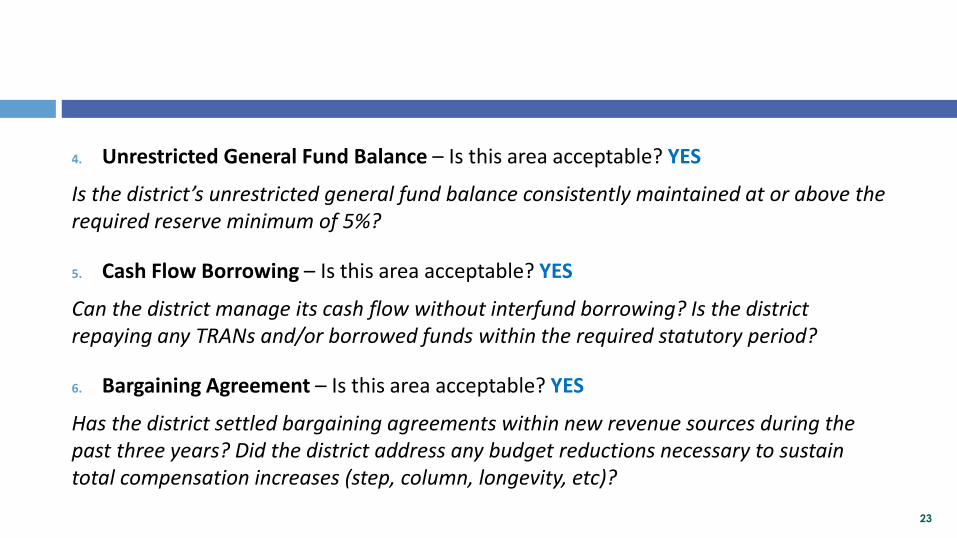

4. Unrestricted General Fund Balance – Is this area acceptable? YES

Is the district’s unrestricted general fund balance consistently maintained at or above the required reserve minimum of 5%?

5. Cash Flow Borrowing – Is this area acceptable? YES

Can the district manage its cash flow without interfund borrowing? Is the district repaying any TRANs and/or borrowed funds within the required statutory period?

6. Bargaining Agreement – Is this area acceptable? YES

Has the district settled bargaining agreements within new revenue sources during the past three years? Did the district address any budget reductions necessary to sustain total compensation increases (step, column, longevity, etc)?

23

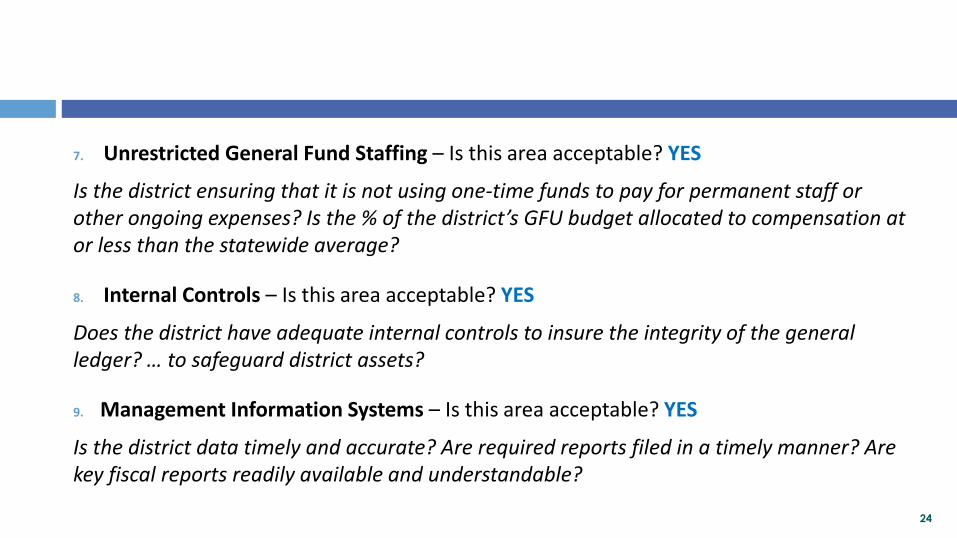

7. Unrestricted General Fund Staffing – Is this area acceptable? YES

Is the district ensuring that it is not using one-time funds to pay for permanent staff or other ongoing expenses? Is the % of the district’s GFU budget allocated to compensation at or less than the statewide average?

8. Internal Controls – Is this area acceptable? YES

Does the district have adequate internal controls to insure the integrity of the general ledger? … to safeguard district assets?

9. Management Information Systems – Is this area acceptable? YES

Is the district data timely and accurate? Are required reports filed in a timely manner? Are key fiscal reports readily available and understandable?

24

10. Position Control– Is this area acceptable? YES / NO Is position control integrated with payroll? Does the district control unauthorized hiring? Does the district have controls over part-time academic staff hiring?

11. Budget Monitoring – Is this area acceptable? YES Is there sufficient consideration to budget related to long-term bargaining agreements? Are budget revisions completed in a timely manner? Does the district openly discuss the impact of budget revisions at the board level? Does the district compile annualized revenue and expenditure projections throughout the year? Are long term debt levels manageable?

12. Retiree Health Benefits – Is this area acceptable? YES Has the district completed a recent actuarial study to determine its unfunded liability? Does the district have a plan for addressing the retiree benefits liabilities?

25

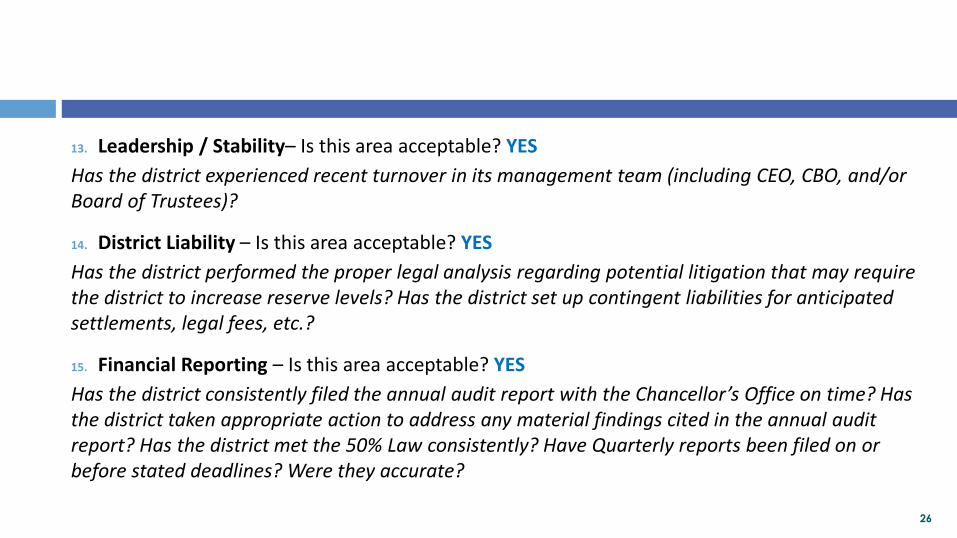

13. Leadership / Stability– Is this area acceptable? YES Has the district experienced recent turnover in its management team (including CEO, CBO, and/or Board of Trustees)?

14. District Liability – Is this area acceptable? YES Has the district performed the proper legal analysis regarding potential litigation that may require the district to increase reserve levels? Has the district set up contingent liabilities for anticipated settlements, legal fees, etc.?

15. Financial Reporting – Is this area acceptable? YES Has the district consistently filed the annual audit report with the Chancellor’s Office on time? Has the district taken appropriate action to address any material findings cited in the annual audit report? Has the district met the 50% Law consistently? Have Quarterly reports been filed on or before stated deadlines? Were they accurate?

26

What is next?

• State Budget by June 30th

• Ohlone 2019-20 Final Budget to the Board on September 11th

27

THANKS! Any questions?