new york geneva miami annual report...

TRANSCRIPT

New York Geneva Miami

www.elizabetharden.com Annual Report 2007

88724_Cov:Layout 1 10/1/07 5:19 PM Page 1

The new fragrance

Catherine Zeta-Jones ©

Eliz

abet

h A

rden

, Inc

.

Corporate Offices2400 S.W. 145 AvenueMiramar, Florida 33027954-364-6900

200 Park Avenue SouthNew York, New York 10003212-261-1000

200 First Stamford PlaceStamford, Connecticut 06902203-462-5700

28, chemin de Joinville1216 Cointrin-Geneva41-22-791-8711

Investor RelationsFor investor information, including filings with the Securities and Exchange Commission and other financial literature, please visit our website at www.elizabetharden.com or write to us at:

Elizabeth Arden, Inc. Investor Relations200 Park Avenue SouthNew York, NY 10003

Transfer Agent and RegistrarAmerican Stock Transfer and Trust Company59 Maiden LaneNew York, New York 10038800-937-5449

Independent RegisteredPublic Accounting FirmPricewaterhouseCoopers LLP300 Madison AvenueNew York, New York 10017

Common Stock InformationOur common stock is traded on the NASDAQ Global Select Market under the symbol “RDEN.”

Annual MeetingOur annual meeting of shareholders will be held onNovember 14, 2007 at 10:00 a.m., local time, at our executive offices located at 2400 S.W. 145 Avenue, Miramar, Florida 33027.

CORPORATE AND INVESTOR INFORMATION

E. Scott BeattieChairman, President

and Chief Executive OfficerElizabeth Arden, Inc.

Fred BerensManaging Director - InvestmentsWachovia Securities, Inc.

Maura J. Clark(1,3)

PresidentCommercial and Industrial EnergyDirect Energy Services, LLC

Richard C.W. MauranPrivate Investor

William M. Tatham(1,2)

Chairman and Chief Executive OfficerNexJ Systems, Inc.

J.W. Nevil Thomas(2,3)

President and Chief Executive Officer Nevcorp

Paul WestVice ChairmanElizabeth Arden, Inc.

D i r e c t o r s

Desig

ned

and

prod

uced

by R

R Do

nnell

ey F

inanc

ial, M

iami, F

lorida

(1) Audit Committee Member(2) Compensation Committee Member(3) Nominating and Corporate Governance Committee Member

(1)Chairperson (2)Chairperson

(3)Chairperson

Elizabeth Arden brands featured on our cover.

1st Row: Danielle by Danielle Steel, Nanette Lepore, M by Mariah Carey, Britney Spears believe, Lulu Guinness, Jewel Alfred Sung

2nd Row: Elizabeth Arden Red Door, PREVAGE®, Ceramide Gold UltraRestorative Capsules, Eight HourCream, Elizabeth Arden Intervene,Elizabeth Arden green tea

3rd Row: with Love... Hilary Duff, BadgleyMischka Fleurs de Nuit, Elizabeth Taylor’s White Diamonds, Wings, fantasy Britney Spears, GANT Adventure

4th Row: HUMMER®, GANT Liquid, Halston Z-14, Daytona 500®,Elizabeth Arden 5th Avenue after five, White Shoulders

5th Row: Elizabeth Arden Provocative Woman,Sunflowers, curious Britney Spears,PS®, Giorgio Beverly Hills, Grey Flannel

88724_Cov:Layout 1 9/28/07 3:30 PM Page 2

1

F I N A N C I A L H I G H L I G H T S

Net sales

Gross profit

Net income, as reported

Net income, as adjusted

Diluted earnings (loss) per commonshare, as reported

Diluted earnings per commonshare, as adjusted

Shareholders’ equity

EBITDA, as reported(g)

EBITDA, as adjusted(g)

$1,127,476

461,319

37,334

39,078(b)

$ 1.30

1.36(b)

$ 320,927

$ 98,524

100,618(b)

$ 920,538

411,364

37,604

39,072(d)

$ 1.25

1.30(d)

$ 259,200

$ 100,038

102,194(d)

$ 954,550

404,072

32,794

34,231(c)

$ 1.10

1.15(c)

$ 277,847

$ 89,608

91,539(c)

$ 832,003

349,200

2,928

27,922(e)

$ (1.66)

1.01(e)

$ 202,060

$ 51,358

93,702(e)

$ 746,142

304,278

9,987

9,863(f)

$ 0.35

0.34(f)

$ 98,989

$ 81,907

81,733(f)

Pro forma twelve months ended(a)in thousands, except per share data

(a) On June 2, 2004, the Company’s Board of Directors approved a fiscal year-end change from January 31 to June 30. The pro forma presentation reflects the unauditedconsolidated selected financial data for the equivalent prior-year periods based on the new fiscal year end, consistent with the presentation on our corporate website.

(b) Adjusted to exclude restructuring charges of $2.1 million.

(c) Adjusted to exclude debt extinguishment charges associated with long-term debt redemption and restructuring charges of $0.8 million and $1.2 million, respectively.

(d) Adjusted to exclude impairment charge related to the then anticipated sale of the Miami Lakes facility of $2.2 million.

(e) Adjusted to exclude debt extinguishment charges associated with long-term debt redemption and corporate restructuring charges of $38.8 million and $3.5 million, respectively, and the accelerated accretion on converted preferred stock.

(f) Adjusted to exclude debt extinguishment gain associated with long-term debt redemption of $0.2 million.

(g) EBITDA is defined as net income plus the provision for income taxes, plus interest expense, plus depreciation and amortization.

Fiscal year endedJune 30, 2007

(Audited)June 30, 2004

(Unaudited)June 28, 2003

(Unaudited)June 30, 2005

(Audited)

Fiscal year ended

NET SALES EPS

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07

June 30, 2006(Audited)

For additional detail and information, including a discussion of EBITDA, please refer to Part II, Item 6, Selected Financial Data in our Annual Report on Form 10-K, which is included in this Annual Report. Also, the fiscal years ended June 30, 2006 and June 30, 2007 reflect share-based payment expenses resulting from the applicationof SFAS 123R, which we adopted on July 1, 2005 for the year ended June 30, 2006 and subsequent periods.

*

* Diluted earnings per common share, as adjusted.

88724_8pgr:Layout 1 10/2/07 5:53 PM Page 2

2

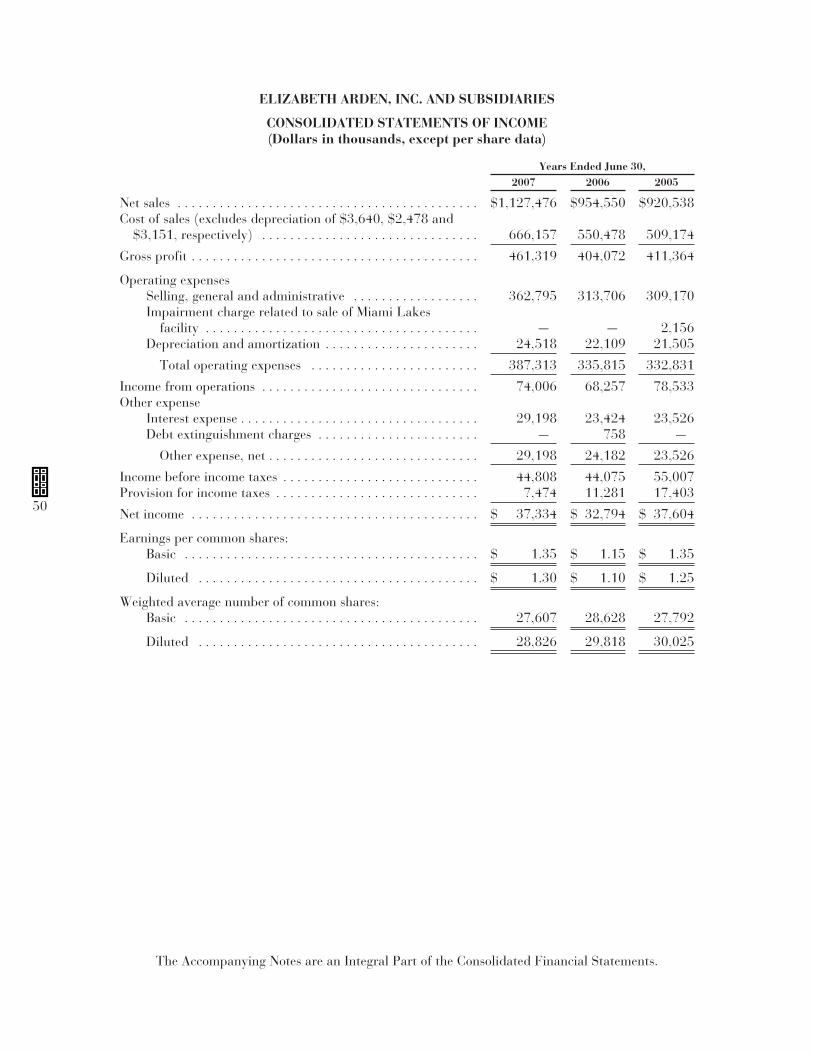

iscal 2007 marked the achievement of a major milestone for Elizabeth Arden as we topped the $1 billion mark in net sales. Total net sales increased by18.1% to a record $1.127 billion, and our reported earnings per diluted

share grew a healthy 18.2% to $1.30 from $1.10.

Our record sales and strong earnings growth reflectthe strength of our multi-dimensional business model.Our business performed well across all facets:geography, tiers of distribution and brand portfolio.In particular, our North America fragrances andInternational businesses contributed strongly to our results, as did our Elizabeth Arden-branded skin care and color cosmetics products. Theseresults were fueled in part by the successful inte-gration of two strategic acquisitions this past year,continued successful innovation in our productofferings and further expansion and developmentof our International markets.

Net Sales of North America Fragrances Business Grew by 23%

The growth of our North America fragrances business was led by the introduction of new ownedbrands and brands that we distribute on behalf ofour beauty partners. During this fiscal year, we integrated both the Riviera Concepts and SovereignSales acquisitions into our business, allowing us tosell to new prestige retailers, expand our productofferings and programs and increase our marketshare. We increased sales with virtually every oneof our key U.S. mass retail customers in fiscal 2007.Our unique ability to create differentiated productofferings in multiple tiers of distribution allows us tocreate additional sales opportunities for our brandsand offer a healthy pipeline of new products to allour North America fragrance retailers.

FE

li

za

be

th

A

rd

en

A

nn

ua

l

Re

po

rt

2

00

7

D E A R F E L L O WS H A R E H O L D E R S :

F

88724_8pgr:Layout 1 9/28/07 2:48 PM Page 3

3

This fiscal year we introduced an unprecedentednumber of fragrances to our mass and mid-tierretail customers, including brands that we own suchas fantasy Britney Spears (which became the numberone new fragrance launch at mass retailers duringcalendar 2006), with Love…Hilary Duff and Danielleby Danielle Steel, as well as fragrance brands we dis-tribute on behalf of other beauty companies. Afterlaunching Danielle by Danielle Steel at U.S. prestigedepartment stores in the fall of 2006, this fragrancewas introduced to additional retailers where itbecame the leading women’s fragrance brand during Mother’s Day 2007 at Kohl’s, JCPenney and Sears, underscoring the strength of our multi-channel distribution model.

Our Britney Spears fragrances, which representedjust under 10% of our net sales in fiscal 2007, continued to perform well and helped drive ourmass retail business. Retail sales of Britney Spearsfragrances were up double digits at mass retailers in the second half of fiscal 2007. Britney Spears fragrances, including fantasy Britney Spears and curious Britney Spears (representing two of the topten launches at U.S. prestige department stores for calender years 2004-2006*), are sold acrossmultiple outlets worldwide. Approximately half of the sales of Britney Spears fragrances in fiscal 2007 occurred outside the U.S. Based on the success of these fragrances and the mostrecent addition to the Britney Spears franchise, midnight fantasy, we believe there continues to be good demand around the world for these fragrances. We are excited about the newestBritney Spears fragrance, Britney Spears believe,which we are introducing in the fall of 2007 in the U.S. and internationally in the spring of 2008.

International Net Sales Increased by 12%

Our International business, which representedapproximately 35% of our net sales in fiscal 2007,also continued its positive performance with strong sales increases in our Asia Pacific and TravelRetail markets and continued solid growth in othermarkets, including Latin America and the Middle East. In January 2007 we opened an office in Dubai,which is serving as our headquarters for ourMiddle East business, where we are experiencingrapid growth in the demand for our products.

As we mentioned last year, we acquired our distrib-utor’s business in China and Taiwan and establishedaffiliates in those markets. These two affiliatestogether with our business in Hong Kong are nowbeing managed as one integrated Greater Chinabusiness from our headquarters in Shanghai.Revenues in Greater China doubled this year, andwe currently expect revenues from this market togrow by another 50% in fiscal 2008.

In China and other developing markets such asIndia and Brazil, where beauty represents an aspira-tional luxury, we are seeing tremendous potential for our brands and are implementing initiatives toexploit these opportunities. In Brazil, for example,we will be implementing a strategy to engage inlocal partnerships and production. This will allow us to make our products more affordable for thelocal consumer and to better service the emergingdemand in this rapidly developing market.

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07

*Source: NPD.

Elizabeth Arden counter in Shanghai

PREVAGE® billboard - China

88724_8pgr:Layout 1 9/28/07 2:48 PM Page 4

Our Travel Retail business has been particularly suc-cessful, with our retail sales growth outpacing thecategory for the past two calendar years. In fact,we are one of a few companies to have increasedour market share in Travel Retail for the past fouryears. Travel Retail outlets represent an ideal shoppingvenue in markets where the retail infrastructure is less developed, such as China, India and LatinAmerica. We benefited in that sector from the success of our licensed brands, such as the BritneySpears and Hilary Duff fragrances, and are particularlypleased by the sales growth of our Elizabeth Arden-branded products, which outpaced the growth ofthe category for the 2006 calendar year. The mostnotable successes included the new PREVAGE®

Eye Anti-Aging Moisturizing Treatment, the continuedsuccess of PREVAGE® Anti-Aging Treatment, whichlaunched in Travel Retail in fiscal 2006, and othercore Elizabeth Arden-branded products, includingEight Hour Cream, Elizabeth Arden Ceramide andElizabeth Arden green tea fragrances.

Net Sales of Elizabeth Arden Skin Care andColor Cosmetics Products Grew by 16%

The Elizabeth Arden brand is key to the strength of our business. We believe that the ElizabethArden brand, which represented nearly $500 mil-lion in net sales in fiscal 2007, is one of the mostrecognized names in beauty globally and has significantgrowth potential. In fiscal 2007, over 60% of thenet sales of Elizabeth Arden-branded products weremade outside the U.S., and we believe there aretremendous opportunities for the growth of thisbrand internationally, particularly in developing markets. Our objective is to elevate the ElizabethArden brand to one that the world recognizes not only as a beauty icon, but as a progressive and innovative brand that continues to maintain relevance with today’s global consumer.

In fiscal 2007, we made tremendous progress infocusing our Elizabeth Arden skin care and colorbusiness on three core skin care lead franchises:Ceramide, our established corrective anti-aging skincare line targeted to women who are 40 and over; Intervene, our pre-emptive anti-aging skin careregime targeted to the 30 to 50 year old whodesires to fight the signs of aging; and PREVAGE®

Anti-Aging Treatment, our premium cosmeceuticalproduct, which is the perfect complement to bothCeramide andIntervene. EightHour Cream, ourall-purpose skincare brand, has a long heritagedating back to the 1930’s. It wasone of the firstbrands ever creat-ed by ElizabethArden herself and still commandssignificant brandloyalty today. By aligning our cos-metic productswith these distinctpillars and rationalizing all of our product offeringsthat cannot be categorized within these franchises, we have simplified our offerings for both consumersand the beauty consultants selling our products.

Award-winning PREVAGE® Anti-Aging Treatmenthas significantly affected the Elizabeth Arden brandsince its November 2005 introduction. PREVAGE®

has elevated the Elizabeth Arden brand image and market share, improved beauty counter productivity,and provided entry into luxury channels of distribu-tion and new markets. Sales of PREVAGE® productsincreased by 45% in fiscal 2007, with 60% of salesoccurring outside the U.S. Given the success ofPREVAGE® in various markets around the world, we believe the potential for this brand is consi-derable. For example, in its first year, PREVAGE®

became the #1 cosmeceutical brand across theAsia-Pacific Travel Retail market. It continues to win numerous awards around the world as well,including most recently the award for highestgrowth for a beauty product in Mexico, the Prix De Marie Claire award in Australia, the Best New

4

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07

Elizabeth Arden displays - Dubai

88724_8pgr:Layout 1 10/2/07 5:25 PM Page 5

Product Award for Prestige Skin Care in Canada and the best campaign in the luxury goods and fashion category at the Media and Marketing pan-European Media Awards.

We believe the strength of PREVAGE®, coupledwith the quality of our innovation, will allow us tocapture additional market share for the ElizabethArden brand globally.

Notable skin care and color products that are beingintroduced in fiscal 2008 include Ceramide GoldUltra Restorative Capsules, PREVAGE® Anti-Aging NightCream, a Limited Edition Eight Hour Cream, a foundationto complement the newly launched Intervene skincare line and a whitening skin care treatment prod-uct, Elizabeth Arden White Glove, targeted for Asia.

The Breadth of our Prestige FragrancePortfolio is a Continued Source of Strength

Our diverse fragrance brand portfolio is a signifi-cant asset to our business. Net sales of fragrancesincreased by approximately 20% globally in fiscal 2007. We classify this expansive portfolio of fragrance brands into the following categories:the Elizabeth Arden-branded fragrances, including

Elizabeth Arden Red Door, Elizabeth Arden 5th Avenue,Elizabeth Arden green tea and our most recentlaunch, Elizabeth Arden Mediterranean, all of which are promoted by our beautiful and elegantcorporate spokesperson, Catherine Zeta-Jones;celebrity fragrances, including Elizabeth Taylor’s White Diamonds, a perennial best-seller, and thenew fragrance M by Mariah Carey, which are eachtargeted towards a specific consumer demographic;designer fragrance brands, including the newlyacquired Badgley Mischka and Alfred Sung fra-grances, which are sold in prestige distribution and target an audience familiar with their clothingand accessory designs, and the Halston and GANTfragrance brands; and lifestyle fragrance brands,including Giorgio Beverly Hills, another global classicfragrance brand we added to our portfolio in fiscal2007, HUMMER® Fragrance for Men, under a licenseagreement with General Motors Corporation,and Paul Sebastian, all of which represent aspira-tional lifestyles with which consumers want to be associated.

5

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07Diverse

FragrancePortfolio

Celebrity

Mariah Carey

Hilary Duff

Britney Spears

Danielle Steel

Elizabeth Taylor

Elizabeth Arden-branded

5th Avenue

green tea

Mediterranean

Provocative Woman

Red Door

Designer

Geoffrey Beene

GANT

Lulu Guinness

Halston

Nanette Lepore

Bob Mackie

Badgley Mischka

Alfred Sung

Lifestyle

Daytona 500

Giorgio

HUMMER®

Paul Sebastian

White Shoulders

88724_8pgr:Layout 1 9/28/07 2:49 PM Page 6

This large selection of brands allows us to sell ourproducts around the world (over 40% of fiscal 2007net sales of our owned and licensed fragrancesoccurred outside the U.S.) and to multiple retailers,from luxury and specialty stores to mass retailers,allowing us to reach a diverse consumer demographic.For example, the recent launch of Badgley Mischkaat Saks 5th Avenue in Dubai achieved the numberone ranking in its first two weeks of launch. ElizabethArden Mediterranean, which was launched in fiscal 2007to retailers in the U.S. and in various internationalmarkets, is still being introduced in additional marketsaround the world. For example, in Australia, ElizabethArden Mediterranean was the best-selling fragrance forthe first four weeks after its launch in August 2007.

We also have a growing and significant portfolio ofdistributed brands, where we partner with otherbeauty companies to distribute top prestige fragrancebrands to mass and mid-tier retailers. This allows usto offer our retailers an even broader assortmentof fine fragrances.

Focus for Fiscal 2008 and Beyond: ImprovedReturn on Invested Capital throughImproved Operating Margins and Cash Flow

Our entire organization is intently focused onimproving our return on invested capital by drivingoperating margins, earnings and cash flow. Our his-torical operating margins were higher than the oper-ating margin reported in fiscal 2007, and our objectiveis to return and to surpass our historical operatingmargins over the next several years. We have iden-tified, and are well underway in implementing, anumber of initiatives, including a re-engineering ofour extended supply chain and logistics functions,improving fragrance portfolio management and the

development of key European account management,to contribute to improved return on invested capital.These initiatives, as well as the improved leverage ofour international platform and global infrastructure,should allow us to achieve our goals.

For fiscal 2008, we also further improved our com-pensation structure to ensure even closer alignmentwith specific financial and operating metrics.

Re-engineering of Supply Chain and Logistics Processes

A major area of opportunity is to better leverageour increased sales volume throughout our extended supply chain and logistics functions. Last year, we hired a world class consulting firmwith over 30 years of experience in assisting companies drive improvements in the areas of product development and supply chain and logistics execution. During fiscal 2007, this firm

6

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07

Harper’s Bazaar-Australia

88724_8pgr:Layout 1 9/28/07 2:49 PM Page 7

completed an extensive review and assess-ment of our global extended supply chainand logistics functions and benchmarked ourperformance against industry standards andidentified specific areas of opportunity toleverage our growth and gain operationalefficiencies. We have begun implementingprograms in areas that include account management, sales and operations planning, materials management, strategic sourcing andlogistics fulfillment. We expect to re-engineerthese processes in fiscal 2008, with the expectedbenefits to more significantly impact our fiscal 2009and fiscal 2010 performance. In addition to improvedoperating margins, we expect this initiative to resultin reduced inventories, increased operating cash flowand improved capacity to handle additional volume.

Fragrance Portfolio Management

With a strategy to find the appropriate balancebetween market relevant support and maximizingreturn on invested capital, we also have completeda review of how we manage our brand supportand allocate resources across our brand portfolio.For example, this year we are allocating a significant per-centage of our advertising spend behind classic fra-grance brands such as Elizabeth Taylor’sWhite Diamonds and Elizabeth ArdenRed Door to increase the profitabilityof our fragrance portfolio. TheElizabeth Taylor fragrance franchise, forexample, continues to be our crownjewel. Year after year, White Diamondsis the top-selling fragrance at mass andmid-tier retailers, and at U.S. depart-ment stores consistently ranks amongthe top ten best-selling holiday giftsets in the fragrance category.

We are also re-balancingthe advertising spend on new launches to more effectively reach consumers by better coordinating ourmedia spend with consumertraffic and launch activity.

Our newest celebrity fra-grance, M by Mariah Carey,is launching in the fall of

2007. Mariah is the best-selling female recordingartist of all time with 17 number one singles in the U.S. and global album sales exceeding 160 million units. Mariah’s popularity spans theglobe as evidenced by her record sales. In fact,record sales for the GRAMMY® award-winningEmancipation of Mimi album exceeded ten millioncopies worldwide. Based on the global appeal of Mariah Carey, we are introducing this brand to retailers in the U.S and internationally at thesame time, a first for us for a major fragrancelaunch. We are excited by the response so far from our consumers and retailers to M by Mariah Carey, including the recently launched mariahcareybeauty.com website, where pre-orders of her fragrance exceeded expectations.

Other fragrance launches slated for fiscal 2008include Fleurs De Nuit, a new Badgley Mischka fragrance, GANT Summer, a new Elizabeth Ardengreen tea fragrance and a new Hilary Duff fragrance, wrapped with love.

European Key Account Focus

In fiscal 2007, we completed the restructuring ofour European sales and marketing organizationsand created a pan-European “key account”organization to better serve European retailers.

Many of our retail customers in Europe, such as Douglas,Sephora and Marionnaud, havebecome more pan-European. As a result, we have realignedour sales infrastructure to bemore account focused, ratherthan geographically focused. We believe these initiatives will help us expand our Europeansales and improve profitability.

7

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07

Mark Badgley and James Mischka at “bottle signing” (Nordstrom, Costa Mesa, California).

88724_8pgr:Layout 1 10/2/07 5:31 PM Page 8

8

We also are applying the skill and expertise that we developed for the U.S. mass retail market ininternational markets where appropriate. We have had success in Australia where we began selling select prestige products to mass retailers in that market. Net sales in Australia grew over50% in fiscal 2007. We are in the process of actively exploring opportunities to implement this strategy in Europe in fiscal 2008. We believethere are significant opportunities given the number of emerging, fast growing and high quality “masstige” retailers.

Expand E-commerce and other distribution channels

We are well underway in elevating our e-commercestrategy and developing additional outlets of distribution for our products, including testingfree standing kiosk-type vending machines throughZoom Systems, which are located in malls, airportsand resorts. In fiscal 2007, we also hired resourcesto more fully develop our e-commerce strategy. Our new e-commerce site is intended to create on-line brand awareness and loyalty and expand theconsumer base. It also provides an ideal avenue to educate consumers about our skin care, cosmetics and fragrance products.

Grow Cash Flow

We generated cash flow from operations of $59million this year and we are committed to growing our cash flow in fiscal 2008, with more significantincreases in fiscal 2009 as the results from the initiatives outlined previously are achieved. We intendto use our free cash flow to pay down our operating

line, make acquisitions as appropriate opportunitiesarise and repurchase stock. Through fiscal 2007, we repurchased approximately $45 million of stockunder our $80 million stock buyback program.

The Support of Our Key Employees and Stakeholders

We thank you, our shareholders, for your conti-nued support and confidence in Elizabeth Arden.As a public company, we are seriously committedto strong principles of corporate governance toensure that we operate at the highest and mostresponsible level. I am pleased to report that ourcorporate governance quotient over the past fouryears, as determined by Institutional ShareholderServices, which ranks over 8,000 companies world-wide on the strengths, deficiencies and risks of acompany's corporate governance practices, puts us in the top 10% of companies that make up theRussell 3000 index.

On behalf of the entire Elizabeth Arden organiza-tion, I also would like to thank our retail and supplypartners around the world.

Finally, I would like to take this opportunity to thankthe talented employees and beauty advisors whoare so very dedicated to the success of ElizabethArden. Thanks to your support and dedication, we look forward to continued success and profitable growth for the foreseeable future.

El

iz

ab

et

h

Ar

de

n

An

nu

al

R

ep

or

t

20

07

E. Scott BeattieChairman, President and Chief Executive Officer

Elizabeth Arden counter in India

88724_8pgr:Layout 1 9/28/07 2:49 PM Page 9

Elizabeth Arden, Inc.

TABLE OF CONTENTS

Page

Part I

Item 1. Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Item 1A. Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Item 1B. Unresolved Staff Comments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Item 2. Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

Item 3. Legal Proceedings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Item 4. Submission of Matters to a Vote of Security Holders . . . . . . . . . . . . . . . . . . . . . . . 26

Part II

Item 5. Market For Registrant’s Common Equity, Related Stockholder Matters andIssuer Purchases of Equity Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Item 6. Selected Financial Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Item 7. Management’s Discussion and Analysis of Financial Condition and Results ofOperation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Item 7A. Quantitative and Qualitative Disclosures About Market Risk . . . . . . . . . . . . . . . . 44

Item 8. Financial Statements and Supplementary Data . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Item 9. Changes in and Disagreements with Accountants on Accounting and FinancialDisclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

Item 9A. Controls and Procedures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

Item 9B. Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

Part III

Item 10. Directors, Executive Officers and Corporate Governance . . . . . . . . . . . . . . . . . . . 87

Item 11. Executive Compensation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

Item 12. Security Ownership of Certain Beneficial Owners and Management and RelatedStockholder Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Item 13. Certain Relationships and Related Transactions, and Director Independence . . . 88

Item 14. Principal Accounting Fees and Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Part IV

Item 15. Exhibits, Financial Statement Schedules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Signatures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

10

PART I

ITEM 1. BUSINESS

General

Elizabeth Arden, Inc., is a global prestige beauty products company with an extensive portfolioof prestige fragrance, skin care and cosmetics brands. We market approximately 100 owned orlicensed prestige brands, including the Elizabeth Arden fragrances: Red Door, Elizabeth Arden 5thAvenue, Elizabeth Arden Provocative Woman, Elizabeth Arden green tea, and Elizabeth ArdenMediterranean; the Elizabeth Arden skin care brands: Ceramide, Eight Hour Cream, Intervene andPREVAGE™; and the Elizabeth Arden branded lipstick, foundation and other color cosmeticsproducts. Our fragrance portfolio also includes the Elizabeth Taylor fragrance brands: WhiteDiamonds and Elizabeth Taylor’s Passion; the Britney Spears fragrance brands: curious BritneySpears, fantasy Britney Spears and Britney Spears believe; the Hilary Duff fragrance withLove...Hilary Duff; the Danielle Steel fragrance Danielle by Danielle Steel; the Mariah Careyfragrance M by Mariah Carey; the fragrance brands White Shoulders, Giorgio Beverly Hills andGiorgio Red; the men’s fragrances: Daytona 500, HUMMERTM Fragrance for Men and PS FineCologne for Men; and the designer fragrance brands of Alfred Sung, Badgley Mischka, BobMackie, GANT, Lulu Guinness, Nanette Lepore, Geoffrey Beene and Halston. In addition toour owned and licensed fragrance brands, we distribute over 300 additional prestige fragrancebrands, primarily in the United States through distribution agreements and other purchasingarrangements.

We sell our prestige beauty products to retailers and other outlets in the United States andinternationally, including;

• department stores such as Macy’s, Dillard’s, Belk, JCPenney, Saks and Nordstroms;

• mass retailers such as Wal-Mart, Target, Sears, Kohl’s, Walgreens, Rite-Aid and CVS; and

• international retailers such as Boots, Debenhams, Sephora, Marionnaud, Hudson’s Bay,Shoppers Drug Mart, Myer, Douglas and various travel retail outlets such as Nuance,Heinemann and WDF.

In the United States, we sell our Elizabeth Arden skin care and cosmetics products primarily inprestige department stores and our fragrances in prestige department stores and mass retailers. Wealso sell our Elizabeth Arden fragrances, skin care and cosmetics products and other fragrance linesin approximately 90 countries worldwide through perfumeries, boutiques, department stores andtravel retail outlets, such as duty free shops and airport boutiques, and on the internet. Ourinternational operations are subject to volatility because of foreign currency exchange rate changes,inflation and changes in political and economic conditions in the countries in which we operate. Thevalue of international assets is affected by fluctuations in foreign currency exchange rates.

On August 11, 2006, we completed the acquisition of certain assets comprising the fragrancebusiness of Sovereign Sales, LLC, including inventory and certain intangible assets. Sovereign Saleswas a distributor of prestige fragrances to mass retail customers. This acquisition has allowed us tooffer additional fragrance brands to our mass retail customers.

On June 29, 2006, we completed the acquisition of certain assets of Riviera Concepts Inc.,including inventory, accounts receivable and brand licenses for a number of fragrance brands,including the fragrance brands of Alfred Sung, HUMMER™, Badgley Mischka, Nannette Lepore andBob Mackie.

11

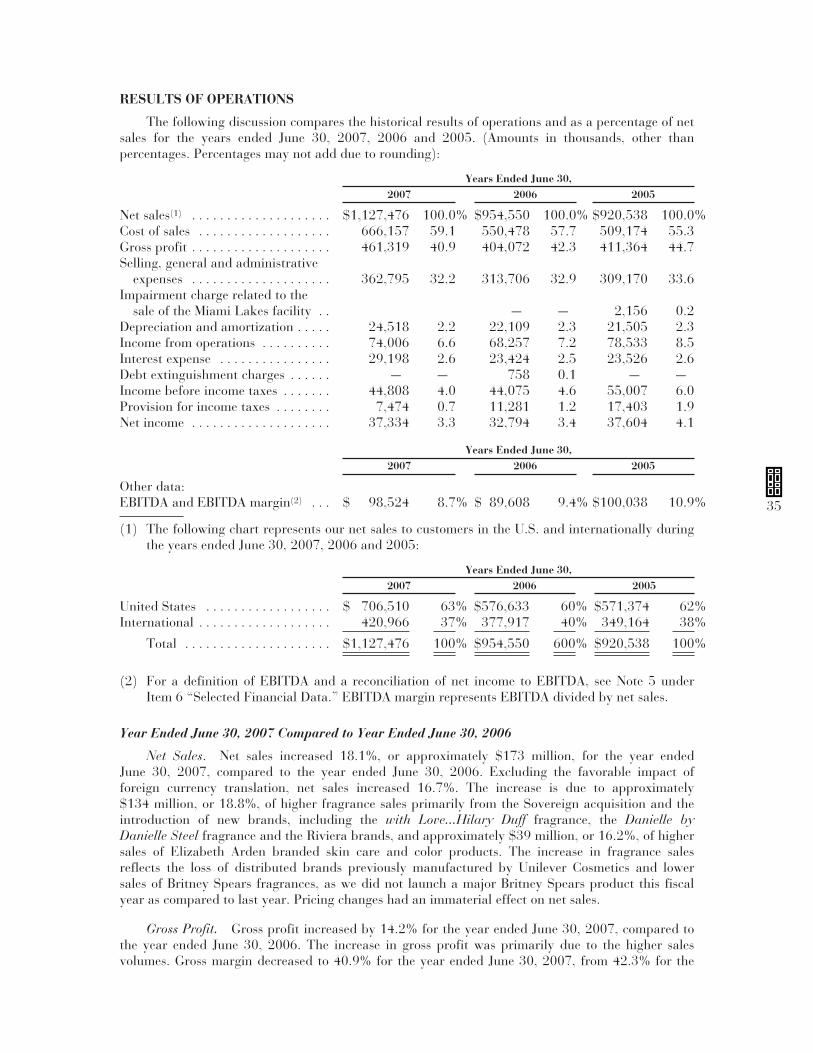

Our net sales to customers in the United States and internationally in dollars and net sales as apercentage of consolidated net sales for the years ended June 30, 2007, 2006 and 2005, are listed inthe following chart:

Years Ended June 30,2007 2006 2005

(Amounts in millions) Sales % Sales % Sales %

United States . . . . . . . . . . . . . . . . . . . . . $ 706.5 63% $576.7 60% $571.4 62%International . . . . . . . . . . . . . . . . . . . . . 421.0 37% 377.9 40% 349.1 38%

Total . . . . . . . . . . . . . . . . . . . . . . . . $1,127.5 100% $954.6 100% $920.5 100%

Our largest foreign countries in terms of net sales for the years ended June 30, 2007, 2006 and2005, are listed in the following chart:

Years Ended June 30,(Amounts in millions) 2007 2006 2005

United Kingdom . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $45.9 $47.5 $45.6Canada . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38.8 32.1 30.7Australia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31.6 20.4 17.9Spain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23.9 23.0 25.4

For information on the breakdown of our long-lived assets in the United States and internationallyand risks associated with our international operations, see Note 19 to the Notes to ConsolidatedFinancial Statements.

Our principal executive offices are located at 2400 S.W. 145th Avenue, Miramar, Florida33027, and our telephone number is (954) 364-6900. We maintain a website with the addresswww.elizabetharden.com. We are not including information contained on our website as part of norincorporating it by reference into this Annual Report on Form 10-K. We make available free ofcharge through our website our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Qand Current Reports on Form 8-K, and amendments to these reports, as soon as reasonablypracticable after we electronically file such material with or furnish such material to the Securitiesand Exchange Commission.

Information relating to corporate governance at Elizabeth Arden, Inc., including our CorporateGovernance Guidelines and Principles, Code of Ethics for Directors and Executive and FinanceOfficers, Code of Business Conduct and charters for the Audit Committee, the CompensationCommittee and the Nominating and Corporate Governance Committee, is available on our websiteunder the section “EA Corporate — Investor Relations — Corporate Governance.” We will providethe foregoing information without charge upon written request to Secretary, Elizabeth Arden, Inc.,2400 S.W. 145th Avenue, Miramar, FL 33027.

Business Strategy

Our business strategy is to grow our brand portfolio by investing behind our core brands and toacquire control of and develop additional prestige brands through brand development, acquisitionsand new licensing and distribution agreements that will complement our existing brand portfolioand target additional demographics. We are also focused on improving our cash flow and operatingmargins, particularly through improving our extended supply chain and logistics functions,managing the advertising spend behind our new fragrance launches and leveraging our globaloverhead structure more efficiently. In fiscal 2008, we plan to launch a number of new brands andproducts, including our new Mariah Carey fragrance, M by Mariah Carey, a new Britney Spearsfragrance, Britney Spears believe, and the night cream PREVAGETM Night, as well as introduce newdistributed fragrance brands to mass retailers on behalf of other beauty companies.

12

During the fiscal year ended June 30, 2007, we (i) acquired the exclusive worldwide license forthe Giorgio Beverly Hills brand, (ii) launched a new Elizabeth Arden skin care line, Intervene,(iii) and launched a new Elizabeth Arden fragrance, Elizabeth Arden Mediterranean, and the withLove...Hilary Duff and Danielle by Danielle Steel fragrances. In addition, during fiscal 2007, wecompleted the acquisition of certain assets comprising the fragrance business of Sovereign Sales,LLC, a prestige fragrance distributor to U.S. mass retailers, and the prestige fragrance brandportfolio of Riviera Concepts Inc., including licenses to manufacture the Alfred Sung, HUMMER™,Badgley Mischka, Nannette Lepore and Bob Mackie fragrance brands. These acquisitions andlicensing arrangements have enabled us to expand our market share with our mass retail customersand sell our products into new retailers and markets, and to broaden our fragrance portfolio.

We are also investing in certain developing markets around the world that we believe havesignificant opportunities for growth of our products. During the fiscal year ended June 30, 2007, weestablished a sales affiliate in Dubai to better serve the Middle East. During the fiscal year endedJune 30, 2006, we acquired the assets of our distributors in Taiwan and China, established affiliatesin those markets and integrated those affiliates with our Hong Kong business to create a GreaterChina market. We are also focusing on expanding sales of our products in other developing marketsincluding Latin America and India.

We continue to pursue business efficiencies throughout the company, particularly in the supplychain, logistics and information technology areas. Improving our working capital efficiencies and ourcost structure also continue to be a significant focus.

Products

Our net sales of products and net sales as a percentage of consolidated net sales for the yearsended June 30, 2007, 2006 and 2005, are listed in the following chart.

Years Ended June 30,2007 2006 2005

(Amounts in millions) Sales % Sales % Sales %

Fragrance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 851.1 75%$716.6 75%$691.0 75%Skin Care . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 200.6 18% 169.0 18% 155.5 17%Cosmetics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75.8 7% 69.0 7% 74.0 8%

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $1,127.5 100%$954.6 100%$920.5 100%

Fragrance. We offer a wide variety of fragrance products for both men and women, includingperfume, cologne, eau de toilette, eau de parfum, body spray and gift sets. Our fragrances are classifiedinto the Elizabeth Arden branded fragrances, such as Elizabeth Arden Red Door and Elizabeth Arden5th Avenue; celebrity fragrances such as Elizabeth Taylor’s White Diamonds and the Britney Spearsfragrances; designer fragrances such as the Badgley Mischka, Halston and GANT fragrance brands;and lifestyle fragrances such as Giorgio Beverly Hills, Paul Sebastian and the HUMMERTM fragrances.Each fragrance is sold in a variety of sizes and packaging arrangements. In addition, bath and bodyproducts that are based on the particular fragrance, such as soaps, deodorants, body lotions, gels,creams and dusting powder are sold to complement the fragrance lines. We tailor the size andpackaging of the fragrance to suit the particular target customer. Our fragrance products generallyretail at prices ranging from $5 to $225, depending on the size, type and packaging of the product.

Skin Care. Our skin care lines are sold under the Elizabeth Arden name and include productssuch as moisturizers, creams, lotions and cleansers. Our core product brands include Ceramide,PREVAGE™, Eight Hour Cream, and Intervene, a new skin care line targeted for the 30 to 50 yearold customer. We sell skin care products internationally and in the United States, primarily inprestige department and specialty stores, perfumeries and travel retail outlets. Our skin careproducts generally retail at prices ranging from $16 to $335.

13

Cosmetics. Under the Elizabeth Arden name, we offer a variety of cosmetics, includingfoundations, lipsticks, mascaras, eye shadows and powders. We offer these products in a wide arrayof shades and colors. Our strategy is to align our color offerings with our core skin care products. Weuse our cosmetic products to attract consumers to the beauty counters at department stores wherethe Elizabeth Arden fragrance and skin care products are also sold. We sell our cosmeticsinternationally and in the United States, primarily in prestige and specialty stores, perfumeries andtravel retail outlets. Our cosmetic products generally retail at prices ranging from $14 to $49.

Trademarks, Licenses and Patents

We own or have rights to use the trademarks necessary for the manufacturing, marketing,distribution and sale of numerous fragrance, cosmetic and skin care brands, including ElizabethArden’s Red Door, Red Door Revealed, Elizabeth Arden 5th Avenue, Elizabeth Arden ProvocativeWoman, Elizabeth Arden Mediterranean, Visible Difference, Plump Perfect, Intervene, Millennium,White Shoulders, Halston, Z-14, PS Fine Cologne for Men, Design and Wings. We have registeredthese trademarks, or have applications pending, in the United States and in certain of the countriesin which we sell these product lines. We consider the protection of our trademarks to be important toour business.

We are the exclusive worldwide trademark licensee for a number of fragrance brands includingthe Elizabeth Taylor fragrances White Diamonds and Elizabeth Taylor’s Passion; the Alfred Sungfragrance brands SUNG Alfred Sung, SHI Alfred Sung and JEWEL Alfred Sung; the HUMMER™fragrances HUMMER™ and H2; the designer fragrance brands of Badgley Mischka, Nanette Lepore,Bob Mackie, Lulu Guinness, Geoffrey Beene and Halston, the Britney Spears fragrances curiousBritney Spears and fantasy Britney Spears; the Hilary Duff fragrance with Love...Hilary Duff; theDanielle Steel fragrances Danielle by Danielle Steel; the Mariah Carey fragrance M by MariahCarey, and the Giorgio fragrances Giorgio Beverly Hills and Giorgio Red. We are the exclusiveworldwide licensee for the PREVAGE™ skin care line for retail outlets. The Taylor license agreementterminates in October 2022 and is renewable by us, at our sole option, for unlimited 20-yearperiods. The Britney Spears license terminates in December 2009 and is renewable by us, at our soleoption, for a 5-year term. The PREVAGE™ license terminates in December 2010 and is renewableby us for unlimited 5-year terms if certain sales targets are achieved. The other license agreementshave terms ranging from 2009 to 2045 and beyond and, typically, have renewal terms dependent onsales targets being achieved.

We also have the right under various exclusive distributor and license agreements to distributeother fragrances in various territories and to use the registered trademarks of third parties inconnection with the sale of these products.

Certain of our skin care and cosmetic products and the PREVAGE™ skin care line incorporatepatented or patent-pending formulations. In addition, several of our packaging methods, packages,components and products are covered by design patents, patent applications and copyrights.Substantially all of our trademarks and all of our patents are held by us or by one of our wholly-owned United States subsidiaries.

Sales and Distribution

We sell our prestige beauty products to retailers in the United States, including departmentstores such as Macy’s, Dillard’s, Saks, JCPenney, Belk and Nordstroms; mass retailers such asWal-Mart, Target, Sears, Kohl’s, Walgreens, Rite-Aid and CVS; and international retailers such asBoots, Debenhams, Sephora, Marionnaud, Hudson’s Bay, Shoppers Drug Mart, Myer, Douglas andvarious travel retail outlets such as Nuance, Heinemann and WDF. We also sell products toindependent fragrance, cosmetic, gift and other stores and through e-commerce. We currently sellour skin care and cosmetics products in the United States primarily in prestige department and

14

specialty stores. We also sell our fragrances, skin care and cosmetic products in approximately 90other countries worldwide through perfumeries, pharmacies, department stores, specialty retailers,“duty free” shops and other retail shops and travel retail locations. In certain countries, we maintaina dedicated sales force that solicits orders and provides customer service. In other countries andjurisdictions, we sell our products through local distributors under contractual arrangements. Wemanage our operations outside of North America from our offices in Geneva, Switzerland.

We also sell our Elizabeth Arden products in the Elizabeth Arden and Red Door beauty salons,which are owned and operated by an unrelated third party. In addition to the sales price of theproducts sold to the operator of these salons, we receive a licensing fee based on the net sales fromeach of the salons for the use of the “Elizabeth Arden” or “Red Door” trademarks.

Our sales and marketing support staff and personnel are organized by customer account. Oursales force routinely visits retailers to assist in the merchandising, layout and stocking of sellingareas. In the U.S., we have a sales force for Elizabeth Arden branded products that are sold inprestige distribution. For many of our mass retailers in the United States and Canada, we sell basicproducts in special packaging that deter theft and permit the products to be sold in open displays.Our fulfillment capabilities enable us to reliably process, assemble and ship small orders on a timelybasis. We use this ability to assist our customers in their retail distribution through “drop shipping”directly to their stores and by fulfilling their sales of beauty products over the Internet. In fiscal2007, we also launched an e-commerce site to sell selected products directly to consumers.

As is customary in the beauty industry, we do not generally have long-term or exclusivecontracts with any of our retail customers. Sales to customers are generally made pursuant topurchase orders. We believe that our continuing relationships with our customers are based uponour ability to provide a wide selection and reliable source of prestige beauty products, our expertisein marketing and new product introduction, and our ability to provide value-added services,including our category management services, to U.S. mass retailers.

Our ten largest customers accounted for approximately 39% of net sales for the year endedJune 30, 2007. The only customer that accounted for more than 10% of our net sales during thatperiod was Wal-Mart (including Sam’s Club), which, on a global basis, accounted for approximately18% of our net sales. The loss of or a significant adverse change in our relationship with any of ourlargest customers could have a material adverse effect on our business, prospects, results ofoperations, financial condition and cash flows.

The industry practice for businesses that market beauty products has been to grant certainretailers, subject to our authorization and approval, the right to either return merchandise or toreceive a markdown allowance for certain promotional products. We establish estimated returnreserves and markdown allowances at the time of sale based upon historical and projectedexperience, economic trends and changes in customer demand. Our reserves and allowances arereviewed and updated as needed during the year, and additions to these reserves and allowancesmay be required. Additions to our reserves and allowances may have a negative impact on ourfinancial results. We have a dedicated sales organization to sell returned products that are saleable.

Marketing

Our marketing approach emphasizes a consistent global image for our brands, and each of ourfragrance, skin care and cosmetics products is distinctively positioned with specific advertisingthemes, logos and packaging tailored for that particular product. We utilize our spokesperson,Catherine Zeta-Jones, and our classic Red Door symbol, to reinforce the Elizabeth Arden brandheritage and contemporize the Elizabeth Arden brand globally. We use traditional print, television

15

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-KÈ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934For the fiscal year ended June 30, 2007

OR‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934For the transition period from to

Commission file number 1-6370

Elizabeth Arden, Inc.(Exact name of registrant as specified in its charter)

Florida 59-0914138(State or other jurisdiction of

incorporation or organization)(I.R.S. Employer

Identification No.)

2400 SW 145th Avenue,Miramar, Florida 33027

(Address of principal executive offices) (Zip Code)(954) 364-6900

(Registrant’s telephone number, including area code)Securities registered pursuant to Section 12(b) of the Act: NoneSecurities registered pursuant to Section 12(g) of the Act: Common Stock, $.01 Par Value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405of the Securities Act. Yes ‘ No È

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 orSection 15(d) of the Act. Yes ‘ No È

Indicate by check mark whether the registrant (1) has filed all reports required to be filed bySection 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or forsuch shorter period that the registrant was required to file such reports), and (2) has been subject tosuch filing requirements for the past 90 days. Yes È No ‘

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K(§229.405 of this chapter) is not contained herein, and will not be contained, to the best ofregistrant’s knowledge, in definitive proxy or information statements incorporated by reference inPart III of this Form 10-K or any amendment to this Form 10-K. È

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, ora non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2of the Exchange Act. (Check one):

Large accelerated filer ‘ Accelerated filer È Non-accelerated filer ‘Indicate by check mark whether the registrant is a shell company (as defined in rule 12b-2 of

the Act). Yes ‘ No È

The aggregate market value of voting Common Stock held by non-affiliates of the registrantwas approximately $461 million based on the closing price of the Common Stock on the NASDAQGlobal Select Market of $19.05 per share on December 31, 2006, the last business day of theregistrant’s most recently completed second fiscal quarter, based on the number of sharesoutstanding on that date less the number of shares held by the registrant’s directors, executiveofficers and holders of at least 10% of the outstanding shares of Common Stock.

As of September 5, 2007, the registrant had 28,820,663 shares of Common Stock outstanding.

Documents Incorporated by ReferencePortions of the Registrant’s definitive proxy statement relating to its 2007 Annual Meeting of

Shareholders, to be filed no later than 120 days after the close of the Registrant’s fiscal year endedJune 30, 2007, are hereby incorporated by reference in Part III of this Annual Report on Form 10-K.

9

and radio advertising, and point-of-sale merchandising, including displays and sampling, as well asless traditional methods, such as the internet, mobile phones and instant messaging. We work withthird party advertising agencies to assist us in our worldwide media planning which includesdeveloping the media strategy for our brands and assisting us in developing the marketingcampaigns for many of our products. We believe these agencies have the expertise to help useffectively market our products. During the last three fiscal years, we increased our advertising topromote our core product franchises.

New product introduction is an important element in attracting consumers to our brands and increating brand excitement with our retail customers. Our marketing personnel work closely withcustomers to develop new products and promotions and extensions of our well-established brands.Our efforts are primarily focused on the identification of consumer needs and shifts in consumerpreferences in order to develop new fragrance, skin care and cosmetic products, develop lineextensions and promotions, and redesign or reformulate existing products.

Our marketing efforts also benefit from cooperative advertising programs with our retailers,often linked with particular promotions. In our department store and perfumerie accounts, weperiodically promote our brands with “gift with purchase” and “purchase with purchase” programs.At in-store counters, sales representatives offer personal demonstrations to market individualproducts. We also engage in extensive sampling programs.

With many of our retail customers, our marketing personnel often design model schematicplanograms for the customer’s fragrance department, identify trends in consumer preferences andadapt the product assortment to these trends, conduct training programs for the customer’s salespersonnel and manage in-store “special events.” Our marketing personnel also work to design giftsets tailored to the customer’s needs. For certain customers, we provide comprehensive sales analysisand active management of the prestige fragrance category. We believe these services distinguish usfrom our competitors and contribute to customer loyalty.

Seasonality

Our operations have historically been seasonal, with higher sales occurring in the first half ofour fiscal year as a result of increased demand by retailers in anticipation of and during the holidayseason. In the year ended June 30, 2007, approximately 59% of our net sales were made during thefirst half of our fiscal year. Due to product innovations and the size and timing of certain ordersfrom our customers, sales, results of operations, working capital requirements and cash flows canvary significantly between quarters of the same and different years. As a result, we expect toexperience variability in net sales, operating margin, net income, working capital requirements andcash flows on a quarterly basis. Increased sales of skin care and cosmetic products relative tofragrances may reduce the seasonality of our business.

Manufacturing, Supply Chain and Logistics

We use third-party contract manufacturers in the United States and Europe to obtainsubstantially all raw materials, components and packaging products and to manufacture finishedproducts relating to our owned and licensed brands. Our fragrance and skin care products areprimarily manufactured by Cosmetic Essence, Inc., an unrelated third party, in plants located inNew Jersey and Roanoke, Virginia, under a manufacturing agreement that expires on January 31,2010. Pricing is based on fixed costs per item. Third parties in Europe manufacture certain of ourfragrance and cosmetic products. We also have a small manufacturing facility in South Africaprimarily to manufacture local requirements of our products.

Except for the Cosmetic Essence, Inc. manufacturing agreement, as is customary in ourindustry, we generally do not have long-term or exclusive agreements with contract manufacturersof our owned and licensed brands or with fragrance manufacturers or suppliers of our distributed

16

brands. We generally make purchases through purchase orders. We believe that we have goodrelationships with manufacturers of our owned and licensed brands and that there are alternativesources should one or more of these manufacturers become unavailable. We receive our distributedbrands in finished goods form directly from fragrance manufacturers, as well as from other sources.Our ten largest fragrance manufacturers or suppliers of brands that are distributed by us on anon-exclusive basis accounted for approximately 28% of our cost of sales for the year endedJune 30, 2007. The loss of, or a significant adverse change in our relationship with, any of our keyfragrance manufacturers for our owned and licensed brands, such as Cosmetic Essence, Inc., orsuppliers of our distributed fragrance brands could have a material adverse effect on our business,prospects, results of operations or financial condition.

Our fulfillment operations for the United States and certain other areas of the world areconducted out of a leased distribution facility in Roanoke, Virginia. The 400,000 square-footRoanoke facility accommodates our distribution activities and houses a large portion of ourinventory. Our fulfillment operations for Europe are conducted under a logistics services agreementby CEPL, an unrelated third party, at CEPL’s facility in Beville, France. The CEPL agreementexpires in June 2008. While we insure our inventory and the Roanoke facility, the loss of either ofthese distribution facilities, as well as the inventory stored in those facilities, would require us to findreplacement facilities and inventory and could have a material adverse effect on our business,prospects, results of operations, cash flows and financial condition.

Government Regulation

We and our products are subject to regulation by the Food and Drug Administration and theFederal Trade Commission in the United States, as well as by various other federal, state, local andinternational regulatory authorities in the countries in which our products are produced or sold.Such regulations principally relate to the ingredients, manufacturing, labeling, packaging andmarketing of our products. We believe that we are in substantial compliance with such regulations,as well as with applicable federal, state, local and international and other countries’ rules andregulations governing the discharge of materials hazardous to the environment.

Management Information Systems

Our primary information technology systems discussed below provide a complete portfolio ofbusiness systems, business intelligence systems, and information technology infrastructure servicesto support our global operations:

• Logistics and supply chain systems, including purchasing, materials management,manufacturing, inventory management, order management, customer service, pricing,demand planning, warehouse management and shipping;

• Financial and administrative systems, including general ledger, payables, receivables,personnel, payroll, tax, treasury and asset management;

• Electronic data interchange systems to enable electronic exchange of order, status, invoice,and financial information with our customers, financial service providers and our partnerswithin the extended supply chain;

• Business intelligence and business analysis systems to enable management’s informationalneeds as they conduct business operations and perform business decision making; and

• Information technology infrastructure services to enable seamless integration of our globalbusiness operations through Wide Area Networks (WAN), personal computing technologies,electronic mail, and service agreements with outsourced computing operations.

These management information systems and infrastructure provide on-line business processsupport for our global business operations. Further, many of these capabilities have been extendedinto the operations of our U.S. customers and third party service providers to enhance these

17

arrangements, with examples such as vendor managed inventory, third party distribution, thirdparty manufacturing, inventory replenishment, customer billing, retail sales analysis, productavailability, pricing information and transportation management.

As part of our continuing efforts to enhance the effectiveness and strategic value of ouroperations and systems, during the year ended June 30, 2007, we launched an e-commerce web siteto sell our selected products directly to consumers, we implemented an enterprise resource planning(ERP) system for our Greater China operations, we implemented business intelligence systems toenable global purchasing analysis and improved forecasting effectiveness, we integrated a largeportion of our prior Canada-based distribution services into our Roanoke logistics center, and weimplemented vendor performance management processes.

We have back-up facilities to enhance the reliability of our management information systems.These facilities will allow us to continue to operate if our main facilities should fail. We also have adisaster recovery plan, which is tested periodically, to protect our business operations and customerinformation. We also have business interruption insurance to cover a portion of any disruption inour management information systems resulting from certain hazards.

Competition

The beauty industry is highly competitive and, at times, subject to rapidly changing consumerpreferences and industry trends. Competition is generally a function of brand strength, assortmentand continuity of merchandise selection, reliable order fulfillment and delivery, and level of brandsupport and in-store customer support. We compete with a large number of manufacturers andmarketers of beauty products, some of which have substantially more resources than we do.

We believe that we compete primarily on the basis of product recognition, quality, performance,price, and our emphasis on providing value-added customer services, including categorymanagement services, to certain retailers. There are products that are better-known and morepopular than the products manufactured or supplied by us. Many of our competitors aresubstantially larger and more diversified, and have substantially greater financial and marketingresources than we do, as well as greater name recognition and the ability to develop and marketproducts similar to and competitive with those manufactured by us.

Employees

As of September 4, 2007, we had approximately 2,250 full-time employees and approximately 600part-time employees in the United States and 17 foreign countries. None of our employees are covered bya collective bargaining agreement. We believe that our relationship with our employees is satisfactory.

Executive Officers of the Company

The following sets forth the names and ages of each of our executive officers as of September 4,2007 and the positions they hold:

Name Age Position with the Company

E. Scott Beattie . . . . . . . . . . . . 48 Chairman, President and Chief Executive OfficerStephen J. Smith . . . . . . . . . . 47 Executive Vice President and Chief Financial OfficerL. Hoy Heise . . . . . . . . . . . . . 61 Executive Vice President, Chief Information Officer and

Operations PlanningMichael H. Lombardi . . . . . . . 64 Executive Vice President, OperationsOscar E. Marina . . . . . . . . . . . 48 Executive Vice President, General Counsel and SecretaryElizabeth Park . . . . . . . . . . . . 44 Executive Vice President, Skin Care & Color Marketing and

General Manager—Arden U.S.Ronald L. Rolleston . . . . . . . . 51 Executive Vice President, Global Fragrance MarketingJoel B. Ronkin . . . . . . . . . . . . 39 Executive Vice President, General Manager—North America

FragrancesJacobus A. J. Steffens . . . . . . . 46 Executive Vice President, General Manager—International

18

Each of our executive officers holds office for such term as may be determined by our board ofdirectors. Set forth below is a brief description of the business experience of each of our executiveofficers.

E. Scott Beattie has served as Chairman of the Board of Directors since April 2000, as ourPresident and Chief Executive Officer since August 2006, as our Chief Executive Officer since March1998 and as a director of the company since November 1995. Mr. Beattie also served as ourPresident from April 1997 to March 2003, as our Chief Operating Officer from April 1997 to March1998, and as our Vice Chairman of the Board of Directors and Assistant Secretary from November1995 to April 1997. Mr. Beattie is a director of Object Video, Inc., an information technologycompany. Mr. Beattie is also a director and a member of the Executive Committee of The Cosmetic,Toiletry & Fragrance Association and a member of the advisory board of the Ivey Business School.

Stephen J. Smith has served as our Executive Vice President and Chief Financial Officer sinceMay 2001. Previously, Mr. Smith was with PricewaterhouseCoopers LLP, an internationalprofessional services firm, as partner from October 1993 until May 2001, and as manager fromJuly 1987 until October 1993.

L. Hoy Heise has served as our Executive Vice President, Chief Information Officer andOperations Planning since May 2006 and as our Senior Vice President and Chief Information Officerfrom May 2004 until May 2006. From February 2003 until May 2004, Mr. Heise was the founderand principal of his own technology consulting firm. From June 1999 until May 2001, Mr. Heise wasSenior Vice President of Gartner, an information technology research firm. Prior to that time,Mr. Heise worked in various management and consulting capacities for Renaissance Worldwide, aglobal provider of business process improvement and information technology consulting services.

Michael H. Lombardi has served as our Executive Vice President, Operations since March2004, as our Senior Vice President, Operations since January 2001 and as Senior Vice President,Marketing/Supply Chain Operations with the Elizabeth Arden Company, a division of UnileverN.V., since April 1999. Prior to joining the Elizabeth Arden Company, Mr. Lombardi worked invarious management capacities for Chesebrough Ponds, Inc.

Oscar E. Marina has served as our Executive Vice President, General Counsel and Secretarysince March 2004, as our Senior Vice President, General Counsel and Secretary from March 2000through February 2004, and as our Vice President, General Counsel and Secretary from March1996 through March 2000. From October 1988 until March 1996, Mr. Marina was an attorney withthe law firm of Steel Hector & Davis L.L.P. in Miami, becoming a partner of the firm in January1995.

Elizabeth Park has served as our Executive Vice President, Skin Care & Color Marketing andGeneral Manager — Arden U.S., since May 2006 and as our Senior Vice President, GlobalMarketing from March 2005 until May 2006. Prior to joining our company, Ms. Park was SeniorVice President Marketing U.S.A. for Lancôme, a division of L’Oreal Products from March 2003 untilMarch 2005. From July 1995 to July 2002, Ms. Park held several marketing management positionswith the Estee Lauder Companies.

Ronald L. Rolleston has served as our Executive Vice President, Global Fragrance Marketingsince May 2006, as our Executive Vice President, Global Marketing since April 2003, as ourExecutive Vice President, Global Marketing and Prestige Sales from February 2002 until April2003, as our Senior Vice President, Global Marketing from February 2001 through January 2002,and as our Senior Vice President, Prestige Sales from March 1999 through January 2001.Mr. Rolleston served as President of Paul Sebastian, Inc., a fragrance manufacturer, from September1997 until January 1999. Mr. Rolleston served as Executive Vice President of Global Marketing ofthe Elizabeth Arden Company from January 1995 to March 1997 and as the General Manager ofEurope for the Calvin Klein Cosmetics Company from May 1990 to September 1994.

19

Joel B. Ronkin has served as our Executive Vice President, General Manager — North AmericaFragrances since May 2006, as our Executive Vice President and Chief Administrative Officer fromMarch 2004 until May 2006, as our Senior Vice President and Chief Administrative Officer fromFebruary 2001 through February 2004, and as our Vice President, Associate General Counsel andAssistant Secretary from March 1999 through January 2001. From June 1997 through March 1999,Mr. Ronkin served as the Vice President, Secretary and General Counsel of National Auto FinanceCompany, Inc., an automobile finance company. From May 1992 until June 1997, Mr. Ronkin wasan attorney with the law firm of Steel Hector & Davis L.L.P. in Miami, Florida.

Jacobus A.J. Steffens has served as our Executive Vice President, General Manager —International since March 2004 and as our Senior Vice President, General Manager — Internationalfrom January 2001 through February 2004. Before joining the company, Mr. Steffens worked invarious management capacities for divisions of Unilever N.V., including as the Chief InformationOfficer of Unilever’s European Ice Cream & Frozen Foods division from January 1997 untilDecember 2000, as the Controller Global Marketing & Creative at the Elizabeth Arden Companyfrom January 1992 until December 1995 and in various financial roles for Unilever’s QuestInternational Flavours and Fragrances division from the end of 1986 until December 1991.

ITEM 1A. RISK FACTORS

The risk factors in this section describe the major risks to our business, prospects, results ofoperations and financial condition and should be considered carefully. In addition, these factorsconstitute our cautionary statements under the Private Securities Litigation Reform Act of 1995 andcould cause our actual results to differ materially from those projected in any forward-lookingstatements (as defined in such act) made in this Annual Report on Form 10-K. Investors should notplace undue reliance on any such forward-looking statements. Any statements that are not historicalfacts and that express, or involve discussions as to, expectations, beliefs, plans, objectives,assumptions or future events or performance (often, but not always, through the use of words orphrases such as “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimated,”“intends,” “plans,” “believes” and “projects”) may be forward-looking and may involve estimatesand uncertainties which could cause actual results to differ materially from those expressed in theforward-looking statements.

Further, any forward-looking statement speaks only as of the date on which such statement ismade, and we undertake no obligation to update any forward-looking statement to reflect events orcircumstances after the date on which such statement is made or to reflect the occurrence ofanticipated or unanticipated events or circumstances. New factors emerge from time to time, and itis not possible for us to predict all of such factors. Further, we cannot assess the impact of each suchfactor on our results of operations or the extent to which any factor, or combination of factors, maycause actual results to differ materially from those contained in any forward-looking statements.

We do not have contracts with customers or most of our suppliers, so if we cannot maintainand develop relationships with customers and suppliers our business, prospects, results ofoperations and financial condition may be materially adversely affected.

We do not have long-term or exclusive contracts with any of our customers and generally do nothave long-term or exclusive contracts with our suppliers of distributed brands. Our ten largestcustomers accounted for approximately 39% of our net sales in the year ended June 30, 2007. Ouronly customer who accounted for more than 10% of our net sales in the year ended June 30, 2007was Wal-Mart (including Sam’s Club), who, on a global basis, accounted for approximately 18% ofour net sales. In addition, our suppliers of distributed brands, which represented approximately 41%of our cost of sales for fiscal 2007, generally can, at any time, elect to supply products to ourcustomers directly or through another distributor. Our suppliers of distributed brands may alsochoose to reduce or eliminate the volume of their products distributed by us. The loss of any of ourkey suppliers or customers, or a change in our relationship with any one of them, could have amaterial adverse effect on our business, prospects, results of operations and financial condition.

20

We rely on third-party manufacturers for substantially all of our owned and licensedproducts.

We do not own or operate any significant manufacturing facilities. We use third-partymanufacturers and suppliers to manufacture substantially all of our owned and licensed products.We currently obtain these products from a limited number of manufacturers and other suppliers.Our business, prospects, results of operations and financial condition could be materially adverselyaffected if our manufacturers were to experience problems with product quality or delays in thedelivery of the finished products or the raw materials or components used to make such product.

The loss of or disruption in our distribution facilities may have a material adverse effect onour business.

We currently have one distribution facility in the United States and use a third-party fulfillmentcenter in France for European distribution. These facilities house a large portion of our inventory.Any loss of or damage to these facilities or the inventory stored in these facilities, could adverselyaffect our business, prospects, results of operations and financial condition.

We may be adversely affected by factors affecting our customers’ businesses.

Factors that adversely impact our customers’ businesses may have an adverse effect on ourbusiness and results of operations also. These factors may include:

• any credit risks presented by the financial condition of our customers;

• the effect of consolidation in the retail industry, including the closure of customer doors,and the uncertainty resulting therefrom; and

• inventory reduction initiatives and other factors affecting customer buying patterns,including retail space committment to fragrances and cosmetics.

We may be adversely affected by domestic and international economic conditions and otherevents that impact consumer confidence and demand.

We believe that consumer spending on beauty products is influenced by general economicconditions and the availability of discretionary income. Domestic or international general economicdownturns, including periods of inflation or high gasoline prices or declining consumer confidence,may affect consumer purchasing patterns and result in reduced net sales to our customers. Inaddition, any reductions in travel or increases in restrictions on travelers’ ability to transport ourproducts on airplanes due to general economic downturns, diseases, acts of war or terrorism couldresult in a material decline in the net sales and profitability of our travel retail business.

The beauty industry is highly competitive and if we cannot effectively compete our businessand results of operations will suffer.

The beauty industry is highly competitive and can change rapidly due to consumer preferencesand industry trends. We compete primarily with global prestige beauty companies, some of whomhave greater resources than we have and brands with greater name recognition and consumer loyaltythan our brands. Our products also compete with new products that often are accompanied bysubstantial promotional campaigns. Our success depends on our products’ appeal to a broad rangeof consumers whose preferences cannot be predicted with certainty and are subject to change, andon our ability to develop new products through product innovations and product line extensions,which involve numerous risks. We may also incur increased expenses in connection with productdevelopment, marketing and advertising that are not subsequently supported by a sufficient level ofsales, which could negatively affect our results of operations. These competitive factors, as well asnew product risks, could have an adverse effect on our business prospects, results of operations andfinancial condition.

21

Our business strategy depends upon our ability to acquire or license additional brands orsecure additional distribution arrangements and obtain the required financing for theseagreements and arrangements.