november 2017 the winning move: industry … / the winning move: industry consolidation in asia...

TRANSCRIPT

The winning move: Industry consolidation in Asia Pacific

I N D U S T RY C O N S O L I D AT I O N

N O V E M B E R 2017

Contents

3 Foreword

4 Survey at a glance • Corporate Asia’s growth strategy

• Asia Pacific’s automakers and consumer goods companies will pursue various actions to grow

• Regional drivers, trends, and challenges

5 Introduction • Short-term drivers and trends

• Supportive policies or regulatory roadblocks?

• Competing corporate priorities

10 Automotive • Wheels of change: Automotive tech trends

• Do not idle: Current and future strategies

14 Consumer goods and retail • Value chain expansion

• Business model evolution

• Internal capabilities still matter

19 Economic outlook: Hope on the horizon? • Country-by-country expectations

• Business model evolution

• Internal capabilities still matter

22 Conclusion and methodology

3 / The winning move: Industry consolidation in Asia Pacific

ForewordWhat form will the corporate growth narrative in Asia Pacific take in 2017 and the years ahead? Will corporate restructuring continue to be a prevailing theme, or will aggressive acquisition and merger campaigns begin unfolding as economic conditions and market expectations begin to thaw?

Those were the questions driving our research into corporate activity across Asia Pacific this year as we asked executives and their management teams as well as other market participants what issues and strategies were top of mind as they planned for the months and years ahead. Their sentiments and shared experiences have helped paint a picture of current priorities, upcoming challenges, and projected outcomes regionwide and within several major industries.

This year, in addition to ascertaining the broader views on the Asia Pacific market, our survey focused on the trends and challenges that are shaping—and in many ways reshaping—the region’s automotive and consumer goods and retail industries. The views of executives in those industries have been both insightful and revealing.

From the market sentiments, it seems at least in the short term that corporate activity will have an internal focus—in the forms of performance improvement and the development of new business models—before decision makers make more-ambitious moves outside their organizations. Those responses suggest that consolidation and mergers within certain industries would happen only after such inward-looking reorganizational ventures are completed.

Recent headlines, however, point to the benefits that M&As among industry competitors could offer if it’s a response taken sooner rather than later. For instance, several merger waves in various industries such as global shipping, European steel, and semiconductor manufacturers show how industry tie-ups are helping corporations otherwise struggling with overcapacity and various economic headwinds. Asia’s automotive and consumer goods companies can take similar steps as they face similar trials, but the question is, will they?

4 / The winning move: Industry consolidation in Asia Pacific

Survey at a glance

Corporate Asia’s growth strategy • Industry consolidation was overwhelmingly chosen as the top forward-looking growth

strategy, according to 69% of respondents, followed by the development of new business models (55%).

• Immediate, short-term priorities will focus on performance improvement (77%), operational cost reduction (31%), and the development of new business models (31%).

Asia Pacific’s automakers and consumer goods companies will pursue various actions to grow

• Fully 87% of respondents in both the automotive and consumer goods industries agreed that industry consolidation will be part of their corporate actions in the next five years.

• In varying degrees, revising business models and adapting them to changing technologies and increasing competition will be top priorities they plan to attend to both now and into the near future.

• Performance improvement is the top priority in both the automotive (63%) and consumer goods (71%) markets.

Regional drivers, trends, and challenges • Increasing competition will be the top driver of corporate actions in the year ahead

in both the automotive and consumer goods industries, but lack of innovation and lack of product development will plague consumer goods companies (58% of respondents), and declining market share will be a concern for automotives (60%).

• In some jurisdictions, such as China and Japan, automotive companies might find it more difficult to restructure or consolidate than consumer goods companies might.

• Only 37% of respondents said economic conditions have remained unchanged during the past 12 months, whereas 80% anticipate a positive outlook despite many signs in each of Asia’s markets that uncertainty lies ahead.

5 / The winning move: Industry consolidation in Asia Pacific

Introduction

Mergers and mega-alliances may represent the saving grace for companies struggling against overcapacity, innovative new industry entrants, and disruptive technologies. And it seems that conviction is only growing stronger among business leaders across Asia.

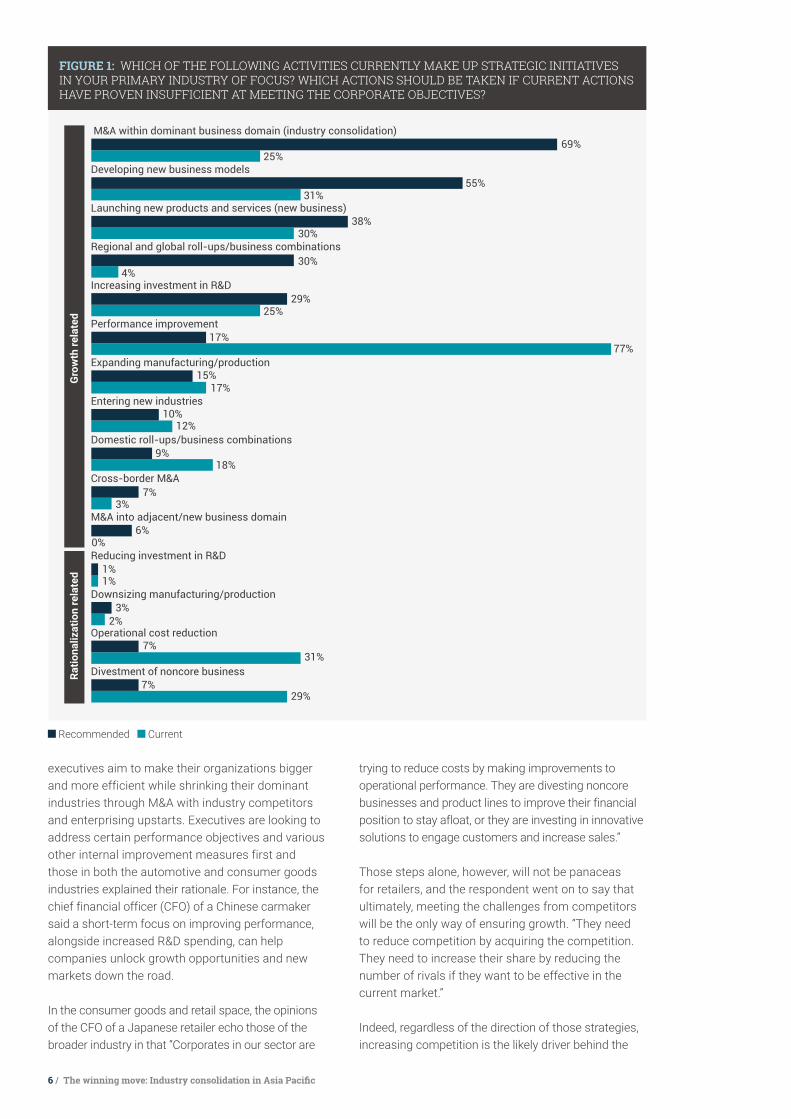

In our research this year, 69% of respondents said M&A within a company’s dominant business domain is the top recommended action companies should consider—especially companies in the automotive and consumer goods spaces (figure 1). That compares with only 31% in a similar survey conducted in 2016.

In highly fragmented industries, M&A seems to be the obvious course of action, and recent trends support the assertion. For instance, the global shipping market has started showing signs of recovery after nearly a decade of uncertainty—a turnaround that has been orchestrated by an uptick in deal making as sweeping consolidation takes shape.1 Likewise, merger mania has helped semiconductor companies gain scale and remain competitive as new entrants, new technologies, and new consumer demands add to cost burdens and other pressures.2

However, in industries that are only just starting to feel the pains of slipping revenue streams or shifting consumer trends, merging with industry rivals may not be one of the first levers management teams decide to pull. Indeed, for most of the Asian corporations surveyed, performance improvement is the go-to solution, and an overwhelming 77% of business leaders report that corporate activity leans heavily on this area of corporate development.

To a much lesser extent, growth initiatives led by the development of new business models (31%) and the launching of new products and services (30%) are also priorities, alongside such rationalization strategies as

operational cost reductions (31%) and divestments of noncore businesses (29%). Despite the forward-looking, 69% of opinions for recommended actions, only 25% of respondents said their corporations were currently trying to acquire or merge with enterprises in their primary industries.

So, what do these results tell us about the mind-set of corporate leaders across Asia? And what has changed since last year to impel them to the deal table in search of merger opportunities?

S H O RT-T E R M D R I V E R S A N D T R E N D SOur survey last year identified restructuring as a key trend as corporations struggled to maintain growth and to operate against various negative economic forces. Managers were busy looking inward to make their companies better and stronger by focusing on financial and operational improvements. Keeping debt levels under control was also a priority.

Not so in 2017, because many respondents said that degrees of certainty and stability had returned to their markets. Now, in addition to boosting strength and performance—and to facilitating growth—

69%Respondents reporting that industry consolidation is both necessary and effective for the achievement of corporate expansion and growth when current actions prove ineffective

1 “Global shipping market shows signs of rebound, says broker,” Financial Times, August 14, 2017. 2 “Back to the Future: Chip makers are putting the silicon back in Silicon Valley,” Forbes, August 3, 2017.

6 / The winning move: Industry consolidation in Asia Pacific

executives aim to make their organizations bigger and more efficient while shrinking their dominant industries through M&A with industry competitors and enterprising upstarts. Executives are looking to address certain performance objectives and various other internal improvement measures first and those in both the automotive and consumer goods industries explained their rationale. For instance, the chief financial officer (CFO) of a Chinese carmaker said a short-term focus on improving performance, alongside increased R&D spending, can help companies unlock growth opportunities and new markets down the road.

In the consumer goods and retail space, the opinions of the CFO of a Japanese retailer echo those of the broader industry in that “Corporates in our sector are

trying to reduce costs by making improvements to operational performance. They are divesting noncore businesses and product lines to improve their financial position to stay afloat, or they are investing in innovative solutions to engage customers and increase sales.”

Those steps alone, however, will not be panaceas for retailers, and the respondent went on to say that ultimately, meeting the challenges from competitors will be the only way of ensuring growth. “They need to reduce competition by acquiring the competition. They need to increase their share by reducing the number of rivals if they want to be effective in the current market.”

Indeed, regardless of the direction of those strategies, increasing competition is the likely driver behind the

Divestment of noncore business

Operational cost reduction

Downsizing manufacturing/production

Reducing investment in R&D

M&A into adjacent/new business domain

Cross-border M&A

Domestic roll-ups/business combinations

Entering new industries

Expanding manufacturing/production

Performance improvement

Increasing investment in R&D

Regional and global roll-ups/business combinations

Launching new products and services (new business)

Developing new business models

M&A within dominant business domain (industry consolidation)

Ratio

naliz

atio

n re

late

d G

row

th re

late

d

69%25%

55%31%

38%30%

30%4%

29%25%

17%77%

15%17%

10%12%

9%18%

7%3%

6%0%

1%1%

3%2%

7%31%

7%29%

FIGURE 1: WHICH OF THE FOLLOWING ACTIVITIES CURRENTLY MAKE UP STRATEGIC INITIATIVES IN YOUR PRIMARY INDUSTRY OF FOCUS? WHICH ACTIONS SHOULD BE TAKEN IF CURRENT ACTIONS HAVE PROVEN INSUFFICIENT AT MEETING THE CORPORATE OBJECTIVES?

Recommended Current

7 / The winning move: Industry consolidation in Asia Pacific

initiatives, ranking among the top triggers in both the automotive and consumer goods industries (figure 2). Competition is increasing in all sectors, fuelled by the emergence of new technologies which breach traditional industries, transform the status quo and dissolve former barriers to entry.

S U P P O RT I V E P O L I C I E S O R R E G U L ATO RY R O A D B LO C K S?Policy frameworks and new regulations across Asia have been mostly accommodating toward corporate restructurings and industry consolidation (figure 3). Survey respondents said many policy makers have started encouraging those actions in various segments of the economy to address overcapacity or as alternatives to corporate revitalization via capital infusions and bailouts from the government. “Governments across Asia are finally understanding the importance of reforms and policy changes to support consolidations and restructuring in key industries,” said the partner of a Chinese law firm. “In many countries, this is a national priority as policy makers try to create an environment that is positive for the investment needed to drive overall economic growth.”

In South Korea, noting an increasingly positive climate, the head of strategy at a South Korean automaker said, “The government last year implemented strong measures to address the debt problem and rising stress levels among the nation’s shipbuilders. Now regulators continue to roll out a strong, efficient system that will help channel sources of capital for companies facing financial difficulties.” Going further, the respondent said such efforts may be necessary

as a short-term save because the nation’s automakers are struggling against weak domestic demand and sluggish exports.

In China, the managing director of a Chinese sovereign wealth fund said the government is implementing regulatory changes to help companies restructure—specifically by trying to create sources of capital that struggling firms can inject into their operations to manage debt.

However, the managing director of a Chinese private-equity firm said that while those changes are happening overall, the Chinese government is still relatively rigid in its policies toward restructuring and industry consolidation. This respondent also mentioned that government policies in Hong Kong were much more conducive to turnarounds and mergers.

Increasing competition

Lack of innovation/product development

Declining market share

Declining revenue

Declining profitability

Political changes/policy uncertainty

67% 65% 60% 45% 53% 52%

47% 58% 43% 58% 30% 23%

FIGURE 2: WHAT ARE THE MOST COMMON EVENTS OR DEVELOPMENTS THAT TRIGGER THE IMPLEMENTATION OF THE INITIATIVES IN YOUR PRIMARY INDUSTRY?

Governments across Asia are finally understanding the importance of reforms... to support consolidations and restructuring in key industries.

Automotive Consumer goods and retailers' own brands

8 / The winning move: Industry consolidation in Asia Pacific

Japan again stands out as the least accommodating jurisdiction for corporate restructuring and consolidations, according to respondents. As the managing director of a South Korean private-equity firm put it, “Much in Japan still happens under the watchful eye of the government, and the government’s involvement in restructuring and consolidation activities is often too deep. Because of that, it’s difficult to complete these tasks in the short time frames they often demand to be effective. Such delays can shake the confidence of investors and other participants that restructurings or consolidations will be successful.”

In the Japanese automotive industry, restructurings and consolidations have been slow to form given the regulatory environment and strict labor laws. “Restructuring and consolidation often mean closing down operations and cutting jobs. Considering the strict Japanese laws and policies on labor, it’s very difficult to go forward with these agendas; and workforce rationalization is often met with government interference in the process,” says the CFO of a Chinese automotive company with business dealings in Japan.

Reiterating that point, the director of strategy at a Japanese automaker said that in Japan, bold structural reforms are required to drive innovation and growth among Japan’s automakers.

C O M P E T I N G C O R P O R AT E P R I O R IT I E SIn the list of current and future priorities, respondents highlighted several competing responses and growth measures they are considering. Taking a longer-term view, industry consolidation in both the automotive and consumer goods industries is likely to take place, albeit gradually, across a five-year time horizon—an opinion shared by 76% of respondents (figure 4). But only 14% of respondents said they anticipated companies in those industries to consolidate in the next six months.

As with earlier commentary and from the insights in figure 1, performance improvement and other growth initiatives will serve as short-term solutions. The director of strategy at a Chinese automaker said the next six months will be spent completing orders, and so improving performance will help them accomplish this. The respondent also said corporations across various industries would likely restructure their operations to improve efficiencies. After that, consolidation would be given more-serious consideration.

Another finding involved revising outdated business models. Elaborating on the need to improve upon this area, the head of a Hong Kong bank said, “Business models that most companies have may be inadequate—especially given the speed with which the market changes. Companies in Asia are generally slower

China60% 77%

South Korea

100% 94%

Japan57% 74%

Hong Kong

80% 77%

FIGURE 3: PERCEPTIONS THAT GOVERNMENT POLICIES AND OTHER ENFORCEMENT VEHICLES TOWARD INDUSTRY CONSOLIDATION AND BROADER RESTRUCTURING WITHIN RESPONDENT PRIMARY INDUSTRY OF FOCUS WERE "ACCOMMODATING".*

Automotive Consumer goods *NOTE: Remaining percentages were rated as "not accommodating".

9 / The winning move: Industry consolidation in Asia Pacific

to adapt to market changes or changes in consumer tastes compared with their Western counterparts, so it’s important for them to start here, reassess their business approaches, and then use that to focus on how they want to grow.”

Shedding light on the direction such changes were likely to take, several executives reported a shift away from diversification strategies to those favoring a focused, concerted effort to enhance the core business. Said the head of finance at a Japanese automaker, “I think that in the next five years, M&A within our core business and core industry will be the main driver of corporate activity because diversification has failed to yield the expected results.”

From those insights, it seems that sentiment supports the restructuring of organizations to provide short-term

fixes to corporate Asia’s more immediate problems. Long-term change and sustained growth will likely come from industry consolidation as respondents continue thinking of such actions in a futuristic sense rather than as urgent priorities.

Although the rationales for their actions appear sound, are these corporations waiting too long to pull the trigger on consolidation? Recent events in the shipping industry, which has seen a number of once-dominant players fall into bankruptcy, would suggest quick action is the right action. And some industries may be reaching a point of critical mass and competition where consolidation is inevitable.

With that question and others in mind, we now look at industry-specific challenges that Asia’s automakers and consumer goods companies face.

Downsizing manufacturing/production

Operational cost reduction

Restructuring

M&A into adjacent/new business domain

Entering new industries

Expanding manufacturing/production

Regional and global roll-ups/business combinations

Cross-border M&A

Domestic roll-ups/business combinations

Performance improvement

Increasing investment in R&D

Launching new products and services (new business)

Developing new business models

M&A within dominant business domain (industry consolidation)

Non

grow

thG

row

th

76%64%14%

44%45%

49%

31%38%

49%

25%30%

20%

14%21%

69%

10%

25%18%

11%

12%17%17%

13%11%

16%

10%5%

2%4%

22%

5%7%

12%

1%0%

0%

1%

20%21%

35%19%

3%

FIGURE 4: WHEN WILL THE FOLLOWING ACTIVITIES LIKELY BE EXECUTED?

In the next five years In the next year In the next six months

10 / The winning move: Industry consolidation in Asia Pacific

In our conversations with Asia’s auto executives, the consensus view was that many in the industry have been slow to catch up to the relentless pace of change via new technologies. The emergence and convergence of those technologies were among the leading reasons that would drive midterm corporate strategies. Indeed, 87% of respondents said industry consolidation will happen as overcrowding and disruptive forces contribute to widespread auto mergers (figure 5).

Market data shows that a rolling wave of consolidations among global automotive suppliers and manufacturers as well as those with technology supporting those operations is already under way. Since 2015, more than US$80 billion in deals globally has been announced, and even though most of that activity has been driven by established automakers in more-mature markets, the rise of Asian autos is contributing to the trend. From the totals, during that same time frame, Asian automotive M&A totalled US$23 billion through 161 deals (figure 6).

Toyota Motor’s acquisition of Daihatsu Motor (a deal valued at US$3.3 billion) and Nissan’s taking a controlling stake in Mitsubishi Motors (US$2.1 billion) have been most notable among recent

original-equipment-manufacturer (OEM) deals in Asia. In the supplier segment, Samsung’s acquisition of Harman (US$8 billion) aimed to accelerate the growth in the South Korean conglomerate’s automotive and connected car segments. KKR’s acquisition of Calsonic Kansei (US$4.5 billion) from Nissan and other investors is expected to increase the speed of industry consolidation.

All of those transactions occurred in 2016. Deal making in 2017 has been more moderate, with fewer megadeals. Deal totals, however, have sustained momentum—rising gradually since the outset of 2015—as ambitious Chinese automakers join the deal making and pursue cross-border buys (figure 6). For instance, China’s Geely in June 2017 inked a deal to buy a stake in Malaysian PROTON and US start-up Terrafugia. Also in June 2017, US-based Key Safety Systems (KSS) agreed to take over air-bag maker Takata following the latter’s filing for bankruptcy. Headquartered in Sterling Heights, KSS was itself acquired by Joyson Electronics, a Chinese company, in 2016.

More such matchups are likely as Asian automakers play more significant roles in the transition to a more concentrated industry. Vertical integrations and global

Automotive

Next six months Next year Next five years

Performance improvement

Industry consolidation

Industryconsolidation63% 87% 87%

Launching new products and services (new business)

Developing new business models

Developing new business models 47% 53%47%

Developing new business models

Domestic roll-ups and business combinations/Increasing investment in R&D

Cross-border M&A30% 37%47%

FIGURE 5: TOP THREE MOST-LIKELY CORPORATE ACTIONS TO BE EXECUTED ACROSS TIME FRAMES

11 / The winning move: Industry consolidation in Asia Pacific

expansion strategies are also likely to contribute to the trend. The head of finance at a Japanese automaker confirms that outlook by saying, “I think that over the course of the next five years, the focus for us and the industry will be entirely on building the business through mergers and acquisitions with our rivals.”

It seems, then, that the auto market in Asia and globally stands on the threshold of a sea change as manufacturers and suppliers shift strategic gears to grow their businesses by shrinking the industry.

W H E E L S O F C H A N G E: A U TO M OT I V E T E C H T R E N D SAs noted, tech was one of the main forces likely to drive industry actions among Asia’s automakers. Indeed, the auto executives in our survey said the relentless march of technology in recent years has blindsided an industry that has seen little in the way of dramatic change in its more-than-100-year history. Now, the industry, long dominated by the internal combustion engine, is making way for new technology entrants and alternatives—such as electric vehicles—as well as autonomous vehicles.

US$23 billionApproximate value of automotive M&A deals since 2015 in Asia Pacific in which both buyer and seller were involved in the automotive/vehicle manufacturing trade

US$

(mill

ions

)

Num

ber of transactions

0

5

10

15

20

Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q12015 2016 2017

11

13

20

13 13

19

16 16 16 16

8

$0

$2,000

$4,000

$6,000

$8,000

FIGURE 6: ASIA PACIFIC AUTOMOTIVE M&A*

Deal volume Deal value*NOTE: Data reflects deals wherein both bidder and target focused predominantly on the automotive trade. Deals involve transactions in which the target was based in Asia Pacific.

12 / The winning move: Industry consolidation in Asia Pacific

From those trends and many others, a new automotive ecosystem is taking shape, and tech is unquestionably behind the wheel of these revolutionary developments. In the list of top new technologies dominating this fast-changing environment, four standouts have been leading the charge: connectivity, autonomous driving, shared mobility, and electrification.

The change has been impressive, to say the least, because just five years ago, neither autonomous cars nor alternative technologies such as electric vehicles were expected to have as much of an impact on the industry as they’ve had (figure 7). Now they’re an entrenched part of the industry’s vernacular. Even more than the speed of those advancements, consumers’ rapid uptake and demand for electric vehicles and hybrid vehicles have moved more quickly than many of the traditional automakers could have predicted.

Most of our survey respondents also did not foresee the automotive landscape in Asia—or globally—as becoming as competitive as it is today. With technology breaking down historically higher barriers of entry, long-held

market shares are far from secure. In addition, the future doesn’t look much better. In the next five years, entrants in the form of new competitors together with alternative technologies will raise significant speed bumps, according to 87% of respondents (figure 8). And the inability to catch up with technological advancements will likewise prove challenging (77%).

D O N OT I D L E: C U R R E NT A N D F U T U R E S T R AT E G I E SRespondents agreed that past strategies took for granted the needs for investment in R&D and for deal making to shore up industry fragmentation. Reflecting on corporate actions, most auto executives noted that they had focused on internal issues—in the forms of operational improvements and organizational restructurings (80%) and on strengthening their current product portfolios (57%)—rather than focusing on strategy—specifically, plans aimed at expansion via inorganic growth (figure 9).

In retrospect, those respondents agreed that greater investment in R&D would have enabled them to drastically expand their technological competencies,

Entrants of new competitors

and alternative technologies

Inability to catch up with technological advancement

Increasing costs

Acquisition by others

No concerns Other

87% 77% 70% 37%

3%3%

FIGURE 8: WHAT ARE THE TOP CONCERNS SURROUNDING YOUR BUSINESS IN THE NEXT FIVE YEARS?

Technology advancement

of autonomous cars/ADAS*

Increase in competition from new entrants and

alternative technologies

Necessity to meet OEM demand for global platform

M&A activities leading to change

in competitive landscape

Other

90% 83% 70% 43%

3%

FIGURE 7: WHAT ARE THE TOP TRENDS OR CHALLENGES THAT YOU DID NOT ANTICIPATE FIVE YEARS AGO?

*NOTE: "ADAS" refers to advanced driver-assistance system.

13 / The winning move: Industry consolidation in Asia Pacific

setting them up to assume stronger market positions today. With regard to future targets and desired outcomes, increasing commitments to research are likely within the next 12 months, as is the rising importance of the development of new business models (mentioned in figure 5) to maximize the advances’ impacts on top-line and bottom-line growth.

The challenge here, then, becomes a financial one. The heavy capital needed for such cutting-edge R&D programs—not to mention the time and talent required—can prove prohibitive, even for traditional OEMs and more so for smaller automakers. As such, the more practical and economical approach to accomplishing technological superiority—and one supported by the wide body of auto executives in our survey—is through mergers. Indeed, as auto OEMs chase technology to remain relevant, with the pushes toward electrification and autonomous driving leading the trend, smaller, cash-strapped carmakers are likely to join with their larger rivals by sharing resources and saving on costs.3

Alternatively, and perhaps as a precursor to a complete merger, partnerships and strategic alliances between traditional OEMs and suppliers and new tech entrants could also serve as channels for sharing and advancing technological competencies while mitigating risks. Partnerships and strategic alliances also help defray the financial and time-related costs of the R&D process. According to 67% of respondents, this course of action was taken and produced desired results.

Recognizing the importance of such moves, the CFO of a Chinese automaker said, “We should have partnered with relevant suppliers and OEMs to get the right technologies and use them to further our growth. We didn’t do that, but our competitors did, and now we’ve seen them create better-value products and attract new customers.”

I think that over the course of the next five years, the focus for us and the industry will be entirely on building the business through mergers and acquisitions with our rivals.

Continue to focuson improving current

operations andorganization

Strengthenproductsportfolio

M&APartner withrelevant suppliers, e.g.,

OEMs, electronics/software companies

Invest in technology

57% 56%

67%

37%

7%

37%

57%

33%

80%

19%

FIGURE 9: WHAT ACTIONS HAVE YOU TAKEN IN THE LAST FIVE YEARS TO ADDRESS CHANGING CONDITIONS IN YOUR INDUSTRY? WHICH ACTIONS SHOULD YOU HAVE TAKEN INSTEAD?

3 “Nissan seals $2.3 billion Mitsubishi Motors stake acquisition,” Bloomberg, October 20, 2016.

Actions taken Should have taken

14 / The winning move: Industry consolidation in Asia Pacific

Reeling from various kinds of weaknesses such as massive debt, declining sales, and disruption to their long-standing business models and anticipating strong headwinds ahead, the consumer goods space is consolidating, and mergers within the industry are expected to be a significant theme

of corporate strategies through the next five years (figure 10). Indeed, since 2015, global mergers in the industry have totalled US$784 billion through 3,766 deals, with such combinations among retail companies accounting for 19% of that value and 37% of all deals.

Consumer goods and retailU

S$ (m

illio

ns)

Num

ber of transactions

0

20

40

60

80

100

Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q12015 2016 2017

5663

69

80

72

60

88

72

51 49

25

$0

$3,000

$6,000

$9,000

$12,000

$15,000

FIGURE 11: ASIA PACIFIC CONSUMER GOODS AND RETAIL INDUSTRY M&A

Deal volume Deal value

Next six months Next year Next five years

Performance improvement

Industry consolidation

Industryconsolidation71% 61% 87%

Developing new business models

Developing new business models

Developing new business models 45% 45%45%

Launching new products and services

Launching new products and services Cross-border M&A45% 42%35%

FIGURE 10: TOP THREE MOST-LIKELY CORPORATE ACTIONS TO BE EXECUTED ACROSS TIME FRAMES

15 / The winning move: Industry consolidation in Asia Pacific

FIGURE 12: WHAT ARE THE BIGGEST CHALLENGES FACING YOUR CONSUMER GOODS/RETAIL BUSINESS RELATED TO INDUSTRY TRENDS? (1 = LOWEST, 5 = HIGHEST)

In Asia, the merger trend is even more pronounced. Since 2015, Asian retail consolidation accounted for 40% of deal value and 33% of total deals. However, both consumer goods industry totals and those for the retail space in Asia have been declining in the past 12 to 15 months (figure 11).

Our discussions with executives shed light on that declining deal momentum in the industry. Even though M&A is still being given consideration, short-term goals will focus on enhancing performance (71%) to make operational and financial improvements to remain competitive and in extreme cases, to remain going concerns.

The development of new business models (45%) will also be a priority—especially for Asia’s retailers as they reinvent the ways they engage with and sell to today’s broad base of digitally savvy consumers. Indeed, a large share of respondents mentioned that as digital technology ravages the retail industry, the need to embrace integrated off-line/online strategies and business models will be necessary for survival. Respondents recognized both the importance and the complexity of that task, with 45% saying it will be a priority across the next five years and, likely, beyond.

Such is the importance of updating business models that it stands out as one of three key trends shaping the consumer goods and retail industry in Asia. Two others are the expansion of the value chain and continuous improvements in manufacturing and other internal capabilities.

VA LU E C H A I N E X PA N S I O NThe line between a pure consumer goods company and a pure retailer is blurring. Indeed, many

businesses in this space are moving up and down the value chain, ultimately looking to transform themselves into integrated consumer-retail companies that harness cost savings and achieve other strategic benefits.

A main reason for that shift—and one supported by data from our survey—is the change in demographics among many Asian retailers’ key customers (figure 12). As executives at retail chains across the region pointed out, core consumers are changing to those born after 1980 and 1990. Those in these age-groups are digitally savvy, and they demand different and more-personalized products and services than their parents’ generations did.

Indeed, given the environment these new customers are growing up in—a society of relative abundance compared with the societies of older generations—they’re no longer satisfied with simply having their basic needs met. They want more-personalized approaches with products, and they are, overall, more demanding. This is the most critical challenge involving industry trends that consumer goods companies face in the region, as highlighted in figure 12.

According to respondents, customers today want good-quality products in addition to engaging shopping experiences. For brand owners, the desire to control

16 / The winning move: Industry consolidation in Asia Pacific

both the brand image and the shopping experience is pushing them to operate their own retail outlets. For retailers, the needs to move beyond purely selling goods and to differentiate themselves are spurring experiential shopping.

B U S I N E S S M O D E L E V O LU T I O NFrom an early focus on companies increasing their e-commerce capabilities and changing to online-to-off-line models, the war for customers is no longer between off-line and online but, rather, on old retail versus new retail. That is, the focus is on taking advantage of the Internet with new technologies such as big data, artificial intelligence, and digital payments to revamp and improve the entire retail model, thereby bringing to life a comprehensive online-to-off-line experience via seamless logistics.

The question is: Are Asia’s consumer goods and retail companies making that change?

The data shows that e-commerce is no longer a key industry trend, with many of our survey respondents saying it’s already “here” and ranking it second to last among the biggest challenges their businesses face (figure 12). However, many executives admitted that they continue struggling to establish a strong

FIGURE 13: WHAT ARE THE BIGGEST CHALLENGES FACING YOUR CONSUMER GOODS/RETAIL BUSINESS RELATED TO STRATEGIC OBJECTIVES? (1 = LOWEST, 5 = HIGHEST)

e-commerce platform, ranking it one of the top challenges related to their strategic objectives (figure 13). Elaborating on that data point, the head of finance of a Hong Kong–based consumer goods company said, “Building these online capabilities is a priority for us, but it’s also difficult and expensive.”

Costs definitely come into play in the consideration of an e-commerce strategy, but respondents overwhelmingly agreed that the cost of doing nothing is far greater. Indeed, companies that are not e-commerce ready face the strongest headwinds as they try to catch up with the most forward-thinking companies that are already experimenting with various new retail models.

Two other things driving new business models are (1) branding and (2) attaining customer loyalty, with the latter the third-greatest challenge related to strategy objectives. As the managing director of strategy at a Hong Kong luxury goods company said, the challenges to business today—specifically, building an effective e-commerce platform—stem from rapidly changing consumer tastes and new mobile apps. Competition with the more established brands is another concern, because “these brands have more capital, which they can invest in their online presence and branding.”

Indeed, in today’s hypercompetitive and fast-moving consumer market, branding is key, and executives realize the need to attain customer loyalty to remain relevant. The new retail concept is establishing an edge for those consumer goods and retail vanguards to attract today’s digitally included core consumer—and customers of the future.

17 / The winning move: Industry consolidation in Asia Pacific

I NT E R N A L C A PA B I L IT I E S S T I L L M AT T E RContinuously improving manufacturing, optimizing spending on cost of goods sold, and enhancing supply chain agility are critical levers for remaining competitive as both product cycles and consumer attention spans shorten. As respondents have conceded, reducing procurement costs and improving supply chain are the second- and third-most important profitability levers (figure 14).

According to the director of finance at a Hong Kong–based consumer goods company, reducing internal costs by “dealing with procurement will be difficult, but companies will have to take decisive steps toward dealing with and developing more-efficient procurement systems. Optimizing supply chains and distribution models will also be necessary to reduce expenditures.”

Also trending in this vein, an overwhelming 74% of respondents said they will be investing more in their manufacturing presence in China during the next two to three years. Similarly, 77% will invest more in their sourcing capabilities in China in that same time frame.

From respondent commentary and industry observations, it can be seen that companies with commodity products have to manage costs if they’re going to maintain their competitiveness in the industry.

Evolving channels and prices are exerting pressure on both consumer product firms and retailers alike. And without more-efficient manufacturing, more-capable supply chains, and stronger procurement capabilities, companies will find it harder to keep up with their rivals.

Equally, the customized products that customers are demanding face the challenge of shortened product life cycles. As such, an agile supply chain coupled with strong manufacturing will help companies in Asia respond to product changes more quickly, thereby ultimately meeting market needs and enabling them to thrive rather than simply survive.

4.35

4.32

4.23

4.19

4.06

4.03

4.00

3.87

3.74

Shorten product development lead time

Shift supply base to low-cost countries

Acquire brands/companies

Reduce product complexity

Reduce manufacturing and conversion costs

Optimize pricing and promotion

Improve supply chain and logistics efficiency

Reduce procurement costs

Optimize channel/distributor models

FIGURE 14: WHAT ARE THE KEY INITIATIVES FOR CONSUMER GOODS COMPANIES TO INCREASE PROFITABILITY? (1 = LOWEST, 5 = HIGHEST)

Building these online capabilities is a priority for us, but it's also difficult and expensive.

18 / The winning move: Industry consolidation in Asia Pacific

74%

26%

China

31%

69%

Taiwan

48%48%

3%

Hong Kong

19%

81%

Indian subcontinent

41%

59%South Korea

17%

66%

17%

Japan

77%

23%

China

45%

55%Taiwan

65%

35%

Hong Kong

28%

72%

South Korea

45%55%

Indian subcontinent

24%

66%

10%

Japan

FIGURE 15: HOW MUCH EFFORT WOULD YOU INVEST IN IMPROVING MANUFACTURING IN THE NEXT TWO TO THREE YEARS?

FIGURE 16: HOW MUCH EFFORT WOULD YOU INVEST IN IMPROVING SOURCING IN THE NEXT TWO TO THREE YEARS?

More effort Same effort Less effort

More effort Same effort Less effort

19 / The winning move: Industry consolidation in Asia Pacific

Compared with past years, respondents said they expect in the next 12 months a moderate uptick in the economic outlook regionally and in their primary regions of focus. A significant 80% anticipate a positive outlook in the next 12 months (figure 17). This was a marked shift from last year, when only 24% of respondents were hopeful of positive economic conditions and 29% expected such conditions to decline.

However positive this sentiment, respondents still recognized certain unavoidable challenges and macroevents that are causing and will cause difficulties for their businesses. Uncertainty in the region’s emerging markets (82%) and a slowdown in global trade (77%) were the top two macrotopics considered to have the most significant impact on the region’s current economic and corporate health (figure 18). Likewise, financial reform and regulatory change (71%) were seen as current challenges.

Going forward, changes in consumer demographics and spending power (91%) and competitive pressure (84%) will likely have the deepest impacts. As the

head of corporate development at a Japanese retailer said, “The ways consumers shop have changed and will continue to change as younger consumers transition from general online shopping to using mobile devices to make purchases. Tackling this problem is definitely a priority, but at the same time, we’re faced with challenges from competitors. For corporations in our sector, to increase sales, many must rethink their strategies, develop new sales channels, and make changes in operations through restructuring to stay competitive.”

Economic outlook: Hope on the horizon?

Moderately worseThe sameModerately betterSubstantially better

16%

61% 64%

37%

19%

1%0%2%

FIGURE 17: HOW DO CURRENT ECONOMIC CONDITIONS IN YOUR PRIMARY REGION OF FOCUS COMPARE WITH THOSE FROM 12 MONTHS AGO? WHAT ARE YOUR EXPECTATIONS FOR THOSE CONDITIONS IN 12 MONTHS' TIME?

37%Respondents who said economic conditions have remained largely unchanged and challenging from 12 months ago

Current compared with 12 months ago 12 months from now

20 / The winning move: Industry consolidation in Asia Pacific

C O U NT RY-BY-C O U NT RY E X P E CTAT I O N SAcross the region, respondents said they anticipated that economic conditions will improve the most in Hong Kong (96%), China (80%), and South Korea (80%) (figure 19). Even Japan is likely to see some economic positivity, according to 64% of respondents—a noticeable uptick from last year, when only 16% held that view.

Despite such hopeful outlooks, do signs and moves in the market match these expectations?

China’s economy ended the first half of 2017 on a positive note and worries about a much sharper slowdown are subsiding, but high levels of debt continue to be burdensome. Credit-rating agency

Moody’s downgrade of China in May was yet another reminder of those concerns and pointed out that more time will be needed to bring levels down to manageable ones. Concerning Chinese corporates, People’s Bank of China governor Zhou Xiaochuan said earlier this year that China’s corporate debt level was still too high and announced plans to contain runaway corporate borrowing.4

In Japan, an economic expansion of 1.3% is expected on the heels of a pickup in trade and growth momentum carried forward from 2016, according to the International Monetary Fund. However, the domestic challenges of an aging population and a shrinking workforce mean greater fiscal support may be needed. And like China,

91%

56%

84%

57%

65%

71%

65%

58%

58%

82%

56%

48%

51%

63%

47%

53%

47%

77%

45%51%

Corporate default rates

Slowdown in global trade

US economic outlook

Exchange rate volatility

Political disruptions (future US policies)

Uncertainty in emerging markets

Volatile commodity prices

Financial reform/regulatory changes

Competitive pressure within industry

Changes in consumer demographics and spending power

FIGURE 18: WHICH OF THE FOLLOWING MACROTOPICS IS HAVING THE MOST SIGNIFICANT IMPACT ON OVERALL CONDITIONS AND CORPORATE RESTRUCTURING ACTIVITY IN YOUR PRIMARY REGION OF FOCUS, AND WHICH DO YOU ANTICIPATE TO HAVE SUCH IMPACT IN THE NEXT 12 MONTHS?

Next 12 months Current

4 “China corporate debt levels excessively high, no quick fix: central bank governor,” Reuters, March 9, 2017.

21 / The winning move: Industry consolidation in Asia Pacific

Japan’s current debt load continues to grow as the government focuses on spending to propel the economy out of deflation.5

The Bank of Korea’s annual June assessment of South Korea’s economy pointed to signs of improvement this year, thanks to a boost in the manufacturing space.6 However, at the corporate level, a growing number of zombie companies (those unable to service their debt with income) continue to plague the former Asian tiger’s growth prospects amid commentary from industry insiders and lawmakers that the situation is becoming an “economic powder keg.”7

It seems Hong Kong may be the lone bright spot, with economic growth figures posting a six-year high amid lackluster forecasts, according to official government figures. However, this growth will be increasingly linked with developments on the mainland.

32%

64%

4%

Hong Kong

52%

12%4%

32%Japan

64%

16%20%

South Korea

20%

76%

4%

China

FIGURE 19: WHAT ARE YOUR EXPECTATIONS FOR ECONOMIC CONDITIONS 12 MONTHS FROM NOW IN THE FOLLOWING JURISDICTIONS?

For [retail] corporations, to increase sales, many must rethink their strategies, develop new sales channels, and make changes in operations through restructuring to stay competitive.

Substantially better Moderately better The same Moderately worse

5 “Japan’s economy minister pledges to stick to primary budget fiscal discipline target,” Reuters, August 9, 2017.6 “South Korea economy to see mild improvement this year: central bank,” Reuters, June 25, 2017.7 “S Korea’s zombie companies threaten ‘economic powder keg’,” Financial Times, May 25, 2017.

22 / The winning move: Industry consolidation in Asia Pacific

Conclusion

“The winners in this space are the consolidators.” The space referred to is the global enterprise IT and software industry, and the observation comes from Kevin Loosemore, executive chairman of United Kingdom–based Micro Focus, speaking on trends in the trade his corporation has come to dominate.8 His company’s almost decade-long mission to shore up the enterprise software industry has enabled the company to become the soon-to-be-largest tech company in the United Kingdom.

While a different industry on a different continent, Loosemore’s words hold merit for Asia’s auto and consumer goods executives and business leaders in the broader market, many of them rethinking their existing playbooks as they hope to make winning moves. Is adopting the M&A agenda the right move to make, and can these companies consolidate their way into improved performance and greater profitability?

Indeed, our survey’s Asia executives will face several difficult choices they’ll have to make in 2017 and beyond. As corporate agendas long dominated by distress and restructuring give way to a more promising outlook, those decision makers will have to determine which tools and tactics to use in their hunt for growth. For some, mergers present the best option. For others, an internal assessment followed by quick action to root out inefficiencies and make operational improvements will prevail.

As tectonic shifts shake industries across Asia Pacific and globally, executives will have to take bold steps if they’re to adapt to those changing circumstances, strong competitors, and advancing technologies. Ideally, they’ll make those moves with purpose and haste—and not be outmaneuvered by volatile fault lines as the automotive and retail maps get redrawn.

8 “Micro Focus faces biggest challenge as mammoth HPE deal closes,” Financial Times, August 30, 2017.

23 / The winning move: Industry consolidation in Asia Pacific

Methodology

In May 2017, Acuris Studios, the publishing division of Acuris Global, surveyed 100 corporations, bankers, lawyers, and fund managers across Asia Pacific to gain insights into the current market for restructuring and industry consolidation. The 100 consisted of 60 respondents from corporations; 15 from major corporate and commercial banks; 15 from sovereign wealth funds, central banks, regulatory bodies, or research groups; 5 from law firms; and 5 from private-equity/hedge funds.

Survey results and figures on graphs may not sum to 100% due to rounding or where respondents were allowed to choose more than one answer.

All $ symbols refer to US dollars unless otherwise stated.

All data quoted is proprietary Acuris Global or AlixPartners data unless otherwise stated.

50% 50%

60%15%

5%

15%

5%

25%

25%25%

25%

CORPORATE RESPONDENT MAIN INDUSTRYRESPONDENT BASE

RESPONDENT PROFESSIONAL PRACTICE/ORGANIZATION

China Hong Kong Japan South Korea Automotive Consumer goods and retailers' own brands

Corporation Government (Sovereign wealth fund, central bank, regulatory body,

research group) Law firm Major corporate and commercial bank Private-equity/Hedge fund

24 / The winning move: Industry consolidation in Asia Pacific

Acuris Studios, the events and publications arm of Acuris Global, offers a range of publishing, research and events services that enable clients to enhance their own profile, and to develop new business opportunities with their target audience.

To find out more, please visit www.acuris.com

Please contact: Pearlie Sham Business Development Manager, Acuris Studios Tel: +852 2158 9788

Mergermarket is an unparalleled, independent mergers & acquisitions (M&A) proprietary intelligence tool. Unlike any other service of its kind, Mergermarket provides a complete overview of the M&A market by offering both a forward-looking intelligence database and a historical deals database, achieving real revenues for Mergermarket clients.

About Mergermarket

25 / The winning move: Industry consolidation in Asia Pacific

F O R M O R E I N F O R M AT I O N, C O NTA CT:

Masahiko Fukasawa Managing Director, Co-head of Asia Business Unit & Co-Japan Representative [email protected] +81 3 5533 4850

Tom Noda Managing Director [email protected] +81 3 5533 4883

Lian Hoon Lim Managing Director [email protected] +852 2236 3525

Michael McCool Managing Director [email protected] +852 2236 3568

George Geh Managing Director [email protected] +86 21 6171 7598

Yung Chung Managing Director & Korea Representative [email protected] +82 2 2160 1806

In today’s fast paced global market timing is everything. You want to protect, grow or transform your business. To meet these challenges we offer clients small teams of highly qualified experts with profound sector and operational insight.

Our clients include corporate boards and management, law firms, investment banks, investors and others who appreciate the candor, dedication, and transformative expertise of our teams. We will ensure insight drives action at that exact moment that is critical for success. When it really matters. alixpartners.com

About AlixPartners

26 / The winning move: Industry consolidation in Asia Pacific

NOTES:

The opinions expressed are those of the author and do not necessarily reflect the views of AlixPartners, LLP, its affiliates, or any of its or their respective professionals or clients. This article (“Article”) was prepared by AlixPartners, LLP (“AlixPartners”) for general information and distribution on a strictly confidential and non-reliance basis. No one in possession of this Article may rely on any portion of this Article. This Article may be based, in whole or in part, on projections or forecasts of future events. A forecast, by its nature, is speculative and includes estimates and assumptions which may prove to be wrong. Actual results may, and frequently do, differ from those projected or forecast. The information in this Article reflects conditions and our views as of this date, all of which are subject to change. We undertake no obligation to update or provide any revisions to the Article. This article is the property of AlixPartners, and neither the article nor any of its contents may be copied, used, or distributed to any third party without the prior written consent of AlixPartners.