oecd review of the ppp governance framework in the united-kingdom: preliminary results

TRANSCRIPT

OECD REVIEW OF THE PPP

GOVERNANCE FRAMEWORK

IN THE UNITED KINGDOM:

PRELIMINARY RESULTS

Annual Meeting of Senior PPP and

Infrastructure Officials 23-24 MARCH, 2015

Paris, France

Ian Hawkesworth Head, Capital Budgeting and PPPs Budgeting and Public Expenditures Division Public Governance and Territorial Development Directorate, OECD

1

The OECD’s PPP Principles (2012) fall under three

main headings:

1. Establishing a clear, predictable and legitimate

institutional framework.

2. Grounding the selection of Public-Private

Partnerships in Value for Money.

3. Using the budgetary process transparently to

minimize fiscal risks.

2

Framework for analysis

In 2012, the UK introduced a new

private finance scheme : PF2

3

Some key characteristics of PF2 :

• Strengthened partnership through public equity stake in SPVs

• Greater flexibility through the exclusion of ‘soft’ services from contracts

• Faster and cheaper procurement through a new ambitious timetable (18 months)

• Improved VfM through more appropriate risk retention by the public sector

• Greater transparency through:

– New control total for PFI/PF2 commitments (GBP 70 billion until 2020)

– Private sector equity return information to be published

– New business case approval tracker available

• Introduction of funding competitions for a part of private sector equity to attract long term investors

1. THE INSTITUTIONAL FRAMEWORK

4

The UK possesses a comprehensive institutional

suite to manage capital investments

- Treasury approvals Points (TAPs) for PPP appraisals

- Spending/budget department

- Public policy

- Planning, prioritisation and enabling of infrastructure investment in the UK

- Includes the PPP policy team (PPP unit), strategy team (NIP), etc.

-Supreme audit institution

- ex-post reporting on PPP projects and processes

- Include sub-national governments, line Departments, and executive agencies (ex Highways Authority)

- Responsible of PPP from planning to exit

- Part of ERG - Assurance process (incl. Gateway Review)

- Commercial and operational support to Departments

- Department for Communities and Local Government

- Scottish Futures Trust

- Local Partnerships

5

HM Treasury

Contracting Authorities

Infrastructure UK (IUK)

National Audit Office

Major Projects

Authority

Others

Principle 1: Ensure public awareness of the relative costs,

benefits and risks of PPPs as part of an integrated public-sector

infrastructure investment framework.

• The UK National Infrastructure Plan and the Top 40 is a process and document well designed to ensure prioritisation, transparency and linkages (see principle 4).

• Several mechanisms are in place to disclose commitment and potential liabilities from PFI/PF2 contracts such as the Whole of Government Accounts (WGA) and the Office of Budget Responsibility (OBR)

• Broad public and private consultation about the limits of PFI leading up to PF2 adoption

• The National Audit Office (NAO) plays a key role in informing the public debate about PFIs

Transparency and open communication about the relative costs, benefits and risks of PFIs is evident in the UK

6

Principle 2: Key institutional roles and responsibilities should

be maintained, and there are clear mandates and sufficient

resources to ensure a prudent procurement process.

• HM Treasury’s Infrastructure UK (IUK) is well capacitated and its different units regularly advise the public sector with regards to the appropriateness of PFIs

– Strengthened commercial capacity of IUK and other institutions

• A wide range of institutional support is available to contracting authorities at the central level (IUK, MPA) and at the devolved level (ex: SFT, LP).

• Public sector capacities are well established, complementary, and roles clearly defined.

• Capacity to prepare, procure, and manage projects at the local level can still be enhanced.

The institutional set up and public sector capabilities for PFIs and capital projects generally are clear and coherent.

7

Principle 3: Ensure that all significant regulation affecting the

operation of Public-Private Partnerships is clear, transparent

and enforced.

• A constantly evolving framework of gradual adjustment and refinement e.g. refinancing gains.

• There is no specific PPP law in the UK, but the government follows contract law and EU procurement directives.

• No issues raised with regards to the regulatory framework of PPP contracts (legal issues, enforcement, or other aspects).

• Steps have been taken to further strengthen the regulation of PFI/Pf2 contracts

– more centralized procurement is emphasized under PF2

– new standardized suite of documentation issued

Rules affecting contracts are clear and enforced in the UK.

8

2. ENSURE VALUE FOR MONEY

9

Principle 4: All investment projects should be prioritised at senior

political level.

• The UK National Infrastructure Plan (NIP) was put in place since 2010 and

– presents a global government vision with respect to infrastructure development in the UK.

– lays out the strategic need for investment in the UK.

– creates transparency about the project pipeline and priority investments in order to show that there is an ongoing market.

– ensures delivery progress by measuring and publishing reports on developments.

• The ‘Top 40’ list of projects on the NIP has been developed in an iterative process with the line Departments, HM Treasury and the Cabinet office.

The NIP and its ‘Top 40’ is a good example of a cabinet sanctioned priority process for projects.

10

Principle 5: Carefully investigate which investment method is

likely to yield most value for money.

• The UK Green Book provides comprehensive guidance for the appraisal of all projects receiving central funding.

• The business case is structured around 5 aspects to ensure that projects are:

– supported by a robust argument for change – the Strategic Case;

– optimise Value for Money – the Economic Case;

– commercially viable (where relevant) – the Commercial Case;

– is financially affordable – the Financial Case; and,

– can be delivered successfully – the Management Case.

• The centrally developed value for money test (PSC) was removed in favor of contracting authorities developing their own quantitative evaluation of projects as an integral part of the business case

– The PSC tool was never intended as a “pass-or-fail” test, but it created a tendency to over-focus attention on the numerical result of the exercise

• Three stages of business case approval by HM Treasury: Strategic Outline Business Case, Outline Business Case, and Full Business Case (see table)

A level playing field exists for the appraisal, comparison, and selection of the delivery mode of projects in the UK via the Green Book.

11

The appraisal and evaluation of projects is

complemented by an independent gateway

review process

12

Source: Cabinet Office & HM Treasury (2011), Major Project approval and assurance guidance, April 2011

Table: Stages of Treasury Approval Points Treasury Approval Point

(TAP)

Scope and timing How does the TAP relate to

MPA approval

Strategic Outline Business

Case (SOBC) - Project

initiation stage

- All new Major Projects to ensure

strategic fit, value for money and

deliverability.

- Approval required before any public

commitment is made.

Preceded by at least one of

the following:

● Starting Gate

● Gateway Review 1

● Project Assessment Review

(PAR)

Outline Business Case (OBC)

- Pre-market stage

- All Major Projects to assess all

options in detail.

- Approval required before going to

the market

Preceded by at least one of

the following:

● Gateway Review 2

● PAR

Full Business Case (FBC) -

Pre-final negotiation

stage

- All Major Projects pre-spending

commitments

Approval required before finalising

commercial contracts.

- For projects using competitive

dialogue as a procurement route,

approval required before close of

dialogue.

Preceded by at least one of

the following:

● Gateway Review 3

● PAR

Principle 6: Define, identify, measure and transfer the risks to

those that manage them best (at the least cost).

• Standardised contracts in the UK provide a sound basis

for the allocation of generic risk in a PFI project.

• An evolutionary process.

• The PF2 consultation process highlighted that a greater

retention of risk by the public sector (ex: utility

consumption risk) could further improve the VfM of

contracts

Greater risk retention by the public sector might improve

VfM.

13

Principle 7: The procuring authorities should be prepared for

the operational phase of the Public-Private Partnerships.

• Ongoing initiatives (ex. MPLA) to strengthen the capacity of project managers to maintain the performance of projects over time

• Ongoing operational savings program to implement savings measures in ongoing projects (in 2013, 118 projects reported savings of GBP 1.6 billion)

• The NAO reviews individual PFI projects, draws useful lessons, and offers suggestions on how to cut cost and improve efficiency

• Ex-post evaluation of projects and systematic data collection for comparison purposes might be enhanced.

Preliminary evidence suggests that performance has been good in terms of on-time and on-budget delivery of PFI assets

14

Principle 8: Value for money should be maintained when

renegotiating.

• A 2008 study found that the monetary impact of

changes to contracts was minimal for projects that were

renegotiated (1.1 % increase in unitary charges)

• Infrequent cases of high impact renegotiations of

infrastructure PFIs (ex: Channel Tunnel Rail Link)

• Some renegotiations shown to have brought significant

savings to projects (NAO 2013)

On balance, contract renegotiations do not appear to be

an issue in the UK

15

Principle 9: Government should ensure there is sufficient

competition in the market.

• Decades-long pipeline and substantial industry has

developed the relevant expertise and skills to furnish

sufficient bids to ensure the basis for a competitive

market process

• General issue that may also affect PFI projects:

sometimes, complex and mega projects may not have

enough bidders (e.g. nuclear energy)

The UK market is open and vigorous in term of

engineering, construction and financial companies

16

• The argument for pursuing the PFI the UK is

premised on increasing value for money

• In addition, developing a viable private sector

delivery modality to challenge then

prevailing public sector approaches may

have played a role

• As may the then off budget accounting

treatment.

17

3. THE BUDGET PROCESS

18

Principle 10: The Central Budget Authority should ensure that the

project is affordable and the overall investment envelope is

sustainable.

• Spending Reviews set a medium term expenditure framework, with firm spending limits for line Departments

• Specific approval procedures for major investment decisions such as PFI/PF2 contracts (HMT TAPs)

• The Office of Budget Responsibility helps the government keep track of the fiscal sustainability of its expenditures

• Control caps: new control total of GBP 70 billion for PFI/PF2 projects up to 2020; limit in place for capital expenditures in Scotland.

HM Treasury spending teams work closely with IUK, the Office of Budget Responsibility, contracting authorities, and other institutions to ensure the affordability and fiscal sustainability of projects within the overall budgeting framework.

19

Principle 11: The project should be treated transparently in the

budget process. The budget documentation should disclose all

costs and contingent liabilities.

• The Whole of Government Accounts (WGA) provides a comprehensive

overview of PFI commitments over the long term, as well as quantifiable

and non-quantifiable information on contingent liabilities.

• Practically all PFIs are on balance sheet in the WGA under IFRS

standards (based on the “control” criterion; also followed by departmental

accounts).

• Individual Departments also required to report contingent liabilities to

Parliament

• Despite the WGA, there can still be an accounting incentive to use PFI,

but this stems mainly from compliance with Eurostat rules (“risk and

rewards” criterion).

There is a strong suite of tools to transparently account for PFI

commitments and contingent liabilities in the UK, regardless of classification 20

The WGA provides a comprehensive

overview of future PFI payments

21

Source: Office for Budget Responsibility (2014), Fiscal Sustainability Report 2014.

Table: Whole of Government Accounts data for total future costs of PFI deals

Principle 12: Government should guard against waste and

corruption by ensuring the integrity of the procurement process.

• Potential conflict of interest from PF2 mitigated by creation of the public equity team in IUK, but too early to judge

• Procurement identified by government as an area of improvement: new tools for simplified, more streamlined procurement procedures (ex: Procurement Routemap)

• PFI/PF2 Tracker newly in place to provide more transparency on the business case process

• Procurement skills sometimes limited at the sub-national level

• Capacity building to strengthen procurement skills of public officials (ex: training on Lean Sourcing principles)

Public procurement displays integrity and discipline, and can further be strengthened.

22

CONCLUSIONS

• More than 20 years of experience with PFI have brought the

government lessons and improvements with respect to all forms of

infrastructure procurement and life-cycle management, such as

discipline in cost control.

• The framework for private finance is still evolving in the UK, but

important lessons have been learned and reforms introduced as

part of PF2.

• There is a positive outlook from both the public and private sectors

about the new model, but …

23

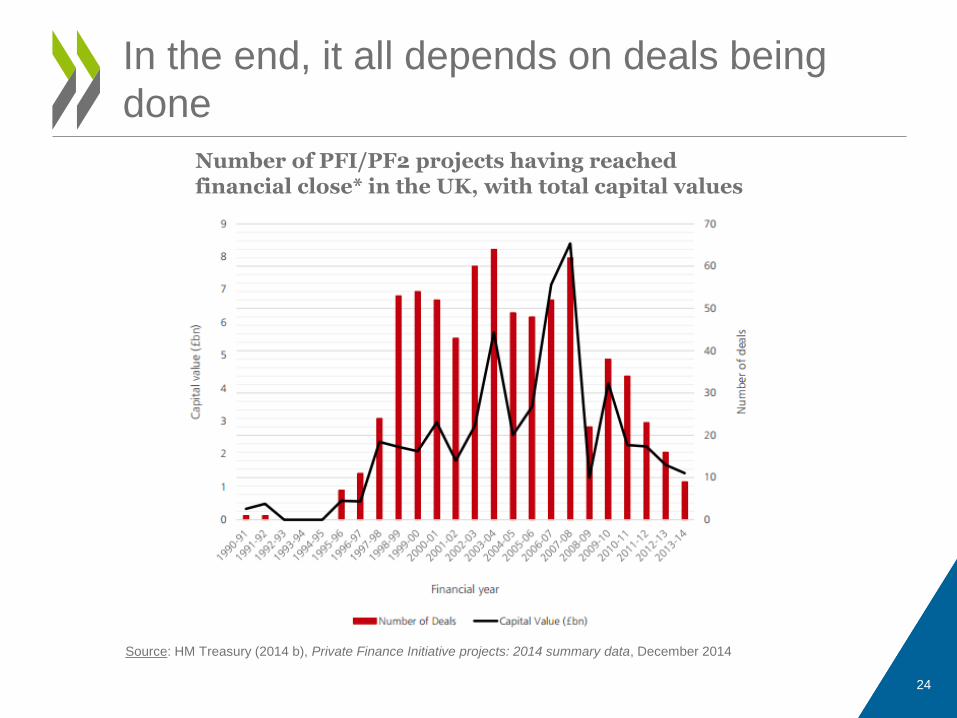

In the end, it all depends on deals being

done

24

Source: HM Treasury (2014 b), Private Finance Initiative projects: 2014 summary data, December 2014

Number of PFI/PF2 projects having reached financial close* in the UK, with total capital values

For more information: www.oecd.org/gov/budgeting/ppp.htm

25