o i l s e a r c h l i m i t e d · under construction (peru lng, qatar gas 2/3/4, rasgas3, sakhalin...

TRANSCRIPT

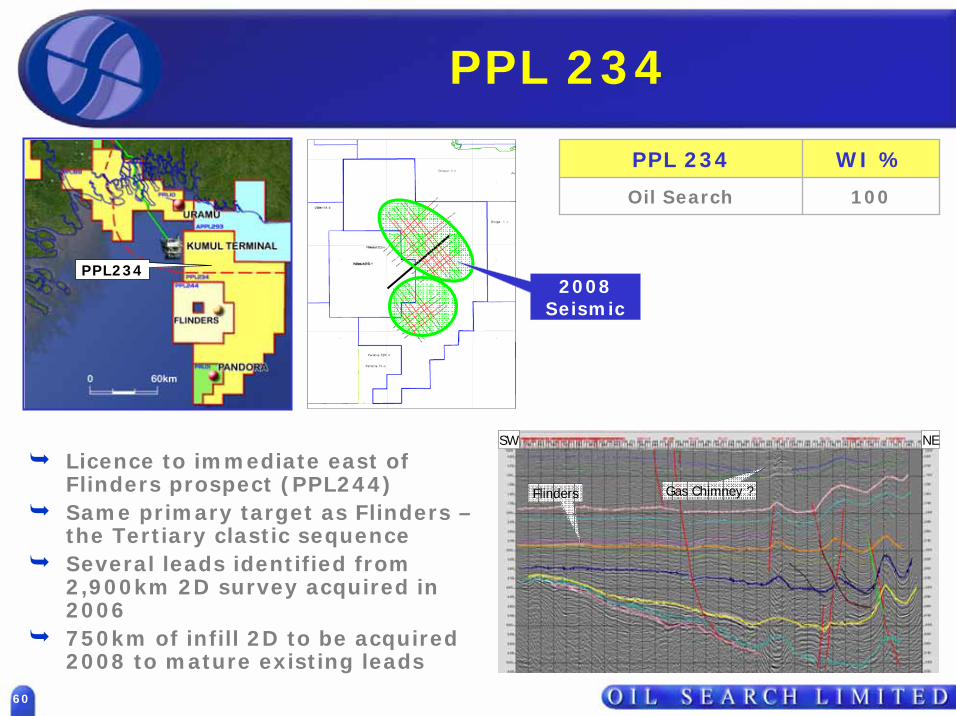

8

Gas Commercialisation

October/November 2007

O I L S E A R C H L I M I T E D

9

Outline

Gas Resources in PNG

LNG markets

ExxonMobil LNG Project

Gas Growth Initiatives

10

Oil Search’s Gas Agenda

Progress ExxonMobil LNG development with FEED entry

Develop ancillary gas businessAdditional LNG trains/plants over timeActive programme to secure and/or find further certifiable reservesReview options for early pipeline developmentExploration and appraisal drilling at Korobosea and appraisal at Barikewa to complement existing discoveries Kimu and Uramu

Continue discussions with petrochemical developers and others

11

Gas Resources in PNG

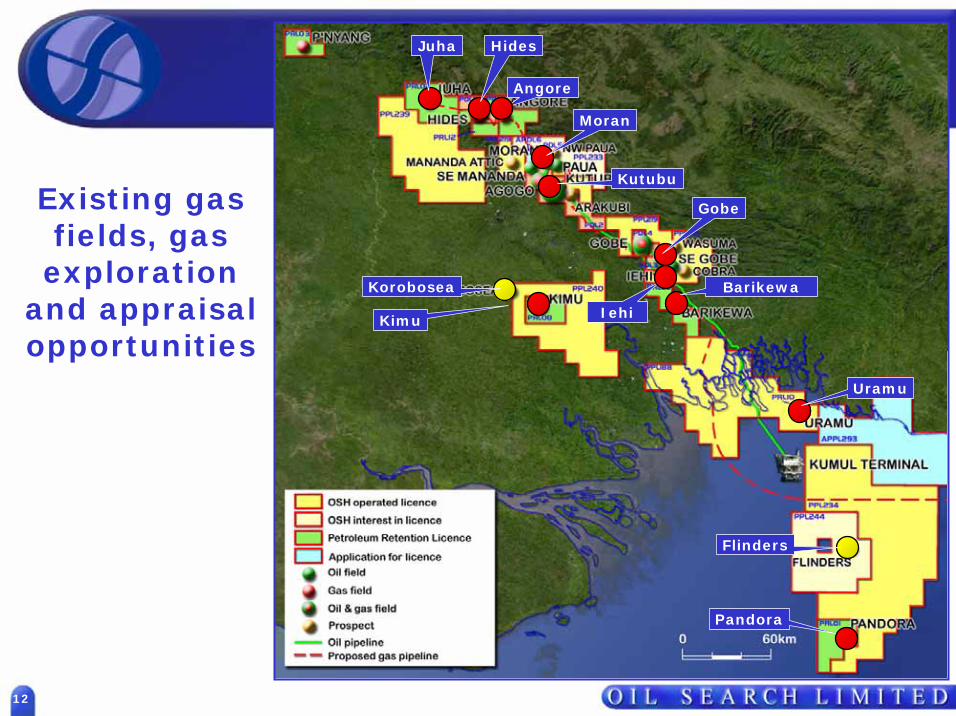

12

Existing gas fields, gas

exploration and appraisal opportunities

Angore

Barikewa

Uramu

Pandora

Juha

Kimu Iehi

Korobosea

Hides

Moran

Kutubu

Gobe

Flinders

13

Gas Resources(Gross PNG)

Current 3P gas resources approximately 24 tcf ex ElkMix of appraisal and exploration is underway to further mature the resource

ElevalaKetuPandoraUramuKimuBarikewaP'nyangAngoreJuhaHidesSE GobeGobe MainMoranAgogoSE ManandaKutubu

0

5

10

15

20

25

30

1P 2P 3P

Recoverable Gas

tcf

14

PNG Gas Resources

Current 2P gas resources of approx 14 tcf

Significant condensate/liquids in conjunction with Highlands gas

Sufficient resources for sequential multi-train LNG development

A prudent mix of appraisal and exploration required to support gas reserves to underpin additional commercial projects

Oil Search net gas and associated liquids resource 940 mmboe

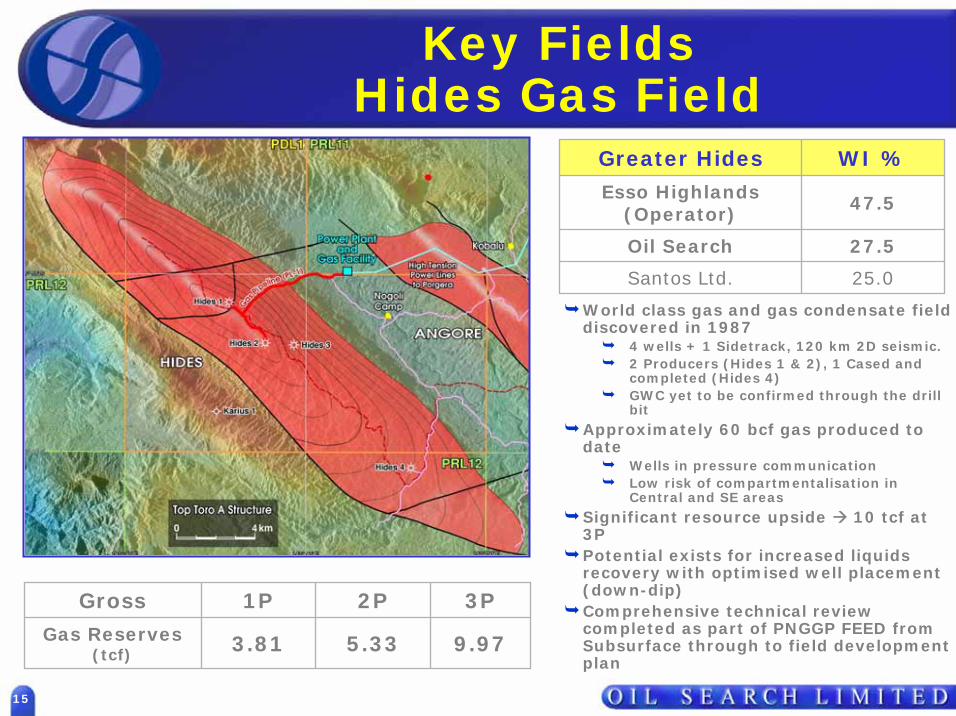

15

Key FieldsHides Gas Field

27.5Oil Search

25.0Santos Ltd.

47.5Esso Highlands (Operator)

WI %Greater Hides

9.975.333.81Gas Reserves (tcf)

3P2P1PGross

World class gas and gas condensate field discovered in 1987

4 wells + 1 Sidetrack, 120 km 2D seismic. 2 Producers (Hides 1 & 2), 1 Cased and completed (Hides 4)GWC yet to be confirmed through the drill bit

Approximately 60 bcf gas produced to date

Wells in pressure communicationLow risk of compartmentalisation in Central and SE areas

Significant resource upside 10 tcf at 3P Potential exists for increased liquids recovery with optimised well placement (down-dip)Comprehensive technical review completed as part of PNGGP FEED from Subsurface through to field development plan

16

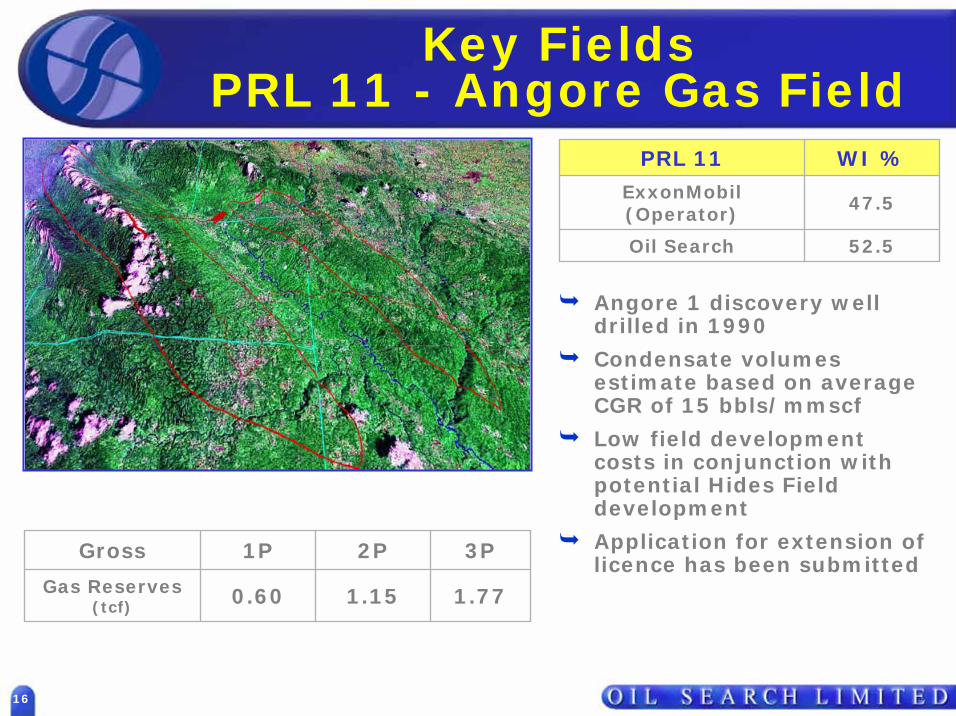

Key FieldsPRL 11 - Angore Gas Field

1.771.150.60Gas Reserves (tcf)

3P2P1PGross

Angore 1 discovery well drilled in 1990

Condensate volumes estimate based on average CGR of 15 bbls/mmscf

Low field development costs in conjunction with potential Hides Field development

Application for extension of licence has been submitted

47.5ExxonMobil (Operator)

52.5Oil Search

WI %PRL 11

17

Key FieldsKutubu & Agogo Gas

Kutubu gas production capacity of 170 mmscf

Gas developments assume new gas conditioning plant is required at CPF

Minimum field capital depending on blowdown rateMay only require dehydration depending on development scenario

Agogo gas currently used for pressure support at Moran

Pipeline to CPF required for gas development

1.611.451.12Gas Reserves (tcf)

3P2P1PGross

18

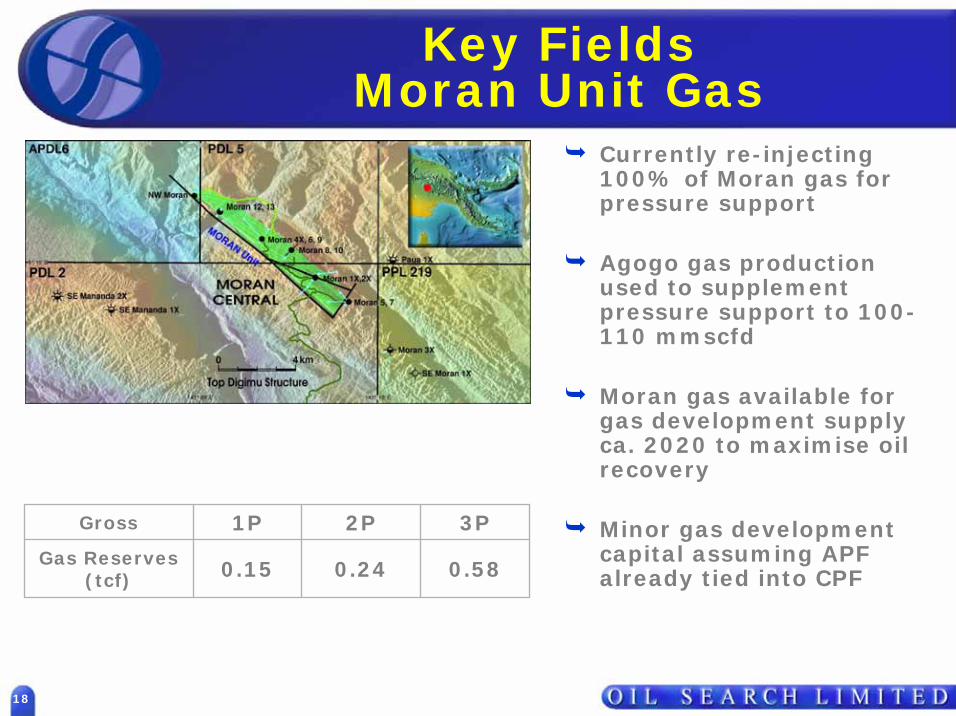

Key FieldsMoran Unit Gas

0.580.240.15Gas Reserves (tcf)

3P2P1PGross

Currently re-injecting 100% of Moran gas for pressure support

Agogo gas production used to supplement pressure support to 100-110 mmscfd

Moran gas available for gas development supply ca. 2020 to maximise oil recovery

Minor gas development capital assuming APF already tied into CPF

19

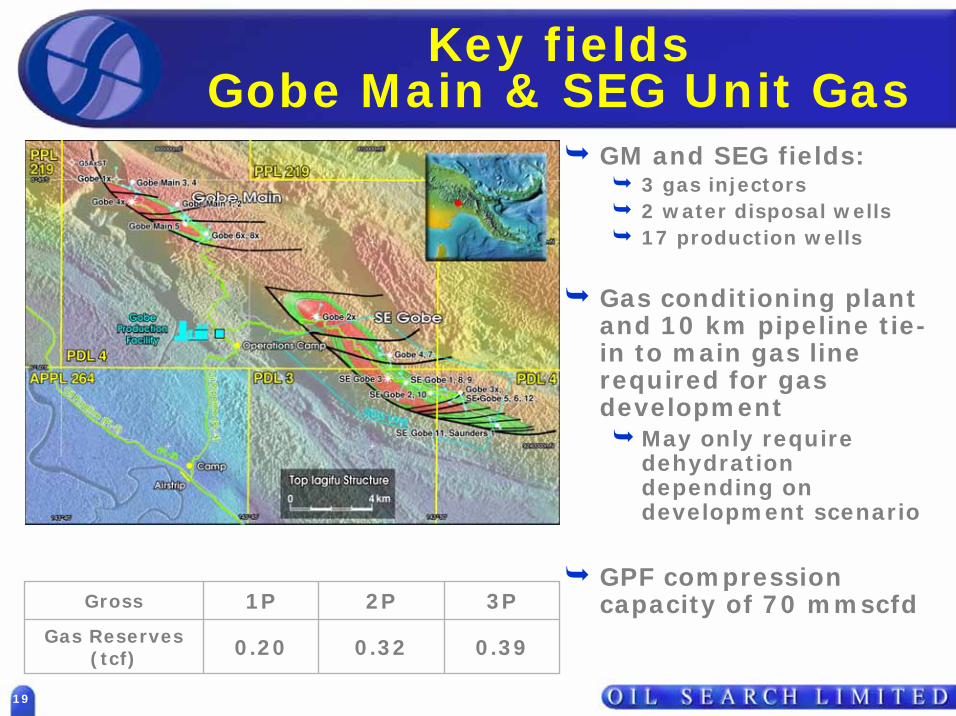

Key fieldsGobe Main & SEG Unit Gas

GM and SEG fields:3 gas injectors2 water disposal wells17 production wells

Gas conditioning plant and 10 km pipeline tie-in to main gas line required for gas development

May only require dehydration depending on development scenario

GPF compression capacity of 70 mmscfd

0.390.320.20Gas Reserves (tcf)

3P2P1PGross

20

Key fieldsPRL 2 - Juha Gas Field

2.001.100.50Gas Reserves* (tcf)

3P2P1PGross

31.5Oil Search

56.0ExxonMobil (Operator)

12.5Merlin Petroleum

WI %PRL 2

Discovered in 1983

Condensate reserves estimate based on average CGR = 60 bbl/mmscfLicence extension granted with a well commitmentJOA allows sole risk development

* - includes both Juha and Juha North pools

Juha-1X

Juha-2X

Juha-3X

10km

PRL2

Juha 4ST1

Juha 5

21

LNG markets and PNG’s positioning

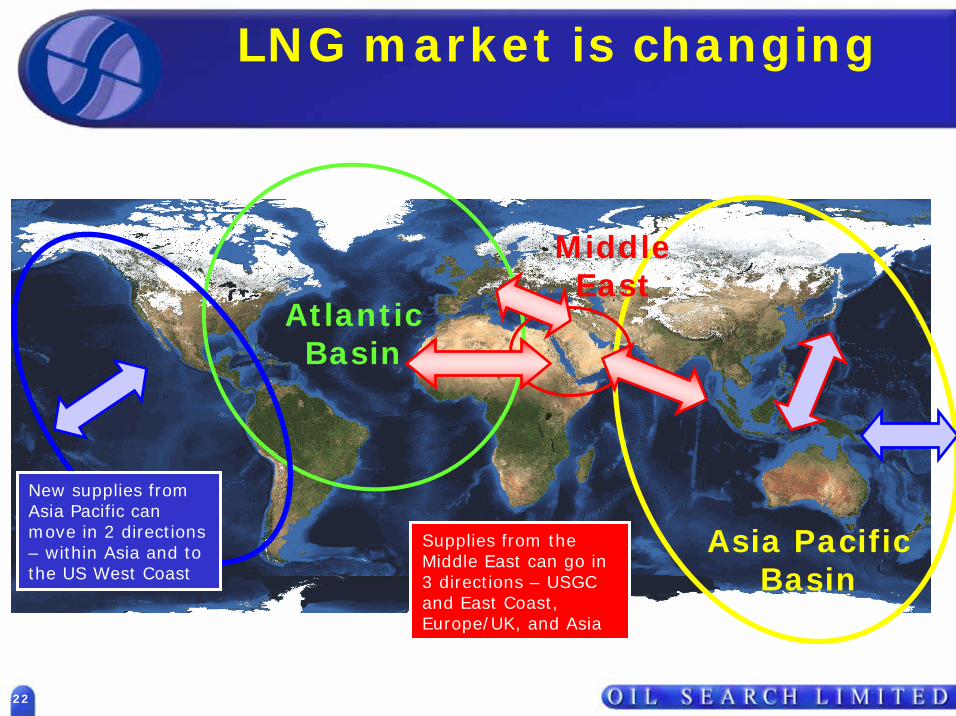

22

AtlanticBasin

MiddleEast

Asia PacificBasin

New supplies from Asia Pacific can move in 2 directions – within Asia and to the US West Coast

Supplies from the Middle East can go in 3 directions – USGC and East Coast, Europe/UK, and Asia

LNG market is changing

Source: FACTS Global Energy, as adapted by Oil Search Limited

23

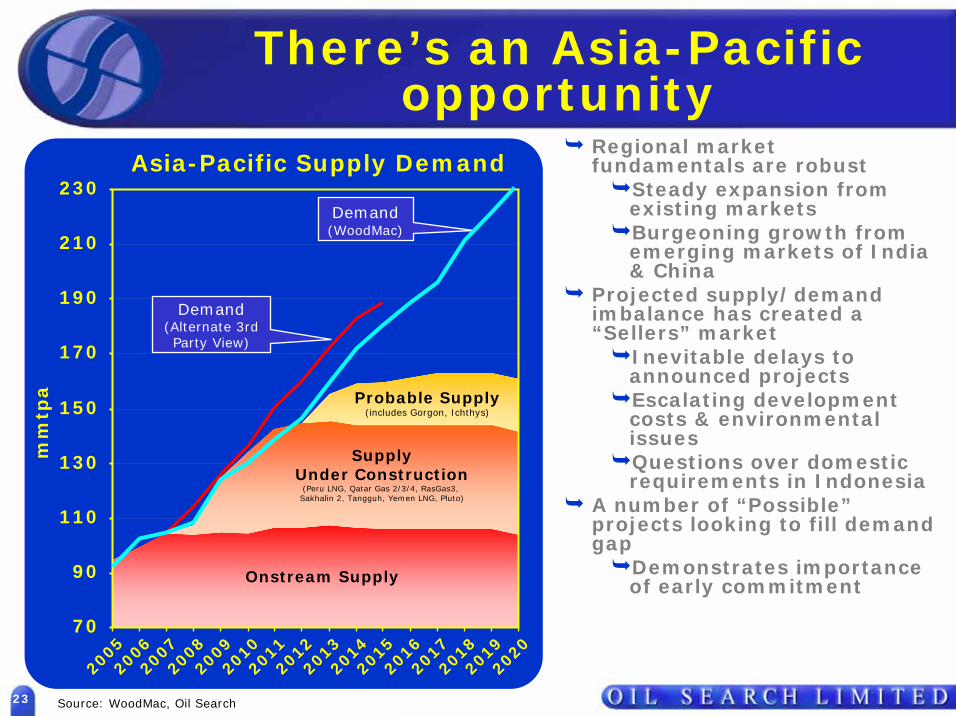

There’s an Asia-Pacificopportunity

Regional market fundamentals are robust

Steady expansion from existing marketsBurgeoning growth from emerging markets of India & China

Projected supply/demand imbalance has created a “Sellers” market

Inevitable delays to announced projectsEscalating development costs & environmental issuesQuestions over domestic requirements in Indonesia

A number of “Possible”projects looking to fill demand gap

Demonstrates importance of early commitment

2005

20

06

2007

20

08

2009

20

10

2011

20

12

2013

20

14

2015

20

16

2017

20

18

2019

20

20

70

90

110

130

150

170

190

210

230

mm

tpa

Onstream Supply

SupplyUnder Construction

(Peru LNG, Qatar Gas 2/3/4, RasGas3, Sakhalin 2, Tangguh, Yemen LNG, Pluto)

Probable Supply(includes Gorgon, Ichthys)

Demand(Alternate 3rd Party View)

Source: WoodMac, Oil Search

Asia-Pacific Supply Demand

Demand(WoodMac)

24

Supply will remain tight until next decade

Only one project made it to FID in 2006 (Peru LNG). Two so far in 2007 (Skikda rebuild and Pluto)

New LNG supply will remain scarce until 2012-13 when greenfield projects come onstream but tightness could last longer as projects continue to face delays

In an environment of rising costs, greenfieldprojects are likely to negotiate price floors to justify the investment and secure financing

Source: FACTS Global Energy

25

Continuous construction cost increaseEnvironmental issuesChallenging conditions/locationsPolitical issues

PROJECTSDELAYED

Source: FACTS Global Energy and Oil Search estimates

Challenges ahead for greenfield projects

Liquefaction Plants Construction Costs: Where Next?

US

$/

t

0

200

400

600

800

1000

1200

1400

1965

-70

1971

-75

1976

-80

1981

-85

1986

-90

1991

-95

96-2

000

2001

-05

2006

-10

Indicative range forPNG LNG

?

26

LNG prices have risen

Higher oil prices mean higher natural gas prices directionally, though gas prices are capped by competition from coal and nuclear at the burner tip, especially in the longer term.Construction costs have risen significantly The United States has entered the LNG market from virtually zero early in the decade, and is very likely going to become the second largest LNG importer next to Japan after 2010. Japan will continue to be the largest importer of LNG through 2020Indonesia, once the world’s largest LNG exporter, is heading for a decline of exports to nearly zero (except for Tangguh) due to a combination of resource problems and political pressure to divert resources to the domestic marketQatar holds most of the cards in the near term

Source: FACTS Global Energy

27

High prices and high future demand?

FACTS view of the future is a HH price of US$7-9/mmbtu (real) long term, despite the current weak prices. However, prices may rise and fall with oil prices

Can the consumer pay US$7-9/mmbtu or higher ex-ship price? FACT believes the consumers in Japan, Korea, Taiwan, and the US have no choice. They are paying the high price for oil and they can afford the high price for gas, but do so reluctantly and with much resistance, particularly in the power sector

Some Asian countries are being asked to pay $8-12/mmbtu today to divert volumes from the West to the East

Can the Chinese and Indian consumers pay such prices? Can fertiliser producers pay such prices? The answer is highly uncertain. China and India are still not addicted to gas. They will find coal as the best buy. Some sectors can pay the high prices, but most cannot, particularly in the traditional state-owned power sector, except where gas replaces fuel oil or naphtha

Source: FACTS Global Energy

28

Higher long-term price benchmarks

NWS Traditional to Japan NWS-T1-3 Bilateral Renewals Gorgon to Japan

Pluto to Japan NWS Allocation Process RasGas to KOGAS from 2007

Crude Oil Parity

Analysis of Recent Contracts to Japan and Korea (DES)

JCC ($/bbl)

LN

G (

$/

mm

btu

)

Oct 05 - Mar 06

Mar - May 06

April - May 06

December 06Sellers are now positioning between these markers

Source: FACTS Global Energy

29

LNG pricing relative to oil

NWS Traditional Contracting

Crude Oil Parity

0

2

4

6

8

10

12

14

15 20 25 30 35 40 45 50 55 60 65 70

LN

G (

$/

mm

btu

)

JCC ($/bbl)

NWS Recent Contracting

10

Source: FACTS Global Energy

30

PNG has competitive advantages

Quality and location of resource makes PNG very competitive in project line up for a 2013 – 2014 development timetable

Advantages of LNG from PNG Highlands:Substantial certified reserve base, sufficient to underwrite development

High liquids content improves economics

Clean gas, minimal impurities (CO2), no additional processing capex required

Onshore, with existing infrastructure base (Kutubu & liquids pipeline)

Environmental approvals well advanced

Excellent location to exploit Asian & US West Coast markets

Competitive labour costs relative to Australia

Favourable fiscal regime with strong Government support

31

PNG well placed geographically

PNG‘s geographical location & stability make it an ideal supplier

32

LNG Projectin PNG

33

LNG with ExxonMobilSummary

ExxonMobil Pre-FEED review progressing well - strong momentum

Participants in LNG pre-FEED are Hides/Angore/ Juha/ Kutubu/ Agogo/ Moran/Gobe Main JVs. OSH’s funding share is 36.6%. Interest post Government back-in/unitisation expected to be ~ 30%

Studies on technical aspects are ongoing and include LNG plant technology, configuration, site development and execution planning

Plant location being finalised

Negotiation of fiscal terms taking place with new PNG Government

Working towards agreement on Unitisation framework, Joint Development Agreement

Capex estimate of around US$10bn for 6.3 mtpa of capacity appears to be robust post Pluto, full bottom-up capex re-build underway pre-FEED

Timetable - target end 2007/early 2008 to enter FEED, up to 18 months to FID, mid-late 2013 for first deliveries

34

ExxonMobil-led LNG Project

Capacity: 6.3 mtpa

Indicative capital cost: US$10 bn

Reserves required (project life): 10-12 tcf

Configuration and cost estimates being refined in pre-FEED work

Kopi

Kutubu & Agogo

Gobe

Hides & Angore

Juha

Port Moresby

75km

Valve & Pigging Station

311 km 32-inch Hides-Kopi pipeline

250 mmscfd (nominal)

960 mmscfd Conditioning Plant

66 km 14-inch gas line

8-inch condensate line

~400km 32/34-inch subsea gas line to LNG Plant at Konebada, Port

Moresby

LNG Facility - 6.3MTA Capacity

2x 125,000m³ LNG Tanks2x 50,000bbls Condensate Tanks2.1km LNG Trestle

35

What’s being done…..

Activities underway include:Plant size & technologySiteGas resourceUnitisationCommercial JV frameworkFiscal regime & State deliverablesFinanceMarketingBenefitsInterface with the existing Oil Projects

36

Plant Size & Technology

Owners have considered the number and size of trains for the initial development

Currently certified resource supports an initial 6.3 mmpta LNG development

Owners elected to run dual pre-FEEDs in order to ensure appropriate technology selection

Pre-FEED work considered a single large train and dual smaller trains

Pre-FEED work also considered APCI technology and Cascade technology

Consideration has been given to risk and economics

Both technologies have proven track records

Work is being finalised

37

LNG Plant Site

Site selection and land tenure issues have been considered

World-scale LNG plant11 potential sites were evaluated, with a focus on coastal locations in the southSite near Port Moresby (portion 152, near Konebada Petroleum Park) is currently favoured:

Large, low relief block suitable for initial LNG development and expansion trainsGood sea accessNeed for a jetty, but no breakwaterRoad access to Port Moresby infrastructure

Confirming processes for site access and tenureOSH assisting

38

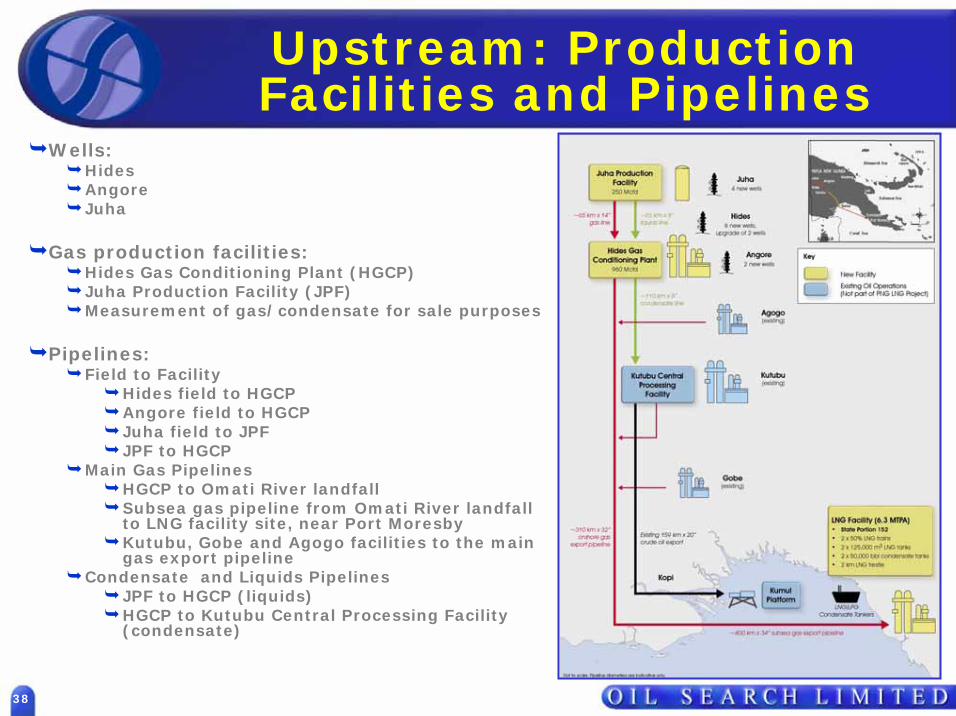

Upstream: Production Facilities and Pipelines

Wells:Hides AngoreJuha

Gas production facilities:Hides Gas Conditioning Plant (HGCP)Juha Production Facility (JPF)Measurement of gas/condensate for sale purposes

Pipelines:Field to Facility

Hides field to HGCPAngore field to HGCPJuha field to JPFJPF to HGCP

Main Gas PipelinesHGCP to Omati River landfallSubsea gas pipeline from Omati River landfall to LNG facility site, near Port MoresbyKutubu, Gobe and Agogo facilities to the main gas export pipeline

Condensate and Liquids PipelinesJPF to HGCP (liquids)HGCP to Kutubu Central Processing Facility (condensate)

39

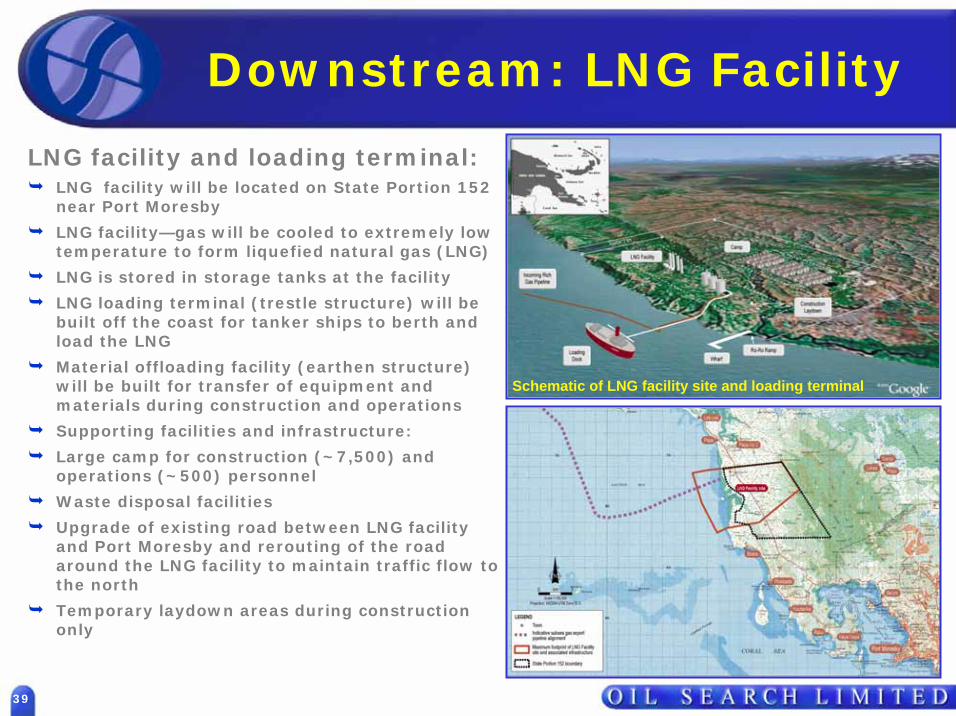

Downstream: LNG Facility

Schematic of LNG facility site and loading terminal

LNG facility and loading terminal:LNG facility will be located on State Portion 152 near Port Moresby

LNG facility—gas will be cooled to extremely low temperature to form liquefied natural gas (LNG)

LNG is stored in storage tanks at the facility

LNG loading terminal (trestle structure) will be built off the coast for tanker ships to berth and load the LNG

Material offloading facility (earthen structure) will be built for transfer of equipment and materials during construction and operations

Supporting facilities and infrastructure:

Large camp for construction (~7,500) and operations (~500) personnel

Waste disposal facilities

Upgrade of existing road between LNG facility and Port Moresby and rerouting of the road around the LNG facility to maintain traffic flow to the north

Temporary laydown areas during construction only

40

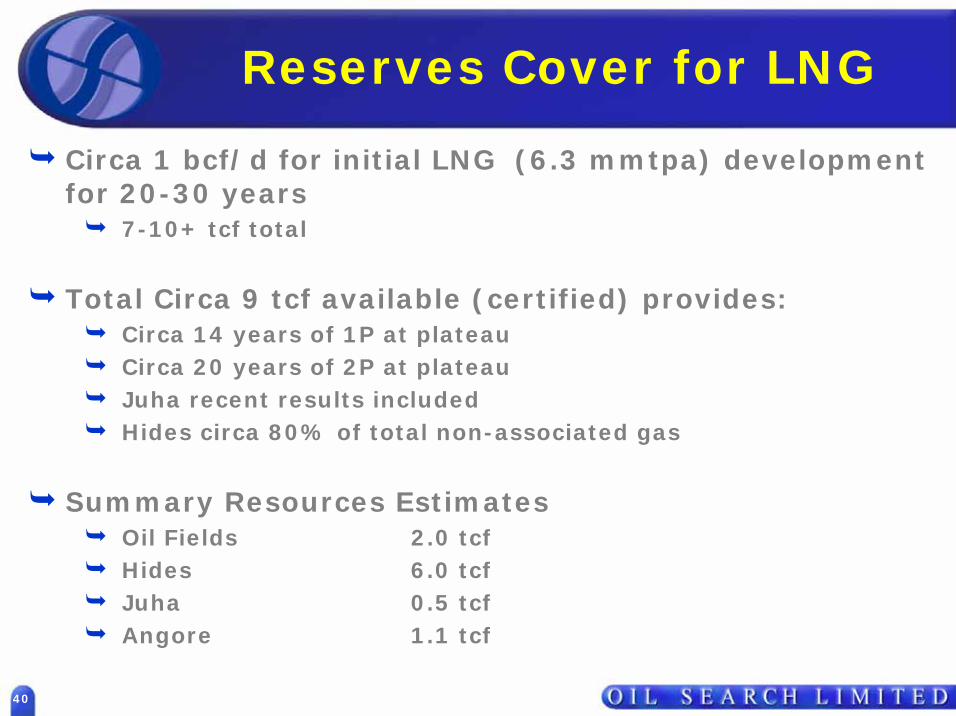

Reserves Cover for LNG

Circa 1 bcf/d for initial LNG (6.3 mmtpa) development for 20-30 years

7-10+ tcf total

Total Circa 9 tcf available (certified) provides:Circa 14 years of 1P at plateauCirca 20 years of 2P at plateauJuha recent results includedHides circa 80% of total non-associated gas

Summary Resources EstimatesOil Fields 2.0 tcfHides 6.0 tcfJuha 0.5 tcfAngore 1.1 tcf

41

Unitisation

Unitisation and cooperative development is required to proceed to FEEDMethodology under discussion Indicative unitisation is as follows:

~ 2%2.7%JPP

18-20%1.1% State / Landowners

~3%3.3%AGL

11-13%13.8%Santos

28-32%36.6%Oil Search

30-34%42.5%ExxonMobil

Indicative Unitisation*

Cost Sharing Agreement

* Oil Search estimates only, based on After State back-in and dependent on assumptions and negotiated outcomes

42

Project Structure

JuhaDevelopment

Hides/AngoreDevelopment

Additional TRAINS

(?)

TRAIN 2

TRAIN 1

Ship

Pipeline JV

Common Facility JV

Developable or expansion capacity?

New FieldDev

GasDevelopment

KGAM Oilfields

LNG Project is a fully integrated JV

43

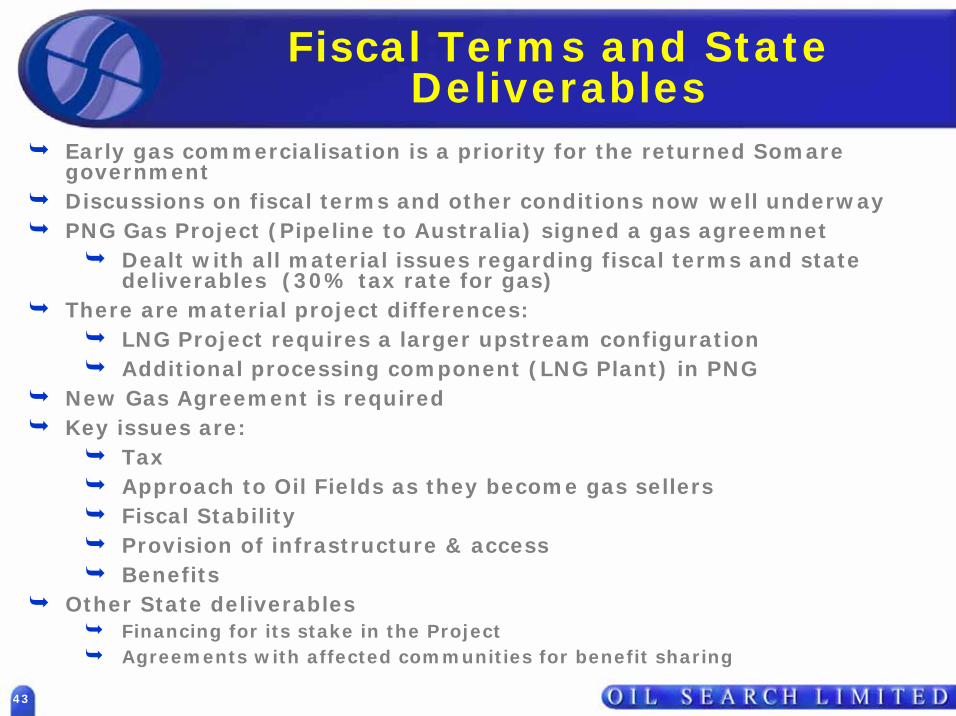

Fiscal Terms and State Deliverables

Early gas commercialisation is a priority for the returned Somare governmentDiscussions on fiscal terms and other conditions now well underwayPNG Gas Project (Pipeline to Australia) signed a gas agreemnet

Dealt with all material issues regarding fiscal terms and state deliverables (30% tax rate for gas)

There are material project differences:LNG Project requires a larger upstream configurationAdditional processing component (LNG Plant) in PNG

New Gas Agreement is required Key issues are:

Tax Approach to Oil Fields as they become gas sellersFiscal StabilityProvision of infrastructure & accessBenefits

Other State deliverablesFinancing for its stake in the ProjectAgreements with affected communities for benefit sharing

44

Finance

Workable finance plan required by FEED entry

Likely to involve multilateral agencies and commercial banks

State equity is fundamental

Finance plan under developmentAdvisor appointed for phase 1

Project based finance

Need for State to work closely with developers on financing

45

Marketing

Owners considering approach to marketing and discussing framework as part of commercial discussions

Expect to commence discussions with potential customers in early 2008, post FEED decision

46

LNG Project Schedule

2007

FEED Program &EPC Contracting

PNG GovernmentApprovals

Benefits SharingAgreement

Project Financing& Marketing

Detailed EngineeringDesign & Procurement

Construction /Commissioning

2008 2009 2010 2011 2012 2013 2014

Pre-FEED

FirstCargoLNG

Schedule is Indicative only

47

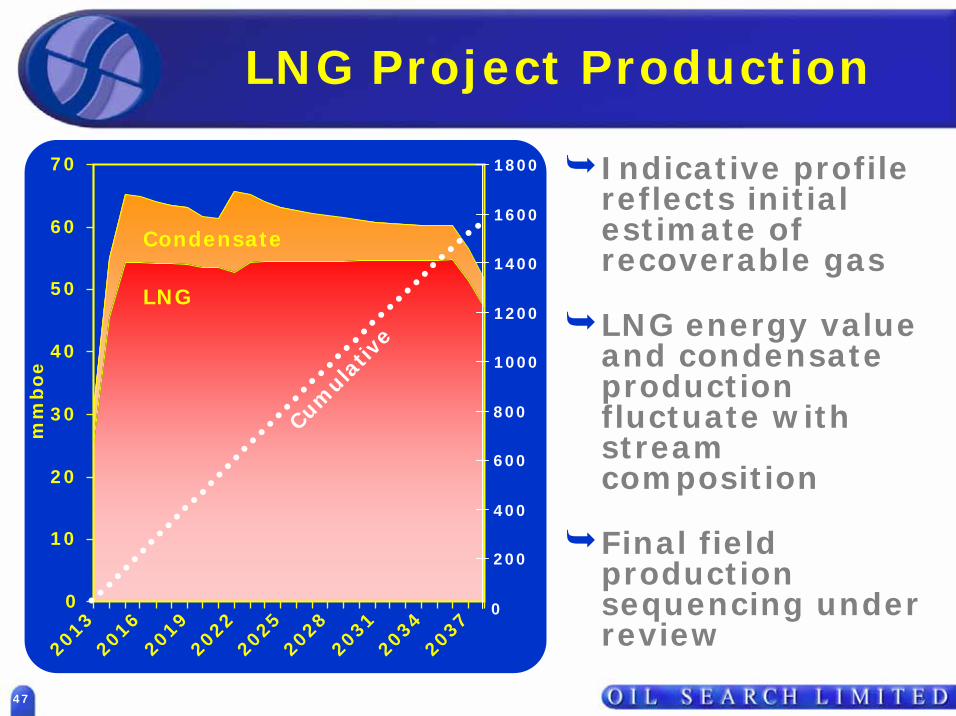

LNG Project Production

Indicative profile reflects initial estimate of recoverable gas

LNG energy value and condensate production fluctuate with stream composition

Final field production sequencing under review

mm

bo

e

0

10

20

30

40

50

60

70

2013

2016

2019

2022

2025

2028

2031

2034

2037

LNG

Condensate

0

200

400

600

800

1000

1200

1400

1600

1800

Cumul

ativ

e

48

Other Potential LNG Projects

InterOil-Merrill Sponsors continue to express confidenceRelies on gas from ElkSeparate plant location near IOL Refinery

BGMOU with Oil Search lapsed at end of October

Reflects progress with ExxonMobil LNG Informal relationship with a view to future LNG opportunities

OthersFrequent inquiries seeking opportunities for involvement with Oil Search in developing LNG from its gas portfolio in PNG

49

Gas Growth

Strategic Opportunity

50

Gas Growth Strategy

Build gas resource base for:LNG expansion, or:Alternative, complementary and possibly accelerated gas development.

By:Prudently exploring and appraising in existing licences.Increasing Oil Search equity in some existing licencesPotential farm-ins to high graded quality acreageMaintaining appropriate momentum on alternative gas commercialisation options

51

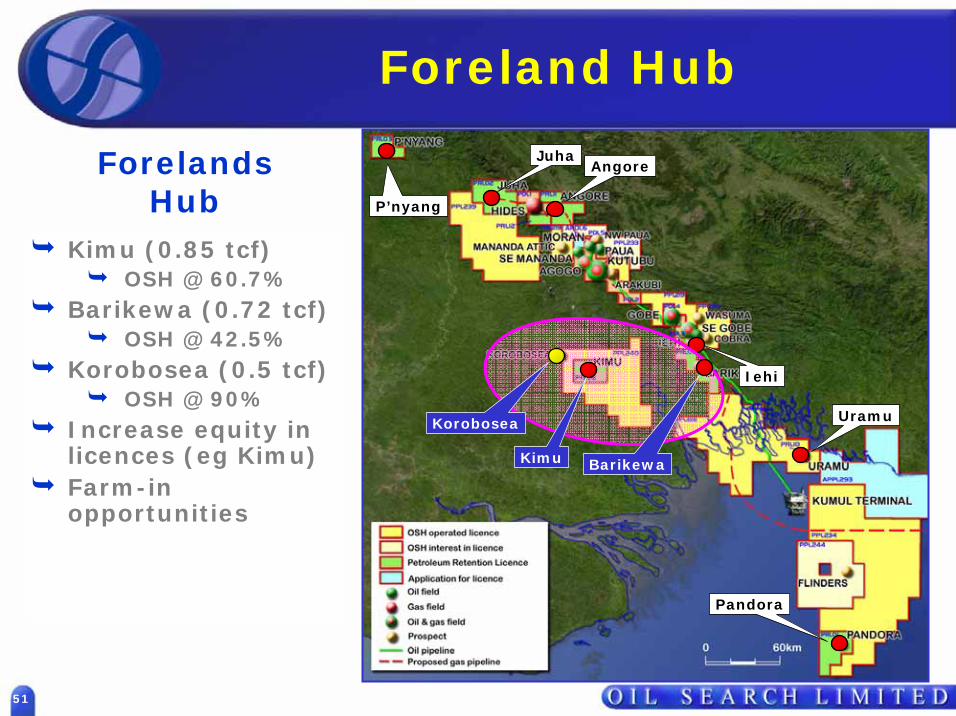

Foreland Hub

Forelands Hub

Kimu (0.85 tcf)OSH @ 60.7%

Barikewa (0.72 tcf)OSH @ 42.5%

Korobosea (0.5 tcf)OSH @ 90%

Increase equity in licences (eg Kimu)Farm-in opportunities

Angore

Uramu

Pandora

Juha

P’nyang

Iehi

BarikewaKimu

Korobosea

52

PRL 8 - Kimu Gas Field

Drilled in 1998/99 by Oil Search intersected a 30m gross gas column

70km new seismic acquired Q3 2007Seismic currently being interpreted

28.6Mosaic Oil Niugini

60.7Oil Search

10.7Cue Energy

WI %PRL 8

Reserves: Current 2P 0.85 tcf

PRL08

PPL240

KIMU

5km

53

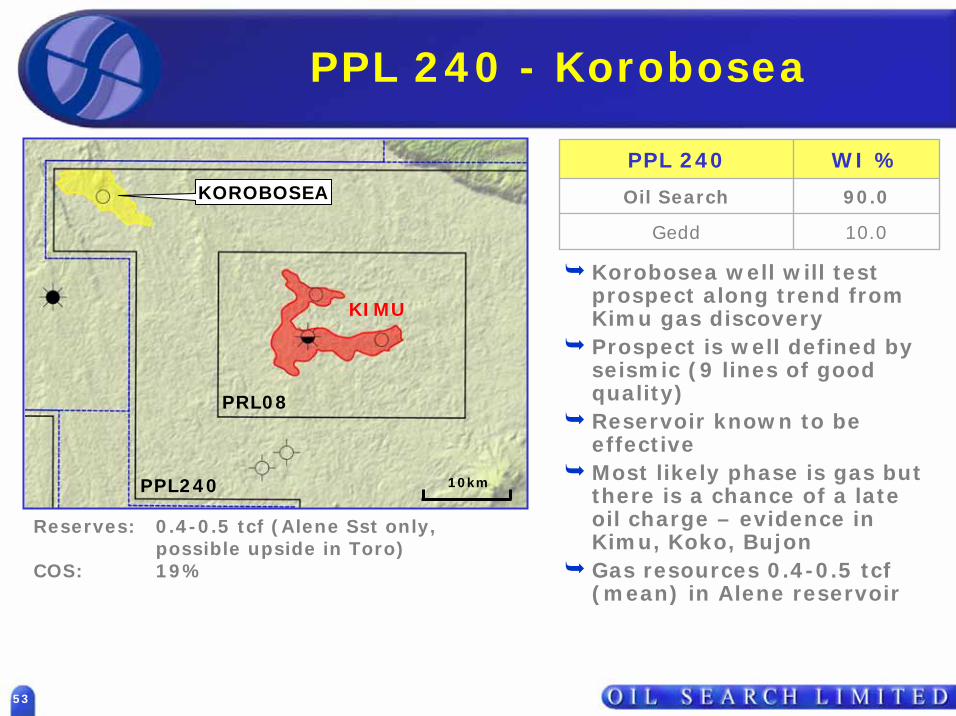

PPL 240 - Korobosea

10.0Gedd

90.0Oil Search

WI %PPL 240

Korobosea well will test prospect along trend from Kimu gas discoveryProspect is well defined by seismic (9 lines of good quality)Reservoir known to be effectiveMost likely phase is gas but there is a chance of a late oil charge – evidence in Kimu, Koko, BujonGas resources 0.4-0.5 tcf (mean) in Alene reservoir

Reserves: 0.4-0.5 tcf (Alene Sst only, possible upside in Toro)

COS: 19%

KIMU

KOROBOSEA

PPL240

PRL08

10km

54

PPL 240 - Korobosea

SW NEKorobosea

2km

Alene Sst

Toro Sst

Darai Lmst

Korobosea Prospect covers 20+km and is well defined by seismicKorobosea-1 spudded 22nd OctoberScheduled to intersect Alene and Toro reservoirs in early November

55

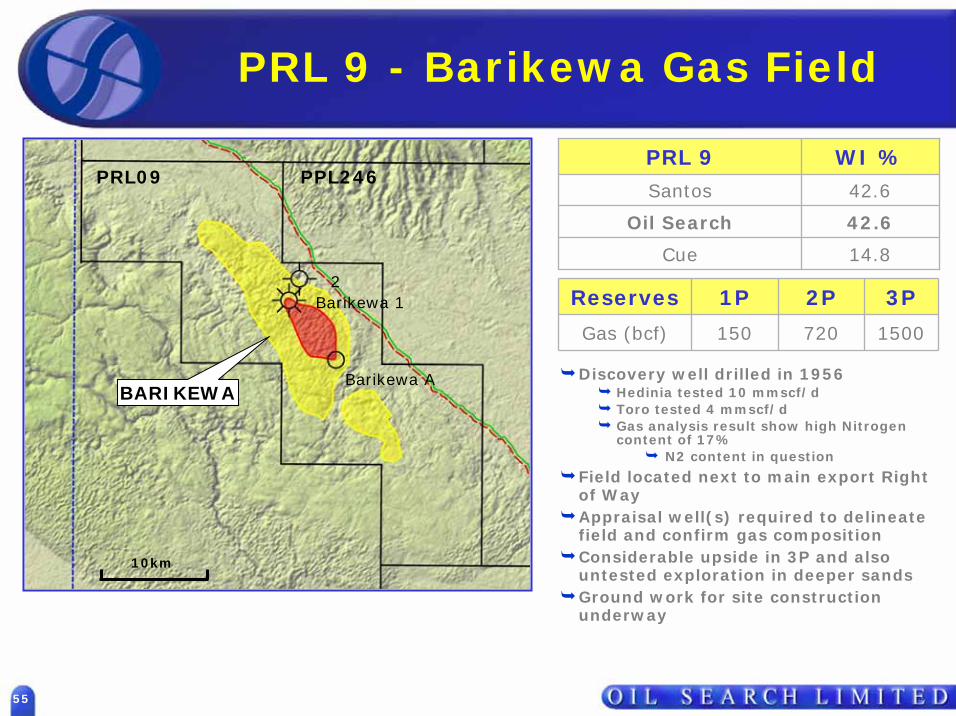

PRL 9 - Barikewa Gas Field

Discovery well drilled in 1956Hedinia tested 10 mmscf/dToro tested 4 mmscf/dGas analysis result show high Nitrogen content of 17%

N2 content in question

Field located next to main export Right of WayAppraisal well(s) required to delineate field and confirm gas compositionConsiderable upside in 3P and also untested exploration in deeper sandsGround work for site construction underway

42.6Oil Search

42.6Santos

14.8Cue

WI %PRL 9

BARIKEWA

PRL09

10km

PPL246

Barikewa 12

Barikewa A

1500720150Gas (bcf)

3P2P1PReserves

56

Offshore Hub

Offshore HubUramu (0.37 tcf)

OSH @ 49.5%Pandora (1.5 tcf)

OSH @ 5%3D seismic scheduled to firm up resource size

Near field exploration opportunities

FlindersPPL 234APPL 293

Angore

Barikewa

Juha

P’nyang

Kimu

Iehi

Korobosea

Flinders

PPL234

Pandora

APPL293

Uramu

57

PRL 1 - Pandora Gas Field

5.0Oil Search

16.4ExxonMobil

48.2Talisman Oil Ltd

12.7Command Petroleum (Cairn)

6.4Claremont Petroleum (Beach)

6.4Pacrim Energy

5.0Secab Niugini (ENI)

WI %PRL 1

500km2 3D to be acquired in 2008Untested Upside

Along trend low relief reefsPandora Mesozoic sub reef section

IssuesOffshore development, with slightly sour gas

26401500230Gas (bcf)

3P2P1PReserves

5 Km

D

C

AJ

B

FG

947 948 949

1019 1020 1021

1091 1092

1163

5 Km

D

C

AJ

B

FG

947 948 949

1019 1020 1021

1091 1092

1163

Pandora 1X

Pandora B1X

PANDORA

58

PRL 10 - Uramu Gas Field

370275Gas (bcf)

2P1PReserves

Drilled in 1968 by Phillipswater depth 6-10 metres3 km offshore30 km NE from Kumul Terminalintersected a 49m gross gas column

Production tested Uramu-1A at 24 mmscfdReservoir pressure ca. 3300 psi (500 psi over-pressured)Field area 10.2 sq. km

40.5ML Energy Investment Fund Upstream (PNG)

49.5Oil Search

10.0Gedd (PNG) Ltd

WI %PRL 10

URAMU

59

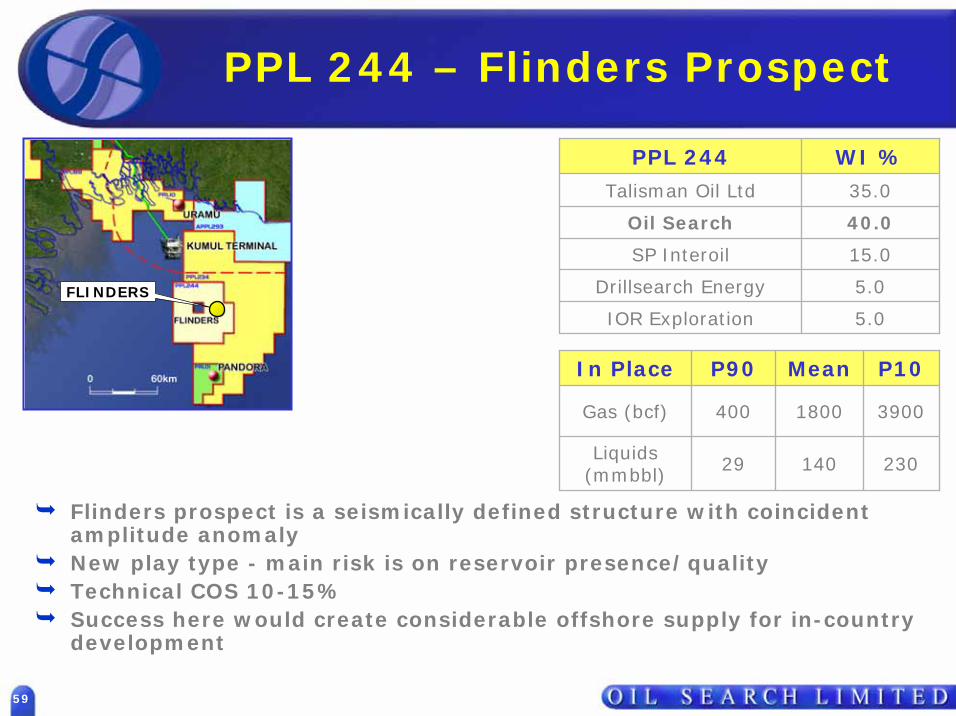

PPL 244 – Flinders Prospect

40.0Oil Search

15.0SP Interoil

35.0Talisman Oil Ltd

5.0Drillsearch Energy

5.0IOR Exploration

WI %PPL 244

Flinders prospect is a seismically defined structure with coincident amplitude anomalyNew play type - main risk is on reservoir presence/qualityTechnical COS 10-15%Success here would create considerable offshore supply for in-country development

39001800400Gas (bcf)

23014029Liquids (mmbbl)

P10MeanP90In Place

FLINDERS

60

PPL 234

100Oil Search

WI %PPL 234

Licence to immediate east of Flinders prospect (PPL244)Same primary target as Flinders –the Tertiary clastic sequenceSeveral leads identified from 2,900km 2D survey acquired in 2006750km of infill 2D to be acquired 2008 to mature existing leads

PPL234

Flinders Gas Chimney ?

SW NE

2008 Seismic

61

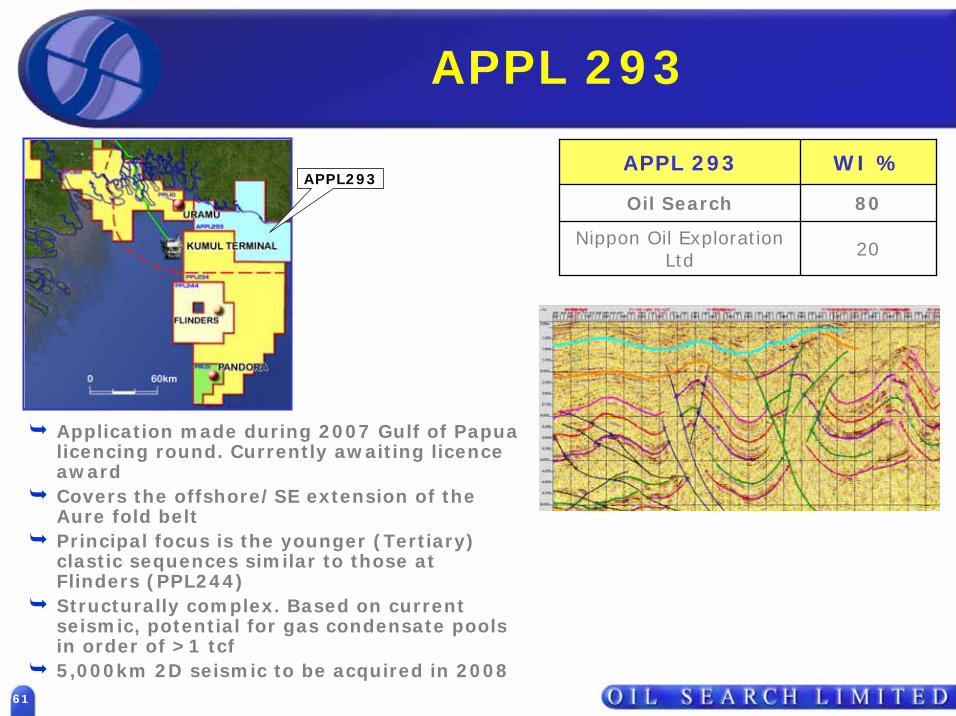

APPL 293

20Nippon Oil Exploration Ltd

80Oil Search

WI %APPL 293

Application made during 2007 Gulf of Papua licencing round. Currently awaiting licence awardCovers the offshore/SE extension of the Aure fold beltPrincipal focus is the younger (Tertiary) clastic sequences similar to those at Flinders (PPL244)Structurally complex. Based on current seismic, potential for gas condensate pools in order of >1 tcf5,000km 2D seismic to be acquired in 2008

APPL293

62

Commercialisation Options

Oil Search continues to drive the following alternative, complementary and possibly accelerated commercialisation options:

LNG expansion:Higher net OSH equity based on upstream fieldsCommercial and technical flexibility to facilitate expansion

Alternative options:Methanol/DMEGas-to-LiquidsSmall scale LNG