nutritec group – commitment to lead the russian baby food market

TRANSCRIPT

November 2005

Nutritec Group –Commitment to lead

the Russianbaby food market

Credit Linked Notes

2Credit Linked Notes November 2005

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Contents

page

Summary 3

The Russian dairy market: impressive growth rates and great potential 4

Whole milk is more than a half of the market. Other products will grow faster 6

Competition: growing concentration 7

Business Strategy: commitment to leadership, growth and profitability 12

Corporate history and structure 17

Growth of networks will increase sales and distribution value 19

Revenue structure 22

Cost structure 23

Capex: when and how much? 24

Nutritec peer comparison: tougher covenants, lower leverage 25

Consolidated Balance Sheet of Nutritec 26

Consolidated Income Statement of Nutritec 27

Consolidated Cash Flow Statement of Nutritec 27

Credit Linked Notes November 2005 3

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

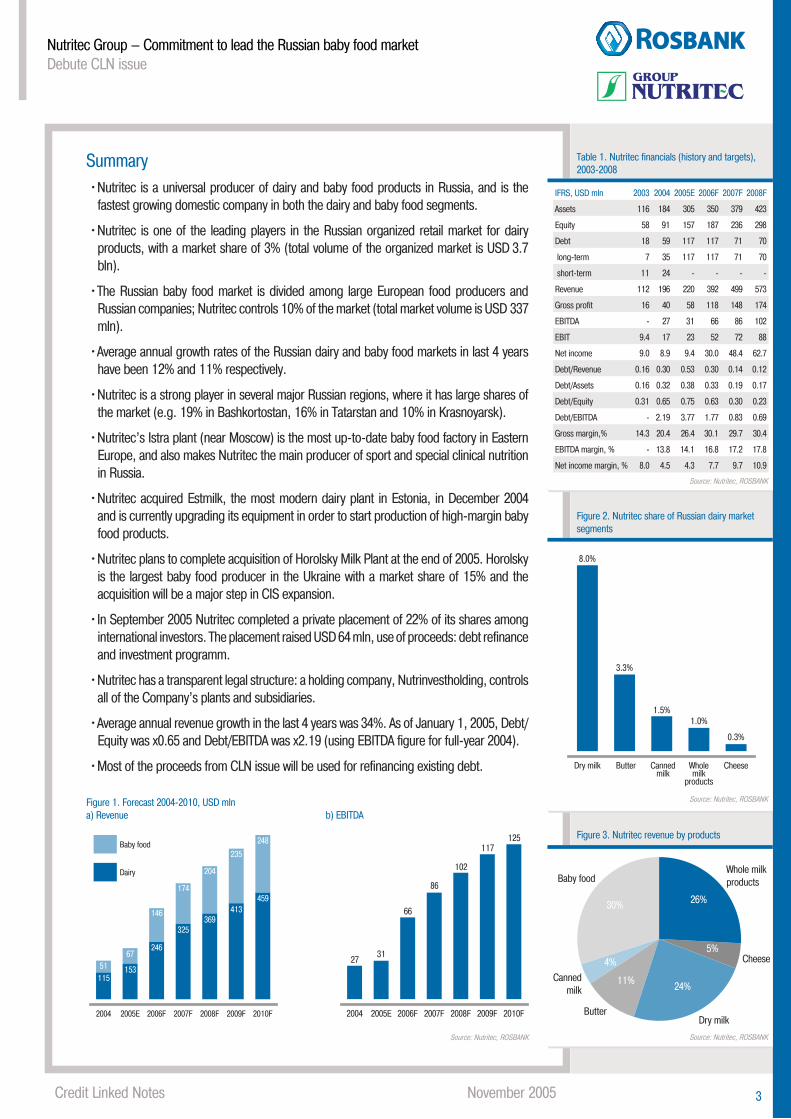

Summary•Nutritec is a universal producer of dairy and baby food products in Russia, and is the

fastest growing domestic company in both the dairy and baby food segments.

•Nutritec is one of the leading players in the Russian organized retail market for dairy products, with a market share of 3% (total volume of the organized market is USD 3.7 bln).

•The Russian baby food market is divided among large European food producers and Russian companies; Nutritec controls 10% of the market (total market volume is USD 337 mln).

•Average annual growth rates of the Russian dairy and baby food markets in last 4 years have been 12% and 11% respectively.

•Nutritec is a strong player in several major Russian regions, where it has large shares of the market (e.g. 19% in Bashkortostan, 16% in Tatarstan and 10% in Krasnoyarsk).

•Nutritec’s Istra plant (near Moscow) is the most up-to-date baby food factory in Eastern Europe, and also makes Nutritec the main producer of sport and special clinical nutrition in Russia.

•Nutritec acquired Estmilk, the most modern dairy plant in Estonia, in December 2004 and is currently upgrading its equipment in order to start production of high-margin baby food products.

•Nutritec plans to complete acquisition of Horolsky Milk Plant at the end of 2005. Horolsky is the largest baby food producer in the Ukraine with a market share of 15% and the acquisition will be a major step in CIS expansion.

•In September 2005 Nutritec completed a private placement of 22% of its shares among international investors. The placement raised USD 64 mln, use of proceeds: debt refinance and investment programm.

•Nutritec has a transparent legal structure: a holding company, Nutrinvestholding, controls all of the Company’s plants and subsidiaries.

•Average annual revenue growth in the last 4 years was 34%. As of January 1, 2005, Debt/Equity was x0.65 and Debt/EBITDA was x2.19 (using EBITDA figure for full-year 2004).

•Most of the proceeds from CLN issue will be used for refinancing existing debt.

Figure 1. Forecast 2004-2010, USD mlna) Revenue b) EBITDA

Baby food

Dairy

2010F2009F2008F2007F2006F2005E2004

248

235

204

174

146

6751

459413

369325

246

153115

2010F2009F2008F2007F2006F2005E2004

125117

102

86

66

3127

Source: Nutritec, ROSBANK

Table 1. Nutritec financials (history and targets), 2003-2008

Source: Nutritec, ROSBANK

Figure 2. Nutritec share of Russian dairy market segments

Source: Nutritec, ROSBANK

Figure 3. Nutritec revenue by products

Source: Nutritec, ROSBANK

IFRS, USD mln 2003 2004 2005E 2006F 2007F 2008F

Assets 116 184 305 350 379 423

Equity 58 91 157 187 236 298

Debt 18 59 117 117 71 70

long-term 7 35 117 117 71 70

short-term 11 24 - - - -

Revenue 112 196 220 392 499 573

Gross profit 16 40 58 118 148 174

EBITDA - 27 31 66 86 102

EBIT 9.4 17 23 52 72 88

Net income 9.0 8.9 9.4 30.0 48.4 62.7

Debt/Revenue 0.16 0.30 0.53 0.30 0.14 0.12

Debt/Assets 0.16 0.32 0.38 0.33 0.19 0.17

Debt/Equity 0.31 0.65 0.75 0.63 0.30 0.23

Debt/EBITDA - 2.19 3.77 1.77 0.83 0.69

Gross margin,% 14.3 20.4 26.4 30.1 29.7 30.4

EBITDA margin, % - 13.8 14.1 16.8 17.2 17.8

Net income margin, % 8.0 4.5 4.3 7.7 9.7 10.9

CheeseWholemilk

products

Cannedmilk

ButterDry milk

0.3%

1.0%1.5%

3.3%

8.0%

30%

4%

11% 24%

5%

26%

Dry milk

Cheese

Whole milkproductsBaby food

Cannedmilk

Butter

Credit Linked Notes November 2005 4

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Russian dairy market is worth USD 7 bln

1700 plants, but they make only half of Russian dairy production

Impessive CAGR of 15-20% during 2001-2004

The Russian dairy market: impressive growth rates and great potentialThe Russian dairy market is one of the largest and fastest growing in Europe, with value of about USD 7 bln in 2004. Only half of Russian dairy products are made at specially equipped processing plants (the “organized” market). The other half is sold unprocessed or with in-house processing, usually close to where the raw milk was produced.Figure 4. Russian dairy production in 2004

Organized53%

63%

24%

10%

3%Nutritec

Unimilk

WBD

Other

Unorganized47%

Source: Euromonitor, Company data

Soviet economic policy decreed that every town in Russia with population over 20,000 had to have its own dairy plant. This has left the Russian dairy market highly fragmented, with over 1700 plants still operating outside the three main dairy companies, which are Wimm-Bill-Dann (WBD), Unimilk and Nutritec.

Milk products are divided into four major categories: whole-milk products, cheese, butter, and dry milk (including both dry whole-milk powder and dry non-fat milk powder). The biggest category is whole-milk products (milk, sour cream, curds, yoghurts, etc.), which represent about 50% of the total Russian dairy market.

The structure of dairy consumption and consumer preferences differ widely inside Russia: Moscow and other large cities increasingly prefer sophisticated, high-value-added products (yoghurts, bio-drinks), while small towns and rural areas remain conservative, exhibiting a preference for traditional products such as curds, ryazhenka (boiled fermented milk), etc.

Annual Russian dairy market growth was about 9% in volume terms and 15-20% in value terms in 2001-2004, according to Euromonitor. The disproportion between volume and value growth is due to the constantly increasing share of high-value-added products in consumption structure.Figure 5. Russian consumption of whole-milk products: 2001-2004 CAGR = 9%, ‘000 tonnes

0

2

4

6

8

10

2004200320022001

8 723

7 7287 452

6 739

Source: Euromonitor, Company data

Credit Linked Notes November 2005 5

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Despite steady growth in recent years, the Russian dairy market is still far behind East European countries in terms of per capita consumption. Russian dairy spending would have to double in order to reach East European levels, according to available statistics. This seems to be evidence of major unsatisfied demand for dairy products in Russia, since the country’s per capita spending on all types of packaged food is much closer to the East European average.Figure 6. Annual dairy consumption: still low compared with peer economies, kg per capita, 2004

0

30

60

90

120

150

UKUSA

FranceGermany

HungaryPortugal

CzechPoland

RomaniaSlovakia

RussiaUkraine

132127

123123

9794

77

605856

2522

Source: Company data

Per capita consumption is still low

Market size is expected to double by 2010

Credit Linked Notes November 2005 6

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

The share of highly value-added products is growing

Whole milk is more than a half of the market. Other products will grow fasterWhole-milk products represent 56.8% of total Russian consumption of dairy products, according to Euromonitor estimates. Whole-milk products include: pasteurised/UHT milk, kefir, yoghurts, and other traditional dairy products such as curds, sour cream, ryazhenka, etc.

Pasteurised milk/UHT milk still had a dominant 34% share of all whole-milk products consumed in Russia in 2004, but its share has been steadily declining as preferences shift to more highly processed and value-added products. Nevertheless, growth of pasteurised milk/UHT milk consumption is expected to continue in the future in absolute terms, as unprocessed milk is gradually driven from the market.

The traditional Russian sour-milk drink, kefir, has 15% volume share in the whole-milk segment. Consumption grew steadily by 5.7% per year in 2002-2004 and traditional kefir is losing ground to “bio-kefir” products.

Yoghurt is one of the fastest growers in the whole-milk segment, with 12.6% consumption CAGR from 2002 to 2004. Yoghurt accounted for 6% of total volumes in the whole-milk segment in 2004. Fruit yoghurts represent 74% of total yoghurt consumption.

Fermented milk products other than kefir have seen the sharpest rise in consumption over the last two years, with CAGR of 13.1% in volume terms. The growth was mainly due to products with special additives, particularly sour dairy drinks with bifido or lacto bacteria and enriched “bio” yoghurts (mainly enriched with vitamins or live bacteria). Enriched milk products have contributed much to overall growth of the Russian dairy market.

Cheese is the growth and margins leader

Cheese saw the highest CAGR (17.9%) among dairy products in 2000-2004 as consumption was encouraged by more choice. However, average per capita consumption of cheese in Russia was still only 3.8 kg in 2004, compared with 12 kg in Europe and over 20 kg in traditionally cheese-eating countries such as Italy, France or Israel. According to USDA estimates, 65-70% of the cheese eaten in Russia is made inside the country. Imports come mainly from Ukraine (33% of imports), Germany (28%) and Lithuania (15%). Cheese offers dairy companies a higher margin than other products.

Butter and dry milk: mostly produced domestically

Consumption of butter and dry milk grew in Russia at CAGR of 9.6% and 3.9% respectively in 2000-2004. Approximately 62% of butter and 77% of dry milk consumed in Russia is produced domestically, and Russian producers are stepping up exports. Large amounts of butter and dry milk are used for production of other food products, mostly baked goods, ice cream and confectionery. Growth in demand for non-branded butter and dry milk is dependent on overall increase in food spending, driven by rising standards of living.

Credit Linked Notes November 2005 7

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

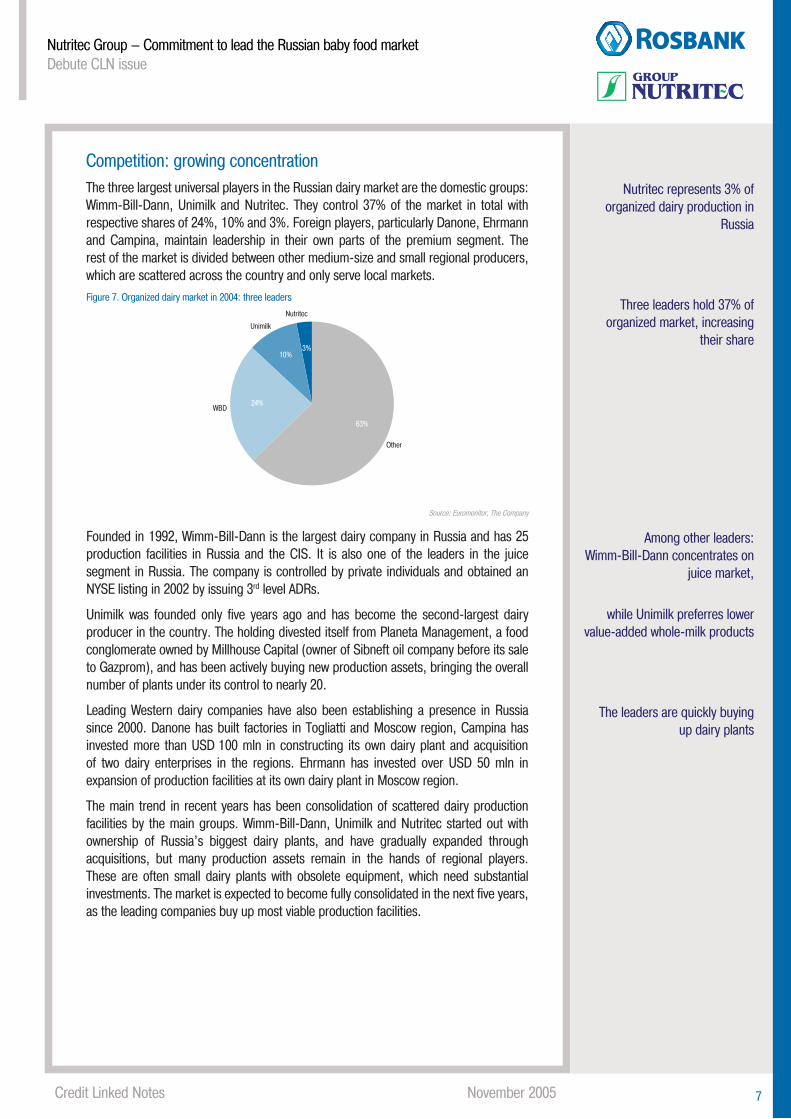

Competition: growing concentrationThe three largest universal players in the Russian dairy market are the domestic groups: Wimm-Bill-Dann, Unimilk and Nutritec. They control 37% of the market in total with respective shares of 24%, 10% and 3%. Foreign players, particularly Danone, Ehrmann and Campina, maintain leadership in their own parts of the premium segment. The rest of the market is divided between other medium-size and small regional producers, which are scattered across the country and only serve local markets.Figure 7. Organized dairy market in 2004: three leaders

3%10%

24%

63%

WBD

Unimilk

Nutritec

Other

Source: Euromonitor, The Company

Founded in 1992, Wimm-Bill-Dann is the largest dairy company in Russia and has 25 production facilities in Russia and the CIS. It is also one of the leaders in the juice segment in Russia. The company is controlled by private individuals and obtained an NYSE listing in 2002 by issuing 3rd level ADRs.

Unimilk was founded only five years ago and has become the second-largest dairy producer in the country. The holding divested itself from Planeta Management, a food conglomerate owned by Millhouse Capital (owner of Sibneft oil company before its sale to Gazprom), and has been actively buying new production assets, bringing the overall number of plants under its control to nearly 20.

Leading Western dairy companies have also been establishing a presence in Russia since 2000. Danone has built factories in Togliatti and Moscow region, Campina has invested more than USD 100 mln in constructing its own dairy plant and acquisition of two dairy enterprises in the regions. Ehrmann has invested over USD 50 mln in expansion of production facilities at its own dairy plant in Moscow region.

The main trend in recent years has been consolidation of scattered dairy production facilities by the main groups. Wimm-Bill-Dann, Unimilk and Nutritec started out with ownership of Russia’s biggest dairy plants, and have gradually expanded through acquisitions, but many production assets remain in the hands of regional players. These are often small dairy plants with obsolete equipment, which need substantial investments. The market is expected to become fully consolidated in the next five years, as the leading companies buy up most viable production facilities.

Nutritec represents 3% of organized dairy production in

Russia

Among other leaders:Wimm-Bill-Dann concentrates on

juice market,

while Unimilk preferres lower value-added whole-milk products

The leaders are quickly buying up dairy plants

Three leaders hold 37% of organized market, increasing

their share

Credit Linked Notes November 2005 8

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

The Company has a strong regional presence

Figure 8. Russian dairy market: set for more growth, USD mln

2010E2009E2008E2007E2006E2005E20042003

14 915

13 327

11 983

10 968

10 053

8 589

6 990

5 819

Source: The Company

Market position: strong and expanding

Nutritec has strong and dominant market shares in several Russian regions, particularly regions where its major production facilities are located. In the whole-milk segment the Company reports that it has approximate market shares of 57% in Penza region, 19% in Bashkortostan, 16% in Tatarstan, 15% in the Vologda region, 10% in Krasnoyarsk region and 7% in Altai region. Much of the competition in these regions is with local producers, who usually have working capital constraints, poor-quality packaging, lower overall product quality and very low marketing expenditures and brand awareness. Nutritec management believes that it will be able to expand its regional market shares at the expense of such weak competitors, building a nationwide base that will also allow the Company to compete successfully with major Russian and international producers.Figure 9. Market share of Nutritec’s whole-milk products in core strategic regional markets, 2004

0

10

20

30

40

50

60

PenzaBashkortostanTatarstanVologdaKrasnoyarsk

57%

19%16%15%

10%

Source: Rosstat, Company data

Nutritec has strong market positions in dry milk products and butter, and had a 1.5% share of the national market for condensed milk in 2004. The Company has also started to produce cheese following acquisition of the Penza plant in 2002 (since modernized) and the Biysk plant in 2003. The Company produced 3126 tonnes of cheese in 2004, although this represents only a modest 0.3% of the total national market.

Credit Linked Notes November 2005 9

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Figure 10. Market share of Nutritec’s core product lines in Russia, 2004

0

1

2

3

4

5

6

7

8

Dry milkButterCondensed milkWhole milkCheese

8.0%

3.3%

1.5%1.0%

0.3%

Source: Company data

Russian baby food: high growth, impressive margins

According to Euromonitor, the baby food market in Russia had value of USD 337 mln in 2004. Its three major segments are milk formula (47%), prepared baby food (28%) and dry baby food (17%). This market is growing dramatically, with CAGR of 11.4% in the last five years and is very attractive due to high margins.Figure 11. Russian baby food market: further increase in value, USD mln

0

100

200

300

400

500

600

2009E2008E2007E2006E2005E200420032002

533

495464

435

389

337298

272

Source: Euromonitor

Russian spending on milk formula has increased by average 10.7% annually in recent years. Two thirds of the milk-formula market are “follow on” milks (used after an initial period of breast feeding), and middle-class parents are increasingly choosing more expensive products. The switch to premium and sophisticated products has been much greater in Moscow and St. Petersburg, where per capita incomes are higher.

There is much potential in Russia for development of hypoallergenic milk formula, since the number of babies with allergies is increasing more rapidly than the birth rate due to worsening of the environmental situation. Hypoallergenic products have been on the market since 1999, but sales are held back by prohibitively high prices (often two to three times more than standard milk formula).

The prepared and dry baby food segments have grown rapidly in value terms, with CAGR of 12.3% in 2000-2004. The rapid development is mainly thanks to affordable products offered by local manufacturers. Dry baby food is usually bought by lower-income households.

Nutritec holds:

– 8.0% of dry milk market;

– 3.3% of butter;

– 1.5% of condenced milk;

– 1.0% of whole-milk

Russian baby food market is highly attractive:

grew by 12% during 2002-2004,

and is expected to grow 10% during 2005-2009

Hypoallergenic and ECN products are particularly

promising

Credit Linked Notes November 2005 10

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Per capita consumption of baby food remains low

Baby food market is heavily fragmented and dominated by

imports,

but Nutritec is a leader among domestic producers, with strong

presence in all sub-segments

Special packaged foods for the sick and diferently abled – enteral clinical nutrition (ECN) products – are traditionally classed with baby foods. ECN products are a small, but high-value-added and rapidly growing niche of the Russian market. They cost a lot to make, including R&D spending, but have the advantage of a dependable customers base (clinics, disabled individuals and others). Most products in the Russian market are imported, but a small number of domestic manufacturers, most notably Nutritec, also produce a range of highly competitive products.Figure 12. Annual per capita consumption of baby food is only half of the level in Eastern Europe, 2004, kg per capita

0

500

1000

1500

2000

2500

3000

3500

4000

USAFrance

UKPortugal

GermanyPoland

HungaryRussia

CzechUkraine

SlovakiaRomania

3 600

3 200

1 400

1 0001 000800

600400400

300300100

Source: Euromonitor

The sport nutrition segment has a similar profile to ECN, with high prices and a narrow but dependable target audience (athletes, bodybuilders, etc.). It has the advantage of a wide product range, which favours advancement of new products and brands. Growth of this market is highly dependent on disposable incomes, and on development of gyms and stores selling sports goods. Findings reported in Russian media suggest that Russian sport nutrition sales doubled in 2004. Nearly all sport nutrition products are imported: the only domestic manufacturer is Nutritec.

Competition

The Russian baby food market is divided between domestic baby food producers, large international food conglomerates, and a group of small and medium-size East European producers. A significant share of the baby food sold by international producers is still imported, but international companies such as Nutricia – subsidiary of Royal Numico (19.5% market share in 2004), Nestle (10.5% market share) and Heinz have established local production facilities. Nutricia acquired a baby food plant in Moscow region in 1992. Heinz launched dried food production in Russia under its own brand in the mid-1990s.Figure 13. Market shares of major baby food producers, 2004

0

20

40

60

80

100Others

Lebedyansky

Tip-Top

Kolinska

Heinz

Azovsky

Friesland

Hipp

Slavex

Nutritec*

Nestle

Nutricia

Puree, juices and otherCerealsBreast feeding substitutes

13%16%18%

12%15%10%

15%17%

9%

20%

6%

8%

18%16%

12%

8%

9%

22%

14%

21%21%

* excluding exports to CIS countries (30-35%)Source: The Company, Euromonitor (by value, retail prices)

Credit Linked Notes November 2005 11

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Royal Numico (owner of Nutricia) is Europe’s largest producer of baby food and clinical nutrition products with €1.722 bln net sales in 2004. It manufactures baby milk formulas, cereals, juices and fruit snacks under brands such as Bambix, Bebilon, Olvarit, Milupa, and Cow & Gate. Nestle is the world’s number-one food company, with sales of USD 76.7 bln in 2004. The Slovenian company Kolinska is the most prominent East European player in Russia, with strong presence in cereals segment.

The leading domestic producers are Nutritec, Slavex, Lebedyansky, the Azovsky Baby Food Plant (Rostov) and the 1st Baby Food Factory (Moscow).

Nutritec is a leader in baby milk formula

Nutritec is particularly strong in the baby milk formula segment. According to Company estimates, its current market share in this segment is about 12% in Russia, and between 6% and 15% in various CIS countries. The Company is also well-positioned in the market for child cereals, with a 2004 market share of 9% according to AC Nielsen (2004). The Company is the sole domestic producer of powdered substitutes for breast feeding (used before follow-on milk products), although competition in the market is strong due to the high share of imported products.

The Company’s main competitors in the baby milk formula segment are foreign manufacturers, particularly Nestle and Nutricia. In the purees, fruit and vegetable juice segment Nutritec is in competition with both foreign and local manufacturers, particularly Nestle and Lebedyansky.

Nutritec holds 12% of baby milk formula market

Credit Linked Notes November 2005 12

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Clear and sound strategy of Nutritec will support its growth &

leadership

Business Strategy: commitment to leadership, growth and profitabilityNutritec’s business strategy is to develop its core business lines (dairy products and baby food) to achieve continuous growth and increasing profitability.

In the dairy market. The Company aims to become one of the country’s top-three producers of dairy products, with a distribution network covering the whole of Russia and some CIS countries. Nutritec is primarily focused on lower middle and middle-income customers, who have average monthly income of USD 300 per month. More than 80 million people in Russia currently fall into this category.

In the baby food market. Nutritec’s focus in the baby food segment is on middle- and upper-middle-income customers, who are expected to offer the fastest growing market. The Company plans to become the top Russian baby food producer, concentrating on high-margin special milk formula products and special nutrition products (ECN) in Russia, the CIS and the Baltics. The Company believes that its product quality and continuous marketing efforts to educate the public about baby food products will lead to significant growth of the segment and increase the Company’s market share.

The company will also work to expand its baby food distribution network to access new markets and will diversify its product portfolio including introduction of a premium brand. Production of niche products, including sport and clinical nutrition products will be increased.

In order to implement its growth strategy the Company plans to:

•Increase the share of value-added products and promote a value-added consumption culture. The Company will continue investments in production facilities and increase expenditure on marketing and new product development in order to boost production and sales of value-added, high-margin dairy products. In particular, the Company is targeting increased sales of yogurts, desserts, and flavoured and enriched dairy products.

•Launch a national umbrella dairy brand in 2006 and carry out re-branding in the baby food segment. The Company plans to introduce its first umbrella dairy brand in 2006 and to start marketing most of its high-margin products under this brand. Re-branding in the baby food segment will be addressed to wealthier customers and the company will introduce a new baby food brand in the premium segment.

•Ensure high product quality thanks to modern equipment. The Company is currently installing new equipment at its facilities. This investment should enable Nutritec products to compete effectively with leading Russian and international manufacturers. The Company will also work with suppliers of raw milk to increase quality control and develop proprietary farming. The Company already has two farming holdings in Russia and Estonia and plans to create additional agricultural holdings in the near future.

•Upgrading of production facilities. The Company plans to continue investing in expansion of its production facilities in 2006, after which medium-term investment needs will be modest.

• Restructuring of operations. Nutritec plans to continue its business restructuring efforts, aiming at greater operating efficiency, cost savings and better utilization of the Company’s production assets. Use of the latest technologies will enable rapid growth without major increase in personnel.

Credit Linked Notes November 2005 13

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

• Centralised management. The Company will keep corporate functions centrally managed in the future and further streamline its distribution system, logistics, and marketing departments at the subsidiary level.

• Expand geographical reach through organic development and strategic acquisitions. The Company has adopted a two-stage programme for development of its distribution network. In 2006 the Company will develop its distribution network in those regions which are located close to production assets. The second stage of the programme, which is due to start in 2008, will expand distribution to all large cities.

Competitive strengths

Nutritec believes that it has the following competitive advantages, which will assist implementation of its business strategy and continued success in the market-place:

• Developed raw milk base. All of the Company’s production assets are located in regions that have a developed raw milk base. The Company supports local farming in these regions by supplying equipment, quality control mechanisms and cash. This support gives the Company strong purchasing power and provides a significant advantage over its local and national competitors, ensuring a regular supply of high-quality raw milk.

• Leading position in the baby food segment among Russian producers. The Company operates three baby food production facilities in Russia and one in Estonia, including the Istra plant, which is the most advanced baby food factory in Russia/CIS/Eastern Europe. The Company’s distribution network covers all major regions of Russia and the CIS. The Company is focused on developing new products, has a dedicated team of R&D specialists and considers itself to be one of the most technologically advanced baby food companies in Europe. The Company is a unique supplier of a full range of baby food products in the Russian market. It is the undisputed leader in enteral clinical nutrition products, where it competes only with foreign imports, and has good potential to develop sport and fitness nutrition products.

• Strong footprint in the regions and favourable geographical location of production assets in the dairy segment. The Company is one of the leading players in the Russian dairy market, with dominant or strong positions in the regions where its production assets are located. The Company has yet to launch a national brand and start an associated marketing campaign, but it already benefits from high brand recognition in the regions. A local approach to regional markets gives the Company substantial competitive advantages compared with national brands. Its strong regional position also provides substantial cost savings, especially in raw milk purchases and direct salary expenses.

• Strong production platform to realize growth potential. A comprehensive technical audit of Nutritec production assets was carried out in 2004 by Valio Ltd. Based on this audit the Company chose new equipment for installation and developed a highly detailed business and technical modernization plan, which is now being implemented. Capex in 2005 and 2006 will ensure that the Company has sufficient spare capacity to support strong organic growth with no need for further substantial investment in fixed assets until 2009 at the earliest.

• Plant specialization. Most of the Company’s production facilities specialize in particular products, depending on demand profile of the regional markets where they are located. This enables the plants to achieve higher returns than non-specialized production facilities.

Nutritec has major competitive strengths

Credit Linked Notes November 2005 14

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

• Research and development expertise. Nutritec has always had its own R&D Centre, which now pools the experience of more than 50 professionals in Russia. The Company has proven ability to assess potential demand and develop new technology-intensive products, such as clinical nutrition and special milk formula products.

• Access to external capital. Nutritec’s size and credit history give it a significant advantage over local competitors in obtaining financing to exploit market growth. In 2005 the Company placed ruble bonds with value equal to USD 42.12 mln. Nutritec can attract financing for a longer period than the average working capital cycle. As a result the Company can produce higher-quality products (particularly cheese) with longer aging characteristics, and efficiently offset seasonality with dry milk production.

•Acquisition and export development. The fragmented nature of the Russian and CIS dairy market will offer significant opportunities for strategic acquisitions. Nutritec will continue making acquisitions in its strategic regions and entering new regional markets, particularly southern Russia and the Volga region. Nutritec also plans to use Estmilk (Estonia) to export baby food products to North Africa, South-East Asia and the EU.

• Strong and dedicated management team. The Company’s highly qualified and motivated senior management team has significant experience in all aspects of the dairy and baby food industry, including production, new product development, sales and marketing, and finance. Company management has proven ability to identify, acquire, integrate, and develop Russia’s best production assets.

Figure 14. Corporate governance and management team: high level of transparency and professionalism

Supply Chain& ProductionValery Rusakov

Baby food segmentVladimir Kruglik

Chief Executive OfficerGeorgiy Sazhinov

FinanceSergey Ogorodnov

Sales and MarketingIlya Dyakonov

Economic Analysisand Strategic Planning

Sergey Ivanov

Chief Operating OfficerGennady Popov

Board of Directors

General ShareholdersMeeting

Source: The Company

Credit Linked Notes November 2005 15

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Table 2. Member of the board and key employees

Name Year of Birth Position

Members of the Board of Directors

Konstantin Malofeev 1974 Chairman of the Board of Directors

Georgiy Sazhinov 1962 CEO, Member of the Board of Directors

Gennady Popov 1953 COO, Member of the Board of Directors

Oleg Rukavishnikov 1964 Member of the Board of Directors

Valery Rusakov 1948 Deputy CEO for Production and Supplies, Member of the Board of Directors

Victor Ozhogin 1961 CEO “Istra plant”, Member of the Board of Directors

Sergey Arhipov 1968 General counsel, Member of the Board of Directors

Sergey Oblapenko 1963 CEO “Nutrinvest”, Member of the Board of Directors

Key Employees

Sergey Ivanov 1972 Director for Economic Analysis and Strategic Planning

Ilya Dyakonov 1968 Director for Sales and Marketing

Sergey Ogorodnov 1975 Deputy CEO for Finance

Vladimir Kruglik 1957 Director of baby food segment

Source: The Company

Board of Directors

Konstantin Malofeev was born in 1974 in Moscow region. He graduated from the Moscow State University in 1996 with a degree in law. He started his career in Renaissance Capital in 1995. He then held executive positions in Interros and other investment companies. From 2002 to 2004, he was Head of Corporate Finance at MDM-Bank. In 2005, Mr. Malofeyev and his partners founded a private equity fund, Marshall Capital Partners.

Georgiy Sazhinov has been Chairman of the Board of Directors of the Company since 2005. Since 2004, Mr. Sazhinov has been Chairman of the Board of Directors of Nutrinvest. In 2001, he served as Deputy Minister of Agriculture of the Russian Federation. In 2000-2001, he served as Head of the Moscow Government Department for Development of the Agricultural Sector. In 1998 he was appointed to manage the Department of Food, Food Processing and Baby Food at the Ministry of Agriculture. In 1996, Mr. Sazhinov was appointed Head of the Department of Baby and Special Food of the Ministry of Agriculture. He graduated from the Leningrad Technological Institute of Refrigeration in 1984 with a PhD in Milk Technologies.

Gennady Popov has been Chairman of the Board of Directors of the Company since 2004 and Deputy CEO for Corporate Governance since 2004. Mr. Popov has been the Deputy CEO of Nutrinvest since 2003. He is also the CEO of the LLC “Investment-Financial Company INVENTA”. He graduated from the Moscow Institute for Engineering and Physics in 1977.

Oleg Rukavishnikov has been a member of the Company’s Board of Directors since 2004 and Deputy CEO for Finance and Economics since 2000. From 1998 to 2000, he held various positions in Baltoil, Baltoil-group, Nutrinvest and the Zelenodolsk plant. He graduated from Kaliningrad State University in 1990.

Valeriy Rusakov has been a member of the Company’s Board of Directors since 2005. He has also been Deputy CEO for Production and Supplies since 1998. From 1980 to 1998, he held various positions in Russian dairy plants and corporations. He graduated from the Moscow Technological Institute for the Dairy and Meat Industry in 1976.

Victor Ozhogin has been a member of the Company’s Board of Directors since 2005. He has also served as Director of the Company’s Baby Food Development Department

Managers of Nutritec are a team of highly experienced

professionals

Credit Linked Notes November 2005 16

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

since 2005. From 2003 to 2005 he served as CEO of the Istra plant. He graduated from the Riga Institute of Civil Aviation Engineers in 1984.

Sergey Arhipov Sergey Arhipov was born in 1968 and graduated from Moscow University of Electronic Technology in 1991. In 1998 he gained a masters degree in law from Moscow Commercial University. Since 2003 he has been head of Nutritec’s legal department.

Sergey Oblapenko has been a member of the Company’s Board of Directors since 2005. He has also been the CEO of Nutrinvest since 2004. From 2002 to 2004 he served as CEO of Filimonovsky Milk Plant. He graduated from the Moscow Energy Institute in 1986.

A new Board of Directors will be elected on shareholders meeting on 18 November 2005. The new Board will include two independent directors put forward by minorities.

Key Employees

Sergey Ivanov has been a member of the Company’s Board of Directors since 2005. He has also been Deputy CEO for Economic Analysis and Strategic Planning at the Company since 1998. From 1995 to 1998, he worked as consultant in PricewaterhouseCoopers. He graduated from the Finance Academy under the Government of the Russian Federation in 1995.

Ilya Dyakonov was born in 1968 in Moscow. He graduated from the Moscow State Institute of Radio Technology, Electronics and Automatics in 1991 and from Kennedy Western University with MBA degree in 2000. Mr. Dyakonov served as CEO of ZAO “Souzplodimport” before joining Nutritec as Commercial Director in 2005.

Sergey Ogorodnov has been Deputy CEO for Corporate Finance since 2005. He held executive positions in large Russian banks such as Alfa Bank and MDM-Bank. In 2005 Mr. Ogorodnov joined the private equity fund Marshall Capital Partners. He graduated from Tyumen State University in 1997 and from Rochester Institute of Technology with an MBA degree in 2000.

Vladimir Kruglik was born in 1957 and graduated from the Odessa Food Industry Institute in 1980. In 1980-1984 Mr. Kruglik served as Chief Operating Officer at a butter plant in Ukraine, before becoming Head of a technology laboratory for food development at the Russian Academy of Medical Sciences in 1986-1990. Mr. Kruglik has held various positions in Nutritec since 1990 and was appointed Head of the Company’s baby food business segment in 2005.

Employees and employee motivation programmes

As of 1 July 2005, the Company and its subsidiaries has 3,929 employees, including dairy farm staff, of whom 56 are executives, 3,270 are manufacturing, technical and maintenance workers, 242 are sales, marketing, customer service and logistics staff, and 361 are other administrative staff. The Company has 3,470 employees based in Russia and 459 in Estonia, of whom 380 are employed by Agro Piim.

Credit Linked Notes November 2005 17

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

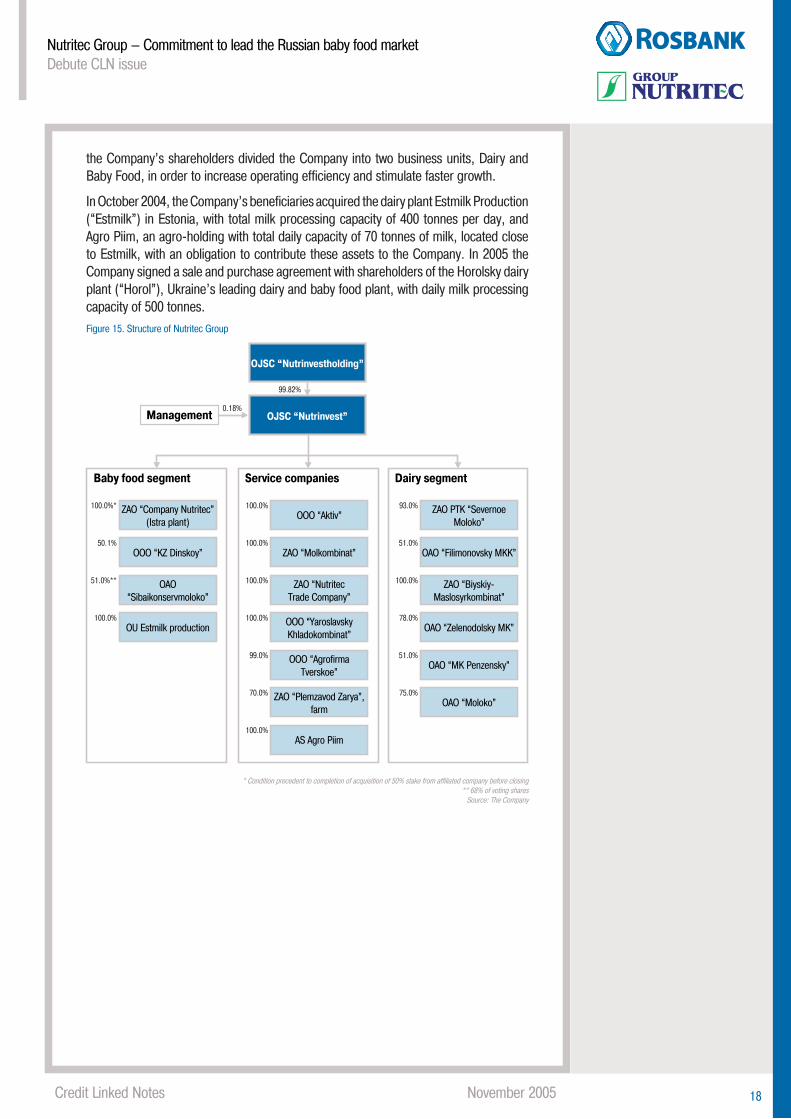

Corporate history and structureNutritec was set up as a research and development centre in 1990. Since 1998, it has demonstrated remarkable growth through organic development and acquisitions, and has an extensive track record in restructuring and successful integration of new assets.

In 1991-1998, the Company’s founders followed a cautious development strategy, shaping key competences and strategic activities, and laid the foundations for future development.

In 1998, the Company began an expansion programme based on regional acquisitions. (The following Russian abbreviations are used below: OAO = public company; OOO = limited company; ZAO = private company)

Nutritec acquired the milk plant OAO “Zelenodolsky MK” (“Zelenodolsk plant”), with daily milk production capacity of 180 tonnes. In 1999, the Company complemented its line of milk formula products with fruit and vegetable purees by acquiring the canning factory OOO “KZ Dinskoy” (“Dinskoy plant”) in Krasnodar region (daily processing capacity of 450 tonnes). The Company made a further acquisition in the baby food segment in 2001, buying the dairy and baby food factory OAO “Sibaikonservmoloko” (“Sibay plant”) in Bashkortostan (daily processing capacity of 450 tonnes).

In 2000, Nutritec acquired the dairy plant OAO “MK Penzensky” (“Penza plant”, daily milk processing capacity of 400 tonnes) in Penza region and the dairy plant OAO “Moloko” (“Belgorod plant”, daily milk processing capacity of 210 tonnes) in Belgorod region. In 2001 the Company acquired the dairy plant ZAO PTK “Severnoye Moloko” (“Vologda plant”) in Vologda region and the dairy plant OAO “Filimonovsky MKK” (“Filimonovo plant”) in Krasnoyarsk region. The last two plants each have daily milk processing capacity of 450 tonnes.

In 2002, the Company completed greenfield construction of a new plant at Istra, near Moscow, owned by the affiliate ZAO “Kompaniya Nutritec”. The Istra plant is the largest and most modern baby food factory in Russia and the CIS, with total annual capacity of approximately 1,500 tonnes of dry baby food, 6,000 tonnes of enteral and special nutrition and 11,000 tonnes of special pure water for use in baby food products.

In 2003, the Company acquired ZAO “Molkombinat”, OOO “Aktiv”, and ZAO “Biyskiy- Maslosyrkombinat” (jointly “Biysk plant”) with daily milk processing capacity of 150 tonnes, and the refrigeration facility OOO “Yaroslavsky Khladokombinat” (“Yaroslavl warehouse”) with logistics capacity for 11,500 tonnes of food products.

In 2003, the Company started production under the “Nutrilak” baby food brand at its production facility in Istra. This coincided with a new phase of Company development, focused on operational restructuring and profitability.

Since 2003 the Company has moved to acquire regional producers of raw ingredients in order to improve the quality of its inputs in the regions and reduce purchasing costs. In 2004 the Company acquired ZAO “Plemzavod Zarya” (“Zarya Agroholding”) in Vologda region. This holding owns more than 21,000 hectares and an average of 14,000 cows, enabling the Company to produce 30,000 tonnes of raw milk per year. The Company plans to consolidate a similar agro-holding in the Penza region in 2005-2006.

The Company has also focused more closely on internal development since 2003, striving to improve the production process and increase operating efficiency. The Company introduced an integrated restructuring programme in 2003, aiming to gradually upgrade all of its production assets by installing the latest foreign-made equipment. In mid-2004

Nutritec has built an asset base through acquisitions since 1998

Credit Linked Notes November 2005 18

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

the Company’s shareholders divided the Company into two business units, Dairy and Baby Food, in order to increase operating efficiency and stimulate faster growth.

In October 2004, the Company’s beneficiaries acquired the dairy plant Estmilk Production (“Estmilk”) in Estonia, with total milk processing capacity of 400 tonnes per day, and Agro Piim, an agro-holding with total daily capacity of 70 tonnes of milk, located close to Estmilk, with an obligation to contribute these assets to the Company. In 2005 the Company signed a sale and purchase agreement with shareholders of the Horolsky dairy plant (“Horol”), Ukraine’s leading dairy and baby food plant, with daily milk processing capacity of 500 tonnes.Figure 15. Structure of Nutritec Group

Management

Baby food segment

ZAO “Company Nutritec”(Istra plant)

100.0%*

OOO “KZ Dinskoy”50.1%

OAO“Sibaikonservmoloko”

51.0%**

OU Estmilk production100.0%

Service companies

OOO “Aktiv”100.0%

ZAO “Molkombinat”100.0%

ZAO “NutritecTrade Company”

100.0%

OOO “YaroslavskyKhladokombinat”

100.0%

OOO “AgrofirmaTverskoe”

99.0%

ZAO “Plemzavod Zarya”,farm

70.0%

ZAO PTK “SevernoeMoloko”

93.0%

OAO “Filimonovsky MKK”51.0%

ZAO “Biyskiy-Maslosyrkombinat”

100.0%

OAO “Zelenodolsky MK”78.0%

OAO “MK Penzensky”51.0%

OAO “Moloko”75.0%

AS Agro Piim100.0%

Dairy segment

0.18%

OJSC “Nutrinvestholding”

OJSC “Nutrinvest”

99.82%

* Condition precedent to completion of acquisition of 50% stake from affiliated company before closing** 68% of voting shares

Source: The Company

Credit Linked Notes November 2005 19

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Growth of networks will increase sales and distribution valueDairy business segment

The Company distributes its products through a variety of channels: wholesalers, direct trade sales, sales under state procurement programmes, independent distributors, supermarket chains, small- and medium-size grocery stores, and open markets.

Key dairy sales personnel are located at representative offices and/or production plants. They are responsible for regional sales, including facilitating orders and coordinating deliveries, customer account management, marketing analysis and daily reporting. The head office ensures compliance with the Company’s uniform corporate standards, develops marketing strategy and procedures to local sales personnel, and provides sales personnel with marketing materials and instructions.

The Company uses a direct distribution model for dry milk and bulk butter, net sales of which brought 35% of total revenue in 2004. The Company currently has 8 regional distribution offices and 31 sales and distribution executives based at its production facilities. A programme for development of the distribution system envisages substantial growth in the number of merchandisers and sales managers, as illustrated in the table below:Table 3. Sales and distribution network

Representative office executives

Current, 2005 Potential, 2009

Merchandisers Sales managers Merchandisers Sales managers

Moscow 8 4 44 22

St. Petersburg 6 3 10 8

Vologda 4 2 24 12

Penza 26 13 72 36

Zelenodolsk 18 9 38 19

Krasnoyarsk 10 5 28 14

Source: The Company

The distribution development programme will be in two stages, and major increase in numbers of sales personnel will be an important component. In the first stage, each of the Company’s key production facilities will add between 1 and 10 new major towns and cities to its distribution network (the towns and cities may be located in a radius of 300 kilometres from the facility itself). In the second stage of the programme, the geography of distribution will be further expanded, so that each key production facility will supply a further 5 to 10 smaller cities in a radius of 500 kilometres.

The Company will use the services of independent distributors. In order to ensure uniform pricing across Russia, the Company will implement a strict system of control over distributors’ pricing policy. The Company plans to have only one distributor per region, thereby preventing destructive competition between regional distributors. An efficient reporting system from the regions should allow the Company to accurately evaluate regional market demand and gauge the maximum amount of dairy products, which the regional distributor could need for the particular region. This will avoid any risk of sales by a distributor to neighbouring regions, which are served by another distributor.

Baby food business segment

The Company has been continuously developing its distribution network in the baby food segment. The network now covers all Russian regions with population above 500,000 and all CIS countries except Tajikistan, the Kyrgyz Republic and Georgia. The

Distribution network: variety of channels split regionally

Sales personnell complies with centralised brand & standards

Development program – dramatic increase of

merchandisers & sales managers

Credit Linked Notes November 2005 20

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Investment program will increase use of capacities

CIS countries accounted for approximately 35% of total baby food revenues in 2004. The Company has a main distribution centre and a team of sales managers responsible for regional markets. The pricing and distribution model, as well as cash flow and risk management, are centrally organized.

Similarly to the dairy business model, the Company avoids internal competition between distributors by having only one distributor per region and exercising a system of strict control over purchasing, which prevents distributors from selling to neighbouring markets. The Company has more than 50 distributors, none of which are exclusive (exclusive distribution is not common practice in the Russian baby food segment, and every distributor strives to offer a full range of products to its customers). The Company currently has strong relationship with all of its distributors and offers them commission rates up to 5% higher than the average market level.

Logistics: supporting and strengthening market positions

In large distribution areas the Company and its distributors have worked together to organize logistics centres, and the Company has put strong control systems in place to ensure constant availability of a full product range in each such centre. Geographically diverse footprints of the Company’s baby food production plants in Russia and Estonia enable major cost savings on transportation of products to markets.

The Company operates two major logistics centres in the Moscow region (total capacity of 5,000 tons of finished products) and in Yaroslavl (a refrigerated cooler facility with total storage capacity of 11,500 tons) to support distribution of dairy products in central Russia. In addition, the Company is currently considering using the Istra baby food production plant as a logistics centre for its baby food products with possible construction of additional premises close to the Istra site.

Ambitious investment program

The Company lacked production capacity to meet demand for whole-milk dairy products in certain regions in 2004, despite low average capacity utilization rate of 43%. Capacity use at the new Istra plant was close to 100% (with single-shift production). The Company has installed new capacity at the Sibay plant and will transfer most of its baby milk formula production from Istra to Sibay. This will allow more efficient use of state-of-the-art capacities at the Istra plant for products with high added value. The reorganization will also give major cost savings for the Company, since direct employee costs at the Sibay plant are only half of those at Istra.

The Company plans to invest USD 35.6 mln in its dairy business segment in 2005-2006, primarily on three major modernization projects at the Vologda, Penza and Biysk plants. Capex at the Vologda plant will include modernization of the facility and expansion of capacity for production of whole-milk dairy products. The investment programme at the Penza plant will focus on installation of new capacity for whole-milk, cheese and powder milk products. At the Biysk plant the Company will renovate and expand cheese and whole-milk capacity.

Other planned investments will be focused on packaging and warehousing of finished goods, energy saving and additional equipment for products with high added value. Most investments in the baby food segment will be allocated to the Istra plant (USD 6.5 mln) for heating and water supply and for a sourcing and warehouse complex. Investments at the Dinskoy plant (USD 3.3 mln) will finance boiler renovation, two production lines for baby food and a refrigeration facility. Investments in the Sibay plant will finance boiler renovation, expansion of baby food production capacity, and renovation and completion of new facilities for baby milk formula production. Total capex for 2005-2006 in the baby

Credit Linked Notes November 2005 21

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

food segment should be about USD 12.5 mln. In 2008-2009 the Company plans to invest USD 7.3 mln on modernization of Estmilk.

Private placement: first step to an IPO in 2007

On September 6 Nutrinvestholding, the owner of Nutritec, made a private placement of 22% of its shares among institutional investors from Europe, the USA and Russia. The placement value was USD 63.79 mln.

A total of 3 038 095 shares were placed at USD 21 per share. More than 90% of shares were acquired by large foreign institutional investors. Before the private placement investment Marshal Milk Investments Limited owned 100% of Nutrinvestholding.

By the year of 2007, Nutritec plans initial public offering.

Credit Linked Notes November 2005 22

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Key revenue drivers are:– whole-milk;

– dry milk;– baby milk formula

(69% of 2004 revenues in total)

Revenue structureThe dairy segment accounts for more than 70% of the Group’s revenue and baby food accounts for 30%. Dairy business expanded as a share of overall Company business compared with 2003.

The main reason for overall revenue growth was rapid increase in Russian consumption and increase of capacity utilization.Figure 16. Revenue breakdown, 2004

5%3%3%

4%

5%

11%

19%24%

26%

Dry milkInfant milk formulaand special nutrition

Butter

Cheese

Whole milk

Other baby foodFruit and vegetable puree and juices

General canning

Condensevd milk

Source: The Company

Figure 17. Revenue growth, 1999-2004, USD mln

200420032002200120001999

170

112

84

68

49

25

Note: based on consolidated management accounts, prepared in accordance with IFRS, excluding financial results of EstmilkSource: Company data

Milk segment. The Company is increasing production of whole-milk products faster than its increases prices in order to capture market share.

Increased output of whole-milk products in 2004 was matched by reduction of powdered milk and butter output. Prices for the Company’s powdered milk and butter have risen in line with the overall market trend.

The Company is rapidly increasing production of cheese thanks to purchase of the Biysk plant.

Baby food segment. Prices for the Company’s baby and special foods grew by 28% in 2004, following the general market trend. Two facts about this segment deserve special mention:

1.Output of breast feeding substitutes by the Istra plant increased three times in 2004 compared with 2003.

2.The special food market is limited and production is order-driven. Special foods remain a small part of total Group production, although their share is increasing.

Canning volumes at the Dinskoy plant were slightly higher in 2004 than in 2003. Baby food canning decreased and general canning increased.

Credit Linked Notes November 2005 23

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Cost structureRaw milk. Raw materials (mainly raw milk) represent 70% of total costs. Significant increase of raw milk prices in 2004 was not wholly compensated by increase in prices of whole-milk products.

Powdered milk and butter. The cost structure for these products is hard to calculate, because Nutritec has not yet updated a misleading methodology, which unjustifiably assumes that raw materials for powdered milk and butter production depending on their fat content. In any case, Nutritec is well able to offset costs of powdered milk and butter, because ample working capital allows the Company to step up sales of these two products in the winter months when their prices rise. This policy helped the company to increase butter and powdered milk margins in 2004 compared with 2003.

Cheese. Components account for up to 50% of total costs and comprise milk ferments and additives.

Baby milk formulas and special food. This group is not homogeneous and includes products with different cost structures. Components are about 60% of costs, and packaging is 25% of costs (the latter including boxes, foil-clad paper and expensive measuring spoons).

Baby food purees, juices and general canning. Raw materials are fruit and vegetables. Higher costs of baby food canning are due to a wide variety of packaging types, smaller lots and higher production quality. Prices for fruit and vegetables were lower in 2004 due to a good harvest, which enabled the Company to earn higher margins.

Credit Linked Notes November 2005 24

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Estmilk and Holor: USD 13.6 mln

– baby food production facilities, USD 12.5 mln

Capital expenditures:– milk production facilities,

USD 35.6 mln over 2005-2006;

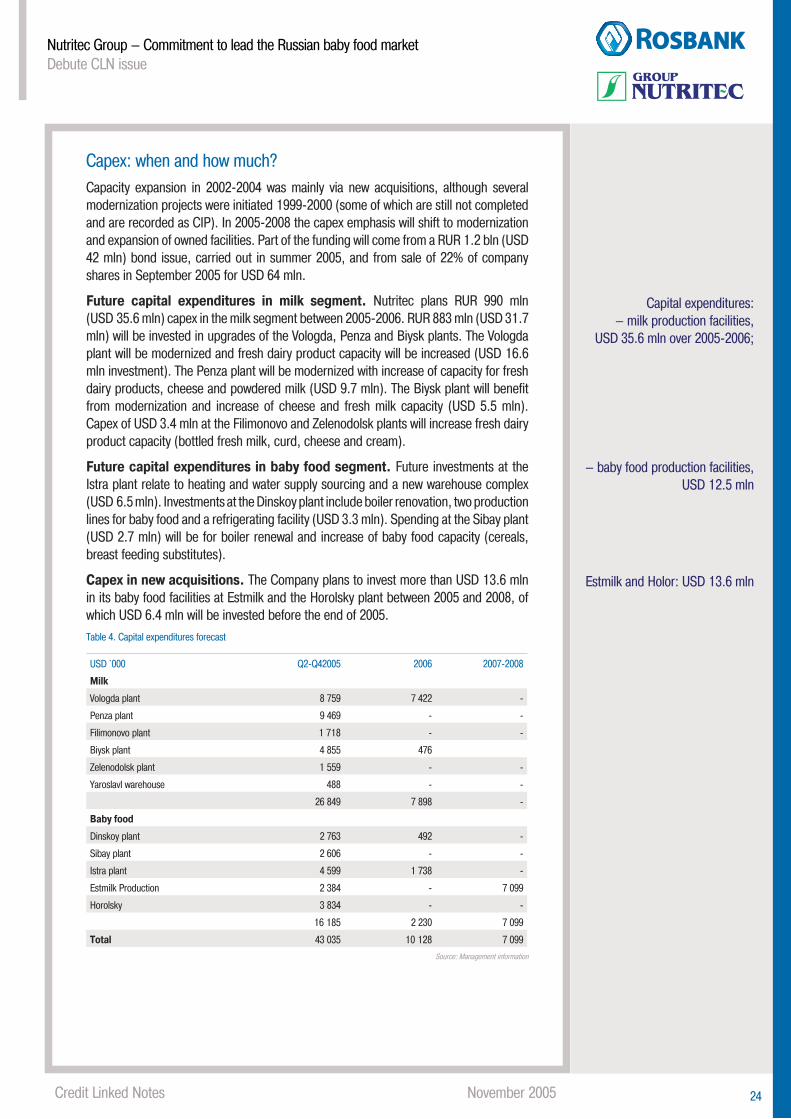

Capex: when and how much?Capacity expansion in 2002-2004 was mainly via new acquisitions, although several modernization projects were initiated 1999-2000 (some of which are still not completed and are recorded as CIP). In 2005-2008 the capex emphasis will shift to modernization and expansion of owned facilities. Part of the funding will come from a RUR 1.2 bln (USD 42 mln) bond issue, carried out in summer 2005, and from sale of 22% of company shares in September 2005 for USD 64 mln.

Future capital expenditures in milk segment. Nutritec plans RUR 990 mln (USD 35.6 mln) capex in the milk segment between 2005-2006. RUR 883 mln (USD 31.7 mln) will be invested in upgrades of the Vologda, Penza and Biysk plants. The Vologda plant will be modernized and fresh dairy product capacity will be increased (USD 16.6 mln investment). The Penza plant will be modernized with increase of capacity for fresh dairy products, cheese and powdered milk (USD 9.7 mln). The Biysk plant will benefit from modernization and increase of cheese and fresh milk capacity (USD 5.5 mln). Capex of USD 3.4 mln at the Filimonovo and Zelenodolsk plants will increase fresh dairy product capacity (bottled fresh milk, curd, cheese and cream).

Future capital expenditures in baby food segment. Future investments at the Istra plant relate to heating and water supply sourcing and a new warehouse complex (USD 6.5 mln). Investments at the Dinskoy plant include boiler renovation, two production lines for baby food and a refrigerating facility (USD 3.3 mln). Spending at the Sibay plant (USD 2.7 mln) will be for boiler renewal and increase of baby food capacity (cereals, breast feeding substitutes).

Capex in new acquisitions. The Company plans to invest more than USD 13.6 mln in its baby food facilities at Estmilk and the Horolsky plant between 2005 and 2008, of which USD 6.4 mln will be invested before the end of 2005.Table 4. Capital expenditures forecast

USD `000 Q2-Q42005 2006 2007-2008

Milk

Vologda plant 8 759 7 422 -

Penza plant 9 469 - -

Filimonovo plant 1 718 - -

Biysk plant 4 855 476

Zelenodolsk plant 1 559 - -

Yaroslavl warehouse 488 - -

26 849 7 898 -

Baby food

Dinskoy plant 2 763 492 -

Sibay plant 2 606 - -

Istra plant 4 599 1 738 -

Estmilk Production 2 384 - 7 099

Horolsky 3 834 - -

16 185 2 230 7 099

Total 43 035 10 128 7 099

Source: Management information

Credit Linked Notes November 2005 25

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

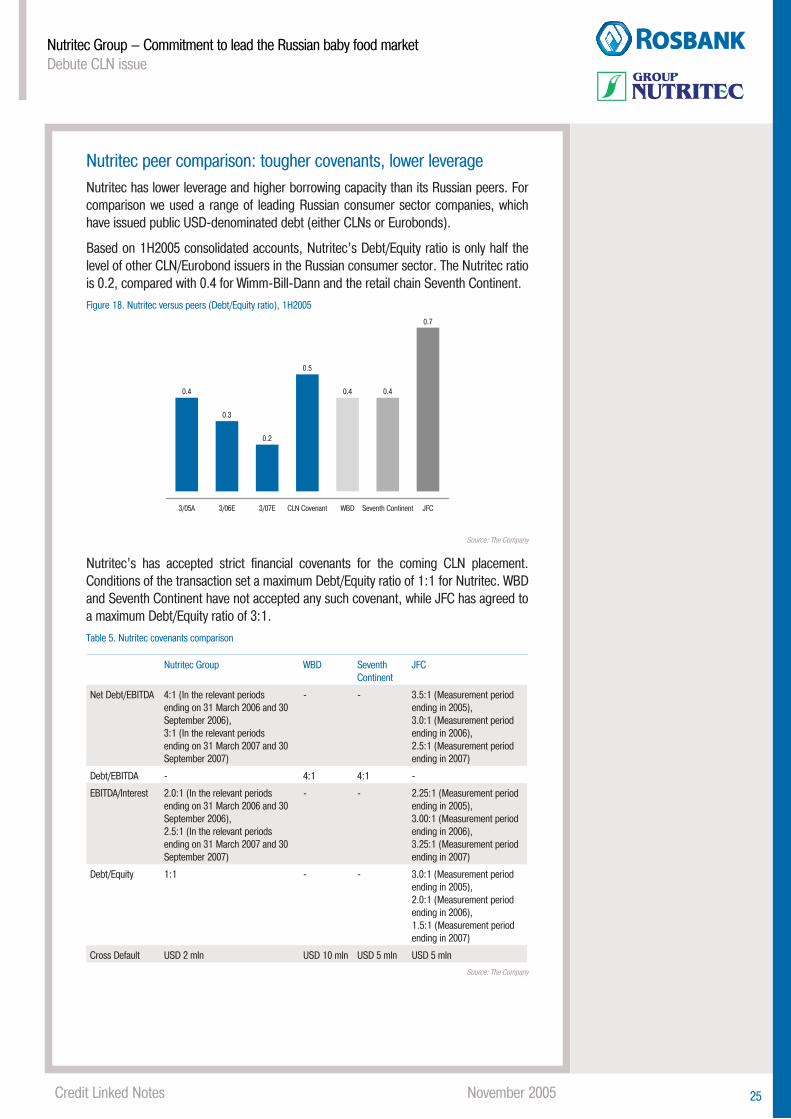

Nutritec peer comparison: tougher covenants, lower leverageNutritec has lower leverage and higher borrowing capacity than its Russian peers. For comparison we used a range of leading Russian consumer sector companies, which have issued public USD-denominated debt (either CLNs or Eurobonds).

Based on 1H2005 consolidated accounts, Nutritec’s Debt/Equity ratio is only half the level of other CLN/Eurobond issuers in the Russian consumer sector. The Nutritec ratio is 0.2, compared with 0.4 for Wimm-Bill-Dann and the retail chain Seventh Continent.Figure 18. Nutritec versus peers (Debt/Equity ratio), 1H2005

JFCSeventh ContinentWBDCLN Covenant3/07E3/06E3/05A

0.7

0.40.4

0.5

0.2

0.3

0.4

Source: The Company

Nutritec’s has accepted strict financial covenants for the coming CLN placement. Conditions of the transaction set a maximum Debt/Equity ratio of 1:1 for Nutritec. WBD and Seventh Continent have not accepted any such covenant, while JFC has agreed to a maximum Debt/Equity ratio of 3:1.Table 5. Nutritec covenants comparison

Nutritec Group WBD Seventh Continent

JFC

Net Debt/EBITDA 4:1 (In the relevant periods ending on 31 March 2006 and 30 September 2006),3:1 (In the relevant periods ending on 31 March 2007 and 30 September 2007)

- - 3.5:1 (Measurement period ending in 2005),3.0:1 (Measurement period ending in 2006),2.5:1 (Measurement period ending in 2007)

Debt/EBITDA - 4:1 4:1 -

EBITDA/lnterest 2.0:1 (In the relevant periods ending on 31 March 2006 and 30 September 2006),2.5:1 (In the relevant periods ending on 31 March 2007 and 30 September 2007)

- - 2.25:1 (Measurement period ending in 2005),3.00:1 (Measurement period ending in 2006),3.25:1 (Measurement period ending in 2007)

Debt/Equity 1:1 - - 3.0:1 (Measurement period ending in 2005),2.0:1 (Measurement period ending in 2006),1.5:1 (Measurement period ending in 2007)

Cross Default USD 2 mln USD 10 mln USD 5 mln USD 5 mln

Source: The Company

26Credit Linked Notes November 2005

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

Consolidated Balance Sheet of Nutrinvestholding, IFRS, USD `000 *

1Q2005 1Q2004

ASSETS

Non-current assets

Property, plant and equipment 92 028 98 968

Investments in unconsolidated subsidiaries 2 331 -

Long term finance assets 54 1 402

Other long term assets 180 2

94 594 100 372

Current assets

Short term finance assets 2 956 338

Inventories 10 997 4 426

Prepaid expenses 2 832 1 977

VAT receivable 2 641 3 983

Trade and other receivables 24 352 16 153

Cash and cash equivalents 14 497 467

58 275 27 343

Total assets 152 868 127 715

SHAREHOLDERS’ EQUITY AND LIABILITIES

Shareholders’ Equity

Share capital 6 6

Retained earnings 34 191 22 095

34 197 22 102

Minority interest 36 293 37 956

Non-current liabilities

Loans and borrowings 12 484 20 645

Deferred tax liabilities 8 360 6 823

20 844 27 467

Current liabilities

Loans and borrowings 26 075 12 039

Short-term portion of long-term loans and borrowings 12 662 3 175

Income tax payable 561 1 354

Trade and other payables 20 172 22 343

Advances received 917 -

Deferred income 1 147 1 280

61 535 40 190

Total Shareholders’ equity and Liabilities 152 868 127 715

* excluding financial results of Estmilk and Plemzavod Zarya

27Credit Linked Notes November 2005

Nutritec Group – Commitment to lead the Russian baby food marketDebute CLN issue

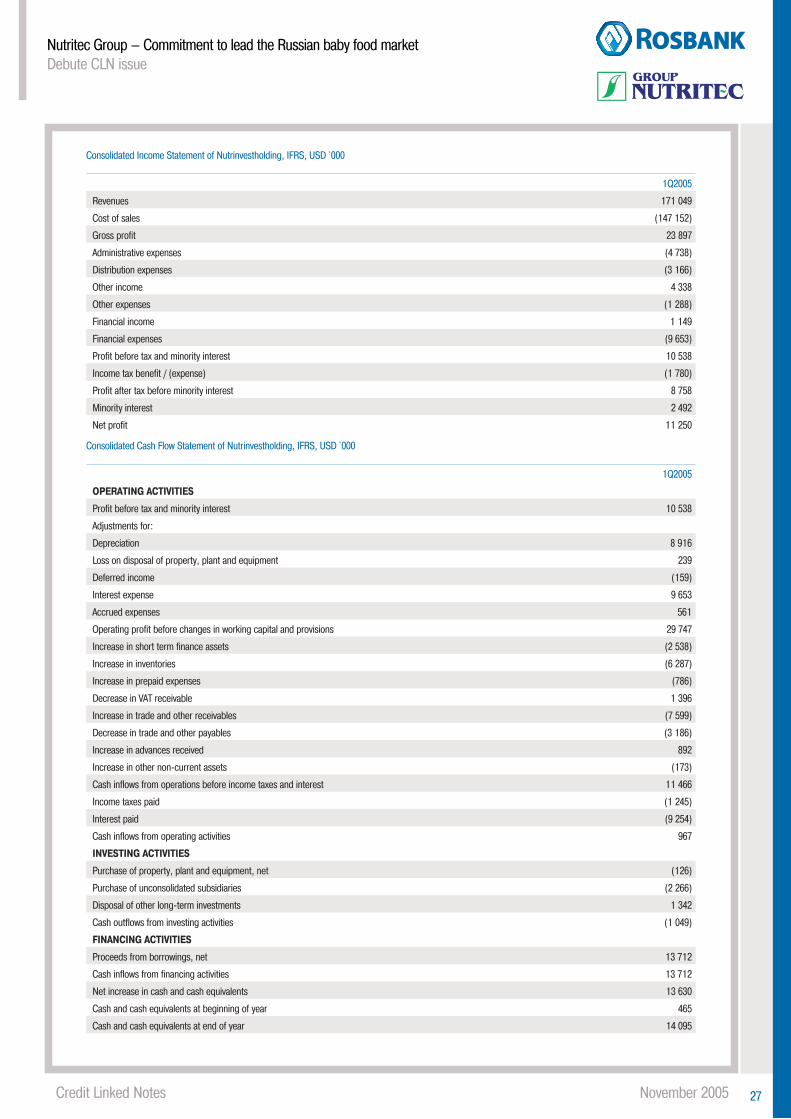

Consolidated Income Statement of Nutrinvestholding, IFRS, USD `000

1Q2005

Revenues 171 049

Cost of sales (147 152)

Gross profit 23 897

Administrative expenses (4 738)

Distribution expenses (3 166)

Other income 4 338

Other expenses (1 288)

Financial income 1 149

Financial expenses (9 653)

Profit before tax and minority interest 10 538

Income tax benefit / (expense) (1 780)

Profit after tax before minority interest 8 758

Minority interest 2 492

Net profit 11 250

Consolidated Cash Flow Statement of Nutrinvestholding, IFRS, USD `000

1Q2005

OPERATING ACTIVITIES

Profit before tax and minority interest 10 538

Adjustments for:

Depreciation 8 916

Loss on disposal of property, plant and equipment 239

Deferred income (159)

Interest expense 9 653

Accrued expenses 561

Operating profit before changes in working capital and provisions 29 747

Increase in short term finance assets (2 538)

Increase in inventories (6 287)

Increase in prepaid expenses (786)

Decrease in VAT receivable 1 396

Increase in trade and other receivables (7 599)

Decrease in trade and other payables (3 186)

Increase in advances received 892

Increase in other non-current assets (173)

Cash inflows from operations before income taxes and interest 11 466

Income taxes paid (1 245)

Interest paid (9 254)

Cash inflows from operating activities 967

INVESTING ACTIVITIES

Purchase of property, plant and equipment, net (126)

Purchase of unconsolidated subsidiaries (2 266)

Disposal of other long-term investments 1 342

Cash outflows from investing activities (1 049)

FINANCING ACTIVITIES

Proceeds from borrowings, net 13 712

Cash inflows from financing activities 13 712

Net increase in cash and cash equivalents 13 630

Cash and cash equivalents at beginning of year 465

Cash and cash equivalents at end of year 14 095

Investment BankingPhone: +7 (095) 234-0947Fax: +7 (095) [email protected]

Head of Investment Banking DepartmentAlexey [email protected]: +7 (095) 234-0974

Capital Markets Division

Origination & Structuring

Managing DirectorMikhail [email protected]: +7 (095) 234-0974

Senior ManagerAlexander [email protected]: +7 (095) 725-5637

ManagerIlya [email protected]: +7 (095) 725-5637

ManagerAlexey [email protected]: +7 (095) 725-5637

Sales & Syndication

DirectorPhilipp [email protected]: +7 (095) 204-9515

ManagerDmitry [email protected]: +7 (095) 725-5477

ManagerIrina [email protected]: +7 (095) 725-5477

AnalystAnna [email protected]: +7 (095) 725-5477

This report is not an offer or solicitation to buy or sell any securities or related financial instruments or to participate in any trading strategy. Although the information and opinions expressed in this report are believed to be accurate as of this date, no express or implied warranties or representation are being made as to accuracy or completeness. The information and opinions presented have not been tailored to any specific transaction of any third party and are not a detailed analysis of a specific situation of any third party. Our opinions may change without further notice. The information and opinions expressed in this report are not a substitute for an independent assessment of an individual’s investment needs and goals. Opinions expressed in this report may differ or be contrary to the opinions of other units of Rosbank (hereinafter referred to as the Bank) as a result of using different assumptions or criteria or analysis of information for different purposes. This document is for information purposes only. Descriptions of any company or companies or their securities or the markets or developments mentioned herein are not intended to be complete. Any statements regarding past performance are not necessarily indicative of future performance. The Bank, its affiliates, officers, directors and/or employees and/or related parties may hold interests in or may have performed services for one or more of the companies mentioned in this report and/or may hold such interests and perform or seek to perform such services in the future subject to the Bank’s internal procedures aimed at avoidance of conflict of interest. The Bank or any of its affiliates may act or have acted as market-makers in securities or other financial instruments mentioned herein or securities underlying such financial instruments or related to those securities. Furthermore, the Bank may have or have had a relationship with or provide or have provided investment banking, capital markets and/or other financial services to the relevant companies. Employees of the Bank or its affiliates may serve or have served as officers or directors of the relevant companies subject to the Bank’s internal procedures aimed at avoidance of conflict of interest. The Bank has developed and introduced special procedures preventing unendorsed use of business information or conflict of interests arising from the provision by the Bank of advisory and other services in the financial market. Neither the Bank nor any of its affiliates accept any liability arising from the use of any of the information or opinions expressed in this report. This report may not be reproduced, distributed or published, in whole or in part, for any purpose without the express written permission of the Bank.

This report may be used by investors within the Russian Federation subject to Russian laws. Foreign investors (including but not limited to those from Switzerland, the Netherlands, Ger-many, Italy, France, Sweden, Denmark, and Austria) may use this report provided they are deemed to be institutional investors under the laws of the country of registration. This report was prepared by the Bank, which is not registered as a broker-dealer by the SEC and is distributed to persons who by their acceptance thereof confirm that they are a major institutional investor in the US as defined in Regulation 15a–16 of the US Securities Act of 1934 and understand the risks involved in executing transactions in securities. This report was prepared by the Bank, which is not registered by the FSA and is not available to private customers in the United Kingdom.

Each research analyst primarily responsible for the content, in whole or in part, of this research report, certifies that with respect to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal views about those securities or issuers; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in the research report and (3) such research analyst does not perform transactions in securities issued by companies that he or she covers. The Bank accepts no responsibility for any use of information based on the views of any research analyst in relation to any relevant securities.