oecd project on institutional investors and long term investment - raffaele della croce, oecd

TRANSCRIPT

OECD PROJECT ON INSTITUTIONAL

INVESTORS AND LONG TERM

INVESTMENT

Raffaele Della Croce

Lead Manager, LTI Project,

Financial Affairs Division - OECD

1. The Demand for LT Assets - Large Pension Fund Survey

2. Attracting Private Finance in Infrastructure - Matching Supply and Demand

3. Taxonomy of Instruments for LTI

4. OECD work on Long Term Investment

2

Contents

The Demand for Long Term

Investment

Role of Institutional Investors

3

Role of Institutional Investors

4

Inst Investors AUM have been growing to USD 92tr AUM in

OECD countries [in EM approx USD5tn AUM]

Assets held by Institutional Investors in the OECD, 2001-2013 (USD Tn)

Source: OECD Global Pension Statistics, Global Insurance Statistics and

Institutional Investors’ Assets databases, and OECD estimates.

Trends in Asset Allocation – Large

Pension Fund Survey 2014

5

Over 70 funds for USD10tn AUM : Trends in Alternatives, overall

limited investment in infrastructure with exceptions (i.e.

Australia & Canada)

Source: OECD

Fixed income and cash 52%

Listed equity 31%

Unlisted Infrastructure

2%

Other Alternatives

15%

LPFs

Fixed income and cash 55%

Listed equity 30%

Unlisted Infrastructure

1%

Other Alternatives

14%

PPRFs

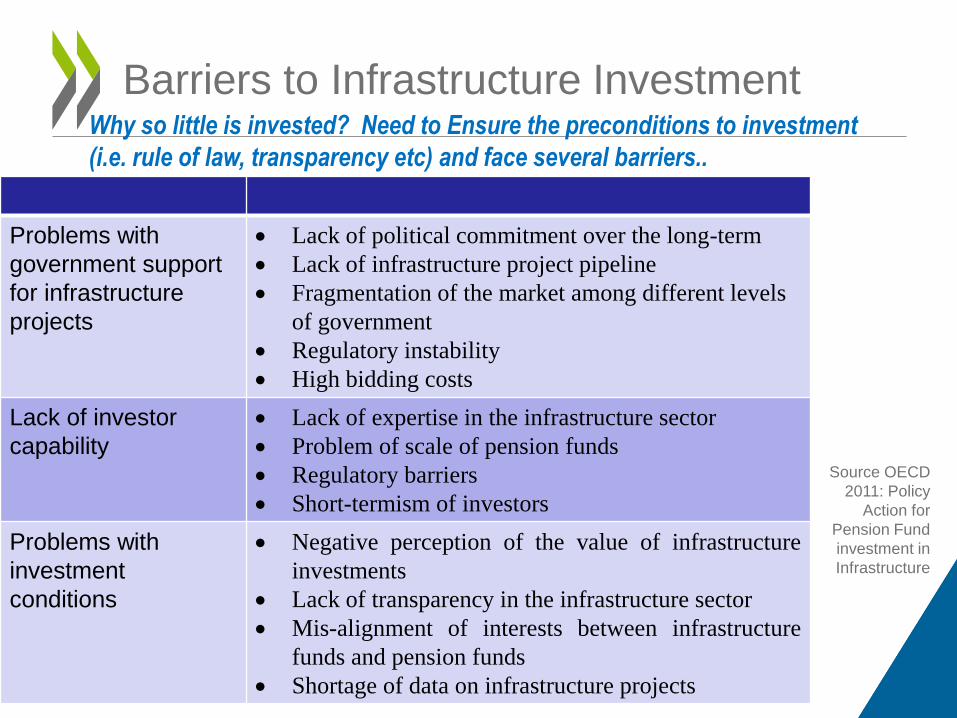

Barriers to Infrastructure Investment

Source OECD

2011: Policy

Action for

Pension Fund

investment in

Infrastructure

Problems with

government support

for infrastructure

projects

Lack of political commitment over the long-term

Lack of infrastructure project pipeline

Fragmentation of the market among different levels

of government

Regulatory instability

High bidding costs

Lack of investor

capability

Lack of expertise in the infrastructure sector

Problem of scale of pension funds

Regulatory barriers

Short-termism of investors

Problems with

investment

conditions

Negative perception of the value of infrastructure

investments

Lack of transparency in the infrastructure sector

Mis-alignment of interests between infrastructure

funds and pension funds

Shortage of data on infrastructure projects

Why so little is invested? Need to Ensure the preconditions to investment

(i.e. rule of law, transparency etc) and face several barriers..

Attracting long term

investment in infrastructure

Matching Supply and Demand

7

Attract Private Finance to Close the

Financing Gap

• The Business Climate: need to establish stable and predictable political environment [the OECD Investment Policy Review, Anti Bribery work]

• Governance of Infrastructure: Standardized legal PPP framework (i.e. independent regulatory institutions, transparent tendering process, coherent regulatory design) [OECD Senior PPP Official Network]

• Bankability of projects: promoting investable projects engaging the investors [OECD Development of Infrastructure as an asset Class/ LTI Network]

– Adequate Risk/return profiles

– Appropriate financial instruments

– Information gap

8

Policy Initiatives: the EU Investment Plan, US Build

America Investment Initiative

Leveraging Private Sector Capital: Policy

Role

9

Risk transfer: What are the risks (Project/Market)? Who is best

positioned to take those risks (public/private, banks inst. Investors)?

Ultimate goal is to

optimize risk allocation

to reduce costs of

financing

Matching Supply and Demand: Development

of Infrastructure as an Asset Class

10

Infrastructure as an Asset Class: A different risk profile will imply

different expected returns from investors

Source: OECD 2014 Policy Initiative: G20 Global Infrastructure HUB

Taxonomy of Instruments to

attract Long Term Investment

In Infrastructure

Investing in the Real Economy

11

BACKGROUND TO THE TAXONOMY

12

Background: Taxonomy of instruments and

incentives for infrastructure

• Taxonomy part of G20 mandate to the OECD to prepare an Analysis of Government and Market Based Incentives for LTI (2013 Feb G20 communique)

• Analysis developed in 2014-15 under the Australian and Turkish G20 presidencies through G20 Investment & Infrastructure (IIWG) & G20/OECD LTI Taskforce, including IOs (WB, IMF, FSB, UN)

13

G20 mandate to the OECD..

Taxonomy - Objective

• Objective of the taxonomy is to create an agreed framework to better understand the wider financing landscape for infrastructure, particularly the relationship of the different flows and types of finance and allow the development of infrastructure as an asset class, in order to leverage private sector capital – in particular institutional investors involvement.

• The taxonomy will also develop a framework for categorizing the risks related to infrastructure projects, match them with available risk mitigation instruments and identify where gaps between the supply and demand for risk mitigation continue to impede investment.

14

What are the investment options available to private investors? What their

risks/returns? Which instruments and incentives to attract the private sector?

What kind of innovative financial instruments should be developed? What is the

role for policy makers?

TAXONOMY STRUCTURE

15

Taxonomy PART I: Mapping infrastructure

investment channels

16

Source OECD

Asset Category Instrument Capital Pool

Corporate Balance

Sheet /

Other Entities

Infrastructure

Project

Debt

Bonds Bond Funds, Bond

Indices

Corporate Bonds,

Green Bonds

Project Bonds

Municipal

Bonds/Revenue

Bonds

Subordinated Bonds Green Bonds/Sukuk

Loans

Debt Funds

Direct/Co-investment

lending to

infrastructure

corporate

Direct/Co- Investment

lending to

Infrastructure project /

project loans Securitised Loans,

Syndicated Loans,

CLOs

Syndicated Loans

Mixed Hybrid Mezzanine debt funds Subordinated Bonds,

Convertible Bonds

Subordinated Loans,

Mezzanine Finance

Equity Listed

Listed

infrastructure

equity funds,

Indices, trusts

Listed infrastructure &

utilities stocks YieldCos, Closed-

end Funds MLPs, REITs, IITs

Unlisted Unlisted

infrastructure

funds

Direct/Co-investment

in infrastructure

corporate equity

Direct/Co-investment

in infrastructure

project equity

Low Risk/ Return Low Risk/ Return Medium Risk/

Return

High Risk/ Return

Bonds Alternative debt “Hybrid”

instruments

Equity

instruments

Government /

municipal bonds

Corporate bonds

Project bonds

Green bonds

/Sukuk

Securitised debt

Debt funds

Direct

lending/Co-

invest

Subordinated

debt

Mezzanine

finance

Listed equity

stocks and funds

Unlisted funds

Direct/Co-

investment

17

Taxonomy PART I: Alternative Financing

Techniques for Infrastructure

Across the Risk/Return Spectrum..

Source OECD

18

Risk

Categories

Political

and

regulatory:

Project feasibility and

inclusion in investments

plan*

Land availability

Change in service tariff, defined by the

regulator/authority

Changes in tariff regulation

Longer bidding phase and

consequent change of

market conditions*

Social acceptance

Authority doesn’t comply with

payment obligations

Termination value different from

expected

Change in taxation

Change in law

Stability of business and legal environment

Macro-

economic

and

market

Land availability Volatility of demand

Availability of affordable funding Refinancing risk

Inflation

Exchange rate fluctuation

Force Majeure

Stability of business and legal environment

Default of operators/SPV

Termination value different from expected

Technical

Quality of project development

Reliability of forecasts for

construction costs and

delivery time

Underperformance of the

infrastructure, which may cause

increase of life cycle costs or further

investments Archaeological Environmental

Technology availability and consistency

Taxonomy Part II: Classification of risk linked to Infra Projects

Development Phase Construction Phase Operation Phase

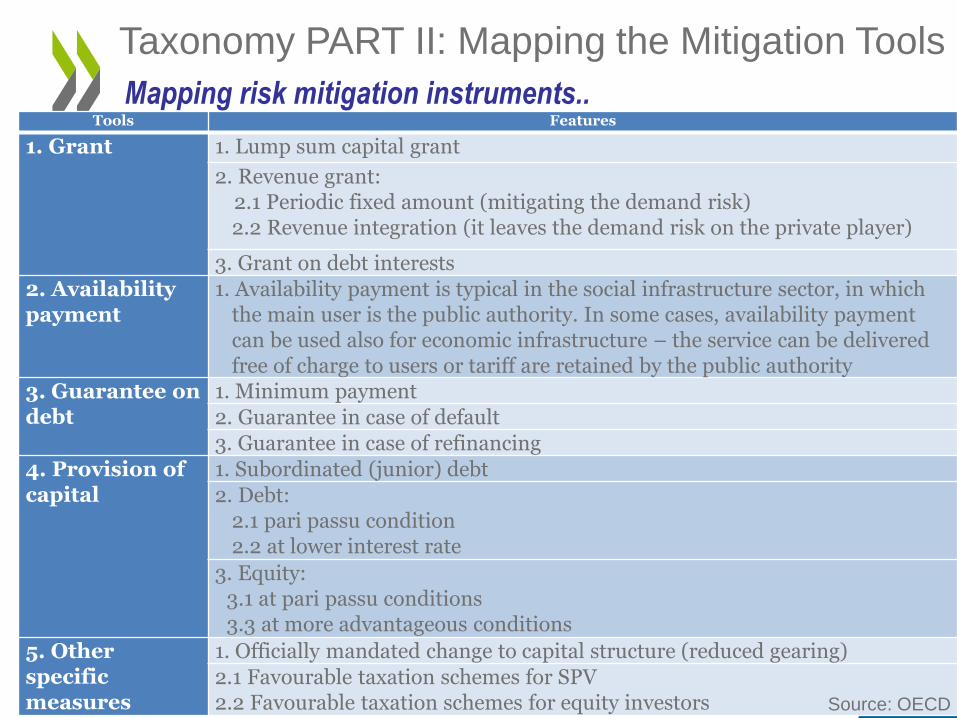

Taxonomy PART II: Mapping the Mitigation Tools

19

Tools Features

1. Grant 1. Lump sum capital grant

2. Revenue grant: 2.1 Periodic fixed amount (mitigating the demand risk) 2.2 Revenue integration (it leaves the demand risk on the private player)

3. Grant on debt interests 2. Availability payment

1. Availability payment is typical in the social infrastructure sector, in which the main user is the public authority. In some cases, availability payment can be used also for economic infrastructure – the service can be delivered free of charge to users or tariff are retained by the public authority

3. Guarantee on debt

1. Minimum payment 2. Guarantee in case of default 3. Guarantee in case of refinancing

4. Provision of capital

1. Subordinated (junior) debt 2. Debt:

2.1 pari passu condition 2.2 at lower interest rate

3. Equity: 3.1 at pari passu conditions 3.3 at more advantageous conditions

5. Other specific measures

1. Officially mandated change to capital structure (reduced gearing) 2.1 Favourable taxation schemes for SPV 2.2 Favourable taxation schemes for equity investors

Mapping risk mitigation instruments..

Source: OECD

Taxonomy PART II: Addressing the Risks

20

.. different Instruments have a specific impact on risks, project cash

flows and ratios of infrastructure projects

Revenues

Capex

Sustainable interests on

debt, meeting target interest

and DSCR

Dividends to meet target IRR equity

2.1 Availability

based

payment

1.2.1 Revenue

grant - fixed

amount

3.1 Minimum

revenue

scheme

1.2.2 Revenue

grant -

revenue

integration

In

crea

sin

g e

ffec

t o

n r

edu

cin

g

dem

an

d r

isk

s

3.2/3.3 Guarantee on debt

4.1 Subordinated debt

4.2.2 Debt provision at lower

interest rate

1.3 Grant on interest

1.1 Grants

4.2.1/4.3.1 Equity

and debt provision

at market

conditions

5.1 Reduced

gearing by law

increased source of funding

Opex and corporate taxation

5.2.1 Reduced

corporate taxation

4.3.2 Equity provision –with

downside protection and upside

leverage

5.2.2 Taxation on dividends and

capital gains

Future OECD Work on LTI

G20 developments and future LTI related OECD events

21

OECD work on long-term investment

• “Patient”,“Engaged”,“Productive” capital

• LTI investors/LT assets

• NB: Short Term not bad

• OECD, APEC & G20 relevance

• Network of LTI Investors (new Advisory Board)

22

What does long-term investment mean and why does it matter?

LTI Project: Deliverables, Structure and

OECD added value

Structure: Modules

Data Collection on Institutional

Investors

Governance

Infrastructure Investment

Regulation

Emerging Markets

Financing

1. Engaging in the Policy Discussion

with G20 and APEC

2. Research/Data Collection

3. Main Events (conf./workshops)

Deliverables/Areas of Activity

• G20/OECD Taskforce on LTI

• Institutional Investors expertise (CMF & IPPC Committees, IOPS)

• Data collection national level/Reference database on Inst Inv.

• Other work from OECD Directorates/divisions (ENV, GOV, DEV etc..)

• Network of stakeholders (i.e. Institutional investors, Asset managers, Universities, Investors Group)

OECD added value

23

Research and Data: Deliverables

• Pooling of Institutional investors capital – Selected Case studies in unlisted equity infrastructure (April 2014)

• Institutional Investors as owners: Who are they and what do they do? (Dec 2013)

• Institutional Investors and Infrastructure Financing (Nov 2013)

• Annual Survey of Large Pension funds (Oct 2013)

• Institutional Investors and green infrastructure investments: Selected case studies (Oct 2013)

• Policy Guidance for investment in Clean Energy Infrastructure (August 2013)

• Pension Fund Investment in Infrastructure: A Comparison between Australia and Canada (July 2013)

• Long-term investment, the cost of capital and the dividend buyback puzzle (May 2013)

24

2. Research/

Data Collection

Deliverables/Areas of Activity

• High Level Principles of LTI financing by institutional investors (Sep 2013)

• Survey Report on Pension Funds’ LTI (Oct 2013)

• Pooling of Institutional investors capital – Selected Case studies in unlisted equity infrastructure (April 2014)

• Private Sector Financing of Infrastructure (Oct 2014)

• Report on Effective Approaches of the G20/OECD High-level Principles on LTI by Institutional Investors (Sep 2014)

• G20/OECD Checklist on Long-term Investment Financing Strategies and Institutional Investors (Sep 2014)

• Mapping Channels to Mobilise Institutional Investment in Sustainable Energy (Feb 2015)

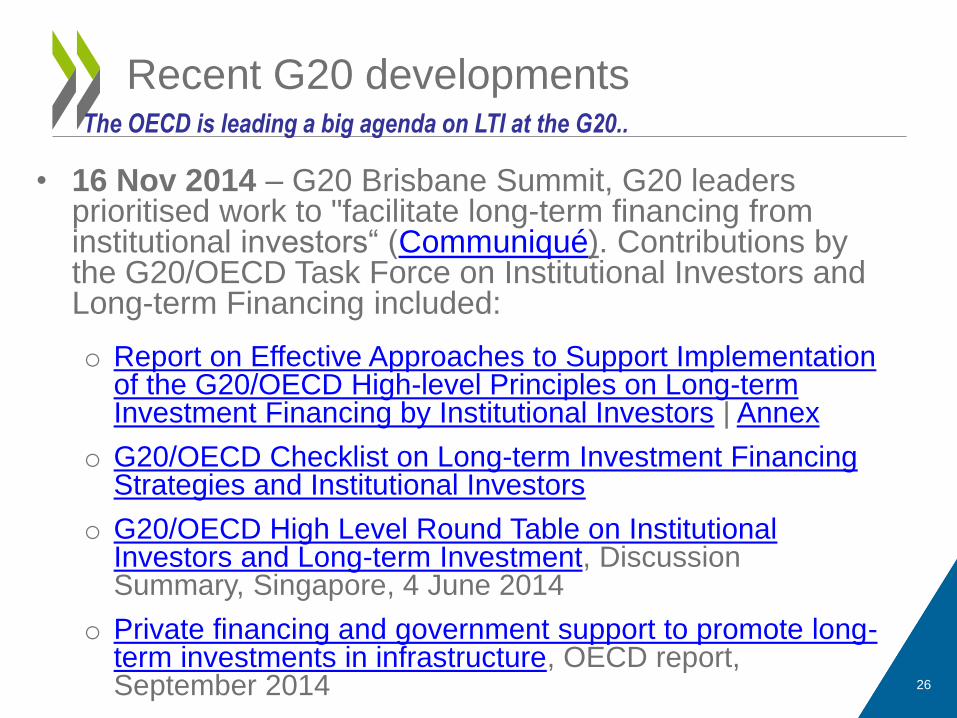

G20-OECD work on

long-term financing

25

Deliverables/Areas of Activity

Work developed through the G20/OECD Taskforce

• 16 Nov 2014 – G20 Brisbane Summit, G20 leaders prioritised work to "facilitate long-term financing from institutional investors“ (Communiqué). Contributions by the G20/OECD Task Force on Institutional Investors and Long-term Financing included:

o Report on Effective Approaches to Support Implementation of the G20/OECD High-level Principles on Long-term Investment Financing by Institutional Investors | Annex

o G20/OECD Checklist on Long-term Investment Financing Strategies and Institutional Investors

o G20/OECD High Level Round Table on Institutional Investors and Long-term Investment, Discussion Summary, Singapore, 4 June 2014

o Private financing and government support to promote long-term investments in infrastructure, OECD report, September 2014 26

Recent G20 developments The OECD is leading a big agenda on LTI at the G20..

• Forthcoming Research:

– Large Insurance Survey – June 2015

– Taxonomy/ Analysis of Instruments and incentives for LTI

– Infrastructure as an Asset Class

– Data collection on Infrastructure performances, investment characteristics

Next Steps - Research

27

• G20/OECD Taskforce on Institutional Investors and Long Term Investment 25th March 2015

• G20/OECD High-Level Roundtable on Institutional Investors and Long-term Investment, May 28 May 2015, Singapore

• OECD/ Euromoney Institutional Investors Roundtable, November 2015 , Paris

Next Steps – Events

www.oecd.org/finance/lti - OECD long-term investment project

28