office of public accountability -...

TRANSCRIPT

Office of Public Accountability

Annual Report

Calendar Year 2018

July 2019

Office of Public Accountability Annual Report

Calendar Year 2018

July 2019 Distribution: Governor of Guam Lt. Governor of Guam Speaker, 35th Guam Legislature Senators, 35th Guam Legislature Guam Media via E‐Mail

Table of Contents Message from the Public Auditor ................................................................................................................ 2

Who We Are? ............................................................................................................................................... 3

Year in Review .............................................................................................................................................. 4

Performance Audits Overview .................................................................................................................. 4

Procurement Appeals Overview ............................................................................................................... 5

Financial Audits Overview ......................................................................................................................... 5

Who Audits the Auditor? .......................................................................................................................... 5

FY 2018 Budget Execution ........................................................................................................................ 6

Staff Time Composition ............................................................................................................................. 6

Strengthening Performance ...................................................................................................................... 7

Performance Audits ..................................................................................................................................... 8

2019 Audit Plan ................................................................................................................................ 10

Procurement Appeals ................................................................................................................................. 12

Financial Audits .......................................................................................................................................... 14

Single Audit Compliance ......................................................................................................................... 15

Auditees with Non‐Federal Funding ....................................................................................................... 16

Management Letter ................................................................................................................................ 17

Procurement of Financial Audit Services ................................................................................................ 17

OPA Legislative Mandates ......................................................................................................................... 18

OPA Hotline (47AUDIT; 472‐8348) ............................................................................................................. 19

OPA Website and Audit Software .............................................................................................................. 20

Staffing Level Challenges............................................................................................................................ 21

Public Outreach and Community Service .................................................................................................. 28

Glossary of GovGuam Entities’ Acronyms ............................................................................................. 31

OPA Financial Statements ...................................................................................................................... 32

APIPA Peer Review Report ..................................................................................................................... 34

Procurement Appeals Synopsis ............................................................................................................. 36

Financial Audits ...................................................................................................................................... 40

Hotline Tips Statistics ............................................................................................................................. 41

Organizational Chart as of December 31, 2018 ..................................................................................... 42

CY 2018 Objectivity • Professionalism • Accountability P a g e | 2

Message from the Public Auditor Hafa Adai! I am pleased to present my first annual report as your elected Public Auditor. The voters of Guam bestowed on me a tremendous honor and responsibility to be the watchdog for the public’s resources when they elected me to fill the remainder of the term left by my predecessor. I am humbled by the trust and confidence placed in me.

As your Public Auditor, I am dedicated to making sure the timely issuance of government agencies’ financial audits. The practice of issuing audits that are not current is unacceptable and intolerable. Issuing timely audits assists the three branches of government in making changes that will result in a more efficient use of our island’s precious limited resources. One of my expressed goals is to have required annual audits issued by March 31.

This past year has been a time of transition and change for the Office of Public Accountability (OPA). One of my first directives in coming into this office was to get a full reporting of OPA’s finances. In receiving this report and confirming the overspending of legislative appropriations, we had to make the tough, but necessary cuts in personnel to stay within the budgeted amounts. As a result, our office lost over 45 years of auditing experience with the departure of five employees.

A second directive was to complete the OPA’s strategic plan, annual audit plan, and stakeholder engagement strategic plan. Our office, with the assistance of the International Organization of Supreme Audit Institutions’ Development Initiative and Pacific Association of Supreme Audit Institutions completed three crucial planning documents that lay the groundwork for the activities of our office.

A third directive was to open the lines of communication with local, regional, federal, and community leaders, as well as the media and public, to reinforce the mandates of this office and offer our assistance on issues that are of mutual importance to our island. My staff and I have been meeting with these stakeholders over the past months to listen, learn, and work for the betterment of our people.

Despite the challenges, the office continued its commitment and dedication to “Auditing for Good Governance” with the issuance of eight performance audits, which collectively identified $47.2 million in questioned costs, lost revenues, and other financial impacts. These performance audits provided 34 recommendations to improve accountability, effectiveness, and efficiency. The office also administered eight procurement appeals and provided oversight on 23 financial audits and three financial audit Request for Proposals of the Government of Guam entities.

Lastly, I would like to extend my heartfelt appreciation to my dedicated staff, whose professionalism, integrity, and commitment have made my role as Public Auditor easier. We will continue to promote accountability and responsibility in government.

Senseramente, Benjamin J.F. Cruz Public Auditor

CY 2018 Objectivity • Professionalism • Accountability P a g e | 3

Who We Are? Public Law (P.L.) 21‐122 established the Office of Public Accountability (OPA) in July 1992. OPA is an instrumentality of the Government of Guam (GovGuam), independent of the executive, legislative, and judicial branches. At OPA, we seek to:

Achieve independent and nonpartisan assessments that promote accountability and efficient, effective management throughout GovGuam; and

Serve the public interest by providing the Governor of Guam, the Guam Legislature, and the people of Guam with dependable and reliable information, unbiased analyses, and objective recommendations on how best to use government resources to support the well‐being of our island and its constituents.

(Standing L‐R) Marisol Andrade, Andriana Quitugua, Christian Rivera, Michele Brillante, Ira Palero, Jerrick Hernandez, Amacris Legaspi, and Thyrza Bagana; (Front L‐R) Edlyn Dalisay, Frederick Jones, Benjamin Cruz, Vincent Duenas, and Clariza Roque.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 4

Year in Review OPA continued its commitment and dedication to “Auditing for Good Governance” despite a major change in management and reduction in staff in the calendar year (CY) 2018. In CY 2018, we:

Issued eight performance audits, which collectively identified $47.2 million (M) in questioned costs, lost revenues, and other financial impacts. These performance audits provided 34 recommendations to improve accountability, effectiveness, and efficiency;

Administered eight procurement appeals; and

Provided oversight on 23 financial audits and three financial audit Request for Proposals (RFP) of the GovGuam entities.

Performance Audits Overview In CY 2018, we issued the following eight performance audits:

1. GRTA Procurement and Billing of Public Transit Services; 2. Guam Football Association Soccer Stadium Contributions; 3. DRT Real Property Tax Assessments and Exemptions; 4. DRT Tobacco Tax; 5. GovGuam Health Insurance Contracts Analysis; 6. GRTA Non‐Appropriated Funds; 7. DPW Inventory Management and Consumable Parts, Supplies, and Materials Inventory;

and 8. GEDA Qualifying Certificate Community Cash Contributions.

Refer to Appendix 1 for the GovGuam Entities’ Glossary of Acronyms.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 5

Procurement Appeals Overview In 2018, OPA received eight procurement appeals, of which five were addressed as follows:

Rendered one decision within 30 to 60 days from the formal hearing;

Dismissed three appeals due to parties’ settlement; and

Dismissed one due to Appellant’s withdrawal of the appeal. Three appeals were carried over to 2019. The agencies involved in these eight appeals were GMHA, DPW, DOA, GSA, and GDOE, with a total procurement value of $8.7M.

Financial Audits Overview Overall, we observed the following for the 23 FY 2017 financial audits issued in CY 2018:

All 23 received unmodified “clean” opinion over their financial reporting;

Only DCA did not issue its financial audit by June 30, 2018; and

16% decrease in management letter comments. The external auditors issued a separate report on compliance for each major federal programs for nine agencies (GWA, PAG, GIAA, GCC, UOG, GDOE, GHURA, GMHA, and GovGuam). We observed a $334 thousand (K) or 67% decrease in questioned costs in FY 2017. GIAA, GWA, GCC, and UOG maintained their low‐risk status.

Who Audits the Auditor? OPA’s financial statements audits are included in the government‐wide financial audit. OPA has not received any management letter comments in connection with its financials. See Appendix 2 for OPA’s 2018 financial statements.

In addition, Government Auditing Standards require independent peer reviews every three years to assure audit organizations are complying with professional standards and legal requirements. Association of Pacific Islands Public Auditors (APIPA) conducted OPA’s latest peer review in September 2017, which covered CY 2014 through CY 2016. This review marked OPA’s 6th “Full Compliance” rating, and the 3rd time that no Management Letter was issued. See Appendix 3 for APIPA’s Peer Review Report.

OPA’s next peer review will be in 2020 covering CY 2017 through CY 2019.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 6

FY 2018 Budget Execution OPA’s expenditures of $1.6M were more than its $1.4M FY 2018 budget plus $135K authorization to carry over lapses. Details of OPA’s FY 2018 funding sources and expenditures follow: Due to the FY 2018 Appropriations shortfall over OPA’s level operations, OPA used its cash reserves to cover the over expenditures. In September 2018, during his first month in office, the newly elected Public Auditor made the tough decision to cut personnel to stay within the budget granted by the Legislature. The following month, OPA issued a transparency report stating that OPA’s FY 2019 Budget Appropriation is $1.3M, of which $1.0M is for personnel.

Staff Time Composition At the beginning of CY 2018, OPA had 17 full‐time staff. This number went down to 13 as of December 31, 2018, comprising of the Public Auditor, 11 Staff Auditors, and 1 Administrative Services Officer (ASO). Refer to Appendix 7 for OPA’s Organizational Chart as of December 31, 2018. Of the total hours available to OPA staff in CY 2018, OPA staff spent:

46% on performance audits, mandates, and investigative works;

9% on financial audits; and

3% on procurement appeals. OPA spent the rest of their time on training, administrative tasks, leaves, and holidays.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 7

Strengthening Performance OPA participated in the INTOSAI Development Initiative (IDI) Supreme Audit Institution (SAI) Performance Measurement Framework (PMF), a tool that measures, monitors, manages, and reports on a SAI’s performance. In May 2017, representatives from the Pacific Association of Supreme Audit Institution (PASAI) and the Republic of Marshall Islands’ Office of the Auditor General assessed OPA. The purpose of the SAI PMF was to assist OPA in identifying the strengths and weaknesses of its audit processes and capabilities against International Standards for Supreme Audit Institutions (ISSAI) and other established good practices. Overall, the SAI PMF assessed OPA’s performance as reasonable considering the constraints and challenges OPA encountered over the years. OPA received overall ratings between 1 and 3. See Table 1.

Table 1: OPA’s Performance Measurement Rating

Domain OPA Score Range

(Highest is 4)

Independence and Legal Framework 2

Internal Governance and Ethics 1‐3

Audit Quality and Reporting 2‐3

Financial Management, Assets and Support Services 3

Human Resource and Training 1‐2

Communication and Stakeholder Management 1‐2

OPA is committed to addressing areas in need of improvement. In January 2019, OPA released its Strategic Plan 2019‐2023, Stakeholders Engagement Plan 2019‐2023, and CY 2019 Audit Plan to correct its SAI PMF deficiencies.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 8

Performance Audits Performance audits provide independent analysis on specific programs:

To assist management and public officials in improving program performance and operations (e.g., effectiveness, economy, efficiency, and compliance); and

To improve public accountability and transparency. Report No. 18‐01: GRTA Procurement and Billing of Public Transit Services

Initiated in response to a request from a Senator in the 34th Guam Legislature.

The procurement record for the management and operations of the public transit services was incomplete and could not support the sole‐source awarding to the vendor. In addition, GRTA did not have a formal contract for this purchase.

GRTA's billing review was inadequate to identify overages.

Report No. 18‐02: Guam Football Association (GFA) Soccer Stadium Contributions

Initiated in response to a citizen concern. GFA officials did not follow the Federation Internationale de Football Association and Asian Football Confederation Codes of Ethics provisions on conflict of interest.

DPR failed to create a Memorandum of Understanding for the use of the Northern Soccer Stadium.

GFA significantly delayed remitting the Event Admission Assessment Fee.

GVB did not request for an accounting of the $400K granted to GFA. Report No. 18‐03: DRT Real Property Tax Assessments and Exemptions

Initiated as part of the annual plan, as well as in response to a request from a Senator in the 34th Guam Legislature.

DRT did not effectively monitor uncollected property taxes or aggressively collect on delinquent property taxes.

DRT systems were unable to identify all owners of new properties added after the 2014 mass re‐appraisal.

The existing systems do not have the ability to create Parcel Identification Numbers.

DRT, DLM, and DPW's systems do not interface.

DRT and DLM did not strictly adhere to the Memorandum of Agreement.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 9

Report No. 18‐04: DRT Tobacco Tax

Initiated in response to concerns received that tobacco taxes may be underreported.

Ninety‐nine percent of imported tobacco was released to private warehouses without immediate assessment and collection of tobacco tax.

CQA and DRT’s policies and procedures for assessing tobacco tax provide opportunities for under‐reporting and fall short of ensuring that all tobacco taxes are paid.

DRT’s data on the number of Guam‐licensed tobacco wholesalers did not match the number of taxpayers filing tobacco tax.

CQA does not maintain comprehensive, detailed data on imported tobacco.

Tax receivables and deferred revenues are not recorded for the imported tobacco products stored in and withdrawn from, the DRT‐controlled section of the wholesaler’s private warehouse.

DRT and CQA do not reconcile the tobacco taxes reported to the tobacco shipments.

Report No. 18‐05: GovGuam Health Insurance Contracts Analysis

Initiated in response to a request from a Senator in the 34th Guam Legislature.

GovGuam generously shouldered a substantial portion

of subscribers' health insurance premiums ($275.6M

or 76%), mainly caused by the law requirement and

lack of price pooling.

The lowest health insurance premium was not always

the employees' top choice.

DOA did not verify the refunds/no refunds accounting

from Carriers.

GovGuam's premiums were higher than the Guam Judiciary and the Federal Government.

Report No. 18‐06: GRTA Non‐Appropriated Funds (NAF)

OPA‐initiated audit.

GRTA did not adopt and maintain an accounting system for the NAF.

GRTA did not have basic control activities, such as maintaining a check register, performing bank reconciliations, and having effective policies and standard operating procedures.

GRTA did not report the NAF's financial activity to the GRTA Board, Governor, Legislature, or OPA.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 10

Report No. 18‐07: DPW Inventory Management and Consumable Parts, Supplies, and Materials Inventory

OPA‐initiated audit.

DPW's Supply Warehouse inventory management systems did not produce accurate records to account for and safeguard consumable inventories.

There were many discrepancies amongst the inventory records because the Supply Warehouse did not perform periodic reconciliation of the three inventory management systems (stock cards, Excel spreadsheets, and the Ron Turley Associates Fleet Management Software).

DPW management has not provided a target date to phase out the stock cards and excel spreadsheets.

Report No. 18‐08: GEDA Qualifying Certificate Community Cash Contributions

Initiated in response to a request from a Senator in the 34th

Guam Legislature.

There was a lack of monitoring on certain community cash contributions.

GEDA has wide discretion over the allocation of community cash contributions. As a result, GEDA allocated 73% or $2.2M to its own marketing and economic development operations.

GEDA did not monitor separately the community cash contributions allocated to economic development from the general operations.

GEDA did not advertise the community cash contributions.

2019 Audit Plan We annually establish an audit plan to determine which government entities and programs to review based on extensive discussions with staff, audit requests from stakeholders, and risk assessments. We solicit input from the public through an online survey. We also request input from all agency heads and public officials. Besides the ongoing audits, the CY 2019 plan includes the following new audits:

1. Use Tax Collection (initiated as of February 2019); 2. Short‐Term Vacation Rental/Bed & Breakfast; 3. Hotel Occupancy Tax Collection (initiated as of February 2019); 4. Cancer Treatment Fund (initiated as of April 2019); 5. Charter Schools Expenditures; 6. Tourist Attraction Fund (TAF) Expenditures; 7. Autonomous Agencies’ Legal Fees (initiated as of February 2019);

CY 2018 Objectivity • Professionalism • Accountability P a g e | 11

8. Travel Per Diem and Expenses; 9. Ambulance Service; 10. Parent‐Teacher Organization; and 11. MCOG Receipts and Disbursements.

The audit plan is a flexible guide that can accommodate other audits based on priority, requests from elected officials, and staff availability. As of May 2019, OPA initiated two audits that were not part of the CY 2019 audit plan. These audits pertain to the transition funds for the Governor and Lieutenant Governor and an audit of tobacco bonded warehouses. Meanwhile, audits initiated in CY 2018 and carried over to CY 2019 are as follows:

1. GMHA Billings and Collections (Issued February 2019, OPA Report No. 19‐01); 2. DOA Special Revenue Fund (Issued March 2019, OPA Report No. 19‐02); 3. DRT Non‐Profit Organization Limited Gaming Tax (Issued March 2019, OPA Report No. 19‐

03); 4. GovGuam Procurement Training and Certification (Issued April 2019, OPA Report No. 19‐

04) 5. Public Safety Overtime (ongoing as of May 2019) 6. Government‐wide Standard Operating Procedures (ongoing as of May 2019)

CY 2018 Objectivity • Professionalism • Accountability P a g e | 12

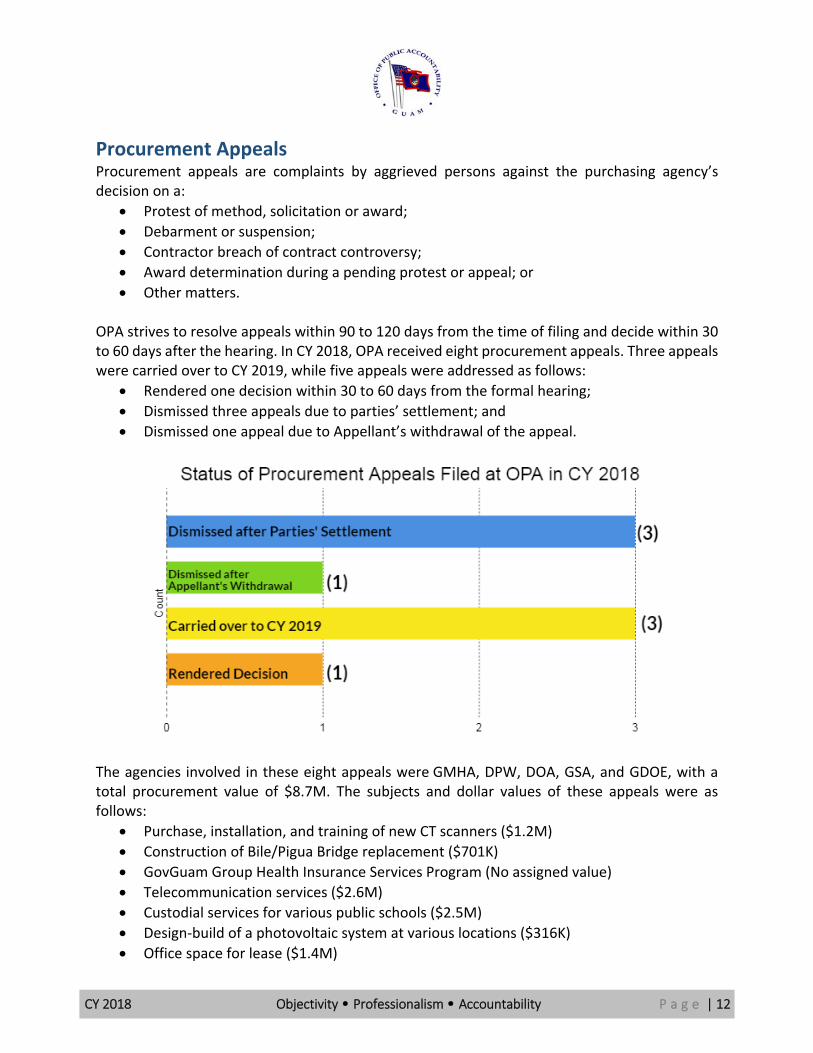

Procurement Appeals Procurement appeals are complaints by aggrieved persons against the purchasing agency’s decision on a:

Protest of method, solicitation or award;

Debarment or suspension;

Contractor breach of contract controversy;

Award determination during a pending protest or appeal; or

Other matters. OPA strives to resolve appeals within 90 to 120 days from the time of filing and decide within 30 to 60 days after the hearing. In CY 2018, OPA received eight procurement appeals. Three appeals were carried over to CY 2019, while five appeals were addressed as follows:

Rendered one decision within 30 to 60 days from the formal hearing;

Dismissed three appeals due to parties’ settlement; and

Dismissed one appeal due to Appellant’s withdrawal of the appeal.

The agencies involved in these eight appeals were GMHA, DPW, DOA, GSA, and GDOE, with a total procurement value of $8.7M. The subjects and dollar values of these appeals were as follows:

Purchase, installation, and training of new CT scanners ($1.2M)

Construction of Bile/Pigua Bridge replacement ($701K)

GovGuam Group Health Insurance Services Program (No assigned value)

Telecommunication services ($2.6M)

Custodial services for various public schools ($2.5M)

Design‐build of a photovoltaic system at various locations ($316K)

Office space for lease ($1.4M)

CY 2018 Objectivity • Professionalism • Accountability P a g e | 13

Refer to Appendix 4 for the summaries of the procurement appeals filed in 2018. Since 2006, OPA received an average of 13 appeals filings per year. GSA had the most appeals filed against them with 47, followed by GDOE with 35 appeals. Procurement Appeals Improve the Procurement Process Aggrieved vendors have been deliberative and reflective and invest time, money, and effort to file an appeal. The Public Auditor concluded that vendors continue to scrutinize the GovGuam procurement process. Vendors are analyzing bids and specifications and challenging premature disqualifications. These efforts help strengthen and improve the procurement process. A common misconception is that appeals prolong the overall procurement process. However, appeals have been resolved generally within 90 to 120 days. We also encourage parties to agree to resolve their procurement issues. Procurement appeals revealed the need for further government procurement training. GCC has courses on the procurement process as required by P.L. 32‐131 (codified in Guam Procurement Law). All GovGuam procurement personnel must take these training courses. OPA Hearing Officers The Public Auditor assigns each time‐sensitive procurement appeal to one of three OPA Hearing Officers who are licensed attorneys. OPA established this pool to handle the workload and prevent potential conflicts. There are cost savings from hiring contractual attorneys on an as‐needed basis versus a full‐time staff attorney. OPA Hearing Officers may also provide other legal advice and services as requested by the Public Auditor.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 14

Financial Audits Financial audits provide independent assessments of an entity’s overall annual performance and financial health; and whether the entity’s financial statements are fairly presented in compliance with applicable professional standards. With limited staff resources, the Public Auditor has continued contracting GovGuam’s financial audits to independent Certified Public Accountant (CPA) firms. We monitor and oversee the work of the contracted audit firms to ensure GovGuam entities’ annual financial audits are issued by June 30 (or nine months) after fiscal year‐end [1 GCA, Chapter 19, §1909(a)]. Of the 23 FY 2017 financial audits issued in 2018, only DCA did not complete its financial audit as of June 30, 2018.

We envision GovGuam as the model for good governance and encourage financial audits to be completed no later than six months (or March 31) after the fiscal year‐end. We commend IACS, GPT, GIAA, and GHC for issuing their financial audits by March 31, 2018. The financial statements of all 23 FY 2017 GovGuam entities/funds received unmodified (or “clean”) opinions. All government financial audits must include a report on internal control over financial reporting and on compliance, whether or not findings are identified.

Listed below are the 23 entities audited for FY 2017 and issued in CY 2018, in order of release date:

1. IACS 2. GPT 3. GIAA* 4. GHC 5. TAF 6. GHF 7. GVB 8. PAG*

9. GWA* 10. GCC* 11. KGTF (PBS Guam) 12. GPA 13. CLTC 14. GGRF 15. GEDA 16. GALC

17. UOG* 18. GHURA* 19. GSWA 20. Government‐wide* 21. GDOE* 22. GMHA* 23. DCA

* Entities subjected to Single Audits.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 15

Single Audit Compliance Government entities that spend more than $750K in federal grants require an additional report on compliance for each major federal program (or “Single Audit”). Of the 23 entities audited, nine (*) were subject to Single Audits in FY 2017. Of the nine entities that required a Single Audits, four (PAG, GWA, GCC, and GMHA) had no findings on their compliance for major federal programs. The other five entities accumulated 27 findings:

GIAA received an unmodified opinion; however, had one significant deficiency pertaining to non‐submission of one quarter’s project financial statements to the Transportation Security Administration.

UOG received an unmodified opinion; however, had one significant deficiency related to not meeting target goals for the Small Business Development Centers’ federal award. This was a repeat finding.

GHURA received a modified opinion and 16 findings, which included 5 material weaknesses and 11 significant deficiencies. These 16 findings comprised seven findings on Public Indian Housing (known as Low Income Housing Assistance Program), four findings on Section 8 Housing Choice Voucher Program, four findings on Supportive Housing for the Elderly, and one finding on Public Housing Capital Fund Program.

Government‐wide received a modified opinion and seven findings, which included three material weaknesses and four significant deficiencies. The seven findings comprised three findings on procurement, two findings on the Supplemental Nutrition Assistance Program, one finding on equipment and real property management and capital assets, and one finding on the Medical Assistance Program.

GDOE received an unmodified opinion; however, had two findings related to procurement, and the lack of coordination between GovGuam and GDOE for the level of effort requirement.

A questioned cost arises from the:

Alleged violation of a law, regulation, or the terms and conditions of a Federal award;

Inadequate documentation of costs at the time of the audit; or

Unreasonable and wasteful expenditure of funds. For the FY 2017 Single Audits, the external auditors raised questioned costs for the Government‐wide and GDOE totaling $168K. This was a decrease by $334K or 67% from FY 2016’s $502K. Low‐Risk Auditee Receiving Federal Funding One of OPA’s goals is for all the GovGuam entities subject to a Single Audit Act to qualify as a low‐risk auditee. To qualify as a low‐risk auditee, an agency must meet the following conditions for

CY 2018 Objectivity • Professionalism • Accountability P a g e | 16

three consecutive audit periods: 1. Single Audits performed annually; 2. Unmodified “clean” opinion on financial statements; 3. No material weaknesses per GAGAS; 4. No substantial doubt to continue as a going concern; and 5. None of the federal programs has material weaknesses, questioned costs exceeding 5%

of total federal awards spent or a modified opinion.

Of the nine entities subject to Single Audits, four maintained their low‐risk status in FY 2017: 1. GCC for 17 years; 2. GIAA for 3 years; 3. UOG for 3 years; and 4. GWA for 2 years.

The other five – PAG, GHURA, GovGuam, GDOE, and GMHA – did not qualify as low‐risk auditees because:

1. PAG submitted a late report to the Federal Clearing House; 2. GHURA received a modified opinion due to several material weaknesses; 3. GovGuam received a modified opinion due to several material weaknesses and $135K in

questioned costs; 4. GDOE remains a high‐risk grantee with the U.S. Department of Education for the past 15

years; and 5. GMHA had an emphasis on its ability to continue as a going concern.

Auditees with Non‐Federal Funding Financial Reporting Compliance Of the 14 entities that did not receive federal funding, 10 (IACS, GPT, GHC, TAF, GVB, PBS, GPA, GGRF, GEDA, and GALC) had no findings on their internal control over financial reporting for FY 2017 financial audits. The remaining four (GHF, CLTC, GSWA, and DCA) have findings:

GHF had no competitive procurement for the $2.4M GRTA bus transportation and procured through sole source method. This was a repeat finding;

CLTC had no lease agreement for the $10K monthly office rent. This was a repeat finding;

GSWA had no competitive procurement for the $1.2M temporary staffing services and $69K independent contractor services. This was a repeat finding; and

DCA’s five findings concerned: (1) Arts revenues not recorded in the proper period, (2) Guam Museum revenues not recorded at the time of the transaction, (3) purchases not recorded when received, (4) deposits per bank reconciliation did not reflect actual deposits, and (5) inventory counts not timely performed at year‐end.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 17

OPA Low‐Risk Auditee Designation For three years, OPA has recognized entities not subject to a Single Audit that achieved similar low‐risk status. To qualify for OPA’s low‐risk auditee, an agency must meet the following conditions for three consecutive audit periods:

1. Unmodified “clean” opinions on financial statements; 2. No material weaknesses, significant deficiencies, and questioned costs; and 3. Financial statements released within six months after fiscal year‐end, or March 31.

Of the 14 entities that did not receive federal funding, five qualified for OPA’s low‐risk auditee in FY 2017:

1. GPT ‐ for a year 2. GHC ‐ for 3 years 3. GVB ‐ for 3 years 4. PBS ‐ for 3 years 5. GGRF ‐ for 3 years

For FY 2016 financial audits, OPA made an exception to the third criteria about the March 31 audit release because of the Governmental Accounting Standards Board (GASB) No. 73 implementation, which aligns the reporting of pensions, ad hoc cost‐of‐living allowance, and supplemental annuity payments. Implementation of GASB No. 73 required an expert valuation, which was an added procedure to the finalization of the financial statements. This event was beyond the control of the affected agencies. Therefore, GVB and PBS qualified for the OPA's designation as low‐risk auditee in FY 2016.

Management Letter The independent auditors issued separate letters to management to report deficiencies related to internal control over financial reporting, Information Technology (IT), and other matters. In FY 2017, 19 of 23 entities collectively received 83 management letters comments, a 16% improvement from FY 2016’s 99 comments. Meanwhile, six entities collectively received 33 comments on their IT issues, which is an improvement from FY 2016’s 38 comments. Refer to Appendix 5 for a summary of the FY 2017 financial audits released in CY 2018.

Procurement of Financial Audit Services Title 1 GCA, Chapter 19, §1908 authorizes the Public Auditor to acquire independent financial audit services from firms. GovGuam entities work with OPA to issue RFPs to procure the financial audit services. In CY 2018, we issued three RFPs in conjunction with PAG, IACS, and GACS. The RFPs for PAG and IACS resulted in audit contracts for FY 2018, FY 2019, and FY 2020. On the other hand, GACS will reissue its RFP.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 18

OPA Legislative Mandates Besides financial oversight and audit activities, we also handle legislative mandates that have expanded our duties and responsibilities. OPA has 49 open mandates as of CY 2018:

25 required various GovGuam agencies to submit reports and other information to OPA;

10 required OPA to conduct audits;

10 required OPA to provide oversight, approval, or conduct a specific activity;

3 required OPA to be a member of a committee, group, or task force; and

1 required OPA to submit reports to the Guam Legislature and Office of Finance and Budget.

Of the 10 mandates requiring OPA to conduct audits, four are included in the annual financial audit, and one required OPA to review GovGuam Agencies’ Standard Operating Procedures (SOP). The SOP audit is ongoing as of May 2019. Meanwhile, OPA is assessing the feasibility of conducting the remaining five audits because of limited resources:

1. P.L. 30‐221 Beverage Container Recycling Deposit Fund 2. P.L. 32‐023 Farmers’ Cooperative Association of Guam 3. P.L. 32‐060 Non‐Profit Organizations Operating any Gaming Activity 4. P.L. 32‐205 Police Patrol Vehicle and Equipment Revolving Fund 5. P.L. 34‐98 Manpower Development Fund

In January 2017, OPA reported the status of all the legislative mandates issued to OPA from January 2001 to September 2016. OPA Report No. 17‐01, OPA’s Status of Legislative Mandates, is posted on our website, www.opaguam.org. This report found that there were 173 mandates imposed to OPA, of which 153 or 88% were closed because they were addressed, the agencies submitted the required reports, the mandates were not the best use of OPA’s limited resources based on our professional judgment, or deadlines to submit the required audits have lapsed. The most significant mandate to OPA is the responsibility to hear and decide all appeals of procurement decisions. P.L. 28‐68 transferred this mandate from the Procurement Appeals Board to OPA in 2005. Prior to P.L. 28‐68, procurement appeals had to be decided in the Superior Court.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 19

OPA Hotline (47AUDIT; 472‐8348) OPA Hotline provides a confidential way for citizens and government employees to share their concerns and report improper government activities:

Illegal acts (such as corruption, bribery, theft, or fraud),

Misuse or abuse of government property or time, and

Gross misconduct, incompetence, or inefficiency. Information received on the hotline helps us assess risks and determine where to focus OPA’s

limited resources. OPA holds all hotline information in the strictest confidentiality. Disclosing privileged communication or information violates 1 GCA §1909.1 as a felony of the third degree. Of the 57 hotline tips received in CY 2018, 25 were closed and 32 remain open as of December 2018. Of the 32 open hotline tips/citizens’ concerns, 10 were forwarded to their respective entity’s internal auditors and external auditors and four are ongoing with OPA.

Although responses may not be immediate, we take all concerns seriously. With limited staff resources, it is often difficult to research, interview, and follow‐up on hotline tips and citizen concerns. Not all the information needed to respond to a hotline tip or citizen concern may have been provided. For a tip or concern to be considered, we suggest that the submission include as many details to answer who, what, where, when, and how.

We received 1,503 hotline tips since OPA established the Hotline in CY 2001. The number of hotline tips received ranged from a high of 177 tips in CY 2004 to a low of 23 tips in CY 2012. Refer to Appendix 6 for more details. Anyone who wishes to submit a hotline tip or express concern may do so by:

Calling 47AUDIT (472‐8348);

Visiting www.opaguam.org;

Faxing sufficient and relevant information to 472‐7951; or

Contacting any of the OPA staff by phone at 475‐0390 or in person. Help make a difference in our government by contacting the OPA Hotline.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 20

OPA Website and Audit Software OPA’s website provides reliable and transparent information about our government’s financial condition. Our website, www.opaguam.org, features user‐friendly navigation, organized content, and mobile device accessibility. Posted on our website are:

OPA performance audits;

GovGuam financial audits, CCRs, and Board Commission meeting audios;

Procurement appeals’ filings and audios; and

OPA budget and expenditure reports, staffing patterns, and SOPs.

In CY 2018, our website averaged 2,328 visits per month, compared to CY 2017’s average of 2,037 per month. Measured according to unique IP addresses, the OPA website averaged 1,091 unique visitors per month, compared to CY 2017’s 827 per month. The OPA website averaged 5,686 page views compared to CY 2017’s average of 5,408 per month. OPA uses information technology to improve our processes and manage audits and procurement appeals.

Managing Audits with TeamMate Since October 2015, OPA has been using TeamMate audit management software for financial and performance audits. Many audit organizations are embracing automation with software for electronic work papers. The U.S. Department of Interior‐Office of Insular Affairs and several PASAI members are using TeamMate. Guam OPA is the only audit office in the Pacific using TeamMate for performance audits. TeamMate has added efficiencies to our audit processes such as:

Hyperlinking working papers to support conclusions;

Establishing working paper templates;

Streamlining quality assurance reviews; and

Managing audit time budgets.

Disclaimer: Guam OPA is not affiliated, connected, endorsed by, or officially associated with www.guamopa.org. Any content published, endorsed, or supported by www.guamopa.org is in no way affiliated with Guam OPA. The official website of Guam OPA is www.opaguam.org. Our email accounts using the domain @guamopa.org are no longer active. Please email employees using the domain @guamopa.com. We apologize for any inconvenience.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 21

Staffing Level Challenges As of December 2018, OPA had 13 full‐time staff and 8 vacancies. The current staffing is comprised of 11 auditors, 1 ASO, and the Public Auditor. More than a decade ago, in 2006, OPA had 18 full‐time staff in the unclassified service, which was the highest staff complement attained since the elected Public Auditor took office in 2001. Of the 11 auditors, five are Auditor IIIs/Accountability Auditor IIIs with an average of seven years of OPA service, two Accountability Auditor IIs with an average of five years of OPA service, and four Accountability Auditor Is/Auditor Is with an average of three years of OPA service. From CY 2012 through CY 2018, OPA lost 18 employees of which:

Three employees resigned and the employment of two probationary employees was discontinued because of overspending by the office;

11 professional staff left because of jobs offering $4K‐$23K more for annual salaries and better opportunities for professional career growth;

The pay received by 14 of the employees at their new positions is unknown; and

One of the employees laterally transferred to another agency. Staffing shortages due to difficulties with recruitment, compensation, promotion, and retention have challenged OPA for many years. In January 2017, P.L. 33‐226 gave OPA hiring autonomy. OPA was finally given much‐needed relief from years of inefficiencies in hiring under DOA’s Human Resource Division because of inadequate compensation and the lengthy hiring process.

Staff Qualifications The Public Auditor supports and encourages personal and professional development for OPA staff. All 13 OPA staff have Bachelor degrees and 10 staff are certified professionals or hold advanced degrees. Some staff holds multiple certifications:

2 CPAs;

2 CGFMs;

2 CGAP;

2 CICAs;

1 CFE;

1 MBA;

1 MPA; and

1 JD.

Of the 13 staff, four are currently pursuing a CPA or CGFM certification and one is an MAOL candidate.

Staff Development Auditors are required to maintain professional competence through 80 hours of continuing professional education (CPE) every two years. At least 24 CPE hours must be related to government auditing or the government environment (U.S. Government Accountability Office’s 2011 Government Auditing Standards). In addition, Guam law requires GovGuam to budget for

CY 2018 Objectivity • Professionalism • Accountability P a g e | 22

the required training for GovGuam accounting and auditing personnel (5 GCA §20304). In CY 2018, OPA auditors averaged 124 CPE hours each. OPA professional development is funded largely by technical assistance grants from the U.S. Department of the Interior’s Office of Insular Affairs (DOI‐OIA).

DOI‐OIA Training Grant In March 2015, OPA received a $76K training grant. OPA applied for and received another $76K training grant after using all prior grant funds at the end of FY 2017. We appreciate DOI‐OIA’s support for OPA and other APIPA members because it has allowed OPA to

Participate in the Department of the Interior’s Office of Inspector General (DOI‐OIG) programs;

Attend training seminars and conferences; and

Purchase various certification review materials. Since 2005, OPA sent several of its staff to intern at DOI‐OIG regional offices in Albuquerque, New Mexico; Denver, Colorado; Sacramento, California; and the Recovery Oversight Office in Herndon, Virginia. There was a four‐year pause in DOI‐OIG’s internship training from 2012 until the 2016 pilot of the Lakewood Experience.

DOI‐OIG’s Lakewood Experience In June 2018, auditors Ira Palero and Amacris Legaspi attended a two‐week training at the DOI‐OIG office in Lakewood, Colorado. They took part in a structured program that encompasses phases of audits. Unlike the prior internship program that other OPA staff attended, the Lakewood Experience consists of coaching by an OIG team leader, classroom training, and a case study with exercises covering various phases of a performance audit. This is the third time Guam OPA participated in the Lakewood Experience. Auditors Thyrza Bagana and Michele Brillante participated in 2016 and Christian Rivera and Andriana Quitugua participated in 2017.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 23

Professional Achievements Fifteen Years of Dedicated Service OPA’s Special Assistant Rodalyn Gerardo was recognized in January 2018 for 15 years of outstanding and dedicated service to OPA. She was the first OPA staff to reach this milestone. She began her audit career as one of OPA’s first UOG Accounting interns while completing her last semester at UOG. After earning her Bachelors in Business Administration, majoring in Accounting, in December 2002, OPA hired her as a staff auditor in January 2003. Since then, she successfully climbed OPA ranks, from Auditor I, Auditor II, Auditor III, Chief Auditor, and Special Assistant.

Five Years of Dedicated Service Two employees were recognized in CY 2018 for five years of outstanding and dedicated service. Auditors Thyrza Bagana and Michele Brillante have been with the OPA since 2013. Thyrza Bagana holds a Bachelor’s degree in Accounting from the University of San Jose Recoletos ‐ Philippines. She started as an Auditor I and worked her way up to her current position as an Auditor III. Prior to joining OPA, she

was in the banking industry as an Auditor I to Audit Senior Manager for 20 years and as Operations Head/Accountant for eight years. She earned her CGFM designation in 2018. Michele Brillante holds a Bachelor’s degree in Accounting from the University of Guam. She started as a UOG Accounting Intern in 2012 and joined OPA in June 2013. She became an Accountability Auditor II in December 2017.

Master of Business Administration In September 2018, Frederick Jones earned his Master of Business Administration degree with a specialization in Project Management from Grantham University. The program focused on the Project Management Institute’s Project Management Body of Knowledge Guide. Additional core studies included an overview and investigation of organizational behavior, ethics, and quantitative analysis. Completion of the degree pushes him another step closer to the goal of testing and acquiring the Project

Management Professional certification.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 24

Certified Government Financial Manager (CGFM) In CY 2018, Auditor III Thyrza Bagana and Accountability Auditor II Amacris Legaspi earned the CGFM designation after demonstrating competency in governmental accounting, auditing, financial reporting, internal controls, and budgeting at the federal, state, and local levels. The CGFM is a respected credential that recognizes the specialized knowledge and experience needed to be an effective

government financial manager.

Certified Public Accountant (CPA) Auditor I Ira Palero successfully completed the U.S. Certified Public Accountant examination. After passing her exam in September 2018, Ira earned her U.S. CPA professional designation in November 2018.

Conferences and Trainings In 2018, OPA staff attended various trainings with hosts such as the Graduate School USA, APIPA, PASAI, AGA, Association of Local Government Auditors (ALGA), International Organization of Supreme Audit Institutions (INTOSAI), Guam Society of CPA’s, and Ernst & Young LLP.

Professional Affiliations OPA is proudly affiliated with several professional organizations in the auditing and accounting profession, such as the PASAI, APIPA, ALGA, and AGA. In addition, some staff are members of other nationally recognized professional organizations, e.g., the American Institute of Certified Public Accountants (AICPA), the Institute of Internal Auditors, and the Association of Certified Fraud Examiners.

PASAI PASAI is a regional organization of 27 audit institutions in the Pacific who are aligned with the goals of the Pacific Plan to achieve stronger national development through better governance. Guam has been a member of PASAI since May 2006. Former Public Auditor Doris Flores Brooks attended the 18th PASAI Governing Board Meeting on February 2018 in Auckland, New Zealand.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 25

PASAI Trainings & Cooperative Audits For the past nine years, PASAI funded various trainings for several staff in performance auditing, cooperative audits, and other workshops.

In April 2018, Deputy Public Auditor Yuka Hechanova and Executive Secretary Llewelyn Terlaje attended the Strategy Planning Management and Reporting Workshop in Nuku’alofa, Tonga.

In April 2018, Special Assistant Rodalyn Gerardo and Auditor Vincent Duenas attended the SAIs Engaging with Stakeholders Strategy Review Meeting in Manila, Philippines.

In June 2018, Special Assistant Rodalyn Gerardo served as a facilitator for IDI‐SAI Engaging with Stakeholders Program. She attended the planning meeting in Uganda.

In July 2018, Executive Secretary Llewelyn Terlaje attended the IDI SAI Fighting Corruption Program Audit Review Meeting in Kathmandu, Nepal as a facilitator.

In November and December 2018, Public Auditor Benjamin Cruz and Auditor Jerrick Hernandez attended the IDI’s Strategy, Performance Measurement and Reporting (SPMR) Program – Operational Planning Workshop in Rorotonga, Cook Islands.

SAI Performance Measurement Framework INTOSAI developed a SAI PMF to assist SAIs in assessing their performance against the International Standards for Supreme Audit Institutions (ISSAIs) and other established international good practices for external public auditing. OPA’s first performance measurement review based on the SAI PMF culminated in January 2017 with a workshop on Guam hosted by PASAI. In May 2017, the Republic of Marshall Islands and PASAI’s Director of Practice Development independently assessed Guam. Similarly, Deputy Public Auditor Yukari Hechanova and Special Assistant Rodalyn Gerardo assessed the Federated States of Micronesia Office of the National Public Auditor in October 2017. Guam’s assessment was completed and submitted to OPA in February 2019.

APIPA APIPA is a regional organization that was founded by the audit organizations of five Pacific island nations, including Guam, and has since expanded to 12 Pacific island nation’s audit organizations. APIPA is made possible by the ongoing, generous support of DOI‐OIA. In August 2018, Deputy Public Auditor Yukari Hechanova and Auditors Thyrza Bagana, Frederick Jones, and Vanessa Valencia attended APIPA’s 29th Annual Conference in Koror, Palau, where the theme was Good Governance: Accountability, Ethics, and Transparency. The conference brought together auditors and finance officers throughout the Pacific including American

CY 2018 Objectivity • Professionalism • Accountability P a g e | 26

Samoa, the Commonwealth of the Northern Mariana Islands (CNMI), the Federated State of Micronesia (FSM), Guam, Kiribati, Pohnpei, Chuuk, Kosrae, RMI, Yap, and Palau.

APIPA Principals’ Meeting On October 31 and November 1, 2018, Guam hosted the annual APIPA Principal’s Meeting. The meeting discussed APIPA‐related matters, including upcoming peer reviews and the annual conference in Palau, among others. The APIPA principals also discussed the upcoming hosting of the 2019 conference and a request from Fiji to join the organization. The APIPA Principals also welcomed Guam’s new Public Auditor, Benjamin Cruz.

Association of Local Government Auditors (ALGA) ALGA is a national organization created to empower the local government auditing community through excellence in advocacy, education, communication, and collaboration to protect and enhance the public good while embracing diversity, equity, and inclusiveness. Guam is a member of ALGA.

OPA Auditors Accept Knighton Award In May 2018, Audit Supervisor Llewelyn Terlaje and Audit Staff Christian Rivera accepted the 2017 Knighton Award during the ALGA 30th Annual Conference in Colorado Springs, Colorado on behalf of OPA. OPA audit report, “Department of Public Works Village Streets Management Strategy,” won the Knighton Award in the extra‐large audit shop category. Judges complimented OPA’s winning audit report on its innovative use of a video to communicate audit findings, clear and evident audit message throughout the report, and excellent use of pictures and graphs. Llewelyn and Christian presented the audit report and showed the video during the conference. They also attended several audit courses during the conference. Part of this trip was paid for by ALGA.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 27

Association of Government Accountants (AGA) AGA is a nationally recognized professional membership organization focused on advancing government accountability, and of which our staff are proud members. Over the years, several held key leadership positions in the Guam Chapter Executive Committee. Advanced Executive Leadership Development Program (ELDP) In March 2018, Auditor III Vincent Duenas attended the Advanced Executive Leadership Development Program. Duenas was among the participants from former graduates from 2009, 2011, and 2013 from insular‐area governments including the Federated States of Micronesia (Yap, Pohnpei, Kosrae, and Chuuk), Palau, Commonwealth of the Northern Mariana Islands, Republic of the Marshall Islands, American Samoa, and Guam. The purpose of the Advanced ELDP meeting was to reenergize alumni of the first three ELDP cohorts as they advance their leadership values and actions. The three goals of the Advanced ELDP Session was to: (1) facilitate an informal network among alumni of the 2009, 2011, and 2013 classes, (2) develop individual leadership development plans that focus on self‐development, and (3) create and define island‐specific plans for advancing leadership projects and skills. The Advanced ELDP experience included leadership training, self‐assessments, guest speakers, and group project specific to our respective islands.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 28

Public Outreach and Community Service Important aspects of OPA’s Strategic Plan include protecting the independence of OPA, delivering quality audit reports that are timely and impactful, delivering timely decisions on procurement appeals, and effectively engaging with stakeholders to communicate and promote OPA's values and benefits. We participated in various community and outreach efforts such as Island Leadership Day, Junior Accountants Society (JAS) tours, DPR’s co‐ed volleyball league, manning the water station at the annual AGA 5K, and donating old newspapers to Feathers N’ Fins.

Island Leadership Day In April 2018, OPA participated in the DYA Island Leadership Day. Students from Santa Barbara Catholic School, Madel Sibal and Joshua Valencia, and Academy of Our Lady of Guam, Kohana Fejeran, observed firsthand experience of being a leader at OPA. The leaders for the day shadowed former Public Auditor Doris Flores Brooks and OPA management team Deputy Public Auditor Yuka Hechanova and Audit Supervisors Rodalyn Gerardo and Llewelyn Terlaje. They participated in various activities including attending financial audit meetings with GovGuam departments, sitting in an OPA management meeting, taking part in audit team updates, and ended the day with a staff meeting.

DPR’s Co‐ed Volleyball League From February to March 2018, the OPA joined in the Department of Parks and Recreation’s annual Co‐ed Volleyball League, Tano Division for the third year in a row. Our team, Net Assets, enjoyed a wonderful season of camaraderie and sportsmanship.

AGA 5K Water Station In June 2018, OPA staff assisted the AGA Guam Chapter’s Annual 5K run by manning one of the water stops. Aside from providing nourishment to the many runners and walkers, OPA provided them a boost by cheering them on as they made their way through the Hagatna course.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 29

Feathers N’ Fins Donation OPA donated newspapers to Feathers N’ Fins in June 2018. After years of accumulating newspapers, OPA made the wise decision to recycle them by donating them to Feathers N’ Fins to be used for cage lining for the store's pets waiting to be adopted.

OPA Bids Farewell to First Elected Public Auditor In June 2018, OPA staff and alumni hosted a luncheon for Doris Flores Brooks to commemorate her 18 years in public service as Guam’s first Chamorro CPA, first elected Public Auditor. Throughout her service to the people of Guam as Public Auditor, Doris Flores Brooks fought for transparency and accountability in our government. Her vision is for GovGuam to be a model for good governance in the Pacific. She pioneered OPA to what it is today, a model robust audit office. Doris Flores Brooks announced her resignation as Guam’s Public Auditor in May 2018 to run for the non‐voting delegate to the US House of Representatives.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 30

OPA Welcomes Second Elected Public Auditor On August 25, 2018, the voters of Guam elected Benjamin J.F. Cruz to serve as Public Auditor in a special election to complete the remainder of his predecessor’s term. Public Auditor Cruz was a former legal counsel to Governor Ricardo Bordallo and a former judge and justice in the Superior and Supreme Courts of Guam. Public Auditor Cruz has held key positions in the three branches of Government of Guam, and at the time of declaring his intent to run for Public Auditor, was serving as Speaker of the 34th Guam Legislature. Out of three candidates for the job, Cruz won a resounding vote of confidence from voters in the 2018 primary election. On September 13, 2018, the Honorable Chief Justice Katherine A. Maraman swore Cruz into office as Guam’s second‐elected Public Auditor. In his address, Public Auditor Cruz mentioned that he would endeavor to hold the Government of Guam fiscally responsible.

CY 2018 Objectivity • Professionalism • Accountability P a g e | 31

Appendix 1 Glossary of GovGuam Entities’ Acronyms

CLTC Chamorro Land Trust Commission

CQA Customs and Quarantine Agency

DCA Department of Chamorro Affairs

DLM Department of Land Management

DOA Department of Administration

DPR Department of Parks and Recreation

DPW Department of Public Works

DRT Department of Revenue and Taxation

DYA Department of Youth Affairs

GALC Guam Ancestral Lands Commission

GCC Guam Community College

GDOE Guam Department of Education

GEDA Guam Economic Development Authority

GGRF Government of Guam Retirement Fund

GHC Guam Housing Corporation

GHF Guam Highway Fund

GHURA Guam Housing and Urban Renewal Authority

GIAA Guam International Airport Authority

GMHA Guam Memorial Hospital Authority

GPA Guam Power Authority

GPT Guam Preservation Trust

GRTA Guam Regional Transit Authority

GSA General Services Agency

GSWA Guam Solid Waste Authority

GVB Guam Visitors Bureau

GWA Guam Waterworks Authority

IACS iLearn Academy Charter School

PAG Port Authority of Guam

KGTF Guam Educational Telecommunication Corporation (PBS Guam)

UOG University of Guam

CY 2018 Objectivity • Professionalism • Accountability P a g e | 32

Appendix 2 Page 1 of 2 OPA Financial Statements

CY 2018 Objectivity • Professionalism • Accountability P a g e | 33

Appendix 2 Page 2 of 2 OPA Financial Statements

CY 2018 Objectivity • Professionalism • Accountability P a g e | 34

Appendix 3 Page 1 of 2 APIPA Peer Review Report

CY 2018 Objectivity • Professionalism • Accountability P a g e | 35

Appendix 3 Page 2 of 2 APIPA Peer Review Report

CY 2018 Objectivity • Professionalism • Accountability P a g e | 36

Appendix 4 Page 1 of 4 Procurement Appeals Synopsis

Appeal No. OPA‐PA‐18‐001 Purchasing Agency: GMHA Appellant: JMI Edison

Appeal Relative To: Purchase, Installation, and Training of New CT Scanners

Value: $1.2M

Procurement Issue: Non‐conformance to IFB requirements JMI asserted that GMHA’s rejection of JMI’s bid on the ground that JMI’s bid did not meet the bid specifications was wrong. JMI requested that, as the lowest‐priced responsive offeror, JMI should be awarded the IFB.

Decision: Upheld. OPA determined that: (1) JMI’s procurement protest is sustained, (2) GMHA’s determination that JMI’s bid was non‐responsive was in error, (3) JMI was the lowest responsible and responsive bidder, and (4) JMI should be awarded the IFB.

Filed: January 16, 2018 Closed: June 29, 2018 Duration: 164 days

Appeal No. OPA‐PA‐18‐002 Purchasing Agency: DPW Appellant: Korando Corporation

Appeal Relative To: Bile/Pigua Bridge Replacement Project Value: $701K

Procurement Issue: Contract Dispute Korando alleged that: (1) DPW violated the Stipulation and Order, and breached the Korando Contract; and (2) DPW breached the implied covenant of good faith and fair dealing.

Dismissed. Dismissed after the parties signed a Stipulation Agreement.

Filed: January 16, 2018 Closed: February 2, 2019 Duration: 392 days

CY 2018 Objectivity • Professionalism • Accountability P a g e | 37

Appendix 4 Page 2 of 4 Procurement Appeals Synopsis

Appeal No. OPA‐PA‐18‐003 Purchasing Agency: DOA Appellant: TakeCare Insurance

Appeal Relative To: GovGuam Group Health Insurance Program Value: $‐

Procurement Issue: Restricted Competition TakeCare Insurance alleged that the GovGuam Health Insurance negotiation team included an invalid minimum requirement in the RFP that was inconsistent with and in violation of Guam law.

Dismissed. Dismissed without prejudice after parties signed a stipulation agreement.

Filed: May 4, 2018 Closed: November 5, 2018 Duration: 185 days

Appeal No. OPA‐PA‐18‐004 Purchasing Agency: GSA Appellant: Teleguam Holdings, LLC

Appeal Relative To: Telecommunication Services Value: $2.6M

Procurement Issue: Incomplete Procurement Record Teleguam Holdings alleged that: (a) its protest was timely, and (b) GSA’s proposed awards were based on a materially incomplete record and were contrary to Guam Law.

Decision: Upheld. OPA determined that Teleguam Holdings’ protest was timely and that the procurement record is materially incomplete. The revised proposed awards were in violation of the law and must be canceled.

Filed: July 26, 2018 Closed: January 29, 2019 Duration: 187 days

CY 2018 Objectivity • Professionalism • Accountability P a g e | 38

Appendix 4 Page 3 of 4 Procurement Appeals Synopsis

Appeal No. OPA‐PA‐18‐005 Purchasing Agency: DOA Appellant: TakeCare Insurance

Appeal Relative To: GovGuam Group Health Insurance Program Value: $‐

Procurement Issue: Non‐conformance to RFP requirements. In a supplemental to its original appeal, TakeCare Insurance alleged several issues regarding the RFP and GovGuam Insurance Negotiating Team to include conflict of issues, lack of voting sheet, improper communication, failure to conduct an investigation, violation of the automatic stay, and failure to maintain a complete procurement record. OPA consolidated this appeal to OPA‐PA‐18‐003.

Dismissed. Dismissed without prejudice after parties signed a stipulation agreement.

Filed: August 1, 2018 Closed: November 5, 2018 Duration: 96 days

Appeal No. OPA‐PA‐18‐006 Purchasing Agency: GDOE Appellant: Guam Cleaning Masters

Appeal Relative To: Custodial Services for Various Public Schools Value: $2.5M

Procurement Issue: Non‐conformance to IFB requirements Guam Cleaning Masters alleged that GDOE only used the lowest bid as the sole criteria in awarding the IFB and not the lowest and most responsible bidder.

Dismissal. Dismissed with prejudice after Guam Cleaning Masters filed a Notice of Withdrawal of Procurement Appeal.

Filed: September 5, 2018 Closed: October 24, 2018 Duration: 49 days

CY 2018 Objectivity • Professionalism • Accountability P a g e | 39

Appendix 4 Page 4 of 4 Procurement Appeals Synopsis

Appeal No. OPA‐PA‐18‐007 Purchasing Agency: DPW Appellant: Micronesia Renewable Energy

Appeal Relative To: Design‐Build of Photovoltaic System Value: $316K

Procurement Issue: Non‐conformance to IFB requirements Micronesia Renewable Energy alleged that DPW awarded to an unqualified, non‐responsive bidder.

Dismissed. Dismissed after Appellant failed to show up at the formal hearing.

Filed: November 26, 2018 Closed: February 25, 2019 Duration: 91 days

Appeal No. OPA‐PA‐18‐008 Purchasing Agency: GSA/DRT Appellant: Joeten Development, Inc.

Appeal Relative To: Office Space Lease for DRT Value: $1.4M

Procurement Issue: Bid Cancellation Joeten Development was the lone bidder for the IFB. GSA rejected their bid due to only one bid received.

Dismissed. Dismissed after parties signed a stipulation agreement.

Filed: December 11, 2018 Closed: December 31, 2018 Duration: 20 days

CY 2018 Objectivity • Professionalism • Accountability P a g e | 40

Appendix 5 Financial Audits

Agency OPA

Website Post Date

Internal Control over Financial Reporting

Single Audit (Compliance for Each Major Federal Programs) Management Letter Comments

OPA Recognition?

Opinion

Total Financial Reporting Findings

Opinion Total Federal

Award Expenditures

Total Questioned

Costs

Total Single Audit

Findings

Low‐Risk Auditee?

Deficiencies & Other Matters Over Financial Reporting

Information Technology

IACS 2/2/2018 Unmodified 0 n/a n/a n/a 0 n/a 2 0 No

GPT 3/18/2018 Unmodified 0 n/a n/a n/a 0 n/a 3 0 Yes

GIAA 3/29/2018 Unmodified 1 Unmodified $14,008,113 $‐ 1 Yes 4 0 n/a

GHC 3/30/2018 Unmodified 0 n/a n/a n/a 0 n/a 1 0 Yes

TAF 4/11/2018 Unmodified 0 n/a n/a n/a 0 n/a 0 0 No

GHF 4/13/2018 Unmodified 1 n/a n/a n/a 0 n/a 0 0 No

GVB 4/15/2018 Unmodified 0 n/a n/a n/a 0 n/a 4 0 Yes

PAG 4/23/2018 Unmodified 1 Unmodified $15,246,945 $‐ 0 No 6 4 n/a

GWA 4/25/2018 Unmodified 0 Unmodified $21,811,030 $‐ 0 Yes 2 7 n/a

GCC 4/26/2018 Unmodified 0 Unmodified $11,964,567 $‐ 0 Yes 0 0 n/a

PBS 4/27/2018 Unmodified 0 n/a n/a n/a 0 n/a 3 0 Yes

GPA 4/30/2018 Unmodified 0 n/a n/a n/a 0 n/a 4 7 No

CLTC 5/2/2018 Unmodified 1 n/a n/a n/a 0 n/a 4 0 No

GGRF 5/3/2018 Unmodified 0 n/a n/a n/a 0 n/a 0 0 Yes

GEDA 5/3/2018 Unmodified 0 n/a n/a n/a 0 n/a 2 0 No

GALC 5/10/2018 Unmodified 0 n/a n/a n/a 0 n/a 2 0 No UOG 5/14/2018 Unmodified 0 Unmodified $28,353,420 $‐ 1 Yes 5 0 n/a

GHURA 6/24/2018 Unmodified 1 Modified $42,185,617 $‐ 16 No 11 0 n/a

GSWA 6/26/2018 Unmodified 1 n/a n/a n/a 0 n/a 3 0 No

GOV‐WIDE

6/27/2018 Unmodified 1 Modified $288,800,695 $135,451 7 No 11 5 n/a

GDOE 7/2/2018 Unmodified 1 Unmodified $66,277,224 $32,260 2 No 6 4 n/a

GMHA 7/3/2018 Unmodified 1 Unmodified $1,296,219 $‐ 0 No 7 6 n/a

DCA 10/19/2018 Unmodified 5 n/a n/a n/a 0 n/a 3 0 No

Totals 14 $489,943,830 $167,711 27 83 33

CY 2018 Objectivity • Professionalism • Accountability P a g e | 41

Appendix 6 Hotline Tips Statistics

Agencies or Programs 2018 2017 2016 2001 to 2015

Total

Other Agencies and Programs 20 14 13 328 375

Department of Education 1 2 3 167 173

Department of Public Works 2 3 3 79 87

Guam International Airport Authority 0 0 0 73 73

Mayors Council of Guam 1 1 2 60 64

Department of Corrections 1 0 6 51 58

Guam Waterworks Authority 3 6 2 46 57

Guam Power Authority 1 0 0 55 56

Guam Memorial Hospital Authority 1 0 1 49 51

Department of Public Health and Social Services 1 14 2 31 48

Department of Administration 0 2 1 38 41

University of Guam 2 8 3 24 37

Office of the Attorney General 5 4 0 26 35

Guam Fire Department 0 3 1 29 33

Government of Guam Retirement Fund 0 0 0 30 30

Guam Housing and Urban Renewal Authority 0 1 0 29 30

General Services Agency 14 0 0 16 30

Guam Police Department 1 1 0 24 26

Department of Parks & Recreation 0 1 1 23 25

Guam Visitors Bureau 2 1 2 20 25

Superior Court of Guam 0 0 0 24 24

Guam Mass Transit Authority 0 1 1 21 23

Office of the Governor 0 1 1 19 21

Port Authority of Guam 1 0 0 20 21

Guam Telephone Authority 0 0 0 18 18

Department of Labor 1 1 0 16 18

Guam Economic Development Authority 0 0 0 13 13

Department of Land Management 0 1 0 10 11

Totals 57 65 42 1,339 1,503

CY 2018 Objectivity • Professionalism • Accountability P a g e | 42

Appendix 7 Organizational Chart as of December 31, 2018

CY 2018 Objectivity • Professionalism • Accountability P a g e | 43

Office of Public Accountability

2018 Annual Report July 2019

Key contributions to this report were made by: Vincent Duenas, Auditor III

Edlyn Dalisay, CPA, CGFM, Accountability Auditor III Benjamin J.F. Cruz, Public Auditor

Objectivity: To have an independent and impartial mind. Professionalism: To adhere to ethical and professional standards. Accountability: To be responsible and transparent in our actions.

The Government of Guam is a model for good governance with

OPA leading by example as a model robust audit office.

To ensure public trust and good governance in the Government of Guam,

we conduct audits and administer procurement appeals with

objectivity, professionalism, and accountability.

VISION

MISSION STATEMENT

CORE VALUES

REPORTING FRAUD, WASTE, AND ABUSE

Call our HOTLINE at 47AUDIT (472‐8348)

Visit our website at www.opaguam.org

Call our office at 475‐0390

Fax our office at 472‐7951

Or visit us at Suite 401, DNA Building in Hagåtña

All information will be held in strict confidence.

ACKNOWLEDGEMENTS