non-core fixed income process & recommendations | … · credit*, 2.8% high yield, 2.4% ......

TRANSCRIPT

December 8-9, 2016 Jason Weiner, Director of Fixed Income Germán Gaymer, Fixed Income Investment Analyst Weston Kasper, RVK

Non-Core Fixed Income Process & Recommendations

Agenda

2

I. Non-Core Fixed Income (NCFI) Timeline & Allocation Objectives

II. NCFI Portfolio Construction III. Manager Search Process IV. Manager Selection Recommendations V. Requested Board Action

I. NCFI Timeline & Allocation Objectives

4

Winter 2015 December Board Meeting: •Board approves 3-phase Pacing Plan for Non-Core Fixed Income in 2016

Spring 2016 June Board meeting: •Phase 1: Board approves Opportunistic Credit managers

Summer 2016 August Board Meeting: •Phase 2: Board approves Direct Lending recommended managers

Current 2016 December Board meeting (Phase 3): •Consider and act on Opportunistic Credit managers •Consider and act on an additional Private Credit manager

NCFI Search Timeline

5

2016 NCFI Search Process Objectives • Excess Return Potential and Controlled Volatility

• Expected excess return consistent with TMRS’ overall objective to identify opportunities to add value through additional active management strategies.

• Determine that the level of risk is within TMRS’ risk tolerance levels.

• Portfolio Diversification • Develop additional strategic allocations within the NCFI asset class to

add value relative to the asset class benchmarks. • Provide further diversification while complementing current fixed income

strategies and other asset classes.

• Targeted Commitment Level • The targeted NCFI Pacing Plan for Phase 3 2016 is $700 million in

commitments.

NCFI Current & Target Portfolio (as of September 30, 2016)

6 * Approved by the board, funding pending. ** Partially funded. A portion of the allocation is pending on the Board’s approval.

Bank Loan/CLO, 3.2%

RMBS/CMBS, 3.1%

Emerging Market Debt*,

1.9%Direct

Lending**, 3.8%

Opportunistic Credit*, 2.8%

High Yield, 2.4%

Unallocated, 2.8%

NCFI Current Allocation

Bank Loan/CLO, 3.2%

RMBS/CMBS, 3.1%

Emerging Market Debt*,

1.9%

Direct Lending**,

4.6%

Opportunistic Credit**, 4.8%

High Yield*, 2.4%

NCFI Expected Allocation

II. NCFI Portfolio Construction

NCFI Portfolio

8

HY14.0%

BL8.7%

CLO7.9% S/D

1.2%CLO Equity

1.0%DL

19.0%Unallocated13.9%

RMBS7.9%

CMBS7.9%

ABS3.0%

NPL6.0% EMD

9.6%

NCFI Asset Allocation The recommendations the Board approved in 2015 and YTD 2016, have been primarily focused on four broad sectors: 1. Corporate Credit 2. Direct Lending 3. Structured Products 4. Emerging Market Debt The 2016 Phase 3 search identifies managers with expertise in the following three sectors: 1. Corporate Credit 2. Structured Products 3. Direct Lending The proposed portfolios target specific investment profiles that are expected to help achieve TMRS’ long term return and diversification objectives.

NCFI Portfolio

9

Current recommendation goals & investment thesis • Select managers that utilize best in class credit capabilities within these broad sectors

and have consistently delivered very attractive risk adjusted returns. • Identify differentiated managers that complement our existing set of managers. • Calibrate allocations to further improve the return profile and diversification of the NCFI

portfolio. • Allocate to managers that can tactically and strategically position their portfolios based

on a relative value orientation predicated on their views of the economic and credit cycles.

HY14.0%

BL8.7%

CLO7.9% S/D

1.2%CLO Equity

1.0%DL

19.0%Unallocated13.9%

RMBS7.9%

CMBS7.9%

ABS3.0%

NPL6.0% EMD

9.6%

NCFI Asset AllocationHY

15.7%

BL10.5%

CLO9.4%

S/D2.6%

CLO Equity1.0%

DL23.0%

RMBS9.2%

CMBS8.0%

ABS5.0%

NPL6.0% EMD

9.6%

NCFI Final Asset Allocation

NCFI Portfolio

10

1. Corporate Credit Strategies Revisited Corporate credit strategies typically include HY bonds (HY), Bank Loans (BL), CLOs, CLO Equity and Stressed/Distressed Debt (S/D). These strategies will have two primary return drivers: 1. High Income: Identify performing debt instruments that generate high income through the payment

of interest and principal. 2. Stressed/Distressed: Acquire debt at a discount due to dislocation and identify a catalyst to drive

price appreciation. Late

SlowdownLate

RecoveryPeak Early

SlowdownTrough Early

Recovery

Build drypowder/layer onhedges, reduce

lower-qualityassets

Stay senior andliquid, start to

increaseexposure as

spreads widen

Increasedistressed andprivate debt,

reduce hedges

Overweighthigh yield,

restructuredequities

Harvest gainson distressed

and mezzanine

Selectively addhigh yield/

junior capitalexposure

Positioning

Source: Bain Capital

Illustration of how managers may tactically allocate according to their economic and market views:

NCFI Portfolio

11

2. Structured Products Revisited • Alternative yield strategies invest in structured credit assets where the value is linked to the

performance of the underlying/reference assets. • Managers perform fundamental analysis on the underlying assets and structural analysis on the

credit vehicle. Structured Products Market:

Autos $190

Credit Cards $129

Other* $245

Student Loans $202

CLOs $436

CMBS $500

RMBS CDOs $76

Non-Agency Mortgage $603

Asset-Backed Securities OutstandingNotional Amount by Sector as of 4Q’15

Total =$2.4 trillion “Non-Traditional ABS”“Other” ABS Category Breakdown

Notional Amount by Sector as of 4Q’15Total =$245 billion

Trust Preferred $38

Multi Sector CDO $20

Aircraft $15

Floorplan $31

Timeshares $6 Trade Receivables, $1

Motorcycle $2 Insurance $1 Franchise $12 Manufactured

Housing [VALUE]

Misc. $18

Equipment $51

Small Balance Commercial $35

Container $6

* “Other” includes approximately 20+ additional ABS sectors. Unless otherwise noted all dollar amounts expressed in billions. Source: Securities Industry and Financial Markets Association (SIFMA), Wells Fargo, Bank of America and Waterfall Asset Management

NCFI Portfolio

12

3. Direct Lending (DL) Revisited This opportunity arises due to bank disintermediation, where smaller companies (sales between $10M to $1B) are forced to seek financing from non-traditional sources. Middle Market key characteristics: Ownership: (Sponsored vs. non-Sponsored) Sponsored: Companies owned by a Private Equity firm. • Usually the owner is more sophisticated with a deeper knowledge of financial markets. • This market tends to be more competitive resulting in lowers yields on average. Non-Sponsored: Companies privately owned by families, entrepreneurs, etc. • Access to financing tends to be more limited. • Less competitive market. Size: (Lower middle market vs. Upper middle market) Lower Middle Market: EBITDA lower than $25 million. • Loan size can go up to roughly $100 million, yet usually they are much smaller, typically ranging

from $25 million to $75 million. • It can take longer to build a large and diversified portfolio. Upper Middle Market: EBITDA greater than $25 million. • Loan size usually ranges from $50 million to $400 million. • Not all DL managers have the capacity to make this type of loan.

III. Manager Search Process

Manager Search Process Review

14

Step 1

• Initial Screening • TMRS evaluated market opportunity and did an initial screening of potential managers. • TMRS fixed income team filtered managers with potential fit in the opportunistic credit and direct lending strategies.

Step 2 • Opportunistic Credit Manager Identification • RVK and TMRS (team) identified 25 managers with opportunistic credit/direct lending capabilities.

Step 3

• Semi-Finalist Candidate Analysis (Best ideas) • The team selected 7 managers to move to the semifinals. • Each of the 7 semi-finalist candidates was scored independently by the team.

Step 4 • Finalist Candidate Analysis • Based on the scoring, 4 managers were selected to move to the finals.

Step 5

• Final Due Diligence & Manager Selection • On site due diligence was performed at the finalist locations. • 4 managers were selected for recommendation to the Board.

Manager Search Process Review

15

After an initial screening was completed by TMRS, the fixed income staff collaborated with RVK (the team) and identified 25 managers for further review. As a result of this review, the team carefully selected 7 managers for the semi-finalist stage. The next table shows the scoring of these managers.

After careful consideration and completing extensive analysis in addition to establishing the complementarity of each manager within a portfolio context, the team decided to recommend four managers for approval at the December Board Meeting.

Scoring Category Possible Points

Adams Street

Bain Capital GoldenTree Waterfall

Semifinalist 1

Semifinalist 2

Semifinalist 3

People (Firm & Team) 0 - 25 23.00 24.33 22.67 24.00 23.67 22.67 22.00

Process (Investment Process & Risk Management) 0 - 25 23.33 24.33 24.33 24.67 23.00 23.33 21.00

Performance History 0 - 25 23.00 19.33 23.67 23.00 22.33 19.67 19.00 Philosophy/Strategy (Attractiveness of Opportunity/Portfolio Fit) 0 - 12.5 12.50 12.50 12.50 12.50 10.00 8.00 7.33

Terms (Fees, Liquidity, etc.) 0 - 12.5 12.50 12.50 12.50 9.00 9.00 9.00 10.00

Total 100 94.33 93.00 95.67 93.17 88.00 82.67 79.33

IV. Manager Selection Recommendations

Executive Summary of Manager Recommendations

17

Summary of Recommendations Recommended Fund Strategy Focus Recommended Amount

Adams Street Private Credit Fund-A LP (Adams Street)

Direct Lending $200 million

Bain Capital Credit, LP (Bain) Relative Value Credit $100 million

GoldenTree Asset Management, LP

(GoldenTree) Relative Value Credit $200 million

Waterfall Eden Fund, LP (Waterfall) Structured Products $200 million

Total Recommendation $700 million

18

Top Candidate Characteristics: Adams Street Firm

• Adams Street was originally founded in 1972 as Brinson Partners and was subsequently purchased by UBS. In 2001 they were spun out of UBS and have been independent and 100% employee owned since then.

• The firm manages over $27 billion across a platform specializing in private equity, venture/growth investments, and secondary investing.

• The firm is headquartered in Chicago with offices in Menlo Park, New York, Boston, London, Beijing, Tokyo, Singapore.

Team • Over 140 employees firm wide with a robust infrastructure. The team managing the

Private Credit Fund is comprised of two partners, a principal, and three more junior associates. Combined average experience of the team is 11 years.

• Bill Sacher, Partner and Head of Private Credit, is building out the team from scratch. He came from Oaktree Capital where he ran a Direct Lending Mezzanine fund that he built out with roughly the same size team he has now. Shahab Rashid, partner and co-founder on this team, joins him from Oaktree where they worked together.

• As of October 2016 the team is fully staffed. The intention is to collaborate with the co-investment team as well on information flow. The team is further supported by over 65 other Adams Street staff.

19

Top Candidate Characteristics: Adams Street Strategy

• Target private equity backed (sponsored) middle-market transactions (companies with an enterprise value of $150-750M or $15-75M EBITDA).

• Debt investments will include senior debt (first lien, unitranche, second lien, etc.) and unsecured debt (senior unsecured, subordinated debt, etc.) and preferred equity.

Senior Lending Mix Mezzanine

Upper Middle Market

Lower Middle Market

20

Top Candidate Characteristics: Adams Street Investment Case • Invest across the capital structure from traditional senior secured debt to unsecured debt

and preferred equity. • The investment process is based on intensive credit analysis, rigorous company due

diligence and in-depth industry analysis to find performing (“money good”) companies and avoid losses.

• Extend their deal pipeline through key relationships given their extensive industry experience and leverage the broader Adams Street platform.

• The senior partners/lead portfolio managers have a long track record of successfully managing credit investments.

• TMRS will be a founding investor in the fund.

Considerations • The team was recently established. The risk of participating in a new fund is mitigated by

Bill’s proven experience of building out successful teams in past years. In addition, the depth of the resources available from the broader Adams Street platform should further mitigate TMRS’ risk.

21

Top Candidate Characteristics: Bain Firm

• Bain (formerly Sankaty Advisors) was founded in 1998 by Jonathan Lavine. The firm is 100% employee owned.

• The firm manages over $31 billion across the full spectrum of credit strategies, including leveraged loans, high-yield bonds, distressed debt, direct lending, structured products, non-performing loans (NPLs) and equities.

• The firm is headquartered in Boston with additional offices in Chicago, New York, London, Melboure, Dublin, and Hong Kong.

Team

• 242 employees firm wide with 119 investment professionals. • Organized in teams of specialists based on either industry-specific research or

particular investment strategies or functions. • 32 industry analysts charged with being industry experts. Analysts vary between

region and geography, depending on the industry. • Unified credit committee where all positions must be approved by the committee.

Bain emphasizes the importance of establishing group consensus among the most senior members of the firm to ensure credit underwriting standards are met.

22

Top Candidate Characteristics: Bain Strategy

• Bottom up fundamentally driven credit firm where all ideas are generated from industry research teams.

• Full credit write up, model development, capital structure and legal analysis culminates their due diligence efforts.

• Portfolio Managers bring a more macro view to asset selection and help with relative value decisions across industries.

Asset Class RangeTarget

AllocationDistressed & Special Situations 0-30% 20%

CLOs 0-20% 15%High Yield 20-60% 30%Bank Loans 20-60% 35%

20%

15%

30%

35%

0%

20%

40%

60%

80%

100%

120%

1

Bain Expected Portfolio

Bank Loans

High Yield

CLOs

Distressed & SpecialSituations

23

Top Candidate Characteristics: Bain Investment Case

• Rigorous bottom-up driven process based on a large team of industry experts and research analysts.

• The manager recognizes the key role that the analyst plays in the investment process and incentivizes them to become specialists.

• Large dedicated distressed and special situations team spreads across Bain’s different offices enables the manager to lever the needed local expertise for each deal.

• Bain employs a diversified investment approach targeting approximately 450 positions in the portfolio to control and reduce risk within the portfolio.

Considerations

• Bain’s highly diversified investment approach could hamper the manager’s ability to outperform in a risk-on environment. Bain has demonstrated consistent risk adjusted returns in all market cycles.

• Bain’s investment process and philosophy complements our more concentrated, high conviction managers within the NCFI portfolio.

24

Top Candidate Characteristics: GoldenTree Firm

• GoldenTree Asset Management was founded in 2000 by Steve Tananbaum. The firm is 100% employee owned with 26 partners.

• The firm manages over $24 billion across a platform specializing in opportunistic credit, high yield, and distressed/special situations.

• The firm is headquartered in New York with an additional office in London. Team

• 224 employees firm wide including 47 investment professionals with average industry experience of 16 years.

• Portfolio managers and analysts are industry specialists, setup by industry and operate as one cohesive unit across all strategies.

• 6 senior members comprise the internal investment committee, headed by the founder, to establish top down, macro strategy.

25

Top Candidate Characteristics: GoldenTree Strategy

• Credit-oriented strategy that relies heavily on their fundamental bottom up research to identify opportunities and ensure the investment has a high margin of safety.

• Look for catalysts to drive total return and use real time relative value analysis. • Investment across the capital structure and asset classes, with the focus on liquid

bonds and loans, structured credit (mainly CLOs), opportunistic distressed, and some credit themed equity.

Asset Class RangeTarget

AllocationDistressed & Special Situations 0-30% 25%

CLOs 0-20% 20%High Yield 20-60% 28%Bank Loans 20-60% 28%

25%

20%

28%

28%

0%

20%

40%

60%

80%

100%

120%

1

Golden Tree Expected Portfolio

Bank Loans

High Yield

CLOs

Distressed & SpecialSituations

26

Top Candidate Characteristics: GoldenTree Investment Case • Senior members of the team have successfully executed GoldenTree’s fundamental value

investment process for over 20 years. • Investment team has an average experience of 16 years. • Proprietary technology to efficiently compare corporate investments across instruments

and industries, forcing constant re-underwriting of the portfolio. • Disciplined fundamental value analysis investing only where there is a catalyst to realize

value and a margin of safety that limits the risk of loss. • Strong European presence with 14 investment professionals based in the London office. Considerations • High conviction manager that builds concentrated portfolios relative to its peers. The

manager’s depth of resources combined with the strong analytic and relative value frameworks should mitigate potential return volatility.

• The investment team has experienced some bouts of turnover. The manager has offset these departures with new hires. Investment staff will continue to monitor to ensure continuity and consistency of coverage.

27

Top Candidate Characteristics: Waterfall Firm

• Waterfall was founded in 2005 by Jack Ross and Tom Capasse. The firm is 75% employee owned, with Dyal Capital (Neuberger Berman entity) owning the balance.

• The firm manages over $6 billion across a platform specializing in structured credit, namely high yield (HY) asset backed securities (ABS) and loans.

• The firm is headquartered in New York with an additional office in London Team

• 84 employees firm wide with 44 Investment Professionals • Low average annual turnover rate at 2% since inception. • Deep experience and expertise in this area, including career ABS bankers, deal

structurers and transaction lawyers. • Individual teams are setup by function, not industry. • 5 member Investment Committee charged with looking at thematic perspective, new

sectors, large trades, European opportunities, etc.

28

Top Candidate Characteristics: Waterfall Strategy

• Waterfall will target niche areas of the 60+ sector HY ABS market where there is a yield premium.

• Invest across the capital structure, investing in loans and bonds, but will not invest in non-performing loans. Distressed ABS is part of the strategy.

• Relative value approach and ability to source from both the public and direct privately negotiated new issue markets.

• Predominantly bottom up research driven process, which is coupled with a top down sector/risk approach driven by their Investment Committee.

• The process relies heavily on ABS sector expertise and proprietary modeling tools.

• Robust surveillance/risk monitoring process. This includes a formal ratings assessment of each underlying holding. Formal surveillance meeting is monthly, but monitored in real time.

29

Top Candidate Characteristics: Waterfall Investment Case

• The founders have been involved in structured finance since the early days of development.

• Waterfall has developed an extensive infrastructure by increasing headcount over time to cover many smaller, more esoteric areas of the structured product market.

• Waterfall employs a robust risk management framework that sets specific sector limits to mitigate risk.

• Long track record and dedicated focus to structured products. Considerations

• The strategy focuses on smaller, less trafficked areas of the structured product market due to the manager’s experience in these areas. These investments have limited liquidity and are complex structures. The manager implemented redemption gates in 2009 to better match the liquidity profile of the fund’s assets. Currently there is cap of 12.5% quarterly liquidity per investor.

V. Requested Board Action

Requested Board Action

31

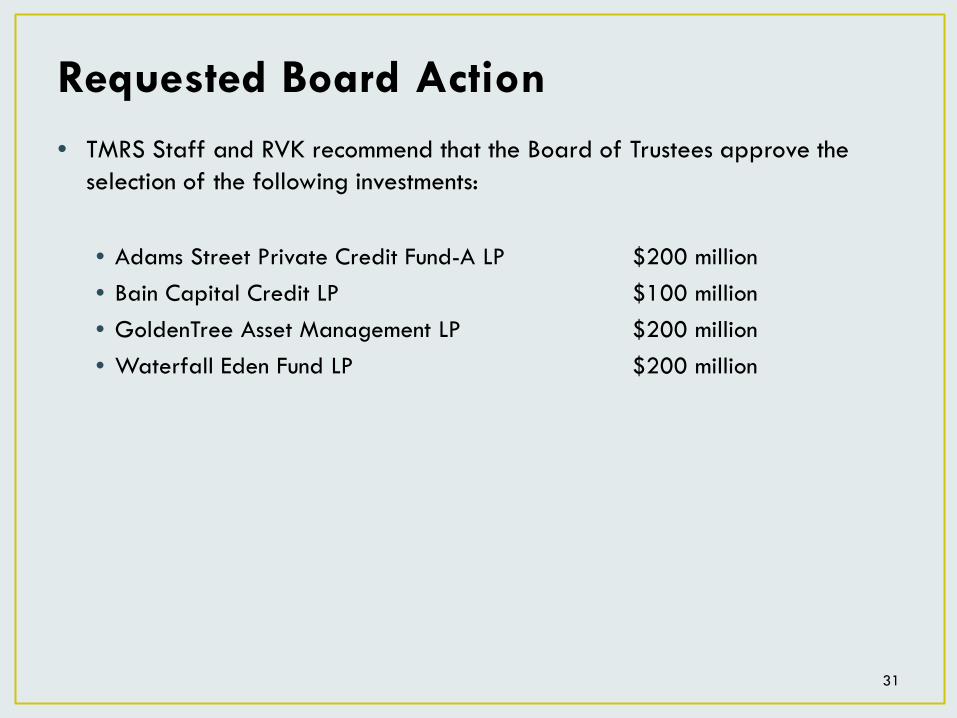

• TMRS Staff and RVK recommend that the Board of Trustees approve the selection of the following investments:

• Adams Street Private Credit Fund-A LP $200 million • Bain Capital Credit LP $100 million • GoldenTree Asset Management LP $200 million • Waterfall Eden Fund LP $200 million

TMRS periodically discloses public information that is not excepted from disclosure under Section 552.0225(b) of the Texas Public Information Act. Information provided by a manager, a general partner or other data

provider to TMRS or a TMRS service provider, and contained in these materials, may have been independently produced or modified by TMRS or the TMRS service provider.

32

Disclosure