normative 05 theories of accounting 1: the case of accounting for

TRANSCRIPT

156

Normative Theories of Accounting 1: The Case of Accounting for Changing Prices and Asset Values

05C H A P T E R

Upon completing this chapter readers should:

be aware of some particular v

limitations of historical cost accounting in terms of its ability to cope with various issues associated with changing prices and changing market conditions;be aware of a number of alternative v

methods of accounting that have been developed to address problems associated with changing prices

and market conditions in arriving at asset values, including fair value accounting;be able to identify some of the v

strengths and weaknesses of the various alternative accounting methods;understand that the calculation of v

income under a particular method of accounting will depend on the perspective of capital maintenance that has been adopted.

LEARNING OBJECTIVESv

dee26734_ch05.indd 156 1/21/2011 5:59:51 PM

5.1 Introduction 157

5.1 Introduction

In Chapter 3 we considered various theoretical explanations about why regulation might be put in place. Perspectives derived from public interest theory, capture theory

and the economic interest theory of regulation did not attempt to explain what form of regulation was most optimal or efficient. Rather, by adopting certain theoretical assumptions about individual behaviour and motivations, these theories attempted to explain which parties were most likely to try, and perhaps succeed in, affecting the regulatory process.

In this chapter we consider a number of normative theories of accounting. Based upon particular judgements about the types of information people need (which could be different from what they want), the various normative theories provide prescriptions about how the process of financial accounting should be undertaken.1

Positive theories, by contrast, attempt to explain and predict accounting practice without seeking to prescribe 1

particular actions. Positive accounting theories are the subject of analysis in Chapter 7.

Various asset valuation approaches are often adopted in the financial statements of large corporations. Non-current assets acquired (or perhaps revalued) in dif-

ferent years will simply be added together to give a total euro value, even though the various costs or valuations might provide little reflection of the current values of the respective assets. For example, pursuant to IAS 16 ‘Property, Plant and Equipment’ it is permissible for some classes of property, plant and equipment to be measured at cost, less a provision for depreciation, while other classes of property, plant and equipment may be measured at their current fair value (supposedly reflective of current market conditions). The different measurements are then simply added together to give a total value of property, plant and equipment – with the total neither representing cost nor fair value.

Issues to consider:What are some of the criticisms that can be made in relation to the practice n

of accounting wherein we add together, without adjustment, assets that have been acquired or valued in different years, when both the purchasing power of the euro and the market conditions that together give rise to valuations were conceivably quite different?What are some of the alternative methods of accounting (alternatives to historical n

cost accounting) that have been advanced to cope with the issue of changing prices and changing market conditions, and what acceptance have these alternatives received from the accounting profession?What are the strengths and weaknesses of the alternatives to historical cost? n

Opening issues

dee26734_ch05.indd 157 1/21/2011 5:59:51 PM

Chapter 05 Accounting for Changing Prices and Asset Values158

Across time, numerous normative theories of accounting have been developed by a number of well-respected academics. However, these theories have typically failed to be embraced by the accounting profession, or to be mandated within financial accounting regulations. Relying in part on material introduced in Chapter 3, we consider why some proposed methods of accounting are ultimately accepted by the profession and/or accounting standard-setters, while many are dismissed or rejected. We question whether the rejection is related to the merit of their arguments (or lack thereof), or due to the political nature of the standard-setting process wherein various vested interests and economic implications are considered. In this chapter we specifically consider various prescriptive theories of accounting (normative theories) that were advanced by various people on the basis that historical cost accounting has too many shortcomings, particularly in times of rising prices and changing market conditions. Some of these shortcomings were summarized by the International Accounting Standards Committee (which was subsequently replaced by the International Accounting Standards Board) in IAS 29 ‘Financial Reporting in Hyperinflationary Economies’:

In a hyperinflationary economy, reporting of operating results and financial position in the local currency without restatement is not useful. Money loses purchasing power at such a rate that comparison of amounts from transactions and other events that have occurred at different times, even within the same accounting period, is misleading. (paragraph 2)

5.2 Limitations of historical cost accounting in times of rising prices

Over time, criticisms of historical cost accounting have been raised by a number of notable scholars, particularly in relation to its inability to provide useful information

in times of rising prices and changing market conditions. For example, criticisms were raised by Sweeney, MacNeal, Canning and Paton in the 1920s and 1930s. From the 1950s the levels of criticism increased, with notable academics (such as Chambers, Sterling, Edwards and Bell) prescribing different models of accounting that they considered provided more useful information than was available under conventional historical cost accounting. Such work continued through to the early 1980s, but declined thereafter as levels of inflation throughout the world began to drop. Subsequently the debate changed to focus on the use of current market values – known as fair values – (supposedly reflecting current market conditions at the accounting date) for valuing assets, rather than amending historic costs simply to take account of inflation.2

Across time, these criticisms appear to have been accepted by accounting regulators – at least on a piecemeal basis. In recent years, for example, various accounting standards have been released that require or permit the application of fair values when measuring assets. These include: financial instruments (pursuant to IAS 39), property, plant and equipment (where the fair value model has been adopted pursuant to IAS 16 – this accounting standard

For example, there is a great deal of debate about whether stock (inventory) measurement rules (which require 2

inventory to be measured at the lower of cost and net realizable value pursuant to IAS 2) provide relevant information in situations where the market (fair) value of the inventory greatly exceeds its cost.

dee26734_ch05.indd 158 1/21/2011 5:59:51 PM

1595.2 Limitations of Historical Cost Accounting in Times of Rising Prices

gives financial statement preparers a choice between the cost model and the fair value model in the measurement of property, plant and equipment), some intangible assets (where there is an ‘active market’ pursuant to IAS 38), investment properties (pursuant to IAS 14), and biological assets (pursuant to IAS 41) that are required to be valued at fair value as opposed to historical cost.

Historical cost accounting assumes that money holds a constant purchasing power. As Elliot (1986, p. 33) states:

An implicit and troublesome assumption in the historical cost model is that the monetary unit is fixed and constant over time. However, there are three components of the modern economy that make this assumption less valid than it was at the time the model was developed.3

One component is specific price-level changes, occasioned by such things as technological advances and shifts in consumer preferences; the second compo-nent is general price-level changes (inflation); and the third component is the fluctuation in exchange rates for currencies. Thus, the book value of a company, as reported in its financial statements, only coincidentally reflects the current value of assets.

Again it is emphasized that under our current accounting standards many assets can or must be measured at historical cost. For example, inventory (or stock) must be measured at cost – or net realizable value if it is lower – and property plant and equipment can be valued at cost where an entity has adopted the ‘cost model’ for a class of property, plant and equipment pursuant to IAS 16. While there was much criticism of historical cost accounting during the high inflation periods of the 1970s and 1980s, there were also many who supported historical cost accounting. The method of accounting predominantly used today is still based on historical cost accounting, although the conceptual frameworks we discuss in the next chapter, and some recent accounting standards (as noted above), have introduced elements of current value – or fair value – measurements. Hence, the accounting profession and reporting entities have tended to maintain at least partial support for this historical cost approach.4 The very fact that historical cost accounting has continued to be applied by business entities has been used by a number of academics to support its continued use, which in a sense is a form of accounting-Darwinism perspective – the view that those things that are most efficient and effective will survive over time. For example, Mautz (1973) states:

Accounting is what it is today not so much because of the desire of account-ants as because of the influence of businessmen. If those who make man-agement and investment decisions had not found financial reports based on

As indicated in Chapter 2, the historical cost method of accounting was documented as early as 1494 by the 3

Franciscan monk Pacioli in his famous work Summa de Arithmetica, Geometrica, Proportioni et Proportionalita.

IAS 16 provides reporting entities with an option to adopt either the ‘cost model’ (measuring property, plant and 4

equipment at historical cost) or the ‘fair value model’ for measuring classes of property, plant and equipment. The ‘fair value model’ requires the revaluation of the assets to their fair value (which in itself means that a modified version of historical cost accounting can be used), which is one way to take account of changing values. Basing revised depreciation on the revalued amounts is one limited way of accounting for the effects of changing prices.

dee26734_ch05.indd 159 1/21/2011 5:59:51 PM

Chapter 05 Accounting for Changing Prices and Asset Values160

historical cost useful over the years, changes in accounting would long since have been made.5, 6

It has been argued (for example, Chambers, 1966) that historical cost accounting information suffers from problems of irrelevance in times of rising prices. That is, it is questioned whether it is useful to be informed that something cost a particular amount many years ago when its current value (as perhaps reflected by its replacement cost, or current market value) might be considerably different. It has also been argued that there is a real problem of additivity. At issue is whether it is really logical to add together assets acquired in different periods when those assets were acquired with euros of different purchasing power.7

In a number of countries, organizations are permitted to revalue their non-current assets. What often happens, however, is that different assets are revalued in different periods (with the local currency – for example dollars or euros – having different purchasing power in each period), yet the revalued assets might all be added together, along with assets that have continued to be valued at cost, for the purposes of disclosure in the statement of financial position (formerly known as the balance sheet).8

There is also an argument that methods of accounting that do not take account of changing prices, such as historical cost accounting, can tend to overstate profits in times of rising prices, and that distribution to shareholders of historical cost profits can actually lead to an erosion of operating capacity. For example, assume that a company commenced operations at the beginning of the year 2012 with €100,000 in inventory comprising 20,000 units at €5.00 each. If at the end of the year all the inventory had been sold, there were assets (cash) of €140,000 and throughout the year there had been no contributions from owners, no borrowings and no distributions to owners, then profit under a historical cost system would be €40,000. If the entire profit of €40,000 was distributed to owners

However, because something continues to be used does not mean that there is nothing else that might not be better. 5

This is a common error made by proponents of decision usefulness studies. Such studies attempt to provide either support for, or rejection of, something on the basis that particular respondents or users indicated that it would, or would not, be useful for their particular purposes. Often there are things that might be more ‘useful’ – but they are unknown by the respondents. As Gray et al. (1996, p. 75) state: ‘Decision usefulness purports to describe the central characteristics of accounting in general and financial statements in particular. To describe accounting as useful for decisions is no more illuminating than describing a screwdriver as being useful for digging a hole – it is better than nothing (and therefore “useful”) but hardly what one might ideally like for such a task.’

Reflective of the lack of agreement in the area, Elliot (1986) adopts a contrary view. Still relying upon metaphors 6

associated with evolution, Elliot (1986, p. 35) states: ‘There is growing evidence in the market place … that historical cost-basis information is of ever declining usefulness to the modern business world. The issue for the financial accounting profession is to move the accounting model toward greater relevance or face the fate of the dinosaur and the messenger pigeon.’

Again, under existing accounting standards, assets such as property, plant and equipment can be measured at fair 7

value or at cost. IAS 16 gives reporting entities the choice between applying the fair value model or the cost model to the different classes of property, plant and equipment. Hence, we are currently left with a situation where, even within a category of assets (for example, property, plant and equipment), some assets might be measured at cost while others might be measured at fair value.

In relation to property, plant and equipment, IAS 16 requires that where revaluations to fair value are undertaken, 8

the revaluations must be made with sufficient regularity to ensure that the carrying amount of each asset in the class does not differ materially from its fair value at the reporting date. Nevertheless, there will still be instances where some assets have not been revalued for three to five years but they will still be aggregated with assets that have been recently revalued.

dee26734_ch05.indd 160 1/21/2011 5:59:51 PM

1615.2 Limitations of Historical Cost Accounting in Times of Rising Prices

in the form of dividends, then the financial capital would be the same as it was at the beginning of the year. Financial capital would remain intact.9

However, if prices had increased throughout the period, then the actual operating capacity of the entity may not have remained intact. Let us assume that the company referred to above wishes to acquire another 20,000 units of inventory after it has paid €40,000 in dividends, but finds that the financial year-end replacement cost has increased to €5.40 per unit. The company will only be able to acquire 18,518 units with the €100,000 it still has available. By distributing its total historical cost profit of €40,000, with no adjustments being made for rising prices, the company’s ability to acquire goods and services has fallen from one period to the next. Some advocates of alternative approaches to accounting would prescribe that the profit of the period is more accurately recorded as €140,000, less 20,000 units at €5.40 per unit, which then equals €32,000. That is, if €32,000 is distributed to owners in dividends, the company can still buy the same amount of inventory (20,000 units) as it had at the beginning of the period – its purchasing power remains intact.10 Despite the problems associated with measuring inventory at historical cost, as illustrated above, organizations are still required to measure their inventory at cost (or net realizable value if it is lower than cost) pursuant to IAS 2.

In relation to the treatment of changing prices we can usefully, and briefly, consider IAS 41 ‘Agriculture’. IAS 41 provides the measurement rules for biological assets (for example, for grapevines or cattle). The accounting standard requires that changes in the fair value of biological assets from period to period be treated as part of the period’s profit or loss. In the development of the accounting standard there were arguments by some researchers (Roberts et al., 1995) that the increases in fair value associated with changing prices should be differentiated from changes in fair value that are due to physical changes (for example, changes in the size or number of the biological assets). The argument was that only the physical changes should be treated as part of profit or loss. Although IAS 41 treats the total change in fair value as part of income it is interesting to note that IAS 41 ‘encourages’ disclosures which differentiate between changes in the fair values of the biological assets which are based upon price changes and those based upon physical changes. As paragraph 51 of IAS 41 states:

The fair value less costs to sell of a biological asset can change due to both physi-cal changes and price changes in the market. Separate disclosure of physical and price changes is useful in appraising current period performance and future prospects, particularly when there is a production cycle of more than one year. In such cases, an entity is encouraged to disclose, by group or otherwise, the amount of the change in fair value less costs to sell included in profit or loss due

While it might be considered that measuring inventory at fair value would provide relevant information, IAS 2 9

‘Inventories’ prohibits the revaluation of inventory. Specifically, IAS 2 requires inventory to be measured at the lower of cost and net realizable value.

In some countries, such as the United States, an inventory cost flow assumption based on the last-in-first-out 10

(LIFO) method can be adopted (this cost flow assumption is not allowed under IAS 2). The effect of employing LIFO is that cost of goods sold will be determined on the basis of the latest cost, which in times of rising prices will be higher, thereby leading to a reduction in reported profits. This does provide some level of protection (although certainly not complete) against the possibility of eroding the real operating capacity of the organization.

dee26734_ch05.indd 161 1/21/2011 5:59:51 PM

Chapter 05 Accounting for Changing Prices and Asset Values162

to physical changes and due to price changes. This information is generally less useful when the production cycle is less than one year (for example, when rais-ing chickens or growing cereal crops).

In relation to the above disclosure guidance it is interesting to consider why the regulators considered that financial statement users would benefit from separate disclosure of price changes and physical changes in relation to agricultural assets when similar suggestions are not provided within other accounting standards relating to other categories of assets. This is somewhat inconsistent.

Returning to the use of historical cost in general, it has also been argued that historical cost accounting distorts the current year’s operating results by including in the current year’s income holding gains that actually accrued in previous periods.11 For example, some assets may have been acquired at a very low cost in a previous period (and perhaps in anticipation of future price increases pertaining to the assets), yet under historical cost accounting the gains attributable to such actions will only be recognized in the subsequent periods when the assets are ultimately sold. As an illustration, let us assume that a reporting entity acquired some land in 2004 for €1,000,000. Its fair value increased to €1,300,000 in 2008 and then €1,700,000 in 2011. A decision is made to sell the land in 2012 for its new fair value of €1,900,000. If the land had been measured at cost then the entire profit of €900,000 would be shown in the 2012 financial year even though the increase in fair value accrued throughout the previous eight years. Arguably placing all the gain in the last year’s profits distorts the results of that financial period as well as the results of preceding periods. Another potential problem of historical cost accounting is it can lead to a distortion of ‘return-on-asset’ measures. For example, consider an organization that acquired some machinery for €1 million and returned a profit of €100,000. Such an organization would have a return on assets of 10 per cent. If another organization later acquired the same type of asset for €2 million (due to rising prices) and generated a profit of €150,000, then on the basis of return on assets the second organization would appear less efficient, pursuant to historical cost accounting.

There is a generally accepted view that dividends should only be paid from profits (and this is enshrined within the corporations laws of many countries). However, one central issue relates to how we measure profits. There are various definitions of profits. One famous definition was provided by Hicks (1946), that is that profits (or ‘income’ as he referred to it) is the maximum amount that can be consumed during a period while still expecting to be as well off at the end of the period as at the beginning of the period. Any consideration of ‘well-offness’ relies upon a notion of capital maintenance – but which one? Different notions will provide different perspectives of profit.

There are a number of perspectives of capital maintenance. One version of capital maintenance is based on maintaining financial capital intact, and this is the position taken in historical cost accounting. Under historical cost accounting, dividends should normally only be paid to the extent that the payment will not erode financial capital, as illustrated in the earlier example of a company needing to replace 20,000 units of inventory where €40,000 is distributed to owners in the form of dividends and no adjustment is made to take account of changes in prices and the related impact on the purchasing power of the entity.

Holding gains are those that arise while an asset is in the possession of the reporting entity.11

dee26734_ch05.indd 162 1/21/2011 5:59:52 PM

1635.2 Limitations of Historical Cost Accounting in Times of Rising Prices

Another perspective of capital maintenance is one that aims at maintaining purchasing power intact.12 Under this perspective, historical cost accounts are adjusted for changes in the purchasing power of the euro (typically by use of the price index) which, in times of rising prices, will lead to a reduction in income relative to the income calculated under historical cost accounting. As an example, under general price level adjustment accounting (which we will consider more fully later in this chapter) the historical cost of an item is adjusted by multiplying it by the chosen price index at the end of the current period, divided by the price index at the time the asset was acquired. For example, if some land, which was sold for €1,200,000, was initially acquired for €1,000,000 when the price index was 100, and the price index at the end of the current period is 118 (reflecting an increase in prices of 18 per cent), then the adjusted cost would be €1,180,000. The adjusted profit would be €20,000 (compared to an historical cost profit of €200,000).13 What should be realized is that under this approach to accounting where adjustments are made by way of a general price index, the value of €1,180,000 will not necessarily (except due to chance) reflect the current market value of the land. Various assets will be adjusted using the same general price index.

Use of actual current values (as opposed to adjustments to historical cost using price indices) is made under another approach to accounting that seeks to provide a measure of profits which, if distributed, maintains physical operating capital intact. This approach to accounting (which could be referred to as current cost accounting) relies upon the use of current values, which could be based on present values, entry prices (for example, replacement costs) or exit prices.

Reflective of the attention that the impact of inflation was having on financial statements, Accounting Headline 5.1 reproduces an article that appeared in Accountancy in January 1974 (a period of high inflation – and a time when debate in this area of accounting was widespread). The impact of high levels of inflation continued into the early 1980s in many western nations and its continued impact on accounting information is reflected in Accounting Headline 5.2, which reproduces a further Accountancy article, this time from 1980.

In the discussion that follows we consider a number of different approaches to undertaking financial accounting in times of rising prices. This discussion is by no means exhaustive but does give some insight into some of the various models that have been prescribed by various parties.14

Gray 12 et al. (1996, p. 74) also provide yet another concept of capital maintenance – one that includes environmental capital. They state ‘it is quite a simple matter to demonstrate that company “income’’ contains a significant element of capital distribution – in this case “environmental capital’’. An essential tenet of accounting is that income must allow for the maintenance of capital. Current organizational behaviour clearly does not maintain environmental capital and so overstates earnings. If diminution of environmental capital is factored into the income figure it seems likely that no company in the western world has actually made any kind of a profit for many years.’ We will consider this issue further in Chapter 9.

Hence, if 13 €20,000 is distributed as dividends, the entity would still be in a position to acquire the same land that it

had at the beginning of the period (assuming that actual prices increased by the same amount as the particular price index used).

For example, we will not be considering one approach to determining income based on present values which did 14

not have wide support, but would be consistent with Hicks’ income definition (and which might be considered as a true income approach). A present value approach would determine the discounted present value of the firm’s assets and liabilities and use this as the basis for the financial statements. Under such an approach the calculated value of assets will depend upon various expectations, such as expectations about the cash flows the asset would return through its use in production (its value in use) or its current market value (value in exchange). Such an approach relies upon many assumptions and judgements, including the determination of the appropriate discount rate. Under a present value approach to accounting, profit would be determined as the amount that could be withdrawn, yet maintain the present value of the net assets intact from one period to the next.

dee26734_ch05.indd 163 1/21/2011 5:59:52 PM

Chapter 05 Accounting for Changing Prices and Asset Values164

Accounting Headline 5.2

The need for accounting for changing prices

… as the president of the Institute [of

Chartered Accountants in England and

Wales], David Richards FCA, made clear at

the annual dinner of the Nottingham Society

of Charted Accountants on 14 March …

[that] useful as it may be, ‘historic cost

accounting has an unfortunate tranquillising

side-effect in not a few boardrooms. The

SSSP 16 – a standard for all

Accounting Headline 5.1

An insight into some professional initiatives in the area

of accounting for changing pricesCPP accounting – an end or a beginning?

There are two methods of inflation

accounting, current purchasing power

[CPP] accounting and replacement cost

accounting [RCA], and the relative merits

of the two were elaborated and discussed

throughout [a] day-long conference,

organised and jointly sponsored by

the English Institute [of Chartered

Accountants] and the Financial Times.

After an introduction by the chairman,

Sir Ronald Leach CBE FCA (also chairman

of the Accounting Standards Steering

Committee), in which he outlined

the compromise reached between the

Government and the Institute on the

production of a provisional [accounting]

standard for inflation accounting, Chris

Westwick presented his case for the use

of CPP accounting. Current purchasing

power accounting involves substitution

of the current pound in the accounts,

whereas replacement cost accounting

utilises revaluation of the company’s

assets on the basis of their replacement

cost. Mr Westwick felt CPP accounting

would provide more information to the

shareholder, being concerned with the

maintenance of the shareholders’ capital

rather than the maintenance of physical

assets (as in the RCA method), and therefore

would be the more suitable technique

to employ. He said that RCA placed too

much importance on the business of the

company, and not enough on making

money for shareholders, also tending to

ignore the gain on long-term money.

The second speaker was R. S. Allen,

a director of J. A. Scrimgeour and a council

member of the society of investment

analysts; he likened CPP accounting

to Esperanto – conceived in idealism

but not practicable; he was, needless

to say, putting the other point of view.

Mr Allen favoured the RCA method as

something within the shareholder’s grasp,

but also acceptable to management and

appropriate, since inflation increases the

value of assets.

Source: Accountancy, January 1974, p. 6.

dee26734_ch05.indd 164 1/21/2011 5:59:56 PM

1655.3 Current Purchasing Power Accounting

historic cost figures often look good – on

paper – and they tend to induce a boardroom

euphoria. It is only when these figures are

adjusted for the effects of a diminishing

pound that the more realistic picture of

past performance of the company begins to

emerge.’Arguably, current cost accounting, and a

general awareness of the effects of inflation,

are, if anything, more important to the small

organisation than to the large. After the best

part of a decade of high-level inflation,

there is little excuse for the medium to large

company being unaware of the problem,

or lacking trained accounting staff to

highlight it.

Source: Accountancy, April 1980, p. 1.

5.3 Current purchasing power accounting

Current purchasing power (CPP) accounting (or as it is also called, general purchasing power accounting, general price level accounting, or constant dollar/euro accounting)

can be traced to the early works of such authors as Sweeney (1964, but originally published in 1936) and has since been favoured by a number of other researchers. CPP accounting has also, at various times, been supported by professional accounting bodies throughout the world, but more in the form of supplementary disclosures to accompany financial statements prepared under historical cost accounting principles. CPP accounting was developed on the basis of a view that, in times of rising prices, if an entity were to distribute unadjusted profits based on historical costs the result could be a reduction in the real value of an entity – that is, in real terms the entity could risk distributing part of its capital (as we saw in an earlier example).

In considering the development of accounting for changing prices, the majority of research initially related to restating historical costs to account for changing prices by using historical cost accounts as the basis, but restating the accounts by use of particular price indices. This is the approach we consider in this section of the chapter. The literature then tended to move towards current cost accounting (which we consider later in this chapter), which changed the basis of measurement to current values as opposed to restated historical values. Consistent with this trend, the accounting profession initially tended to favour price-level-adjusted accounts (using indices), but then tended to switch to current cost accounting which required the entity to find the current values of the individual assets held by the reporting entity.15, 16

CPP accounting, with its reliance on the use of indices, is generally accepted as being easier and less costly to apply than methods that rely upon current valuations of particular

Current values could be based on 15 entry or exit prices. As we will see, there is much debate as to which ‘current’ value is most appropriate.

Professional support for the use of replacement costs appeared to heighten around the time of the 1976 release of 16

ASR 190 within the United States.

dee26734_ch05.indd 165 1/21/2011 5:59:58 PM

Chapter 05 Accounting for Changing Prices and Asset Values166

From the above data we can see that prices have increased. The price index in the base year is frequently given a value of 100 and it is also frequently assumed that consumption

Commodity A Commodity B Commodity CYear Price € Quantity Price € Quantity Price € Quantity

Base year (2012) 10.00 100 15.00 200 20.00 250

2013 12.00 15.50 21.20

assets.17 It was initially considered by some people that it would be too costly and perhaps unnecessary to attempt to find current values for all the individual assets. Rather than considering the price changes of specific goods and services, it was suggested on practical grounds that price indices be used.

Calculating indicesWhen applying general price level accounting, a price index must be applied. A price index is a weighted average of the current prices of goods and services relative to a weighted average of prices in a prior period, often referred to as a base period. Price indices may be broad or narrow – they may relate to changes in prices of particular assets within a particular industry (a specific price index), or they might be based on a broad cross-section of goods and services that are consumed (a general price index, such as a Consumer Price Index (CPI) or Retail Price Index (RPI)).

But which price indices should be used? Should we use changes in a general price index (for example, as reflected in the UK by the CPI or RPI) or should we use an index that is more closely tied to the acquisition of production-related resources? There is no clear answer. From the shareholders’ perspective the CPI or RPI may more accurately reflect their buying pattern – but prices will not change by the same amount for shareholders in different locations. Further, not everybody will have the same consumption patterns as is assumed when constructing a particular index. The choice of an index can be very subjective. Where CPP accounting has been recommended by particular professional bodies, CPI/RPI-type indices have been suggested.

Because CPP relies upon the use of price indices, it is useful to consider how such indices are constructed. To explain one common way that indices may be constructed we can consider the following example which is consistent with how the UK Consumer Price Index is determined. Let us assume that there are three types of commodities (A, B and C) that are consumed in the following base year quantities and at the following prices:

However, many questions can be raised with regard to what the restated value actually represents after being 17

multiplied by an index such as the general rate of inflation. This confusion is reflected in studies that question the relevance of information restated for changes in purchasing power.

dee26734_ch05.indd 166 1/21/2011 5:59:58 PM

1675.3 Current Purchasing Power Accounting

quantities (or proportions between the different commodities) thereafter remain the same, such that the price index at the end of year 2011 would be calculated as:

10012 00 100 15 50 200 21 2010 00 100 15 00×

× + × + ×× + ×

( . ) ( . ) ( .( . ) ( .

250)2200) (20.00 250)+ × = 106 67100.

From the above calculations we can see that the prices within this particular ‘bundle’ of goods have been calculated as rising on average by 6.67 per cent from the year 2012 to the year 2013. The reciprocal of the price index represents the change in general purchasing power across the period. For example, if the index increased from 100 to 106.67, as in the above example, the purchasing power of the euro would be 93.75 per cent (100/106.67) of what it was previously. That is, the purchasing power of the euro has decreased.

Performing current purchasing power adjustmentsWhen applying CPP, all adjustments are done at the end of the period, with the adjustments being applied to accounts prepared under the historical cost convention. When considering changes in the value of assets as a result of changes in the purchasing power of money (due to inflation) it is necessary to consider monetary assets and non-monetary assets separately. Monetary assets are those assets that remain fixed in terms of their monetary value, for example cash and claims to a specified amount of cash (such as trade debtors and investments that are redeemable for a set amount of cash). These assets will not change their monetary value as a result of inflation. For example, if we are holding €10 in cash and there is rapid inflation, we will still be holding €10 in cash, but the asset’s purchasing power will have decreased over time.

Non-monetary assets can be defined as those assets whose monetary equivalents will change over time as a result of inflation, and would include such things as plant and equipment and inventory. For example, inventory may cost €100 at the beginning of the year, but the same inventory could cost, say, €110 at the end of the year due to inflation. Relative to monetary assets, the purchasing power of non-monetary assets is assumed to remain constant even in the presence of inflation.

Most liabilities are fixed in monetary terms (there is an obligation to pay a pre-specified amount of cash at a particular time in the future independent of the change in the purchasing power of the particular currency) and hence liabilities would typically be considered as monetary items (monetary liabilities). Non-monetary liabilities, on the other hand, although less common, would include obligations to transfer goods and services in the future, items which could change in terms of their monetary equivalents.

Net monetary assets would be defined as monetary assets less monetary liabilities. In times of inflation, holders of monetary assets will lose in real terms as a result of holding the monetary assets, as the assets will have less purchasing power at the end of the period relative to what they had at the beginning of the period (and the greater the level of general price increases, the greater the losses). Conversely, holders of monetary liabilities will gain, given that the amount they have to repay at the end of the period will be worth less (in terms of purchasing power) than it was at the beginning of the period.

Let us consider an example to demonstrate how gains and losses might be calculated on monetary items (and under CPP, gains and losses will relate to net monetary assets rather

dee26734_ch05.indd 167 1/21/2011 5:59:58 PM

Chapter 05 Accounting for Changing Prices and Asset Values168

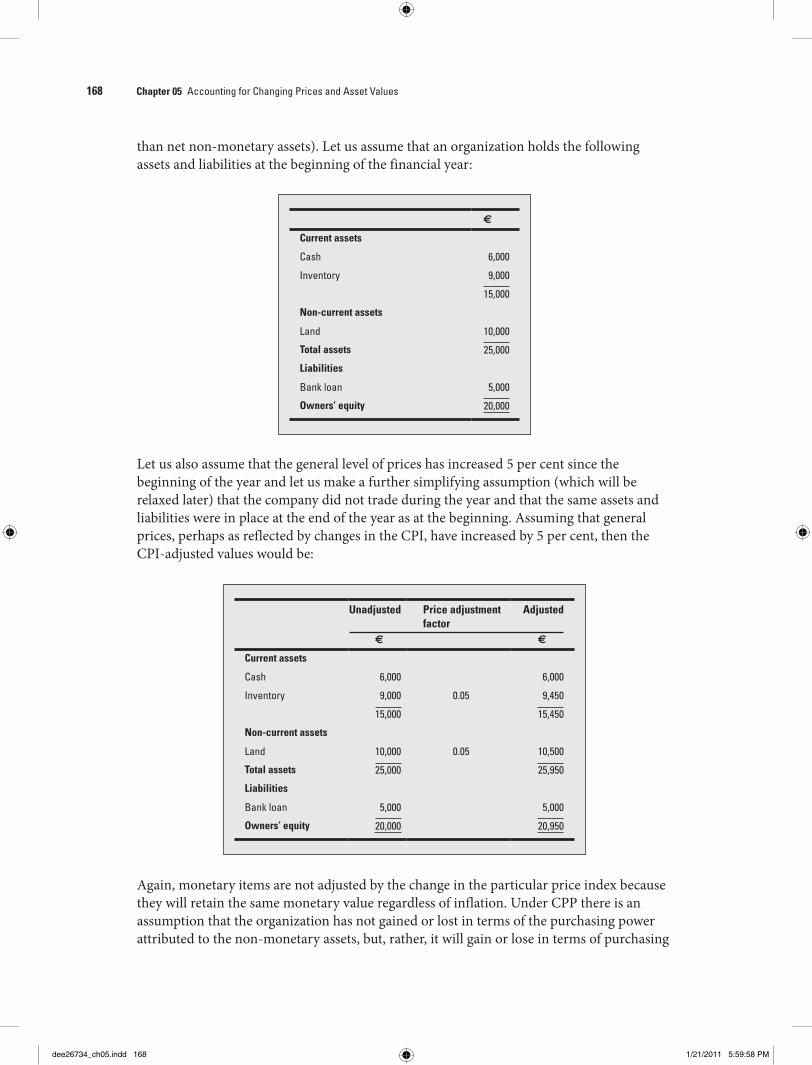

than net non-monetary assets). Let us assume that an organization holds the following assets and liabilities at the beginning of the financial year:

€

Current assets

Cash 6,000

Inventory 9,000

15,000

Non-current assets

Land 10,000

Total assets 25,000

Liabilities

Bank loan 5,000

Owners’ equity 20,000

Let us also assume that the general level of prices has increased 5 per cent since the beginning of the year and let us make a further simplifying assumption (which will be relaxed later) that the company did not trade during the year and that the same assets and liabilities were in place at the end of the year as at the beginning. Assuming that general prices, perhaps as reflected by changes in the CPI, have increased by 5 per cent, then the CPI-adjusted values would be:

Unadjusted Price adjustment factor

Adjusted

€ €

Current assets

Cash 6,000 6,000

Inventory 9,000 0.05 9,450

15,000 15,450

Non-current assets

Land 10,000 0.05 10,500

Total assets 25,000 25,950

Liabilities

Bank loan 5,000 5,000

Owners’ equity 20,000 20,950

Again, monetary items are not adjusted by the change in the particular price index because they will retain the same monetary value regardless of inflation. Under CPP there is an assumption that the organization has not gained or lost in terms of the purchasing power attributed to the non-monetary assets, but, rather, it will gain or lose in terms of purchasing

dee26734_ch05.indd 168 1/21/2011 5:59:58 PM

1695.3 Current Purchasing Power Accounting

power changes attributable to its holdings of the net monetary assets. In the above example, to be as ‘well off ’ at the end of the period the entity would need €21,000 in net assets (which equals €20,000 × 1.05) to have the same purchasing power as it had one year earlier (given the general increase in prices of 5 per cent). In terms of end-of-year euros, in the above illustration the entity is €50 worse off in adjusted terms (it only has net assets with an adjusted value of €20,950, which does not have the same purchasing power as €20,000 did at the beginning of the period). As indicated above, this €50 loss relates to the holdings of net monetary assets and not to the holding of non-monetary assets, and is calculated as the balance of cash, less the balance of the bank loan, multiplied by the general price level increase. That is, (€6,000 - €5,000) × 0.05. If the monetary liabilities had exceeded the monetary assets throughout the period, a purchasing power gain would have been recorded. If the amount of monetary assets held was the same as the amount of monetary liabilities held, then no gain or losses would result.

Again, it is stressed that under CPP no change in the purchasing power of the entity is assumed to arise as a result of holding non-monetary assets. Under general price level accounting, non-monetary assets are restated to current purchasing power and no gain or loss is recognized. Purchasing power losses (or gains) arise only as a result of holding net monetary assets. As noted at paragraph 7 of Provisional Statement of Standard Accounting Practice 7 (PSSAP 7), issued in the United Kingdom in 1974:

Holders of non-monetary assets are assumed neither to gain nor to lose purchas-ing power by reason only of inflation as changes in the prices of these assets will tend to compensate for any changes in the purchasing power of the pound.

An important issue to consider is how the purchasing power gains and losses should be treated for income purposes. Should they be treated as part of the period’s profit or loss, or should they be transferred directly to a reserve? Generally, where this method of accounting has been recommended it has been advised that the gain or loss should be included in income. Such recommendations are found in the US Accounting Research Bulletin No. 6 (issued in 1961); in the Accounting Principles Board (APB) Statement No. 3 (issued in 1969 by the American Institute of Certified Public Accountants (AICPA)); in the Financial Accounting Standards Board’s (FASB) Exposure Draft entitled ‘Financial Reporting in Units of General Purchasing Power’; and within Provisional Statement of Accounting Practice No. 7 issued by the Accounting Standards Steering Committee (UK) in 1974.

As a further example of calculating gains or losses in purchasing power pertaining to monetary items, let us assume four quarters with the following CPI index figures:

At the beginning of the year 120

At the end of the first quarter 125

At the end of the second quarter 130

At the end of the third quarter 132

At the end of the fourth quarter 135

dee26734_ch05.indd 169 1/21/2011 5:59:58 PM

Chapter 05 Accounting for Changing Prices and Asset Values170

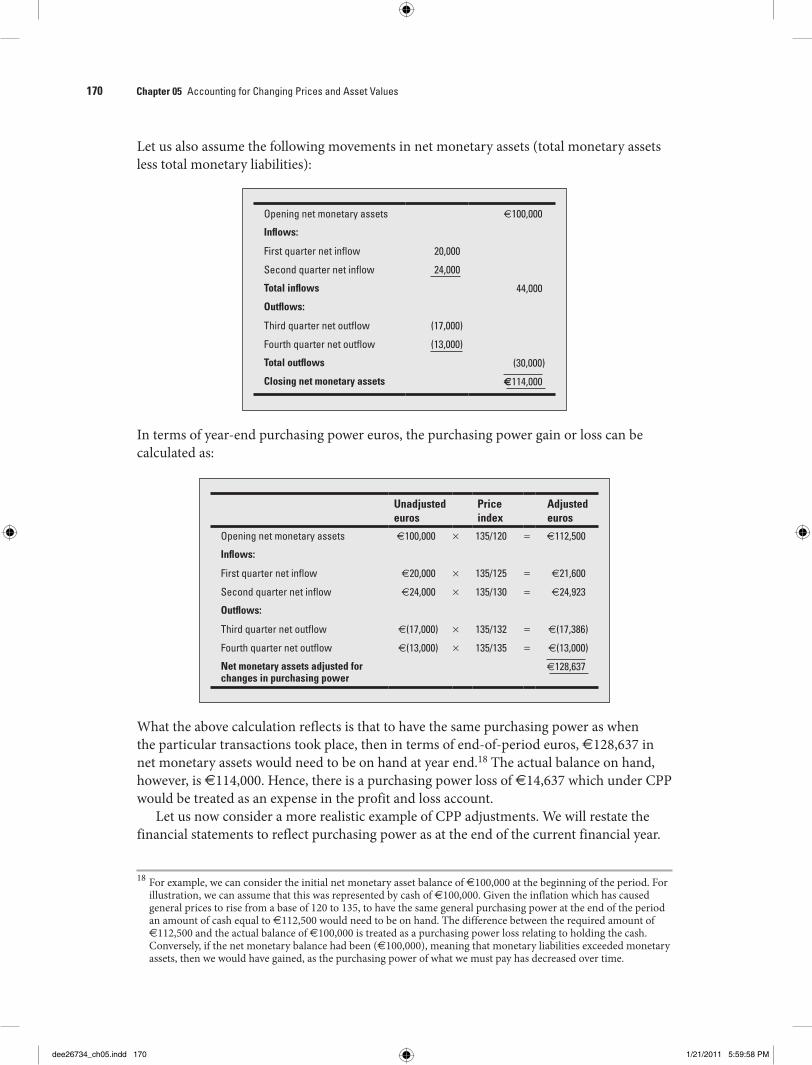

Let us also assume the following movements in net monetary assets (total monetary assets less total monetary liabilities):

Opening net monetary assets €100,000

Inflows:

First quarter net inflow 20,000

Second quarter net inflow 24,000

Total inflows 44,000

Outflows:

Third quarter net outflow (17,000)

Fourth quarter net outflow (13,000)

Total outflows (30,000)

Closing net monetary assets €114,000

In terms of year-end purchasing power euros, the purchasing power gain or loss can be calculated as:

What the above calculation reflects is that to have the same purchasing power as when the particular transactions took place, then in terms of end-of-period euros, €128,637 in net monetary assets would need to be on hand at year end.18 The actual balance on hand, however, is €114,000. Hence, there is a purchasing power loss of €14,637 which under CPP would be treated as an expense in the profit and loss account.

Let us now consider a more realistic example of CPP adjustments. We will restate the financial statements to reflect purchasing power as at the end of the current financial year.

For example, we can consider the initial net monetary asset balance of 18 €100,000 at the beginning of the period. For

illustration, we can assume that this was represented by cash of €100,000. Given the inflation which has caused general prices to rise from a base of 120 to 135, to have the same general purchasing power at the end of the period an amount of cash equal to €112,500 would need to be on hand. The difference between the required amount of €112,500 and the actual balance of €100,000 is treated as a purchasing power loss relating to holding the cash. Conversely, if the net monetary balance had been (€100,000), meaning that monetary liabilities exceeded monetary assets, then we would have gained, as the purchasing power of what we must pay has decreased over time.

Unadjusted euros

Price index

Adjusted euros

Opening net monetary assets €100,000 × 135/120 = €112,500

Inflows:

First quarter net inflow €20,000 × 135/125 = €21,600

Second quarter net inflow €24,000 × 135/130 = €24,923

Outflows:

Third quarter net outflow €(17,000) × 135/132 = €(17,386)

Fourth quarter net outflow €(13,000) × 135/135 = €(13,000)

Net monetary assets adjusted for changes in purchasing power

€128,637

dee26734_ch05.indd 170 1/21/2011 5:59:58 PM

1715.3 Current Purchasing Power Accounting

CPP plc income statement for year ended 31 December 2012Sales revenue 200,000

Less:

Cost of goods sold

Opening inventory 25,000

Purchases 110,000

135,000

Closing inventory 35,000 100,000

Gross profit 100,000

Other expenses

Administrative expenses 9,000

Interest expense 1,000

Depreciation 9,000 19,000

Operating profit before tax 81,000

Tax 26,000

Operating profit after tax 55,000

Opening retained earnings 0

Dividends proposed 15,000

Closing retained earnings 40,000

Let us assume that the entity commenced operation on 1 January 2012 and the unadjusted statement of financial position (or balance sheet) is as follows:

CPP plc statement of financial position as at 1 January 2012

Current assets

Cash 10,000

Inventory 25,000 35,000

Non-current assets

Plant and equipment 90,000

Land 75,000 165,000

Total assets 200,000

Current liabilities

Bank overdraft 10,000

Non-current liabilities

Bank loan 10,000

Total liabilities 20,000Net assets 180,000

Represented by:

Shareholders’ funds

Paid up capital 180,000

As a result of its operations for the year, CPP plc had the historical cost income statement (profit and loss account) and balance sheet at year end as shown below:

dee26734_ch05.indd 171 1/21/2011 5:59:58 PM

Chapter 05 Accounting for Changing Prices and Asset Values172

As we have already stated, under CPP gains or losses only occur as a result of holding net monetary assets. To determine the gain or loss, we must consider the movements in the net monetary assets. For example, if the organization sold inventory during the year, this will ultimately impact on cash. However, over time, the cash will be worth less in terms of its ability to acquire goods and services, hence there will be a purchasing power loss on the cash that was received during the year. Conversely, expenses will decrease cash during the year. In times of rising prices, more cash would be required to pay for the expense, hence in a sense we gain in relation to those expenses that were incurred earlier in the year (the logic being that if the expenses were incurred later in the year, more cash would have been required).

We must identify changes in net monetary assets from the beginning of the period until the end of the period.

CPP plc statement of financial position as at 31 December 2012

Current assets

Cash 100,000

Trade debtors 20,000

Inventory 35,000 155,000

Non-current assets

Plant and equipment 90,000

Accumulated depreciation (9,000)

Land 75,000 156,000

Total assets 311,000

Current liabilities

Bank overdraft 10,000

Trade creditors 30,000

Tax payable 26,000

Provision for dividends 15,000

81,000

Non-current liabilities

Bank loan 10,000

Total liabilities 91,000

Net assets 220,000

Represented by:

Shareholders’ funds

Paid up capital 180,000

Retained earnings 40,000

220,000

dee26734_ch05.indd 172 1/21/2011 5:59:59 PM

1735.3 Current Purchasing Power Accounting

Movement in net monetary assets from 1 January 2012 to 31 December 2012 1 January 2012 31 December 2012

Monetary assets

Cash 10,000 100,000

Trade debtors 20,000

10,000 120,000

Less:

Monetary liabilities

Bank overdraft 10,000 10,000

Trade creditors 30,000

Tax payable 26,000

Provision for dividends 15,000

Bank loan 10,000 10,000

Net monetary assets (10,000) 29,000

To determine any adjustments in CPP plc we must identify the reasons for the change in net monetary assets.

Reconciliation of opening and closing net monetary assets

Opening net monetary assets (10,000)

Sales 200,000

Purchase of goods (110,000)

Payment of interest (1,000)

Payment of administrative expenses (9,000)

Tax expense (26,000)

Dividends (15,000)

Closing net monetary assets 29,000

What we need to determine is whether, had all the transactions taken place at year end, the company would have had to transfer the same amount, measured in monetary terms, as it actually did. Any payments to outside parties throughout the period would have required a greater payment at the end of the period if the same items were to be transferred. Any receipts during the year will, however, be worth less in purchasing power.

To adjust for changes in purchasing power we need to have details about how prices have changed during the period, and we also need to know when the actual changes took place. We make the following assumptions:

The interest expense and administrative expenses were incurred uniformly throughout n

the year.The tax liability did not arise until year end. n

dee26734_ch05.indd 173 1/21/2011 5:59:59 PM

Chapter 05 Accounting for Changing Prices and Asset Values174

31 December 2012 140

Average for the year 135

Average for first quarter 132

Average for second quarter 135

Average for third quarter 137

Average for fourth quarter 139

Unadjusted Index Adjusted

Opening net monetary assets (10,000) 140/130 (10,769)

Sales 200,000 140/135 207,407

Purchase of goods (110,000) 140/135 (114,074)

Payment of interest (1,000) 140/135 (1,037)

Payment of administrative expenses (9,000) 140/135 (9,333)

Tax expense (26,000) 140/140 (26,000)

Dividends (15,000) 140/140 (15,000)

Closing net monetary assets 29,000 31,194

The difference between €29,000 and the amount of €31,194 represents a loss of €2,194. It is considered to be a loss, because to have the same purchasing power at year end as when the entity held the particular net monetary assets, the entity would need the adjusted amount of €31,194, rather than the actual amount of €29,000. This loss of €2,194 will appear as a ‘loss on purchasing power’ in the price-level-adjusted income statement (see below).

The dividends were declared at the end of the year. n

The inventory on hand at year end was acquired in the last quarter of the year. n

Purchases of inventory occurred uniformly throughout the year. n

Sales occurred uniformly throughout the year. n

We also assume that the price level index at the beginning of the year was 130. Subsequent indices were as follows:

Rather than using price indices as at the particular dates of transactions (which would generally not be available) it is common to use averages for a particular period.

From the above balance sheet we can again emphasize that the non-monetary items are translated into euros of year-end purchasing power, whereas the monetary items are already stated in current purchasing power euros, and hence no changes are made to the reported balances of monetary assets.

One main strength of CPP is its ease of application. The method relies on data that would already be available under historical cost accounting and does not require the

dee26734_ch05.indd 174 1/21/2011 5:59:59 PM

1755.3 Current Purchasing Power Accounting

Price-level-adjusted income statement for year ended 31 December 2012

Sales revenue 200,000 140/135 207,407Less Cost of goods sold Opening inventory 25,000 140/130 26,923Purchases 110,000 140/135 114,074 135,000 140,997Closing inventory 35,000 140/139 35,252

100,000 105,745Gross profit 100,000 101,662Other expenses Administrative expenses 9,000 140/135 9,333Interest expense 1,000 140/135 1,037Depreciation 9,000 140/130 9,692

19,000 20,062Operating profit before tax 81,000 81,600Tax 26,000 140/140 26,000Operating profit after tax 55,000 55,600Loss on purchasing power 2,194

53,406Opening retained earnings 0 0Dividends proposed 15,000 140/140 15,000Closing retained earnings 40,000 38,406

Price-level-adjusted statement of financial position as at 31 December 2012

Current assets Cash 100,000 100,000Trade debtors 20,000 20,000Stock 35,000 140/139 35,252Total current assets 155,000 155,252Non-current assets Plant and equipment 90,000 140/130 96,923Accumulated depreciation (9,000) 140/130 (9,692)Land 75,000 140/130 80,769Total non-current assets 156,000 168,000Total assets 311,000 323,252Current liabilities Bank overdraft 10,000 10,000Trade creditors 30,000 30,000Tax payable 26,000 26,000Provision for dividends 15,000 15,000Non-current liabilities Bank loan 10,000 10,000Total liabilities 91,000 91,000Net assets 220,000 232,252Represented by: Shareholders’ funds Paid up capital 180,000 140/130 193,846Retained earnings 40,000 38,406

220,000 232,252

dee26734_ch05.indd 175 1/21/2011 5:59:59 PM

Chapter 05 Accounting for Changing Prices and Asset Values176

5.4 Current cost accounting

Current cost accounting (CCA) was one of the various alternatives to historical cost accounting that tended to gain the most acceptance. Notable advocates of this

approach have included Paton (1922), and Edwards and Bell (1961). Such authors decided to reject historical cost accounting and CPP in favour of a method that considered actual valuations. As we will see, unlike historical cost accounting, CCA differentiates between profits from trading and those gains that result from holding an asset.

Holding gains can be considered as realized or unrealized. If a financial capital maintenance perspective is adopted with respect to the recognition of income, then holding gains or losses can be treated as income. Alternatively, they can be treated as capital adjustments if a physical capital maintenance approach is adopted.19 Some versions of CCA, such as that proposed by Edwards and Bell, adopt a physical capital maintenance approach to income recognition. In this approach, which determines valuations on the basis of replacement costs,20 operating income represents realized revenues, less the replacement cost of the assets in question. It is considered that this generates a measure of income which represents the maximum amount that can be distributed, while maintaining operating capacity intact. For example, assume that an entity acquired 150 items of

In some countries non-current assets can be revalued upward by way of an increase in the asset account and an 19

increase in a reserve, such as a revaluation reserve. This increment is typically not treated as income and therefore the treatment is consistent with a physical capital maintenance approach to income recognition (this approach is embodied within IAS 16 as it relates to property, plant and equipment, and within IAS 38 as it relates to intangible assets).

We will also see later in this chapter that there are alternative approaches to current cost accounting that rely upon 20

exit (sales) prices.

reporting entity to incur the cost or effort involved in collecting data about the current values of the various non-monetary assets. CPI (or RPI) data would also be readily available. However, and as indicated previously, movements in the prices of goods and services included in a general price index might not be reflective of price movements involved in the goods and services involved in different industries. That is, different industries may be affected differently by inflation.

Another possible limitation is that the information generated under CPP might actually be confusing to users. They might consider that the adjusted amounts reflect the specific value of specific assets (and this is a criticism that can also be made of historical cost information). However, as the same index is used for all assets this will rarely be the case. Another potential limitation that we consider at the end of the chapter is that various studies (which have looked at such things as movements in share prices around the time of disclosure of CPP information) have failed to find much support for the view that the data generated under CPP are relevant for decision-making (the information when released caused little if any share price reaction).

Following the initial acceptance of CPP in some countries in the 1970s, there was a move towards methods of accounting that used actual current values. Support for CPP declined. We will now consider such approaches.

dee26734_ch05.indd 176 1/21/2011 5:59:59 PM

1775.4 Current Cost Accounting

inventory at a cost of €10.00 each and sold 100 of the items for €15 each when the replacement cost to the entity was €12 each. We will also assume that the replacement cost of the 50 remaining items of inventory at year end was €14. Under the Edwards and Bell approach the operating profit that would be available for dividends would be €300, which is 100 × (€15 - €12). There would be a realized holding gain on the goods that were sold, which would amount to 100 × (€12 - €10), or €200, and there would be an unrealized holding gain in relation to closing inventory of 50 × (€14 - €10), or €200. Neither the realized nor the unrealized holding gain would be considered to be available for dividend distribution.21

In undertaking CCA, adjustments are usually made at the year-end using the historical cost accounts as the basis of adjustments. If we adopt the Edwards and Bell approach to profit calculation, operating profit is derived after ensuring that the operating capacity of the organization is maintained intact. Edwards and Bell believe operating profit is best calculated by using replacement costs.22, 23 As noted above, in calculating operating profit, gains that accrue from holding an asset (holding gains) are excluded and are not made available for dividends – although they are included when calculating what is referred to as business profit. For example, if an entity acquired goods for €20 and sold them for €30, then business profit would be €10, meaning that €10 could be distributed and still leave financial capital intact (this would be the approach taken in historical cost accounting). But if the replacement cost to the entity of the goods at the time they were sold was €23, then €3 would be considered a holding gain, and to maintain physical operating capacity only €7 could be distributed – current cost operating profit would be €7. No adjustment is made to sales revenue. This €7 distribution can be compared to what could be distributed under historical cost accounting. Because historical costs accounting adopts a financial capital maintenance approach, €10 could be distributed in dividends thereby maintaining financial capital (but nevertheless causing an erosion in the operating ability of the organization).

In relation to non-current assets, for the purposes of determining current cost operating profit, depreciation is based on the replacement cost of the asset. For example, if an item of machinery was acquired at the beginning of 2012 for €100,000 and had a projected life of 10 years and no salvage value, then assuming the straight-line method of depreciation is used, its depreciation expense under historical cost accounting would be €10,000 per year. If at the end of 2012 its replacement cost had increased to €120,000, then under current cost accounting a further €2,000 would be deducted to determine current cost operating profit. However, this €2,000 would be treated as a realized cost

Comparing this approach to income calculations under historical cost accounting we see that if we add CCA 21

operating profit of €300 and the realized holding gain of €200, then this will give the same total as we would have calculated for income under historical cost accounting.

In a sense, the Edwards and Bell approach represents a ‘true income’ approach to profit calculation. They believe 22

that profit can only be correctly measured (that is, ‘be true’) after considering the various asset replacement costs.

Those who favour a method of income calculation that requires a maintenance of financial capital (advocates 23

of historical cost accounting) treat holding gains as income, while those who favour a maintenance of physical capital approach to income determination (such as Edwards and Bell) tend to exclude holding gains from income. A physical capital perspective was adopted by most countries in their professional releases pertaining to CCA.

dee26734_ch05.indd 177 1/21/2011 5:59:59 PM

Chapter 05 Accounting for Changing Prices and Asset Values178

saving (because historical cost profits would have been lower if the entity had not already acquired the asset) and would be recognized in business profit (it would be added back below operating profit) and the other €18,000 would be treated as an unrealized cost saving and would also be included in business profit. As with CPP, no restatement of monetary assets is required as they are already recorded in current euros and hence in terms of end-of-period purchasing power euros.

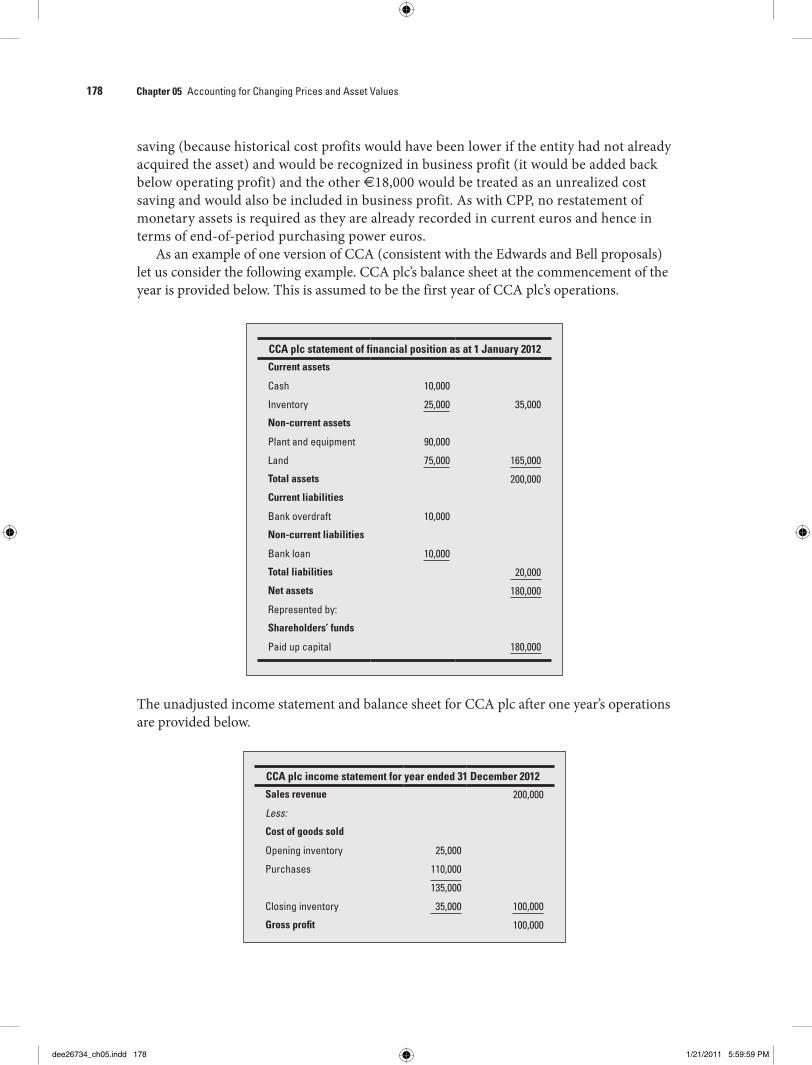

As an example of one version of CCA (consistent with the Edwards and Bell proposals) let us consider the following example. CCA plc’s balance sheet at the commencement of the year is provided below. This is assumed to be the first year of CCA plc’s operations.

The unadjusted income statement and balance sheet for CCA plc after one year’s operations are provided below.

CCA plc income statement for year ended 31 December 2012

Sales revenue 200,000

Less:

Cost of goods sold

Opening inventory 25,000

Purchases 110,000

135,000

Closing inventory 35,000 100,000

Gross profit 100,000

CCA plc statement of financial position as at 1 January 2012

Current assets

Cash 10,000

Inventory 25,000 35,000

Non-current assets

Plant and equipment 90,000

Land 75,000 165,000

Total assets 200,000

Current liabilities

Bank overdraft 10,000

Non-current liabilities

Bank loan 10,000

Total liabilities 20,000

Net assets 180,000

Represented by:

Shareholders’ funds

Paid up capital 180,000

dee26734_ch05.indd 178 1/21/2011 5:59:59 PM

1795.4 Current Cost Accounting

Other expenses

Administrative expenses 9,000

Interest expense 1,000

Depreciation 9,000 19,000

Operating profit before tax 81,000

Tax 26,000

Operating profit after tax 55,000

Opening retained earnings 0

Dividends proposed 15,000

Closing retained earnings 40,000

We will assume that the inventory on hand at the year-end comprised 3,500 units that cost €10 per unit. The replacement cost at year end was €11.00 per unit. We will also assume that the replacement cost of the units actually sold during the year was €105,000

CCA plc statement of financial position as at 31 December 2012

Current assets

Cash 100,000

Trade debtors 20,000

Inventory 35,000 155,000

Non-current assets

Plant and equipment 90,000

Accumulated depreciation (9,000)

Land 75,000 156,000

Total assets 311,000

Current liabilities

Bank overdraft 10,000

Trade creditors 30,000

Tax payable 26,000

Provision for dividends 15,000

81,000

Non-current liabilities

Bank loan 10,000

Total liabilities 91,000

Net assets 220,000

Represented by:

Shareholders’ funds

Paid up capital 180,000

Retained earnings 40,000

220,000

dee26734_ch05.indd 179 1/21/2011 5:59:59 PM

Chapter 05 Accounting for Changing Prices and Asset Values180

(as opposed to the historical cost of €100,000) and that the year-end replacement cost of the plant and equipment increased to €115,000. The plant and equipment has an expected life of 10 years with no residual value. The replacement cost of the land is believed to be €75,000 at year end.

CCA plc income statement for year ended 31 December 2012 Adjusted by application of current cost accounting

Sales revenue 200,000

Less:

Cost of goods sold 105,000

95,000Other expenses

Administrative expenses 9,000

Interest expense 1,000

Tax 26,000

Depreciation (€115,000 × 1/10) 11,500 47,500

Current cost operating profit 47,500

Realized savings

Savings related to inventory actually sold 5,000

Savings related to depreciation actually incurred [(115,000 – 90,000) × 1/10]

2,500

Historical cost profit 55,000

Unrealized savings

Gains on holding inventory – yet to be realized 3,500

Gains on holding plant and machinery – not yet realized through the process of depreciation [(115,000 – 90,000) × 9/10)]

22,500

Business profit 81,000

Opening retained earnings 0

Dividends proposed 15,000

Closing retained earnings 66,000

CCA plc statement of financial position as at 31 December 2012 Adjusted by application of current cost accounting

Current assets

Cash 100,000

Trade debtors 20,000

Inventory (3,500 × €11.00) 38,500 158,500

Non-current assets

Plant and equipment 115,000

Accumulated depreciation (11,500)

Land 75,000 178,500

Total assets 337,000

dee26734_ch05.indd 180 1/21/2011 5:59:59 PM

1815.4 Current Cost Accounting

Current liabilities

Bank overdraft 10,000

Trade creditors 30,000

Tax payable 26,000

Provision for dividends 15,000

81,000

Non-current liabilities

Bank loan 10,000

Total liabilities 91,000

Net assets 246,000

Represented by:

Shareholders’ funds

Paid up capital 180,000

Retained earnings 66,000

246,000

Consistent with the CCA model prescribed by Edwards and Bell, all non-monetary assets have to be adjusted to their respective replacement costs. Unlike historical cost accounting, there is no need for inventory cost flow assumptions (such as last-in-first-out; first-in-first-out; weighted average). Business profit shows how the entity has gained in financial terms from the increase in cost of its resources – something typically ignored by historical cost accounting. In the above illustration, and consistent with a number of versions of CCA, no adjustments have been made for changes in the purchasing power of net monetary assets (in contrast to CPP).24

The current cost operating profit before holding gains and losses, and the realized holding gains, are both tied to the notion of realization, and hence the sum of the two equates to historical cost profit.

Differentiating operating profit from holding gains and losses (both realized and unrealized) has been claimed to enhance the usefulness of the information being provided. Holding gains are deemed to be different from trading income as they are due to market-wide movements, most of which are beyond the control of management. Edwards and Bell (1961, p. 73) state:

These two kinds of gains are often the result of quite different decisions. The business firm usually has considerable freedom in deciding what quantities of assets to hold over time at any or all stages of the production process and what quantity of assets to commit to the production process itself … The difference

Some variants of CCA do include some purchasing power changes as part of the profit calculations. For example, 24

if an entity issued €1 million of debt when the market required a rate of return of 6 per cent, but that required rate subsequently rises to 8 per cent, then the unrealized savings would include the difference between what the entity received for the debt and what they would receive at the new rate. This unrealized saving would benefit the organization throughout the loan as a result of the lower interest charges.

dee26734_ch05.indd 181 1/21/2011 6:00:00 PM

Chapter 05 Accounting for Changing Prices and Asset Values182

between the forces motivating the business firm to make profit by one means rather than by another and the difference between the events on which the two methods of making profit depend require that the two kinds of gain be sepa-rated if the two types of decisions involved are to be meaningfully evaluated.

As with CPP, the CCA model described above has been identified as having a number of strengths and weaknesses. Some of the criticisms relate to its reliance on replacement values. The CCA model we have just described uses replacement values, but what is the rationale for replacement cost? Perhaps it is a reflection of the ‘real’ value of the particular asset. If people in the market are prepared to pay the replacement cost, and if we assume economic rationality, then the amount paid must be a reflection of the returns it is expected to generate. However, it might not be worth that amount (the replacement cost) to all firms – some firms might not elect to replace a given asset if they have an option. Further, past costs are sunk costs and if the entity were required to acquire new plant it might find it more efficient and less costly to acquire different types of assets. If it did buy it, then this might reflect that it is actually worth much more. Further, replacement cost does not reflect what it would be worth if the firm decided to sell it.

As was indicated previously, it has been argued that separating holding gains and losses from other results provides a better insight into management performance, as such gains and losses are due to impacts generated outside the organization; however, this can be criticized on the basis that acquiring assets in advance of price movements might also be part of efficient operations.

Another potential limitation of CCA is that it is often difficult to determine replacement costs. The approach also suffers from the criticism that allocating replacement cost via depreciation is still arbitrary, just as it is with historical cost accounting.

An advantage of CCA is better comparability of various entities’ performance, as one entity’s profits are not higher simply because it bought assets years earlier and therefore would have generated lower depreciation under historical cost accounting.

Chambers, an advocate of CCA based on exit values, was particularly critical of the Edwards and Bell model of accounting. He states (1995, p. 82) that:

In the context of judgement of the past and decision making for the future, the products of current value accounting of the Edwards and Bell variety are irrel-evant and misleading.

We now briefly consider some of the key principles underlying the alternative accounting model prescribed by Chambers and a number of others – a model that relies upon the use of exit values.

5.5 Exit price accounting: the case of Chambers’ continuously contemporary accounting

Exit price accounting has been proposed by researchers such as MacNeal, Sterling and Chambers. It is a form of current cost accounting that is based on valuing assets at

their net selling prices (exit prices) at the accounting date and on the basis of orderly sales. Chambers coined the term ‘current cash equivalent’ to refer to the cash that an entity would

dee26734_ch05.indd 182 1/21/2011 6:00:00 PM

1835.5 Exit Price Accounting: The Case of Chambers’ Continuously Contemporary Accounting

expect to receive through the orderly sale of an asset, and he held the view that information about current cash equivalents was fundamental to effective decision-making. He labelled his method of accounting continuously contemporary accounting, or CoCoA.

Although he generated some much cited research throughout the 1950s (such as Chambers, 1955) a great deal of his work culminated in 1966 in the publication of Accounting, Evaluation and Economic Behavior. This document argued that the key information for economic decision-making relates to capacity to adapt – which was argued to be a function of current cash equivalents (Chambers, 1966). The statement of financial position (balance sheet) is considered to be the prime financial statement under CoCoA, and should show the net selling prices of the entity’s assets. Profit would directly relate to changes in adaptive capital, with adaptive capital reflected by the total exit values of the entity’s assets. In other words, profit is directly tied to the increase (or decrease) in the current net selling prices of the entity’s assets. No distinction is drawn between realized and unrealized gains. Unlike some other models of accounting, all gains are treated as part of profit. Profit is that amount that can be distributed, while maintaining the entity’s adaptive ability (adaptive capital). CoCoA abandons notions of realization for recognizing revenue, and hence revenue recognition points change relative to historical cost accounting. Rather than relying on sales, revenues are recognized at such points as production or purchase.

As indicated previously in this chapter, how one calculates income is based, in part, on how one defines wealth. According to Sterling, an advocate of exit price accounting, (1970b, p. 189).

The present [selling] price is the proper and correct valuation coefficient for the measurement of wealth at a point in time and income is the difference between dated wealths so calculated.

In developing the CoCoA model, Chambers made a judgement about what people need in terms of information. Like authors such as Edwards and Bell, and unlike some of the earlier work which documented existing accounting practices to identify particular principles and postulates (descriptive research),25 Chambers set out to develop what he considered was a superior model of accounting – a model that represented quite a dramatic change from existing practice. We call this prescriptive or normative research. The research typically highlighted the limitations of historical cost accounting and then proposed an alternative on the basis of an argument that it would enable better decision-making. Chambers adopted a decision usefulness approach and within this approach he adopted a decision-models perspective.26

As a specific example of the inductive (descriptive) approach to theory development we can consider the work of 25

Grady (1965). This research was commissioned by the American Institute of Certified Public Accountants and documented the generally accepted conventions of accounting of the time.

As indicated in Chapter 1, decision usefulness research can be considered to have two branches, these being the 26