nondepository financial institutions chapter 10. life insurance companies oldest type of...

Post on 21-Dec-2015

214 views

TRANSCRIPT

Nondepository Financial Institutions

Chapter 10

Life Insurance Companies Oldest type of intermediary in the U.S. 1759 in Philadelphia (now called Presbyterian

Ministers’ Fund) Invest funds obtained through the sale of policies. Primary investments: Long term taxable, not

highly marketable securities: corporate bonds and commercial mortgages.

Income paid to policy holders is tax exempt - return on the policy holders investment

Insure against dying too soon and living too long.

Life Insurance Companies

Regulation of life insurance companies includes: Sales practices Premium rates Allowable investments

Usually overseen by a state insurance commissioner, who might also be the state banking commissioner

Types of Life Insurance Policies

Whole Life Insurance Constant premium that is paid

through entire life of policy Build up cash reserves or savings

which can be withdrawn as borrowing or outright by canceling the policy

Savings component pays a money market rate of interest that changes with market conditions

Types of Life Insurance Policies

Term Life Insurance Pure insurance with no cash reserve or savings

element Premiums are relatively low at first but increase with

the age of the insured individual Universal (variable) Life

Variation on whole life policy “Unbundle” the term insurance and tax-deferred

savings component Owner can elect how to allocate the savings

component among a menu of investment options, thereby potentially earning above money market rates

Life Insurance Companies Based on actuarial tables, life insurance

companies have ability to predict cash flow Typically insurance companies use excess

funds to buy long-term corporate bonds and commercial mortgages Higher yields Unlikely of having to sell prior to maturity

However, lately they have branched out into riskier ventures such as common stock and real estate

Life Insurance Basics Public makes payments in exchange for

protection Companies lend out the funds collected. Companies use the interest and

dividend income received to pay benefits to policyholders

Insurance companies have a reasonably predictable stream of payments to policy holders distributed over time.

Dealing with Asymmetric-Information Problems in Insurance

Limiting adverse selection Restricting the availability and quantity of

insurance. Limiting moral hazard in insurance

Deductible: A fixed amount of an insured loss that a policyholder must pay before the insurer is obliged to make payments.

Coinsurance: A policy feature that requires a policyholder to pay a fixed percentage of a loss above a deductible.

Pension Funds Program established by an employer to

provide retirement benefits to employees.

History established at the end of the 19th century by

railroads. 1875 - American Express Company who was

closely associated with railroading. Many failed during the depression - led to

increased regulation.

Pension Funds

Individuals need pension plans to supplement Social Security benefits

Most pension fund assets are in employer-sponsored plans

Defined Benefit Plan Defined Contribution Plan

Defined Benefit Plan Retirement benefits are defined by the plan Employer contributions are adjusted to meet the

benefits and insure the plan is fully funded—enough funds to meet future obligations

Vesting Retirement benefits remain with the employee if they

leave the firm and is based on length of employment Employee Retirement Income Security Act (ERISA)

Establishes minimum reporting, disclosure, vesting, funding and investment standards to safeguard employee pension rights

Pension Benefit Guaranty Corporation— Guarantees some benefits in defined benefit plans if

company is unable to meet its accrued pension liabilities

Defined Contribution Plan Contributions are defined by the plan Contribution may be made by employees or

employers or a combination of the two Employee contributions are tax deferred—

taxes payable when funds are withdrawn Benefits depend on the performance of the

assets in the plan Avoids the problems of vesting and funding Individual employee has the ability to choose

the assets in which to invest Most common are 403(b) and 401(k)

Pension Funds Defined contribution plans are the type

favored by most employers, although some employers offer both plans

In addition to employer-sponsored plans, some individuals are given tax incentives to set up their own pension plans Keogh Plans—self-employed individuals Individual Retirement Accounts (IRAs)—

working people who are not covered by company-sponsored pension plans

Pension Fund Basics Tax-exempt institutions set up to

provide participants with retirement income that will supplement other sources of income.

The number of people likely to retire each year is quite predictable.

As a result they invest about 80% of their funds in corporate equities.

Property and Casualty Insurance Companies

Insure against casualties such as automobile accidents, fire, theft, personal negligence, malpractice, etc.

Losses can be unexpected and highly variable.

Invest in tax-free municipal bonds and short-term securities.

Property and Casualty Insurance Companies (Cont.)

State insurance commissions set ranges for rates, enforce operating standards, and exercise overall supervision over company policies

Little federal involvement in regulating these companies

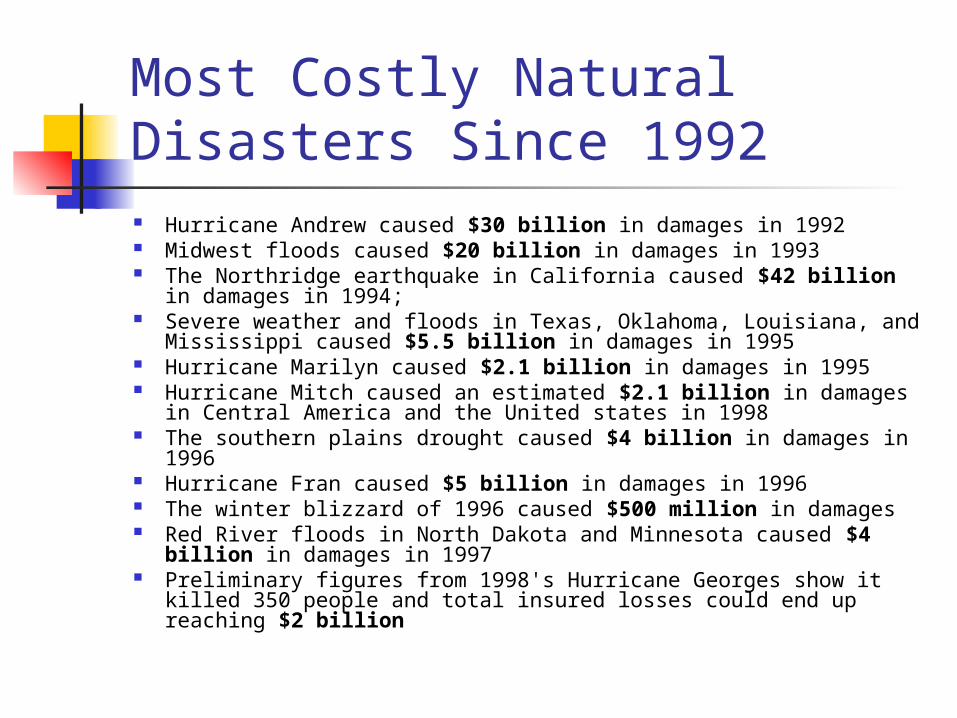

Most Costly Natural Disasters Since 1992 Hurricane Andrew caused $30 billion in damages in 1992 Midwest floods caused $20 billion in damages in 1993 The Northridge earthquake in California caused $42 billion in

damages in 1994; Severe weather and floods in Texas, Oklahoma, Louisiana, and

Mississippi caused $5.5 billion in damages in 1995 Hurricane Marilyn caused $2.1 billion in damages in 1995 Hurricane Mitch caused an estimated $2.1 billion in damages in

Central America and the United states in 1998 The southern plains drought caused $4 billion in damages in 1996 Hurricane Fran caused $5 billion in damages in 1996 The winter blizzard of 1996 caused $500 million in damages Red River floods in North Dakota and Minnesota caused $4 billion

in damages in 1997 Preliminary figures from 1998's Hurricane Georges show it killed

350 people and total insured losses could end up reaching $2 billion

Cost to insurers ACE and XL

Capital: $1bn-1.1bn

AIG: $500m Allianz: $930m AXA: $300-400m Berkshire

Hathaway: $2.2bn www.berkshirehath

away.com CNA Financial:

$200m-350m

•Chubb: $500-600m •Employers' Re: $600m•GE: $600m•Hannover Re: $365m•Munich Re: $1.95bn•Partner Re: $350-400m•Royal & Sun Alliance: $220m•Scor: $150m-200m•Swiss Re: $1.25bn•Zurich Financial: $400m

Mutual Funds Money Market Mutual funds have been

prominent on the American financial scene since the 1970s

However, stock market mutual funds (Mutual Funds) have been in existence since the 1950s.

A mutual fund pools the funds of many people and managers invest the money in a diversified portfolio of securities to achieve some stated objective

Open-end Mutual Fund Sell redeemable shares in the fund to the

general public Shares represent a proportionate ownership in

a portfolio held by the fund Shareholder can go directly to fund and buy

additional shares or redeem shares at their net asset value (NAV)

No-load Funds--Sold directly to public at the current NAV

Load Funds—Sold through brokers and buyer pays a sales commission

Open-End Mutual Funds

Net Asset Value (NAV) Fund calculates the total market value

of its portfolio and divides this figure by the number of outstanding shares.

Redeem outstanding shares or issue new ones at the NAV.

Number of shares is not fixed but increases as more money is invested.

Commonly known as Mutual Funds.

Closed-End Investment Company

Issues a fixed number of shares. Invests the proceeds in a portfolio

of assets. No load but brokerage fee. Shares are transferable. Price of the share is determined by

supply and demand.

Mutual Funds Mutual funds are regulated by the

Securities and Exchange Commission (SEC) Primary objective of regulation is the

enforcement of reporting and disclosure requirements to protect the investor

Many investors are attracted to families of mutual funds Number of mutual funds operated under one

management umbrella Investors can easily transfer money among

funds within the family

Net Asset Value Example

A fund has 10 million shares and is worth $100 million. NAV = $10.00

Investors invest $20 million more. At $10/share → 2 million shares →

$120 million in assets with 12 million shares.

You can buy fractional shares.

Low-load Funds

Load is ≤ 3% and goes to the fund. Front end load

Charged when shares are purchased. Back end load

Charged when shares are sold.

Full Load Funds

Sold by salespeople who earn a commission.

Load is split between the salesperson and the fund.

Max load allowed by the SEC is 9.589%

12b-1 Plans

Charge for advertising and selling expenses, including sales commissions to brokers.

All shareholders in the fund bear the burden, not just new investors.

Funds that use 12b-1 plans call themselves “no-load”.

Mutual Fund Information Mutual Fund Education Alliance Morningstar.com Valueline.com Vanguard.com Wall Street Journal Bloomberg.com

Finance Companies Consumer Finance Companies

Make consumer loans Specialty Finance Companies—specialize in

credit card financing Commercial finance Companies

Make commercial loans usually on a secured (collateralized) basis

Loans not as risky as consumer loans Since lending is short-term, these

companies borrow substantial amounts in commercial paper market

Finance Companies Historically finance companies have played

an important role in financing growing undercapitalized companies

Commercial finance companies originated the concept of leveraged buyout (LBOs) which relies heavily on debt to pay for acquisition of a company

Captive Finance Companies—Finance purchase of commercial and retail oriented businesses such as General Motors products (GMAC)

Securities Brokers and Dealers and Investment Banks These financial institutions play a

crucial role in the distribution and trading of huge amounts of securities

Investment Banks Sell and distribute new stocks and bonds directly from

issuing corporations to original purchasers League Tables rank investment banks by the volume

of securities they underwrite Underwriting is typically conducted through a

syndicate which includes many investment banks and brokerage firms

Investment banks derive a substantial amount of income from offering advice to firms involved in mergers and acquisitions

What price one firm should pay for another How the transaction should be structured Provide strategic advice in hostile takeovers—when one

firm seeks to acquire another against the other’s wishes

Brokers and Dealers Involved in the secondary market,

trading “used” or already outstanding securities

Brokers match buyers and sellers and earn a commission

Dealers commit their own capital in the buying and selling of securities and hope to make profit on the transaction

Brokers and Dealers Many of the nationwide stock exchange

firms act as investment bankers, dealers, and brokers

A number of large stock exchange firms have branched out to provide new types of financial services previously out of their operating charter

Commercial banks, investment banks, and broker dealers have now combined under single holding company umbrellas

Venture Capital Funds, Mezzanine Debt Funds, and Hedge Funds Venture capital funds, mezzanine debt funds,

and hedge funds are usually not available to public investors and not registered with SEC

Funding comes from wealthy individuals or other financial institutions, possibly sponsored by brokerage firms and banks

Both venture capital funds and mezzanine debt funds provide an important source of funding to small and midsize companies

Financing by both venture and mezzanine funds is non-traded and held until maturity

Venture Capital Funds Invest funds in start-up companies Traditional bank financing for these firms in

the early stage of growth would be very limited

The Venture Capital Fund receives a substantial equity stake in the firm

Although many start-up companies will fail, significant profit on those that are successful

Receives profits when it takes the successful company public in an initial public offering (IPO).

Mezzanine Debt Funds Provide debt funds to small and midsize

companies Issue convertible debt and

subordinated debt Sometimes simply invest in a

combination of high-yielding debt and equity issued by the same company

Used to provide long-term funds, sometimes part of a management-buyout financing package

Hedge Funds

Hedge funds: Limited partnerships that, like mutual

funds, manage portfolios of assets on behalf of savers, but with very limited governmental oversight as compared with mutual funds.

Long Term Capital Management

Founded by John Meriwether in 1993 LTCM had more credibility than the

average broker/dealer on Wall St. Two Nobel laureates: Robert Merton

and Myron Scholes Former Vice Chair of the Board of

Governors of the Federal Reserve: David Mullins

Biggest losers

LTCM partners $1.1 billion UBS $690 million Dresdner Bank $100 million Sumitomo Bank $100 million Bank of Italy $100 million Credit Suisse $55 million

Banks Versus Nondepository Institutions Many nondepository institutions offer

services that compete directly with banks Traditionally many of the different

markets were segmented, however, today they often compete for the same business

The Gramm-Leach-Bliley Act of 1999 allowed the creation of financial holding companies (FHCs) that can own commercial banks, investment banks, and insurance underwriters

Banks Versus Nondepository Institutions (Cont.)

The creation of FHCs brings the United States much closer to the universal banking regulatory model adopted by the European Union