newday earnings call details: date: thursday 15 june time ... · 2015 2016 2017 q1 ltm open...

TRANSCRIPT

NewDayQuarter-end 31 March 2017

Results presentation

Earnings call details:

Date: Thursday 15 June

Time: 14:00 BST

Participants dial in: (+44) [0] 1452 554 265

0800 694 1630 (UK Free)

ID: 40552993

Important disclaimerThis presentation has been prepared by NewDay Cards Limited on behalf of NewDay Group (Jersey) Limited (the “Company”) on a confidential basis solely for information purposes. For

purposes of this notice, the presentation that follows shall mean and include the slides that follow, the oral presentation of the slides by the Company or any person on behalf of the

Company, any question-and-answer sessions that follows the oral presentation, printed copies of this document and any materials distributed at, or in connection with the presentation

(collectively, this “Presentation”). By attending the meeting at which this Presentation is made, or by reading this Presentation, you will be deemed to have (i) agreed to the following

restrictions and made the following undertakings and (ii) acknowledged that you understand the legal and regulatory sanctions attached to the misuse, disclosure or improper circulation of

this Presentation.

All financial information contained in this Presentation relates to the unaudited consolidated financial results of the Company (and not, except where expressly stated to the

case, NewDay BondCo plc). The financial information contained in this Document has not been audited, reviewed or verified by any independent accounting firm. All non-financial

information contained in this Presentation relates to the business, assets and operations of the Company together with its subsidiaries and subsidiary undertakings (the “Group”). Certain

financial data included in this presentation consists of “non-IFRS financial measures”. These non-IFRS financial measures, as defined by the Company, may not be comparable to similarly-

titled measures as presented by other companies, nor should they be considered as an alternative to the historical financial results or other indicators of the Company’s cash flow based on

IFRS. Even though the non-IFRS financial measures are used by management to assess the Company’s financial position, financial results and liquidity and these types of measures are

commonly used by investors, they have important limitations as analytical tools, and you should not consider them in isolation or as substitutes for analysis of the Company’s financial

position or results of operations as reported under IFRS. The inclusion of such non-IFRS financial measures in this Presentation or any related presentation should not be regarded as a

representation or warranty by the Company, any member of the Group, any of their respective affiliates, advisors or representatives or any other person as to the accuracy or completeness

of such information’s portrayal of the financial condition or results of operations of the Company and should not be relied upon when making an investment decision.

This Presentation may contain forward-looking statements. All statements other than statements of historical fact included in this Presentation are forward-looking statements. Forward-

looking statements express the Company’s current expectations and projections relating to their financial condition, results of operations, plans, objectives, future performance and

business. These statements may include, without limitation, any statements preceded by, followed by or including words such as “aim,” “anticipate,” “believe,” “can have,” “could,”

“estimate,” “expect,” “intend,” “likely,” “may,” “plan,” “project,” “should,” “target,” “will,” “would” and other words and terms of similar meaning or the negative thereof. Such forward-looking

statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or

achievements to be materially different from the expected results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements

are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which it will operate in the future. You acknowledge that

circumstances may change and the contents of this Presentation may become outdated as a result.

The information contained in this Presentation should be considered in the context of the circumstances prevailing at the time and will not be updated to reflect material developments that

may occur after the date of this Presentation. The information and opinions in this Presentation are provided as at the date of this Presentation and are subject to change without notice.

None of the Company, any member of the Group, any of their respective affiliates, advisors or representatives or any other person shall have any liability whatsoever (in negligence or

otherwise) for any loss howsoever arising from any use of this Presentation or its contents or otherwise arising in connection with this Presentation, or any action taken by you or any of

your officers, employees, agents or associates on the basis of the information in this Presentation.

This Presentation is not for publication, release or distribution in any jurisdiction where to do so would constitute a violation of the relevant laws of such jurisdiction nor should it be taken or

transmitted into such jurisdiction.

2

Presenters

James Corcoran

CEO

Paul Sheriff

CFO

3

Agenda / Contents

1 Key highlights

2 Business performance

3 Financial results

4 Q&A

5 Appendix

4

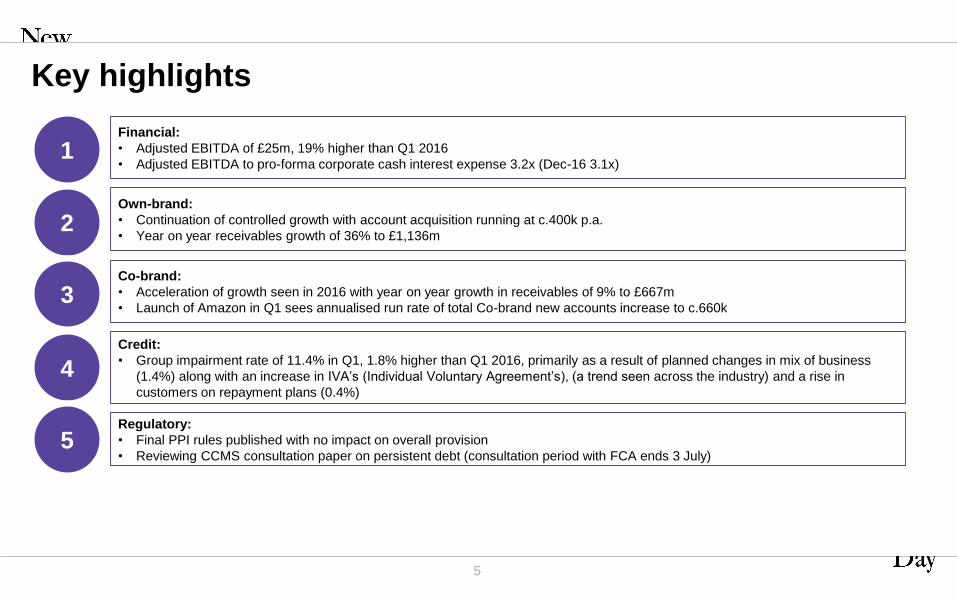

Key highlights

1

2

4

Financial:

• Adjusted EBITDA of £25m, 19% higher than Q1 2016

• Adjusted EBITDA to pro-forma corporate cash interest expense 3.2x (Dec-16 3.1x)

Own-brand:

• Continuation of controlled growth with account acquisition running at c.400k p.a.

• Year on year receivables growth of 36% to £1,136m

Credit:

• Group impairment rate of 11.4% in Q1, 1.8% higher than Q1 2016, primarily as a result of planned changes in mix of business

(1.4%) along with an increase in IVA’s (Individual Voluntary Agreement’s), (a trend seen across the industry) and a rise in

customers on repayment plans (0.4%)

3Co-brand:

• Acceleration of growth seen in 2016 with year on year growth in receivables of 9% to £667m

• Launch of Amazon in Q1 sees annualised run rate of total Co-brand new accounts increase to c.660k

5

5Regulatory:

• Final PPI rules published with no impact on overall provision

• Reviewing CCMS consultation paper on persistent debt (consultation period with FCA ends 3 July)

New accounts origination Growing average balances Receivables growth

Risk-adjusted margin Risk-adjusted income

341 389 398

682 632 629

1,023 1,021 1,027

2015 2016 Q1 2017 LTM

(‘000)

Own-brand Co-brand

1,1611,287 1,279

363 397 417

Mar-16 Dec-16 Mar-17

(£)

Own-brand Co-brand

8351,093 1,136

614

722 6671,449

1,815 1,803

Mar-16 Dec-16 Mar-17

(£m)

Own-brand Co-brand

94137 140

113

119 122

207

256 262

2015 2016 Q1 2017 LTM

(£m)

Own-brand Co-brand

14.6% 14.9% 14.1%

16.7%18.4% 18.7%

2015 2016 Q1 2017 LTM

Own-brand Co-brand

6

Stable new accounts origination and maturing average balances

providing RAI growth

Income growth underpinned by strong margins

Own-brand: Continued controlled growth and stable margins provide

growing returns

603

936

660

986

184

157

175

150

787

1,093

835

1,136

Dec-15 Dec-16 Mar-16 Mar-17

Open book Closed book

Gross receivables (£m)

277 273 276

64 116 122

341389 398

2015 2016 Q1 2017 LTM

aqua marbles

Strong organic growth

Risk-adjusted income (£m) Risk-adjusted margin

11.7% 12.6% 12.3%

20.9%25.2% 25.2%

2015 2016 Q1 2017 LTM

Open book Closed book

53

95 99

41

42 4194

137 140

2015 2016 Q1 2017 LTM

Open book Closed book

New accounts (‘000)

Own-brand key highlights

Current run rate c.400k new accounts per annum

Receivables growth of £301m in the 12 months to March 2017,

driven by the open book

Risk adjusted income of £33m in Q1 in 2017, LTM of £140m

Risk-adjusted margin on the open book has dropped 0.3% to

12.3% for the 12 months to March 2017, due to higher

impairment rates

Expansion of healthcheck campaigns, helping to educate

customers on financial wellbeing

• For the 12 months to March 2017, 63% of customers

received a credit line increase

• For the 12 months to March 2017, 58% of reprices were

downwards

7

Co-brand: Improving margins combined with growth of new retailers

Open book growth (gross receivables in £m)

630 693569 641

5429

45 26

684 722

614 667

Dec-15 Dec-16 Mar-16 Mar-17

Open book Closed book

96.1%92.7%

Successful integration delivering improved profitability

Risk-adjusted income (£m) Risk-adjusted margin

105 113 116

8 6 6113 119 122

2015 2016 2017 Q1 LTM

Open book Closed book

17.7% 18.6% 18.8%

2015 2016 2017 Q1 LTM

Open book

% Open book

96.0%92.1%

Co-brand key highlights

Open book receivables returned to growth during 2016, with

£72m growth in the 12 months to March 2017

Improving RAM reflecting continued strong underwriting and

growth of good credit risk revolving balances

Risk-adjusted income of £33m in Q1 2017, LTM £122m

Step change growth in online account bookings in Q1 (c.3x

growth in new online account bookings)

Following the launch of TUI in Q4 2016, Amazon launched in Q1

2017 with Q2 already seeing accelerated growth and additional

Amazon products due in H2

8

Servicing / average receivables

Consistent improvement in servicing efficiency

Income growth exceeds costs growth

Operating highlights

Continued focus on efficiency and further execution of cost

saving initiatives

Income is growing approximately three times faster than costs,

leveraging the scalable nature of the business

Continued investment in improved functionality and customer

service

Customer satisfaction remains very strong with transactional

NPS scores at +65

9

Improved cost income ratio leveraging stable cost base

4.9%4.7% 4.6%

2015 2016 2017 Q1 LTM

321

412 435

136 161 164

2015 2016 2017 Q1 LTMIncome Costs

1.9%

42.4%

39.0%

37.7%

2015 2016 Q1 2017 LTM

Improving cost income ratio

£m 2016 Q1 2017 Q1 2016ALTM

Mar-17

Interest income 91 113 392 416

Cost of funds (7) (9) (30) (33)

Fee income 11 14 50 52

Total income 95 118 412 435

Total impairment (35) (52) (156) (173)

Risk-adjusted income 60 66 256 262

Servicing costs and collection fees (17) (20) (67) (69)

Investment costs (11) (11) (52) (53)

Underlying contribution 32 35 137 140

Salaries, benefits & overheads (11) (11) (42) (42)

Depreciation & amortisation - 1 1 2

Adjusted EBITDA 21 25 96 100

Average gross receivables 1,455 1,814 1,567 1,649

Gross interest and fee yield (%) 28.0 28.0 28.2 28.4

Cost of funds (%) 2.4% 2.5% 2.4% 2.5%

Pro-forma net corporate senior

secured debt to adjusted EBITDA 4.2x 3.1x 3.1x 3.1xAdjusted EBITDA to pro-forma

corporate cash interest expense(a) 2.5x 3.2x 3.1x 3.2x

Underlying cost to income ratio improving

EBITDA interest cover

Growing adjusted EBITDAHistorical performance illustrates growth potential

(a) Proforma adjustment for the full year interest expense on the senior secured bond10

Group income statement

96 100

21 25

2016A LTM Mar-17

2016 Q1 2017 Q1

3.1x 3.2x

2.5x

3.2x

2016A LTM Mar-17

2016 Q1 2017 Q1

39.0% 37.7%41.1%

36.0%

2016A LTM Mar-17

2016 Q1 2017 Q1

(a) Working capital includes other assets, restricted cash, other provisions and other liabilities

(b) Exceptional costs in 2017 relate to the transaction fees associated with the acquisition by funds advised by

Cinven and CVC in January 2017. These costs have been excluded from the adjusted LTM numbers above

Working capital movements are predominantly driven by:

o Changes in restricted cash balances as the Group’s funding

structure has developed

o Changes in operational settlement accounts

Growth in receivables funded by drawdowns under financing

facilities as well as internal cash flow generation

Q1 2017 saw a number of expected costs associated with the

acquisition by funds advised by Cinven and CVC together with

costs related to raising the senior secured bond

In addition to free cash flow available for debt service, there was

undrawn capacity under the VFN of £547m at Mar-17 to provide

further liquidity, of which £33m was available but had not been

drawn down as at 31 March 2017 (£5m was available at 31

December 2016)

The reduction in net financing cash flow is mainly driven by the

slight deleveraging at the portfolio level as a result of the

increased undrawn capacity on the VFNs

CommentsSummary cash flow statement

11

Group cash flow

£m 2016 2017 Mar-LTM2017 Mar-LTM

Adjusted(b)

Adjusted EBITDA 96 100 100

Impairment provision build 20 27 27

Adjusted EBITDA excluding change in

impairment provision116 127 127

Change in working capital(a) (7) (18) (18)

PPI and CCA provision utilisation (12) (12) (12)

Capex (5) (9) (9)

Tax paid (1) (2) (2)

Exceptional costs(b) (4) (14) (5)

FCF available for growth and debt

service87 72 81

(Increase) in gross receivables (364) (377) (377)

Net financing cash flow (ABS) 392 354 354

Undrawn liquidity available from VFN 5 33 33

Fully leveraged FCF available for debt

service120 82 91

Highlights

Pro-forma LTM net corporate senior secured debt to adjusted

EBITDA 3.1x (Dec-16 3.1x). Adjusting for undrawn available

liquidity from the VFN, this ratio would be 2.8x (Dec 16 3.0x)

Continued strong cash generation as a result of operating

performance and stable funding

A number of exceptional cash flow items associated with the

acquisition and bond issuance

Deleveraging through cash and profit growth

12

Strong cash flow generation leading to continued de-leveraging

£m 20162017 Mar-

LTM

Fully leveraged FCF available for debt service 120 82

Equity raised for acquisition bonus net of payments - 5

Net cash proceeds from senior secured debt - 412

Funding received via shareholder loans - 594

Purchase of LuxCo - (990)

Distributions (60) (60)

Net increase in unrestricted cash (fully leveraged) 60 43

£m31-Dec 31-Mar

2016 2017

Proforma senior secured debt 425 425

Unrestricted cash (129) (114)

Pro-forma net corporate senior secured debt 296 311

Pro-forma net corporate senior secured debt to adjusted

EBITDA ratio3.1x 3.1x

Undrawn liquidity available from VFN 5 33

Adjusted proforma net corporate senior secured debt to

adjusted EBITDA ratio3.0x 2.8x

Cost of funds

300 300

565

250

175

550 60475

850

625

250

2017 2018 2019 2020

Issued bonds VFN

(£m)

Key funding highlights

Cost of funds remains stable at 2.5% for Q1 2017 (LTM 2.5%)

Debt profile, excluding senior secured notes, remains unchanged

Plans being executed for 2017 funding

Debt maturity profile (a) (excl. senior secured notes)

13

Unchanged debt maturity and stable cost of funding

(a) Debt maturity profile above relates to total capacity under VFNs and total face value of issued bonds

including amounts retained by NewDay

83% 81%

2.7% 2.7%

Dec-2016 Mar-2017

Own-brand

Advance Rate Cost of funds

91% 90%

1.9% 1.8%

Dec-2016 Mar-2017

Co-brand

Advance Rate Cost of funds

Breakdown in group impairment movementKey credit drivers

Group impairment increases driven by mix of the portfolio and in

line with plan

The proportion of the Group comprising of Own-brand

receivables, which attracts a higher impairment rate than

Co-brand, has increased to 63% (Mar-16: 58%)

As the Own-brand closed portfolio runs off the open

books comprises a larger part of the total and attracts a

higher impairment rate. Open book made up 87% of the

total Own-brand book (Mar-16: 79%)

Increase in IVA’s, as seen across the industry, have increased

charge off rates together with an increase in customers on

repayment plans

Industry data shows a YoY increase of 35% in IVA’s in Q1 2017

from Q1 2016

Continued focus on underwriting and collections

14

Group impairment rate has increased by 1.8 ppts, driven by portfolio mix

9.6%11.4%

0.7%0.7%

0.4%

Q1'16 Own-brand /Co-brand mix

Own-brand -Open /

Closed mix

Underlyingperformance

Q1'17

15

Excess spread (rolling 3-month average)(a) Commentary

Significant excess spread provides cushion against an increase in

charge off rates, a decrease in yield and / or an increase in LIBOR

We monitor the excess spread and all other triggers and can

deploy multiple operational levers (for example, adjusting portfolio

growth or repricing)

Tick up in Own-brand charge offs consistent with our impairment

performance

Slight reduction in Co-brand charge off rate

Gross annualised charge-off rate

(a) Excludes the VFNs from the Master Trusts and the secondary funding facilities as they are not directly comparable. The VFNs are revolving in nature and the inter-month drawings on those notes would impact calculations of

excess spread, which are based on month-end balances. The excess spread for the following series, as calculated in April 2017 for the rolling 3-month period, are: NewDay Funding Secondary Funding Facility Senior VFN –

16.66%; NewDay Funding Partnership Master Trust, Series 2014-VFN – 18.74%; and NewDay Funding Master Trust, Series 2015-VFN – 14.03%.

Source: ABS Investor Reports available on NewDay website as of April-2017

Report Date

Report Date

Significant and consistent excess spread and stable loss performance

0%

5%

10%

15%

20%

25%

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

ND Funding | Series 2015 - 1 ND Partnership | Series 2014 - 1ND Funding | Series 2015 - 2 ND Partnership | Series 2015 - 1ND Funding | Series 2016 - 1

0%

5%

10%

15%

20%

25%

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

ND Funding ND Partnership

Q&A

Appendix

Underlying earnings adjustments

Other costs: primarily consist of a £19m increase in PPI provision taken

in 2016, reflecting expected increased claim rates across the industry

following the proposals for the new rules and guidelines relating to PPI

complaints handling set out in the FCA’s consultation paper “CP16/20:

Rules and guidance on payment protection insurance complaints:

feedback on CP15/39 and further consultation” issued in August 2016

All colleague acquisition bonus: reflecting a bonus paid to colleagues

relating to the recent acquisition

Exceptional costs: relating to the transaction fees associated with the

acquisition by Cinven and CVC in January 2017.

Amortisation: reflects the amortisation of the intangible assets

recognised on the acquisition by Cinven and CVC in January 2017

Interest on shareholder loans: reflects the interest cost of 12% on the

shareholder loan of £594m, issued as part of the acquisition by Cinven

and CVC on 26 January 2017

Fair value unwind: reflects the amortisation of a fair value adjustment

on the Group’s acquired portfolios

Key descriptions

18

Underlying earnings

(a) Note that the statutory loss before tax of £(18m) in 2017 Q1 is on a segmental basis as disclosed in the quarterly

consolidated financial information. Statutory loss before tax on the face of the income statement is £(28m) (£(32)m after tax)

reflecting the period from 27th January to 31st March 2017 only. All numbers in this presentation reflect results from 1st

January to 31st March on a proforma basis

£m 2016Mar 2017-

LTM2017 Q1 (a)

Adjusted EBITDA 96 100 25

Other costs (18) (19) (1)

All colleague acquisition bonus (9) (10) (1)

Exceptional costs - (11) (11)

Total non-recurring costs (27) (40) (13)

Depreciation and amortisation including

amortisation of acquisition intangibles(1) (11) (10)

Senior secured debt interest and

related costs- (7) (7)

Interest on shareholder loans - (13) (13)

Fair value unwind 5 4 -

Statutory PBT 73 33 (18)

Taxation (1) (5) (3)

Statutory PAT 72 28 (21)

£m 2016 Q1 2017 Q1 2016ALTM

Mar-17

Interest income(a) 57 77 262 281

Cost of funds (4) (6) (19) (21)

Fee income 7 10 31 34

Total income 60 81 274 294

Total impairment (29) (48) (137) (154)

Risk-adjusted income 31 33 137 140

Servicing costs and collection

fees(6) (8) (22) (24)

Investment costs (3) (4) (16) (17)

Underlying contribution 22 21 99 99

Average gross receivables 811 1,114 920 994

Gross interest and fee yield (%) 31.6 31.2 31.9 31.7

Impairment rate (%) 14.3 17.2 14.9 15.5

RAM (%) 15.3 11.8 14.9 14.1

£m 2016 Q1 2017 Q1 2016ALTM

Mar-17

Interest income(a) 34 36 132 135

Cost of funds (3) (3) (11) (11)

Fee income 4 4 18 18

Total income 35 37 139 142

Total impairment (6) (4) (20) (20)

Risk-adjusted income 29 33 119 122

Servicing costs and collection

fees(10) (12) (42) (42)

Investment costs (8) (7) (36) (36)

Underlying contribution 11 14 41 44

Average gross receivables 645 690 647 658

Gross interest and fee yield (%) 23.6 23.2 23.2 23.3

Impairment rate (%) 3.7 2.3 3.1 3.0

RAM (%) 18.0 19.1 18.4 18.5

Co-brand income statementOwn-brand income statement

(a) Excludes fair value unwind19

Underlying earnings by segment

Increase in receivables driven primarily by growth of the Own-

brand open book

Conservative provisioning with impairment coverage increasing

from 5.4% of gross receivables in March 2016 to 6.5% in March

2017

Fair value of total assets following the acquisition introduced

£396m of intangibles, primarily relating to the customer and

retailer relationships, the brand, trade names and intellectual

property

Evolution of gross receivables (£m)Summary balance sheet

Key highlights

20

Group balance sheet

£m Mar-16 Dec-16 Mar-17

Gross receivables 1,449 1,815 1,804

Bad debt provisions (90) (105) (117)

Other 30 50 57

Net receivables 1,389 1,760 1,744

Restricted cash 33 40 40

Unrestricted cash 105 129 114

Intangibles - 4 392

Goodwill - - 275

Other assets 37 74 54

Total assets 1,564 2,007 2,619

Asset-backed bonds 976 1,279 1,265

Wholesale funding 187 290 235

Senior bonds - - 431

PPI provision 47 56 54

Other provisions 6 12 5

Other liabilities(a) 52 71 53

Shareholder loans - - 607

Total liabilities 1,268 1,708 2,650

Shareholders' equity 296 299 (32)

Total liabilities and equity 1,564 2,007 2,619

42%60% 63%

58%

40% 37%

1,449

1,815 1,804

Mar-16 Dec-16 Mar-17

Own-brand Co-brand

(a) Other liabilities includes capitalised debt funding fees

Regulation – Credit Card Market Study (CCMS)

Persistent Debt Unsolicited Credit Line Increases (UCLIs)

• FCA Consultation Paper (4th April) includes a new Persistent Debt definition and a new outlined “escalating intervention” strategy targeted at these customers; industry consultation period ends 3 July.

• Definition:– Payments of interest, fees & charges exceed repayment of

principal over 18 months, & the outstanding balance is continually > £200

• Outlined Strategy (assumed to be effective from March 2018 (Day 1))

– Month 18: Stand-alone prompt communication required

– Month 27: Follow-up stand-alone communication required(including harder prompts and CRA flag note)

– Month 36: Paydown plan engagement needed with customers with 3 possible outcomes dependent upon customer affordability and engagement, ranging from collections activity to full card suspension

• The definition seems straight-forward but already is subject to multiple questions/challenges within UKCA – e.g. what fees should be included (default, service, annual), is the £200 threshold a continuous assessment or on-off, how should closed/paying down accounts be treated?

Next Steps/Impacts

• We will continue to actively engage in UKCA (United Kingdom Cards Association) dialogue within the consultation period, lobbying as appropriate to support outcomes in line with our NewDay Manifesto. We will monitor the situation and develop our analysis but we believe we have a range of options to drive improved customer outcomes and reduce the proportion of customers triggering Persistent Debt definitions.

• FCA Consultation Paper (4th April) has firmed up expected views.

• Within the outlined strategy an “Opt in” customer is one who needs to call within the CLI notice period in order for it to be actioned, an “Opt out” customer is one where the CLI is automatically actioned unless the customer calls in (as today).

• Outlined Strategy:– New customers: Provided with “Opt in” choice– Existing customers: “Opt in” opportunity made visible within comms– Rule 1: <110% payment ratio 7/8 months – move to “Opt in”– Rule 2: <110% payment ratio 13/14 months – exclude from CLIs– Rule 3: TBC: potential for high utilisation overlays to be applied

Next Steps/Impacts

• We will monitor the situation and develop our analysis but we believe there will be limited impacted from the potential changes. Once requirements are confirmed we can integrate delivery into our digital & front-end transformation roadmaps.

Information Remedies (agreed pre-Consultation Paper)

• New mandatory remedies industry has agreed to implement. Implementation progress being tracked by Lending Standards Board.– Promo expiry alert (final deadline – Mar-18)– Payment day choice (final deadline – Mar-18)– Credit limit proximity alert (final deadline – Jun-18)

Next Steps/Impacts

• We remain on track to deliver these within agreed FCA deadlines, and do not consider that they will have a commercial impact. They are in line with initiatives we have already delivered ourselves to support better customer outcomes and are directly in line with our NewDay Manifesto values.

21

NewDay Group Holdings

S.à r.l. (Lux)

NewDay Ltd

(UK)

NewDay Reserve

Funding Ltd (UK)

NewDay Partnership

Funding 2014-1 Plc (UK)NewDay Partnership

Funding 2015-1 Plc (UK)NewDay Funding 2015-1

Plc (UK)

NewDay Funding 2015-2

Plc (UK)

NewDay Cards Ltd

(UK)

Invicta Card Services

Limited (UK) (dormant)

NewDay Loyalty Ltd

(UK)

Progressive Credit

Limited (UK) (dormant)

SAV Credit Limited (UK)

(dormant)

NewDay Group Ltd

(UK)

NewDay Holdings

Ltd (UK)NewDay Partnership Transferor Plc (UK)

Structured Finance

Management Offshore

Limited (Jersey)

NewDay Funding Loan Note Issuer Ltd (UK)

NewDay Partnership

Securitisation Holdings Ltd (UK)

NewDay Partnership Loan Note Issuer Ltd (UK)

SFM Corporate Services

Limited (UK)

NewDay Funding

Transferor Ltd (UK)

TMF Trustee Limited

(UK)

NewDay Partnership

Secondary Funding Ltd

(UK)

NewDay Partnership

Receivables Trustee Ltd

(Jersey)

NewDay Funding

Receivables Trustee Ltd

(Jersey)

NewDay Group Structure Chart

NewDay Funding Securitisation

Holdings Ltd (UK)

Crestbridge Corporate

Trustees Limited

(Jersey)

Key

Group company

Orphan special purpose vehicles (not a group company)

Corporate services provider (not a group company)

NewDay Group (Jersey)

Limited

(Jersey)

NewDay BondCo Plc

(UK)

NewDay Group UK

Limited (UK)

NewDay UK Limited

(UK)

100%

100%

100%

100%

NewDay Funding 2016-1

Plc (UK)

CO-BRAND FUNDING STRUCTURE

100% 100%

100% (on

trust)

100% (on

trust)

100% (on trust) 100% (on trust)

100% (on trust)

100% 100%100%100%100%

100% (on trust)

OWN-BRAND FUNDING STRUCTURE

100%

TMF Trustee Limited

(UK)

NewDay Secondary

Funding Limited (UK)

NewDay UPL

Transferor Ltd

(UK)

100%

100%

100%

22