notes chap005

DESCRIPTION

ACCOUNTSTRANSCRIPT

Chapter 05 - Income Measurement and Profitability Analysis

CHAPTER 5INCOME MEASUREMENT AND PROFITABILITY ANALYSIS

OverviewThe timing of revenue recognition is critical to income measurement. Revenue affects income,

and, under the matching principle, expenses are recognized in the period in which the related revenues are recognized, so revenue recognition determines the recognition of some expenses as well. The focus of this chapter is revenue recognition. We also continue our discussion of financial statement analysis.

Learning Objectives1. Discuss the general objective of the timing of revenue recognition, list the two general criteria

that must be satisfied before revenue can be recognized, and explain why these criteria usually are satisfied at a specific point in time.

2. Describe the installment sales and cost recovery methods of recognizing revenue for some types of installment sales and explain the unusual conditions under which these methods might be used.

3. Discuss the implications for revenue recognition of allowing customers the right of return.4. Identify situations that call for the recognition of revenue over time and distinguish between the

percentage-of-completion and completed contract methods of recognizing revenue for long-term contracts.

5. Discuss the revenue recognition issues involving multiple-deliverable contracts, software, and franchise sales.

6. Identify and calculate the common ratios used to assess profitability.7. Discuss the primary differences between U.S. GAAP and IFRS with respect to revenue

recognition.

Lecture Outline

Part A: Revenue Recognition

I. Revenue Recognition in GeneralA. FASB definition: “Revenues are inflows or other enhancements of assets of an entity or

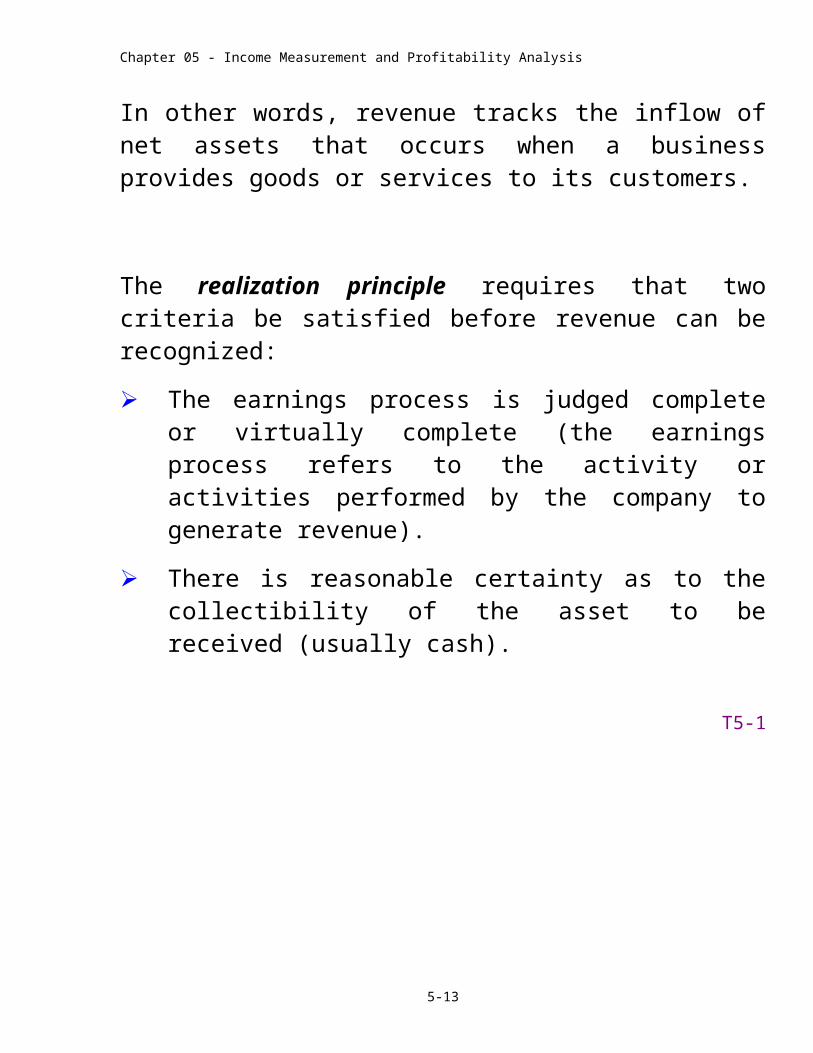

settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations.” In other words, revenue tracks the inflow of net assets that occurs when a business provides goods or services to its customers. (T5-1)

B. The realization principle requires that two criteria be satisfied before revenue can be recognized: 1. The earnings process is judged to be complete or virtually complete.2. There is reasonable certainty as to the collectibility of the asset to be received.

5-1

Chapter 05 - Income Measurement and Profitability Analysis

C. Staff Accounting Bulletin No. 101 summarized the SEC’s views on revenue recognition. The bulletin provides additional criteria for judging whether or not the realization principle is satisfied:1. Persuasive evidence of an arrangement exists.2. Delivery has occurred or services have been rendered.3. The seller’s price to the buyer is fixed or determinable.4. Collectibility is reasonably assured.

D. IFRS revenue recognition concepts focus on transfer of economic benefits. IFRS allows revenue to be recognized when the following conditions have been satisfied:1. The amount of revenue and costs associated with the transaction can be measured

reliably,2. It is probable that the economic benefits associated with the transaction will flow to

the seller,3. (for sales of goods) the seller has transferred to the buyer the risks and rewards of

ownership, and doesn’t effectively manage or control the goods,4. (for sales of services) the stage of completion can be measured reliably.These requirements are similar to U.S. GAAP, and revenue typically is recognized at a similar point under IFRS and U.S. GAAP. (T5-2)

II. Revenue Recognition at DeliveryA. While revenue usually is earned during a period of time, revenue often is recognized at

one specific point in time when both revenue recognition criteria are satisfied. B. Revenue from the sale of products usually is recognized at the point of product delivery,

but can be delayed past delivery if material uncertainties exist or allowed prior to delivery for long-term contracts. (T5-3, T5-4)

C. Service revenue often is recognized over time, in proportion to the amount of service performed. If there is one final service that is critical to the earnings process, revenues and costs are deferred and recognized after this service has been performed.

III. Revenue Recognition after DeliveryA. Significant uncertainties about cash collection could cause a delay in recognizing revenue

from the sale of a product or a service. (T5-3, T5-4)B. Installment sales

1. Revenue recognition for most installment sales takes place at the point of delivery, because reliable estimates of potential uncollectible amounts can be made.

2. When exceptional uncertainty exists, two accounting methods are available:a. The installment sales method.b. The cost recovery method.

3. The installment sales method recognizes gross profit by applying the gross profit percentage on the sale to the amount of cash actually received. (T5-5)

4. The cost recovery method defers all gross profit recognition until cash equal to the cost of the item sold has been received. (T5-6)

F. Right of Return (T5-7)

5-2

Chapter 05 - Income Measurement and Profitability Analysis

1. When the right of return exists, revenue cannot be recognized at the point of delivery unless the seller is able to make reliable estimates of future returns. In most retail situations, reliable estimates can be made and revenue and costs are recognized at point of delivery.

2. Otherwise, revenue and cost recognition is delayed until the uncertainty is resolved.

IV. Revenue Recognition prior to DeliveryA. It often is desirable to recognize revenue over time for long–term contracts. (T5-3, T5-4)

The types of companies that make use of long-term contracts are many and varied, although they are most prevalent in the construction industry. (T5-8) In these situations, there are two methods of accounting for revenue and expense recognition:1. The completed contract method.2. The percentage-of-completion method.

C. Much of the accounting is the same under both of these methods (T5-9, T5-10)1. All costs of construction are recorded in an asset (inventory) account called

construction in progress.2. Period billings are credited to billings on construction contract, a contra account to the

construction in progress account. This serves to reduce the carrying value of the physical asset (construction in progress) when a financial asset (accounts receivable) is also recognized; otherwise the project would be double-counted on the balance sheet.

3. Construction in progress is debited for the amount of gross profit recognized. The same total amount of gross profit is recognized under the two methods – the only difference is timing. (T5-10, T5-11)

D. The completed contract method is equivalent to recognizing revenue at the point of delivery, that is, when the project is complete.1. No revenues or expenses are recognized until the project is complete. (T5-10, T5-11)2. The completed contract method does not properly portray a company's performance

over the construction period and should only be used in unusual situations when forecasts of costs to complete the project are highly uncertain.

E. The percentage-of-completion method allocates a fair share of a project's revenues and expenses to each reporting period during construction. How is that fair share determined? (T5-12)1. The allocation of project profit is accomplished by estimating progress to date.2. Progress to date (the percentage of completion) can be estimated as the proportion of

the project's cost incurred to date divided by total estimated costs, by project milestones, or by relying on an engineer's or architect's estimate. The “cost to cost” approach is most common.

3. To determine periodic gross profit (revenues less expenses), the percentage of completion is multiplied by estimated gross profit to determine gross profit earned to date, and then the current period's gross profit is determined by subtracting from this amount the gross profit recognized in previous periods.

4. Periodic revenues are determined by multiplying the percentage of completion by the total contract price and then subtracting revenue recognized in prior periods. In most cases, the cost of construction equals the construction costs incurred during the period. (T5-13)

5-3

Chapter 05 - Income Measurement and Profitability Analysis

F. Balance sheet effects: Construction in progress is compared to billings on construction contract. (T5-14)1. A debit balance indicates costs (plus profits for the percentage-of-completion method)

in excess of billings and is reported as an asset.2. A credit balance indicates billings in excess of costs (plus profits for the percentage-

of-completion method) and is reported as a liability. G. Long-term contract losses

1. A loss could occur on a profitable project if the estimated costs to complete were underestimated in prior periods.

2. An estimated loss on a long-term contract is fully recognized in the first period that the loss is anticipated, regardless of the revenue recognition method used. (T5-15)

3. Recognized losses on long-term contracts reduce the construction in progress account.H. IFRS: IAS No. 11 governs revenue recognition for long-term construction contracts.

(T5-16)1. Like U.S. GAAP, the international standard requires the use of percentage-of-

completion accounting when estimates can be made precisely. 2. Unlike U.S. GAAP, the international standard requires the use of the cost recovery

method rather than the completed contract method when estimates cannot be made precisely enough to allow percentage-of-completion accounting.a. Under the cost recovery method, contract costs are expensed as incurred, and an

exactly offsetting amount of contract revenue is recognized, such that no gross profit is recognized until all costs have been incurred.

b. Under both the cost recovery and completed contract methods, no gross profit is recognized until the contract is essentially completed, but revenue and construction costs will be recognized earlier under the cost recovery method than under the completed contract method.

V. Industry-Specific Revenue IssuesA. Multiple-deliverable arrangements (T5-17)

1. If a software arrangement (sale) includes multiple elements, the revenue from the arrangement should be allocated to the various elements based on the relative fair values of the individual elements (Vendor-specific objective evidence”).

2. More generally, if an arrangement contains multiple deliverables, revenue should be allocated to individual deliverables if that qualify for separate revenue recognition (e.g., they must have value on a stand-alone basis). Otherwise, revenue is delayed until completion of later deliverables. The revenue is allocated based on relative selling prices, and those prices can be estimated if they are not available.

3. IFRS: IAS No. 18 is the general revenue recognition standard in IFRS. There is not much guidance about multiple-deliverable contracts or industry-specific revenue recognition in IFRS.

B. In a franchise sale, the fees to be paid by the franchisee to the franchisor usually comprise (1) the initial franchise fee, and (2) continuing franchise fees. (T5-18)1. GAAP requires that the franchisor has substantially performed the services promised

in the franchise agreement and that the collectibility of the initial franchise fee is reasonably assured before the fee can be recognized.

5-4

Chapter 05 - Income Measurement and Profitability Analysis

2. Continuing franchise fees are paid to the franchisor for continuing rights as well as for advertising and promotion and other services over the life of the agreement and are recognized by the franchisor as revenue in the period received, which corresponds to the periods the services are performed.

Part B: Profitability Analysis

I. Activity Ratios (T5-19)A. Activity ratios measure a company's efficiency in managing its assets.B. The asset turnover ratio measures a company's efficiency in using assets to generate

revenue and is calculated by dividing a company's net sales or revenues by the average total assets available for use during the period.

C. The receivables turnover ratio offers an indication of how quickly a company is able to collect its accounts receivable.1. The ratio is calculated by dividing a period's net credit sales by the average net

accounts receivable.2. An extension of this ratio is the average collection period, which is computed by

dividing 365 days by the receivable turnover ratio.D. The inventory turnover ratio measures a company's efficiency in managing its investment

in inventory.1. The ratio is calculated by dividing the period's cost of goods sold by the average

inventory balance.2. An extension of this ratio is the average days in inventory, which is computed by

dividing 365 days by the inventory turnover ratio.

II. Profitability Ratios (T5-20)A. Profitability ratios assist in evaluating various aspects of a company's profit-making

activities.B. The profit margin on sales measures the amount of net income achieved per sales dollar

and is computed by dividing net income by net sales.C. The return on assets (ROA) indicates a company's overall profitability.

1. It is calculated by dividing net income by average total assets.2. The return on assets can also be computed by multiplying the profit margin on sales

by the asset turnover.D. The return on shareholders' equity measures the return to suppliers of equity capital. It is

calculated by dividing net income by average shareholders' equity.

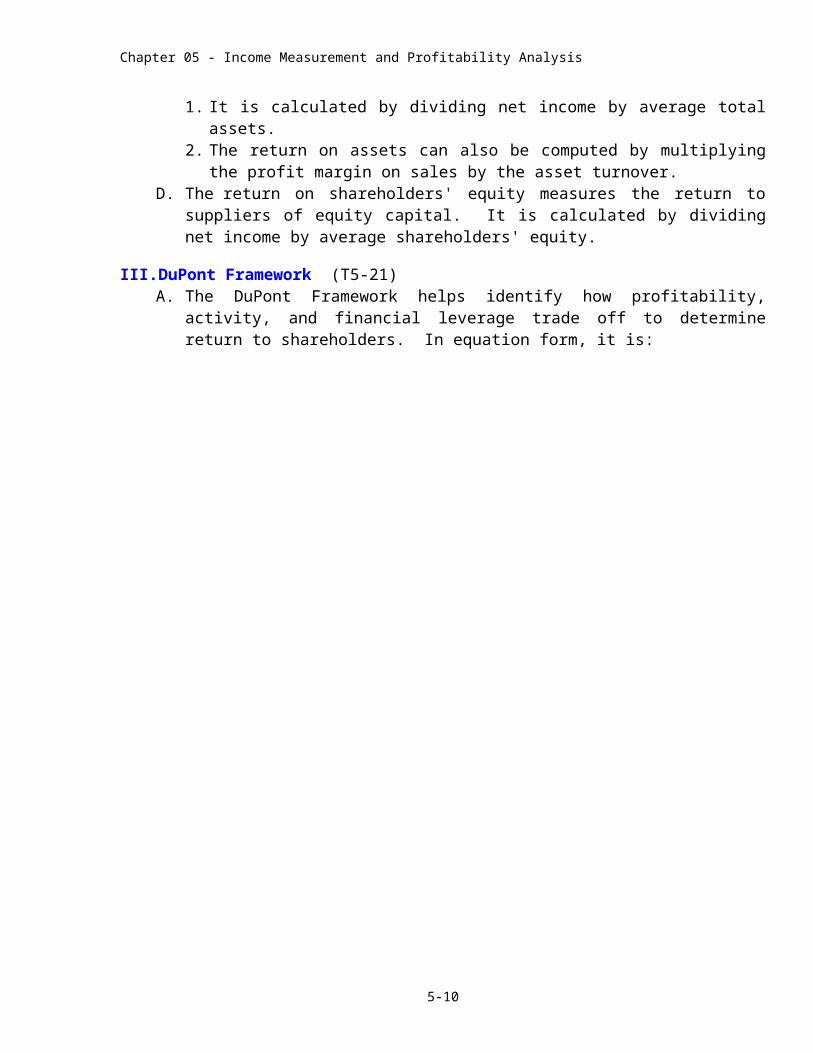

III. DuPont Framework (T5-21)A. The DuPont Framework helps identify how profitability, activity, and financial leverage

trade off to determine return to shareholders. In equation form, it is:

5-5

Chapter 05 - Income Measurement and Profitability Analysis

Return on equity = Profit margin

X Asset turnover X Equity multiplier

Net incomeAve. total equity

= Net incomeTotal sales

X Total salesAve. total assets

X Ave. total assetsAve. total equity

B. Because profit margin and asset turnover combine to equal return on assets, the DuPont framework can also be written as:

Return on equity = Return on assets X Equity multiplier

Net incomeAve. total equity

= Net incomeAve. total assets

X Ave. total assetsAve. total equity

Appendix: Interim ReportingA. Interim reports are issued for periods of less than a year, typically as quarterly financial

statements.B. With only a few exceptions, the same accounting principles applicable to annual reporting

are used for interim reporting.C. Complete financial statements are not required for interim reporting, but certain minimum

disclosures are required:1. Sales, income taxes, extraordinary items, cumulative effect of accounting principle

changes, and net income.2 Earnings per share.3 Seasonal revenues, costs, and expenses.4. Significant changes in estimates for income taxes.5. Discontinued operations, extraordinary items, and unusual or infrequent items.6. Contingencies.7. Changes in accounting principles or estimates.8. Significant changes in financial position.

PowerPoint SlidesA PowerPoint presentation of the chapter is available at the textbook website.

Teaching Transparency Masters

The following can be reproduced on transparency film as they appear here, or you can use the disk version of this manual and first modify them to suit your particular needs or preferences.

5-6

Chapter 05 - Income Measurement and Profitability Analysis

According to the FASB, “Revenues are inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations.”

In other words, revenue tracks the inflow of net assets that occurs when a business provides goods or services to its customers.

The realization principle requires that two criteria be satisfied before revenue can be recognized:

The earnings process is judged complete or virtually complete (the earnings process refers to the activity or activities performed by the company to generate revenue).

There is reasonable certainty as to the collectibility of the asset to be received (usually cash).

T5-1

5-7

DEFINITION AND

REALIZATION PRINCIPLE

Chapter 05 - Income Measurement and Profitability Analysis

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Revenue Recognition Concepts. IAS No. 18 governs most revenue recognition under IFRS. Similar to U.S. GAAP, it defines revenue as “the gross inflow of economic benefits during the period arising in the course of the ordinary activities of an entity when those inflows result in increases in equity, other than increases relating to contributions from equity participants.” IFRS allows revenue to be recognized when the following conditions have been satisfied:

1. The amount of revenue and costs associated with the transaction can be measured reliably,

2. It is probable that the economic benefits associated with the transaction will flow to the seller,

3. (for sales of goods) the seller has transferred to the buyer the risks and rewards of ownership, and doesn’t effectively manage or control the goods,

4. (for sales of services) the stage of completion can be measured reliably.

Note: These general conditions typically will lead to revenue recognition at the same time and in the same amount as would occur under U.S. GAAP, but there are exceptions (e.g., multiple-deliverable contracts).

More generally, IFRS has much less industry-specific guidance that does U.S. GAAP, leading to fewer exceptions to applying these revenue recognition conditions.

T5-2

5-8

Chapter 05 - Income Measurement and Profitability Analysis

Graphic 5-2

In most situations, the revenue recognition criteria are satisfied at the point of product delivery.

T5-3

5-9

RELATION BETWEEN EARNINGS PROCESS AND REVENUE

RECOGNITION METHODS

Chapter 05 - Income Measurement and Profitability Analysis

Usually Recognize Revenue for:Nature of the Revenue Sale of a Product Sale of a Service

Revenue Recognition Prior to Delivery, Be-cause:

Dependable estimates of progress are available.

Each period during the earnings process (e.g., long-term construction contract) in proportion to its percentage of com-pletion (percentage-of-completion method)

Each period during the earnings process (e.g., rental period) in propor-tion to its percentage of performance.

Dependable estimates of progress are not avail-able.

At the completion of the project (com-pleted contract method)

Not applicable

Revenue Recognitionat Delivery

When product is delivered and title transfers

When the key activity is performed

Revenue Recognition After Delivery, Because:

• Payments are signifi-cantly uncertain

When cash is collected (installment sales or cost recovery method)

When cash is collected

• Reliable estimates of product returns are unavailable

When critical event occurs that reduces product return uncertainty

Not applicable

• The product sold is out on consignment

When the consignee sells the product to the ultimate consumer

Not applicable

T5-4, Graphic 5-3

5-10

REVENUE RECOGNITION

Chapter 05 - Income Measurement and Profitability Analysis

INSTALLMENT SALES METHOD The installment sales method recognizes gross profit by applying the

gross profit percentage on the sale to the amount of cash actually received.

On November 1, 2011, the Belmont Corporation, a real estate developer, sold a tract of land for $800,000. The sales agreement requires the customer to make four equal annual payments of $200,000 plus interest on each November 1, beginning November 1, 2011. The land cost $560,000 to develop. The company’s fiscal year ends on December 31.

Illustration 5-1

Gross Profit Recognition

Date Cash CollectedCost Recovery

($560/$800=70%)Gross Profit

($240/$800=30%)Nov. 1, 2011 $200,000 $140,000 $ 60,000Nov. 1, 2012 200,000 140,000 60,000Nov. 1, 2013 200,000 140,000 60,000Nov. 1, 2014 200,000 140,000 60,000

Totals $800,000 $560,000 $240,000

T5-5

5-11

Chapter 05 - Income Measurement and Profitability Analysis

INSTALLMENT SALES METHOD(continued)

Journal Entries

Nov. 1, 2011 To record installment saleInstallment receivables.................................................. 800,000

Inventory................................................................... 560,000Deferred gross profit.................................................. 240,000

Nov. 1, 2011 To record cash collection from installment saleCash.............................................................................. 200,000

Installment receivables.............................................. 200,000

To recognize gross profit from installment saleDeferred gross profit..................................................... 60,000

Realized gross profit.................................................. 60,000

T5-5 (continued)

5-12

Chapter 05 - Income Measurement and Profitability Analysis

COST RECOVERY METHOD

The cost recovery method defers all gross profit recognition until cash equal to the cost of the item sold has been recovered.

On November 1, 2011, the Belmont Corporation, a real estate developer, sold a tract of land for $800,000. The sales agreement requires the customer to make four equal annual payments of $200,000 plus interest on each November 1, beginning November 1, 2011. The land cost $560,000 to develop. The company’s fiscal year ends on December 31.

Illustration 5-1

Gross Profit Recognition

Date Cash Collected Cost Recovery Gross ProfitNov. 1, 2011 $200,000 $200,000 $ - 0 -Nov. 1, 2012 200,000 200,000 - 0 -Nov. 1, 2013 200,000 160,000 40,000Nov. 1, 2014 200,000 - 0 - 200,000

Totals $800,000 $560,000 $240,000

T5-6

5-13

Chapter 05 - Income Measurement and Profitability Analysis

COST RECOVERY METHOD(continued)

Journal Entries

Nov. 1, 2011 To record installment saleInstallment receivables....................................... 800,000

Inventory......................................................... 560,000Deferred gross profit....................................... 240,000

To record cash collection from installment sale

Nov. 1, 2011, 2012, 2013, and 2014Cash................................................................... 200,000

Installment receivables................................... 200,000

To recognize gross profit from installment sale

Nov. 1, 2011 and 2012No entry

Nov. 1, 2013Deferred gross profit.......................................... 40,000

Realized gross profit....................................... 40,000

Nov. 1, 2014Deferred gross profit.......................................... 200,000

Realized gross profit....................................... 200,000

T5-6 (continued)

5-14

Chapter 05 - Income Measurement and Profitability Analysis

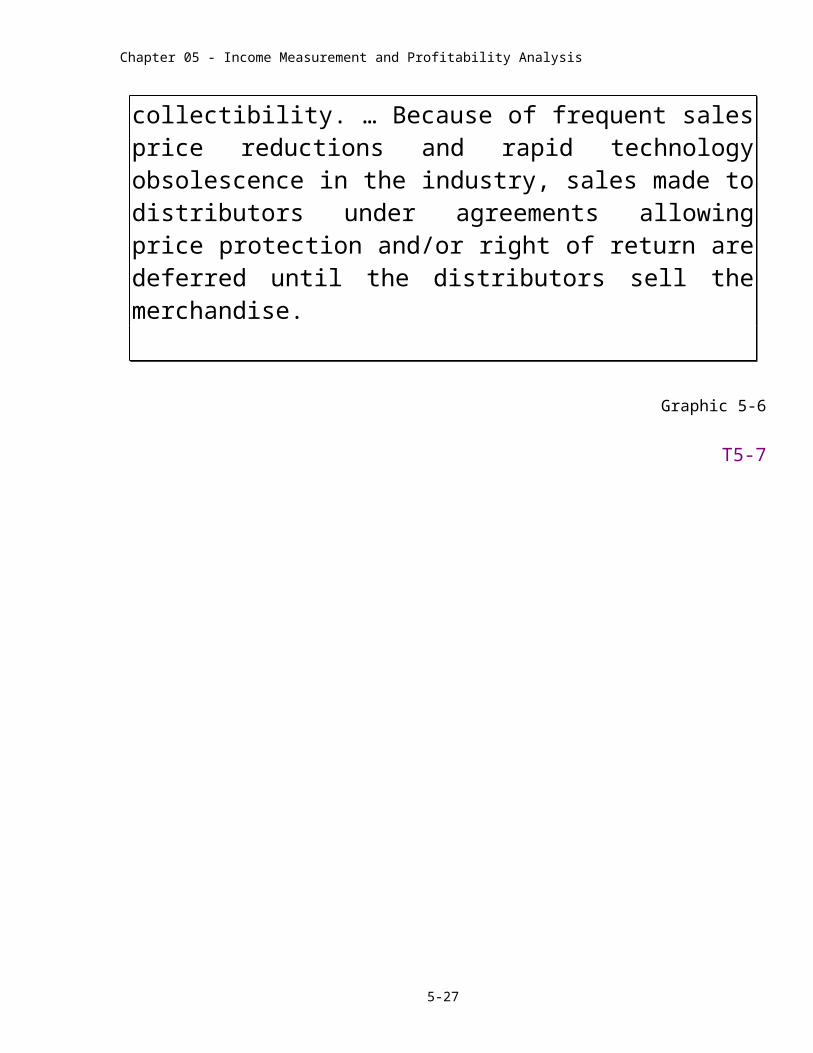

RIGHT OF RETURN

When the right of return exists, revenue cannot be recognized at the point of delivery unless the seller is able to make reliable estimates of future returns. In most retail situations, reliable estimates can be made and revenue and costs are recognized at point of delivery.

Otherwise, revenue and cost recognition is delayed until the uncertainty is resolved.

Disclosure of Revenue Recognition Policy — Intel Corporation

Notes: Revenue Recognition

The company recognizes net revenue when the earnings process is complete, as evidenced by an agreement with the customer, transfer of title and acceptance, if applicable, as well as fixed pricing and probable collectibility. … Because of frequent sales price reductions and rapid technology obsolescence in the industry, sales made to distributors under agreements allowing price protection and/or right of return are deferred until the distributors sell the merchandise.

Graphic 5-6

T5-7

5-15

Chapter 05 - Income Measurement and Profitability Analysis

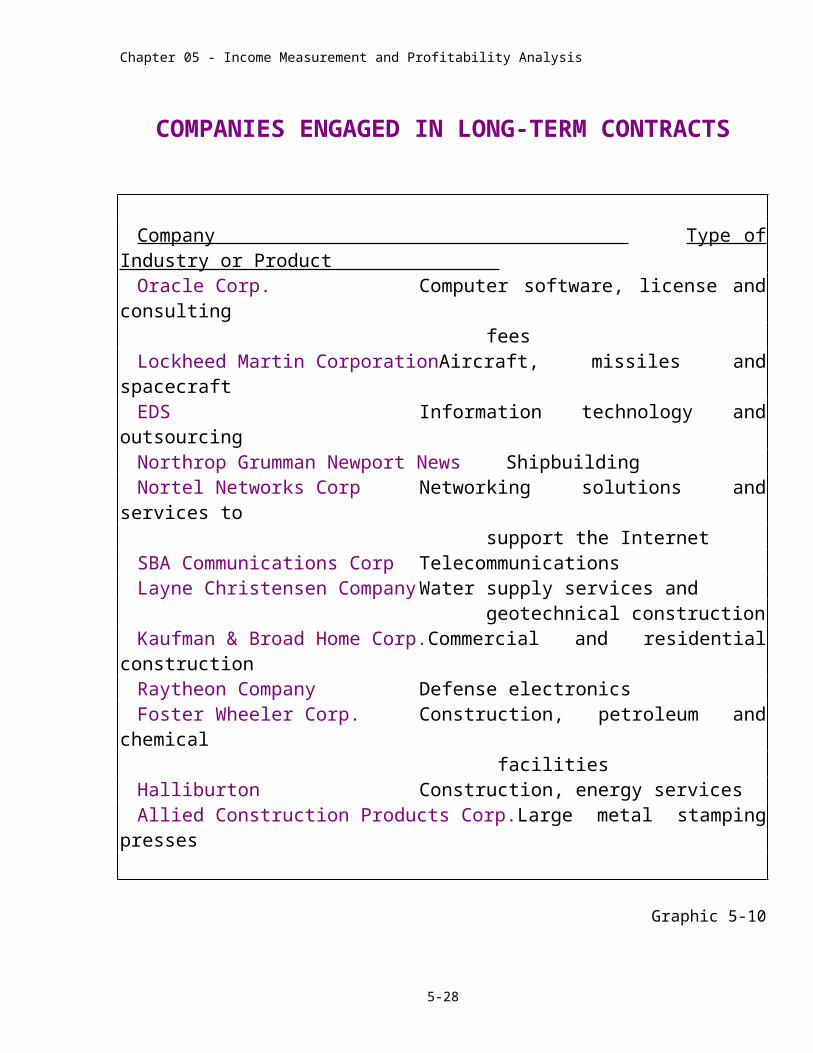

COMPANIES ENGAGED IN LONG-TERM CONTRACTS

Company Type of Industry or Product Oracle Corp. Computer software, license and consulting

feesLockheed Martin Corporation Aircraft, missiles and spacecraftEDS Information technology and outsourcingNorthrop Grumman Newport News ShipbuildingNortel Networks Corp Networking solutions and services to

support the InternetSBA Communications Corp TelecommunicationsLayne Christensen Company Water supply services and

geotechnical constructionKaufman & Broad Home Corp. Commercial and residential constructionRaytheon Company Defense electronicsFoster Wheeler Corp. Construction, petroleum and chemical

facilitiesHalliburton Construction, energy servicesAllied Construction Products Corp. Large metal stamping presses

Graphic 5-10

T5-8

5-16

Chapter 05 - Income Measurement and Profitability Analysis

COMPLETED CONTRACT AND PERCENTAGE-OF-COMPLETION METHODS: AN EXAMPLE

At the beginning of 2011, the Harding Construction Company received a contract to build an office building for $5 million. The project is estimated to take three years to complete. According to the contract, Harding will bill the buyer in installments over the construction period according to a prearranged schedule. Information related to the contract is as follows:

2011 2012 2013 Construction costs incurred during the year $1,500,000 $1,000,000 $1,600,000 Construction costs incurred in prior years - 0 - 1,500,000 2,500,000 Cumulative construction costs 1,500,000 2,500,000 4,100,000 Estimated costs to complete at end of year 2,250,000 1,500,000 - 0 - Total estimated and actual construction costs $3,750,000 $4,000,000 $4,100,000 Billings made during the year $1,200,000 $2,000,000 $1,800,000 Cash collections during year 1,000,000 1,400,000 2,600,000

Illustration 5–2

T5-9

5-17

Chapter 05 - Income Measurement and Profitability Analysis

JOURNAL ENTRIES

2011 2012 2013BOTH METHODS:Construction in progress 1,500,000 1,000,000 1,600,000 Cash, materials, etc. 1,500,000 1,000,000 1,600,000To record construction costs.

Accounts receivable 1,200,000 2,000,000 1,800,000 Billings on construction contract 1,200,000 2,000,000 1,800,000To record progress billings.

Cash 1,000,000 1,400,000 2,600,000 Accounts receivable 1,000,000 1,400,000 2,600,000To record cash collections.

COMPLETED CONTRACT:Construction in progress (gross profit) 900,000Cost of construction 4,100,000 Revenue from long-term contracts 5,000,000To record gross profit.

Billings on construction contract 5,000,000 Construction in progress 5,000,000To close accounts. PERCENTAGE-OF-COMPLETION:Construction in progress (gross profit) 500,000 125,000

275,000

Cost of construction 1,500,000 1,000,000 1,600,000 Revenue from long-term contracts 2,000,000 1,125,000 1,875,000To record gross profit.

Billings on construction contract 5,000,000 Construction in progress 5,000,000To close accounts.

Illustrations 5-2a-c

T5-10

5-18

Chapter 05 - Income Measurement and Profitability Analysis

A COMPARISON OF THE TWO METHODS — INCOME RECOGNITION

Percentage-of-Completion

Completed Contract

Gross profit recognized:2011 $500,000 - 0 -2012 125,000 - 0 -2013 275,000 $900,000

Total gross profit $900,000 $900,000

T5-11

5-19

Chapter 05 - Income Measurement and Profitability Analysis

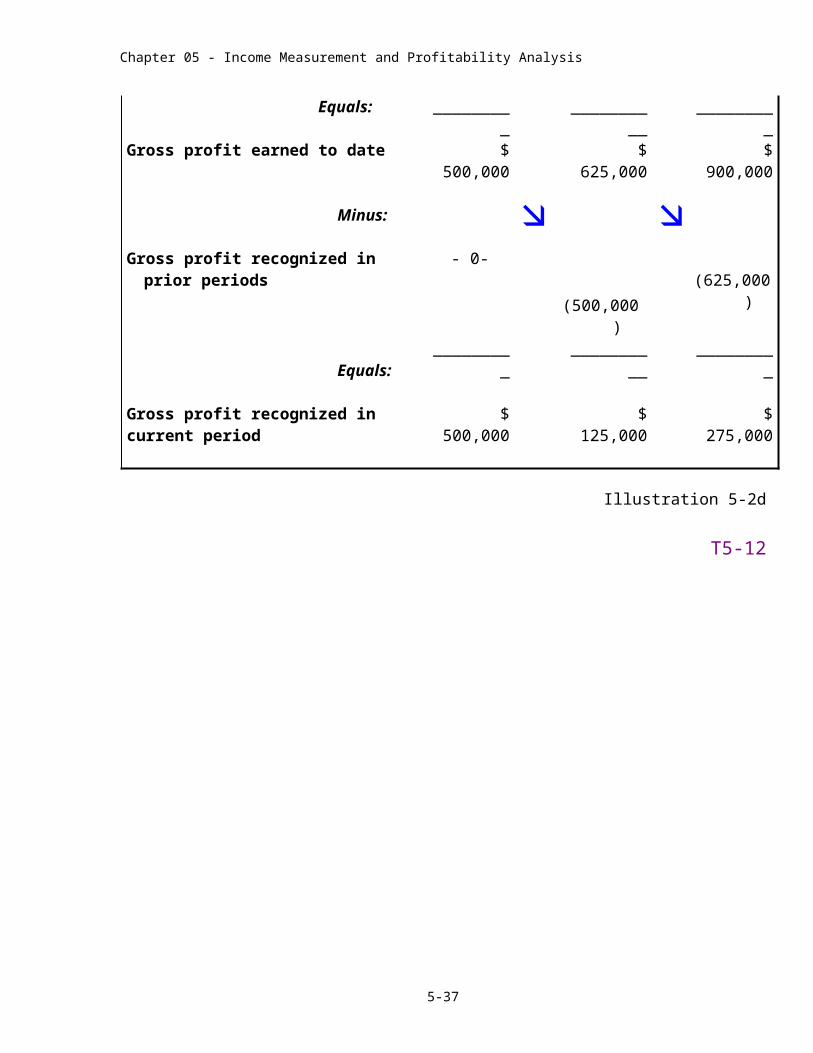

CALCULATING GROSS PROFIT UNDER THE PERCENTAGE-OF-COMPLETION METHOD

2011 2012 2013

Contract price $5,000,000 $5,000,000 $5,000,000

Construction costs: Construction costs incurred during the year $1,500,000 $1,000,000 $1,600,000 Construction costs incurred in prior years -0- 1,500,000 2,500,000 Cumulative construction costs to date $1,500,000 $2,500,000 $4,100,000 Estimated costs to complete at end of year 2,250,000 1,500,000 -0- Total estimated and actual construction costs $3,750,000 $4,000,000 $4,100,000

Total gross profit (estimated for 2011 & 2012, actual in 2013):

Contract price minus total estimated and actual costs

$1,250,000 $1,000,000 $900,000

Multiplied by: X X X

Percentage-of-completion:Actual costs to date divided by the estimated total project cost

$1,500,000$3,750,000

= 40%

$2,500,000$4,000,000

= 62.5%

$4,100,000$4,100,000

= 100% Equals: _________ __________ _________

Gross profit earned to date $ 500,000 $ 625,000 $ 900,000 Minus:

Gross profit recognized in prior periods - 0-

(500,000)

(625,000)

Equals:_________ __________ _________

Gross profit recognized in current period $ 500,000 $ 125,000 $ 275,000

Illustration 5-2d

5-20

Chapter 05 - Income Measurement and Profitability Analysis

T5-12

5-21

Chapter 05 - Income Measurement and Profitability Analysis

REVENUE AND COST OF CONSTRUCTION: PERCENTAGE-OF-COMPLETION METHOD

2011Revenue recognized in 2011 ($5,000,000 x 40%) $2,000,000

Cost of construction 1,500,000Gross profit $ 500,000

2012Revenue recognized to date ($5,000,000 x 62.5%) $3,125,000

Less: Revenue recognized in 2011 (2,000,000 )Revenue recognized in 2012 $1,125,000

Cost of construction 1,000,000Gross profit $ 125,000

2011Revenue recognized to date ($5,000,000 x 100%) $5,000,000

Less: Revenue recognized in 2011 and 2012 (3,125,000 )Revenue recognized in 2013 $1,875,000

Cost of construction 1,600,000Gross profit $ 275,000

Illustration 5-2e

T5-13

5-22

Chapter 05 - Income Measurement and Profitability Analysis

BALANCE SHEET PRESENTATION

Balance Sheet (End of year)

2011 2012Percentage-of-completion:Current assets: Accounts receivable $ 200,000 $800,000 Costs and profit ($2,000,000) in excess of billings ($1,200,000) 800,000Current liabilities: Billings ($3,200,000) in excess of costs and profit ($3,125,000) 75,000

Completed contract:Current assets: Accounts receivable $ 200,000 $800,000 Costs ($1,500,000) in excess of billings ($1,200,000) 300,000Current liabilities: Billings ($3,200,000) in excess of costs ($2,500,000) 700,000

Illustration 5-2f

T5-14

5-23

Chapter 05 - Income Measurement and Profitability Analysis

LONG-TERM CONTRACT LOSSES

An estimated loss on a long-term contract is fully recognized in the first period that the loss is anticipated, regardless of the revenue recognition method used.

2011 2012 2013 Construction costs incurred during the year $1,500,000 $1,260,000 $2,440,000 Construction costs incurred in prior years - 0 - $1,500,000 $2,760,000 Cumulative construction costs 1,500,000 2,760,000 5,200,000 Estimated costs to complete at end of year 2,250,000 2,340,000 - 0 - Total estimated and actual construction costs $3,750,000 $5,100,000 $5,200,000

Comparison of Periodic Gross Profit (Loss)

Percentage-of-completion Completed Contract

Gross profit (loss) recognized:2011 $500,000 - 0 -2012 (600,000) $(100,000)2013 (100,000 ) (100,000 )

Total project loss $(200,000 ) $(200,000 )

T5-15

5-24

Chapter 05 - Income Measurement and Profitability Analysis

INTERNATIONAL FINANCIAL REPORTING STANDARDS

Long-Term Construction Contracts. IAS No. 11 governs revenue recognition for long-term construction contracts. Like U.S. GAAP, IAS No. 11 requires use of percentage-of-completion accounting when estimates can be made precisely. Unlike U.S. GAAP, IAS No. 11 requires use of the cost recovery method rather than the completed contract method when estimates cannot be made precisely enough to allow percentage-of-completion accounting. Under the cost recovery method, contract costs are expensed as incurred, and an exactly offsetting amount of contract revenue is recognized, such that no gross profit is recognized until all costs have been incurred. Under both the cost recovery and completed contract methods, no gross profit is recognized until the contract is essentially completed, but revenue and construction costs will be recognized earlier under the cost recovery method than under the completed contract method.

T5-16

5-25

Chapter 05 - Income Measurement and Profitability Analysis

SOFTWARE AND OTHER MULTIPLE-DELIVERABLE ARRANGEMENTS

If a software arrangement (sale) includes multiple elements, the revenue from the arrangement should be allocated to the various elements based on “VSOE” (vendor-specific objective evidence) of the individual elements.

More generally, for multiple-deliverable arrangements, revenue should be allocated to individual deliverables that qualify for separate revenue recognition. Otherwise, revenue is delayed until completion of later deliverables. Revenue is allocated according to the deliverables’ relative selling prices. These can be estimated if items aren’t sold separately.

T5-17

5-26

Chapter 05 - Income Measurement and Profitability Analysis

FRANCHISE SALES

On March 31, 2011, the Red Hot Chicken Wing Corporation entered into a franchise agreement with Thomas Keller. In exchange for an initial franchise fee of $50,000, Red Hot will provide initial services to include the selection of a location, construction of the building, training of employees, and consulting services over several years. $10,000 is payable on March 31, 2011, with the remaining $40,000 payable in annual installments which include interest at an appropriate rate. In addition, the franchisee will pay continuing franchise fees of $1,000 per month for advertising and promotion provided by Red Hot, beginning immediately after the franchise begins operations. Thomas Keller opened his Red Hot franchise for business on September 30, 2011.

Initial Franchise Fee

March 31, 2011 To record franchise agreement and down paymentCash.............................................................................. 10,000Note receivable............................................................. 40,000

Unearned franchise fee revenue................................. 50,000

Sept. 30, 2011 To recognize franchise fee revenueUnearned franchise fee revenue..................................... 50,000

Franchise fee revenue................................................ 50,000

Continuing Franchise Fees

To recognize continuing franchise fee revenueCash (or accounts receivable)........................................ 1,000

Service revenue......................................................... 1,000

Illustration 5-3

5-27

Chapter 05 - Income Measurement and Profitability Analysis

T5-18

5-28

Chapter 05 - Income Measurement and Profitability Analysis

ACTIVITY RATIOS

Activity ratios measure a company's efficiency in managing its assets.

Asset turnover ratio = Net sales Average total assets

Receivables turnover ratio = Net sales Average accounts receivable (net)

Average collection period = 365 Receivables turnover ratio

Inventory turnover ratio = Cost of goods sold Average Inventory

Average days in inventory = 365 Inventory turnover ratio

T5-19

5-29

Chapter 05 - Income Measurement and Profitability Analysis

PROFITABILITY RATIOS

Profitability ratios assist in evaluating various aspects of a company's profit-making activities.

Profit margin on sales = Net income Net sales

Return on assets = Net income Average total assets

Return on shareholders' = Net income equity Average shareholders' equity

T5-20

5-30

Chapter 05 - Income Measurement and Profitability Analysis

DUPONT FRAMEWORK

The DuPont Framework helps identify how profitability, activity, and financial leverage trade off to determine return to shareholders:

Return on equity =

Profit margin X

Asset turnover X

Equity multiplier

Net incomeAvg. total

equity=

Net incomeTotal sales X

Total salesAvg. total

assetsX

Avg. total assetsAvg. total

equity

Because profit margin and asset turnover combine to equal return on assets, the DuPont framework can also be written as:

Return on equity =

Return on assets X

Equity multiplier

Net incomeAvg. total

equity=

Net incomeAvg. total

assetsX

Avg. total assetsAvg. total

equity

T5-21

5-31

Chapter 05 - Income Measurement and Profitability Analysis

Suggestions for Class Activities

1. Real World Scenario

The following is an excerpt from an article that appeared in the August 25, 2002 edition of The Seattle Times:

When Cutter & Buck revealed two weeks ago that it padded sales figures in 2000 by recording $5.8 million in shipments that were mostly returned, the news came as a surprise to many investors. But it wasn’t the first time the Seattle sportswear retailer’s shipping and accounting practices have been called into question. Shortly before co-founder Joey Rodolfo left in 1997, he accused the company of shipping orders months before customers were expecting them, a method of prematurely booking sales.

Some customers and former employees say early shipments persisted for years after Rodolfo raised the issue. And late last week, Chief Executive Fran Conley said an internal investigation has found that early shipments were “more extensive than I had known” and may force the company to further restate sales figures.

Shipping and booking orders ahead of schedule to meet short-term sales goals — a practice sometimes called channel stuffing — is not, by definition, illegal. But by essentially borrowing from future sales to claim bigger current sales and profit, it can be used to boost a company’s bottom line and create a misleading appearance of growth for investors.

Suggestions:This article provides a good way to introduce the topic of channel stuffing. When a company

stuffs the channel, it ships inventory ahead of schedule filling its distribution channels with more product than is needed. Since companies often record sales as soon as they ship products, channel stuffing can make it appear that business is booming. Is this practice legal? Is it an acceptable practice according to GAAP? Is it an ethical practice?

Points to note:Channel stuffing is not an uncommon practice. There are many examples you can find for

your students. A text case references the Sunbeam incident that occurred in the late 90s. More recent examples include Microsoft, Novell, Network Associates, and AOL.

GAAP do not address channel stuffing specifically. The key is whether or not the practice leads to excessive future sales returns that are not adequately provided for by the seller. There may be an issue with respect to the legality of the practice if it can be shown that the practice resulted in misleading information to the investing public. And there are ethical dimensions to the practice as well.

5-32

Chapter 05 - Income Measurement and Profitability Analysis

2. Research Activity

Probably most of your students have purchased merchandise via the Internet. You can buy the products of many companies on line. Some of these companies, such as Amazon.com, often act merely as intermediaries between the manufacturer and the consumer. Revenue recognition for this type of transaction has been controversial. If Amazon sells something to a customer for $100 that costs $80, the profit on the transaction is clearly $20. But should Amazon recognize $100 in revenue and $80 in cost of goods sold (the gross method), or should it recognize only the $20 in gross profit (the net method)?

Suggestions:Discuss with your class the implications of one reporting method versus the other. Why should it

make a difference? What factors might dictate whether or not Amazon should recognize the transaction gross versus net? Have them access Amazon’s most recent financial statements using Edgar (at http://www.sec.gov/edgar.shtml). Or, you can show them Amazon’s disclosure note and discuss the contents of the note. The following is a portion of the company’s revenue recognition disclosure note that appeared in its 2008 financial statements:

We recognize revenue from product sales or services rendered when the following four revenue recognition criteria are met: persuasive evidence of an arrangement exists, delivery has occurred or services have been rendered, the selling price is fixed or determinable, and collectibility is reasonably assured. Additionally, revenue arrangements with multiple deliverables are divided into separate units of accounting if the deliverables in the arrangement meet the following criteria: the delivered item has value to the customer on a standalone basis; there is objective and reliable evidence of the fair value of undelivered items; and delivery of any undelivered item is probable.

We evaluate the criteria outlined in Emerging Issues Task Force (EITF) Issue No. 99-19, Reporting Revenue Gross as a Principal Versus Net as an Agent, in determining whether it is appropriate to record the gross amount of product sales and related costs or the net amount earned as commissions. Generally, when we are primarily obligated in a transaction, are subject to inventory risk, have latitude in establishing prices and selecting suppliers, or have several but not all of these indicators, revenue is recorded gross. If we are not primarily obligated and amounts earned are determined using a fixed percentage, a fixed-payment schedule, or a combination of the two, we generally record the net amounts as commissions earned.

5-33

Chapter 05 - Income Measurement and Profitability Analysis

3. Google Analysis

Have students, individually or in groups, go to the most recent Google annual report using Edgar which can be located at: http://www.sec.gov/edgar.shtml. Ask them to:

1. Compute the receivables turnover ratio, the profit margin on sales, the return on assets ratio, and the return on shareholders' equity ratio for the most three years. Are there any discernible trends? How might they be interpreted?

2. Read the "Revenues" section of "Management's Discussion and Analysis of Results of Operations and Financial Condition." Has there been any significant shift over the last three years in the company's service revenue mix?

3. Use Edgar to locate the most recent annual report information for Yahoo, Google’s competitor. Using the most recent annual report information for both companies, compare the receivables turnover ratio, the profit margin on sales, the return on assets ratio, and the return on shareholders' equity ratio. Are there any differences in the way the companies recognize revenue?

4. Note: another peer comparison of this nature is Federal Express vs. United Parcel Service.

4. Professional Skills Development Activities

The following are suggested assignments from the end-of-chapter material that will help your students develop their communication, research, analysis and judgment skills.

Communication Skills. In addition to Communication Case 5-15, Judgment Case 5-14 can be adapted to ask students to choose one of the two alternatives and write a memo supporting their position. Communication Case 5-5, Judgment Case 5-4, and IFRS Case 5-17 do well as group assignments. Research Case 5-6 and Ethics Case 5-8 create good class discussions. Problem 5-12 and Analysis Case 5-21 are suitable for student presentation(s).

Research Skills. In their careers, our graduates will be required to locate and extract relevant information from available resource material to determine the correct accounting practice, perhaps identifying the appropriate authoritative literature to support a decision. Research Cases 5-11, 5-12 and 5-13 provides an excellent opportunity to help students develop this skill.

Analysis Skills. The “Broaden Your Perspective” section includes Analysis Cases that direct students to gather, assemble, organize, process, or interpret data to provide options for making business and investment decisions. In addition to Analysis Case 5-21; Exercises 5-20, 5-21, and 5-22; Problems 5-11, 5-12, 5-13, and 5-14, and Judgment Case 5-17 also provide opportunities to develop and sharpen analytical skills.

5-34

Chapter 05 - Income Measurement and Profitability Analysis

Judgment Skills. The “Broaden Your Perspective” section includes Judgment Cases that require students to critically analyze issues to apply concepts learned to business situations in order to evaluate options for decision-making and provide an appropriate conclusion. In addition to Judgment Cases 5-2, 5-3, 5-4, 5-9, 5-10, 5-13, 5-14, and 5-22 Real World Case 5-1 also requires students to exercise judgment.

5. Ethical Dilemma

The chapter contains the following ethical dilemma:

ETHICAL DILEMMA

The Precision Parts Corporation manufactures automobile parts. The company has reported a profit every year since the company’s inception in 1977. Management prides itself on this accomplishment and believes one important contributing factor is the company’s incentive plan that rewards top management a bonus equal to a percentage of operating income if the operating income goal for the year is achieved. However, 2011 has been a tough year, and prospects for attaining the income goal for the year are bleak.

Tony Smith, the company’s chief financial officer, has determined a way to increase December sales by an amount sufficient to boost operating income over the goal for the year and earn bonuses for all top management. A reputable customer ordered $120,000 of parts to be shipped on January 15, 2012. Tony told the rest of top management “I know we can get that order ready by December 31 even though it will require some production line overtime. We can then just leave the order on the loading dock until shipment. I see nothing wrong with recognizing the sale in 2011, since the parts will have been manufactured and we do have a firm order from a reputable customer.” The company’s normal procedure is to ship goods f.o.b. destination and to recognize sales revenue when the customer receives the parts.

You may wish to discuss this in class. If so, discussion should include these elements.

Step 1—The Facts:Precision Parts Corporation has reported profits since its inception and given top management

bonuses when the operating income goal is achieved. In 2011, however, the company does not expect to achieve its profit goal. Tony Smith, the CFO, wants to record a sale in 2011 that will not be shipped until January 2012, so that management will receive bonuses for achieving the profit goal. The CFO is attempting to manipulate the recognition of revenue. The company's normal procedure is to recognize sales revenue when goods are shipped f.o.b. destination. Although sales revenue may be recognized when production ends if certainty of collection exists, nothing in the case indicates that there is reasonable certainty as to the collectibility of the revenue at the end of production.

5-35

Chapter 05 - Income Measurement and Profitability Analysis

Step 2—The Ethical Issue and the Stakeholders:The ethical issue or dilemma is whether Tony Smith's obligation to top management to show a

profit is greater than his obligation to provide information that is not misleading to users of financial statements.

Stakeholders include Tony Smith, CFO, other corporate managers, auditors, present and future creditors, and current and future investors.

Step 3—Values: Values include competence, honesty, integrity, objectivity, loyalty to the company, and

responsibility to users of financial statements.

Step 4—Alternatives:1. Record the parts sales revenue in 2011.2. Record the parts sales revenue in 2012, when the goods are shipped.

Step 5—Evaluation of Alternatives in Terms of Values:1. Alternative 1 illustrates loyalty to the company and other top managers.2. Alternative 2 exhibits the values of competence, honesty, integrity, objectivity, and

responsibility to users of the financial statements.

Step 6—Consequences:Alternative 1Positive consequences: Tony would enable other top managers to receive bonuses and permit the

company to meet their operating income goal.Negative consequences: Users of the financial statements would be misinformed. Users of

financial statements may sue the company upon learning the truth if the amount of revenue is material and affects their financial decisions. Auditors may refuse to give a positive opinion on the fair presentation of the financial statements. Tony may lose the respect of the rest of top management and his job.

Alternative 2Positive consequences: Users of financial statements would receive more relevant and reliable

reported revenue. Tony would maintain his integrity. He may receive praise for being honest and keep his job.

Negative consequences: Tony may incur the disfavor of the rest of top management for not enabling others to receive a bonus. He may lose the trust of other managers and lose his job.

Step 7—Decision: Student(s) must decide their course of action.

5-36

Chapter 05 - Income Measurement and Profitability Analysis

Assignment ChartLearning Est. time

Questions Objective(s) Topic (min.)

5-1 1 Revenue recognition criteria 55-2 1 Revenue recognition at point of delivery 55-3 2 Installment sales 55-4 2 Installment sales and cost recovery methods 55-5 2 Deferred gross profit—installment sales method 55-6 3 Right of return 55-7 1 Consignment sale 55-8 4 Service revenue 55-9 4 Percentage-of-completion and completed contract

methods5

5-10 4,7 IFRS; cost recovery method for long-term contracts 55-11 4 Billings on construction contract 55-12 4 Estimated loss on construction project 55-13 5 Software sales 55-14 5,7 IFRS; multiple-deliverable arrangements 55-15 5 Franchise fee revenue recognition 55-16 6 Activity ratios 55-17 6 Profitability ratios 55-18 6 DuPont framework 55-19 1 Interim reports [based on Appendix] 5

Brief Learning Est. time

Exercises Objective(s) Topic (min.)

5-1 1 Point of delivery recognition 55-2 2 Installment sales method 105-3 2 Cost recovery method 105-4 2 Installment sales method 105-5 3 Right of return 55-6 4 Percentage-of-completion method; profit recognition 105-7 4 Percentage-of-completion method; balance sheet 105-8 4 Completed contract method 55-9 4,7 IFRS; cost recovery method for long-term contracts 10

5-10 4 Long-term contract accounting; loss on entire project 105-11 5 Multiple-deliverable contracts 105-12 5,7 IFRS; multiple deliverable contracts 105-13 5 Franchise sales 55-14 6 Turnover ratios 55-15 6 Profitability ratios 105-16 6 DuPont framework 105-17 6 Inventory turnover ratio 10

5-37

Chapter 05 - Income Measurement and Profitability Analysis

Learning Est. timeExercises Objective(s) Topic

(min.)5-1 1 Service revenue 155-2 2 Installment sales method 205-3 2 Installment sales method; journal entries 155-4 2 Installment sales; alternative recognition methods 15

5-5 1,2Journal entries; point of delivery, installment sales, and cost recovery methods 25

5-6 2Installment sales and cost recovery methods; solve for unknowns 10

5-7 2Installment sales method and repossession.

205-8 1,2 Real estate sales; gain recognition 155-9 4 Percentage-of-completion and completed contract

methods20

5-10 4,7IFRS; long-term contract; percentage of completion and completed contract methods 30

5-11 4Percentage-of-completion method; loss projected on entire project 30

5-12 4Completed contract method; loss projected on entire project 20

5-13 4Income (loss) recognition; percentage-of-completion and completed contract methods compared 50

5-14 4 Percentage-of-completion method; solve for unknowns 255-15 5 Revenue recognition; software 105-16 5 Revenue recognition; Multiple-deliverable contracts 155-17 5,7 IFRS; multiple-deliverable contracts 155-18 5 Revenue recognition; franchise sales 105-19 2,3,4,5,6 Concepts; terminology 155-20 6 Inventory turnover; calculation and evaluation 105-21 6 Evaluating efficiency of asset management 105-22 6 Profitability ratios 105-23 6 DuPont framework 10

5-24 1Interim financial statements; income tax expense [based on Appendix] 10

5-25 1Interim reporting; recognizing expenses [based on Appendix] 10

5-26 1Interim financial statements; reporting expenses [based on Appendix] 10

5-27 4 Percentage-of-completion, codification 105-28 2,3,4 Percentage-of-completion, installment, and cost-recovery

methods, right of return, codification15

5-38

Chapter 05 - Income Measurement and Profitability Analysis

CPA Learning Est. time

Review Questions Objective(s) Topic (min.)

5-1 1 Revenue recognition upon delivery 35-2 2 Installment sales method 35-3 2 Installment sales method 35-4 4 Percentage-of-completion method 25-5 4 Percentage-of-completion method 35-6 4 Percentage-of-completion method 3

CMAReview Questions

LearningObjective(s) Topic

Est. time(min.)

5-1 1 Revenue recognition upon delivery and bad debts 35-2 4 Percentage-of-completion method 35-3 4 Percentage-of-completion method 3

Learning Est. timeProblems Objective(s) Topic

(min.)

5-1 2Income statement presentation; installment sales method [Chapters 4 and 5] 25

5-2 2 Installment sales and cost recovery methods 305-3 2 Installment sales; alternative recognition methods 30

� 5-4 2 Installment sales and cost recovery methods, multiple years

30

5-5 4 Percentage-of-completion method 455-6 4 Completed contract method 405-7 4,7 IFRS; Construction accounting 405-8 4 Construction accounting; loss projected on entire project 25

� 5-9 4 Percentage-of-completion and completed contract methods

45

� 5-10 2,5 Franchise sales, installment sales method 25

5-11 6 Calculating activity and profitability ratios 20

5-12 6Use of ratios to compare two companies in the same industry; Johnson and Johnson, Pfizer 40

� 5-13 6 Creating a balance sheet from ratios; chapters 3 and 5 50

5-14 6Use of ratios to compare two companies in the same industry; chapters 3 and 5 40

5-15

� Star Problems

1 Interim financial reporting [based on Appendix] 15

5-39

Chapter 05 - Income Measurement and Profitability Analysis

Learning Est. timeCases Objective(s) Topic

(min.)Real World Case 5-1 1 Revenue recognition and earnings management;

Sunbeam20

Judgment Case 5-2 1 Revenue recognition 15Judgment Case 5-3 1 Revenue recognition for initial and monthly fees 15Judgment Case 5-4 1 Revenue recognition; trade-ins 20Communication Case 5-5 1 Revenue recognition 20Research Case 5-6 4 Long-term contract accounting 45Research Case 5-7 1 Earnings management techniques for revenues 30Ethics Case 5-8 1 Revenue recognition 15Judgment Case 5-9 1,2 Revenue recognition ; installment sales 20Judgment Case 5-10 1 Revenue recognition; SAB 101 questions, codification 20Research Case 5-11 3 Revenue recognition; right of return; Hewlett Packard,

Advanced Micro Devices, codification45

Research Case 5-12 1 Earnings management: gross vs. net and EITF 99-19; Google, codification

30

Judgment Case 5-13 1,4 Revenue recognition, service sales 15Judgment Case 5-14 4 Revenue recognition; long-term construction contracts 15Communication Case 5-15 4 Percentage-of-completion and completed contract

methods50

IFRS Case 5-16 1,4,7IFRS; Comparison of revenue recognition in Sweden and the U.S.A.; Vodafone 15

IFRS Case 5-17 4,7 IFRS; Construction accounting 30Trueblood Accounting Case 5-18 1 Revenue recognition for a license agreement 60Trueblood Accounting Case 5-19 5 Revenue recognition for multiple-element contracts 45Real World Case 5-20 5 Revenue recognition; franchise sales; Jack in the Box 50Analysis Case 5-21 6 Evaluating profitability and asset management 60Judgment Case 5-22 6 Relationships among ratios, chapters 3 and 5 30Integrating Case 5-23 6 Using ratios, chapters 3 and 5 45

British Airways Case 7 IFRS, Multiple-deliverable contracts; British Airways 30

CPA Simulation 5-1 Installment sales method; percentage-of-completion method, franchise sales; research

5-40