nyc cpbi drafth tamends-may7rd

TRANSCRIPT

Who’s Risk Is It Anyway?

May 27, 2015

Henry TapperSimon Nelson, FCIA FSA

Four Worries and a Funeral

De-risking or re-risking?Can we democratize

ownership?Does choice equal freedom?

Is the State provider or facilitator?

And did this man kill British pensions?

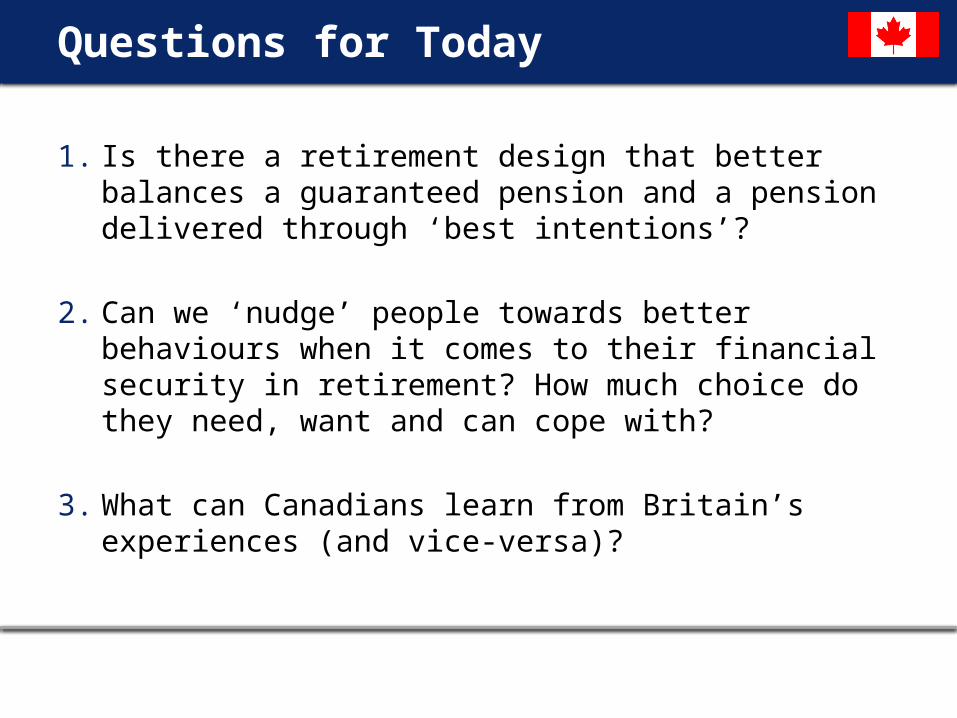

Questions for Today

1. Is there a retirement design that better balances a guaranteed pension and a pension delivered through ‘best intentions’?

2. Can we ‘nudge’ people towards better behaviours when it comes to their financial security in retirement? How much choice do they need, want and can cope with?

3. What can Canadians learn from Britain’s experiences (and vice-versa)?

Challenges with Traditional DB Plans

Low interest rates, volatile equity

markets, maturing plans, increasing

longevityUnacceptable volatility and

asymmetrical risks for plan sponsors

Mark-to-market accounting

Seen as a public sector employee

‘perk’

Relief measures are short-term solutions;

don’t address underlying issues

Complex regulatory environment

Challenges with Traditional CAP Plans

Predictable costs, but unpredictable benefits in

retirement

Members exposed to significant risks,

especially in retirement

Complex decisions left to plan members; ‘choice

overload’

Few efficient ‘decumulation’ products

Few benefits from pooling of costs/risks, reducing

efficiency

First ‘cohort’ of career-DC employees yet to reach

retirement

1. De-risking corporate pensions

But who will take on the risk?

Discussion #1

2. Democratising Pension Ownership

1. Triple lock on state pensions guarantees a minimum 2.5% pension increase p.a.

2. Public sector DB subject 3. Private sector DB protected by pension

protection fund4. Auto-enrolled DC pensions for 10m new

workers

1.2m DC pensions to be set up in next 3 years

But can employers help transfer the risk?

1.2m new employers set up workplace pensions

Where is Canada today?

1. Private Sector and Not for Profit

2. Public Sector

3. Multi-Employer Trades

Where is Canada today?

Private Sector and Not for Profit

• Legacy mode for DB (freezes and de-risking)

• Movement to fixed cost DC

• Unions the remaining stronghold for private sector DB

Where is Canada today?

Public Sector (with solvency exemptions)

• Municipal, Hospitals, University and Education sectors

• Generally unionized environment

• Lots of design and governance changes

• Consolidation of plans is the current theme

Where is Canada today?

Multi-Employer Trades

• Temporary solvency exemptions

• Still a strong DB landscape

• Need permanent funding rule solutions in most jurisdictions

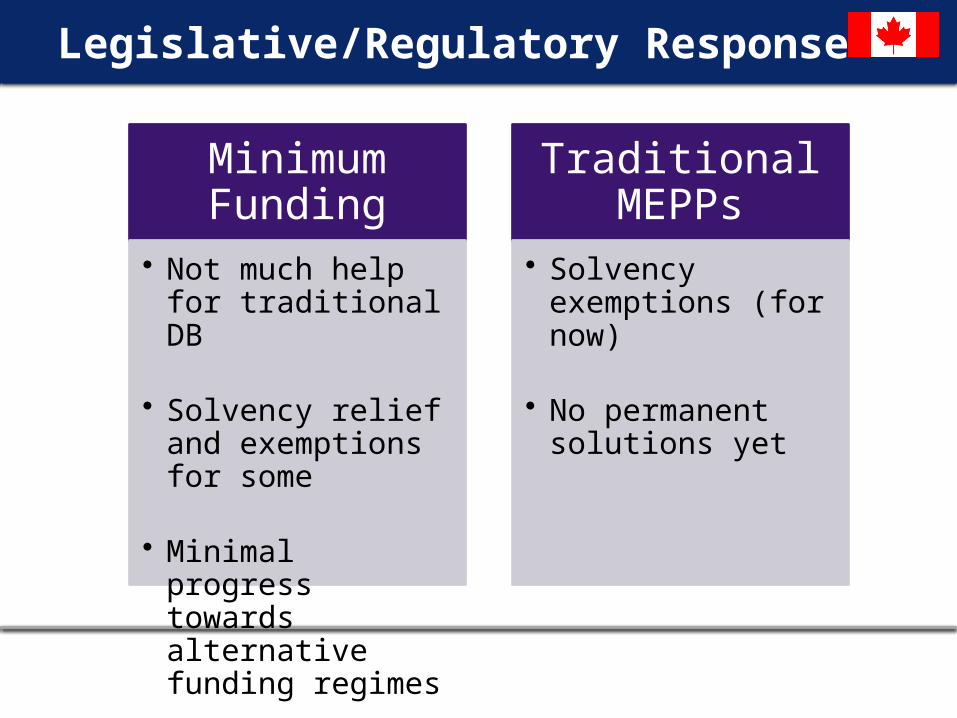

Legislative/Regulatory Response

1. Minimum Funding

2. Traditional MEPPs

3. Termination Benefits

4. Hurdles for Innovation

Legislative/Regulatory Response

Minimum Funding

• Not much help for traditional DB

• Solvency relief and exemptions for some

• Minimal progress towards alternative funding regimes

Traditional MEPPs

• Solvency exemptions (for now)

• No permanent solutions yet

Legislative/Regulatory Response

Termination Benefits

• Concepts of being ‘asset share based’

Hurdles for Innovation• Regulatory change

is slow

• Legal concerns; lawsuits in New Brunswick

• Many issues surround conversion, consent and funding

Discussion #2

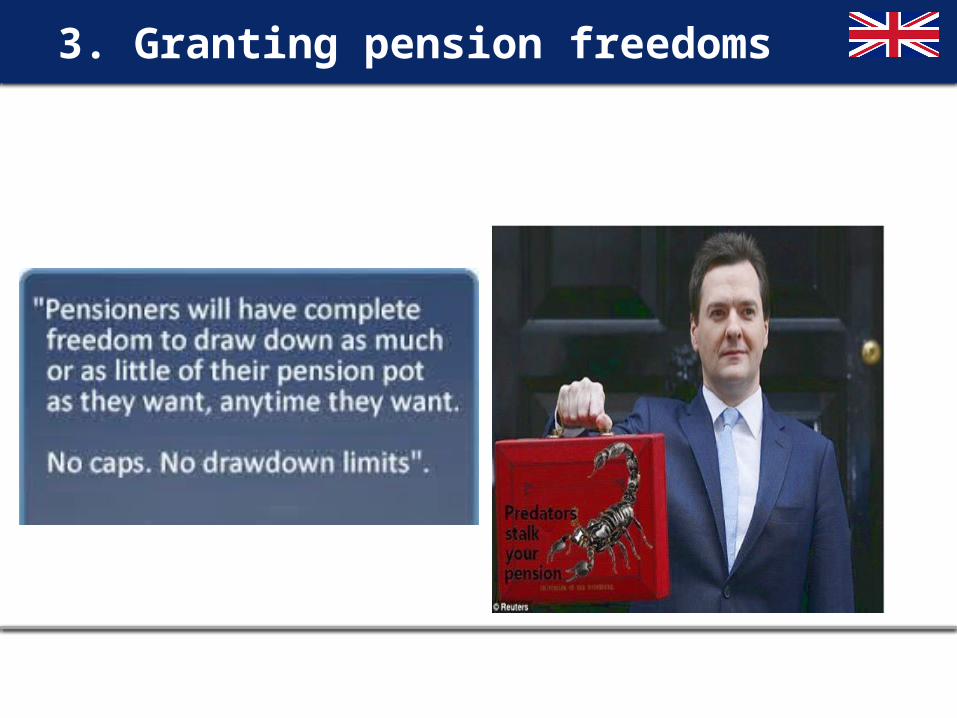

Where is Britain headed?

DrawdownCash Annuity

Freedom and choice Pension

Wise

State funded guidan

ce

3. Granting pension freedoms

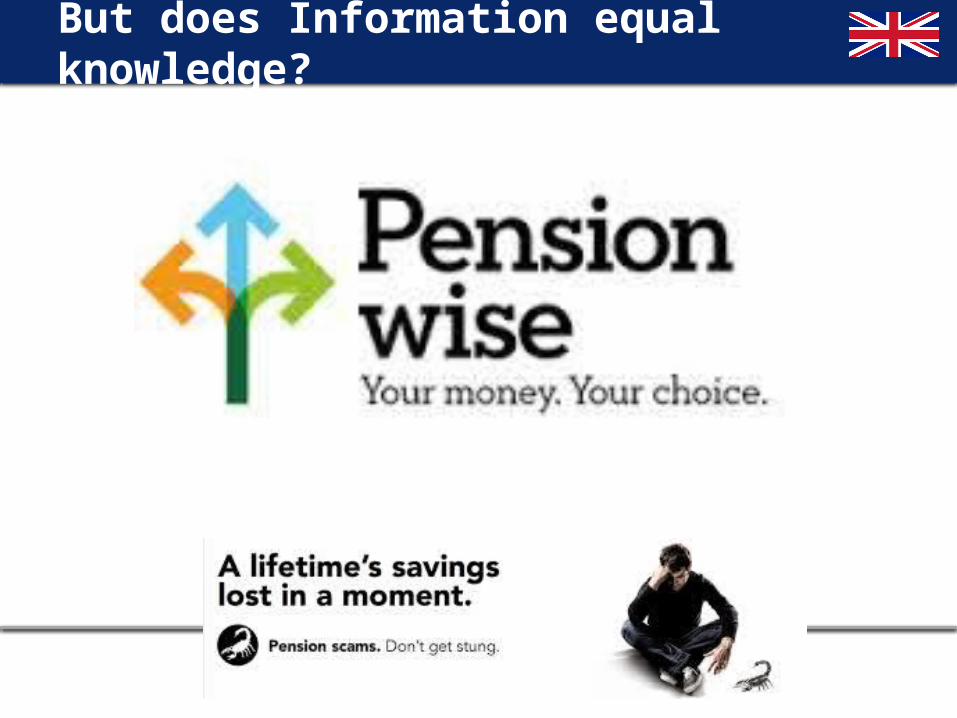

Plenty of information

But does Information equal knowledge?

Where is Canada headed?

Innovative Designs

Workplace Plans Expansions

and Enhancements

State Plans

Workplace Plans: Innovation

Push for regulators to be open to new types of pension deals and transitional approaches

Jointly Trusteed arrangements

Consolidation of plans and/or assets

Workplace Plans: Target Benefit Plans

TBPs, or ‘defined ambition’ plans, aim to combine the best of DB and DC (and remove the worst of both)

Typical features:1. Fixed contributions2. Members receive a target DB-type benefit, with few (or

no) guarantees3. Benefits may be adjusted up or down to balance

funding

Not currently accommodated by most jurisdictions’ regulations

Discussion #3

4. The State and British Pensions Providing -

Single state pension – simpler but less ambitious A safety net for insolvent DB covenants

Compelling – employers to auto-enrol staff in workplace Insurers to manage legacy and improve governance

Protecting– the consumer with charge caps

Educating - at retirement– Pension Wise

Facilitating risk sharing – Not New Brunswick (yet) Encouraging reluctant employers Enabling collective decumulation

State Plans

Hot political issue

Significant debate over extent of Canadian retirement crisis

Importance of state plans in Canada stems from: Poor usage of existing retirement savings vehicles

(RRSPs) Few employees covered by workplace pension plans Limited government support programs for middle

class

State Plans - CPP

Enhance Canada Pension Plan (CPP)

2013 efforts to enhance CPP stalled

Is now likely to be part of 2015 Federal election platforms

Provincial support is needed (but is mixed)

State Plans - ORPP

2. Development of Ontario Retirement Pension Plan (ORPP)

Belief that Ontario would prefer CPP enhancements; stalls have led to proposal of “Made in Ontario” MEPP-like mandatory public pension plan for Ontario employees,

Target is to replace15% of an employee’s earnings in retirement

Would supplement existing pension arrangements, personal savings, CPP, OAS and GIS

Grappling with questions on implementation and design– particularly breadth of scope, earnings thresholds and self-employed

citizens

Discussion #4

Wrap Up

Who’s risk is it anyway?