office market northern virginia - cresacresa.com/webfiles/dc/research/va market report q2...

TRANSCRIPT

1 | Northern Virginia | Offiice Market | Q2 2016

Office Market NORTHERN VIRGINIAQ2 2016

Federal Move Outs Throttle Occupancy Gains

Executive Summary

Technology tenants continued to expand their presence in Q2 2016,

signing five of the largest new leases totaling roughly 328K SF. Of note,

ScienceLogic took 62K SF in Reston, Opower finalized its new HQ lease

taking 45K SF at 2311 Wilson Blvd., and Amazon leased 52K SF in

Ballston. Rosslyn was popular among shared office concepts as Regus

took another 50K SF at 1101 Wilson Blvd., and Eastern Foundry signed a

19K SF lease at 1100 Wilson Blvd.

Although the tenant base in Northern Virginia is slowly diversifying, ongoing

contraction by the Federal government offset the occupancy gains in Q2

as five agencies vacated roughly 375K SF of space throughout the market.

Among those, the Environmental Protection Agency and the Federal

Supply Service consolidated and gave back roughly 250K SF of space

to the market. Despite sluggish fundamentals, investment sales activity is

robust, particularly outside the beltway along Metro’s Silver Line.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

8%

10%

12%

14%

16%

18%

20%

22%

-2.5 M

-2.0 M

-1.5 M

-1.0 M

-0.5 M

0.0 M

0.5 M

1.0 M

1.5 M

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average Vacancy Rate

Net Absorption

Economy

Northern Virginia outperforms MSA employment growth

Year-over-year employment growth in Northern Virginia fell in April 2016,

after four months of growth. Despite the down month, NoVA’s April

annualized job growth of 32,900 represents 46% of jobs added by the

MSA as a whole. NoVA also saw continued reduction in its unemployment

rate, which fell to 2.8%, the lowest level achieved in eight years.

Nationally, the economy is stabilizing following years of slow post-

recessionary recovery growth. The annualized national employment

growth rate (1.86%) has been on a gradual decline since January 2015,

and the unemployment rate has arrested at 5%. Despite a down month,

NoVa’s employment growth rate had been trending upward for the last

$28.50

$29.00

$29.50

$30.00

$30.50

$31.00

$31.50

$32.00

$32.50

$33.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average Asking Rent

Q2 Key Market Indicators

Total Vacancy

Net Absorption

Rental Rate

New Deliveries

YoYΔ Q2

20.0%

34,241 SF

$31.54

82,500 SF

2 | Northern Virginia | Offiice Market | Q2 2016

24 months, and has surpassed the national rate for the last 12 months.

Looking under the lens of office-use employment sector growth, NoVA

has been underachieving relative to national growth rates. NoVA is

only outperforming national growth in Membership Associations and

Organizations (3.4% NoVA to 1.0% USA) and State/Local Government

(1.1% NoVA to -1.7% USA).

Demand

Weak net demand despite increased activity

Tenant demand, influenced by Millennials in the workforce, is laser-

focused on Metro-accessible, amenity-rich product particularly along

the Silver Line. Along with Technology and financial services tenants,

there has been increased leasing activity from government contractors

due to a 5% and 3% increase in the DoD budget in 2016 and 2017,

respectively. However, traditionally strong submarkets located inside the

beltway, such as those in the R-B Corridor, have not seen a meaningful

reduction in vacancy since Sequestration in 2011. Crystal City is a

bright spot, but much of that demand has been generated by landlords

offering highly favorable concession packages and term buyouts. As

both government and businesses become more efficient with their real

estate footprint, space reductions upon renewal will persist into 2018.

Increasing concessions and public sector incentive packages are helping

to offset weakness in the leasing market, but greater economic expansion

in the private sector beyond current levels is necessary to drive down

vacancy. As new construction increases supply and weak demand keeps

vacancy rates in existing inventory elevated, tenants will continue to have

considerable leverage in lease negotiations.

Vacancy and Supply

New construction poses continued oversupply risk

After declining through much of 2015, Northern Virginia’s vacancy rate

has risen for the second consecutive quarter in 2016 and now stands

at 20.3%. Contrary to market-wide trends, where best-in-class assets

outperform commodity-driven properties, Class A vacancy has increased

to 21.7% compared to Class B vacancy, which has held relatively steady

and stands at 17.6%.

The level of new construction in Northern Virginia threatens to put further

pressure on the supply side given the lackluster absorption figures

since 2010. Preleasing in multi-tenant spec buildings has been slow,

as evidenced by the delivery of 1775 Tysons Boulevard in Q2 2016 only

40% leased. Commonly used preleasing figures take into consideration

owner-occupied projects such as the 975K SF Capital One HQ and the

340K SF MITRE building, but those projects were never available for lease

from the onset. Upon completion, Capital One in particular will vacate a

considerable amount of leased space in Northern Virginia, contributing to

increased vacancy and further weakness in the market.

Net Absorption by County

Unemployment Rate NoVa

Employment Growth by Month NoVa

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

April 2011 April 2012 April 2013 April 2014 April 2015 April 2016

DC MSA

(20,000)

-

20,000

40,000

60,000

80,000

100,000

MSA

-300 K

-200 K

-100 K

0 K

100 K

200 K

300 K

400 K

Alexandria County Arlington County Fairfax County Loudoun County

Q2 YTD

3 | Northern Virginia | Offiice Market | Q2 2016

Market Outlook

Consolidations by the Federal government and private companies

continue to throttle office market fundamentals. Overall job

creation is outpacing the national growth rate, but office-using

employment is slowing in key sectors necessary to facilitate

an improvement in occupancy rates. Demand remains muted

and hyper focused on a select number of product types and

submarkets, leaving much of Northern Virginia with a substantial

oversupply. Record concession packages are becoming the new

normal in order to win business, so tenants looking to reduce

occupancy costs have numerous options across all property

types and locations.

Building Submarket Size Sale Price Price (PSF) Buyer

1735 N Lynn Street Rosslyn 293,539 $106,500,000 $362.81 MeridianGroup

1110 N Glebe Road Ballston 233,929 $79,000,000 $337.71 NGP V

Management LLC

2000 N 14th StreetClarendon/Courthouse

114,843 $43,000,000 $374.42 Penzance

196 Van Buren Street Herndon 100,103 $22,132,157 $221.09 Goldman

Sachs

198 Van Buren Street Herndon 101,169 $22,367,843 $221.09 Goldman

Sachs

Tenant Submarket Size Type

GSA: TSA Pentagon City (2 locations) 551,916 Renewal

TEGNA Inc. Tysons Corner 70,227 Prelease

ManTech Route 28 South 59,958 Renewal

ScienceLogic Reston 33,743 New

Exostar LLC Herndon 28,388 New

Q2 Top Leases

Q2 Top Sales

Rental Rates

Record concessions mask falling rents

Asking rents for direct space decreased $0.06 from Q2 2015 to $31.64/

SF. Class A rents ticked down $0.29 to average $32.93 while Class B

rents fell $0.23 to $28.33/SF. Best-in-class assets in core submarkets are

commanding rents in the $50-55/SF range. Although rent growth been flat

to slightly negative since 2011, record concession packages have made

high-quality office space much more affordable for occupiers.

Muted touring activity combined with substantial oversupply has

caused landlords to become more aggressive to win business. In select

submarkets, tenant improvement allowances of $85-125/SF with 1.5-2

months of free rent per year of term have been achieved. In addition to TI

and abatement, it is becoming increasingly common for landlords to buy

out the existing lease liability in order to entice early relocations. Landlords

are very interested in keeping pro-forma rents stable so their property’s

valuation is not impacted by the soft market. Property values are directly

related to in-place cash flows and often do not take into consideration

concession dollars spent to get leases signed. This enables tenants

with considerable term remaining to take advantage of favorable market

conditions to lower occupancy costs.

4 | Northern Virginia | Offiice Market | Q2 2016

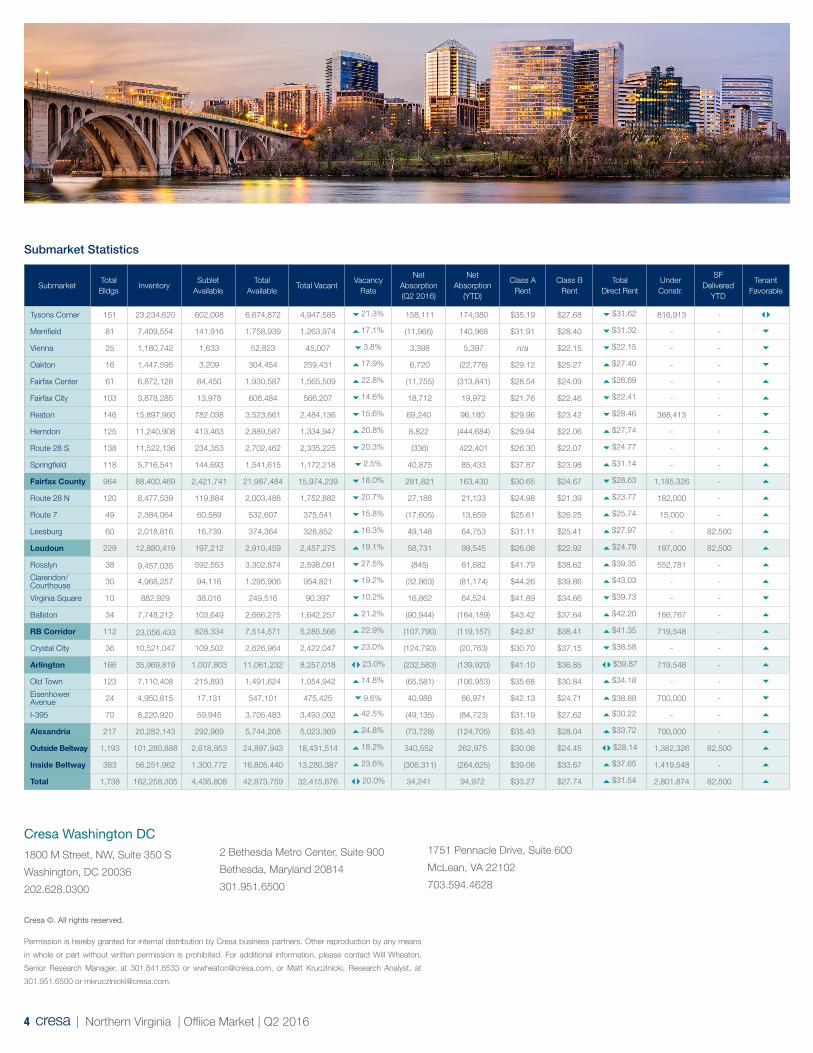

SubmarketTotal Bldgs

InventorySublet

AvailableTotal

AvailableTotal Vacant

Vacancy Rate

Net Absorption (Q2 2016)

Net Absorption

(YTD)

Class A Rent

Class B Rent

Total Direct Rent

Under Constr.

SF Delivered

YTD

TenantFavorable

Tysons Corner 151 23,234,620 602,008 6,674,872 4,947,585 21.3% 158,111 174,380 $35.19 $27.68 $31.62 816,913 -

Merrifield 81 7,409,554 141,916 1,758,939 1,263,974 17.1% (11,966) 140,968 $31.91 $28.40 $31.32 - -

Vienna 25 1,180,742 1,633 52,823 45,007 3.8% 3,398 5,397 n/a $22.15 $22.15 - -

Oakton 16 1,447,595 3,209 304,454 259,431 17.9% 6,720 (22,776) $29.12 $25.27 $27.40 - -

Fairfax Center 61 6,872,128 84,450 1,930,587 1,565,509 22.8% (11,755) (313,841) $28.54 $24.09 $26.69 - -

Fairfax City 103 3,878,285 13,978 608,484 566,207 14.6% 18,712 19,972 $21.76 $22.46 $22.41 - -

Reston 146 15,897,960 782,038 3,523,661 2,484,136 15.6% 69,240 96,180 $29.96 $23.42 $28.46 368,413 -

Herndon 125 11,240,908 413,463 2,889,587 1,334,947 20.8% 8,822 (444,684) $29.94 $22.06 $27.74 - -

Route 28 S 138 11,522,136 234,353 2,702,462 2,335,225 20.3% (336) 422,401 $26.30 $22.07 $24.77 - -

Springfield 118 5,716,541 144,693 1,541,615 1,172,218 2.5% 40,875 85,433 $37.87 $23.98 $31.14 - -

Fairfax County 964 88,400,469 2,421,741 21,987,484 15,974,239 18.0% 281,821 163,430 $30.65 $24.67 $28.63 1,185,326 -

Route 28 N 120 8,477,539 119,884 2,003,488 1,752,882 20.7% 27,188 21,133 $24.98 $21.39 $23.77 182,000 -

Route 7 49 2,384,064 60,589 532,607 375,541 15.8% (17,605) 13,659 $25.61 $26.25 $25.74 15,000 -

Leesburg 60 2,018,816 16,739 374,364 328,852 16.3% 49,148 64,753 $31.11 $25.41 $27.97 - 82,500

Loudoun 229 12,880,419 197,212 2,910,459 2,457,275 19.1% 58,731 99,545 $26.06 $22.92 $24.79 197,000 82,500

Rosslyn 38 9,457,035 592,553 3,302,874 2,598,091 27.5% (845) 61,682 $41.79 $38.62 $39.35 552,781 -

Clarendon/Courthouse 30 4,968,257 94,116 1,295,906 954,821 19.2% (32,863) (81,174) $44.26 $39.86 $43.03 - -

Virginia Square 10 882,929 38,016 249,516 90,397 10.2% 16,862 64,524 $41.89 $34.66 $39.73 - -

Ballston 34 7,748,212 103,649 2,666,275 1,642,257 21.2% (90,944) (164,189) $43.42 $37.64 $42.20 166,767 -

RB Corridor 112 23,056,433 828,334 7,514,571 5,285,566 22.9% (107,790) (119,157) $42.87 $38.41 $41.35 719,548 -

Crystal City 36 10,521,047 109,502 2,626,964 2,422,047 23.0% (124,793) (20,763) $30.70 $37.15 $38.58 - -

Arlington 166 35,969,819 1,007,803 11,061,232 8,257,018 23.0% (232,583) (139,920) $41.10 $36.85 $39.87 719,548 -

Old Town 123 7,110,408 215,893 1,491,624 1,054,942 14.8% (65,581) (106,953) $35.68 $30.84 $34.18 - -

Eisenhower Avenue 24 4,950,815 17,131 547,101 475,425 9.6% 40,988 66,971 $42.13 $24.71 $38.88 700,000 -

I-395 70 8,220,920 59,945 3,705,483 3,493,002 42.5% (49,135) (84,723) $31.19 $27.62 $30.22 - -

Alexandria 217 20,282,143 292,969 5,744,208 5,023,369 24.8% (73,728) (124,705) $35.43 $28.04 $33.72 700,000 -

Outside Beltway 1,193 101,280,888 2,618,953 24,897,943 18,431,514 18.2% 340,552 262,975 $30.06 $24.45 $28.14 1,382,326 82,500

Inside Beltway 383 56,251,962 1,300,772 16,805,440 13,280,387 23.6% (306,311) (264,625) $39.06 $33.67 $37.65 1,419,548 -

Total 1,738 162,258,305 4,435,808 42,873,759 32,415,676 20.0% 34,241 94,972 $33.27 $27.74 $31.54 2,801,874 82,500

Submarket Statistics

Cresa ©. All rights reserved.

Permission is hereby granted for internal distribution by Cresa business partners. Other reproduction by any means

in whole or part without written permission is prohibited. For additional information, please contact Will Wheaton,

Senior Research Manager, at 301.841.6533 or [email protected], or Matt Kruczlnicki, Research Analyst, at

301.951.6500 or [email protected].

Cresa Washington DC

1800 M Street, NW, Suite 350 S

Washington, DC 20036

202.628.0300

2 Bethesda Metro Center, Suite 900

Bethesda, Maryland 20814

301.951.6500

1751 Pennacle Drive, Suite 600

McLean, VA 22102

703.594.4628