nigeria power sector program

TRANSCRIPT

NIGERIA POWER SECTOR PROGRAM: STRATEGIES FOR EXPANSION OF THE OFF-GRID SECTOR

January 25, 2019

DISCLAIMER: This publication was prepared for review by the United States Agency for International Development. The author’s views expressed

in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States

Government.

1

NIGERIA POWER SECTOR PROGRAM:

STRATEGIES FOR EXPANSION OF THE OFF-GRID

SECTOR IDIQ Contract No. 720-674-18-D-00003 Power Africa Extension (PAE)

Task Order No. 720-674-18-F-00003 Nigeria Power Sector Program (NPSP)

USAID | Southern Africa

Contracting Officer’s Representative: John Garrison

Submitted: December 14, 2018

Resubmitted: January 25, 2019

ACKNOWLEDGEMENT:

This document was produced for review by the United States Agency for International Development. It was prepared

under Task Order No. 01: The Nigeria Power Sector Reform Program (the “Task Order”) of the Power Africa

Indefinite Delivery, Indefinite Quantity (“IDIQ”) Contract No. 720-674-18-D-00003 implemented by Deloitte

Consulting LLP.

2

TABLE OF CONTENTS

1. INTRODUCTION ....................................................................................................................................... 4

2. CUSTOMER ANALYSIS .............................................................................................................................. 5

2.1. Customer needs ......................................................................................................................... 5

2.2. Addressing customer needs ...................................................................................................... 8

3. STRATEGIES FOR EXPANSION ............................................................................................................. 15

3.1. Company group types introduction ........................................................................................ 15

3.2. Local Start-Ups ........................................................................................................................ 19

3.3. Emerging Household Names .................................................................................................. 26

3.4. Energy Access Pioneers ........................................................................................................... 32

3.5. International Independents ..................................................................................................... 40

3.6. Business model strategies specific to mini-grid developers .................................................. 45

4. STAKEHOLDER ENGAGEMENT ............................................................................................................. 48

4.1. Investors.................................................................................................................................... 48

4.2. International Donors ............................................................................................................... 66

4.3. Other Market Enablers ............................................................................................................ 73

4.4. Nigerian Government .............................................................................................................. 76

4.5. Community ............................................................................................................................... 78

5. ADDITIONAL RESOURCES ..................................................................................................................... 80

5.1. General off-grid energy resources .......................................................................................... 80

5.2. Solar Home System companies (and other standalone systems) specific resources ......... 81

5.3. Mini-grid specific resources ..................................................................................................... 81

LIST OF ACRONYMS

AECF – Africa Enterprise Challenge Fund

AFD – (Agence Française de Développement) French development agency

AfDB – African Development Bank

ALSF – Africa Legal Support Facility

BOI – Bank of Industry

CAPEX – Capital Expenditure

DCA – USAID Development Credit Authority

DFI – Development Finance Institution

DFID – Department for International Development (UK development agency)

DFS – Digital Finance Solutions

DisCo – Distribution Company

EBITDA – Earnings Before Interest, Tax, Depreciation, and Amortization

ESMAP – Energy Sector Management Assistance Program

EU – European Union

FEI – Facility for Energy Inclusion

FGN – Federal Government of Nigeria

FMCG – Fast Moving Consumer Goods

3

GIZ – Deutsche Gesellschaft für Internationale Zusammenarbeit (German development agency)

GMG – Green Mini-Grid

GoN – Government of Nigeria

ICT – Information and Communication Technologies

IFC – International Finance Corporation

kWh – Kilowatt Hours

LCA – Lead Contractor Agreements

MSME – Micro, Small, and Medium Enterprises

MYTO – Multi-Year Tariff Order

NED – Nigerian Energy Database

NEP – Nigeria Electrification Program

NERC – Nigerian Electricity Regulatory Commission

NESP – Nigeria Electricity Support Program

NCIC – Nigeria Climate Innovation Center

NGN – Nigerian Naira

NGO – Non-Governmental Organization

NiRER – Nigeria Renewable Energy Roundtable

NOMAP – Nigeria Off-grid Market Acceleration Program

NPSP – Nigeria Power Sector Program

O&M – Operations and Maintenance

OEM – Original Equipment Manufacturer

OGEAF – Off-Grid Energy Access Fund

PAE – Power Africa Extension

PAYG – Pay As You Go

PSA – Pooling and Servicing Agreement

PV – Photovoltaic

R&D – Research & Design

REA – Rural Electrification Agency

RMI – Rocky Mountain Institute

SEED – Sustainable Energy for Economic Development

SEFA – Sustainable Energy Fund for Africa

SHS – Solar Home Systems

SME – Small and Medium Enterprises

SOGE – Scaling Off-Grid Energy

SUNREF – Sustainable Use of Natural Resources and Energy Finance

TA – Technical Assistance

UNDP – United Nation Development Programme

USADF – United States African Development Foundation

USAID – United States Agency for International Development

USTDA – United States Trade and Development Agency

4

1. INTRODUCTION

This document is intended as a companion document to the NPSP Baseline Study and the NPSP

Capital Map and Donor Gap Analysis. This document provides an overview of successful

approaches to engaging in the off-grid energy market in Nigeria. Companies expanding in or

entering the Nigerian off-grid energy market can use this guide to refine their own strategies,

adapting from lessons learned and using an understanding of market needs to best fill the major

gaps.

The document has been developed in coordination with the NPSP Baseline Study through a process

involving direct interviews and secondary research. NPSP interviewed 29 SHS and mini-grid

companies, reviewed 21 select research materials and publications, 50 SHS and mini-grid company

websites and 10 websites for off-grid associations, conferences and initiatives. Additionally, NPSP

engaged SHS and mini-grid customers as well as non-users for whom off-grid solutions may be

appropriate to ascertain needs gaps and to validate (and challenge) perceptions of customer needs

held by leading off-grid companies. Finally, NPSP interviewed numerous market enablers such as

digital financial services providers for next generation business models and approaches.

Although this document is not intended as immediately actionable advice applicable to every

company in or entering the market, interested firms can reach out to the NPSP team (NPSP Chief

of Party, Mary Worzala, [email protected]) to learn more about how the information in this

document can be tailored to specific needs.

5

2. OFF-GRID COMPANIES CAN ADOPT NEW STRATEGIES TO

BETTER ADDRESS CUSTOMER NEEDS

This section leverages the NPSP Baseline Study, and some content of this section appears as written

therein. More details on the baseline for off-grid activities in Nigeria can be found in the NPSP Baseline

Study.

2.1. Customer Analysis – Who are the key customers and what are their

needs?

While the Nigerian off-grid energy market represents a large and diverse set of customers, the

major customer groups that are currently underserved by off-grid (and under-grid) energy

solutions can be categorized by proximity to the city, state of grid connection, use of energy, and

the likely best means of providing the most cost effective off-grid solutions. These customer

archetypes are not comprehensive but, rather, represent the major groups that can be well

served by existing off-grid technologies in Nigeria. Additionally, there are some customers that

fall within these categories but would not necessarily be good fits for any off-grid solutions for a

variety of reasons such as an inability to pay or geographical inaccessibility.

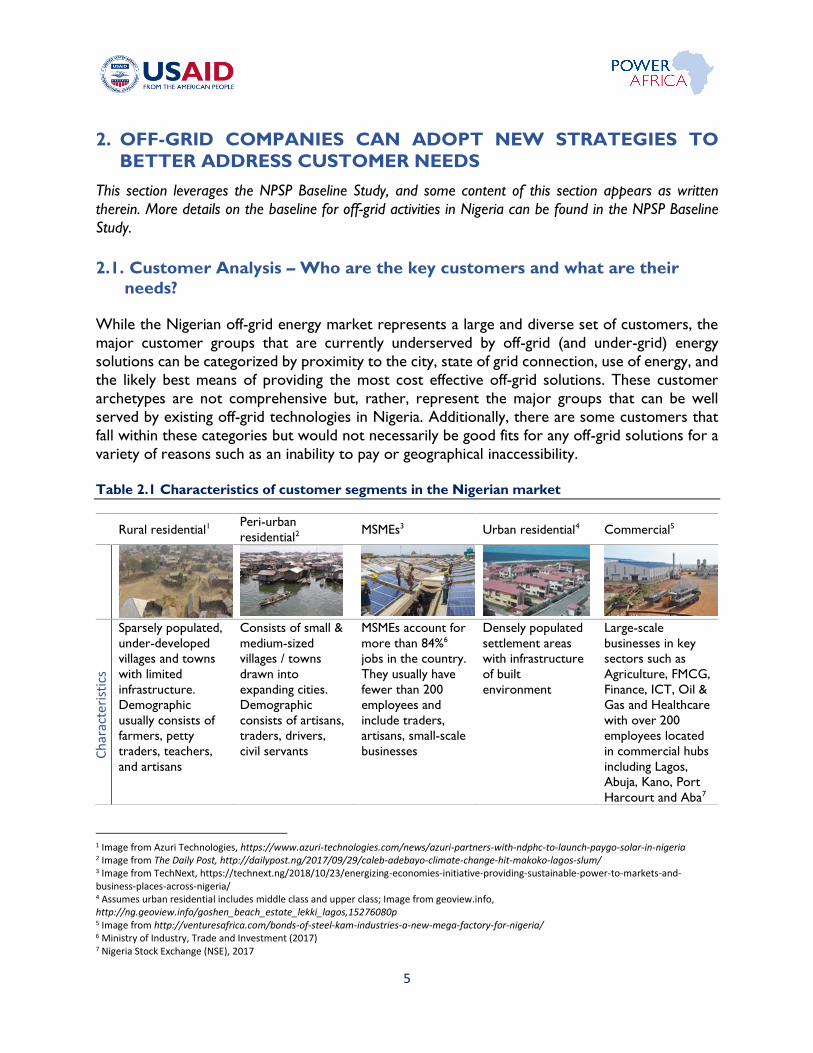

Table 2.1 Characteristics of customer segments in the Nigerian market

1 Image from Azuri Technologies, https://www.azuri-technologies.com/news/azuri-partners-with-ndphc-to-launch-paygo-solar-in-nigeria 2 Image from The Daily Post, http://dailypost.ng/2017/09/29/caleb-adebayo-climate-change-hit-makoko-lagos-slum/ 3 Image from TechNext, https://technext.ng/2018/10/23/energizing-economies-initiative-providing-sustainable-power-to-markets-and-business-places-across-nigeria/ 4 Assumes urban residential includes middle class and upper class; Image from geoview.info, http://ng.geoview.info/goshen_beach_estate_lekki_lagos,15276080p 5 Image from http://venturesafrica.com/bonds-of-steel-kam-industries-a-new-mega-factory-for-nigeria/ 6 Ministry of Industry, Trade and Investment (2017) 7 Nigeria Stock Exchange (NSE), 2017

Rural residential1 Peri-urban

residential2 MSMEs3 Urban residential4 Commercial5

Sparsely populated,

under-developed

villages and towns

with limited

infrastructure.

Demographic

usually consists of

farmers, petty

traders, teachers,

and artisans

Consists of small &

medium-sized

villages / towns

drawn into

expanding cities.

Demographic

consists of artisans,

traders, drivers,

civil servants

MSMEs account for

more than 84%6

jobs in the country.

They usually have

fewer than 200

employees and

include traders,

artisans, small-scale

businesses

Densely populated

settlement areas

with infrastructure

of built

environment

Large-scale

businesses in key

sectors such as

Agriculture, FMCG,

Finance, ICT, Oil &

Gas and Healthcare

with over 200

employees located

in commercial hubs

including Lagos,

Abuja, Kano, Port

Harcourt and Aba7

Ch

arac

teri

stic

s

6

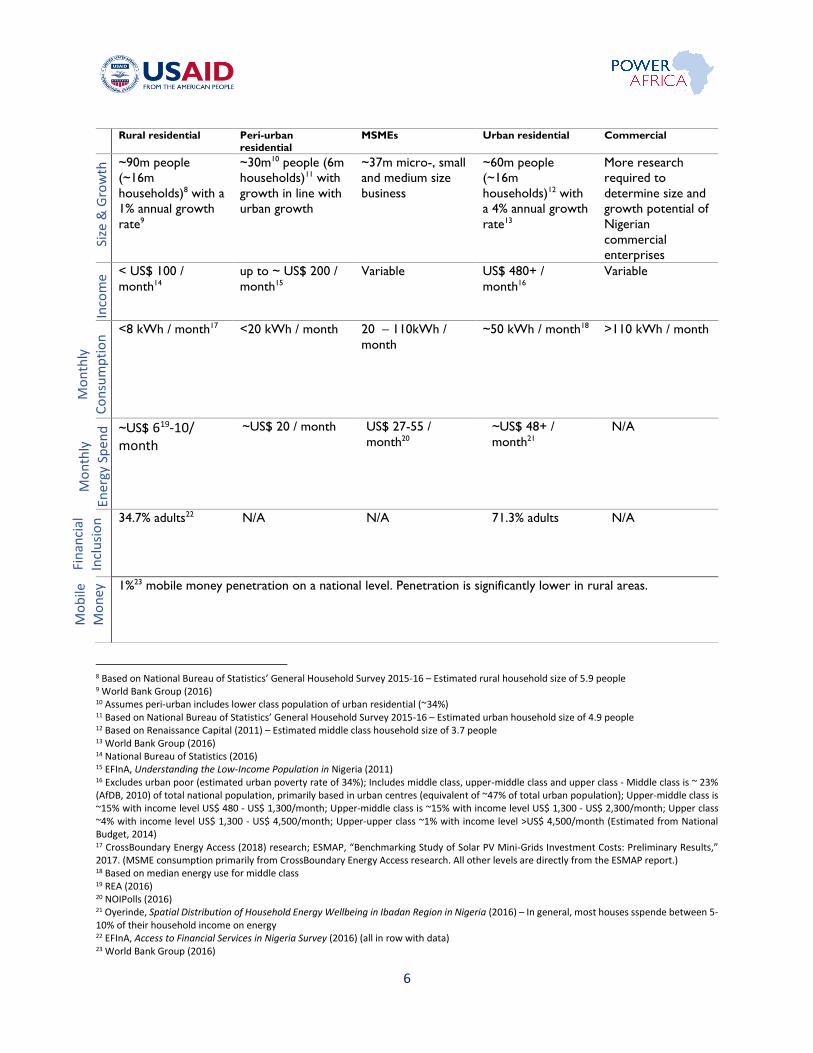

8 Based on National Bureau of Statistics’ General Household Survey 2015-16 – Estimated rural household size of 5.9 people 9 World Bank Group (2016) 10 Assumes peri-urban includes lower class population of urban residential (~34%) 11 Based on National Bureau of Statistics’ General Household Survey 2015-16 – Estimated urban household size of 4.9 people 12 Based on Renaissance Capital (2011) – Estimated middle class household size of 3.7 people 13 World Bank Group (2016) 14 National Bureau of Statistics (2016) 15 EFInA, Understanding the Low-Income Population in Nigeria (2011) 16 Excludes urban poor (estimated urban poverty rate of 34%); Includes middle class, upper-middle class and upper class - Middle class is ~ 23% (AfDB, 2010) of total national population, primarily based in urban centres (equivalent of ~47% of total urban population); Upper-middle class is ~15% with income level US$ 480 - US$ 1,300/month; Upper-middle class is ~15% with income level US$ 1,300 - US$ 2,300/month; Upper class ~4% with income level US$ 1,300 - US$ 4,500/month; Upper-upper class ~1% with income level >US$ 4,500/month (Estimated from National Budget, 2014) 17 CrossBoundary Energy Access (2018) research; ESMAP, “Benchmarking Study of Solar PV Mini-Grids Investment Costs: Preliminary Results,” 2017. (MSME consumption primarily from CrossBoundary Energy Access research. All other levels are directly from the ESMAP report.) 18 Based on median energy use for middle class 19 REA (2016) 20 NOIPolls (2016) 21 Oyerinde, Spatial Distribution of Household Energy Wellbeing in Ibadan Region in Nigeria (2016) – In general, most houses sspende between 5-10% of their household income on energy 22 EFInA, Access to Financial Services in Nigeria Survey (2016) (all in row with data) 23 World Bank Group (2016)

Rural residential Peri-urban residential

MSMEs Urban residential Commercial

~90m people

(~16m

households)8 with a

1% annual growth

rate9

~30m10 people (6m

households)11 with

growth in line with

urban growth

~37m micro-, small

and medium size

business

~60m people

(~16m

households)12 with

a 4% annual growth

rate13

More research

required to

determine size and

growth potential of

Nigerian

commercial

enterprises

< US$ 100 /

month14

up to ~ US$ 200 /

month15

Variable US$ 480+ /

month16

Variable

<8 kWh / month17

<20 kWh / month 20 – 110kWh /

month

~50 kWh / month18 >110 kWh / month

~US$ 619-10/ month

~US$ 20 / month US$ 27-55 /

month20

~US$ 48+ /

month21

N/A

34.7% adults22 N/A N/A 71.3% adults N/A

1%23 mobile money penetration on a national level. Penetration is significantly lower in rural areas.

Fin

anci

al

Incl

usi

on

Si

ze &

Gro

wth

In

com

e

Mo

nth

ly

Co

nsu

mp

tio

n

Mo

bile

Mo

ney

M

on

thly

Ener

gy S

pen

d

7

Numerous companies (as detailed in the Baseline Study) are already providing energy solutions

across these five customer groups. However, significant opportunities remain for additional off-

grid companies to enter Nigeria and offer energy services. An influx of new international entrants

over the past year is a strong indicator for the variety of opportunities in the market.

To gain consumer feedback on where energy needs were and were not being met by existing

solutions, to determine the major barriers to increasing use of off-grid products, and to ascertain

consumer perceptions (and misperceptions) about off-grid energy solutions, NPSP conducted

interviews with Nigerian consumers across groups of off-grid solution users and non-users. Refer

to the Appendix (also in NPSP Baseline Study Section 2.1 Demand Side Overview and Section

2.3 Addressable Market) for a high-level overview of off-grid demand and gaps in Nigeria.

“Current status” classification of customers is defined by whether they currently use any kind of modular solar solutions. “Consumption potential” classification of customers is as follows:

• Low use: rural residential, peri-urban residential, MSMEs, urban residential (middle class)

• Medium / high use: commercial, urban residential (~5%: upper class and upper-upper class

may also be included)

Key themes emerge by customer group:

Table 2.2 Themes and challenges by customer group

Consumption potential

Low

(<50kWh/month)

Medium / high

(>50kWh/month)

Curr

ent

statu

s

Use

r

Common themes:

• Choice to start using solar is

almost entirely price driven

• Sales driven by word-of-mouth or

door-to-door

• Relationship between

customer and agent is critical to

continued payment - mentioned

agents being part of their

community / friends - creates an

accountability measure

Common challenges:

• Batteries stop holding charge after

just 4 months

• Dust accumulates on panels after 6

months, making them notably less

effective

Common themes:

• Sales driven by word-of-mouth

or door-to-door

• Relationship directly with

company owner (or associate)

is key to building trust around

maintenance and customer

service

• Payment plans often

negotiated directly with company

based on personal relationships

Common challenges:

• Batteries failed and needed to

be replaced

• Dust accumulates on panels after

6 months, making them notably

less effective

8

• Low response rate on customer

service

No

n-u

ser

Common themes:

• General excitement about

growth in availability of solar

• Strong awareness of at least one

friend, family member, or neighbor

using SHS

Reasons for non-use:

• Never exposed to sales agents or

marketing material in general

• Perception of solar as an

expensive option

• Able to find lower cost (or no cost)

alternatives for low energy use needs

Common themes:

• Interest in renewable energy for

social and environmental

reasons

• High value placed on

reliability

Reasons for non-use:

• Concern about battery life –

high cost of battery replacement

• Sunk cost fallacy – recent

purchase of generator prevents

transition

• Minimal exposure to sales agents or marketing material in

general

2.2. Off-grid companies can implement strategies to overcome the challenges identified

by customers and potential customers regarding off-grid energy solutions

Insights from customer and potential customer feedback can help off-grid companies adjust their

approaches along the value chain – from marketing modifications to after sales customer

education improvements. The section below highlights the key customer-centric challenges

identified through customer interviews and proposes strategies for overcoming these challenges.

The challenges and strategic approaches to overcoming challenges in this section are broadly

applicable to different off-grid company types.

Customer experience with SHS sales and marketing:

• Customers across energy use categories rely largely on peer recommendations for

information about off-grid energy solutions. This trend is particularly true for niche players

but also remains a

challenge for the

companies already

operating at scale.

Customers note that

while they have family or

peers they know to be

using solar solutions,

they lack knowledge

about acquiring such

services.

I would love to try solar. I have heard that it is clean and cheap and not noisy, but I have never seen it for sale in the market. It is easy to find

what I need for my generator - Hospitality industry employee, peri-urban

Lagos

“

”

9

Some non-users remark that while they would like to use solar solutions and have heard

positive reviews, they find it far easier to access the fuel and parts they need for

maintenance for generators.

• The limiting factor for growth of solar sales in some market segments may simply be a

result of the relatively small amount companies that are currently investing in Marketing

and Sales. For example, one leading SHS company in Nigeria has largely relied on a passive

sales strategy for most of its growth through 2018. The company, Lumos, partnered with

a major telecommunications company, MTN, and, until recently, relied almost entirely on

agents in the telecommunications company’s store fronts to drive sales of its systems.

While this passive approach was an excellent way to increase sales while expending

relatively little on marketing and sales efforts, it is seriously limited by the number of

customers already visiting the telecom storefronts. Since many of these customers have

already been exposed to SHS solutions, new customers will need to be gained through

more active sales strategies (and potentially at higher costs).

In addition to active sales and marketing strategies, off-grid companies can formalize

‘word-of-mouth’ marketing by incorporating referral program incentives such as

discounts, credits, or prizes. Through incentive programs, the companies can nurture

customers while minimizing advertising spend. Referral strategies tend to be the most

effective in ethnically defined and close-knit family neighborhoods, where outsiders such as external salespeople are often viewed with skepticism. Since the benefits of solar are

Companies entering or growing in the off-grid energy market in Nigeria can

consider sales strategies that mirror the sales of generator fuel and parts. To

reach scale, companies will need to change customer behavior around the purchase of

energy solutions, moving their point of purchase from markets to the preferred solar

solution sales location (such as locations well synced with partnerships strategies: mobile

service provider stores, FMCG stores, etc.). Alternatively, they can adapt to existing

consumer behavior by meeting them at their current location of energy purchase (such as

where they currently buy petroleum, diesel, and generators or generator parts).

Nigerian SHS companies can look to East African SHS companies, many of

whom have actively courted customers through mobile sales units, to develop

their own active sales strategies. Greater proliferation of active sales units could help

companies access larger numbers of customers that are eager to explore solar solutions.

Mobile sales units include door-to-door sales as well as mobile kiosks. SHS companies in

East Africa have experienced significant success in sales and marketing through engagement

of agent networks to bring product demonstrations to the doors of residences in target

markets. Nigerian SHS companies, some of whom have relied on more passive sales

strategies dependent on strategic partnerships, can emulate this model.

10

often best validated by satisfied users, referrals remain the most cost-effective way to

acquire new customers.

• Finally, there is already significant misinformation about solar solutions among non-users

in the lower energy potential consumer segment. Many believe SHS are far more

expensive than traditional sources of power.

Customer experience and perception regarding batteries:

Poor performance of batteries and concerns about the high replacement cost for batteries

remains an issue among customers across all use levels. Non-users remark that when

evaluating solar options as replacements for current energy sources, they have significant

concerns about the longevity of batteries.

Off-grid companies may be able to capture market share by incorporating high performing

batteries with performance guarantees. Medium to high energy users have also expressed

a willingness to pay more for guaranteed battery performance.

Poor performance of batteries may also be a result of misuse or poor load management.

Some batteries, for example, lose capacity to hold charge significantly faster if they are

frequently fully charged and fully discharged.

A successful sales and marketing strategy will need an educational component

to clarify the economics of SHS, demonstrating cost effectiveness for lower

energy use customers in particular.

Incorporating performance guarantees for batteries may enable off-grid

companies to charge a premium while assuring customers of performance over the long-term.

11

• Whatever the case, existing off-grid companies need to improve their ability to address poor battery performance. Each case of poor battery performance (or poor performance

of any solar component) damages the overall reputation of solar as a viable energy

replacement.

While there is not yet a universal product certification label for high quality SHS

components, including batteries, the World Bank Group through Lighting Global has

developed a quality assurance process and reports on its website all products that meet

these standards. Currently, companies whose products meet Lighting Global quality

standards can use specific pre-approved phrases in their marketing, but there is not yet a

label for this certification.24 Pre-approved phrases include: (a) “Meets/Passed Lighting

Global Quality Standards,” (b) “This product meets/has passed the Lighting Global Quality

Standards,” or (c) “Third-party test results verification for product are available at

www.lightingglobal.org/products/product-name/.” Off-grid companies in Nigeria could

collaborate with each other and with Lighting Global to develop a widely recognizable

certification label – demonstrating when a product is Lighting Global certified – to help

customers understand when they are purchasing sub-standard products, thus protecting

the reputation of high-quality products. A physical label could help customers (both in

Nigeria and elsewhere) unable to research which products are Lighting Global certified

online. It would also help popularize the Lighting Global certification, compounding its

positive quality assurance effects.

24 Lighting Global, “Communications and Branding Guidelines,” 2014.

Better education about load management and battery use specific to each system’s battery may help reduce customer misuse, thereby reducing reputational damage and/or the need for costly replacements. It is important for SHS companies to educate customers, most of whom are new to the technology, on how to optimize performance of a solar home system. The customer education must be appropriately tailored to each demographic, finding the right balance between simplicity and comprehensiveness. When designing educational programming around product use, companies can better adapt to local needs by engaging local representatives, such as community leaders or agents. For example, customer education on product use can better account for regional language barriers. Companies serving rural areas where English is not the primary language of commerce (or where literacy is particularly low) can adapt educational materials to local languages.

12

Customer experience regarding dust:

• Customers across use levels, particularly those in Abuja and other parts of Northern

Nigeria, remark that accumulation of dust has a significant impact on the effectiveness of

their SHS. They also note that they are not educated on means of quickly remedying this

challenge

25

Finally, SHS companies should take into consideration the locations of

customers when allocating resources to management of dust. Customers at

street level along dirt roads in the dry season will likely have far greater needs than

customers mounting SHS on the 2nd or 3rd floor of buildings along asphalt roads, for example. Additionally, communities with limited access to water may be more

dramatically impacted by the accumulation of dust. Companies can differentiate

themselves through superior customer care in recognizing the unique circumstances of

each installation.

25 Duke University, "Large reductions in solar energy production due to dust and particulate air pollution," Mike Bergin, Chinmay

Ghoroi, Deepa Dixit, Jamie Schauer, Drew Shindell. Environmental Science & Technology Letters, June 26, 2017.

In the meantime, companies can work with Lighting Global to ensure their own products

meet Lighting Global standards. Additionally, in their customer education efforts,

companies can reference the Lighting Global standards to demonstrate the

quality of their own products while dissuading use of substandard products.

Two strategies are needed to address customer concerns regarding aggregation of dust:

First, customers need to be educated on the real impact of dust accumulation.

Although significant losses can be associated with large amounts of airborne

particles (as much as 35% in regions with substantial migratory dust), PV panels

remain largely effective with minor dust accumulation. Customers may see dust

and consequently believe they are getting less energy from their SHS, even if this is not

entirely true. Education at point of sale can help customers understand to what degree this

is true and how or if they should intervene. Proper instructions for panel cleaning (and

effects of dust accumulation) can be included in the initial instructional materials.

Second, customers should be given adequate tools and instructions to clean

panels without causing them damage. Some customers interviewed noted that they

reached out to their SHS company when dust aggregated. This burdens a SHS company’s

customer service and can be more cost-effectively handled through customer self-care.

13

Customer experience regarding customer service:

• Long-term customer satisfaction with customer service is driven largely by the

relationship between customers and their agents or primary points of contact with their

off-grid energy service provider. Customers appreciate when agents (or primary points

of contact with companies) are individuals from their own communities. Building this trust

helps customers tolerate maintenance issues or challenges with performance. The

relationship gives them

the assurance that an

individual they know

personally can help them

address any issues. As

companies work to scale

their customer service,

they can continue

gaining these benefits by

recruiting agents from

local communities.

• Some customers of smaller off-grid companies have reported having difficulty contacting

their customer service representatives, noting that these individuals won’t answer phone

calls for extended periods. New entrants can consider differentiating themselves through

superior infrastructure for customer service and maintenance.

Existing players who do not yet have adequate resources or infrastructure to address

customer concerns quickly should consider the impact that failure to respond may have

on the reputation of their companies as well as on off-grid solutions as a whole. There

may be long-term damage to sales.

As off-grid companies scale their operations in Nigeria, it is essential that their service

retain a human face by sourcing sales agents from the communities where services are

being provided.

When our agent comes, he really listens to our concerns

- Owner of small gambling / betting business in Abuja

“

”

14

There are two important aspects of customer service that will significantly improve

interactions with customer:

- Quick and efficient response: To deliver prompt service, off-grid companies need

to have call centers and dedicated agents able to access customers in remote areas.

Off-grid companies need to build the internal capacity to be able to deploy agents

quickly and effectively to avoid losing customer trust. In areas with lower mobile

penetration, companies can ensure agents are well-prepared to address common

customer service challenges and that they are incentivized to address customer

problems quickly

- Proactive outreach: Off-grid companies need to be able to quickly identify unsatisfied

customers through a combination of proactive outreach and customer data

management. It is particularly crucial for lower income customers that may not have

airtime for calls. These companies can use agents to consistently collect customer data

and track metrics in order to identify triggers of poor functionality or dissatisfaction.

The service teams will need to quickly intervene once alerted.

15

3. STRATEGIES IN THE OFF-GRID SECTOR CAN BE CUSTOMIZED

TO THE SPECIFIC CHARACTERISTICS OF EACH COMPANY

This section leverages the NPSP Baseline Study, and some content of this section appears as written

therein. More details on the baseline for off-grid activities in Nigeria can be found in this document.

3.1. Off-grid companies in Nigeria can be categorized into four groups by their

key characteristics Key company characteristics among off-grid companies in Nigeria are determined largely by two

factors: the company’s business life cycle stage and whether the company is local or international.

• Business needs can vary significantly depending on a company’s current business

life cycle stage. To meet these needs, firms at different stages in their business life cycle

must adopt different strategies. Also, business life cycle stage progression is generally gradual,

so needs may need to be met incrementally – for example, it may not benefit a Seed stage

company to begin implementing strategies specifically applicable to Growth stage companies.

Seed stage companies need to prove their models, so the strategies associated are largely

about accelerating that process. Meanwhile, strategies for Growth stage companies largely

involve upscaling operations and management, which would be less impactful on a Seed stage

company. Gradual advancement is also critical for the fundraising process. As businesses

mature, they typically gain access to lower cost capital

• Company origin (international versus local) matters because international

companies often have far greater access to international funding sources, from

foundation grants to Silicon Valley venture capital to Private Equity. While local companies

may also gain access to such funding, it is typically far more accessible for international

companies due to improved access to networks and a greater familiarity with the fundraising

landscape. Local companies, however, have local knowledge and expertise that international

companies are less able to access except through partnerships and targeted hiring of local

staff into key positions. Because partnerships come with costs, and talent is often scarce,

there is a clear advantage to having in-house access to deep knowledge of local markets

Using these characteristics, companies in the off-grid space can be roughly categorized into four

groups in the figure below.

16

Figure 3.1 Nigerian off-grid company categories

Local Start-Ups

The vast majority of homegrown small and medium enterprises (SMEs) in the off-grid solar market

fall into this category. These are usually in seed or start-up stages with limited funding; they typically assemble products from low-tech, locally adapted, or open-source designs or source

customer-ready products entirely from other companies. Most are still in a ‘proof-of-concept’

phase and require business model refinement such as attracting and optimizing funding, product

selection and sourcing, and/or effective marketing and distribution strategies to capture market

share. Examples of Local Start-Ups in Nigeria include: Solarpawa, Folub, and Solar Kobo.

Emerging Household Names

Emerging Household Names are home-grown companies that have strong local capabilities and a

distribution network to go with their scale. Often, they are able to vertically integrate their value

chain due to their technological advancement and/or core competencies. They have an

understanding of the technical fundamentals such as product design, installations, distribution, and

after-sales services (though may still have substantial room for improvement in one or more of

these areas). Arnergy is one of the emerging SHS players with an installed capacity of over

Seed Expansion

Loca

l

Low-to

-High In

tegra

tion fr

om R

&D to D

istrib

ution

Start-Up Growth

Inte

rnat

ion

al

Emerging

‘Household Names’

Energy Access

Pioneer Brands

International

Independents

Local

Start-Ups

Business Life Cycle Stage

Ori

gin

17

1.5MW. They have products tailored to various market segments but have now shifted focus to

urban and commercial consumers. Sales, installation, and distribution are carried out by a

combination of a dedicated in-house team and directly recruited and trained agent network. End-

user support is provided by specialized trained agents, and payments and collections are carried

out through an online payment portal. The company has a strong technological focus using

algorithms to manage credit risk and optimize customer experience. This business model has

seen Arnergy steadily increase market share.

Energy Access Pioneer Brands

These are primarily expanding international firms that are buoyed by success in the East African

off-grid market. They typically focus on building distribution partnerships with strong local players

to sell their energy access technologies. Within the last two years, nearly 10 companies, including

leading East African players such as Greenlight Planet, d.light, Off-Grid Electric (operating as Zola

Electric), Fenix International, and BBOXX, have entered the Nigerian market. Greenlight Planet has two distinct business models for products sales. These are direct sales to end-users and

distribution partnerships through microfinance institutions like LAPO Microfinance Bank and

some FMCG companies. Lumos formed a partnership with Nigeria’s largest mobile network

operator, MTN, to provide low-cost MTN Mobile Electricity or ‘MTN Yellow Box’, a pay-as-you-

go solar home system.26

International Independents

These are typically start-ups or smaller firms from more developed markets. Their primary focus

is designing and marketing a suitable single product for the Nigerian market. Manufacturing of

devices is usually outsourced to other companies, while they tend to form partnerships with

other providers for distribution. An example of an international independent is Oolu Solar, a

solar homes solutions company founded in 2015 that raised initial seed round funding through

Silicon Valley’s Y Combinator. Oolu Solar launched a pilot in Senegal and since then has expanded

into other West African countries including Nigeria. Oolu has received funding and significant

strategic support from international early stage investor Persistent Energy, which is a common

characteristic of International Independents. Oolu Solar started piloting its products in South-

West states including Oyo, Osun, and Ekiti. Oolu Solar is providing two sets of products that

match the income levels of rural and peri-urban Nigerian consumers. It is also offering flexible

payments options like annual and monthly payments in addition to outright purchase. This

provides more rural households an opportunity to afford its solar systems depending on their

income levels. As a start-up, Oolu has chosen to focus on specific aspects of the value chain such

as distribution and customer acquisition to keep costs low, and they are not involved in

manufacturing.27

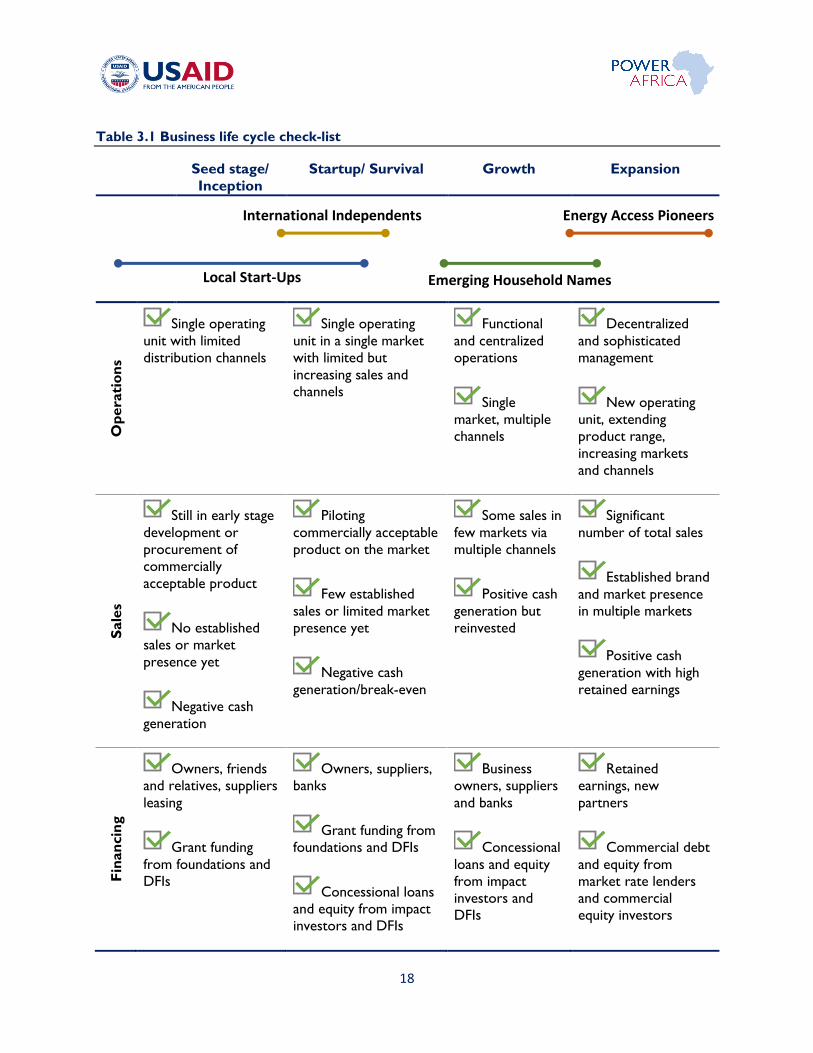

Companies can use the check-list below to determine their current business life cycle stage.

26 CrossBoundary research 27 Oolu Solar (2018), https://oolusolar.com

18

Table 3.1 Business life cycle check-list

Seed stage/

Inception

Startup/ Survival Growth Expansion

Op

era

tio

ns

Single operating

unit with limited

distribution channels

Single operating

unit in a single market

with limited but

increasing sales and

channels

Functional

and centralized

operations

Single

market, multiple

channels

Decentralized

and sophisticated

management

New operating

unit, extending

product range,

increasing markets

and channels

Sale

s

Still in early stage

development or

procurement of

commercially

acceptable product

No established

sales or market

presence yet

Negative cash

generation

Piloting

commercially acceptable

product on the market

Few established

sales or limited market

presence yet

Negative cash

generation/break-even

Some sales in

few markets via

multiple channels

Positive cash

generation but

reinvested

Significant

number of total sales

Established brand

and market presence

in multiple markets

Positive cash

generation with high

retained earnings

Fin

an

cin

g

Owners, friends

and relatives, suppliers

leasing

Grant funding

from foundations and

DFIs

Owners, suppliers,

banks

Grant funding from

foundations and DFIs

Concessional loans

and equity from impact

investors and DFIs

Business

owners, suppliers

and banks

Concessional

loans and equity

from impact

investors and

DFIs

Retained

earnings, new

partners

Commercial debt

and equity from

market rate lenders

and commercial

equity investors

International Independents

Local Start-Ups

Energy Access Pioneers

Emerging Household Names

19

The strategies companies can adopt to succeed in the Nigerian off-grid market are determined

to a large degree by the company’s current group type because of each group’s competitive

advantages. Typically, international companies benefit from easier access to funding, and local

companies benefit from local knowledge and expertise. Additionally, later stage companies benefit

from significant operational experience.

The sections below describe for each major off-grid company group type, what resources give

them unique advantages in the Nigerian market, what unique challenges they face, how success

can be defined, and strategies for using their resources to succeed.

3.2. Local Start-Ups can leverage their local advantages to become Emerging

Household Names

3.2.1. Defining success in growth

Success for Local Start-Ups entails advancing through the business stage life cycle. Local Start-

Ups are either in their Seed or Start-Up stage, with the majority in Nigeria currently in their

Start-Up stage. Seed stage Local Start-Ups must advance to Start-Up/ Survival stage, and Start-

Up stage companies must advance to Growth stage. Operational, sales, and financing

improvements, as described in the table below, are the core characteristics of business stage

advancement.

Table 3.2 Defining growth for Local Start-Ups

Seed Start-up Growth

Key issues

Sales

• Obtaining

customers

Operations

• Economical

production

Sales

• Revenues

Operations

• Expenses

Sales/Operations

• Managed

growth

Financing

• Accessing

resources

OP

ER

AT

ION

S

Management

role and style

• Direct

supervision

• Entrepreneurial,

individualistic

• Supervised supervision

• Entrepreneurial,

administrative

• Delegation,

coordination

• Entrepreneurial,

coordinated

Organization

structure • Minimal or no

structure • Minimal structure

• Functional,

centralized

Product and

market

research • Minimal research • Some initial research

• Some new

product

development

Systems and

controls

• Simple

bookkeeping,

eyeball control

• Simple bookkeeping,

personal control

• Expense control

• Accounting

systems, simple

control reports

20

Seed Start-up Growth

FIN

AN

CIN

G Major source

of finance

• Owners, friends

and relatives,

suppliers leasing

• Owners, suppliers,

banks

• Banks, new

partners,

retained

earnings

Major

investment • Plant and

equipment • Working capital

• Working capital

• Expanding

manufacturing

capacity (if

applicable)

SA

LE

S

Cash

generation • Negative • Negative/breakeven

• Positive but

reinvested

Product-

market

• Single line and

limited channels

and markets

• Single line and market

but increasing scale and

channels

• Broadened but

limited lines

• Single market,

multiple

channels

Another way to define success for Local Start-Ups: they must become Emerging Household

Names.

21

Figure 3.2: Advancing in business life cycle, Local Start-Ups

3.2.2. Competitive advantages

The core advantage of a Local Start-Up is almost entirely its local expertise and access to local

knowledge. Local Start-Ups are better positioned to understand the unique logistical and

operational difficulties that must be overcome to operate in Nigeria. They also are better

connected to local business networks, which they can leverage for knowledge and/or advocacy

when problems arise.

Considering the key functions along the off-grid company value chain, this local expertise is most

valuable for two functions: (1) Sales & Distribution and (2) Payments and Collections. This is

largely why Local Start-Ups’ core strengths tend to be in these two functions.

Seed Expansion

Loca

l

Low-to

-High In

tegra

tion fr

om R

&D to D

istrib

ution

Start-Up Growth

Inte

rnat

ion

al

Emerging

‘Household Names’

Energy Access

Pioneer Brands

International

Independents

Local

Start-Ups

Business Life Cycle Stage

Ori

gin

Advance in Business

Life Cycle to compete with Emerging Household Names

22

Sales & Distribution in the off-grid sector in Nigeria remains largely dependent on word-of-

mouth and door-to-door sales. Local Start-Ups can engage their personal networks to build their

initial customer base, enabling the business to have a local human face. Indeed, many customers

of Local Start-Ups note that their first point of contact with the business was with a business

owner directly or with a friend (or friend of friend) of the owner or an employee. This

personalized approach to sales helps build trust between the customer and the business –

something much more difficult for an international player to do.

Payments & Collections in the off-grid sector in Nigeria are managed through mobile apps or

online web portals, cash collections through door-to-door agents or stationary kiosks, USSD

codes, and/or mobile money. Due to mobile money regulatory challenges and low mobile money

penetration (less than 2%) most off-grid companies in Nigeria still rely heavily on agent networks

for collection. Local Start-ups can leverage their knowledge of local communities and gain an

advantage with door-to-door agents and agents at kiosks who are well-connected within communities, helping ensure timely payments through social pressures while the company is still

refining other aspects of its business model. Strong agent networks will likely remain essential

even as regulations related to mobile money become less restrictive because of Nigeria’s low

mobile money penetration and challenges to internet reliability.

3.2.3. Challenges

To advance their companies along the business stage life cycle, Local Start-Ups can focus efforts

on overcoming core operational, sales, and financing challenges.

The greatest Operational and Sales challenges include:

• Low production volume makes Production & Assembly extremely costly per unit

• Word-of-mouth and door-to-do Sales & Distribution work well on a small scale but

are ineffective for reaching less accessible markets

• Because Local Start-Ups rely on lean teams, they often do not have the capacity to respond well in After Sales Support. Additionally, they lack the operational expertise

necessary to effectively deliver customer support

The greatest Financing challenges specific to Local Start-Ups include:

• Inability to demonstrate business success and potential due to poor bookkeeping or

inability to track key performance metrics

• Lack of familiarity with investor expectations, data needs, or manner of communicating

23

3.2.4. Strategies to grow

Figure 3.3: Strategic growth focus areas along value chain, Local Start-Ups

The competitive advantages and key challenges stated above are true for most Local Start-Ups in

the off-grid space in Nigeria. For earlier stage companies to compete with the most successful

Local Start-Ups, they usually must emulate their competitive advantages. Key strategies to

maximize potential for success include:

• While some Local Start-Ups choose to make direct purchases from international OEM

suppliers (such as from China), most are well-suited to partnerships with larger SHS

players for Production & Assembly, such as International Energy Access Pioneers. There

is a strategic advantage in using Energy Access Pioneers for Production &

Assembly partnerships in that they provide superior quality control and

reduce the risks of regularly sourcing good products by relying on existing

established supply chains. The alternatives for quality control, such as on-site

inspections at the point of production or post-delivery inspections are costly and time

consuming, rarely an effective use of energy for resource-constrained Local Start-Ups.

Early investment in quality control is essential to reducing After Sales Support costs and

to avoiding brand damage to help maintain sales growth.

Local Start-Up Solarpawa, for example, has opted to purchase its products from

International Energy Access Pioneer Fosera (Germany-based). This partnership allows

Solarpawa to focus on its Sales & Distribution with the guarantee of high-quality products with minimal investment of time and energy at this point in the value chain.

Note: when Local Start-Ups intend to use a partnerships approach for production and

assembly of systems that relies on an Energy Access Pioneer, they should be wary of the

potential for the Energy Access Pioneer to enter the market. Some Energy Access

Pioneers, such as d.light, have used local company partnerships in Nigeria before entering

the market themselves. Local Start-Ups can mitigate this risk by evaluating the market

entry strategy of their potential partner. If the partner has previously used local

partnerships to evaluate a market before entering, this may be a risky partnership. While

Research & Design

Sales & Distribution

Payments & Collections

Consumer Finance

After Sales Support

Production & Assembly

Marketing

Opportunity for internal improvement

Opportunity for partnership

Lower priority for current stage

Strategic focus areas

Currently a core strength (Note: for some areas that are already core strengths, companies can continue making strategic improvements)

24

it should not necessarily be a strategic priority at this stage in the business life cycle, Local

Start-Ups can also consider Marketing strategies that preemptively reduce the risk of

competition from a partner entering the market. For example, if the Local Start-Up brands

the products with its own product name, it may be able to retain its customers more

easily if the Energy Access Pioneer partner enters the market. Solarpawa has taken this

approach.

• Local Start-Ups can use their existing local advantages and can follow the

model of Emerging Household Names to increase control over and build up

their agent networks. Exercising control over agent networks is an efficient

means of improving three functions across the value chain that are essential

to Local Start-Up growth.

First, investment in agent network training and build-up has significant impact on

effectiveness of Sales & Distribution. Arnergy, a Local Household Name, for example, has

directly recruited and trained over 1,000 agents for sales and distribution and has built an

in-house team of 40 (as of Oct. 2018). Arnergy has avoided any major partnerships for

sales and distribution (contrary to the strategies of International Energy Access Pioneers)

in order to avoid loss of profits through such partnerships. Additionally, because Arnergy

has trained the agents themselves, they can more closely control the quality of the

customer experience. Local Household Names are best positioned to follow the approach

that Arnergy has taken. They benefit less from local sales & distribution partnerships than

an International Energy Access Pioneer might and also likely are better equipped to handle

gradual growth rather than accelerated growth associated with large telecom or FMCG

partnerships.

Second, the same agent network developed for Sales & Distribution can also be effectively

used for Payments & Collections. A number of Emerging Household Names, like ASolar,

operate as many as 24,000 units while still using cash payments through stationary and

mobile agents.

Note: While Local Start-Ups are well-positioned for cash collections through agent

networks at a small scale and even as they reach Growth stage, this approach becomes a major challenge as Local Emerging Household Names attempt to move into an Expansion

phase and/or to compete with International Energy Access Pioneer Brands, as will be

discussed in the section below.

Finally, Local Start-Ups can use the same agent networks required to scale their systems

for Sales & Distribution and Payments & Collections to scale After Sales Support.

Customers of Local Start-Ups often note some lack of satisfaction with their After Sales

Support, including lack of responsiveness, inability to quickly address issues, failure to

follow through on service requests, or lack of understanding of how to reach out for

support in the first place.

25

Local Start-Ups can differentiate themselves by offering superior customer support. A

strategic focus on After Sales Support will also have medium-term benefits for sales,

especially for Local Start-Ups, which rely so heavily on word-of-mouth for sales. Intensive

training of agents (or other in-house team members) can help reduce problems related

to After Sales Support.

3.2.5. Some Local Start-Ups have adopted alternative strategies to play niche roles in the market

Some Local Start-Ups have developed businesses to serve as niche providers at a single point in

the value chain rather than attempting to work toward vertical integration. By focusing on a

specific strategic point in the value chain, such as providing local Production and Assembly to

reduce cost of imports for other companies, Local Start-Ups can grow horizontally rather than

through vertical integration.

ESUSU AGENTS | Leveraging local thrift savings networks for affordability

The Esusu scheme is prevalent among many market women who contribute a daily portion

of their trading profit to a collective. This scheme becomes an informal savings and credit

system among many unbanked women in rural communities. There is an opportunity for

local start-ups to partner with these Esusu groups in various communities for sales and

distribution. The local companies can also look into consumer financing through Esusu

groups since these are established informal microfinance groups. Local Start-Ups can work

with Esusu groups to structure monthly repayment options for SHS. Over 50% of the

Nigerian population is unbanked and most of the micro-entrepreneurs largely rely on the

informal sector due to stringent conditions of formal financial institutions to practices like

granting of loans. Additionally, many commercial banks and even microfinance institutions

do not make funds available to reach lower income customers.

In Nigeria thrift collection known as

Esusu, Ajo, or Adashe, has been executed on a micro level. Members

of many communities save money in

small rotating contributory savings

schemes with trusted community

members. At the end of each month,

contributors collect the money they

have saved. These group savings serve

as a source of borrowing in

emergencies, a way to grow savings

or a means to achieve a communal

goal.

26

For example, Greenage Technologies is a Nigerian company founded in 2017 that produces

inverters locally. Greenage argues that local production helps with adaption to Nigerian use and

climate (such as “short-circuit detection, which is not common in foreign products”). They also

suggest that local production better enables them to keep costs low.28

Another example of a niche player, Blue Camel

Energy Limited is a Nigerian renewable energy

company that specializes in solar powered

outdoor lighting, such as street lights, solar

systems for high-use houses and office buildings,

and solar borehole and water reticulation systems.

Blue Camel is unique for having its own Production

Plant and Training Center in Kaduna State, giving it the advantages of local production.

There may be additional opportunities in the off-grid energy sector for local

production of SHS and mini-grid components that can benefit from savings from

import duties and from designs specific to unique Nigerian challenges and use

patterns. Similarly, there may be additional opportunities for Nigerian companies to

serve off-grid energy companies through provision of local sales and distribution

services and local installation and technical maintenance, which a November 2018

GOGLA brief suggests account for the majority of local jobs created in the off-grid

energy value chain.29

Engaging USAID Power Africa: NPSP can provide early stage fundraising support to Local

Start-Ups by reviewing the identified capital needs, advising on pros and cons of various funding

structures, and reviewing and providing recommendations on fundraising materials like

investment teasers. NPSP can connect Local Start-Ups to well-funded Energy Access Pioneers to

bridge the gap between local market knowledge and operational capabilities and funding.

3.3. Emerging Household Names can leverage their local advantages and in-

country operational experience to compete with Energy Access Pioneers

3.3.1. Defining success in growth Success for Emerging Household Names entails advancing through the business stage life cycle

from the Growth stage to the Expansion stage. Operational, sales, and financing improvements,

as described in the table below, are the core characteristics of business stage advancement. Some

Emerging Household Names could be considered to have already advanced to Expansion stage.

For these companies, success largely revolves around ability to increase market penetration and

enter new markets.

28 https://www.greenagetech.com/the-company/ 29 GOGLA, “Employment opportunities in an evolving market; Off grid solar: creating high-value employment in key markets,”

2018.

27

Table 3.3 Defining growth for Emerging Household Names

Growth Expansion

Key issues

Sales

• Managed growth

Operations

• Accessing resources

Financing

• Financing growth

Operations

• Maintaining control

OP

ER

AT

ION

S

Management

role and style

• Delegation, co-ordination

• Entrepreneurial,

coordinated

• Decentralized and

coordinated

• Professional

• Administrative

Organization

structure

• Functional, centralized • Functional, decentralized

and coordinated

Product and

market

research

• Some new product

development

• New product innovation

• Market research

Systems and

controls

• Accounting systems, simple

control reports

• Budgeting systems

• Monthly sales and

production reports

• Delegated control

FIN

AN

CIN

G

Major source

of finance

• Retained earnings

• New partners

• Banks30

• Retained earnings

• New partners

• Secured long-term debt

Major

investment

• Working capital

• Expanding manufacturing

capacity (if applicable)

• New operating units

SA

LE

S Cash

generation

• Positive but reinvested • Positive cash generation

• Smaller dividend

Product-

market

• Broadened but limited lines

• Single market, multiple

channels

• Extended range

• Increased markets and

channels

Another way to define success of Local Emerging Household Names: they must actively compete

with International Energy Access Pioneer Brands across all aspects of their business functions.

For the most part, International Energy Access Pioneer Brands in Nigeria have greater market

share than Local Emerging Household Names. To compete for some of this market share (and

to access markets that International Energy Access Pioneer Brands are not yet accessing) requires

Emerging Household Names to function as effectively across their operations, sales, and financing

as the leading International Energy Access Pioneer Brands.

30 While banks are not currently a major source of funding, companies are hopeful they can begin to access local debt financing

from commercial banks in the near future.

28

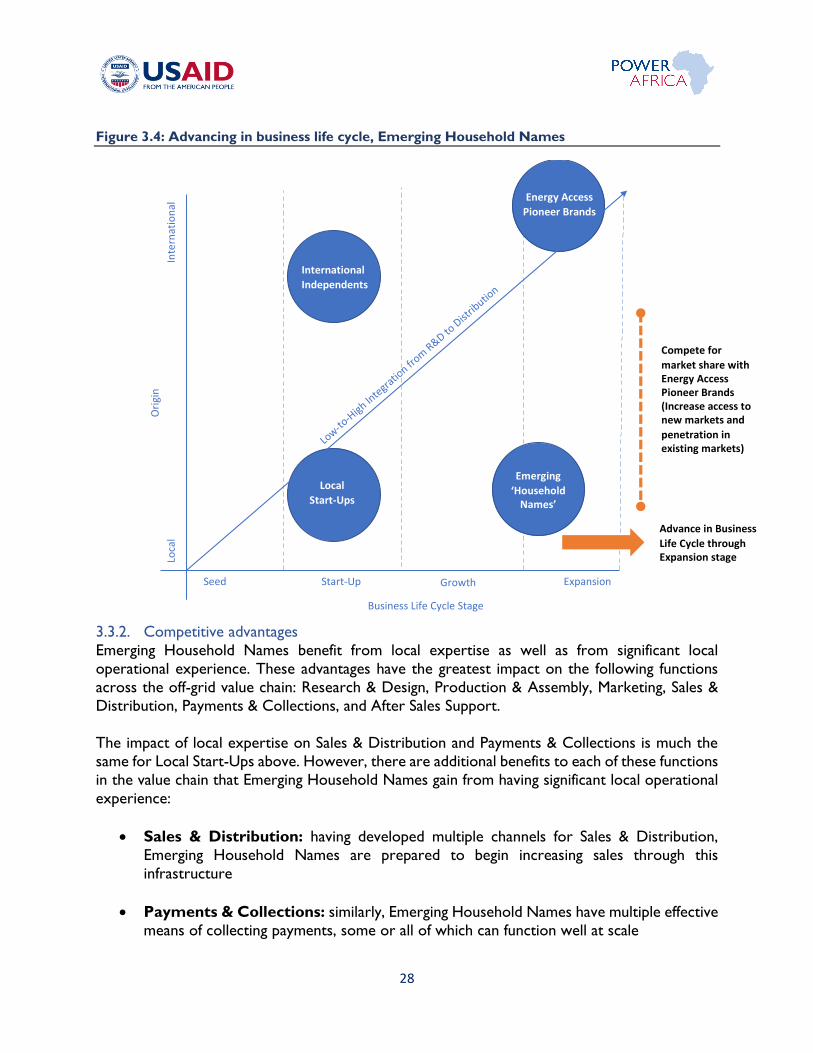

Figure 3.4: Advancing in business life cycle, Emerging Household Names

3.3.2. Competitive advantages

Emerging Household Names benefit from local expertise as well as from significant local

operational experience. These advantages have the greatest impact on the following functions

across the off-grid value chain: Research & Design, Production & Assembly, Marketing, Sales &

Distribution, Payments & Collections, and After Sales Support.

The impact of local expertise on Sales & Distribution and Payments & Collections is much the

same for Local Start-Ups above. However, there are additional benefits to each of these functions

in the value chain that Emerging Household Names gain from having significant local operational

experience:

• Sales & Distribution: having developed multiple channels for Sales & Distribution,

Emerging Household Names are prepared to begin increasing sales through this

infrastructure

• Payments & Collections: similarly, Emerging Household Names have multiple effective

means of collecting payments, some or all of which can function well at scale

Seed Expansion

Loca

l

Low-to

-High In

tegra

tion fr

om R

&D to D

istrib

ution

Start-Up Growth

Inte

rnat

ion

al

Emerging

‘Household Names’

Energy Access

Pioneer Brands

International

Independents

Local

Start-Ups

Business Life Cycle Stage

Ori

gin

Compete for

market share with Energy Access Pioneer Brands (Increase access to new markets and

penetration in existing markets)

Advance in Business

Life Cycle through Expansion stage

29

Additionally, local operational experience positions Emerging Household Names to succeed along

the following functions:

• Research & Design: having gained significant experience delivering products and gaining

user feedback, Emerging Household Names are well-positioned to incorporate this

feedback into design that best serves their individual customers. Depending on their

existing degree of integration and current level of engagement with R&D, Emerging

Household Names may be able incorporate this information into their own operations or

present this information to their selected product provider. Most companies will still use

an external product provider for R&D. Additionally, because Emerging Household Names

are focused only on the Nigerian market, they do not have to retain the adaptability of

their products that International companies may need and can focus all R&D efforts on

products for Nigerian customers. Examples of a Nigerian centric R&D approach may

include: using the number of light bulbs in kits that corresponds to the average number

of rooms in a given customer groups’ homes, accommodating the fact that one light bulb

is likely to be used outdoors for security purposes in some Nigerian markets, or including

multiple USB inputs depending on average number of mobile devices per family

• Production & Assembly: operational experience has enabled Emerging Household

Names to work on major problems related to Production & Assembly. Because of this competency, many Emerging Household Names are able to vertically integrate their value

chain to some degree

• Marketing: local knowledge combined with operational experience enables Emerging

Household Names to transform their local success stories into effective marketing

materials. Additionally, by stressing local nature of ownership and employees (with a track

record to prove their commitment to support of local communities), Emerging Household

Names can demonstrate a better alignment of interests than might be possible from

International companies

• After Sales Support: Emerging Household Names operate at sufficient scale that they

are able to provide meaningful After Sales Support. Because of significant experience

addressing customer issues, the cost of addressing each issue can be significantly reduced.

Also, the same systems developed for Sales & Distribution and Payments & Collections

can be used for After Sales Support

3.3.3. Challenges

The greatest Operational and Sales challenges include:

• Marketing remains largely inhibited by company’s own normal operating capacity and

lack of expertise in large-scale marketing campaigns. Restricted access to capital prevents

significant investment in external resources for such campaigns

• Companies remain largely dependent on agent networks for Sales & Distribution.

While such networks are effective for gradual growth, Emerging Household Names are

30

being outcompeted in Sales & Distribution by international companies that have elected

to use partnerships with telecommunications and FMCG companies for rapid Sales &

Distribution growth

• Similarly, companies remain dependent on agent networks for Payments &

Collections. When relying on agent networks, incentives to increase sales are not always

perfectly aligned, as agents are often focused on selling multiple products for multiple

companies (not just off-grid solar solutions)

• After Sales Support challenges for Emerging Household Names are caused by the same

agent network limitations noted above

The greatest financial challenges include:

• Consumer Finance: Most SHS companies in the market provide one or more of the

following three types of payment options for the consumers:

1. Outright purchase

2. Lease-to-own

3. Power-as-a-service

The vast majority of SHS companies prefer outright purchase due to the up-front

payment and reduced risk of payment defaults but most adopt the lease-to-own model

to help with affordability.

In the Nigerian market, only a few companies offer consumers credit and staggered

payment solutions to increase affordability. Some of these companies have high default

rates (or nonpayment rates in the case of PAYG systems). For example, one off-grid

company in Nigeria has noted that they consider payment rates over 75% to be

acceptable (at least as they focus on expansion of operations) and consider 50%

payment rates to be the threshold below which re-possession of off-grid assets must

be considered.31 By comparison, payment rates in East African SHS companies typically

range from 80% to 95%, where rates below 80% are considered poor performance.32

Some companies have developed mitigation measures to reduce the incidence of

customers defaulting on lease-to-own contracts. They have set weekly payments and

repossessions after 4 weeks of defaulting payments. Many developers in the market

are not willing to bear the credit risk so they seek to partner with microfinance

institutions and banks that are able to provide consumer financing to the target

segment. However, the major problem with consumer financing remains the extremely

high interest rates impacting affordability for lower income consumers.

Section 4 provides additional details on the financing landscape.

31 CrossBoundary Research (2018-2019): Interview with Fenix (2019) 32 CrossBoundary Research.

31

3.3.4. Strategies to grow Figure 3.5: Strategic growth focus areas along value chain, Emerging Household Names

• Emerging Household Names can invest in customer research to create a map of target

customers and develop Marketing approaches that are tailored specifically to each

customer archetype. Companies targeting affluent residential customers can use social

media and brand ambassadors, following the model used by many FMCG companies. An

example of this type of influencer marketing has been employed by a renewable energy

company called Reohob. Reohob engaged public figures from a national reality TV show,

Big Brother Nigeria, as brand ambassadors on Instagram

• While earlier stage companies can benefit from increased investment in exercising control

over agent networks through trainings, Emerging Household Names can significantly

improve Sales & Distribution and After Sales Support by recruiting agents as full-

time staff on a fixed salary with additional sales incentives. This approach helps address

mis-alignment of agent incentives. More mature companies are beginning to adopt this

approach, moving away from paying agents sales commission. This approach is also

intended to boost performance and ensure agent retention. Since most of these agents

are based within the communities, they are typically used for after-sales support and post-

installation maintenance. Some Emerging Household Names are providing ‘formalized’

comprehensive after-sales services for product differentiation. However, this service is

targeted at higher income customers who are able to pay additional fees for formal

services

• For transformative growth, Emerging Household Names must diversify channels for

Payments & Collections. Increasing the channels for Payments & Collections gives

companies access to more markets. Although companies eventually will need to move

toward greater use of mobile money and web-based payment systems as mobile penetration in Nigeria increases, given current levels of mobile penetration in Nigeria, no

single channel gives companies access to every potential customer. Mobile money systems

for payment remain a competitive advantage in terms of convenience and accessibility for

those with access, and cash collection through mobile or stationary agents remains critical

for customers without (or with unreliable) mobile access. Emerging Household Names

hoping to compete with mobile money enabled Energy Access Pioneer Brands will also

Research & Design

Sales & Distribution

Payments & Collections

Consumer Finance

After Sales Support

Production & Assembly

Marketing

Opportunity for internal improvement

Opportunity for partnershipLower priority for current stage

Strategic focus areas

Currently a core strength (Note: for some areas that are already core strengths, companies can continue making strategic improvements)

32

need to have multiple payment channels that optimize accessibility for all customer types

targeted

• Strategies for consumer finance are essential to improving customer ability to access

products. Such strategies are discussed in the Section 4 below

Engaging USAID Power Africa: As Emerging Household Names seek to expand, NPSP can

assist with fundraising and deal structuring by advising on approaches and methodologies for

structuring transactions, including selection of appropriate forms of capital (equity, debt or

hybrid) and risk allocation. NPSP can also connect the companies to the appropriate investors.

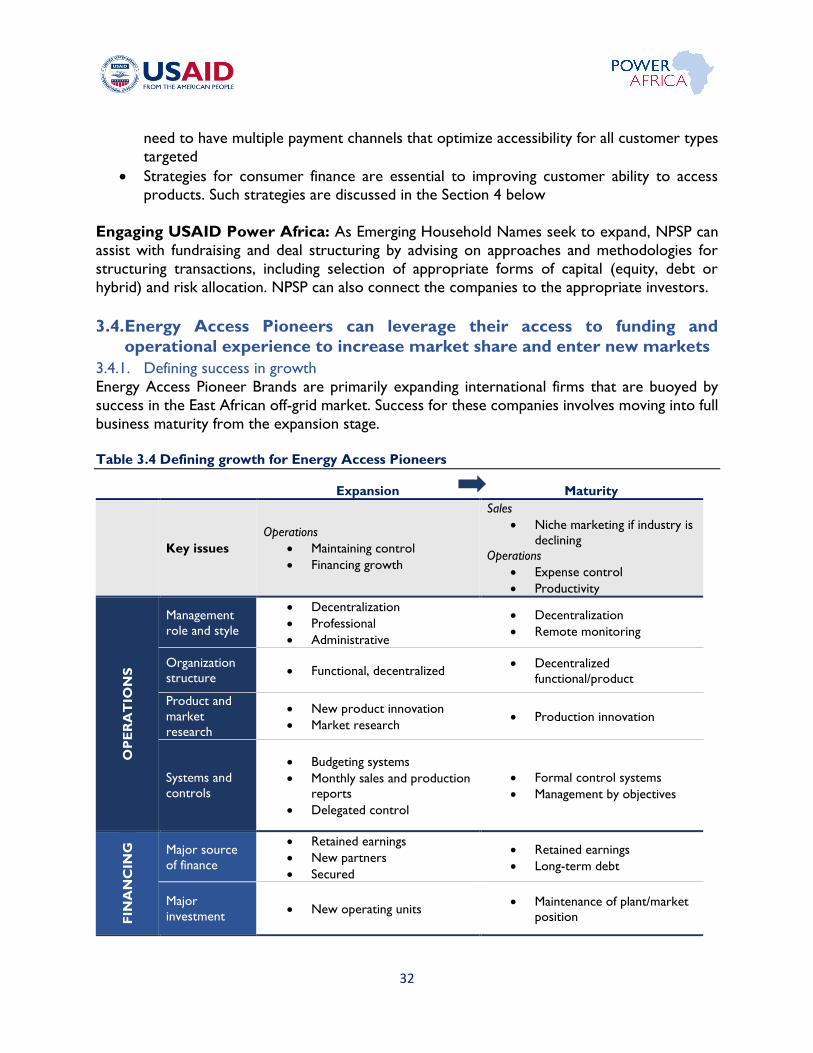

3.4. Energy Access Pioneers can leverage their access to funding and

operational experience to increase market share and enter new markets

3.4.1. Defining success in growth

Energy Access Pioneer Brands are primarily expanding international firms that are buoyed by

success in the East African off-grid market. Success for these companies involves moving into full

business maturity from the expansion stage.

Table 3.4 Defining growth for Energy Access Pioneers

Expansion Maturity

Key issues

Operations

• Maintaining control

• Financing growth

Sales

• Niche marketing if industry is

declining

Operations

• Expense control

• Productivity

OP

ER

AT

ION

S

Management

role and style

• Decentralization

• Professional

• Administrative

• Decentralization

• Remote monitoring

Organization

structure • Functional, decentralized

• Decentralized

functional/product

Product and

market

research

• New product innovation

• Market research • Production innovation

Systems and

controls

• Budgeting systems

• Monthly sales and production

reports

• Delegated control

• Formal control systems

• Management by objectives

FIN

AN

CIN

G

Major source

of finance

• Retained earnings

• New partners

• Secured

• Retained earnings

• Long-term debt

Major

investment • New operating units

• Maintenance of plant/market

position

33

Expansion Maturity S

AL

ES

Cash

generation

• Positive cash generation

• Smaller dividend

• Cash generator

• Higher dividend

Product-

market

• Extended range

• Increased markets and

channels

• Contained lines

• Multiple markets and

channels

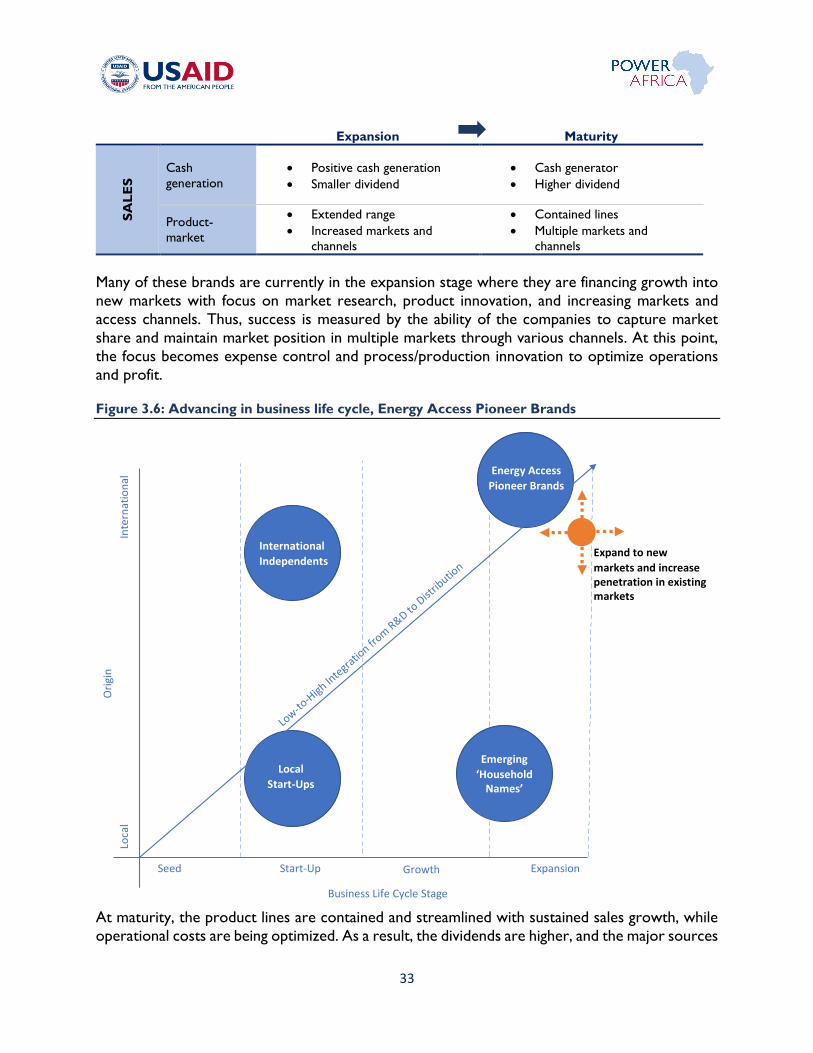

Many of these brands are currently in the expansion stage where they are financing growth into

new markets with focus on market research, product innovation, and increasing markets and

access channels. Thus, success is measured by the ability of the companies to capture market

share and maintain market position in multiple markets through various channels. At this point,

the focus becomes expense control and process/production innovation to optimize operations

and profit. Figure 3.6: Advancing in business life cycle, Energy Access Pioneer Brands

At maturity, the product lines are contained and streamlined with sustained sales growth, while

operational costs are being optimized. As a result, the dividends are higher, and the major sources

Seed Expansion

Loca

l

Low-to

-High In

tegra

tion fr

om R

&D to D

istrib

ution

Start-Up Growth

Inte

rnat

ion

al

Emerging

‘Household Names’

Energy Access

Pioneer Brands

International

Independents

Local

Start-Ups

Business Life Cycle Stage

Ori

gin

Expand to new

markets and increase penetration in existing markets

34