nominal and real values nominal and real values in macroeconomics macroeconomics makes a big issue...

TRANSCRIPT

NOMINAL AND REAL VALUES

Nominal and Real Values in Macroeconomics

Macroeconomics makes a big issue of the distinction between nominal values and real values:

• Nominal GDP and real GDP• Nominal wage rate and real wage rate• Nominal interest rate and real interest rate

NOMINAL AND REAL VALUES

Just because you get an increase in the nominal value, doesn’t mean you are better off than you were before.

We will need to deflate nominal values by the price index to calculate real values for anything- Wages, Income, GDP, etc…

Formula for Real Values

Real = Nominal__________________

Price Index

* The price index can be the CPI, PPI, or the GDP Deflator.

X 100

NOMINAL AND REAL VALUES

Nominal and Real Wage Rates

Nominal wage rate

The average hourly wage rate measured in current dollars.

Real wage rate

The average hourly wage rate measured in the dollars of a given reference base year. Reflects inflation!

NOMINAL AND REAL VALUES

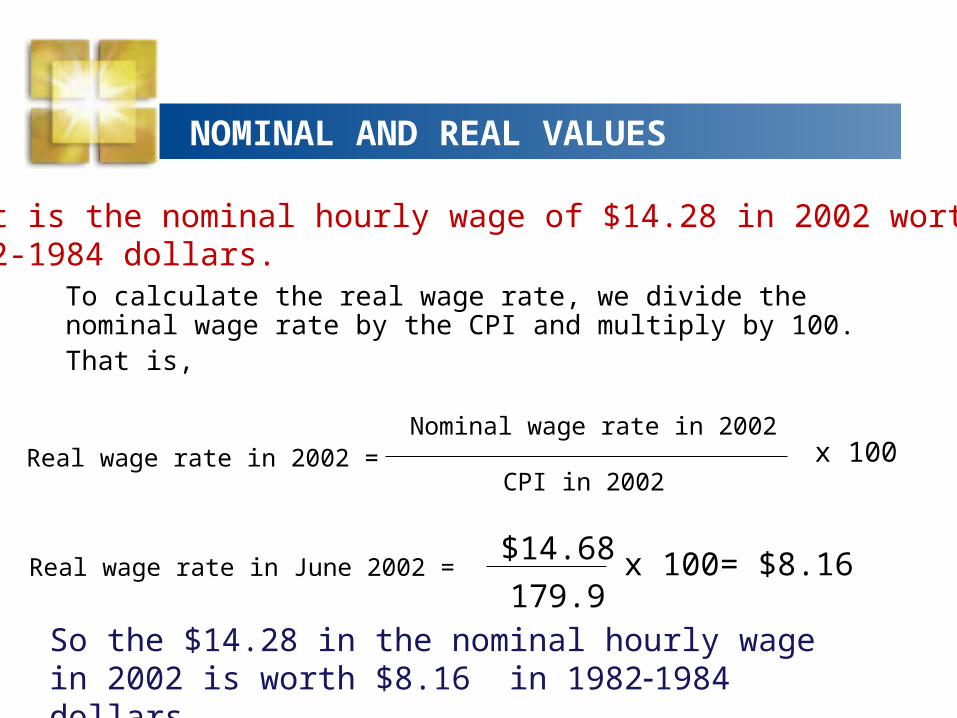

Real wage rate in June 2002 = = $8.16 $14.68

179.9x 100

To calculate the real wage rate, we divide the nominal wage rate by the CPI and multiply by 100. That is,

Nominal wage rate in 2002

CPI in 2002x 100Real wage rate in 2002 =

So the $14.28 in the nominal hourly wage in 2002 is worth $8.16 in 19821984 dollars.

What is the nominal hourly wage of $14.28 in 2002 worth in 1982-1984 dollars.

22.3 NOMINAL AND REAL VALUES

Figure 22.4 shows nominal and real wage rates: 1975–2005.

The nominal wage rate has increased every year since 1975.

The real wage rate increased briefly during the late 1970s, decreased through the mid-1990s, and then increased slightly.

Nominal and Real Income

Example: 2002- Nominal income is $40,000 2003- Nominal Income is $41,000 2002- CPI 181.6 2003- CPI 185

Q. 1- What is my real income for each year?

Q. 2- Did my purchasing power increase in

2003? Am I better off in 2003?

Nominal and Real Income

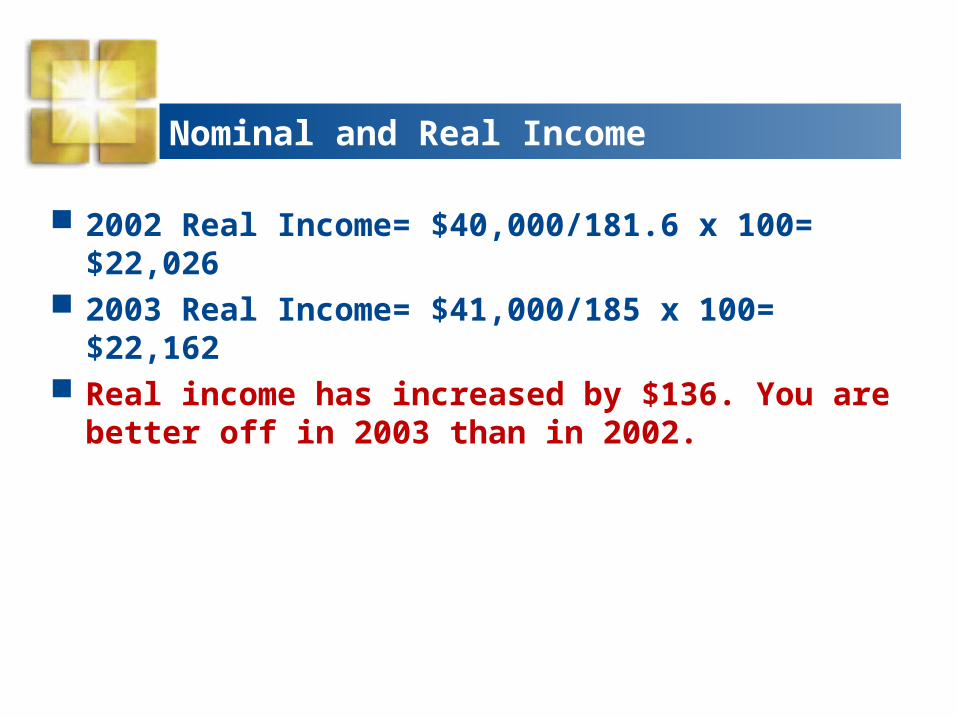

2002 Real Income= $40,000/181.6 x 100= $22,026 2003 Real Income= $41,000/185 x 100= $22,162 Real income has increased by $136. You are better

off in 2003 than in 2002.

Nominal and Real Income

What if your income only increased to

$40,500 in 2003.

Calculate: 1) Real income for each year.

2) Did your purchasing power

increase in 2003?

Nominal and Real Income

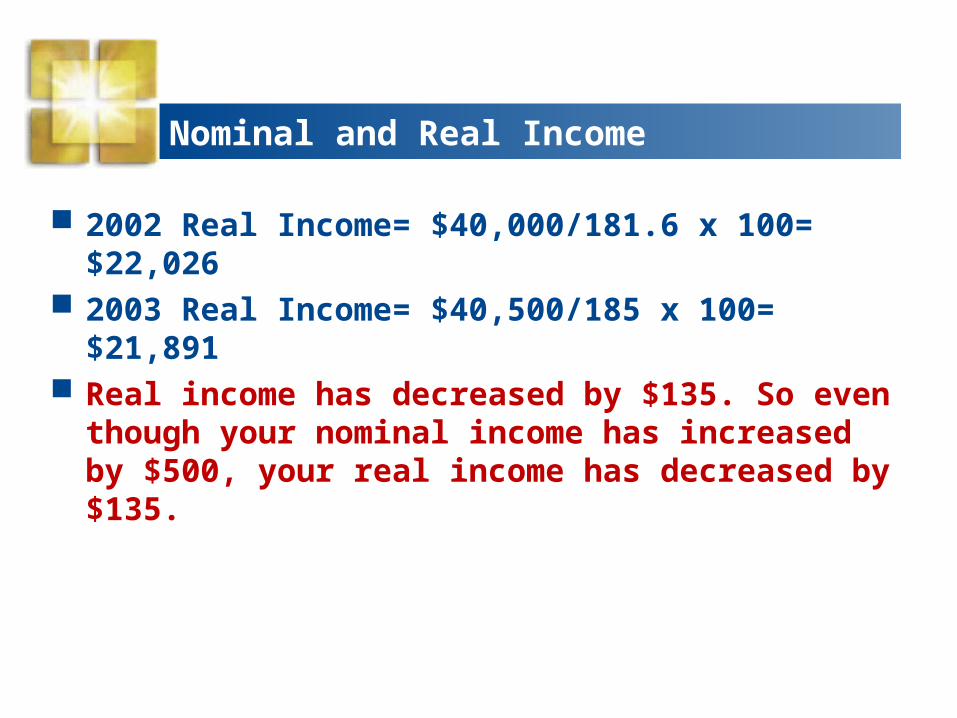

2002 Real Income= $40,000/181.6 x 100= $22,026 2003 Real Income= $40,500/185 x 100= $21,891 Real income has decreased by $135. So even though

your nominal income has increased by $500, your real income has decreased by $135.

Inflation

Anticipated Versus Unanticipated Inflation

The effects of inflation on individuals depends upon which type of inflation exists.

Anticipated Inflation

Anticipated Inflation

The rate of inflation that the majority of individuals believe will occur. If the rate of inflation is 10% and that is what the majority expected, then inflation was fully anticipated.

Unanticipated Inflation

Unanticipated Inflation

Inflation that comes as a surprise to individuals in the economy. If people expected an inflation rate of 5% and the actual rate of inflation was 10%, then 5% of the actual inflation rate was unanticipated inflation.

This is the inflation that wreaks havoc on the economy!

Unanticipated inflation hurts many people. When inflation is anticipated some of these people (lenders) are able to protect themselves.

All of this is important when dealing with interest rates!

22.3 NOMINAL AND REAL VALUES

Nominal and Real Interest Rates

Nominal interest rate

The percentage return on a loan expressed in todays dollars.

Real interest rate

The percentage return on a loan, calculated by purchasing power—the nominal interest rate adjusted for the effects of inflation.

Real interest rate = Nominal interest rate – Inflation rate

Inflation/Interest Rates

Real Interest Rate

1982 -- Home Mortgage• Nominal Interest Rate 15%• Increase in the price of housing of 25% (inflation)

Real Rate = 15% - 25% = -10%

Inflation/Interest Rates

Real Interest Rate

1998 -- Home Mortgage• Nominal Interest Rate 6.5%• Increase in the price of housing of 2%

Real Rate = 6.5% - 2% = 4.5% Question

Which scenario is the best for the lender? the borrower?

Does Inflation Necessarily Hurt Everyone?

All of this is extremely important with borrowers and creditors.

Banks must anticipate the inflation rate to cover all loans. Try to increase interest rates with the rate of inflation. This is not an exact science. Creditors/lenders must make sure that the nominal rate of interest is greater than anticipated inflation. It is the unanticipated inflation they can not predict.

Creditor gains if real interest rate is positive. Debtor gains if real rate of interest is negative Unanticipated inflation is the key!!

Higher unanticipated inflation helps borrowers/hurts creditors.

Does Inflation Necessarily Hurt Everyone?

Nom. Int. Rate - Infl. Rate = Real Int. Rate

10% 5% 5% creditor wins

10% 10% 0% draw

10% 15% -5% debtor wins

In the past inflation and nominal interest have risen and fallen together.

Effects of Inflation

Creditors (Lenders) Lose: Net creditors are individuals or businesses that have more savings than debt. A net creditor receives interest and, therefore, receives a reduced real interest return when there is unanticipated inflation.

Debtors (borrowers) Win: Net debtors are individuals or businesses that have more debt than savings. A net debtor pays interest, and therefore, pays a lower real interest rate when there is unanticipated inflation. A fixed rate of interest helps a debtor in the long term. Paying back a loan with less purchasing power during times of inflation.

NOMINAL AND REAL VALUES

Figure shows real and nominal interest rates: 1965–2005.

The nominal interest rate increased during the high-inflation 1980s.

During the 1970s, the real interest rate became negative.

Inflation

Protecting Against Inflation

Cost-of-living adjustments (COLAs)• Clauses in contracts that allow for increases in

specified nominal values to take account of changes in the cost of living

ARMS- Banks offer “Adjustable Rate Mortgages” that adjust the interest rate to keep up with changes in inflation

23

Types of Inflation

Demand- Pull Inflation- More dollars chasing less goods. An increase in aggregate demand. Often results for too much money in the economy.

Cost-Push Inflation- Inflation due to an increase in production/ input costs. Results in a decrease of aggregate supply.