news your pension team the rbs group pension · pdf filethe rbs group pension fund message...

TRANSCRIPT

The RBS Group Pension Fund

Message from the ChairmanWelcome to the 2012 newsletter for members of the Group Fund.

Members’ Newsletter 2012

The RBS Group Pension Fund 01

Contents

> 01 Message from the Chairman

> 02 Investment report

> 03 Distribution of assets

> 04 Fund finances

> 05 News

> 06 Your pension team

This newsletter is produced by the Trustee Board to keep you abreast of changes in the Fund, and to provide you with an update on the Fund’s financial position.

The Fund is one of the largest pension schemes in the UK and the Trustee Board keeps the financial health of the Fund under constant review.

I am pleased to report that the value of the net assets increased during the year to £22.8 billion at 31 March 2012.

The Investment Executive has continued to support the Trustee Board in all aspects of investing the Fund’s assets, and I am able to report another year of excellent performance, with investment income and capital growth adding over £2.2 billion to the value of the Fund over the year.

More details of the Fund’s assets and the work of the Investment Executive are included on pages 2, 3 and 4.

We continue to review the funding strategy for the Fund and work effectively with the Principal Employer as scheme sponsor.

The Trustee Board has been informed by the Group that in order to control the cost of its final salary pension benefit responsibilities, the Group is currently consulting with staff concerning a number of proposed contractual changes to pensions. These changes are presently subject to the outcome of a consultation with members.

Details of the main changes are summarised below:

– Increase in normal pension age for future service to age 65, without affecting the existing RBSelect charge. However, employees can elect to pay an additional RBSelect charge of 5% to maintain their normal pension age of 60 for future service.

– Increase in the age of eligibility to receive an undiscounted pension from age 50 to 55.

The Group has agreed to keep the Trustee Board informed throughout the consultation period.

It is important that you plan for your retirement and make informed decisions about your retirement savings. With this in mind, current employees who are members of the Group Fund are able to make use of the retirement planner provided by the Group which may be accessed through Your Reward online.

Merger with the RBS AA Pension Scheme The final salary section of the RBS AA Pension Scheme (formerly the ABN Amro UK Pension Fund) was merged with the Group Fund on 31 March 2012.

A new section has been created within the Group Fund, which will be known as the ‘AA Section of the RBS Group Fund’. This section will be financially separate from the remainder of the Group Fund, and the benefit rules of the AA Scheme will be incorporated into this new AA Section.

Changes to the Board There have been a number of changes to the Trustee Board since last year’s newsletter.

John McGuire retired on 21 March 2012 after nine years as a Trustee Director, during which he served as chairman of the Administration and Benefits and Funding and Monitoring Committees, and was latterly Deputy Chairman of the Trustee Board. I would like to thank him for the valuable contribution he made to the Board.

Following John McGuire’s retirement, David Morrison has been appointed by the Trustee Board as Deputy Chairman and Chairman of the Administration and Benefits Committee.

The Board welcomed two new Trustee Directors. George Graham and Fiona Davis joined as bank appointed Trustee Directors on 21 September 2011 and 21 March 2012 respectively.

We hope you find this newsletter informative, and if you want more information on anything we have covered, please contact Group Pension Services.

Finally, I would like to thank my fellow Trustee Directors and our internal and external advisors for their commitment and support throughout yet another challenging year.

Miller McLean Chairman - RBS Pension Trustee Limited

August 2012

Your pension team The Trustee Board is responsible for operating the Fund in line with its formal rules and pensions law. We also have a duty to protect the interests of all our Fund members, including our pensioners and those who are no longer employed by the Group, but who still have benefits in the Fund (our deferred members).

Find out moreThe following documents are available on request from Group Pension Services:

> Latest Actuarial Valuation Report Contains details of the Fund’s financial position as at 31 March 2010.

> Latest Annual Report and Accounts

Shows the Fund’s income and expenditure in the 12 months to 31 March 2012.

> Current Schedule of ContributionsShows how much money is being paid into the Fund.

> Trustee’s Statement of Funding PrinciplesExplains how we plan to make sure enough money is paid into the Fund to provide the benefits that members have built up.

> Trustee’s Statement of Investment PrinciplesExplains how we invest the money paid into the Fund.

> Latest Engagement & Voting Report

Contact usIf you have a question, please email Group Pension Services:

Employee members

External [email protected]

Internal RBS Staff pension queries

Deferred members [email protected]

Pensioners [email protected]

Alternative formats This communication is available in large print, Braille or audio on request from Group Pension Services.

06 The RBS Group Pension Fund

Your current Trustee Directors are:Company SelectedMiller McLean [Chairman]David Morrison [Deputy Chairman]Stephen BoyleFiona DavisGeorge GrahamDonald Workman

Member electedPeter BoydPeter EastonStephen FallowellColin Wilson

Group Pension Services HR Shared Services The Royal Bank of Scotland Group PO Box 1390 Croydon CR9 1YB

The Royal Bank of Scotland Registered in Scotland No. 45551 Registered Office: 36 St. Andrew Square Edinburgh EH2 2YB

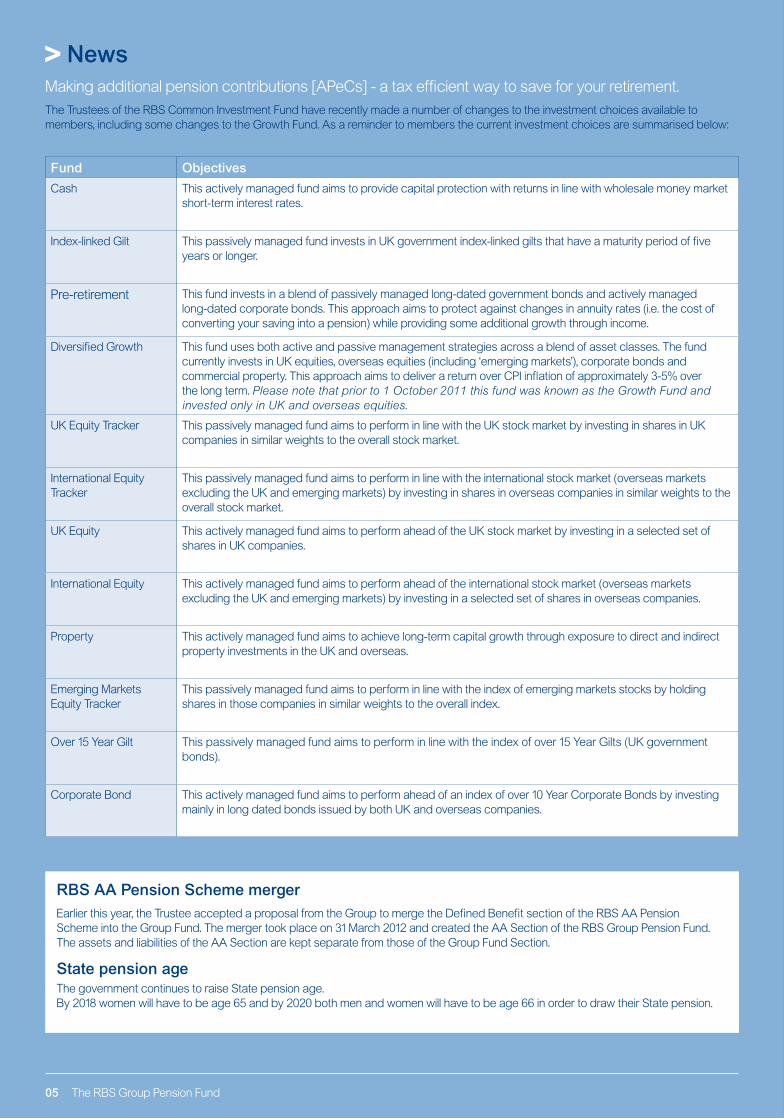

NewsMaking additional pension contributions [APeCs] - a tax efficient way to save for your retirement.The Trustees of the RBS Common Investment Fund have recently made a number of changes to the investment choices available to members, including some changes to the Growth Fund. As a reminder to members the current investment choices are summarised below:

Fund Objectives

Cash This actively managed fund aims to provide capital protection with returns in line with wholesale money market short-term interest rates.

Index-linked Gilt This passively managed fund invests in UK government index-linked gilts that have a maturity period of five years or longer.

Pre-retirement This fund invests in a blend of passively managed long-dated government bonds and actively managed long-dated corporate bonds. This approach aims to protect against changes in annuity rates (i.e. the cost of converting your saving into a pension) while providing some additional growth through income.

Diversified Growth This fund uses both active and passive management strategies across a blend of asset classes. The fund currently invests in UK equities, overseas equities (including ‘emerging markets’), corporate bonds and commercial property. This approach aims to deliver a return over CPI inflation of approximately 3-5% over the long term. Please note that prior to 1 October 2011 this fund was known as the Growth Fund and invested only in UK and overseas equities.

UK Equity Tracker This passively managed fund aims to perform in line with the UK stock market by investing in shares in UK companies in similar weights to the overall stock market.

International Equity Tracker

This passively managed fund aims to perform in line with the international stock market (overseas markets excluding the UK and emerging markets) by investing in shares in overseas companies in similar weights to the overall stock market.

UK Equity This actively managed fund aims to perform ahead of the UK stock market by investing in a selected set of shares in UK companies.

International Equity This actively managed fund aims to perform ahead of the international stock market (overseas markets excluding the UK and emerging markets) by investing in a selected set of shares in overseas companies.

Property This actively managed fund aims to achieve long-term capital growth through exposure to direct and indirect property investments in the UK and overseas.

Emerging Markets Equity Tracker

This passively managed fund aims to perform in line with the index of emerging markets stocks by holding shares in those companies in similar weights to the overall index.

Over 15 Year Gilt This passively managed fund aims to perform in line with the index of over 15 Year Gilts (UK government bonds).

Corporate Bond This actively managed fund aims to perform ahead of an index of over 10 Year Corporate Bonds by investing mainly in long dated bonds issued by both UK and overseas companies.

05 The RBS Group Pension Fund

RBS AA Pension Scheme merger Earlier this year, the Trustee accepted a proposal from the Group to merge the Defined Benefit section of the RBS AA Pension Scheme into the Group Fund. The merger took place on 31 March 2012 and created the AA Section of the RBS Group Pension Fund. The assets and liabilities of the AA Section are kept separate from those of the Group Fund Section.

State pension age The government continues to raise State pension age. By 2018 women will have to be age 65 and by 2020 both men and women will have to be age 66 in order to draw their State pension.

Changes during the yearJohn McGuire retired as a Trustee Director and Deputy Chairman of the Trustee Board on 21 March 2012.

David Morrison was appointed Deputy Chairman of the Trustee Board on 21 March 2012.

Peter Easton stepped down from the Investment Committee and joined the Administration and Benefits Committee on 21 March 2012.

Colin Wilson stepped down from the Administration and Benefits Committee and joined the Investment Committee on 21 March 2012.

Trustee meetings during the yearThe Trustee Board met five times during the period.

In addition the Trustee Board met the Group on a number of occasions to discuss the funding strategy of the Fund.

The Trustee Board sub committees met as follows during the period:

• The Administration and Benefits Committee met seven times• The Funding and Monitoring Committee met seven times• The Investment Committee met five times

Data protection We hold information about you in order to provide your pension benefits (such as pensions, lump sums, death benefits), which may include information obtained from third parties.

This information may be shared with:

• Companies within the Royal Bank of Scotland Group (please contact us if you do not want us to share your information with these companies);

• Other third parties who assist us in administering your benefits (e.g. updating personal data, calculating and paying benefits);

• Those where we have your permission to do so; and • Those where we are required to do so by law

If you want a copy of the information we hold about you, please contact us. A fee may be payable.

Investment report Market commentary: The key issues affecting markets in the last year have been the US economy’s return to growth and the debt crisis in Europe.

02 The RBS Group Pension Fund 03

Distribution of assets Asset mix as at 31 March 2012

22%

5%

26%

9%

28%

1%2%

3%

4%

Asset RBS Group RBS AAclass £m £mDirect Global Equity 4,959 18

Private Equity 1,193 -

Credit 5,698 82

Property 805 36

Hedge Funds 588 -

Reinsurance 395 -

Infrastructure 200 -

Index-linked bonds & liability hedging 6,032 515

Cash & Liquid Assets 2,059 16

Total assets 21,929 667

22%

5%

26%

9%

28%

1%2%

3%

4%

22%

5%

26%

9%

28%

1%2%

3%

4%

22%

5%

26%

9%

28%

1%2%

3%

4%

The RBS Group Pension Fund 04

Fund financesThe table below is a summary of the financial statements contained in the Trustee Annual Report & Accounts for the year ended 31 March 2012 which has been independently audited by Deloitte LLP.

£ million

Fund value at 31 March 2011 19,469

Income:

contributions 1,131

transfers in 681

other income –

Total income 1,812

Expenditure:

benefit payments (678)

member transfers out (43)

administrative expenses (25)

Total expenditure (746)

Net returns on investments 2,223

Fund value at 31 March 2012 22,758

Fund membership

RBS Group section At 31 March 2011 At 31 March 2012

Active members 46,618 41,957

Deferred pensioners 116,461 118,932

Pensioner members 58,642 60,014

221,721 220,903

RBS AA section

Active members – 92

Deferred pensioners – 2,156

Pensioner members – 646

2,894

Total 221,721 223,797

0%

5%

10%

15%

20%

1 Year 3 Years 5 Years

Fund Return Strategic Benchmark Return

11.4% 11.4%

5.2% 5.7%

17.7%

16.2%

The performance of the Fund broadly mirrored that of bond and equity markets; the FTSE Index Linked Gilt Index (UK government bonds) returned 18.1% while the FTSE All World Index (global equity) returned -0.2%.

Fund performanceAssets returned 11.4% for the year to 31 March 2012

> In the UK the coalition government has set out austerity policies which aim to reduce spending and maintain confidence in the government bond markets. So far the UK has retained its AAA credit rating. The Bank of England has kept interest rates at low levels and continued with quantitative easing (‘QE’) to encourage growth through private and corporate spending.

> Europe is struggling to deal with the diverging economic conditions in the core (e.g. Germany where there has been strong manufacturing growth over the past two years) and the periphery (e.g. Greece, Italy, Spain where assets prices have fallen and growth was extremely weak). Markets are concerned by the creditworthiness of the periphery countries and Europe is being forced to look for political solutions.

> The US, the world’s largest economy, has been the main bright spot in the last year. US growth has improved with the housing market showing signs of stabilising and unemployment starting to fall. US companies have shown strong levels of profitability. With an election due later in 2012, a key question is whether the US government will continue spending and maintain tax breaks to support growth.

> Emerging markets have continued to see higher levels of growth than the West. China and India benefit from a lower cost base than the West, giving them a competitive advantage for manufacturing and exports, while strength of commodity markets has been key for Brazil and Russia. However, inflation has picked up in China eroding some of its advantage and the rate of growth appears to be moderating. A key issue is whether the emerging economies can transition from wealth generated by exports only to a more balanced mix of exports and domestic spending.

Growth assets > Growth assets are investments such as equities, credit, property, hedge funds and alternative investments; basically assets whose purpose is to provide growth rather than match the liabilities.

> The new strategic benchmark has been designed to allocate absolute amounts (in Sterling terms) to growth assets as opposed to maintaining percentage weights; this allows the Fund to manage its exposures more efficiently in volatile markets.

> The mix of growth assets in the new strategic benchmark has been designed to increase diversification and reduce the concentration of risk to equity markets.

Liability hedging> The Fund uses UK government bonds and derivative contracts such as interest rate and inflation swaps to help offset movements in the liabilities.

> Over the 12 months to March 2012 hedging levels have increased, further reducing investment risk against the liabilities.

Implementation

> The new strategic benchmark is being phased in through 2011 and 2012. So far the Fund has reduced its equity exposure by £2 billion to reduce investment risk and introduced two new asset classes – reinsurance and infrastructure.

The UK is pursuing austerity to protect its credit rating.

Growth in Europe is weak and debts in some of the periphery countries are too high to be sustainable.

Supported by high levels of government spending, the US has seen a return to growth, with corporate America making healthy profits.

Politics will be key for both Europe and America in deciding the path going forward.

The allocation to growth assets is designed to produce an excess return over the liabilities which, along with the deficit contributions being paid by the Group, will help close the deficit from the 2010 Actuarial Valuation.

Liability hedging involves holding investments which offset the impact of changes in interest rates and inflation on the value of liabilities.

The new strategic benchmark is designed to reduce investment risk while also allowing the Fund to close the deficit over time.

Activity: In the second half of 2011 the Investment Executive undertook a full review of the strategic benchmark for the Trustee. A new strategic benchmark was adopted which incorporates growth assets as well as a liability hedging portfolio.

At 31 March 2012 the Group Fund had additional exposure to equity markets through futures contracts of £3,195m, equivalent to 14% of Fund assets.

These figures exclude AVC investments, current assets and current liabilities of £162m.

Clockwise from the top:

Investment report Market commentary: The key issues affecting markets in the last year have been the US economy’s return to growth and the debt crisis in Europe.

02 The RBS Group Pension Fund 03

Distribution of assets Asset mix as at 31 March 2012

22%

5%

26%

9%

28%

1%2%

3%

4%

Asset RBS Group RBS AAclass £m £mDirect Global Equity 4,959 18

Private Equity 1,193 -

Credit 5,698 82

Property 805 36

Hedge Funds 588 -

Reinsurance 395 -

Infrastructure 200 -

Index-linked bonds & liability hedging 6,032 515

Cash & Liquid Assets 2,059 16

Total assets 21,929 667

22%

5%

26%

9%

28%

1%2%

3%

4%

22%

5%

26%

9%

28%

1%2%

3%

4%

22%

5%

26%

9%

28%

1%2%

3%

4%

The RBS Group Pension Fund 04

Fund financesThe table below is a summary of the financial statements contained in the Trustee Annual Report & Accounts for the year ended 31 March 2012 which has been independently audited by Deloitte LLP.

£ million

Fund value at 31 March 2011 19,469

Income:

contributions 1,131

transfers in 681

other income –

Total income 1,812

Expenditure:

benefit payments (678)

member transfers out (43)

administrative expenses (25)

Total expenditure (746)

Net returns on investments 2,223

Fund value at 31 March 2012 22,758

Fund membership

RBS Group section At 31 March 2011 At 31 March 2012

Active members 46,618 41,957

Deferred pensioners 116,461 118,932

Pensioner members 58,642 60,014

221,721 220,903

RBS AA section

Active members – 92

Deferred pensioners – 2,156

Pensioner members – 646

2,894

Total 221,721 223,797

0%

5%

10%

15%

20%

1 Year 3 Years 5 Years

Fund Return Strategic Benchmark Return

11.4% 11.4%

5.2% 5.7%

17.7%

16.2%

The performance of the Fund broadly mirrored that of bond and equity markets; the FTSE Index Linked Gilt Index (UK government bonds) returned 18.1% while the FTSE All World Index (global equity) returned -0.2%.

Fund performanceAssets returned 11.4% for the year to 31 March 2012

> In the UK the coalition government has set out austerity policies which aim to reduce spending and maintain confidence in the government bond markets. So far the UK has retained its AAA credit rating. The Bank of England has kept interest rates at low levels and continued with quantitative easing (‘QE’) to encourage growth through private and corporate spending.

> Europe is struggling to deal with the diverging economic conditions in the core (e.g. Germany where there has been strong manufacturing growth over the past two years) and the periphery (e.g. Greece, Italy, Spain where assets prices have fallen and growth was extremely weak). Markets are concerned by the creditworthiness of the periphery countries and Europe is being forced to look for political solutions.

> The US, the world’s largest economy, has been the main bright spot in the last year. US growth has improved with the housing market showing signs of stabilising and unemployment starting to fall. US companies have shown strong levels of profitability. With an election due later in 2012, a key question is whether the US government will continue spending and maintain tax breaks to support growth.

> Emerging markets have continued to see higher levels of growth than the West. China and India benefit from a lower cost base than the West, giving them a competitive advantage for manufacturing and exports, while strength of commodity markets has been key for Brazil and Russia. However, inflation has picked up in China eroding some of its advantage and the rate of growth appears to be moderating. A key issue is whether the emerging economies can transition from wealth generated by exports only to a more balanced mix of exports and domestic spending.

Growth assets > Growth assets are investments such as equities, credit, property, hedge funds and alternative investments; basically assets whose purpose is to provide growth rather than match the liabilities.

> The new strategic benchmark has been designed to allocate absolute amounts (in Sterling terms) to growth assets as opposed to maintaining percentage weights; this allows the Fund to manage its exposures more efficiently in volatile markets.

> The mix of growth assets in the new strategic benchmark has been designed to increase diversification and reduce the concentration of risk to equity markets.

Liability hedging> The Fund uses UK government bonds and derivative contracts such as interest rate and inflation swaps to help offset movements in the liabilities.

> Over the 12 months to March 2012 hedging levels have increased, further reducing investment risk against the liabilities.

Implementation

> The new strategic benchmark is being phased in through 2011 and 2012. So far the Fund has reduced its equity exposure by £2 billion to reduce investment risk and introduced two new asset classes – reinsurance and infrastructure.

The UK is pursuing austerity to protect its credit rating.

Growth in Europe is weak and debts in some of the periphery countries are too high to be sustainable.

Supported by high levels of government spending, the US has seen a return to growth, with corporate America making healthy profits.

Politics will be key for both Europe and America in deciding the path going forward.

The allocation to growth assets is designed to produce an excess return over the liabilities which, along with the deficit contributions being paid by the Group, will help close the deficit from the 2010 Actuarial Valuation.

Liability hedging involves holding investments which offset the impact of changes in interest rates and inflation on the value of liabilities.

The new strategic benchmark is designed to reduce investment risk while also allowing the Fund to close the deficit over time.

Activity: In the second half of 2011 the Investment Executive undertook a full review of the strategic benchmark for the Trustee. A new strategic benchmark was adopted which incorporates growth assets as well as a liability hedging portfolio.

At 31 March 2012 the Group Fund had additional exposure to equity markets through futures contracts of £3,195m, equivalent to 14% of Fund assets.

These figures exclude AVC investments, current assets and current liabilities of £162m.

Clockwise from the top:

Investment report Market commentary: The key issues affecting markets in the last year have been the US economy’s return to growth and the debt crisis in Europe.

02 The RBS Group Pension Fund 03

Distribution of assets Asset mix as at 31 March 2012

22%

5%

26%

9%

28%

1%2%

3%

4%

Asset RBS Group RBS AAclass £m £mDirect Global Equity 4,959 18

Private Equity 1,193 -

Credit 5,698 82

Property 805 36

Hedge Funds 588 -

Reinsurance 395 -

Infrastructure 200 -

Index-linked bonds & liability hedging 6,032 515

Cash & Liquid Assets 2,059 16

Total assets 21,929 667

22%

5%

26%

9%

28%

1%2%

3%

4%

22%

5%

26%

9%

28%

1%2%

3%

4%

22%

5%

26%

9%

28%

1%2%

3%

4%

The RBS Group Pension Fund 04

Fund financesThe table below is a summary of the financial statements contained in the Trustee Annual Report & Accounts for the year ended 31 March 2012 which has been independently audited by Deloitte LLP.

£ million

Fund value at 31 March 2011 19,469

Income:

contributions 1,131

transfers in 681

other income –

Total income 1,812

Expenditure:

benefit payments (678)

member transfers out (43)

administrative expenses (25)

Total expenditure (746)

Net returns on investments 2,223

Fund value at 31 March 2012 22,758

Fund membership

RBS Group section At 31 March 2011 At 31 March 2012

Active members 46,618 41,957

Deferred pensioners 116,461 118,932

Pensioner members 58,642 60,014

221,721 220,903

RBS AA section

Active members – 92

Deferred pensioners – 2,156

Pensioner members – 646

2,894

Total 221,721 223,797

0%

5%

10%

15%

20%

1 Year 3 Years 5 Years

Fund Return Strategic Benchmark Return

11.4% 11.4%

5.2% 5.7%

17.7%

16.2%

The performance of the Fund broadly mirrored that of bond and equity markets; the FTSE Index Linked Gilt Index (UK government bonds) returned 18.1% while the FTSE All World Index (global equity) returned -0.2%.

Fund performanceAssets returned 11.4% for the year to 31 March 2012

> In the UK the coalition government has set out austerity policies which aim to reduce spending and maintain confidence in the government bond markets. So far the UK has retained its AAA credit rating. The Bank of England has kept interest rates at low levels and continued with quantitative easing (‘QE’) to encourage growth through private and corporate spending.

> Europe is struggling to deal with the diverging economic conditions in the core (e.g. Germany where there has been strong manufacturing growth over the past two years) and the periphery (e.g. Greece, Italy, Spain where assets prices have fallen and growth was extremely weak). Markets are concerned by the creditworthiness of the periphery countries and Europe is being forced to look for political solutions.

> The US, the world’s largest economy, has been the main bright spot in the last year. US growth has improved with the housing market showing signs of stabilising and unemployment starting to fall. US companies have shown strong levels of profitability. With an election due later in 2012, a key question is whether the US government will continue spending and maintain tax breaks to support growth.

> Emerging markets have continued to see higher levels of growth than the West. China and India benefit from a lower cost base than the West, giving them a competitive advantage for manufacturing and exports, while strength of commodity markets has been key for Brazil and Russia. However, inflation has picked up in China eroding some of its advantage and the rate of growth appears to be moderating. A key issue is whether the emerging economies can transition from wealth generated by exports only to a more balanced mix of exports and domestic spending.

Growth assets > Growth assets are investments such as equities, credit, property, hedge funds and alternative investments; basically assets whose purpose is to provide growth rather than match the liabilities.

> The new strategic benchmark has been designed to allocate absolute amounts (in Sterling terms) to growth assets as opposed to maintaining percentage weights; this allows the Fund to manage its exposures more efficiently in volatile markets.

> The mix of growth assets in the new strategic benchmark has been designed to increase diversification and reduce the concentration of risk to equity markets.

Liability hedging> The Fund uses UK government bonds and derivative contracts such as interest rate and inflation swaps to help offset movements in the liabilities.

> Over the 12 months to March 2012 hedging levels have increased, further reducing investment risk against the liabilities.

Implementation

> The new strategic benchmark is being phased in through 2011 and 2012. So far the Fund has reduced its equity exposure by £2 billion to reduce investment risk and introduced two new asset classes – reinsurance and infrastructure.

The UK is pursuing austerity to protect its credit rating.

Growth in Europe is weak and debts in some of the periphery countries are too high to be sustainable.

Supported by high levels of government spending, the US has seen a return to growth, with corporate America making healthy profits.

Politics will be key for both Europe and America in deciding the path going forward.

The allocation to growth assets is designed to produce an excess return over the liabilities which, along with the deficit contributions being paid by the Group, will help close the deficit from the 2010 Actuarial Valuation.

Liability hedging involves holding investments which offset the impact of changes in interest rates and inflation on the value of liabilities.

The new strategic benchmark is designed to reduce investment risk while also allowing the Fund to close the deficit over time.

Activity: In the second half of 2011 the Investment Executive undertook a full review of the strategic benchmark for the Trustee. A new strategic benchmark was adopted which incorporates growth assets as well as a liability hedging portfolio.

At 31 March 2012 the Group Fund had additional exposure to equity markets through futures contracts of £3,195m, equivalent to 14% of Fund assets.

These figures exclude AVC investments, current assets and current liabilities of £162m.

Clockwise from the top:

The RBS Group Pension Fund

Message from the ChairmanWelcome to the 2012 newsletter for members of the Group Fund.

Members’ Newsletter 2012

The RBS Group Pension Fund 01

Contents

> 01 Message from the Chairman

> 02 Investment report

> 03 Distribution of assets

> 04 Fund finances

> 05 News

> 06 Your pension team

This newsletter is produced by the Trustee Board to keep you abreast of changes in the Fund, and to provide you with an update on the Fund’s financial position.

The Fund is one of the largest pension schemes in the UK and the Trustee Board keeps the financial health of the Fund under constant review.

I am pleased to report that the value of the net assets increased during the year to £22.8 billion at 31 March 2012.

The Investment Executive has continued to support the Trustee Board in all aspects of investing the Fund’s assets, and I am able to report another year of excellent performance, with investment income and capital growth adding over £2.2 billion to the value of the Fund over the year.

More details of the Fund’s assets and the work of the Investment Executive are included on pages 2, 3 and 4.

We continue to review the funding strategy for the Fund and work effectively with the Principal Employer as scheme sponsor.

The Trustee Board has been informed by the Group that in order to control the cost of its final salary pension benefit responsibilities, the Group is currently consulting with staff concerning a number of proposed contractual changes to pensions. These changes are presently subject to the outcome of a consultation with members.

Details of the main changes are summarised below:

– Increase in normal pension age for future service to age 65, without affecting the existing RBSelect charge. However, employees can elect to pay an additional RBSelect charge of 5% to maintain their normal pension age of 60 for future service.

– Increase in the age of eligibility to receive an undiscounted pension from age 50 to 55.

The Group has agreed to keep the Trustee Board informed throughout the consultation period.

It is important that you plan for your retirement and make informed decisions about your retirement savings. With this in mind, current employees who are members of the Group Fund are able to make use of the retirement planner provided by the Group which may be accessed through Your Reward online.

Merger with the RBS AA Pension Scheme The final salary section of the RBS AA Pension Scheme (formerly the ABN Amro UK Pension Fund) was merged with the Group Fund on 31 March 2012.

A new section has been created within the Group Fund, which will be known as the ‘AA Section of the RBS Group Fund’. This section will be financially separate from the remainder of the Group Fund, and the benefit rules of the AA Scheme will be incorporated into this new AA Section.

Changes to the Board There have been a number of changes to the Trustee Board since last year’s newsletter.

John McGuire retired on 21 March 2012 after nine years as a Trustee Director, during which he served as chairman of the Administration and Benefits and Funding and Monitoring Committees, and was latterly Deputy Chairman of the Trustee Board. I would like to thank him for the valuable contribution he made to the Board.

Following John McGuire’s retirement, David Morrison has been appointed by the Trustee Board as Deputy Chairman and Chairman of the Administration and Benefits Committee.

The Board welcomed two new Trustee Directors. George Graham and Fiona Davis joined as bank appointed Trustee Directors on 21 September 2011 and 21 March 2012 respectively.

We hope you find this newsletter informative, and if you want more information on anything we have covered, please contact Group Pension Services.

Finally, I would like to thank my fellow Trustee Directors and our internal and external advisors for their commitment and support throughout yet another challenging year.

Miller McLean Chairman - RBS Pension Trustee Limited

August 2012

Your pension team The Trustee Board is responsible for operating the Fund in line with its formal rules and pensions law. We also have a duty to protect the interests of all our Fund members, including our pensioners and those who are no longer employed by the Group, but who still have benefits in the Fund (our deferred members).

Find out moreThe following documents are available on request from Group Pension Services:

> Latest Actuarial Valuation Report Contains details of the Fund’s financial position as at 31 March 2010.

> Latest Annual Report and Accounts

Shows the Fund’s income and expenditure in the 12 months to 31 March 2012.

> Current Schedule of ContributionsShows how much money is being paid into the Fund.

> Trustee’s Statement of Funding PrinciplesExplains how we plan to make sure enough money is paid into the Fund to provide the benefits that members have built up.

> Trustee’s Statement of Investment PrinciplesExplains how we invest the money paid into the Fund.

> Latest Engagement & Voting Report

Contact usIf you have a question, please email Group Pension Services:

Employee members

External [email protected]

Internal RBS Staff pension queries

Deferred members [email protected]

Pensioners [email protected]

Alternative formats This communication is available in large print, Braille or audio on request from Group Pension Services.

06 The RBS Group Pension Fund

Your current Trustee Directors are:Company SelectedMiller McLean [Chairman]David Morrison [Deputy Chairman]Stephen BoyleFiona DavisGeorge GrahamDonald Workman

Member electedPeter BoydPeter EastonStephen FallowellColin Wilson

Group Pension Services HR Shared Services The Royal Bank of Scotland Group PO Box 1390 Croydon CR9 1YB

The Royal Bank of Scotland Registered in Scotland No. 45551 Registered Office: 36 St. Andrew Square Edinburgh EH2 2YB

NewsMaking additional pension contributions [APeCs] - a tax efficient way to save for your retirement.The Trustees of the RBS Common Investment Fund have recently made a number of changes to the investment choices available to members, including some changes to the Growth Fund. As a reminder to members the current investment choices are summarised below:

Fund Objectives

Cash This actively managed fund aims to provide capital protection with returns in line with wholesale money market short-term interest rates.

Index-linked Gilt This passively managed fund invests in UK government index-linked gilts that have a maturity period of five years or longer.

Pre-retirement This fund invests in a blend of passively managed long-dated government bonds and actively managed long-dated corporate bonds. This approach aims to protect against changes in annuity rates (i.e. the cost of converting your saving into a pension) while providing some additional growth through income.

Diversified Growth This fund uses both active and passive management strategies across a blend of asset classes. The fund currently invests in UK equities, overseas equities (including ‘emerging markets’), corporate bonds and commercial property. This approach aims to deliver a return over CPI inflation of approximately 3-5% over the long term. Please note that prior to 1 October 2011 this fund was known as the Growth Fund and invested only in UK and overseas equities.

UK Equity Tracker This passively managed fund aims to perform in line with the UK stock market by investing in shares in UK companies in similar weights to the overall stock market.

International Equity Tracker

This passively managed fund aims to perform in line with the international stock market (overseas markets excluding the UK and emerging markets) by investing in shares in overseas companies in similar weights to the overall stock market.

UK Equity This actively managed fund aims to perform ahead of the UK stock market by investing in a selected set of shares in UK companies.

International Equity This actively managed fund aims to perform ahead of the international stock market (overseas markets excluding the UK and emerging markets) by investing in a selected set of shares in overseas companies.

Property This actively managed fund aims to achieve long-term capital growth through exposure to direct and indirect property investments in the UK and overseas.

Emerging Markets Equity Tracker

This passively managed fund aims to perform in line with the index of emerging markets stocks by holding shares in those companies in similar weights to the overall index.

Over 15 Year Gilt This passively managed fund aims to perform in line with the index of over 15 Year Gilts (UK government bonds).

Corporate Bond This actively managed fund aims to perform ahead of an index of over 10 Year Corporate Bonds by investing mainly in long dated bonds issued by both UK and overseas companies.

05 The RBS Group Pension Fund

RBS AA Pension Scheme merger Earlier this year, the Trustee accepted a proposal from the Group to merge the Defined Benefit section of the RBS AA Pension Scheme into the Group Fund. The merger took place on 31 March 2012 and created the AA Section of the RBS Group Pension Fund. The assets and liabilities of the AA Section are kept separate from those of the Group Fund Section.

State pension age The government continues to raise State pension age. By 2018 women will have to be age 65 and by 2020 both men and women will have to be age 66 in order to draw their State pension.

Changes during the yearJohn McGuire retired as a Trustee Director and Deputy Chairman of the Trustee Board on 21 March 2012.

David Morrison was appointed Deputy Chairman of the Trustee Board on 21 March 2012.

Peter Easton stepped down from the Investment Committee and joined the Administration and Benefits Committee on 21 March 2012.

Colin Wilson stepped down from the Administration and Benefits Committee and joined the Investment Committee on 21 March 2012.

Trustee meetings during the yearThe Trustee Board met five times during the period.

In addition the Trustee Board met the Group on a number of occasions to discuss the funding strategy of the Fund.

The Trustee Board sub committees met as follows during the period:

• The Administration and Benefits Committee met seven times• The Funding and Monitoring Committee met seven times• The Investment Committee met five times

Data protection We hold information about you in order to provide your pension benefits (such as pensions, lump sums, death benefits), which may include information obtained from third parties.

This information may be shared with:

• Companies within the Royal Bank of Scotland Group (please contact us if you do not want us to share your information with these companies);

• Other third parties who assist us in administering your benefits (e.g. updating personal data, calculating and paying benefits);

• Those where we have your permission to do so; and • Those where we are required to do so by law

If you want a copy of the information we hold about you, please contact us. A fee may be payable.

The RBS Group Pension Fund

Message from the ChairmanWelcome to the 2012 newsletter for members of the Group Fund.

Members’ Newsletter 2012

The RBS Group Pension Fund 01

Contents

> 01 Message from the Chairman

> 02 Investment report

> 03 Distribution of assets

> 04 Fund finances

> 05 News

> 06 Your pension team

This newsletter is produced by the Trustee Board to keep you abreast of changes in the Fund, and to provide you with an update on the Fund’s financial position.

The Fund is one of the largest pension schemes in the UK and the Trustee Board keeps the financial health of the Fund under constant review.

I am pleased to report that the value of the net assets increased during the year to £22.8 billion at 31 March 2012.

The Investment Executive has continued to support the Trustee Board in all aspects of investing the Fund’s assets, and I am able to report another year of excellent performance, with investment income and capital growth adding over £2.2 billion to the value of the Fund over the year.

More details of the Fund’s assets and the work of the Investment Executive are included on pages 2, 3 and 4.

We continue to review the funding strategy for the Fund and work effectively with the Principal Employer as scheme sponsor.

The Trustee Board has been informed by the Group that in order to control the cost of its final salary pension benefit responsibilities, the Group is currently consulting with staff concerning a number of proposed contractual changes to pensions. These changes are presently subject to the outcome of a consultation with members.

Details of the main changes are summarised below:

– Increase in normal pension age for future service to age 65, without affecting the existing RBSelect charge. However, employees can elect to pay an additional RBSelect charge of 5% to maintain their normal pension age of 60 for future service.

– Increase in the age of eligibility to receive an undiscounted pension from age 50 to 55.

The Group has agreed to keep the Trustee Board informed throughout the consultation period.

It is important that you plan for your retirement and make informed decisions about your retirement savings. With this in mind, current employees who are members of the Group Fund are able to make use of the retirement planner provided by the Group which may be accessed through Your Reward online.

Merger with the RBS AA Pension Scheme The final salary section of the RBS AA Pension Scheme (formerly the ABN Amro UK Pension Fund) was merged with the Group Fund on 31 March 2012.

A new section has been created within the Group Fund, which will be known as the ‘AA Section of the RBS Group Fund’. This section will be financially separate from the remainder of the Group Fund, and the benefit rules of the AA Scheme will be incorporated into this new AA Section.

Changes to the Board There have been a number of changes to the Trustee Board since last year’s newsletter.

John McGuire retired on 21 March 2012 after nine years as a Trustee Director, during which he served as chairman of the Administration and Benefits and Funding and Monitoring Committees, and was latterly Deputy Chairman of the Trustee Board. I would like to thank him for the valuable contribution he made to the Board.

Following John McGuire’s retirement, David Morrison has been appointed by the Trustee Board as Deputy Chairman and Chairman of the Administration and Benefits Committee.

The Board welcomed two new Trustee Directors. George Graham and Fiona Davis joined as bank appointed Trustee Directors on 21 September 2011 and 21 March 2012 respectively.

We hope you find this newsletter informative, and if you want more information on anything we have covered, please contact Group Pension Services.

Finally, I would like to thank my fellow Trustee Directors and our internal and external advisors for their commitment and support throughout yet another challenging year.

Miller McLean Chairman - RBS Pension Trustee Limited

August 2012

Your pension team The Trustee Board is responsible for operating the Fund in line with its formal rules and pensions law. We also have a duty to protect the interests of all our Fund members, including our pensioners and those who are no longer employed by the Group, but who still have benefits in the Fund (our deferred members).

Find out moreThe following documents are available on request from Group Pension Services:

> Latest Actuarial Valuation Report Contains details of the Fund’s financial position as at 31 March 2010.

> Latest Annual Report and Accounts

Shows the Fund’s income and expenditure in the 12 months to 31 March 2012.

> Current Schedule of ContributionsShows how much money is being paid into the Fund.

> Trustee’s Statement of Funding PrinciplesExplains how we plan to make sure enough money is paid into the Fund to provide the benefits that members have built up.

> Trustee’s Statement of Investment PrinciplesExplains how we invest the money paid into the Fund.

> Latest Engagement & Voting Report

Contact usIf you have a question, please email Group Pension Services:

Employee members

External [email protected]

Internal RBS Staff pension queries

Deferred members [email protected]

Pensioners [email protected]

Alternative formats This communication is available in large print, Braille or audio on request from Group Pension Services.

06 The RBS Group Pension Fund

Your current Trustee Directors are:Company SelectedMiller McLean [Chairman]David Morrison [Deputy Chairman]Stephen BoyleFiona DavisGeorge GrahamDonald Workman

Member electedPeter BoydPeter EastonStephen FallowellColin Wilson

Group Pension Services HR Shared Services The Royal Bank of Scotland Group PO Box 1390 Croydon CR9 1YB

The Royal Bank of Scotland Registered in Scotland No. 45551 Registered Office: 36 St. Andrew Square Edinburgh EH2 2YB

NewsMaking additional pension contributions [APeCs] - a tax efficient way to save for your retirement.The Trustees of the RBS Common Investment Fund have recently made a number of changes to the investment choices available to members, including some changes to the Growth Fund. As a reminder to members the current investment choices are summarised below:

Fund Objectives

Cash This actively managed fund aims to provide capital protection with returns in line with wholesale money market short-term interest rates.

Index-linked Gilt This passively managed fund invests in UK government index-linked gilts that have a maturity period of five years or longer.

Pre-retirement This fund invests in a blend of passively managed long-dated government bonds and actively managed long-dated corporate bonds. This approach aims to protect against changes in annuity rates (i.e. the cost of converting your saving into a pension) while providing some additional growth through income.

Diversified Growth This fund uses both active and passive management strategies across a blend of asset classes. The fund currently invests in UK equities, overseas equities (including ‘emerging markets’), corporate bonds and commercial property. This approach aims to deliver a return over CPI inflation of approximately 3-5% over the long term. Please note that prior to 1 October 2011 this fund was known as the Growth Fund and invested only in UK and overseas equities.

UK Equity Tracker This passively managed fund aims to perform in line with the UK stock market by investing in shares in UK companies in similar weights to the overall stock market.

International Equity Tracker

This passively managed fund aims to perform in line with the international stock market (overseas markets excluding the UK and emerging markets) by investing in shares in overseas companies in similar weights to the overall stock market.

UK Equity This actively managed fund aims to perform ahead of the UK stock market by investing in a selected set of shares in UK companies.

International Equity This actively managed fund aims to perform ahead of the international stock market (overseas markets excluding the UK and emerging markets) by investing in a selected set of shares in overseas companies.

Property This actively managed fund aims to achieve long-term capital growth through exposure to direct and indirect property investments in the UK and overseas.

Emerging Markets Equity Tracker

This passively managed fund aims to perform in line with the index of emerging markets stocks by holding shares in those companies in similar weights to the overall index.

Over 15 Year Gilt This passively managed fund aims to perform in line with the index of over 15 Year Gilts (UK government bonds).

Corporate Bond This actively managed fund aims to perform ahead of an index of over 10 Year Corporate Bonds by investing mainly in long dated bonds issued by both UK and overseas companies.

05 The RBS Group Pension Fund

RBS AA Pension Scheme merger Earlier this year, the Trustee accepted a proposal from the Group to merge the Defined Benefit section of the RBS AA Pension Scheme into the Group Fund. The merger took place on 31 March 2012 and created the AA Section of the RBS Group Pension Fund. The assets and liabilities of the AA Section are kept separate from those of the Group Fund Section.

State pension age The government continues to raise State pension age. By 2018 women will have to be age 65 and by 2020 both men and women will have to be age 66 in order to draw their State pension.

Changes during the yearJohn McGuire retired as a Trustee Director and Deputy Chairman of the Trustee Board on 21 March 2012.

David Morrison was appointed Deputy Chairman of the Trustee Board on 21 March 2012.

Peter Easton stepped down from the Investment Committee and joined the Administration and Benefits Committee on 21 March 2012.

Colin Wilson stepped down from the Administration and Benefits Committee and joined the Investment Committee on 21 March 2012.

Trustee meetings during the yearThe Trustee Board met five times during the period.

In addition the Trustee Board met the Group on a number of occasions to discuss the funding strategy of the Fund.

The Trustee Board sub committees met as follows during the period:

• The Administration and Benefits Committee met seven times• The Funding and Monitoring Committee met seven times• The Investment Committee met five times

Data protection We hold information about you in order to provide your pension benefits (such as pensions, lump sums, death benefits), which may include information obtained from third parties.

This information may be shared with:

• Companies within the Royal Bank of Scotland Group (please contact us if you do not want us to share your information with these companies);

• Other third parties who assist us in administering your benefits (e.g. updating personal data, calculating and paying benefits);

• Those where we have your permission to do so; and • Those where we are required to do so by law

If you want a copy of the information we hold about you, please contact us. A fee may be payable.