november 2011 - london stock · pdf filerbs “global growth ... 6,000 8,000 10,000 12,000...

TRANSCRIPT

1

The UK Retail Bond Market

November 2011

2

A. Introduction

3

The World today…. An increasing problem on raising debt

“Global growth fears sink world stocks”

“European banks under pressure as corporate

bond markets dry up”

“Europe’s debt problems hit markets”

“Difficulty in refinancing diminishes low rates

appeal”

0

10

20

30

40

50

2009 2010 2011

£ bn

Volume GBP Issuance

Q1

Q2

Q3

Q4

0

200

400

600

800

1000

1200

1400

Bps

Sovereign 5 Yr CDS

Spain

France

Germany

Ireland

Italy

United Kingdom

0

50

100

150

200

250

300

350

400

450

Bps

Bank 5 Yr CDS

Lloyds

Santander

Barclays

RBS

4

“Our investors want household

names like John Lewis or

Nationwide”

“We have seen overwhelming

demand by retail investors”

“Retail bonds are performing

strongly in the secondary market”

“Investors finally have the

opportunity to lock in a secured

income with upside potential”

Source: Evolution Securities survey of retail stockbrokers

“Thanks to the Tesco Bank retail

bond we have won 91 new

clients and taken another £1m

under management”

Retail Bond Market – a new source of borrowing

► September 2011 - National

Grid became the first ever

company to launch an

inflation-linked retail bond

► February 2011 - Tesco Bank

first ever corporate to launch

a retail bond

►March 2011 - Provident

Financial second retail bond

– doubles amount raised

► June 2011 - Places for

People first Housing

Association to launch a retail

bond

5

B. The Retail Opportunity

6

A Seismic Shift in Savings post 2008

► Retail investors are looking for new ways to save

Impact of low deposit rates

Diversification away from the banks

Need for greater yield

Protection against inflation

Shift from equity to debt

UK Retail Savings Market

Retail Investment £’bn Source

NS&I 99 NS&I 2011

Term Deposits* 275 BoE April 2011

Bond Funds 107 IMA 2011

Stock ISAs 178 ONS Jan 2011

Cash ISAs 172 ONS Jan 2011

SIPPs 90 (e) Pension

Management

* £92bn worth fixed rate deposits accounts are

maturing in 2011, HSBC Research

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Re

tail

sale

s in

to b

on

d f

un

ds

(GB

P M

illio

ns)

FTSE

10

0 In

de

x

Retail sales into bond funds FTSE 100 Index

ISA Sales 2010-11

Retail £’bn

Cash ISA 32

Stocks ISA 13

TOTAL ISA 45

► Impacted by rising marginal rates of tax

Increased use of tax efficient vehicles –

SIPPs and ISAs

Shift towards high yielding products in SIPPs

and ISAs

► While Bond Funds have gained from this move

Many investors are looking for direct investment in

Bonds, often for the first time

• Certainty of income

• Capital repaid at par on maturity

► London Stock Exchange responded to this move

with the ORB

Increased profile for retail bonds

Improved access for retail investors

Transparent pricing in the secondary market

7

An exciting new opportunity for Borrowers

► A new market for debt, providing

Diversification

• A new group of investors

• A different attitude to credit

• A different view of value

Greater flexibility on size

• New Issues for £25m plus

Predictability

• Steady demand

• Impact of market movements limited

• Preference for frequent issuance

Price

• Price savings for the right borrower

• Strong wish for named Corporates

• No requirement for ratings

Brand enhancement

• Increased profile for the business

• Opportunities for retail “cross-selling”

Retail Bond Distribution

A B C D

Distributors 57 47 47 82

Underlying

Clients 7,000 5,000 6,500 12,000

Average

Ticket £13,000 £10,000 £21,000 £21,000

% ISAs/SIPPs 55% 50% 57% 53%

Source: Evolution Securities

Key Stats and Guestimates from Recent Deals

£125m

5.2% 7 ½ years

Senior Retail Bond

Joint Bookrunner & Distributor

£50m

7.5% 5 ½ years

Senior Bond

Sole Bookrunner & Distributor

£140m

5% 5 ½ years

Senior Unsecured Bond

Sole Bookrunner & Distributor

£260m

1.25% 10 years

Inflation-linked

Joint Bookrunner & Distributor

This has created a unique opportunity for borrowers

8

In a sector where demand currently far outstrips supply

Shortage of eligible issues in the secondary market

Generally well above par

Only 8 major new transactions to date

Usually heavily over-subscribed

All bar one trading at a substantial premium to par

Secondary Trading Performance

0

20

40

60

80

100

Gilts Corps Supras

Number of Issues on ORB

Aug-10 Aug-11

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

Aug-10 Aug-11

£

ORB Corporate TurnoverRetail Bonds

Borrower Maturity Issue

Size £'m Coupon

% Rating

Market Price

Yield

National Grid 2021 282.5 1.25 RPI Baa1 101.5 1.22%

Places for People 2016 140 5.00 Aa3 104.7 3.92%

Tesco Bank 2018 125 5.20 None 106.8 3.99%

Lloyds 2015 75 5.38 A+ 100.0 4.85%

Lloyds 2016 150 5.50 A+ 100.8 5.32%

Provident Financial 2020 25 7.00 None 101.0 6.68%

Provident Financial 2016 50 7.50 None 107.0 5.77%

EIB 2016 350 3.25 AAA 105.8 1.98%

RBS 2018 15 3.30-

8.55 None 95.1 6.33%

9

C. Retail Demand in Sterling

10 10

► Retail demand has always accounted for between 10-15%

of the secondary market for Sterling Bonds

► Traditionally it has been dominated by:

Ultra High Net Worth individuals and family offices.

• Located offshore in the Channel Islands and Switzerland, as

well as the UK, and

• Serviced by the Private Banks and the UHNW Wealth

Managers, with

• Typical investments of between £100k-£2.5m

► Over the last two years they have been joined by an increasing group of:

Traditional bank depositors and smaller individual investors

• Located Onshore

• Serviced by the retail stockbrokers and wealth managers

• Often buying for ISAs and SIPPs

• With typical ticket sizes of GBP £5k-£30k

11

Distributor Total Asset under Manament £ (bn)

Number of UK offices Number of advisors

in UK

Brewin 24.8 41 630

Rathbones 14.6 11 170

Investec 12.6 11 206

Charles St 10.1 33 500

Collins Stewart 7.9 1 37

Wdb

6.1 7 100

Redmayne 2.9 37 119

Killik 2.6 10 67

These investors are accessed by a wide range of Distributors, such as

TOTAL 81.6 151 1,829 Source: Money Guide, Private Client

Wealth Management, FT 18 June 2011

12

D. The UK Retail Bond Market

13

Development of the Market in 2011

► UK Retail Bond market currently consists of

Debt issues with minimum denominations of £100/£1000

Tradable through the ORB

► In 2011, there has been 9 New Issues for over £750m. This compares with 3 New Issues for £100

million in 2010

► In addition there have been a number of unlisted issues totalling £75 million for borrowers like John

Lewis.

Announced 2011

Borrower Maturity Issue Size £'m Coupon % Bond Rating

Places for People 2016 140 5.00 AA-

Tesco Bank 2018 125 5.20 None

Lloyds 2016 150 5.50 A+

Provident Financial 2016 50 7.50 None

EIB 2016 350 3.25 AAA

RBS 2018 15 3.30-8.55 None

RBS 2017 10 2.00 (FRN) None

National Grid 2021 282.5 1.25 RPI Linked BBB+

RBS 2018 20 2% fixed coupon None

14

► All of the New Issues met or substantially exceeded borrowers initial objectives on size

Borrower MaturityIssue Size

£'m

Coupon

%Rating

Market

PriceYield

Spread to

Mid Swap

Spread to

Wholesale

National Grid 2021 282.5 1.25 RPI Baa1 101.5 1.16% N/A 29

Places for People 2016 140 5.00 Aa3 104.7 3.87% 203 20

Tesco Bank 2018 125 5.20 None 106.8 3.93% 181 N/A

Lloyds 2015 75 5.38 A+ 100.9 4.53% 289 -39

Lloyds 2016 150 5.50 A+ 100.0 5.15% 335 7

Provident Financial 2020 25 7.00 None 101.0 6.53% 415 -253

Provident Financial 2016 50 7.50 None 107.0 5.71% 391 -277

EIB 2016 350 3.25 AAA 105.8 1.98% 14 N/A

RBS 2018 15 3.30-8.55 None 95.1 6.19% 421 N/A

Retail Bonds

► All have subsequently traded at a significant premium to their issue price

► All have outperformed their equivalents in the Wholesale Market

Development of the Market in 2011

100

101

102

103

104

105

106

107

108

109

21

-Fe

b

07

-Mar

21

-Mar

04

-Ap

r

18

-Ap

r

02

-May

16

-May

30

-May

13

-Ju

n

27

-Ju

n

11

-Ju

l

25

-Ju

l

08

-Au

g

22

-Au

g

05

-Se

p

19

-Se

p

03

-Oct

17

-Oct

31

-Oct

Tesco Bank 5.2% 2018

100

101

102

103

104

105

106

107

108

109

25

-Mar

08

-Ap

r

22

-Ap

r

06

-May

20

-May

03

-Ju

n

17

-Ju

n

01

-Ju

l

15

-Ju

l

29

-Ju

l

12

-Au

g

26

-Au

g

09

-Se

p

23

-Se

p

07

-Oct

21

-Oct

04

-No

v

Provident Financial 7.5% 20162011 UK Retail Bond League Table

Bank Underwriting Volume £’m

# of deals

Evolution Securities 388 5

Barclays 193 2

Lloyds 75 1

RBC 75 1

RBS 25 2

15

E. Accessing Retail Bond Investors

16

Accessing the Market

► New Issues in the Sterling Bond Market have traditionally been designed for efficient distribution to a small group of

Wholesale investors

Extensive pre-sounding but only with a limited group of buyers

Restricted road show

Short formal sales process, generally 2/4 hours

Indicated terms during the sales period

No protection on orders

Price fixed/Stock only allocated after the close of the sales period

► Retail Distributors/Wealth Managers have generally struggled to gain access to Bonds in the New Issue Market

► In any case the process is ill suited to the needs of the Retail Market

Fixed Price

Certainty on allocation

Time required to communicate with investment advisors/end clients

Broad dissemination of information on the borrower/the transaction

► Evolution has developed a mechanism designed specifically to empower the Retail Distributors in the

Issue and provide time for retail Investors to buy

17

► There are 50-80 individual Distributors/ Wealth Managers involved in any new issue

► They are drawn from 4 distinct groups of operators

17

Execution Only Broker

Execution Only Accounts

10-15% of demand

Stockbroker

Discretionary, Advisory and

Execution Only Accounts

50% of demand

Wealth Manager

Discretionary and Advisory

Accounts

20 -30% of demand

Private Banks

Discretionary, Advisory Accounts

15-20% of demand

Accessing the Market

18

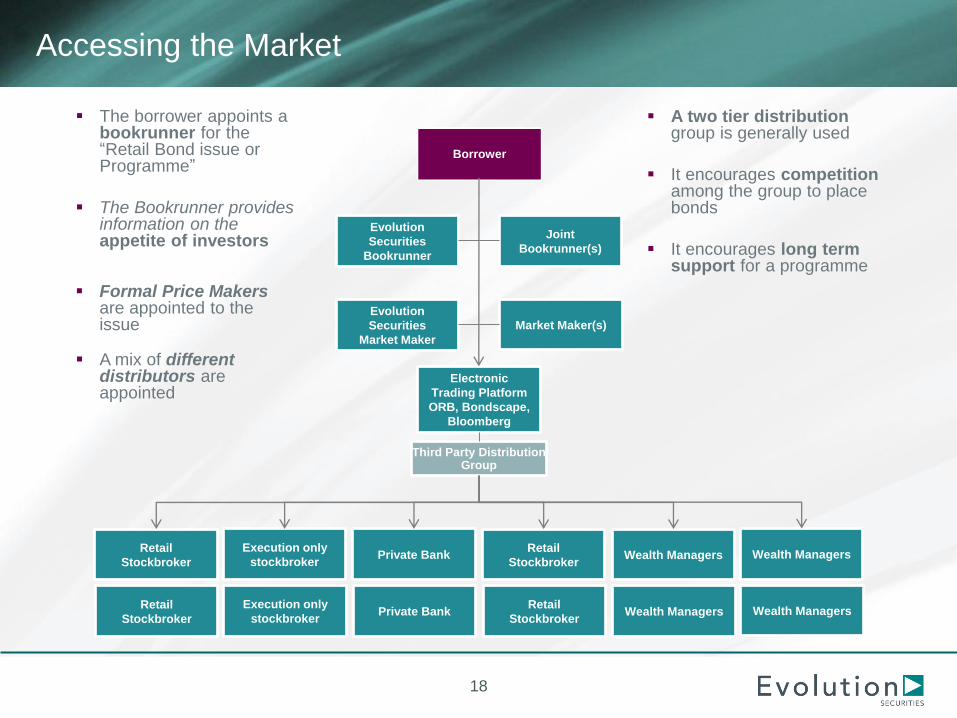

Borrower

Joint

Bookrunner(s)

Evolution

Securities

Bookrunner

Market Maker(s)

Evolution

Securities

Market Maker

Wealth Managers Wealth Managers Retail

Stockbroker

Third Party Distribution Group

Electronic

Trading Platform

ORB, Bondscape,

Bloomberg

Execution only

stockbroker Private Bank

Retail

Stockbroker

The borrower appoints a bookrunner for the “Retail Bond issue or Programme”

The Bookrunner provides information on the appetite of investors

A two tier distribution group is generally used

It encourages competition among the group to place bonds

It encourages long term support for a programme

Wealth Managers Wealth Managers Retail

Stockbroker

Execution only

stockbroker Private Bank

Retail

Stockbroker

Formal Price Makers are appointed to the issue

A mix of different distributors are appointed

Accessing the Market

19

LSE Globe Event – welcoming new Retail Bond listing

20

Evolution Retail Bond Team

► Dedicated to the development of a transparent and orderly retail market

► Committed to connecting sources of capital to companies looking for diversification

► Experienced investment and sub-investment grade bond specialists focused on advice and

origination for large and mid size corporates, housing associations, local authorities and SSAs

21

Credentials

£125m

5.2% 7 ½ years

Senior Retail Bond

Joint Bookrunner & Distributor 2011

£350m

3.25% 5 ¾ years

Senior Bond

Co-Lead Manager 2011

£140m

5% 5 ½ years

Senior Unsecured Bond

Sole Bookrunner & Distributor 2011

£50m

7.5% 5 ½ years

Senior Bond

Sole Bookrunner & Distributor 2011

£260m

1.25% 10 years

Inflation-linked Retail Bond

Joint Bookrunner & Distributor 2011

22

UK Interest Rates

UK Term Rates (Gilt curve)

UK Term Rates (Gilt curve)

Source: Bloomberg 14-11-11

Source: Bloomberg