non-profit organization player in student loan origination and servicing outstanding customer...

TRANSCRIPT

Non-Profit organization

Player in Student loan Origination and Servicing

Outstanding customer service

Default prevention

• Federal Regulations Requirement

• Your school is unable to release your loan funds until you complete this session.

• Agreement to pay back the loan(s)• Multi-year feature vs. New promissory note per year• Used for subsidized and unsubsidized Stafford loans

– Subsidized : need based loan; gov’t pays interest while enrolled

– Unsubsidized : non-need based loan; student pays for all interest

• Borrower rights and responsibilities detailed on MPN

• Variable interest rates that change every July 1st

• Capped at 8.25%• Current rates as of July 1, 2005

– 4.7% for In-school, grace & deferment– 5.3% for Repayment & forbearance

• Loan fees are automatically deducted from each disbursement– Originations fee : up to 3%– Guarantee fee : up to 1%

• Loans are disbursed in two installments– 1st installment @ the beginning of the enrollment

period (e.g., beginning of the fall semester)– 2nd installment @ the midpoint of the enrollment

period (e.g., beginning of the spring semester)

Student is responsible for updating the school/lender/servicer about the following changes:

Drop below half-timeWithdrawal from schoolTransfer to another schoolChange in graduation dateAddress changePhone number changeName change (e.g., due to marriage)SSN change

Loan Cancellation:You may cancel your loan anytime before lender sends money to school (before disbursement)OrIf loan reaches school, student has 14 days from the date on the disbursement notice the school sends to the student

Borrowing money is a serious matter and all loans must be paid back

• Not receiving payment coupons or payment schedule is not an excuse for not making payments

• Even if you don’t graduate or find a job, or you are dissatisfied with quality of education, you must pay back the loan(s).

First Payment is due after the 6 month grace period

* Graduation

* Enrollment of less than half time

* Complete withdrawal from School

.

• Standard Plan

• Graduated Plan

• Extended Plan

• Income-sensitive Plan

• Lender may sell or transfer loan

• Student will be notified of change of ownership

• Borrower rights do not change

Student

Lender

Servicer

Secondary Market

Guaranty Agency

Death of borrower

Total and permanent disability of borrower

You have the right to defer your student loan payment if you submit proper documentation!

DEFERMENT TYPESTAFFORD / PLUS /

CONSOLIDATION LOANS(NEW BORROWER)

after 7/1/93

I N- SCHOOL Full- time Half- time

YesNo Limit

EDUCATI ON RELATED Graduate fellowship Rehabilitation program

YesNo Limit

ECONOMI C HARDSHI P Up to 36 months

UNEMPLOYMENTUp to 36 months

* If you have an outstanding loan that was disbursed before July 1, 1993, you may be eligible forother deferments not listed above. Contact your lender or servicer for other deferments.

DEFERMENT: a period of time during which your lender temporarily suspends your regular payments

• A period of time during which your lender temporarily suspends or reduces your loan payments.– Usually granted to borrowers without

deferment eligibility– You are responsible for all interest that

accrues during forbearance– Interest may be paid as it accrues

during forbearance or may be added to your principal

• Allows borrowers to combine one or more federal educations loans

• You can consolidate once you are in school, in-grace or in repayment.

• Original loans are paid in-full– New loan is created for the combined balance– Only one payment each month– New terms– New interest rate that is fixed for the life of the loan– You can receive a 10 year repayment option or more. Payment can

increase up to 30 years .– You can receive deferment during consolidation of loans.

months past due or 270 days

• You can be sued

• You will be reported to the National Credit Agencies

• Your wages may be garnished

• Your Federal Income Tax Refund may be withheld

• You will be ineligible for future Federal Financial Aid

• You will be liable for all costs associated with the collection of your loan

• Lottery winnings may be withheld

• The renewal of any professional or occupational license may be denied

• You are entitled to a repayment period of at least 5 years as long as you meet the monthly minimum payments.

• You have the right to repay all or any part of your loan at any time without penalty.

• You are entitled to ask your Lender/Holder/Servicer/School/Guarantor any questions about your student loan.

http://ombudsman.ed.gov1-877-557-2575

1-512-219-4502, in Texas

Sources of Income for College

StudentsGrants & scholarshipsCollege work-study or part-time jobStudent loans

College ExpensesTuition & fees

Books & supplies

Rent or dorm

Utilities & gas for your car

Groceries or meal plan

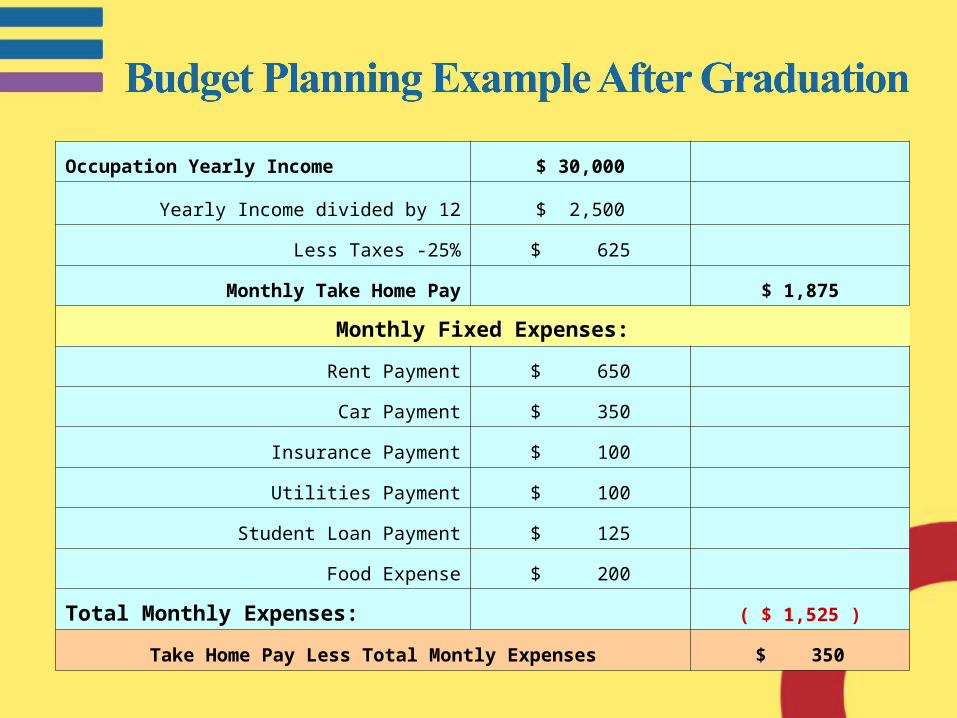

Occupation Yearly Income $ 30,000

Yearly Income divided by 12 $ 2,500

Less Taxes -25% $ 625

Monthly Take Home Pay $ 1,875

Monthly Fixed Expenses:

Rent Payment $ 650

Car Payment $ 350

Insurance Payment $ 100

Utilities Payment $ 100

Student Loan Payment $ 125

Food Expense $ 200

Total Monthly Expenses: ( $ 1,525 )

Take Home Pay Less Total Montly Expenses $ 350

• Keep in mind when you will receive your loan funds– 1st time borrowers have a 30 day delay

• Keep track of how much you borrow every year in college• Consider making interest and/or principal payments• Remember that credit cards are also loans• Be realistic about earnings after college• Keep all your loan records• Do not spend beyond your means-Lifestyle should be that

of a college student, not a professional

• Know your school’s Refund Policy• Know your school’s requirements for

Satisfactory Academic Progress– Know your school’s Appeals process

• Know your school’s Withdrawal procedures• Know your school’s Packaging philosophy

Contact your Financial Aid Office for more Information