nhs procurement - cips speaker... · nhs procurement mick corti commercial & business...

TRANSCRIPT

NHS Procurement Mick Corti

Commercial & Business Development Director

NHS London Procurement Partnership

CIPS London Branch Event 8th Sept 2015

The Financial Imperative

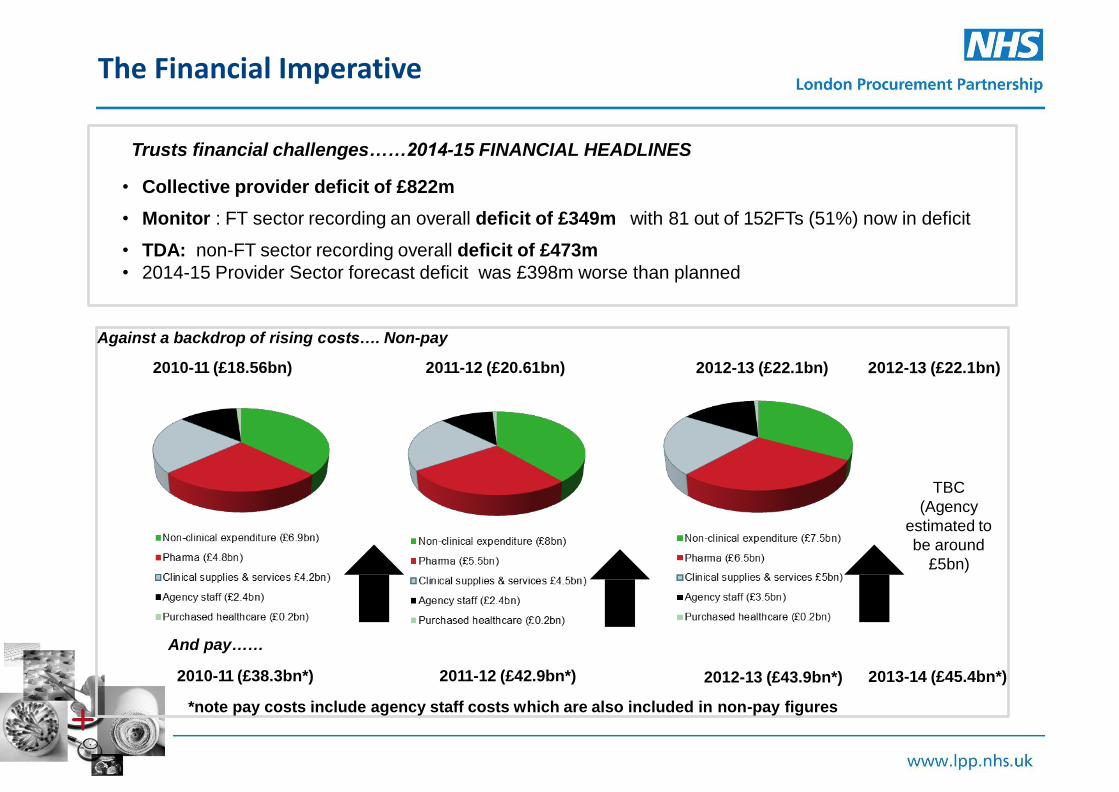

Trusts financial challenges……2014-15 FINANCIAL HEADLINES • Collective provider deficit of £822m • Monitor : FT sector recording an overall deficit of £349m with 81 out of 152FTs (51%) now in deficit • TDA: non-FT sector recording overall deficit of £473m

• 2014-15 Provider Sector forecast deficit was £398m worse than planned

Against a backdrop of rising costs…. Non-pay

2010-11 (£18.56bn) 2011-12 (£20.61bn)

TBC

(Agency

estimated to

be around

£5bn)

2012-13 (£22.1bn) 2012-13 (£22.1bn) 2012-13 (£22.1bn)

And pay……

2010-11 (£38.3bn*) 2011-12 (£42.9bn*) 2012-13 (£43.9bn*)

*note pay costs include agency staff costs which are also included in non-pay figures

2013-14 (£45.4bn*)

Are We Surprised?

The reason for increasing

pressures on trusts’ spending is

evident from trends in hospitals’

workloads.

Trends in:

• Referrals increasing at around

3.2% per year

• Outpatients 3.2%

• A&E 1.8%

• Elective 2.8%

• eEmergency admissions 1.8%

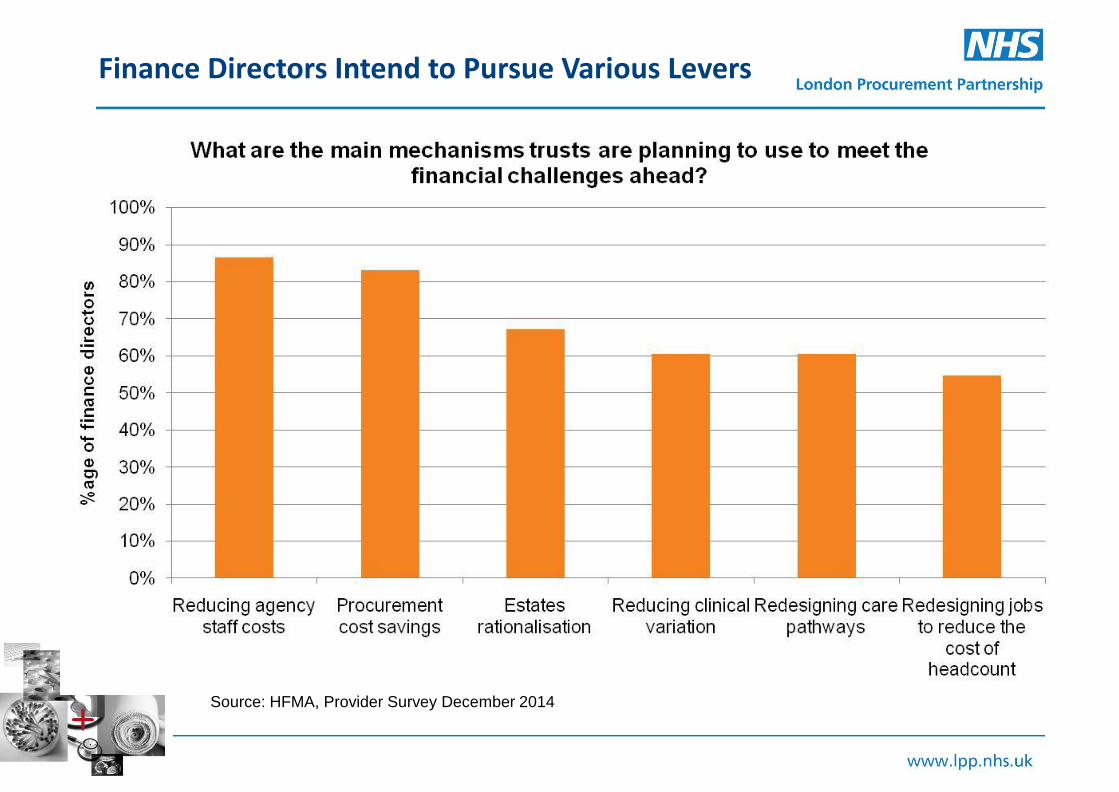

Finance Directors Intend to Pursue Various Levers

Source: HFMA, Provider Survey December 2014

Current Procurement Landscape

Department of Health

Commercial

medicines unit

Crown

Commercial

Service

NHS Supply

Chain

Collaborative

procurement

hubs

Procurement

teams in NHS

trusts

Suppliers

Structure of clinical and non-clinical procurement for goods and services within provider side.

NHS Supply Chain

CCS

Hubs (x6)

£1.5bn (mainly Clinical Goods)

£2.2bn (Common G&S and Agency)

c£3.0bn (Clinical, Non-clinical and Agency

Total £6.7bn

NHS Providers' Spend – 2013/14 Unless pay and pharma are addressed other savings become insignificant….

5 DH – Leading the nation’s health and care

(Agency

£2.4bn)

(Bank est.

£2.5bn)

Influence of intermediaries:

*

*Note financing costs not included in

non-pay figures on previous slide

Succession of policies to improve NHS procurement aligned to health policy (devolved NHS,

local accountability)…… but local autonomy does not maximise NHS purchasing muscle

Multiple reports have been heavily critical…... issues are symptomatic of local

autonomy:

• Lack of leadership

• Poor data and systems

• Multiple orders and invoices

• Variation in prices paid and products used

• Variable capability and capacity

• Fragmented system and culture of ‘no sharing’

• Inefficient logistics in trusts

• Competing procurement landscape confusing and costly

• No mechanism for sharing information and knowledge

• No joined up category strategies or supplier management

2 DH – Leading the nation’s health and care

Background to NHS procurement

Regtster !()(dally procurement and supply chatn news tyy ematll

Lord Carter appointed NHS procurement champion " " wanr the latest procurement and supply cham news

deltvered strarght to your mt>ox' Sign up for the SUpply

Management Da ly

20 June 2014 1 Wilt Green

Lord C •n or of Col. s has been appoint10d to thl! post of NHS

proc urem•nt champion.

The Labour peer, who has conducted a number or reviews for

the govemmen Will "help hOspitals to cut waste. save money

New Parliament = Focus on Efficiency

5 DH – Leading the nation’s health and care

*

*Note financing costs not included in

non-pay figures on previous slide

Hospital Efficiency Index

• Tightening, workflow, and step-down

• Tightening:

• Workforce

• Pharmacy

• Estates

• Procurement

• Adjusted Treatment Index

• Model of Hospital Efficiency

• Informed by cohort of 22 (now 32) provider trusts

What would procurement look like in a model hospital?

• A single NHS catalogue?

• Covering all products bought by trusts

• Supported by stores and logistics systems where possible

• Backed up by compliance policies, procedures and systems

• Phased approach: basic consumables, nurse led and doctor led products

Pay

£45.3b

Non Pay

£27.2b

Non Influence

£8.2b

Pharma

£6b

Property

£3b

Goods + Services

£9b

SERVICES

CAT.

AUTO

REPLENISH

CAT.

SPOT PURCHASE

LEAKAGE

FUTURE OPERATING MODEL WILL BE KEY

NHS London Procurement Partnership is:

• A collaborative procurement organisation funded and governed by our NHS members

• Established April 2006: Permanent

organisation since 2011

• Steering Board

• Professional, operational and process efficiencies to procurement and supply chain services

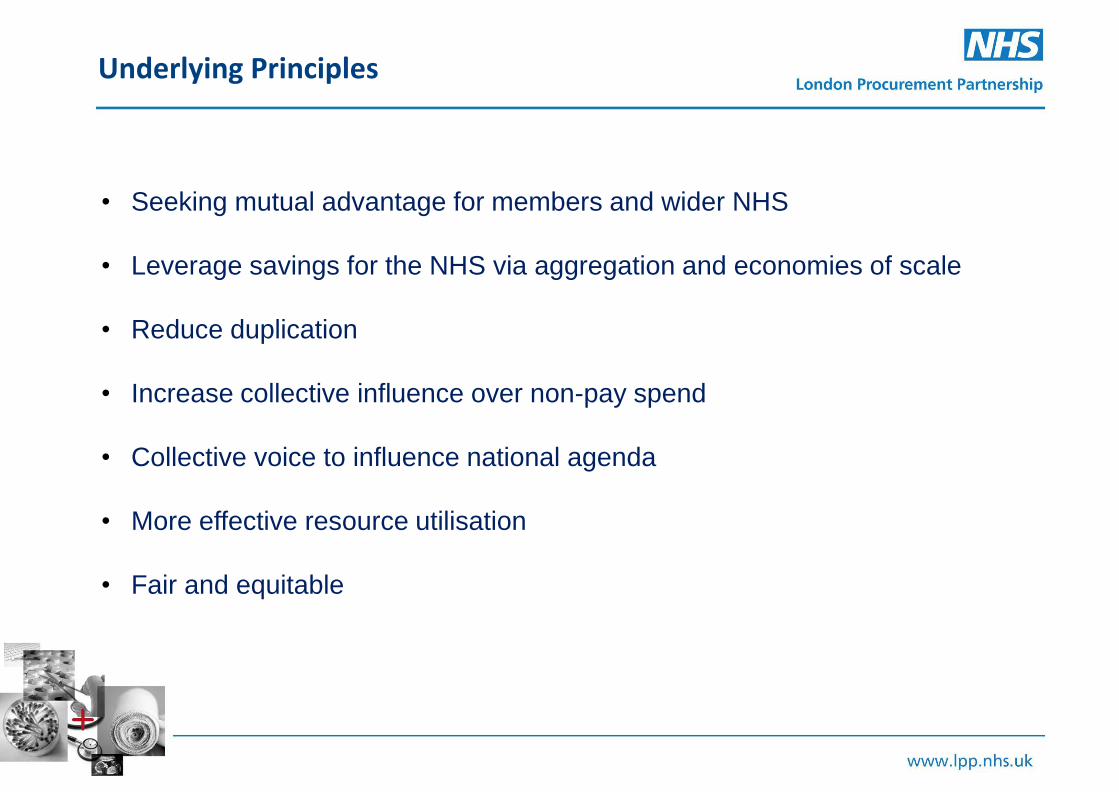

Underlying Principles

• Seeking mutual advantage for members and wider NHS

• Leverage savings for the NHS via aggregation and economies of scale

• Reduce duplication

• Increase collective influence over non-pay spend

• Collective voice to influence national agenda

• More effective resource utilisation

• Fair and equitable

NHS London Procurement Partnership focus

• Agency and Temporary Staffing

• Estates, Facilities and Professional Services

• Medical, Surgical and Supply Chain

• Medicines Optimisation and Pharmacy Procurement

• Technology

We now have £7-8bn of spend data,

and influence £3bn of that

2014-15:

Total 2006-15:

£ 103m

£ 755m

Savings

The NHS Collaborative Procurement Partnership

NHS London Procurement Partnership

North of England Commercial Procurement Collaborative

East of England Commercial Procurement Hub

NHS Commercial Solutions

• Opening up frameworks

• Reducing duplication

• Creating new national opportunities:

• National Collaborative Framework for the

supply of Nursing and Nursing related staff

• Total Orthopaedic Solutions

• Total Cardiology Solutions

Major Acute – Total Orthopaedic Solutions Framework

Phase 1

• As-Is analysis completed based on Supplier RFI data received in advance of framework

• £377k (inc VAT) cash releasing savings identified across applicable lots

• Access agreement signed, suppliers notified, pricing live within 10 days

• Implemented 1st February 2015

Phase 2

• Trust led surgeon discussion to identify resistance to change and overcome opposition

• Scenario analysis requested to highlight options available for Hips and Knees

• Options submitted to Trust for consideration

Phase 3

• Dual award selected by surgeons; Hips (65:35) and Knees (50:50)

• £435k (inc VAT) additional cash releasing savings identified from revised spend

• Rationalised from 10 Hips systems to 2 and from 6 Knee systems to 5

• Implemented 1st June 2015 with enhanced growth banding applied 1st July 2015

Total Framework savings to date - £813,542 (inc VAT)

Further rationalisation underway covering Trauma, Spinal and Extremities

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul-

07

Sep

-07

No

v-0

7

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-0

8

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Growth Colony Stimulating Factors (GCSF) Market Share Jul 07 to Nov 14

GRANOCYTE NEUPOGEN NEULASTA RATIOGRASTIM ZARZIO

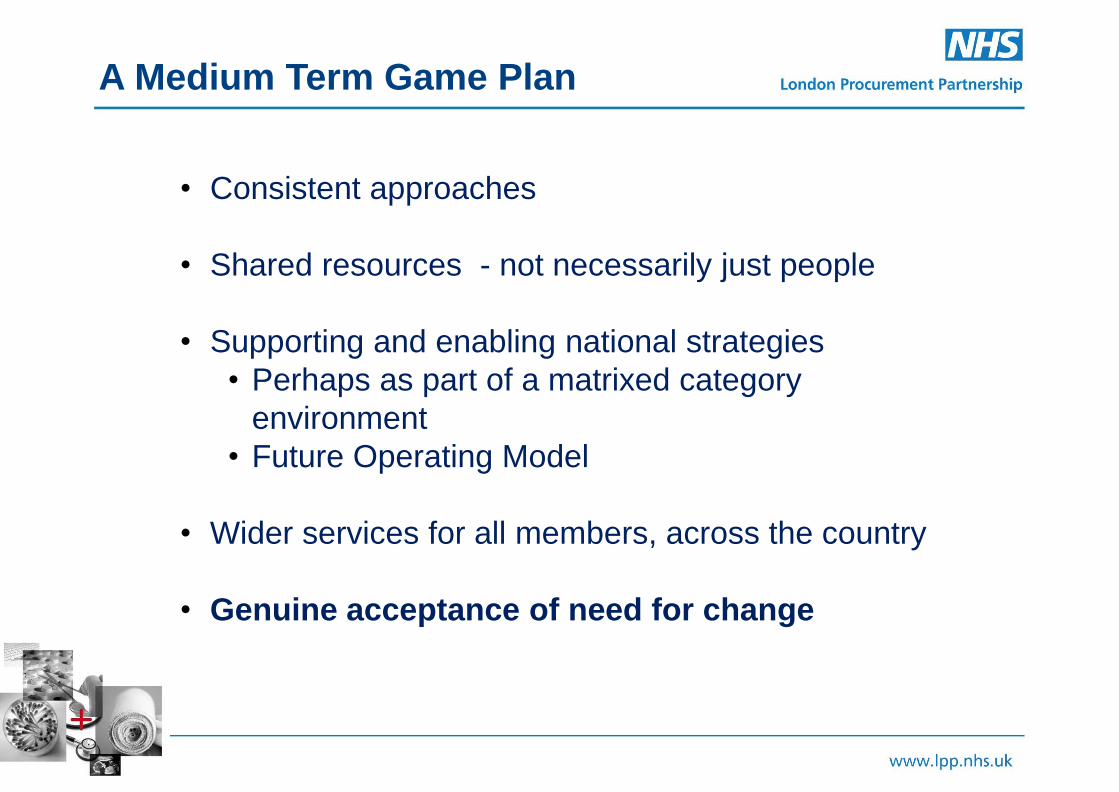

A Medium Term Game Plan

• Consistent approaches

• Shared resources - not necessarily just people

• Supporting and enabling national strategies

• Perhaps as part of a matrixed category

environment

• Future Operating Model

• Wider services for all members, across the country

• Genuine acceptance of need for change

Thank You Any questions?

Mick Corti Commercial and Business Development Director, NHS London Procurement Partnership [email protected]