nyse i nasdaq

TRANSCRIPT

NY2:\1190087\23\P$9Z23!.DOC\99990.0899

Weil, Gotshal & Manges LLP

MEMORANDUM

Minimum Corporate Governance Standards for Companies Whose Securities Trade in the U.S. (As of November 4, 2003)1

The first comprehensive set of minimum corporate governance standards for companies whose securities trade in the U.S. is

currently developing as a result of recent federal legislation and a series of new and proposed Securities and Exchange Commission (“SEC”) regulations and stock market listing requirements (taken together with pre-existing SEC and stock market requirements). The chart that follows summarizes these minimum corporate governance standards. Many of these standards that were proposed were recently finalized – in some cases with effective dates extending for another year or so -- with the result that a comprehensive set of minimum governance standards for companies that trade in the U.S. will for the first time come into effect in the course of 2003 and 2004.

To a significant extent, these new minimum standards embody what up to now have been non-binding best practices: (1) populating boards with a majority of independent directors; (2) strict standards for determining director independence; (3) instituting wholly independent audit, compensation and nominating/governance committees and allocating specific responsibilities to these committees; (4) establishing the responsibility of audit committees for the annual independent audit of the corporation and over the corporation’s satisfaction of its other financial reporting, disclosure and legal and regulatory compliance obligations; (5) regular meetings of non-management directors; (6) regular board and committee self-evaluations and (7) the development and publication by companies of specific governance guidelines and codes of conduct for their operation, all with the goal of enhancing the effectiveness of board oversight of corporate affairs. However, the new standards involve a greater degree of formality and rigor than has customarily been involved in these matters when they have been addressed in the past. The new standards will impact both foreign and domestic companies whose securities trade in the U.S., although the requirements applicable to publicly-owned domestic companies are of greater reach. 1 On November 4, 2003, the SEC approved the corporate governance listing standards filed by the NYSE and Nasdaq (Release No. 34-48745). On June 30, 2003, the SEC

approved shareholder approval requirements filed by the NYSE and Nasdaq (Release No. 34-48108). On April 10, 2003, the SEC released the text of the rules it adopted under Section 301 of the Act, requiring all U.S. stock exchanges and Nasdaq to adopt listing standards setting certain minimum standards regarding the composition and functions of audit committees (Release No. 33-8220).

November 4, 2003 edition. Copyright Weil, Gotshal & Manges LLP, 2003.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 2

While these new corporate governance standards do not alter the basic fiduciary duties of care and loyalty of corporate directors and officers, they do provide detailed mandates that have implications for, and should be considered carefully when assessing, what directors and officers should do in order to satisfy their fiduciary duties to the corporation and its shareholders.

There are three primary sources of the emerging minimum corporate governance standards:

• The Sarbanes-Oxley Act of 2002 (the “Act”), which became law on July 30, 2002, includes several corporate governance-related provisions, along with new corporate disclosure requirements and auditor regulatory and securities law enforcement measures. Most of the provisions relating to board structure and function require for implementation SEC rulemaking, which has for the most part now been completed. However, certain important provisions relating to audit committees are to be effectuated through the self- regulatory process of stock market listing standards (mandated by new “national market system” provisions which Section 301 of the Act added to Section 10A of the Securities Exchange Act of 1934, as amended (the “Exchange Act”)). These listing standard requirements are to be implemented by the stock markets during 2003. While some of the corporate governance-related requirements of the Act and the implementing rules (including the listing standards required by the Act) have already become effective, others will go into effect over the course of this year and 2004.

• The New York Stock Exchange (“NYSE”) submitted to the SEC (initially on August 16, 2002 and amended and supplemented throughout 2002 and 2003) proposed listing requirements which create a wide-ranging set of corporate governance standards, supplementing the standards it had already established (which related primarily to audit committees and shareholder approval requirements). The proposals were adopted by the SEC on November 4, 2003. They include provisions intended to satisfy the requirements regarding audit committees mandated by the Act. As adopted, generally, the deadline for compliance with the new corporate governance standards will be the company’s first annual meeting occurring after January 15, 2004, but not later than October 31, 2004, except that, in the case of a company with a classified board, to the extent compliance would require a change in a director whose term of office is not scheduled to end by such time, the company will have until the second annual meeting of shareholders after January 15, 2004, but not la ter than December 31, 2005, to comply. Non-U.S. companies have until July 31, 2005 to come into compliance with the audit committee requirements and must make the necessary disclosures regarding how their governance practices differ from those required by the listing standards starting with their annual report filed in 2004.

• The NASDAQ Stock Market (“Nasdaq”) also submitted to the SEC (initially on October 8 and 9, 2002 and amended and supplemented throughout 2002 and 2003) more than 25 new corporate governance requirements for listing, supplementing its pre-existing listing standards (which also related primarily to audit committees and shareholder approval requirements). The proposals were adopted by the SEC on November 4, 2003. Generally, they cover the same subjects as the NYSE standards and they include provisions intended to satisfy the requirements regarding audit committees mandated by the

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 3

Act. As adopted, generally, the deadline for compliance with the new corporate governance standards will be the company’s first annual meeting occurring after January 15, 2004, but not later than October 31, 2004, except that, in the case of a company with a classified board, to the extent compliance would require a change in a director whose term of office is not scheduled to end by such time, the company will have until the second annual meeting of shareholders after January 15, 2004, but not later than December 31, 2005, to comply. In addition, Nasdaq listed companies will need to adopt a code of conduct by May 3, 2004 and must have related party transactions approved by the ir audit committee effective January 15, 2004. Non-U.S. companies have until July 31, 2005 to come into compliance with the audit committee requirements and must make the necessary disclosures regarding how their governance practices differ from those required by the listing standards starting with their annual report filed in 2004.

The attached chart summarizes the corporate governance standards and requirements established by the Act and the SEC’s implementing regulations and those that now apply upon adoption of the NYSE and Nasdaq corporate governance listing standards to companies which list their common shares for trading in those markets (both U.S. and non-U.S. companies). Some of the listing standards pertaining to audit committees will also apply to companies who have not listed their common shares but have listed other equity or debt securities. Certain of the corporate governance requirements of the Act are also applicable to companies which have securities that are registered with the SEC under Section 12 of the Exchange Act or that are required to file periodic reports with the SEC under Section 15(d) of the Exchange Act because they have made a public offering of securities, even if their securities are not listed on any exchange or Nasdaq.

This material is intended to provide general information regarding corporate governance standards and should not be taken or used as legal advice that is applicable to specific situations, which depends on considering the prevailing factual circumstances.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 4

The emerging minimum corporate governance standards for companies whose securities trade in the U.S. markets are presented below organized into the following subject areas:

Page

• The Role and Authority of Independent Directors 5

• Director Independence Criteria 7

• Composition and Role of the Audit Committee 10

• Other Board Committee Requirements 18

• Codes of Conduct and Ethics; Governance Guidelines 20

• Other Standards Applicable to Directors and Officers 22

• Shareholder Approval Requirements 23

• Education and Training of Directors 25

• Applicability to Non-U.S. Companies 26

• Enforcement 28

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 5

Minimum Corporate Governance Standards for Companies Whose Securities Trade in the U.S. (As of November 4, 2003)

ROLE AND AUTHORITY OF INDEPENDENT DIRECTORS

SARBANES-OXLEY ACT / SEC RULES

The Act does not address the role and authority of independent directors, except with regard to audit committee activities (as separately discussed below).

NYSE REQUIREMENTS (§ 303A, ¶ ¶ 1, 3 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(c))

Majority of Independent Directors . Independent directors must comprise a majority of the board. Controlled companies (companies in which more than 50 percent of the voting power is held by an individual, group or another company), limited partnerships and companies in bankruptcy are exempt from this requirement.1

Majority of Independent Directors . Independent directors must comprise a majority of the board. The company must disclose in its annual proxy statement (or, if the company does not file a proxy statement, in its annual report) those directors that the board has determined to be independent. Controlled companies (companies in which more than 50 percent of the voting power is held by an individual, group or another company) are exempt from these requirements.2

Executive Sessions . Non-management directors must meet in regularly scheduled executive sessions (without management). The name of the director presiding at the executive sessions or the procedure by which the presiding director is selected for each executive session must be disclosed in the company’s annual proxy statement (or, if the company does not file a proxy statement, in the company’s annual report), together with information about how interested parties can communicate with either the presiding director or the non-management directors as a group. If the regularly scheduled executive sessions of non-management directors include non-independent directors, then an executive session with only independent directors should be scheduled at least once a year.

Executive Sessions . Boards must convene regular meetings of the independent directors in executive session.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 6

ROLE AND AUTHORITY OF INDEPENDENT DIRECTORS

NYSE REQUIREMENTS (§ 303A, ¶ ¶ 1, 3 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(c))

Cure. The NYSE does not have a cure provision. Cure. If a company fails to comply with the majority independent director requirement because a director is no longer independent for reasons beyond the director’s reasonable control, or due to a vacancy on the board, the company shall regain compliance with the requirement by the earlier of its next annual meeting or one year from the event that caused the failure to comply with the requirement. A company relying on this provision must provide notice to Nasdaq immediately upon learning of the event or circumstance that caused the noncompliance.

Committee Requirements . In addition to an audit committee composed entirely of independent directors (the audit committee requirements are discussed separately below), companies must have:

• a compensation committee (see “Other Board Committee Requirements” below for a description of the functions to be performed by the committee) composed entirely of independent directors3; and

• a nominating/corporate governance committee (see “Other Board Committee Requirements” below for a description of the functions to be performed by the committee) composed entirely of independent directors.4

Companies may allocate the responsibilities of the nominating/corporate governance and compensation committees to committees of their own denomination (but, however denominated, such committees must be composed entirely of independent directors).

Committee Requirements . In addition to an audit committee composed entirely of independent directors (the audit committee requirements are discussed separately below), companies must provide:

• that the compensation of the chief executive officer and other executive officers5 must be determined or recommended to the board for determination by a compensation committee composed solely of independent directors or by a majority of all the independent directors. The CEO may not be present during voting or deliberations regarding his/her compensation.6 One non-independent director who is not then an officer or employee or a family member of an officer or employee is permitted to serve on a compensation committee (of at least three members) for a period of not more than two years in “exceptional and limited circumstances” as determined by the board of directors and disclosed in the annual proxy statement (or, if the company does not file a proxy statement, in its annual report), for a period of no longer than two years; and

• that director nominees are selected or recommended for the board’s selection by a nominating committee composed solely of independent directors or by a majority of all the independent directors.7 One non-independent director may serve on the nominating committee (of at least three members) if such director is not then an officer or employee or a family member of an officer or employee in “exceptional and limited circumstances” as determined by the board of directors and disclosed in the annual proxy statement (or, if the company does not file a proxy statement, in its annual report), for a period of no longer than two years.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 7

DIRECTOR INDEPENDENCE CRITERIA

SARBANES-OXLEY ACT / SEC RULES

The Act addresses a director’s status as “independent” only for audit committee purposes, as provided in Section 301 of the Act, and for such purposes focuses on only two criteria -- the acceptance of compensatory fees from the company or any subsidiary (other than for services as a director) and whether or not the director is an “affiliated person” of the company. (See “Composition and Role of the Audit Committee,” below.)

NYSE REQUIREMENTS (§ 303A, ¶ 2 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4200)

Applicability of Definition. An “independent director” is one who has no “material relationship”8 with the listed company9; this definition applies for all purposes throughout the NYSE listing standards, except that additional restrictions, consistent with Section 301 of the Act, apply to membership on the audit committee (as discussed further below).

Applicability of Definition. An “independent director” is one who has no relationship which would interfere with the exercise of independent judgment in carrying out the responsibilities of a director; this definition applies for all purposes throughout the Nasdaq listing standards, except that additional restrictions, consistent with Section 301 of the Act, apply to membership on the audit committee (as discussed further below).

Independence Criteria. For a director to be deemed “independent,” the board must affirmatively determine that the director has no “material relationship” with the company either directly or “as a partner, shareholder or officer of an organization that has a relationship with the company.” Directors having any of the following relationships are not eligible to be considered independent:

• a person who is an employee or is an immediate family member10 of an executive officer of the company;11

• a person who receives, or is an immediate family member of a person who receives, compensation directly from the listed company, other than director compensation or pension or deferred compensation for prior service (provided such compensation is not contingent in any way on continued service), of more than $100,000 per year;12

Independence Criteria. An “independent director” is defined as a person who is not an officer or employee of the company or any of its subsidiaries or any individual having a relationship which, in the opinion of the board of directors, would interfere with the exercise of independent judgment in carrying out the responsibilities of a director. In addition, the board has an affirmative responsibility to determine that a director does not have any relationship that disqualifies him or her from being independent. Persons having any of the following relationships are not eligible to be considered independent:

• a person who is employed by the company or by any parent13 or subsidiary of the company;

• a person who is a family member14 of an individual who is employed by the company or any parent or subsidiary of the company as an executive officer;

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 8

DIRECTOR INDEPENDENCE CRITERIA (CONTINUED)

NYSE REQUIREMENTS (§ 303A, ¶ 2 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4200)

• a person who is affiliated with or employed by, or is an immediate family member of a person who is affiliated with or employed in a professional capacity by, a present or former internal or external auditor of the company;

• a person or an immediate family member of a person who has been part of an interlocking compensation committee arrangement; and

• a person who is an executive officer or an employee, or is an immediate family member of a person who is an executive officer, of a company that makes payments to or receives payments from the listed company for property or services in an amount that in a single fiscal year exceeds the greater of 2% of such other company’s consolidated gross revenues or $1 million.15

Additional independence criteria apply for purposes of determining eligibility for audit committee membership. See below.

• a person who is, or has a family member who is, a current partner of the company’s outside auditor or was a partner or employee of the company’s outside auditor who worked on the company’s audit at any time during any of the past three years;

• a person who accepts, or is a family member of a person (other than an employee of the company or a parent or subsidiary of the company) who accepts, payments from the company or any of its affiliates in excess of $60,000 during the current or any of the past three fiscal years of the company;16

• a person who is, or has a family member who is, “a partner in, or a controlling shareholder or an executive officer of,” any organization to which the company made, or from which the company received, payments for property or services that exceed 5% of the recipient’s consolidated gross revenues or $200,000, whichever is more, for the current or any of the past three fiscal years;17 or

• a person who is, or who has a family member who is, employed as an executive officer of another company where any of the company’s executive officers serve on the other company’s compensation committee.

Additional independence criteria apply for purposes of determining eligibility for audit committee membership. See below.

Three Year Independence “Cooling Off” Period. In applying the independence criteria discussed above by which specific relationships are considered to impair independence, a three-year “cooling off” period is to be applied, and no individual who has had – even though he no longer has – such a relationship within the “cooling off” period, or who is an immediate family member of an individual who had such a

Three Year Independence “Cooling Off” Period. In applying the independence criteria discussed above by which specific relationships are considered to impair independence, a three-year “cooling off” period is to be applied, and no individual who has had – even though he no longer has – such a relationship within the “cooling off” period, or who is a family member of an individual who had such a relationship, can be considered independent.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 9

DIRECTOR INDEPENDENCE CRITERIA (CONTINUED)

relationship, can be considered independent.

Note that during the first year immediately following the effective date of the listing standard, the “look back” period referenced above will be a one-year look back period and the full three-year look back period will begin to apply after the first anniversary of the effective date of the listing standard.

Note that the three-year look back period for bullets 1,2,3 and 6 above begin on the date the relationship ceases. For example, a director who is employed by the company will not be independent until three years after such employment terminates.

Shareholdings. “[A]s the concern is independence from management, the Exchange does not view ownership of even a significant amount of stock, by itself, as a bar to an independence finding.” However, shareholding will be relevant to determine a person’s status as an “affiliated person” for purposes of applying the independence requirement of the Act applicable to audit committee membership. See “Composition and Role of the Audit Committee” below.

Shareholdings. “Because Nasdaq does not believe that ownership of company stock by itself would preclude a board finding of independence, it is not included in the aforementioned objective factors.” However, shareholding will be relevant to determine a person’s status as an “affiliated person” for purposes of applying the independence requirement of the Act applicable to audit committee membership. See “Composition and Role of the Audit Committee” below.

Disclosure of Immateriality Determinations; Customized Materiality Standards . The basis for a board’s determination that a relationship between a company or its management and a director is not material must be disclosed in the company’s proxy statement (or, if the company does not file a proxy statement, in the company’s annual report). A board may adopt categorical standards to assist it in determining if relationships are material for purposes of determining director independence; if it does so, it must disclose such standards. In such cases, a general disclosure may be made that a director is considered independent by reason of the application of such categorical standards to relationships addressed by such standards, without further explanation. This is intended to give investors adequate means for assessing board independence while avoiding excessive disclosure about immaterial relationships.

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 10

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE

SARBANES-OXLEY ACT / SEC RULES

Minimum Listing Standards Regarding Audit Committees (Section 301 of the Act / Section 10A(m) of the Exchange Act; Rule 10A-3). Section 301 of the Act directs the SEC to adopt regulations that require the stock exchanges and Nasdaq to prohibit the listing of any security of a company that does not have an audit committee that meets certain standards, as established by the statute and described below. The SEC on April 9, 2003 adopted Rule 10A-3 to implement this provision of the Act; it requires all U.S. stock exchanges and Nasdaq to adopt listing standards requiring as a minimum condition for original or continued listing of any equity or debt security (subject to certain exceptions) compliance by the listed company with the following requirements. The rule does not mandate that a listed company have a separate audit committee or address the size of the committee; however, if a company does not have an audit committee, then in accordance with Section 2(a)(3) of the Act, its full board of directors is considered as the audit committee and under the rule, as a condition of listing, all members of the board must meet the rule’s minimum independence standard, which would preclude any member of management from membership on the board.

• Audit Committee Independence. Every member of the audit committee must be “independent” in that he or she (i) may not accept any direct or indirect18 compensatory fee from the company or any of its subsidiaries, other than compensation for service as a director and certain kinds of deferred compensation19, and (ii) may not be an “affiliated person” of the company. An “affiliated person” is defined as “a person that directly, or indirectly through one or more intermediaries, controls, or is controlled by, or is under common control with, the person specified.”20 In determining control, a “safe harbor” is available under which a person who is not an executive officer of, and is not the beneficial owner of more than 10 percent of any class of voting securities of, the listed company would be deemed not to control the company.21 The exchanges and Nasdaq may adopt additional independence criteria for audit committee membership (which NYSE and Nasdaq have done in that audit committee members of their listed companies will be required to be independent under the standards required for a majority of board members, as discussed above.)

• Auditor Oversight. The audit committee must be provided authority over, and be made “directly responsible” for, appointing, compensating and retaining the company’s independent auditor and for overseeing the work of the auditor in preparing or issuing any audit report (and any related work), including resolving any disagreements between management and the auditor regarding financial reporting.

• “Accounting Complaint” Procedures. The audit committee must establish procedures for the receipt, retention and treatment of complaints regarding accounting, internal accounting controls or auditing matters and for the confidential, anonymous submission by employees of concerns regarding questionable accounting or auditing matters.22

• Authority to Engage Advisers . The audit committee must have authority to engage independent counsel and other advisers as the committee determines necessary to carry out its duties.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 11

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

• Authority over Funding of Audits and Compensation of Audit Committee Advisers and Activities. The listed company must provide funding, as determined by the audit committee to be appropriate, for compensation for (i) the audit work of the company’s independent auditor, (ii) any other audit, review or attest services provided to the company by a registered public accounting firm, (iii) any advisers engaged by the audit committee and (iv) the committee’s ordinary administrative expenses.

The rule establishes these as minimum standards for listing and the exchanges and Nasdaq are permitted to establish other standards regarding audit committees and other corporate governance matters that go beyond these requirements, including provisions which coordinate the minimum standards required with respect to audit committees to the other corporate governance listing standards which the NYSE and Nasdaq have done (as discussed below). (Examples would be a requirement regarding the minimum size of the audit committee or a requirement that a “cooling off” period be used in applying the no-compensation or no-affiliation independence criteria.) Listing standards sufficient to comply with Rule 10A-3 had to be proposed by the exchanges and Nasdaq by July 15, 2003 and must be approved by the SEC by December 1, 2003. These standards must provide that listed issuers be in compliance with these standards by the earlier of the listed issuer’s first annual meeting after January 15, 2004 or October 31, 2004, except for foreign private issuers and small business issuers23 who will have until July 31, 2005 to come into compliance. Approval of Audit Engagements and of Non-Audit Services To Be Provided by an Auditor (Sections 201 & 202 of the Act / Sections 10A(h) & (i) of the Exchange Act). In addition to the foregoing requirements under Section 301 pertaining to listed companies, the Act requires for all companies whose securities trade in the U.S.24 that the audit committee (or, if none, the full board of directors) approve all audit services (including the provision of a comfort letter in connection with a securities offering) and, as well, all permitted non-audit services to be provided by the auditor or its associated persons,25 before the services are provided (subject to certain di minimus exceptions).26 Required Reports to the Audit Committee (Section 204 of the Act / Section 10A(k) of the Exchange Act). The Act and the implementing regulations also require for all companies whose securities trade in the U.S. (even if none of the company’s securities are listed on an exchange or Nasdaq) that the auditor report to the audit committee on a timely basis (i) all critical accounting policies and practices used in the company’s audited financial statements, (ii) all alternative treatments of financial information within generally accepted accounting principles that have been discussed with management officials of the issuer, the ramifications on the use of such alternative disclosures and treatments and the treatment preferred by the auditor and (iii) other material written communications between the auditor and the company’s management such as a management letter or schedule of unadjusted differences.27 Audit Committee Financial Expert Disclosure (Section 407 of the Act and Item 401(h) of Regulation S-K). All companies whose securities trade in the U.S (even if none of the company’s securities are listed on an exchange or Nasdaq) must disclose in their annual reports whether or not the audit committee includes at least one member who is a “financial expert” (and, if not, the reasons), subject to certain exceptions. The identity of the expert and whether he is independent under the standards of Rule 10A-3 must also be disclosed. An “audit committee financial expert” is a person who, as a result of (a) education and experience as a public accountant, auditor, principal financial officer, controller or principal accounting officer of a company, or a position involving similar functions, (b) experience actively supervising a principal financial officer, principal accounting officer, controller, public accountant, auditor or

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 12

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

person performing similar functions, (c) experience overseeing or assessing the performance of companies or public accountants with respect to the preparation, auditing or evaluation of financial statements, or (d) other relevant experience; has (i) an understanding of financial statements, generally accepted accounting principles (“GAAP”), internal controls and procedures for financial reporting and audit committee functions, (ii) an ability to assess the general application of GAAP in connection with accounting for estimates, accruals and reserves and (iii) experience in preparing, auditing, analyzing or evaluating financial statements that present a breadth and level of complexity comparable to that which can be expected to be raised by the company’s financial statements, or experience in actively supervising one or more persons engaged in such activities.28 Code of Ethics for Senior Financial Officers and Chief Executive Officer (Section 406 of the Act; Item 406 of Regulation S-K and Item 10 of Form 8-K). The audit committee is often given the responsibility of ensuring compliance with the company’s code of ethics. (See “Codes of Conduct and Ethics; Governance Guidelines,” below.) Required CEO/CFO Reports to the Audit Committee (Section 302 of the Act; Rule 13a-14). In addition, under the Act and the implementing regulations, the chief executive officer and chief financial officer of each company whose securities trade in the U.S. (even though not listed, subject to certain very limited exceptions) are required to certify along with each quarterly and annual financial report submitted by the company to the SEC that the report does not contain any untrue statement of a material fact or omit to state a material fact and he or she is responsible for establishing and maintaining the company’s system of internal financial and disclosure controls and procedures and based on his or her evaluation of such system in connection with the annual report he or she has reported to the audit committee and the independent auditor: (i) all significant deficiencies in the design or operation of the company’s internal controls which could adversely affect the company's ability to record, process, summarize and report financial data, and identified for the auditors any material weaknesses in the internal controls; and (ii) any fraud, whether or not material, that involves management or other employees who have a significant role in the issuer's internal controls. The CEO and CFO must also certify that any periodic report that contains financial statements fully complies with the requirements of section 13(a) or 15(d) of the Exchanges Act and fairly presents, in all material respects, the financial condition, results and operations of the issuer. Attorney Reports of Material Violations (Section 307 of the Act; Part 205 of the SEC Rules of Practice). Under the attorney responsibility rules implementing Section 307 of the Act, attorneys representing an SEC reporting company are required to report to the company’s audit committee (assuming the company has one or, if not, to the full board of directors) credible evidence of which the attorney becomes aware of any material violation of the U.S. securities laws or material breach of a fiduciary duty under U.S. law, or similar material violation of U.S. law, if, after reporting the evidence to the company’s chief legal officer, the company has not provided an appropriate response to the report within a reasonable time. If in response to such a report the company determines to assert a defense in any proceeding relating to the reported evidence (assuming there is a “colorable defense” for purposes of the rules), the audit committee is required to approve the retention of counsel who will assert such defense and the chief legal officer is required to report to the audit committee regularly on the progress of the proceeding. Companies have the option under these regulations to establish, in advance of receiving a report, a “qualified legal compliance committee” of its board of directors to act on such attorney reports (either to receive, in lieu of the chief legal

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 13

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

officer, such reports or to investigate and act on reports received by the chief legal officer and referred to it by him and, in either case, to determine any remedial action to be taken in the event a material violation is found to have occurred), in which case such committee, rather than the audit committee, would deal with such matters. Such a committee must be composed entirely of independent directors and one member must be a member of the audit committee. The SEC has indicated that it expects to apply the same definition of independence for this purpose that it has established under Rule 10A-3 to determine independence for audit committee purposes. Alternatively, the audit committee may be designated as the company’s qualified legal compliance committee and given the functions and authority the regulations require such committee to have.

NYSE REQUIREMENTS (§ 303A (¶ ¶ 6, 7) of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(d), (m))

Independent Audit Committee Required. As the NYSE has required for many years, all listed companies must have an audit committee, composed of at least three members, all of whom must be independent. The independence standards discussed above will apply for this purpose. Additional Independence Requirements for Audit Committee Members . An audit committee member must meet the independence requirements of Section 301 of the Act and Exchange Act Rule 10A-3(b)(1) (subject to the exemptions provided for in Rule 10A-3(c)) (discussed above).

Independent Audit Committee Required. As Nasdaq has required since 1999, all listed companies must have an audit committee, composed of at least three members, all of whom must be independent. Nasdaq’s independence standards, as discussed above, will apply for the purpose of determining audit committee eligibility; provided, however, that one member need not meet such standards if the board of directors has determined under “exceptional and limited circumstances” that such individual’s membership is required by the best interest of the company and its shareholders and he (i) meets the criteria for audit committee membership of Section 10A(m)(3) and the rules thereunder, and (ii) is not a current officer or employee or a family member of an employee. The board must disclose in the proxy statement for the next annual meeting (or, if the company does not file a proxy statement, in its annual report) subsequent to such determination the nature of the relationship and the reasons for that determination. However, a member appointed on such an exceptional basis may not serve longer than two years and may not chair the committee. Additional Independence Requirements for Audit Committee Members . An audit committee member must meet the independence requirements of Section 301 of the Act and Exchange Act Rule 10A-3(b)(1) (subject to the exemptions provided for in Rule 10A-3(c)) (discussed above) and must not have participated in the preparation of the financial statements of the company or any current subsidiary at any time during the past three years.30

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 14

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

Other Audit Committee Membership Requirements – Financial Literacy; Financial Expertise. Audit committee members must be financially literate, as determined by the board, or must become financially literate within a reasonable period of time following their appointment. In addition, at least one member of the committee (who need not be the committee chair) must have “accounting or related financial management expertise.” A board may presume that a person who would be considered an audit committee financial expert under Section 407 of the Act as expressed in Item 401(h) of Regulation S-K has accounting or related financial management expertise.29

Other Audit Committee Membership Requirements – Financial Literacy. Audit committee members must be able to read and understand financial statements at the time of appointment. In addition, at least one member of the committee will be required to have had past employment experience in finance or accounting, professional certification in accounting or other comparable experience or background such as being or having been a chief executive officer, chief financial officer or other senior official with financial oversight responsibilities, that results in the individual’s financial sophistication. A director who qualifies as an audit committee financial expert under Item 401(h) of Regulation S-K is presumed to qualify as a financially sophisticated audit committee member.

Audit Committee Responsibilities/Charter. The audit committee charter (which must be in writing) must specify the committee’s purpose, which must include assisting board oversight of:

• the integrity of the company’s financial statements; • the company’s compliance with legal and regulatory

requirements; • the independent auditor’s qualifications and independence;

and • the performance of the company’s internal audit function

and independent auditors. The charter must also detail the duties and responsibilities of the audit committee, including:

• appointing, retaining, compensating, evaluating and terminating the company’s independent auditors (this includes resolving disagreements between management and the independent auditor);

• establishing procedures for the receipt, retention and treatment of complaints from company employees on accounting, internal accounting controls or auditing matters,

Audit Committee Responsibilities/Charter. The audit committee charter (which must be in writing) must specify the scope of the committee’s responsibilities (including structure, processes and membership requirements) and specify:

• the committee’s responsibility for ensuring the receipt from the independent auditor of a formal, written statement delineating all relationships between the auditor and the company, consistent with auditor professional responsibility standards (I.S.B. No. 1); and for actively engaging in a dialogue with the auditor with respect to a disclosed relationship or services that may impact the objectivity and independence of the auditor and for taking, or recommending that the board take, appropriate action to oversee the independence of the auditor;

The committee’s authority over and responsibility for, as provided by the Act:

• appointing, retaining, compensating, evaluating and terminating the company’s independent auditors (this includes resolving disagreements between management and the independent auditor);

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 15

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

as well as for the confidential, anonymous submissions by company employees of concerns regarding questionable accounting or auditing matters;

• having the authority to engage independent counsel and other advisors as it determines necessary to carry out its duties; and

• receiving appropriate funds, as determined by the audit committee, from the company for payment of compensation to the outside legal, accounting or other advisors employed by the audit committee.

Note: The foregoing charter requirements correspond to the requirements of Rule 10A-3. • at least annually, to obtain and review a report by the

independent auditor describing (i) the auditor’s internal quality control procedures, (ii) any material issues raised by the auditor’s most recent internal quality control review or by its most recent peer review or raised within the preceding five years by any investigation or inquiry by governmental or professional authorities of an independent audit carried out by the firm and any steps taken to deal with such issues and (iii) in order to assess the auditor’s independence, all relationships between the independent auditor and the company;

• to discuss the annual audited financial statements and quarterly financial statements with management and the independent auditor and the company’s disclosure in the related “Management’s Discussion and Analysis of Financial Condition and Results of Operations”;

• to discuss earnings press releases, as well as financial information and earnings guidance that is given to analysts and rating agencies;

• to discuss policies with respect to risk assessment and risk

• establishing procedures for the receipt, retention and treatment of complaints from company employees on accounting, internal accounting controls or auditing matters, as well as for the confidential, anonymous submissions by company employees of concerns regarding questionable accounting or auditing matters;

• having the authority to engage independent counsel and other advisors as it determines necessary to carry out its duties; and

• receiving appropriate funds, as determined by the audit committee, from the company for payment of compensation to the outside legal, accounting or other advisors employed by the audit committee.

Note: The foregoing charter requirements correspond to the requirements of Rule 10A-3. In addition, the committee is responsible for assessing annually the sufficiency of its charter.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 16

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

management; • to meet separately, periodically, with management, with the

internal auditors and with the independent auditors; • to review with the independent auditor any audit problems

or difficulties and management’s response; • to set clear hiring policies for employees or former

employees of the independent auditor; and • to report regularly to the board on any issues that arise

within its oversight responsibilities. In addition, the committee is responsible for:

• preparing an audit committee report that SEC rules require be included in the company’s annual proxy statement; and

• conducting an annual evaluation of its performance of its responsibilities.

The company’s website must include the charter of the audit committee. The company’s annual report must state that the charter is available on its website and that it is available in print to any shareholder that requests it.

Related Party/Conflict of Interest Transactions . No specific audit committee responsibility, except insofar as implicit in the other audit committee responsibilities referred to above. However, the board is required to establish a code of conduct that addresses conflict of interest transactions.31

Related Party/Conflict of Interest Transactions . All related party transactions must be approved by the audit committee (or comparable independent body of the board) as part of the company’s obligation to conduct an “appropriate review … on an on-going basis” of such transactions. “Related party transaction” refers to transactions that are required to be disclosed pursuant to Regulation S-K, Item 404. For a body to be deemed “comparable” to the audit committee, all directors of such a body that review and approve a related party transaction must be independent under Nasdaq rules and also disinterested in the transaction. 32

Internal Audit. Every company must have an internal audit function. As indicated above, the audit committee will have oversight responsibility over such function.

Internal Audit. Not mandated.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 17

COMPOSITION AND ROLE OF THE AUDIT COMMITTEE (CONTINUED)

Cure. Listed companies will be provided the opportunity to cure any defects for failing to comply with any of the requirements of Section 301 and Rule 10A-3 discussed above.

Cure. If a company fails to comply with the audit committee composition requirements because a committee member is no longer independent for reasons beyond the member’s reasonable control, or due to a vacancy on the committee, the company will have up to the earlier of its next annual meeting or one year from the event that caused the failure to comply with the composition requirements. A company relying on this provision must provide notice to Nasdaq immediately upon learning of the event or circumstance that caused the noncompliance.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 18

OTHER BOARD COMMITTEE REQUIREMENTS

SARBANES-OXLEY ACT/SEC RULES

The Act does not address the role or composition of board committees, other than the audit committee.33 NYSE REQUIREMENTS

(§ 303A, ¶¶ 4, 5 of the Listed Company Manual) NASDAQ REQUIREMENTS

(Rule 4350(c)) Nominating/Corporate Governance Committee. The nominating/corporate governance committee composed of independent directors must have a written charter34 that addresses the committee’s purpose and responsibilities, which must include:

• identifying individuals who are qualified to become board members consistent with criteria that was approved by the full board and selecting, or recommending that the board select, the director nominees for election at the annual meeting of shareholders;

• developing and recommending to the board a set of corporate governance principles for the corporation; and

• overseeing the evaluation of the board and management. The committee also must conduct an annual evaluation of its performance. In addition, the charter should give the committee sole authority to hire and fire any search firm to be used to identify director candidates.35 The company’s website must include the charters of its most important committees (this could be applicable to the nominating/corporate governance committee). If the charter is on the company’s website, the company’s annual report must state that and that it is available in print to any shareholder that requests it.

If the company is required by contract or otherwise to provide a party the ability to nominate one or more directors, the selection and nomination of such directors need not be subject to the nominating committee process.

Nominating/Corporate Governance Committee. A nominating committee composed of independent directors must have the authority to select or recommend for the board’s selection individuals for election as directors, unless the independent directors as a group have such authority (except that one member of the nominating committee need not be an independent director in limited and exceptional circumstances), as described above under “Role and Authority of Independent Directors.”36 Companies must adopt a charter or board resolution, as applicable, regarding the nominations process and other such related matters as may be required under the federal securities laws (such as disclosures about shareholder nominees required in a company’s proxy statement). However, the rules do not provide specific requirements for the nominating committee charter. The Nasdaq listing standards do not require a corporate governance committee. Where the right to nominate a director does not reside with a company by reason of a lawful arrangement, the provision for nomination of directors by independent directors does not apply. However, the company is still obligated to comply with the nominating, compensation and audit committee composition requirements under the listing standards.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 19

OTHER BOARD COMMITTEE REQUIREMENTS (CONTINUED)

NYSE REQUIREMENTS (§ 303A, ¶¶ 4, 5 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(c))

Compensation Committee. The compensation committee composed of independent directors must have a written charter37 that addresses the committee’s purpose and responsibilities, which must include:

• producing a compensation committee report on executive compensation that must be included in the company’s annual proxy statement or in the company’s annual report;

• reviewing and approving corporate goals and objectives relevant to compensation of the chief executive officer, evaluating the CEO’s performance in light of those goals and objectives, and either as a committee or together with the other independent directors (as directed by the board), determining and approving the CEO’s compensation level based on such evaluation;38 and

• making recommendations to the board with respect to non-CEO compensation, incentive compensation plans and equity-based plans.39

The committee must also conduct an annual evaluation of its performance. In addition, the charter should give the committee sole authority to retain and terminate any consulting firm to assist in the evaluation of director or senior executive compensation, including sole authority to approve the firm’s compensation and other retention terms. The company’s website must include the charters of its most important committees (this could be applicable to the compensation committee). If the charter is on the company’s website, the company’s annual report must state that and that it is available in print to any shareholder that requests it.

Compensation Committee. The rules do not require a charter for the compensation committee. Note that a compensation committee composed of independent directors must have the authority to determine or recommend to the board for determination the compensation of all officers, unless the independent directors as a group have such authority (except that one member of the compensation committee need not be an independent director in limited and exceptional circumstances), as described above under “Role and Authority of Independent Directors.”40

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 20

CODES OF CONDUCT AND ETHICS; GOVERNANCE GUIDELINES

SARBANES -OXLEY ACT / SEC RULES

Code of Ethics for Senior Financial Officers and Chief Executive Officers (Section 406 of the Act; Item 406 of Regulation S-K and Item 10 of Form 8-K). Companies are required to disclose in their annual reports whether or not they have adopted a code of ethics applicable to their principal financial officer and comptroller or principal accounting officer and, as a result of SEC rulemaking, their principal executive officers as well (and, if not, why not). The code of ethics must include standards reasonably necessary to promote: honest and ethical conduct, including the handling of actual or apparent conflicts of interest between personal and company interests; full, fair, accurate, timely and understandable disclosure in SEC periodic reports; and compliance with applicable governmental rules. In addition, the company must promptly disclose any change in or waiver of the code of ethics. While the SEC’s rules do not explicitly require board oversight of the code of ethics, given the seniority of the officers involved and the subject matter, responsibility to adopt and oversee the code will usually be a board responsibility, which, given the customary audit committee charter, may fall within the audit committee’s responsibilities.41 Interference with Audits (Section 303 of the Act; Rule 13b2-2 of the Exchange Act). No action may be taken by any director or officer of the company (or other person acting under the direction thereof), to fraudulently influence, coerce, manipulate or mislead any independent auditor of the company’s financial statements if that person knew or should have known that such action, if successful, could result in rendering the financial statements materially misleading.42

NYSE REQUIREMENTS (§ 303A, ¶¶ 9, 10 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(n))

Code of Business Conduct and Ethics. Companies are required to adopt and disclose a Code of Business Conduct and Ethics for directors, officers and employees that addresses:

• conflicts of interest; • corporate opportunities; • confidentiality; • fair dealing; • protection and proper use of company assets; • compliance with laws, rules and regulations (including

insider trading laws); and • encouraging the reporting of any illegal or unethical

behavior.

Code of Conduct. Companies must adopt a code of conduct for all directors, officers and employees that is publicly available and includes the elements necessary to meet the code of ethics requirements established by the SEC pursuant to Section 406 of the Act. In addition, the code must provide for an enforcement mechanism.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 21

CODES OF CONDUCT AND ETHICS; GOVERNANCE GUIDELINES (CONTINUED)

NYSE REQUIREMENTS (§ 303A, ¶¶ 9, 10 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(n))

Waivers . Companies must promptly disclose any waivers under the Code of Business Conduct and Ethics given to directors or executive officers and the waivers must be approved by the board or a board committee.

Waivers . Companies must disclose any waivers given to executive officers or directors and the waivers must be approved by the board.

Corporate Governance Guidelines. Companies are required to adopt and disclose corporate governance guidelines, which must address:

• director qualification standards; • director responsibilities; • director access to management and, as necessary and

appropriate, to independent advisors; • director compensation; • director orientation and continuing education; • management succession; and • an annual self-evaluation of the board’s performance.

The company’s website must include its corporate governance guidelines and the charters of its most important committees (including at least the audit committee). The company’s annual report must state that the foregoing information is available on its website and that it is available in print to any shareholder who requests it.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 22

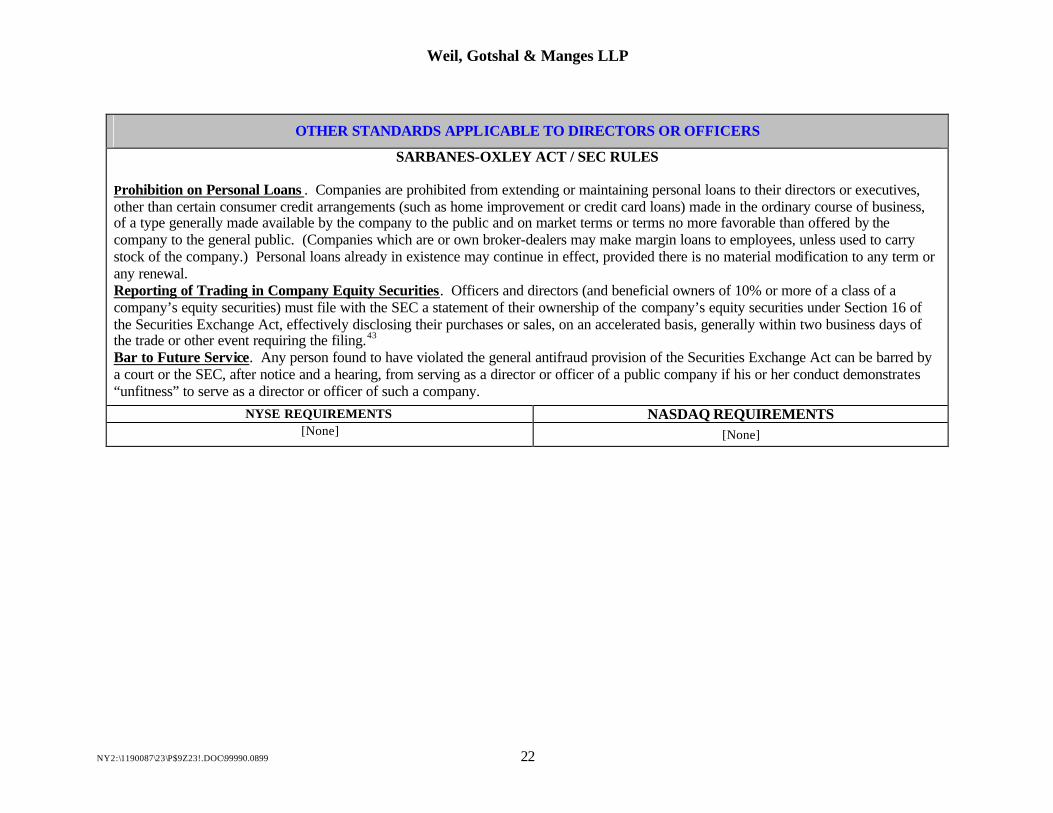

OTHER STANDARDS APPLICABLE TO DIRECTORS OR OFFICERS

SARBANES-OXLEY ACT / SEC RULES

Prohibition on Personal Loans . Companies are prohibited from extending or maintaining personal loans to their directors or executives, other than certain consumer credit arrangements (such as home improvement or credit card loans) made in the ordinary course of business, of a type generally made available by the company to the public and on market terms or terms no more favorable than offered by the company to the general public. (Companies which are or own broker-dealers may make margin loans to employees, unless used to carry stock of the company.) Personal loans already in existence may continue in effect, provided there is no material modification to any term or any renewal. Reporting of Trading in Company Equity Securities. Officers and directors (and beneficial owners of 10% or more of a class of a company’s equity securities) must file with the SEC a statement of their ownership of the company’s equity securities under Section 16 of the Securities Exchange Act, effectively disclosing their purchases or sales, on an accelerated basis, generally within two business days of the trade or other event requiring the filing.43 Bar to Future Service. Any person found to have violated the general antifraud provision of the Securities Exchange Act can be barred by a court or the SEC, after notice and a hearing, from serving as a director or officer of a public company if his or her conduct demonstrates “unfitness” to serve as a director or officer of such a company.

NYSE REQUIREMENTS NASDAQ REQUIREMENTS [None] [None]

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 23

SHAREHOLDER APPROVAL REQUIREMENTS

SARBANES-OXLEY ACT / SEC RULES

The Act does not address shareholder approval requirements.44 EXISTING NYSE RULES

(§ 312.03(b), (c) and (d) of the Listed Company Manual) EXISTING NASDAQ RULES

(Rule 4350(i)(1)(B)-(D))

Voting on Common Stock Issuance and Change of Control. Shareholders must be given the opportunity to vote to approve or disapprove the issuance of securities to:

(1) a director, officer or substantial security holder of the company (a “Related Party”); (2) a subsidiary, affiliate or other closely-related person of a Related Party; or (3) any company or entity in which a Related Party has a substantial direct or indirect interest;

if the number of shares of common stock to be issued, or if the number of shares of common stock into which the securities may be convertible or exercisable, exceeds either 1% of the number of shares of common stock or 1% of the voting power outstanding before the issuance. Shareholders must be given the opportunity to vote to approve or disapprove the issuance of securities, in any transaction or series of related transactions if:

(1) the common stock has, or will have upon issuance, voting power equal to or in excess of 20 percent of the voting power outstanding before the issuance of such stock or of securities convertible into or exercisable for common stock; or (2) the number of shares of common stock to be issued is, or will be upon issuance, equal to or in excess of 20 percent of the number of shares of common stock outstanding before the issuance of the common stock or of securities convertible into or exercisable for common stock;

Voting on Common Stock Issuance and Change of Control. Shareholders must be given the opportunity to vote to approve or disapprove the issuance of designated securities in connection with the acquisition of the stock or assets of another company if:

(1) any Related Party has a 5% or greater interest (or such persons collectively have a 10% or greater interest), directly or indirectly, in the company or assets to be acquired or in the consideration to be paid in the transaction(s) and the issuance of securities could result in an increase in outstanding common shares or voting power of 5% or more; or (2) where, due to the present or potential issuance of securities other than a public offering for cash:

(a) the common stock has or will have upon issuance voting power equal to or in excess of 20% of the voting power outstanding before the issuance of such securities; or (b) the number of shares of common stock to be issued is or will be equal to or in excess of 20% of the number of shares or common stock outstanding before the issuance of the securities.

Shareholders must be given the opportunity to vote to approve or disapprove the issuance of designated securities in connection with a transaction (other than a public offering) involving: (i) the sale, issuance or potential issuance by the issuer of securities at a price less than the greater of book or market value which together with sales by Related Parties of the company equals 20% or more of common stock or 20% or more of the voting power outstanding before the issuance; or

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 24

SHAREHOLDER APPROVAL REQUIREMENTS (CONTINUED)

EXISTING NYSE RULES (§ 312.03(b), (c) and (d) of the Listed Company Manual)

EXISTING NASDAQ RULES (Rule 4350(i)(1)(B)-(D))

subject to certain limited exceptions. Shareholders must be given the opportunity to vote to approve or disapprove an issuance that will result in a change of control of the issuer.

(ii) the sale, issuance or potential issuance by the company of securities equal to 20% or more of the common stock or 20% or more of the voting power outstanding before the issuance for less than the greater of book or market value of the stock

Shareholders must be given the opportunity to vote to approve or disapprove an issuance that will result in a change of control of the issuer. Exceptions to the above shareholder approval requirements may be made upon application to Nasdaq when the delay in securing stockholder approval would seriously jeopardize the financial viability of the enterprise and reliance by the company on this exception is expressly approved by the audit committee or a comparable body of the board of directors.

NYSE REQUIREMENTS (§ 303A, ¶ 8 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(i)(1)(A)

Voting on Equity Compensation Plans. Shareholders must be given the opportunity to vote to approve or disapprove all equity-compensation plans and material revisions thereto, except employment-inducement awards, option plans acquired through mergers, tax-qualified plans such as ESOPs and 401(k) plans, plans that merely provide a convenient way to purchase shares on the open market or from the listed company at fair market value and plans that are made available to shareholders generally; brokers may only vote customer shares on proposals for such plans pursuant to customer instructions.45

Voting on Equity Compensation Plans. Shareholder approval must be obtained for all stock option plans and for any material modification of such plans except for inducement grants to new employees if such grants are approved by an independent compensation committee or a majority of the independent directors, certain tax qualified, non-discriminatory employee benefit plans if such plans are approved by an independent compensation committee or a majority of the independent directors, option plans acquired through mergers and plans that merely provide a convenient way to purchase shares on the open market or from the issuer at fair market value.46

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 25

EDUCATION AND TRAINING OF DIRECTORS

SARBANES-OXLEY ACT / SEC RULES

The Act does not address education and training of directors. NYSE REQUIREMENTS NASDAQ REQUIREMENTS

Continuing Education of Directors . Listed companies’ corporate governance guidelines will be required to address the matter of continuing education and training of directors and NYSE has indicated that it intends to help develop and sponsor appropriate director education and training programs.

Continuing Education of Directors . Nasdaq has announced that it will provide directors of listed companies opportunities to receive relevant continuing education regarding their governance responsibilities.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 26

APPLICABILITY TO NON-U.S. COMPANIES

SARBANES-OXLEY ACT / SEC RULES

Many of the Act’s provisions (including those referred to above) apply to all companies (organized within or outside the U.S.) that have registered equity or debt securities with the SEC under the Securities Exchange Act of 1934, as amended, although some, including those regarding the composition and functioning of audit committees, apply only to companies (organized within or outside the U.S.) whose equity securities are listed on an exchange or on the Nasdaq Stock Market.47

Exemptions Relating to Foreign-Listed Company Audit Committees. Certain limited exemptions to the independence and other audit committee requirements of Rule 10A-3 apply to listed companies not organized in the U.S.48:

• Notwithstanding the no-compensation (and the no-affiliation) prong of the independence requirements, an employee of a foreign private issuer49 who is not an executive officer may sit on the audit committee if the employee was elected or named to the board of directors or audit committee of the company pursuant to home country legal or listing requirements or the company’s governing documents or a collective bargaining or similar agreement.

• Notwithstanding the no-affiliation prong of the independence requirements, a controlling shareholder, or representative of a controlling shareholder or shareholder group, may serve on the audit committee of a foreign private issuer if (i) such person satisfies the “no-compensation” prong of the independence requirements; (ii) such person has only observer status on, and is not a voting member or the chair of, the audit committee; and (iii) such person is not an executive officer of the company.

• Notwithstanding the no-affiliation prong of the independence requirements, a representative or designee of a foreign government or governmental entity that controls (or is under common control with) a foreign private issuer may serve on the audit committee of the foreign private issuer, if (i) such person satisfies the “no-compensation” prong of the independence requirements and (ii) such person is not an executive officer of the company.

• Foreign private issuers that have boards of auditors or statutory auditors as expressly required or permitted by home country legal or listing provisions need not have a separate independent audit committee if (i) such body is, as required by home country legal or listing requirements, separate from the company’s board of directors or includes person who are not directors, (ii) such body is responsible, in accordance with home country legal or listing provisions or the company’s governing documents, for the appointment, retention and oversight, to the extent permitted by law, of any registered public accounting firm engaged for the purpose of preparing or issuing any audit report or performing other audit, review or attest services for the company, (iii) such body is not elected by management of the company and no executive officer of the company is a member, and (iv) standards of independence from the company and its management are applicable to such body under home country legal or listing provisions. To the extent permitted by law, such body must establish complaint procedures and have the ability to hire advisers and be provided funds to compensate the company’s auditor and its advisers and for its operations as provided by Rule 10A-3 with respect to an audit committee.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 27

APPLICABILITY TO NON-U.S. COMPANIES (CONTINUED)

NYSE REQUIREMENTS (§ 303A, ¶ 11 of the Listed Company Manual)

NASDAQ REQUIREMENTS (Rule 4350(a))

Exemption of Foreign Issuers; Disclosures Required. The NYSE corporate governance standards will continue to defer to home-country practices in most instances. However, foreign issuers will be required to comply with most of the audit committee requirements (including committee independence, size and certain functions) and will also be required to promptly notify the NYSE after any executive officer of the company becomes aware of any material non-compliance with any applicable provisions of the listing standards. In addition, listed foreign issuers must disclose any significant ways in which their corporate governance practices differ from those required by the other NYSE listing standards. The disclosure may be made in a brief, general summary of material differences.

Exemption of Foreign Issuers; Disclosures Required. Subject to requirements applicable under Section 301 of the Act to audit committees, none of the listing standards shall apply to require a foreign private issuer to do any act that is contrary to law or a rule or regulation of any public authority exercising jurisdiction over it or that is contrary to generally accepted business practices in its country of domicile. Where a requirement is applicable, a foreign private issuer may obtain exemption from compliance with Nasdaq’s corporate governance listing standards (at the time of listing or thereafter), but must disclose the alternative practices it will follow in lieu of any waived requirement(s) annually in its annual report to the SEC.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 28

ENFORCEMENT

SARBANES-OXLEY ACT / SEC RULES

Enforcement and Sanction for Violation of Standards Relating to Listed Company Audit Committees. Rule 10A-3 prohibits the national securities exchanges and Nasdaq from listing or continuing the listing of securities of a company that is not in compliance with the audit committee requirements of the rule, subject to providing an opportunity for a listed company to cure its noncompliance. Accordingly, subject to the interpretive and any exemptive power which an exchange or Nasdaq has over its listing standards and subject to the opportunity to cure any noncompliance which must be provided to the listed company, delisting is mandated upon noncompliance with the audit committee requirements of the rule. Under the rule, the securities exchanges and Nasdaq must require each of their listed companies to notify them promptly after an executive officer of the listed company becomes aware of any material noncompliance by the listed company with the audit committee requirements of the rule. Enforcement and Sanction for Violation of Other Corporate Governance Requirements of the Act. With regard to the disclosure and other requirements of the Act discussed above, the Act provides the SEC with authority to promulgate rules and regulations in furtherance of the Act (which generally should provide it with interpretive and exemptive power) and treats a violation of the Act as a violation of the Securities Exchange Act, for which a broad variety of sanctions may be imposed.50

NYSE REQUIREMENTS NASDAQ REQUIREMENTS

CEO Certification. The company’s chief executive officer must certify each year that he is not aware of any violations of the NYSE listing standards. The certification must be disclosed in each annual report to shareholders.

Notification. Each company CEO will be required to promptly notify the NYSE in writing after any executive officer of the company becomes aware of any material noncompliance with any applicable provisions of the listing standards.

Notification. Each company is required to promptly notify Nasdaq after an executive officer becomes aware of any material noncompliance with Nasdaq’s corporate governance rules.

Public Reprimand Letter and Delisting. Upon finding a violation of an Exchange listing standard, the NYSE may issue a public reprimand letter to any company and ultimately suspend or delist an offending company.

Delisting . A material misrepresentation or omission by a company to Nasdaq may result in the company’s being delisted.

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 29

ENDNOTES

1 A company that relies upon the controlled company exemption must disclose in its annual proxy statement (or, if the company does not file a

proxy statement, in its annual report) that it is a controlled company and the basis for that determination.

2 See endnote 1.

3 Controlled companies, limited partnerships and companies in bankruptcy are exempt. See endnote 1.

4 Controlled companies, limited partnerships and companies in bankruptcy are exempt. See endnote 1.

5 For this purpose, “executive officers” are those persons subject to the “short-swing” trading reporting requirements of Section 16(a) of the Securities Exchange Act, as defined in SEC Rule 16a-1(f) as officers. A person who is classified as an “executive officer” under SEC Regulation S-K, Item 401(b) is considered an officer for purposes of Rule 16a-1(f) and, thus, for purposes of these listing standards.

6 Controlled companies are exempt. See endnote 1.

7 Controlled companies are exempt. See endnote 1.

8 The commentary indicates that a “material relationship” can include commercial or industrial (presumably including as a supplier or customer), banking, consulting, legal, accounting, charitable and familial relationships, among others.

9 References to “company” include a parent or subsidiary that is in a consolidated group with the company.

10 An immediate family member includes a person’s spouse, parents, children, siblings, mothers- and fathers-in-law, sons- and daughters-in-law, brothers- and sisters-in-law, and anyone (other than domestic employees) who shares such person’s home.

11 Service as an interim CEO or Chairman does not automatically disqualify a person from being considered independent following such employment.

12 Compensation received (i) for prior service as an interim Chairman or CEO need not be considered for this independence test and (ii) by an immediate family member for service as a non-executive employee of the listed company need not be considered for this independence test.

13 A “parent” or “subsidiary” includes entities that are controlled by the issuer and are consolidated with the financial statements of the issuer as filed with the SEC (but not if the issuer reflects such entity solely as an investment in its financial statement).

Weil, Gotshal & Manges LLP

NY2:\1190087\23\P$9Z23!.DOC\99990.0899 30

14 A family member includes a person’s spouse, parents, children, siblings, mothers- and fathers-in-law, sons- and daughters-in-law, brothers- and

sisters-in-law, whether by blood, marriage or adoption or someone who has the same residence as the person.

15 The payments and consolidated gross revenue numbers to be used for this independence test must be those from the last completed fiscal year. Charitable organizations are not considered “companies” for the purposes of this independence test. However, the listed company must disclose in its annual proxy statement (or, if the company does not file a proxy statement, in the company’s annual report) any charitable contributions from the company to a charitable organization that one of their directors is an executive officer of, if, within the previous three years, contributions in a single fiscal year exceeded the greater of 2% of such charity’s consolidated gross revenues or $1 million.

16 Payments received as compensation for board or committee service or arising solely from investments in the company’s securities, compensation paid to a family member who is an employee of the company or a parent or subsidiary of the company (but not if such person is an executive officer of the company or a parent or subsidiary of the company), benefits under a tax-qualified retirement plan or non-discretionary deferred compensation and loans permitted under Section 402 of the Act are excluded from the $60,000 limitation.

17 Payments arising solely from investments in the company’s securities or under non-discretionary charitable contribution matching programs are not included in the limitation.