november 2015 examination

TRANSCRIPT

November 2015 Examination

PAPER 5

Inheritance Tax, Trusts & Estates

Part I Suggested Solutions

2

1. Lifetime IHT due: £ Gift 700,000 Nil rate band (325,000) (1/2)

375,000

Tax payable 20/80 £93,750 (1)

Additional IHT due on death: £ Gift 700,000 Tax paid 93,750

Gross chargeable transfer 793,750 (1) Nil rate band (325,000) (1/2)

468,750

Tax payable @ 40% 187,500 (1/2) Lifetime tax paid (93,750) (1/2)

Tax payable 93,750

(4) 2. £ Initial value 485,000 Nil rate band (325,000) (1/2)

160,000

Notional IHT @ 20% 32,000 (1/2)

Effective rate 32,000/485,000 x 100% 6.598% (1/2)

Complete quarters for period 18th birthday to exit

Ie 10 May 2011 to 10 May 2014 =

12 quarters

(1/2)

Actual rate of tax 6.598% x 30% x 12/40 0.594% (1/2)

IHT payable 0.594% x £200,000

1,188 (1/2)

No inheritance tax is payable if capital is paid from an age 18-to-25 trust to a beneficiary on or before attaining the age of 18 (1/2). The liability calculated above would therefore not be payable if the trust fund were paid to Bella when she attained age 18. (1/2) (4) NB Rates of tax to 3 decimal places. Credit given for other rounding. 3. 1) The gift is made as part of the donor’s normal expenditure, (1/2) i.e. the donor establishes

a regular (i.e. at least annual) pattern of giving (1/2). Taking one year with another (1/2), it is made out of the donor’s surplus income. (1/2) The gift leaves the donor with sufficient income to maintain his usual standard of living. (1/2) without the need to spend any of his capital. (1/2)

2) Gifts between individuals are normally treated as PETs. However, where gifts meet the

conditions for normal expenditure out of income, the gifts are immediately exempt from inheritance tax. (1)

(4)

3

4. The trustees are deemed to sell and immediately reacquire the assets for their market value (1/2) thus triggering a capital gains tax event. (1/2) As a qualifying interest in possession trust, holdover relief under s.260 TCGA 1992 is not available (1/2) and therefore holdover relief under s.165 TCGA 1992 (1/2) is only available for qualifying business assets (1/2). The trustees are liable to capital gains tax at 28% (1/2) on any gains in excess of the annual exemption, which is £5,500 for the 2014/15 tax year. (1/2) The annual exemption is shared with any other trusts created by the same settlor, with a minimum available of £1,100. (1/2) If the asset is worth less than when it was originally settled/acquired by the trustees, a capital loss will arise (1/2). This loss must be set against gains arising to the trustees between 6 April and the date of appointment. (1/2) Any excess losses on the asset transferred may be passed to the beneficiary (1/2) but the loss can only be offset against future gains arising on the same asset. (1/2)

(max 4) 5. The transfer of value for a life policy is the greater of premiums paid (3 x £10,000 pa = £30,000) (1/2) and the open market value of the life policy (£25,000) (1/2) £ Value of gift (taking higher value) 30,000 (1/2) AEs – already used nil (1/2 if state AEs already used)

30,000 (2) 6. £ Capital value 427,000 (1/2) Deemed accumulation 2010 21,000 (1/2) Deemed accumulation 2009 18,000 (1/2)

466,000 Nil rate band (325,000) (1/2)

141,000

Tax @ 20% 28,200 (1/2) Effective rate 28,200/466,000 x 100 6.052% (1/2) Actual rate 6.052% x 30% 1.816% (1/2) Tax due 1.816% x £466,000 £8,463 (1/2)

NB Rates of tax to 3 decimal places. Credit given for other rounding. (4) 7. 25 December 2013 - Covered by small gift exemptions so nil

transfer of value (1/2)

5 April 2014 - Covered by charity exemption so nil transfer of value

(1/2)

10 May 2014 - Covered by 2014/15 annual exemption so nil transfer of value

(1/2)

8 August 2014 £10,000 (£5,000) Marriage exemption (1/2) (£2,000) 2014/15 annual exemption (1/2) (£3,000) 2013/14 annual exemption (1/2)

Nil so nil transfer of value (3)

4

8. £ £ Gift of cash Nil Not a chargeable asset (1/2) Gift of cars Nil Cars suitable for private

use are exempt from capital gains tax

(1/2)

Gift of property Market value 320,000 Less Original cost (260,000) (1/2) Less Auction costs (9,300) }(1/2 if both) Less Improvements (27,000) }

(296,300)

23,700 Less Annual exemption (11,000) (1/2)

12,700

Tax due @ 28% 3,556 (1/2)

(3) 9. £ Gross chargeable transfer 494,000 Fall in value (£466,200 – £450,000) (16,200) (1/2)

477,800 Nil rate band (325,000) (1/2)

152,800

Tax @ 40% 61,120 (1/2) Lifetime tax paid (33,800) (1/2)

27,320 (2) Note The original value of the shares to the donee was £494,000 + £6,000 (annual exemptions) - £33,800 (tax paid by donee) = £466,200. However, candidates were given full credit for identifying that fall in value relief was applicable and making a reasonable attempt at the calculation. 10. £ Bank interest £440 x 100/80 550 (1/2)

Tax @ 20% on £200* 40 (1/2) Tax @ 45% on balance (£350) 158 (1/2)

198 Less tax deducted at source (110) (1/2) Income tax payable by Trustees 88

*Basic rate band limited to greater of £1,000/10 = £100 or minimum amount of £200. (1) NB The inheritance tax liability is not deductible from income, as it is only payable in relation to trust capital (1/2 for omitting from calculation) The due date for an electronic trust return is 31 January 2016. (1/2)

(4)

5

11. £ £ Interest 324 Dividends (£1,678 x 100/90) 1,864 Rents 6,000

6,324 1,864

Tax @ 20% 1,265 Tax @ 10% 186 Tax @ source (186)

Tax payable by Executors

1,265 Nil (1)

Rents 6,000 Interest 324 Dividends 1,864 Tax deducted (1,200) (65) (186)

4,800 259 1,678 Distribution (4,800) (200) NIL (1)

Carry forward

Nil 59 1,678

R185 £ Net £ Tax Rents (Non savings) 4,800 1,200 (1) Interest (Savings) 200 50 (1)

5,000 1,250 (4) 12. Trust management expenses are taken into account in calculating how much of the discretionary trust’s income is chargeable at the rate applicable to trusts (1/2), as the income used to pay these expenses is only taxed at the basic rate or dividend rate (1/2). In the income tax computation, trustees’ expenses are grossed up (1/2) before deducting them from income which has been grossed up (1/2) at the rate appropriate to the source of the income. (1/2) The order of the income for the deduction of these expenses is important. Dividend income is used to pay trust management expenses before savings income and then non savings income (1/2). (max 2)

November 2015 Examination

PAPER 5

Inheritance Tax, Trusts & Estates

Part II Suggested Solutions

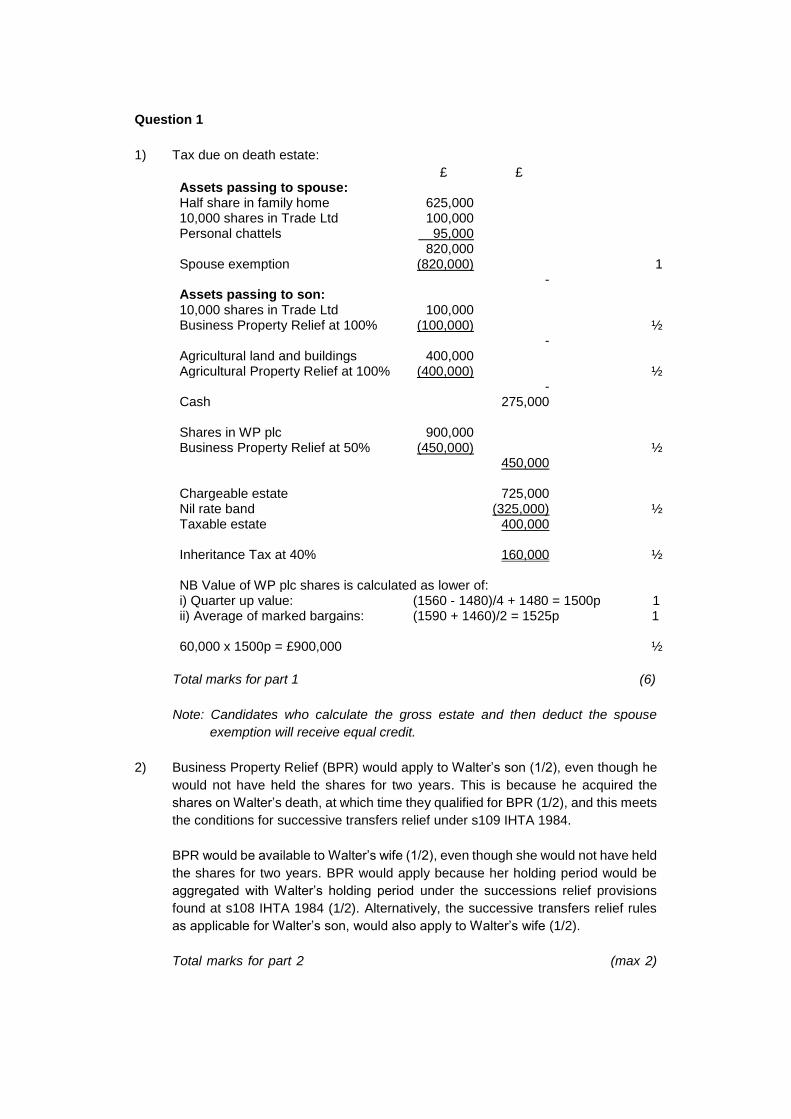

Question 1

1) Tax due on death estate:

£ £ Assets passing to spouse: Half share in family home 625,000 10,000 shares in Trade Ltd 100,000 Personal chattels 95,000 820,000 Spouse exemption (820,000) 1 - Assets passing to son: 10,000 shares in Trade Ltd 100,000 Business Property Relief at 100% (100,000) ½ - Agricultural land and buildings 400,000 Agricultural Property Relief at 100% (400,000) ½ - Cash 275,000 Shares in WP plc 900,000 Business Property Relief at 50% (450,000) ½ 450,000 Chargeable estate 725,000 Nil rate band (325,000) ½ Taxable estate 400,000 Inheritance Tax at 40% 160,000 ½ NB Value of WP plc shares is calculated as lower of: i) Quarter up value: (1560 - 1480)/4 + 1480 = 1500p 1 ii) Average of marked bargains: (1590 + 1460)/2 = 1525p 1 60,000 x 1500p = £900,000 ½

Total marks for part 1 (6)

Note: Candidates who calculate the gross estate and then deduct the spouse

exemption will receive equal credit.

2) Business Property Relief (BPR) would apply to Walter’s son (1/2), even though he

would not have held the shares for two years. This is because he acquired the

shares on Walter’s death, at which time they qualified for BPR (1/2), and this meets

the conditions for successive transfers relief under s109 IHTA 1984.

BPR would be available to Walter’s wife (1/2), even though she would not have held

the shares for two years. BPR would apply because her holding period would be

aggregated with Walter’s holding period under the successions relief provisions

found at s108 IHTA 1984 (1/2). Alternatively, the successive transfers relief rules

as applicable for Walter’s son, would also apply to Walter’s wife (1/2).

Total marks for part 2 (max 2)

3) Agricultural Property Relief (APR) is available at the rate of 50% where the

agricultural land is let to a third party (e.g. a farmer) (1/2) who uses it for agricultural

purposes (1/2) and the letting agreement/lease was signed before 1 September

1995 (1). In addition, at the time of the transfer, the landowner cannot obtain vacant

possession within two years (1/2).

Total marks for part 3 (max 2)

4) BPR will be denied on the original transfer if:

the donee has disposed of the property received from the transferor before the

transferor’s death (1).

the donee sold the original property and none or only part of the sale proceeds

from the disposal are invested in a new qualifying property (1).

the property received no longer qualifies for BPR on the transferor’s death. (1).

the property transferred was unquoted shares and the company becomes

quoted before the transferor’s death (1).

Any three of the above.

Total marks for part 4 (max 3)

5) A withdrawal of APR or BPR will only affect the Inheritance Tax payable at the time

of the transferor’s death (1/2). The withdrawn relief is added back to the gross

chargeable transfer and the death tax is then calculated in the usual way (1/2), with

a deduction for the lifetime tax paid (1/2).

The settlor’s cumulative total is not adjusted and remains as it was after the original

transfer with the deduction for APR or BPR (1/2). There is also no effect on any

lifetime tax which has already been paid (1/2)

Total marks for part 5 (max 2)

NB In sections 2 to 5, credit will be given for any other valid points.

Total (15)

Question 2

Memorandum

To: Tax Partner

From: A Student

Date: 1 November 2015

Subject: Mr & Mrs Sutton

Format mark (1)

1) Mrs Sutton’s domicile position

Mrs Sutton is currently only liable to UK IHT on her UK situs assets (1/2). If she

made an election to be domiciled in the UK for IHT purposes, she would become

liable to UK IHT on her worldwide assets (1/2).

While Mrs Sutton remains non-UK domiciled, the spouse exemption available for

transfers from Mr Sutton to Mrs Sutton is restricted to the value of the nil rate band,

currently £325,000 (1/2). There is no limit to the spouse exemption available on gifts

from Mrs Sutton to Mr Sutton (1/2).

Lifetime gifts utilise this exemption first and gifts in excess of the restricted spouse

exemption will be treated as PETs (1/2). On Mr Sutton’s death, the unused restricted

spouse exemption (if any) will be available for assets passing from Mr Sutton to Mrs

Sutton (1/2).

Should Mrs Sutton elect to be domiciled in the UK the couple would benefit from a

full unrestricted spouse exemption to be used against lifetime and death transfers

from Mr Sutton to Mrs Sutton (1/2).

Total marks for part 1 (including presentation mark) (max 3)

2) Income Tax payable by the Rillington Trust for 2014/15

NS S D £ £ £ Rental income 28,000 Less: Boiler repair cost (500) ½ 27,500 Bank interest: £12,800 x 100/80 16,000 ½ Dividends: £3,600 x 100/90 4,000 ½ Total income 27,500 16,000 4,000 TMEs: £2,700 x 100/90 --------- --------- (3,000) 1 Income after expenses 27,500 16,000 1,000 Tax payable: Standard rate: £1,000 at 20% 200 ½ (£27,500 - £1,000) + £16,000 at 45% 19,125 ½ £1,000 at 37.5% 375 ½ £3,000 at 10% 300 ½ 20,000

Less tax credits: Bank interest (3,200) ½ Dividends (400) for

both Total tax payable by trustees 16,400

Total marks for part 2 (5)

3) The Rillington Trust’s estimated 2015/16 Income Tax liability

£ Split of income: Discretionary income: £30,000 x 3/4 22,500 ½ Interest in possession income: £30,000 x 1/4 7,500 For both Discretionary part of fund: Tax payable: Standard rate: £1,000 at 20% 200 ½ (£22,500 - £1,000) at 45% 9,675 ½ 9,875 Life interest part of fund: Tax payable: £7,500 x 20% 1,500 ½ Total tax liability of the trustees 11,375

Total marks for part 3 (2)

4) Complete constitution of a trust

A trust becomes completely constituted when the legal title to the trust

property is vested in the trustees (1).

A settlor may completely constitute a trust in one of two ways:

Transfer of the trust property by the settlor to the trustees in the manner

required by law, so that the trustees legally hold the property. (1)

The settlor declares that he himself is to hold the property on trust for the

beneficiaries. (1)

Total marks for part 4 (3)

5) Covering letter for engagement letter

It is recommended that the covering letter for an engagement letter should

Include the following sections:

Who the firm is acting for (1/2)

Period of engagement (1/2)

Scope of services (1/2)

Fees (1/2)

Limitation of liability (1/2)

Agreement of letter (1/2)

Total marks for part 5 (max 2)

NB In sections 1 and 5, credit will be given for any other valid points.

Total (15)

Question 3

1) 2013/14 Capital Gains Tax computation:

£ £ Antique vase: Disposal proceeds 7,500 Cost (3,500) ½ Gain 4,000 Gain using chattels rule: 5/3 x (£7,500 - £6,000) 2,500 1 Take lower of two: 2,500 ½ Shares in Gadgetron Ltd: Disposal proceeds 35,000 Cost: 10,000/70,000 x 175,000 (25,000) 1 10,000 Total chargeable gains in year 12,500 Annual exemption: £5,500 / 3 (1,833) ½ Taxable gain 10,667 CGT @ 28% 2,987 ½

Total marks for part 1 (4)

2) Exit charge on 5 September 2014:

£ Amount on which exit charge is due (ie loss to trust basis): £40,000 + (£100,000 - £80,000) £60,000 1 Tax rate: Initial value of relevant property in trust 700,000 Nil rate band at date of exit (325,000) ½ 375,000 Notional IHT at 20% 75,000 ½

Effective rate of tax: £75,000 / £700,000 10.714% ½ Actual rate of tax: 10.714% x 30% x 14/40* 1.125% ½ IHT payable: £60,000 x 1.125% 675 ½ * 14 complete quarters 1 March 2011 to 5 September 2014 ½

Total marks for part 2 (4)

3) The trustees must make a disposal which is a chargeable event for Inheritance Tax,

(1/2) although it is not necessary for any Inheritance Tax to be payable (1/2).

In order to obtain holdover relief, a claim must be made and submitted to HM

Revenue & Customs (1/2), which is usually submitted with the trust’s tax return.

(1/2). For trustees to claim holdover relief, a joint claim must be made by the

trustees and the recipient of the asset (1/2).

(max 2)

The time limit for making a claim is four years from the end of the tax year of

disposal. (1)

Total marks for part 4 (max 3)

4) Gain heldover on transfer of 123 plc shares:

£ Sale proceeds (deemed to be MV): 10,000 x £10 100,000 ½ Cost: £280,000 x 10,000/40,000 (70,000) 1 Gain 30,000 Less gain immediately chargeable: Actual profit made on disposal (£80,000 - £70,000) (10,000) 1 Capital gain eligible for holdover (s260 TCGA) 20,000 ½

Total marks for part 3 (3)

5) When deciding whether to accept a new client, a member must consider whether

the member and firm will have the skills and competence to service the client’s

requirements during the course of the engagement. (1)

A member must carry out his professional work with a proper regard for the technical

and professional standards expected (1).

A member must not undertake professional work which the member is not

competent to perform, whether because of lack of experience or the necessary

technical or other skills (1), unless appropriate advice or assistance is obtained to

ensure that the work is properly completed (1/2).

A member who does not have the expertise or the staff resources available to

meet his client’s needs should refer the client to another professional adviser (1).

A member should take care when making referrals and should aim to give the client

a choice of adviser (1).

A member should make it clear to his client that the member has no responsibility

for the work undertaken by the other professional adviser (1).

Total marks for part 5 (max 4)

NB In sections 3 and 5, credit will be given for any other valid points.

Total (18)

Question 4

1) For a will to be valid:

It must be in writing (1/2)

It must be signed by the testator (1/2)

The testator’s signature must be witnessed by two persons who are

present together when the testator signs the will (1/2). The witnesses must then

each sign the will in the presence of the testator and of each other (1/2)

The testator must be sui juris (over 18 and have mental capacity) (1/2)

The testator must intend the will to be operative as a testamentary disposition

(1/2)

The will should be dated (1/2)

Scottish alternative

For a will to be valid:

It must be in writing (1/2)

It must be subscribed by the testator (1/2)

It must be signed at the end (1/2)

However, if it is witnessed by one witness and if it extends over more than one

sheet, each sheet is signed by the testator, the will is also presumed to be

validly signed (1)

The testator must comprehend the nature of the testamentary act. (1/2)

The testator must be at least 12 years old (1/2)

Total marks for part 1 (max 3)

2) Any four of the following typical clauses which can be found in a will:

Revocation of all former wills and codicils (1)

Details regarding burial or cremation and anatomical use of organs (1)

Appointment of executors and trustees (1)

Appointment of guardians of minor children (1)

Specific gifts of personal property (1)

Specific gifts of freehold or leasehold properties (1)

Gifts of shares (1)

Pecuniary (cash) legacies (1)

Gift of the residue (1)

Whether legacies are subject to IHT or free of IHT (1)

Total marks for part 2 (max 4)

3) Any two of the following ways in which a will can be revoked:

By executing a later will which impliedly revokes an earlier will (i.e. where the

later will is inconsistent with terms of the earlier will) (1)

By executing a later will which includes an express revocation (1) of all former

wills

By marriage or forming a civil partnership (1/2) unless the will is in

contemplation of marriage/civil partnership with a particular person (1/2)

By destruction (1/2) if the testator intends his will to be revoked (1/2)

By a letter signed by the testator and witnessed by two persons. (1)

Scottish alternative

Ways in which a will can be revoked:

If a testator expressly revokes an earlier will in a later will (1)

If a testator makes provisions in a later will which are inconsistent with the

earlier will (1)

Under common law there is a rebuttable presumption that an earlier will is

revoked by the birth of subsequent children where the testator has made no

provision for these children (1). A child must challenge the will for this

assumption to be made (1/2).

Total marks for part 3 (max 2)

4) An IIP trust created under the terms of a will is known as an immediate post death

interest (IPDI) (1/2), and it will be a “qualifying interest in possession” (QIIP) (1/2),

which means the trust fund is treated as forming part of the estate of the life tenant

(1/2) and so it will be liable to IHT on the death of the life tenant (1/2).

The IHT treatment for the testator will therefore depend on the identity of the life

tenant. Where the life tenant is the spouse or civil partner of the testator, the assets

to be transferred to the trust are exempt (1/2). Where the life tenant is any other

individual, the assets are chargeable to IHT (1/2).

There are no exit charges (1/2) or principal charges (1/2) on assets subject to a

QIIP during the lifetime of the trust.

Total marks for part 4 (max 3)

NB Throughout the question, credit will be given for any other valid points.

Total (12)