news & analysis - web1.amchouston.comweb1.amchouston.com/flexshare/001/cfa/moody's/mco 2016...

TRANSCRIPT

MOODYS.COM

11 AUGUST 2016

NEWS & ANALYSIS Corporates 2 » Walmart Accelerates Online Presence with Credit-Positive

Jet.com Purchase » Steinhoff’s Acquisition of Mattress Firm Is Credit Positive

for Both » China Railway Group Signs Credit-Positive Construction Project » China Evergrande’s Purchase of China Vanke Stake Is

Credit Negative

Infrastructure 7 » INVEPAR’s Asset Sales Are Credit Positive

Banks 9 » BICSA Board Members’ Resignation Will Drive Up Funding

Costs, a Credit Negative » National Bank of Greece’s €300 Million SME Securitisation Is

Credit Positive » Pakistani Banks Would Benefit from Amendments to Financial

Institutions Law » Philippine Regulators’ Fine Against Rizal Commercial Banking

Corporation Is Credit Negative

Asset Managers 16 » TIAA’s Proposed Acquisition of EverBank Is Credit Negative

US Public Finance 17 » Maryland Governor’s Decision to Withhold Pension and School

Funds Is Credit Negative for Counties » Atlantic City, New Jersey’s Loan Agreement with the State Is

Credit Positive

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 21 » Go to Last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Corporates

Walmart Accelerates Online Presence with Credit-Positive Jet.com Purchase On Monday, Wal-Mart Stores, Inc. (Aa2 stable) said that it would pay $3.3 billion to buy Jet.com, a fledgling pure-play online retailer launched in 2015 that has yet to generate a profit. The deal, which will also give Walmart’s management access to the online expertise of Jet’s co-founder and CEO Marc Lore, who will become Walmart’s head of US e-commerce, is credit positive for Walmart and continues the company’s aggressive efforts to expand its online operations.

Walmart is building its online business, which currently generates $14-$15 billion in annual revenue, to help augment the retailer’s approximately $470 billion of revenue brick-and-mortar business. Although we expect that it will likely be a while before we can assess the return on this pending acquisition, Walmart’s financial strength and excellent liquidity give the company plenty of time from a credit perspective to integrate and leverage Jet.

The Jet acquisition follows Walmart’s joint-venture in China with JD.com in June and demonstrates that Walmart is attacking online retail with significant zeal. Although we believe that catching up to online retailing giant Amazon.com, Inc. (Baa1 stable) from both a revenue and brand perspective is an unrealistic goal for any brick-and-mortar retailer, Walmart now has a definite advantage over its competitors in the very important race to be No. 2 online. Being online shoppers’ second-most-clicked site after Amazon is important for brick-and-mortar retailers as they continue to morph online. Walmart is aggressively positioning itself to be that site.

Walmart’s online sales grew around 12% for fiscal 2016, which ended 31 January 2016, down from the 22% growth rate the company recorded a year earlier. In round numbers, Walmart sells around $200 billion in grocery-equivalents of the $350 billion or so of its total US sales (including its Sam’s Club subsidiary). Of the remaining $150 billion in US revenue that we believe it can move online, we estimate that Walmart is selling around $11 billion online in the US out of the $14-$15 billion it sells globally. To put this into context, we estimate that Target Corporation’s (A2 stable) 34% year-over-year growth in online sales in the fiscal 2016 fourth quarter, which ended January 2016, resulted in the company’s online business totaling only around $2 billion for the fiscal year. In addition, we note that it took Amazon roughly 10 years to reach $11 billion in sales, which it did in 2006.

Just as we have said that we do not expect a brick-and-mortar retailer to catch up to Amazon online, Amazon will not catch up with too many retailers from a brick-and-mortar perspective, which is where more than 90% of retail sales occur. Still, a $14-$15 billion global online business for Walmart is no small feat, especially when it augments a brick-and-mortar business that generates around $470 billion in annual sales.

Charlie O’Shea Vice President - Senior Credit Officer +1.212.553.3722 charles.o’[email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Steinhoff’s Acquisition of Mattress Firm Is Credit Positive for Both Last Sunday, Steinhoff International Holdings N.V. (Baa3 stable) announced that it will buy Mattress Holding Corp. (Mattress Firm, B1 review for upgrade) for $3.8 billion. Steinhoff will fund the purchase using a $2 billion term loan with staggered maturities over two to five years and a $1.8 billion bridge loan, which it intends to replace with equity. The transaction is credit positive for both companies: Steinhoff will pay down Mattress Firm’s $1.4 billion of debt and increase its own scale and geographic diversification into the US, a new market for it that has favorable long-term growth prospects for mattress demand.

The transaction also demonstrates Steinhoff management’s commitment to funding large-scale acquisitions with an appropriate balance of debt and equity to protect the company’s credit metrics (see exhibit). Following the announcement, we affirmed Steinhoff’s ratings and outlook and placed Mattress Firm’s ratings on review for upgrade.

Steinhoff’s Debt/Equity After Mattress Firm Acquisition Replacing the bridge loan with equity reduces debt/equity below our Ba1 quantitative guidance.

Sources: Moody’s Investors Service, Steinhoff International Holdings and Mattress Holding

We expect Steinhoff to expand Mattress Firm’s in-store product offering and take advantage of cross-selling opportunities to customers, as it has done with its European retail outlets. Steinhoff will remove management’s non-value-added tasks related to public company management, also consistent with the company’s past acquisitions. This will allow Mattress Firm’s seasoned management team to focus more on growth opportunities and expediting delivery of synergies derived from Mattress Firm’s integration of its recent Sleepy’s acquisition.

Over the next several quarters, we expect Mattress Firm to have only modest earnings growth because of tepid consumer demand for big-ticket items amid macroeconomic uncertainty and temporary weakness from rebranding acquired stores. Mattress Firm underperformed its public guidance in 2015 and first-quarter 2016, and Sleepy’s experienced a significant EBITDA decline in fourth-quarter 2015, both driven in part by distraction from the acquisitions. We expect that some of this effect will be masked in the scaling effect of Steinhoff’s credit metrics and by pro forma considerations for acquisitions at both companies, where the effect may not be initially apparent in Steinhoff’s earnings.

3.32x

3.86x

3.37x

3.3x

3.4x

3.5x

3.6x

3.7x

3.8x

3.9x

Steinhoff2015

Steinhoff + Mattress FirmForecast Fiscal 2017 Including Bridge

Loan

Steinhoff + Mattress FirmForecast Fiscal 2017 Bridge Loan

Replaced with Equity

Actual and Forecast Ba1 Quantitative Guidance > 3.5x

Douglas Rowlings Assistant Vice President - Analyst +971.4.237.9543 [email protected]

Raya Sokolyanska Vice President - Senior Analyst +1.212.553.7415 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Nevertheless, Mattress Firm should demonstrate solid earnings growth over the next several years. We view store openings as a key growth driver, given that new stores pay back on a cash basis within a year and reach maturity quickly. Mattress Firm also has opportunities to grow accessory and private-label sales. We also foresee positive industry fundamentals owing to a release of pent-up demand driven by a return to average US household formation levels and mattress replacement needs. Mattress Firm’s growth opportunities and synergy potential, along with favorable fundamentals, should result in an increase in Steinhoff’s US earnings.

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

China Railway Group Signs Credit-Positive Construction Project On Tuesday, China Railway Group Limited (CRG, A3 negative) announced that it had signed a RMB20.8 billion railway construction contract for the Bangladesh Padma Bridge Railway Link Project with Bangladesh Railway. The contract, CRG’s second in Bangladesh and significantly larger than its first one, is credit positive for CRG because it will help the company gain more business in Bangladesh. This latest contract will equal approximately 1.2% of CRG’s total order backlog and 3.3% of the company’s RMB621 billion revenue in 2015. The project involves building a 168.6-kilometer railway over 54 months.

We expect CRG’s revenue from its overseas operations to grow to 7%-8% of its total revenue over the next three years from about 5% in 2015, reflecting the company’s efforts to penetrate overseas markets. CRG’s revenue should grow by 3%-4% annually in 2016 and 2017, supported by its strong order backlog of RMB1.8 trillion at the end of 2015, continued overseas expansion and the likelihood that China’s solid infrastructure spending on railways, urban rail and roads will continue over the next two years. Additionally, we expect the company to maintain an adjusted EBITDA margin of 5.0%-5.5% over the next two years, versus the 5.1% recorded in 2015, given its extended service offerings and continued cost controls.

CRG plans to keep its investments in real estate development, and its build-transfer, build-operate-transfer and public-private partnership projects to manageable levels, limiting increases in debt over the next two years. We project CRG’s adjusted debt/EBITDA falling to about 5.5x during 2016-17 from 6.3x in 2015, driven by steady earnings growth and limited debt growth. Excluding CRG’s non-recourse build-operate-transfer project debt, the company’s adjusted debt/EBITDA will decrease to about 4.8x in 2017 from 5.5x in 2015. This level of leverage is in line with its standalone credit quality.

Chenyi Lu Vice President - Senior Analyst +852.3758.1353 [email protected]

Iris Liu Associate Analyst +852.3758.1532 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

China Evergrande’s Purchase of China Vanke Stake Is Credit Negative Last Thursday, China Evergrande Group (B2 negative) announced that it had acquired a 4.68% stake in China Vanke Co., Ltd. (Baa1 stable) for around RMB9.1 billion. The investment is credit negative for Evergrande because it undermines the company’s effort to control its debt growth and raises financial and investment risk.

We believe the acquisition is a financial investment with little strategic value given its small size. The acquisition continues Evergrande’s active investment activity in recent years, including purchasing equity stakes in Shengjing Bank as well as in companies in the insurance, consumer goods and healthcare services sectors.

Evergrande’s pursuit of debt-funded expansion to support its business growth lowered the company’s adjusted revenue/debt ratio to 35% in 2015 from 52% in 2014. The series of investments and acquisitions announced this year will consume some of Evergrande’s cash on hand, which will constrain its ability to limit further debt growth. We expect that Evergrande’s debt leverage, as measured by revenue/debt, will remain elevated at 40%-45% over the next 12-18 months as the company continues to pursue debt-funded acquisitions. This debt leverage level is weak for the company’s B2 corporate family rating.

However, the liquidity drain from acquiring the China Vanke stake is manageable for Evergrande since it has sufficient cash reserves to fund the investment. In particular, the scale of the investment constitutes around 5.6% of the company’s RMB164 billion of cash at the end of 2015. On a pro forma basis, the company’s ratio of cash to short-term debt would weaken to around 98% from 103% as of the end of 2015.

Additionally, Evergrande’s strong contracted sales growth will likely support its liquidity: the company, one of the largest residential developers in China, recorded contracted sales of RMB184.8 billion for the first seven months of 2016, up 82.6% from the same period in 2015. At 31 December 2015, Evergrande’s land bank totaled 156 million square meters in gross floor area in 162 Chinese cities.

Franco Leung Vice President - Senior Credit Officer +852.3758.1521 [email protected]

Victor Wong Associate Analyst +852.3758.1569 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Infrastructure

INVEPAR’s Asset Sales Are Credit Positive On Monday, Brazilian infrastructure company Investimentos e Participações em Infraestrutura S.A. - INVEPAR (B2/Ba2.br negative) announced that it had sold Línea Amarilla S.A.C. (LAMSAC, unrated) and PEX Peru (unrated) to Vinci Highways for BRL4.5 billion (approximately $1.4 billion, gross of taxes). The asset sales, which require regulatory approval, are credit positive for INVEPAR because they will provide liquidity as the company grapples with substantially lower operating revenues at its transportation infrastructure concessions in Brazil.

LAMSAC, an urban express toll road in Lima, Peru, and PEX Peru, an electronic payment service provider focused on Peru, accounted for 13% of INVEPAR’s consolidated EBITDA in 2015. Vinci Highways is a subsidiary of France’s Vinci S.A. (A3 stable), the holding company of one of Europe’s largest concession and construction companies.

A key factor behind INVEPAR’s revenue challenges has been Guarulhos International Airport (GRU Airport, unrated), the 40.8%-owned concessionaire in the municipality of Guarulhos in the Brazilian state of São Paolo. GRU Airport is INVEPAR’s single-largest revenue-generating asset and Brazil’s prolonged domestic recession has stymied the realization of revenue forecasts originally envisaged in a scenario of economic expansion.

Using our standard adjustments, INVEPAR’s credit metrics have materially deteriorated since 2015, with the company’s funds from operations (FFO) falling to negative BRL33 million in the 12 months that ended 31 March 2016, from BRL470 million in 2015. The company’s FFO/debt ratio also fell to negative 0.1% in the 12 months that ended 31 March 2016, from 1.9% in 2015, while its cash interest coverage declined to 1.0x from 1.4x. As of 31 March 2016, INVEPAR had BRL1.8 billion of financial debt maturing in the next 12 months, in addition to BRL1.3 billion in short-term maturing concession fees, which we treat as debt. Concession fees of BRL1.1 billion relate to GRU Airport, BRL350 million of which the company paid on 11 July, with the balance to be paid in monthly installments until December 2016 (see Exhibit 1).

EXHIBIT 1

INVEPAR’s Debt Maturity Profile as of 31 March 2016

Source: INVEPAR

0

1

2

3

4

5

6

ResourcesAvailable

Apr 2016 -Mar 2017

Apr - Dec2017

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027+

BRL

Billi

on

Cash and Cash Equivalents Financial Debts Concession Payments Sale of LAMSAC

Alexandre Leite Vice President - Senior Credit Officer +55.11.3043.7353 [email protected]

Camila Yochikawa Associate Analyst +55.11.3043.6079 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

As Exhibit 2 shows, selling LAMSAC and PEX Peru will substantially improve INVEPAR’s liquidity. In addition, we expect that INVEPAR will be able to refinance a substantial portion of its soon-to-be maturing short-term debt, given that the company has demonstrated its ability to access the capital markets and obtain financing from Brazil’s state-owned development bank Banco Nacional de Desenvolvimento Econômico e Social.

EXHIBIT 2

INVEPAR’s Credit Metrics

31 December 2014

31 December 2015

12 Months to 31 March 2016

12-18 Month Forward

View

Cash Interest Coverage 2.6x 1.4x 1.0x 1.5x

Funds from Operations/Debt 5.2% 1.9% -0.1% 2.1%

Current Ratio (Current Assets/Current Liabilities) 62.1% 23.3% 17.3% 52.6%

(Cash + Marketable Securities)/Short-Term Debt 59.1% 15.3% 16.5% 41.0%

Source: Moody’s Financial Metrics

Notwithstanding the credit-positive effects of the LAMSAC and PEX Peru sales, some of INVEPAR’s concessions have relatively large capex requirements, which means that a sustainable improvement in INVEPAR’s credit metrics will depend on assets whose performance strongly correlates with economic growth.

Rio de Janeiro, Brazil-based INVEPAR has concessions in urban mobility projects, toll roads and the GRU Airport. For the 12 months that ended 31 March 2016, INVEPAR had consolidated net revenues (excluding construction revenues) of BRL3.5 billion, EBITDA (including interest income) of BRL1.9 billion and total debt of BRL23.9 billion (including the GRU Airport concession fee payments), all based on using our standard adjustments.

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Banks

BICSA Board Members’ Resignation Will Drive Up Funding Costs, a Credit Negative Last Thursday, three board members of Banco Internacional de Costa Rica, S.A. (BICSA, B1 negative, b21) resigned amid an ongoing conflict between the bank’s two shareholders. The resignations of three board members, which constitute one third of the bank’s board, are credit negative because turmoil around BICSA’s corporate governance and business strategy threatens to create funding and liquidity stress that reduces profitability. This contributed to our downgrade on Tuesday of BICSA’s baseline credit assessment to b2 from ba2, and its foreign currency deposit rating to B1 from Ba2 with a negative outlook.

BICSA is a Panamanian subsidiary of two government-owned Costa Rican banks, and depends on confidence-sensitive short-term wholesale funding. Over the past year, its liquidity has weakened as a result of rapid loan growth, reducing its capacity to manage increased headline risks stemming from disagreements between the bank’s 51% majority shareholder, Banco de Costa Rica (BCR, Ba1/Ba1 negative, ba2), and 49% minority shareholder, Banco Nacional de Costa Rica (BNCR, Ba1/Ba1 negative, ba2). The three board members who resigned had been appointed by BNCR.

Funding costs at BICSA are likely to continue to rise in part as a result of increased market volatility and rising reputational risk related to the “Panama Papers” leak, which raised questions about anti-money laundering controls at Panamanian financial institutions. Total interest expenses jumped about 20% as of June 2016 from a year earlier, led by a 61% rise in deposit costs. This, in part, contributed to a 40% drop in net income, and funding outlays may rise further until new board members are appointed.

Over the coming months, we expect BICSA’s management to focus on protecting its funding and strengthening its liquidity rather than growing its business. Liquid assets were around 16% of BICSA’s total assets as of June 2016, up from 12.5% three months earlier, but still below the 22% recorded in March 2015. Throughout the second half of 2015, and especially in early 2016, the bank drew down its liquid assets, mostly interbank deposits, to grow its loan book, and its relatively thin liquidity cushion leaves the bank more exposed to rollover risks.

The jump in BICSA’s funding costs comes as the bank confronts other profitability challenges. BICSA has tried to grow its regional corporate banking franchise, but competition from larger banks has led to a decline in its net interest margins. Additionally, BICSA is making significant investments to upgrade its information technology capabilities, which will reduce its already modest efficiency. As a result of these challenges, we expect BICSA’s annualized net income to fall to around 0.5% of tangible assets at the end of 2016, from 0.67% as of June and 0.9% as of December 2015 (see exhibit below).

1 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating (where available) and baseline

credit assessment.

Georges Hatcherian Analyst +52.55.1555.5301 [email protected]

Vicente Gomez Associate Analyst +52.55.1555.5304 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Banco Internacional de Costa Rica’s Key Profitability Metrics

Source: Moody’s Investors Service

0%

10%

20%

30%

40%

50%

60%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2014 2015 1Q16 2Q16

Cost-Income - right axis NIM - left axis Net Income/Tangible Assets - left axis

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

National Bank of Greece’s €300 Million SME Securitisation Is Credit Positive On Monday, National Bank of Greece S.A. (NBG, Caa3/Caa3 stable, caa32) announced that it had completed a small and midsize enterprise (SME) securitisation that will raise up to €300 million of medium-term funding by placing the senior notes with the European Investment Bank (Aaa stable), European Investment Fund (Aaa stable) and European Bank for Reconstruction and Development (Aaa stable). The deal is credit positive for NBG because it lowers NBG’s funding cost and provides an alternative funding source that will help the bank reduce its dependence on emergency liquidity assistance (ELA) from the Bank of Greece.

The SME securitisation is the first of its kind in Greece since 2007, given that international investors have been hesitant to invest in Greek assets over the past few years owing to the country’s dire economic conditions. Greek banks have not been able to access the international bond market since 2014. We consider this SME securitisation to be a sign of increased confidence toward both NBG and Greek assets as collateral, paving the way for similar transactions with multilateral European entities that have a mandate to support Greece’s SME sector. However, given the deep challenges the market continues to face, we expect private investor interest for such deals to remain low until there is an ongoing improvement in Greece’s economy.

The transaction will allow NBG to partly reduce its dependence on the costly ELA, which equals approximately €5.8 billion currently, down from €17.6 billion in June 2015 (see exhibit below). All Greek banks’ central bank funding, including borrowing from the European Central Bank and the ELA, increased dramatically in the first half of 2015 because of a sustained deposit outflow until the imposition of capital controls in late June 2015. Since then, all Greek banks have sought to reduce their dependence on the ELA, and gradually move toward a more self-sufficient and sustainable funding profile.

National Bank of Greece’s Central Bank Funding

Source: The bank

2 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating (where available) and baseline

credit assessment.

€ 14.2€ 9.8 € 10.0 € 10.1

€ 12.5 € 11.8€ 9.6 € 8.4

€ 13.9€ 17.6 € 15.6 € 11.5 € 11.0

€ 11.2

€ 5.8

€ 0

€ 5

€ 10

€ 15

€ 20

€ 25

€ 30

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 May-16 Aug-16

€Bi

lions

European Central Bank Emergency Liquidity Assistance

Nondas Nicolaides Vice President - Senior Credit Officer +357.25.693.006 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

NBG has been able to reduce its ELA balance significantly by more than €5 billion since March 2016, mainly because of €3.5 billion in proceeds from the sale of its Turkish subsidiary Finansbank AS (Ba1/Ba1 review for downgrade, ba3 review for downgrade) to Qatar National Bank (Aa3 negative, baa1), and an increase in its interbank repos in recent months. Additionally, the bank announced in late July that it was able to fully repay its government-guaranteed bonds used for ELA purposes, which carried an additional cost through fees paid to the government. As a result, NBG currently has the best funding risk profile among similarly rated local peers, although not strong enough to trigger a positive rating action.

Further reducing its high-cost ELA through this SME securitisation and potentially through new deposits will lower the bank’s funding cost and support its net interest margin, which was around 280 basis points in March 2016. This, in turn, will support NBG’s efforts to return to positive profitability (€26 million profit after tax in first-quarter 2016) and end the capital-consumption cycle that it has been through over the past few years.

Despite the relatively small size of Monday’s SME securitisation, it meets one of NBG’s strategic initiatives to support Greek SMEs and mid-cap companies through relatively cheap funding, creating employment for Greece’s youth. This is aligned with the bank’s commitment, as the second-largest commercial bank in the country, to be a leading force in Greece’s economic recovery.

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Pakistani Banks Would Benefit from Amendments to Financial Institutions Law Last Thursday, Pakistan’s National Assembly approved amendments to the Financial Institutions (Recovery of Finances) (Amendment) Bill 2016 that will benefit banks by enhancing their recovery efforts and strengthening their ability to resolve problematic assets in a timely manner. Such enhancements will improve the quality of banks’ loan books and clean up their balance sheets, a credit positive. Together with Pakistan’s Corporate Restructuring Companies Bill, which lawmakers approved earlier this year, these changes will address weaknesses in the legal framework for secured lending and foreclosures. The bill awaits final approval by Pakistan’s president before it becomes law.

The proposed amendments in the foreclosure clauses will allow banks to take hold of and sell mortgaged properties by means of a public auction without the intervention of courts. The amended law will also penalize wilful defaults (deliberate or intentional failure to make a payment to a bank when due) with imprisonment of up to seven years and/or a fine not exceeding the defaulted amount. Additionally, borrowers that have defaulted will be prohibited for 10 years from receiving bank loans.

The amendments will benefit banks by enhancing their recovery efforts and facilitating a more timely resolution of nonperforming loans (NPLs). Pakistani banks have been operating in a weak and inefficient recovery environment amid gaps in the legal and judicial framework with respect to collateral execution. As a result, banks’ balance sheets have been burdened with a large stock of legacy problem debts. According to the State Bank of Pakistan’s latest financial stability report, 86% of all NPLs are classified in the loss category (in arrears for more than a year).

National Bank of Pakistan (B3 stable, caa13) will benefit most from these amendments, given its higher stock of problem loans (20% of gross loans as of March 2016). Habib Bank Ltd. (B3 stable, b3), United Bank Ltd. (B3 stable, b3), MCB Bank Limited (B3 stable, b3) and Allied Bank Limited (B3 stable, b3) will also benefit from the introduction of these amendments, given their high exposure to collateralized corporate lending.

The amendments will remove certain legislative impediments, such as the inability to foreclose on property, that have made banks reluctant to extend mortgages. Mortgages currently constitute less than 1% of banks’ loan books and equaled around 0.2% of GDP as of March 2016 (see exhibit). This suggests that there is ample room for credit growth in an underserved segment and will allow banks to extend longer-term financing at higher yields. Indicatively, according to State Bank of Pakistan, current mortgage portfolio yields average around 10% for an average 12.5-year maturity.

3 The bank ratings shown in this report are the banks’ local currency rating and baseline credit assessment.

Corina Moustra, CFA Associate Analyst +357.25.693003 [email protected]

Elena Panayiotou Assistant Vice President - Analyst +357.25.693010 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Pakistani Banks’ Loan Book Composition as of March 2016

Source: State Bank of Pakistan

The bill also will promote a healthier credit culture in Pakistan by minimizing the risk of defaults, and will make available previously unrecoverable amounts that can be directed to new lending in the private sector. We expect that the improvements in the legal and judicial framework, along with the implementation of the China Pakistan Economic Corridor,4 will bolster economic growth and lending to the private sector.

4 The China Pakistan Economic Corridor is a $46 billion construction project to upgrade Pakistan’s infrastructure and connect

Pakistan and China through a transport link, the development of special economic zones and coal, wind, solar and hydro energy projects.

Agriculture, Hunting and Forestry6%

Food Products and Beverages10%

Textiles13%

Chemicals5%

Manufacturing - Other11%

Electricity, Gas and Water Supply6%

Construction and Real Estate4%

Commerce and Trade5%

Transport, Storage and Communications4%

Personal Loans8%

Mortgages1%

Government and Public Sector Entreprises22%

Other5%

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Philippine Regulators’ Fine Against Rizal Commercial Banking Corporation Is Credit Negative Last Friday, Rizal Commercial Banking Corporation (RCBC, Baa3/Baa3 stable, ba15) announced that the Philippines’ central bank had imposed a PHP1 billion ($21.3 million) fine on the bank in connection with an $81 million cyber heist from Bangladesh Bank (unrated). The imposition of the fine is credit negative because it will directly reduce the bank’s profitability. Additionally, the fine points to weaknesses in RCBC’s internal controls, particularly around anti-money laundering and other risk management systems.

The fine equals around 19% of the bank’s annualized net profit as of the first half of 2016. However, the bank will pay the penalty in two equal payments over the next year, easing the fine’s negative effect. In addition, as a direct consequence of the investigation, we expect that the bank will increase spending to strengthen its risk management and information-technology systems, which will raise operating costs over the next 12-18 months.

In February 2016, $81 million was electronically stolen from Bangladesh Bank and deposited into an RCBC branch. The funds were subsequently withdrawn from the bank, with some of the stolen money allegedly transferred to casinos based in the Philippines. The fallout from the cyber heist included the May 2016 resignation of then-RCBC CEO Lorenzo V. Tan. An internal investigation has since cleared Mr. Tan of breaching any bank rules and policies in connection with the heist. Another casualty of the heist was Atiur Rahman, governor of Bangladesh’s central bank, who resigned in March 2016.

We believe that this incident has harmed the bank’s reputation, as reflected by the negative growth in deposits in the first quarter of 2016 (see exhibit), when the incident was first reported. Although we do not know yet if the deposit outflow is entirely related to the investigation, the bank has sufficient liquidity buffers to withstand any further outflows. Liquid assets equaled about 29% of the bank’s tangible assets at the end of 2015.

Rated Philippine Banks’ Quarter-over-Quarter Deposit Growth

Note: The exhibit does not include data for Land Bank of the Philippines and United Coconut Planters Bank, for which quarterly data are not available. Sources: The banks

5 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating and baseline credit assessment.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

BDO UNIBANK, INC Bank of the PhilippineIslands

Metropolitan Bank & TrustCompany

Philippine National Bank Rizal Commercial BankingCorporation

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016

Alka Anbarasu Vice President - Senior Analyst +65.6398.3712 [email protected]

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Asset Managers

TIAA’s Proposed Acquisition of EverBank Is Credit Negative On Monday, Teachers Insurance and Annuity Association of America (TIAA, Aa1 stable), a provider of employer-sponsored retirement plans, announced that it had agreed to acquire savings and loan thrift EverBank Financial Corp. (unrated) for approximately $2.5 billion. Although the acquisition complements TIAA’s core pension business in the not-for-profit market, it is credit negative because the immediate negative financial effect (such as lower asset quality, risk-based capital and higher financial leverage) overwhelms any benefits that will accrue to TIAA over the next 12-18 months.

Although TIAA has not indicated how it intends to finance the transaction, we expect that TIAA will fund the bulk of the acquisition with liquid securities from its general account assets. Any use of incremental debt to pay the balance of the purchase price not covered by its general account assets will increase TIAA’s financial leverage and reduce earnings coverage, although only modestly given the size of the transaction.

TIAA will merge EverBank into its much smaller banking operations, which at 30 June 2016 had approximately $4 billion in total assets and $2.8 billion in total deposits, versus EverBank’s $27.4 billion in total assets and $18.8 billion in deposits as of the same date. The acquisition follows TIAA’s acquisition of Nuveen Investments, Inc. (unrated) in 2014 for $6.25 billion.

Although profitable, we view EverBank, which will be owned by TIAA, as a lower-quality investment with a modest competitive position. It has recently expanded rapidly into new business lines that are untested in a stress cycle. Additionally, one quarter of the $2.5 billion purchase price is allocated to goodwill, increasing TIAA’s exposure to intangibles and lowering our assessment of its asset quality through a higher high-risk asset ratio. When combined with a capital base that, under our stress scenario, is vulnerable to the performance of TIAA’s equity-related holdings (which now include EverBank), TIAA’s risk-based capital weakens.

The transaction accelerates TIAA’s strategy to expand its banking and lending capabilities to provide a broader suite of products to existing customers and the broader not-for-profit market. The acquisition also enhances distribution by giving the company access to a complementary customer base of approximately 300,000 retail clients and 13,000 commercial customers to whom it can cross-sell other TIAA products and services. However, given that TIAA expects to close the transaction in first-quarter 2017, and the transaction carries execution, integration and rebranding risks, it will take years for TIAA to realize the acquisition’s benefits.

TIAA has expanded into businesses that complement its core pension business and allow the company to diversify its income sources, expand its target market, provide financial solutions to retail customers along their different life stages, and create a one-stop financial services provider for institutional clients. We recognize the earnings diversification of these businesses and their service toward addressing the slow growth of the pension business. But asset management and banking are relatively weaker franchises. The Baa2 stable senior debt rating of TIAA Asset Management Finance Company, LLC, the immediate parent of Nuveen, are largely derived from the standalone credit profile of its only asset – Nuveen. And, because we consider EverBank as having a lower credit profile than its new owner, TIAA and its insurance subsidiaries will continue to be the foundation of TIAA’s credit quality.

Rokhaya Cissé, CFA Analyst +1.212.553.3870 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

US Public Finance

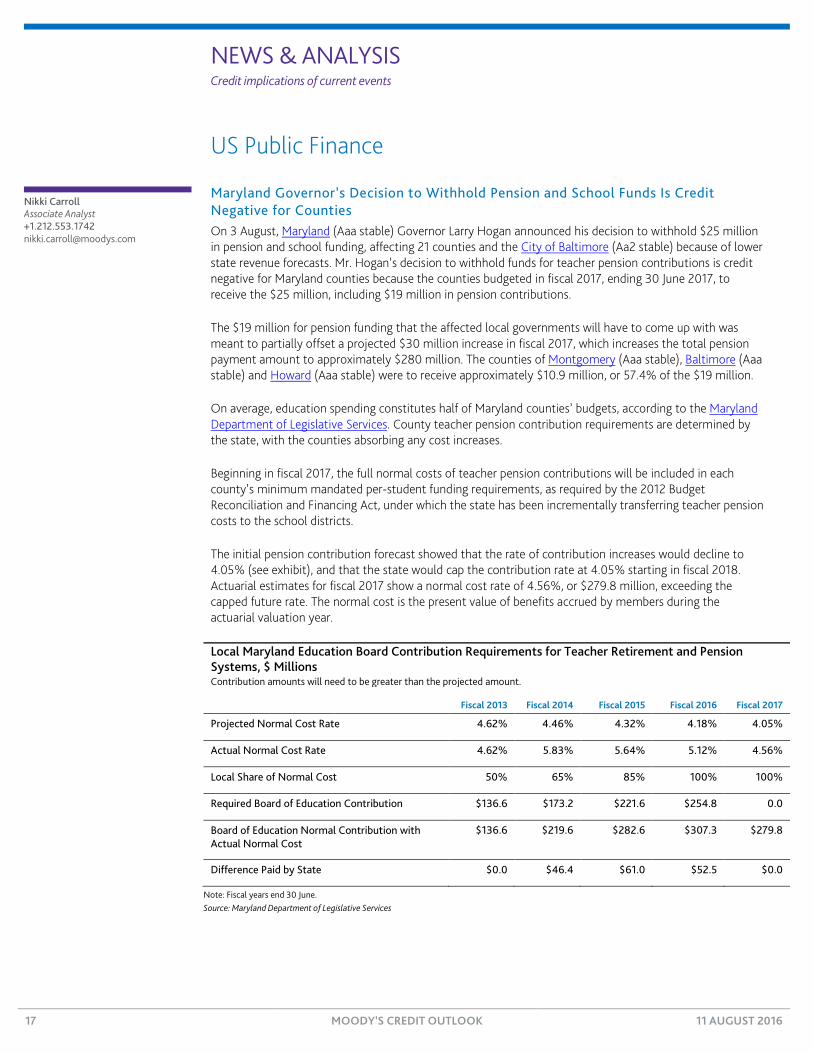

Maryland Governor’s Decision to Withhold Pension and School Funds Is Credit Negative for Counties On 3 August, Maryland (Aaa stable) Governor Larry Hogan announced his decision to withhold $25 million in pension and school funding, affecting 21 counties and the City of Baltimore (Aa2 stable) because of lower state revenue forecasts. Mr. Hogan’s decision to withhold funds for teacher pension contributions is credit negative for Maryland counties because the counties budgeted in fiscal 2017, ending 30 June 2017, to receive the $25 million, including $19 million in pension contributions.

The $19 million for pension funding that the affected local governments will have to come up with was meant to partially offset a projected $30 million increase in fiscal 2017, which increases the total pension payment amount to approximately $280 million. The counties of Montgomery (Aaa stable), Baltimore (Aaa stable) and Howard (Aaa stable) were to receive approximately $10.9 million, or 57.4% of the $19 million.

On average, education spending constitutes half of Maryland counties’ budgets, according to the Maryland Department of Legislative Services. County teacher pension contribution requirements are determined by the state, with the counties absorbing any cost increases.

Beginning in fiscal 2017, the full normal costs of teacher pension contributions will be included in each county’s minimum mandated per-student funding requirements, as required by the 2012 Budget Reconciliation and Financing Act, under which the state has been incrementally transferring teacher pension costs to the school districts.

The initial pension contribution forecast showed that the rate of contribution increases would decline to 4.05% (see exhibit), and that the state would cap the contribution rate at 4.05% starting in fiscal 2018. Actuarial estimates for fiscal 2017 show a normal cost rate of 4.56%, or $279.8 million, exceeding the capped future rate. The normal cost is the present value of benefits accrued by members during the actuarial valuation year.

Local Maryland Education Board Contribution Requirements for Teacher Retirement and Pension Systems, $ Millions Contribution amounts will need to be greater than the projected amount.

Fiscal 2013 Fiscal 2014 Fiscal 2015 Fiscal 2016 Fiscal 2017

Projected Normal Cost Rate 4.62% 4.46% 4.32% 4.18% 4.05%

Actual Normal Cost Rate 4.62% 5.83% 5.64% 5.12% 4.56%

Local Share of Normal Cost 50% 65% 85% 100% 100%

Required Board of Education Contribution $136.6 $173.2 $221.6 $254.8 0.0

Board of Education Normal Contribution with Actual Normal Cost

$136.6 $219.6 $282.6 $307.3 $279.8

Difference Paid by State $0.0 $46.4 $61.0 $52.5 $0.0

Note: Fiscal years end 30 June. Source: Maryland Department of Legislative Services

Nikki Carroll Associate Analyst +1.212.553.1742 [email protected]

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Under the act, each county was provided a projected normal cost to budget for their teacher pensions each year over the course of the five-year phase-in period, with the state supplementing part of the difference between the projected and the actual costs at an average of around $50 million per year.

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

Atlantic City, New Jersey’s Loan Agreement with the State Is Credit Positive On 6 August, we received confirmation that the Atlantic City, New Jersey (Caa3 negative), City Council had agreed to the terms of a bridge loan from the State of New Jersey (A2 negative) in an amount up to $73 million. Although the terms of the bridge loan are strict, the city reaching a loan agreement with the state is credit positive for the city and the Atlantic City School District.

Without the loan, there was a high probability the city would default in the next few months. Although this risk remains, the loan should buy the city time to complete its financial turnaround plan which is due in November. The loan also guarantees that the school district will continue to receive its full property tax payment from the city, a major source of concern for the district and a major burden for the city, which collects and guarantees the payments from its own tax levy. The loan also likely ensures that bondholders will receive the full $18.1 million in debt service payments that the city owes for the remainder of the year (see exhibit).

Atlantic City, New Jersey’s Monthly Debt Payments for the Rest of 2016 Debt payments peak in November 2016.

Date Payment Amount Security Enhancement1

15 August $165,000 2008 General Obligation Bonds None

1 September $1,911,488 2015A General Obligation Bonds; 2015B General Obligation Bonds

NJ MQBA

1 October $69,942 2012 Pension Obligation General Obligation Bonds AGM

1 November $9,362,311 2012 Tax Appeal General Obligation Bonds; 2012 Tax Appeal General Obligation Bonds - Taxable

AGM

1 December $2,331,175 2013 Tax Appeal General Obligation Bonds; 2013 General Obligation Bonds

None

15 December $4,777,527 2011 Tax Appeal General Obligation Bonds AGM

Notes: 1 NJ MQBA = New Jersey Municipal Qualified Bond Act. As part of the MQBA program, the 1 September payment will be made by the state and deducted from state aid funds owed to Atlantic City. AGM = Assured Guaranty Municipal Corp. Source: Atlantic City, New Jersey

The loan comes with some very tight conditions. In exchange for up to $73 million, the city pledged for repayment to the state particular revenue streams and assets, including the Atlantic City Alliance and investment alternative tax funds owed to the city. The state also reserves the right to withhold state aid and the right to force the city to sell its municipal water system and the former Bader Field airport if necessary. Additionally, the city will not receive the money in a lump sum, but instead as monthly payments, and all city requests for funds from the state must be made 10 days in advance. Theoretically, the city is allowed to make only a single request per month, but there is a provision to waive this condition with state consent. The loan is interest free, so long as the city makes its repayments on time. If the city were to default on any of the loan conditions, the loan would accrue interest at 1.75% per year.

Although the loan is nominally for up to $73 million, a portion of the nominal loan funds have already been spent or pledged. The city is obligated to use the initial proceeds from the loan to repay $8.5 million advanced by the state to cover the school district’s July tax levy, to pay the $9.8 million owed to the school district by the city for its first payment for fiscal 2017, which ends 30 June 2017, and to cover other post-employment benefits and pensions. We estimate that the remaining funds will be sufficient to cover the city’s debt obligations through November, at which time the city must present a financial recovery plan to the state, which would take over the city if the recovery plan is not accepted.

Douglas W. Goldmacher Analyst +1.212.553.1477 [email protected]

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

The city’s position remains dire given its dependence on a shrinking casino industry, as reflected by the announced closure earlier this month of the Trump Taj Mahal Casino. The casino, which intends to shut down on 10 October, employed 1,805 workers as of 30 June. Workers had been on strike for more than a month. Although we expect that other casinos in Atlantic City will capture a portion of the Trump Taj Mahal’s revenue, citywide gambling revenue is likely to decline. This, in turn, could have a knock-on effect on the city as the casinos’ payments in lieu of taxes (PILOT) can fluctuate depending on total casino revenues. This adds another layer of uncertainty to an already complex situation, given that the state, Atlantic County (Aa2 negative) and city have yet to determine how the PILOT payments will be divided among them.

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Monday’s Credit Outlook on moodys.com

21 MOODY’S CREDIT OUTLOOK 11 AUGUST 2016

NEWS & ANALYSIS Corporates 2 » Cott's Coffee Deal Perks-Up Diversification, a Credit Positive » Emerson Electric's Planned Business Divestitures Are

Credit Positive » Tenet's Settlement Agreement Is Credit Negative » Taj Mahal Casino's Demise Affords Remaining Atlantic City

Casinos a Bigger Share of Shrinking Gaming Revenues » ZF's Planned Acquisition of Haldex Will Slow Deleveraging » Fantasia's Leverage Will Increase with Wanda Property

Management Acquisition » CNOOC's Deal to Lower Natural Gas Pricing in Joint Venture

with Husky Energy Is Credit Positive

Infrastructure 9 » Exelon and Entergy Will Benefit from New York State's

Nuclear Power Subsidy » Aurizon Sells Stake in Sydney Intermodal Terminal Alliance, a

Credit Positive

Banks 11 » First Hawaiian's Initial Public Offering Is Credit Positive » HSBC's Share Buyback Is Credit Negative » Recommended 3% Leverage Ratio for European Union Banks

Would Be Credit Positive » Polish Banks' Profitability Will Decline If Currency Spreads

Are Reimbursed » Increased Tourism in Georgia Will Benefit Banks » Korea's Plan to Develop Mega Investment Banks Is Credit

Negative for Securities Companies » India's Proposal to Strengthen Debt Recovery Laws Is Credit

Positive for Banks » India's Non-Bank Finance Companies Will Benefit from Bank

Licensing Revisions

Insurers 25 » MetLife's $2 Billion Variable Annuity Reserve Charge Is

Credit Negative » Argentina's Higher Capital Requirements for Insurers and

Reinsurers Are Credit Positive » Taiwan Insurers’ Will Need Less Capital to Hold Domestic

Equity Investments, a Credit Negative

Sovereigns 31 » Moldova Will Benefit from Romania's Liquidity Support and

Staff-Level Agreement with IMF » Kuwait's Fuel Subsidy Reform Is Credit Positive

US Public Finance 34 » Zika Travel Advisory for Miami Is Credit Negative for City

and County

Securitization 36 » Japan's ¥28 Trillion Stimulus Package Credit Is Positive for

SMEs' Structured Finance Deals

MOODYS.COM

Report: 191587

© 2016 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

EDITORS SENIOR PRODUCTION ASSOCIATE Jay Sherman and Elisa Herr Amanda Kissoon